Analyst Meeting No. 3/2020 14 October 2020

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Analyst Meeting No. 3/2020

14 October 2020

Agenda

• Economic growth and inflation projections

• Monetary policy decisions, financial and credit measures

• Key factors affecting outlook of the Thai economy

2/23

Outlook of the Thai economy

The Thai economy is expected to contract

2019* 2020E 2021E significantly in 2020 as a result of the COVID-19

GDP Growth 2.4 -7.8 3.6 outbreak and is likely to expand moderately in 2021

(-8.1) (5.0) due to limitation in admitting foreign tourists.

Headline Inflation 0.7 -0.9 1.0 Headline inflation in 2020 is expected to be less

(-1.7) (0.9) negative as oil prices increase and would turn

Core Inflation 0.5 0.3 0.2 positive in 2021 while being close to the lower bound

(0.0) (0.1) of the target range.

Going forward, economic growth and inflation

* Outturn, E Estimated projections remain highly uncertain with risks of being

( ) Monetary Policy Report, June 2020

below the baseline scenario.

Source: Monetary Policy Report, September 2020

3/23

Details of the economic forecasts

2020E 2021E

(% YoY) 2019* The impacts of the worldwide COVID-19

Jun 20 Sep 20 Jun 20 Sep 20

GDP Growth 2.4 -8.1 -7.8 5.0 3.6 pandemic are severe. The recoveries of tourism

- Private Consumption 4.5 -3.6 -3.5 2.5 2.0

and merchandise exports remain highly

- Private Investment 2.8 -13.0 -11.4 5.6 4.2

- Government Consumption 1.4 3.8 3.4 3.1 5.1 uncertain.

- Government Investment 0.2 5.8 8.8 14.1 11.4

- Exports of Goods and Services -2.6 -22.7 -21.2 8.4 4.3

Domestic demands both in terms of private

- Imports of Goods and Services -4.4 -18.9 -16.6 7.3 4.4 consumption and private investment are

Current Account (Billion USD) 37.0 15.5 14.0 20.2 14.6 expected to improve slightly while employment

- Value of Merchandise Exports -3.3 -10.3 -8.2 4.5 4.5 and income remain weak which will take some time

- Value of Merchandise Imports -5.6 -16.2 -13.7 4.1 4.4

Headline Inflation 0.7 -1.7 -0.9 0.9 1.0

to recover.

Core Inflation 0.5 0.0 0.3 0.1 0.2

The recovery will be greatly uneven among

Assumptions

economic sectors, regions, and firms in different

- Number of Tourists (Million) 39.8 8.0 6.7 16.2 9.0

- Dubai Oil Price (USD/Barrel) 63.5 35.1 41.5 37.0 45.8

segments.

Note: * Outturn, E Estimated

Source: Monetary Policy Report, September 2020

4/23

Thai economic recovery remains highly uncertain and depend primarily on the

re-opening of the country to foreign tourists.

Number of daily foreign tourist arrivals through 5 major airports*

Persons China ordered travel agencies to suspend

140,000 tourism-related operations on Jan 24, 2020.

2019 2020

On Mar 26, the Emergency

120,000 From Jul 1, eleven categories of non-leisure

100,000

Decree became effective. visitors have been allowed to enter Thailand. • The outbreak situation abroad is more

80,000 prolonged than expected owing to second

60,000

From Jul 22, four

waves of the outbreak in several countries as

40,000 categories of foreign

visitors have been well as uncontainable pandemic situations in

20,000 allowed to enter

Thailand. some countries .

0

15 Feb

24 Feb

13 Aug

22 Aug

31 Aug

8 Jul

17 Jul

26 Jul

1 Jan

10 Jan

19 Jan

28 Jan

4 Mar

13 Mar

22 Mar

31 Mar

9 Apr

18 Apr

27 Apr

2 Jun

11 Jun

20 Jun

29 Jun

6 May

15 May

24 May

6 Feb

4 Aug • The re-opening of the country to foreign

Note: * 5 major airports include Suvarnabhumi, Donmuang, Chiang Mai, Hat Yai and tourists is likely to be gradual and is expected

Phuket International Airports

Source: TAT Intelligence Center to be opened more widely during the second

Projected number of foreign tourists half of 2021.

2020 2021

(Million)

June 20 8.0 16.2

September 20 6.7 9.0

5/23Thai exports experienced a slower recovery compared to other countries in the region

and recorded a 12 percent contraction due to structural factors

Percent (2019) Share of export products compared to other regional countries

100

Changes in export values compared to regional countries , seasonally adjusted 1/ 80

(compared 4th quarter 2019 with trough during COVID crisis and July 2020) 60

Percent 40

9

10 7 20

-2 -2 -5

0 -6 -9

0

-12 -13 TH KR ID TW PH VT MY SG HK

-10 -6 -3 Others Petroleum product Chemical

Machinery transports Electrical appliance

-20 -18 -20 -19 Electronics Agro manu. Agriculture

-30 -23

-27 -28

-40 Share of Thai export market compared to other regional countries

Percent (2019)

100

-50

-50 80

-60

60

40

trough during the COVID-19 crisis the latest data as of Jul 20 20

0

Note: 1/ Thai export excludes gold. Hong Kong and Singapore exports exclude re-export MYASEAN SG ChinaTH ID

Japan USKR EUTW Middle

PH East VT OthersHK

Source : Trade map, Customs Department, calculated by Bank of Thailand 6/23Thai economic recovery would take at least two years before returning to

the pre-pandemic level while many risk factors remain and warrant close monitoring.

Projection of Thai economic growth in various cases

Real GDP seasonally adjusted, Projection period

natural log Vulnerable period Factors that could delay the recovery

• Re-opening country to foreign

Base case visitors could not be commenced

until vaccines become widely

available.

Case of long delay in re-opening • The global economy could

country to foreign tourists

significantly contract again due to

occurrences of a more severe

outbreak that could trigger stricter

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

containment measures.

2017 2018 2019 2020 2021 2022

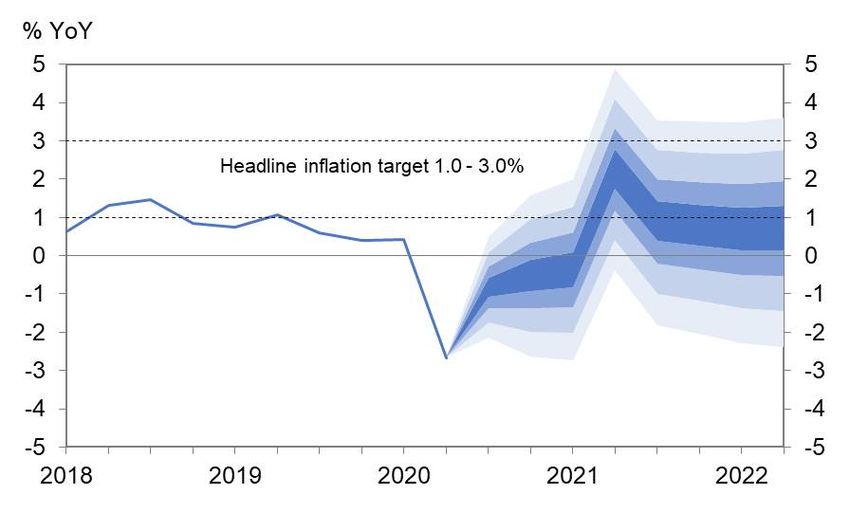

7/23Headline inflation would gradually rise in line with economic recovery

and stay close to the lower bound of the target range in 2021

Contribution of headline inflation

3 %YoY

2

1 Aug 20 • Headline inflation projection for 2020 is

0

-1 -0.50% less negative due mainly to upward revision

-2

-3

in oil prices assumption.

-4

Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul • Core inflation projection is revised upward

14 15 16 17 18 19 20

as government measures in reducing utility

Raw food (15.69%) Energy (11.75%) Core Inflation (72.56%) Headline Inflation

Sources: Ministry of Commerce calculated by Bank of Thailand, () Share in Headline Inflation expenses exhibit smaller-than expected

Projection of inflation rates impacts on inflation. Nevertheless, overall

% YoY 2019* 2020 2021 core inflation is expected to remain at a low

Headline inflation -0.9 1.0 level.

0.7

(-1.7) (0.9)

Core inflation 0.3 0.2

0.5

(0.0) (0.1)

* Outturn, ( ) Monetary Policy Report, June 2020 8/23Risks to the Thai financial system remain high following

a sharp economic contraction caused by the COVID-19 outbreak.

The economic recovery will take some time and is likely to be highly uneven.

Risks to the Thai financial system remain high due to a sharp economic contraction this

year which could result in the following:

• Deterioration of households and businesses’ balance sheet and increased risk of defaults.

Financial stability remains sound in several aspects.

• Financial institution stability: high levels of capital fund and loan loss provision which are

preserved to withstand economic uncertainties.

• External stability: high level of international reserves and low external debt to GDP

• Fiscal stability: low level of pre-COVID public debt with long average maturity while most of

the debt is denominated in Thai baht.

The Thai economic recovery would take at least two years before returning to the pre-pandemic

level while facing many uncertainties. Moreover, the recovery would be highly uneven among

economic sectors, regions and firms in each segment. This could affect the long-term potential

economic growth.

9/23The MPC pro-actively implemented accommodative monetary policy

since the beginning of the COVID-19 outbreak.

The policy rate was cut three times from 1.25 percent to a historically low record of 0.50 percent

MPC Meeting No.1 (Feb 5) Early signs of risks from the COVID-19 outbreak were observed

Special MPC Meeting (Mar 20) The COVID-19 outbreak would severely affect the

GDP forecast economy, liquidity as well as the functioning of the Thai

MPC Meeting No. 2 (Mar 25) in 2020 – 5.3% financial markets.

BOT announced a reduction in the FIDF Global economic activities were disrupted by the containment

contribution by 0.23 percent (Apr 7) measures, which led to a-more-severe-than-expected impacts on the

economy, employment and financial stability.

MPC Meeting No. 3 (May 20) Several measures pro-actively implemented should be evaluated

GDP forecast

MPC Meeting No. 4 (Jun 24) in 2020 – 8.1% before implementing additional measures.

MPC Meeting No. 5 (Aug 5) Limited monetary policy space should be preserved

GDP forecast and used only in the most effective timing.

MPC Meeting No. 6 (Sep 23) in 2020 – 7.8%

The MPC stands ready to use additional appropriate monetary policy tools if necessary.

10/23Financial conditions in Thailand continued to be accommodative as reflected by

low policy interest rate and low short-term rates in the financial market

together with declining new loan rates.

Policy interest rates in emerging markets Government bond yields Reference loan rates of commercial banks

Percent Percent Percent

per year per year per year

Dec-19 Oct-20 1.75 policy interest rate 9

6 MLR 1/ NLR 2/ policy interest rate

2-year government bond 8

5 1.50 3-month government bond Oct 7, 2020

7

4 1.25 6

5 5.36

3 1.00 4

2 0.75 Oct 7, 2020 3 3.52*

1 2

0.50 1

0 0 0.50

0.25

ID IN PH MY KR TH

Jan-06

Jan-08

Jan-10

Jan-12

Jan-14

Jan-16

Jan-18

Jan-20

Jan-20

Mar-20

Apr-20

Jul-20

Oct-20

Feb-20

Jun-20

Aug-20

Sep-20

May-20

Source: Bloomberg

Note: Policy interest rate as of Oct 7, 2020 1/ Calculated by averaging the monthly minimum lending rates (MLR)

Source: ThaiBMA

of 5 largest commercial banks

2/ The new loan rate (NLR) published in the table FM_RT_001_S2

interest rates in the financial markets (2005-present) latest data in Aug 2020

* Latest NLR data is in Aug 2020

Article in the box: the new loan rates: true lending costs of businesses Monetary Policy Report, September 2020 11/23Thai baht depreciated from the previous quarter in line with

the declining current account surplus. If the baht were to appreciate rapidly,

the economic recovery would be affected. The MPC would assess the necessity of

implementing additional appropriate measures.

Percentage change of regional currencies from the end of the previous year Current account balance to GDP

percent percent

6% 12%

4.8% 4.8% Forecast

4% 10%

2.9%

Average between 2017 – 2019

2% 8% 7.3 percent

0% -0.3%

6%

-0.8%

-2% -1.2% Average between 2020 – 2021

4% 2.8 percent

Depreciation against the U.S. dollar -2.7%

-4%

-4.1% 2%

-6% -5.2%

0%

PHP

KRW

TWD

SGD

CNY

THB

MYR

INR

IDR

2017 2018 2019 2020F 2021F

Source: Bank of Thailand and Reuters (as of October 7, 2020) Source: Bank of Thailand

12/23Government should continuously implement policies in a targeted and

timely manner to facilitate appropriate adjustments of businesses and households.

Policies should also be coordinated, coherent and consistent.

H1/20 COVID-19 (lockdown) H2/20 . . . . .

The economy gradually recovered

The economy was affected by the COVID-19 • It would take at least two years before returning to

outbreak, especially the implementation of strict the pre-pandemic level.

Excessive

containment measures which led to disruptions • The economy would face many high uncertainties.

production

of economic activities. • The recovery would be greatly uneven among capacity

economic sectors, regions and firms in each segment.

Broad-based and timely Continuously, targeted and timely

Policy Focus to facilitate appropriate adjustments of businesses and households

implemented pro-active

Monetary policy monetary policy accommodation Continue to be accommodative

since the beginning of the year

Financial and credit promptly introduced a broad-based Distribute liquidity in a targeted manner and pro-actively implement debt

debt moratorium, liquidity injection

measures and lessen debt servicing burden restructuring to support changing business structure.

implemented temporary relief Fiscal and supply-sided policies should take a greater roles to address excessive production

Fiscal and supply- measures to alleviate and remedy capacity, support the changing economic structure, patterns of business operation and

sided policies those affected by the outbreak labor skill development to be consistent with the post-COVID environment.

13/23Government should continue to implement financial and credit measures

with more emphasis on targeted measures.

Distribute liquidity Pro-active debt restructuring

to affected households and businesses that is consistent with changing business structures and

in a targeted and timely manner borrowers’ flow of income

• Enhance the effectiveness of the BOT’s soft loan program

Business-sector borrowers

through the special credit guarantee facility called PGS Soft

Loan Plus totaled 57,000 million baht. • “The DR BIZ program” helps solve existing debt problems of

• Revise framework of credit measures previously announced businesses with multiple creditors as well as provides new

to be more targeted as well as covering more affected credits to potential borrowers.

groups, especially small SMEs in tourism-related businesses. Retail borrowers

• Establish a certain standard regarding credit term to speed up • Debt restructuring for retail borrowers by implementing debt

payments from the suppliers and increase liquidity to SMEs. consolidation that does not ruin credit history, lessen debt

• Encourage digital lending and digital factoring for households servicing burden with no additional cost while remaining credit

and SMEs to provide them an easier access to financial lines remain usable.

services.

Article in the box: Additional financial and credit measures from the government, Monetary Policy Report, September 2020

14/23Government should accelerate job creation, especially sectors that are severely affected

but have good potential and these measures should be region-specific in line with their economic activities.

The number of unemployed and underemployed increased Each economic sector was affected differently, while those Workers moved to their domicile and some got employed locally

significantly, although the figures slightly improved following relying heavily on foreign demand were severely affected. but concentrated in the low-paid sectors.

the relaxation of containment measures. The number of working hour missing due to the temporary

suspension of business (section 75) Unemployed and underemployed

Million people (3-month moving average, seasonally adjusted) Missing an-Month (1,000 Man-Month) workers (persons)

6 400 Motor

Underemployed workers (working less than 4 hours per day)

Rubber and plastic 1,046 319,386

5 Unemployed workers

300 Electronics Top two provinces with the highest

4 Aug 2020 Other manufacturing unemployment are Nakhon Ratchasima and

Restaurant and recreation Nakhon Si Thammarat.

3 200

Hotel and tourism share of each economic sector in absorbing workers

2 Commerce

100 Transportation

1 Others 6%

commerce 9% agriculture

0 0 13% 50%

Aug-19

Aug-20

Feb-20

Mar-20

Sep-19

Jul-20

Apr-20

Oct-19

May-20

Jun-20

Dec-19

Jan-20

Nov-19

Jan-14

Jan-15

Jan-16

Jan-17

Jan-18

Jan-19

Jan-20

Jul-13

Jul-14

Jul-15

Jul-16

Jul-17

Jul-18

Jul-19

Jul-20

7%

15%

Source: Department of Labor Protection and Welfare, calculated by Bank Source: National Statistical Office,

Source: Social Security Office, calculated by Bank of Thailand

of Thailand calculated by Bank of Thailand

Should accelerate job creation both Should encourage potential business sectors to Should design area-based policy to match

maintain employment and develop labor skills. region-specific economic activities

full-time and part-time job

15/23Appendix

16/23Risks to growth and inflation projections tilt downward.

Growth forecast

Note: Fan chart covers 90% of the probability distribution

Headline inflation forecast Core inflation forecast

Note: Fan chart covers 90% of the probability distribution Note: Fan chart covers 90% of the probability distribution

17/23Forecast assumptions

%YoY 2019* 2020 2021

Trading partners’ GDP growth (% YoY)2/ 2.7 -4.5 (-4.6) 4.4 (4.2)

Fed funds rate (% year end) 1.50 - 1.75 0.00 - 0.25 (0.00 - 0.25) 0.00 - 0.25 (0.00 - 0.25)

Regional currencies per USD (excl. RMB)3/ 156.6 158.2 (159.5) 156.6 (159.5)

Dubai oil price (USD per barrel) 63.5 41.5 (35.1) 45.8 (37.0)

Farm income (% YoY) 2.4 -1.7 (-3.7) 3.4 (5.7)

Government consumption (billion baht)1/ 2,723 2,833 (2,871) 3,038 (3,028)

Government investment (billion baht)1/ 966 1,051 (1,029) 1,182 (1,184)

Note: 1/assumption includes spending on infrastructure investment plans

2/weighted by each trading partner’s share in Thailand’s total exports

3/increasing index represents depreciation. Decreasing index represents appreciation.

* Outturn

( ) previous assumptions in Monetary Policy Report, June 2020

18/23Assumptions on trading partner’s GDP growth

%YoY Weight

2019* 2020 2021

(%)

United States 18.2 2.2 -5.4 (-7.0) 3.4 (3.2)

Euro area 9.9 1.3 -7.8 (-10.0) 4.5 (4.2)

Japan 14.3 0.7 -5.9 (-5.4) 2.0 (1.7)

China 17.0 6.1 2.1 (0.9) 8.4 (8.9)

Asia (excluding Japan and China)** 32.4 2.7 -5.6 (-3.9) 4.2 (3.6)

Total*** 100 2.7 -4.5 (-4.6) 4.4 (4.2)

Note: *Outturn

**weighted by 7 trading partners’ shares in Thailand’s exports in 2019: Singapore (5.1%) Hong Kong (6.8%)

Malaysia (6.1%) Taiwan (2.3%) Indonesia (5.3%) South Korea (2.7%) and the Philippines (4.0%)

***weighted by proportion of Thai exports to 13 trading partner’s countries in 2019 (including the UK and Australia)

( ) previous assumptions in Monetary Policy Report, June 2020

19/23Changes in Dissemination Frequency of the Financial Account in the Balance of Payment (BOP)

from Monthly basis to Quarterly basis

20/23Changes in dissemination frequency of the financial account in the balance

of payment from a monthly basis to a quarterly basis

Rationale for changing Improvements

dissemination frequency Reduce user confusion induced by frequent

Discrepancy between preliminary and actual data revision and large revision

leads to large revision which could mislead users.

BOT publishes Key BOP data as indicative

Loss of main data source due to the relaxation of estimates with one-month lag time.

regulation regarding cross-border transactions and the

BOT’s policy to lessen data reporting burden. New practice is comparable to

other countries’ standard

Cross-border transactions become more complex as

payments could be settled through electronic IMF recommended to disseminate BOP data on

payment rather than settling through commercial quarterly basis. This new practice is adopted by

banks. most countries.

21/23New BOP and FA data dissemination practice will start from October 30, 2020 onward.

New data dissemination practice will start from October 30, 2020 onward.

Summarized BOP data will be released on a monthly basis, called “partial BOP”:

Current Account (CA) - maintain similar level of detail and release with 1-month lag

Financial Account (FA) – release only FA of Central Bank, General government and Other depository corporations

BOP

Balance of Payments

with 1-month lag

Detailed BOP data will be released on a quarterly basis:

CA & FA – maintain similar level of detail and release with 1-month lag to be in line with the survey results

Frequency of data adjustments will be reduced.

FA data will be released on a monthly basis, called “partial FA”:

Indicative estimates of FA in the nonbank sector will be released with (1) the recent 2

FA to 4 months estimates (2) 1-month lag and (3) only 6 key components

(i.e. direct investment, portfolio investment, currency and deposits and loans)

Financial Account

Cancel the previous format of monthly FA time series

Read additional details in the Stat Horizon article titled “Ease of doing business and policy trade-offs: Reconsidering Dissemination Frequency for the Balance of Payments” retrieved from

https://www.bot.or.th/Thai/Statistics/Articles/Pages/HorizonPage.aspx

22/23Example of new dissemination format

Balance of Payment (summary) Monthly economic indicators: Balance of Payment

Reduce some categories Add balance of payment table

2020 E 2563 E

2562 p 2020 E

… Jul E Aug E Sep E 2019 P ก.ค. E ส.ค. E ก.ย. E

Q1P Q2P

1. Exports (f.o.b.) JulE AugE SepE

General government

2. Imports (f.o.b.)

Central bank

3. Trade balance

Other depository corporations

4. Net services, primary income and secondary income

Other sectors:

5. Current account balance

6. Capital account Foreign Direct Investment

7. Financial account - Exclude Trade credits and Reinvested earnings

8. o/w: Central bank

- Include Trade credits and Reinvested earnings

9. General government

Thai Direct Investment Abroad

10. Other depository corporations

- Exclude Trade credits and Reinvested earnings

11. Other sectors

- Include Trade credits and Reinvested earnings

12. Other financial corporations

Portfolio investment (Assets)

13. Nonfinancial corporations, households, and NPISHs

Portfolio investment (Liabilities)

14. Net errors & omissions

Currency and deposits

15. Overall balance

Loans

23/23You can also read