COMMERCIAL REAL ESTATE OUTLOOK: 2018.Q3 - National Association of REALTORS - CORFAC International

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

National Association of REALTORS® COMMERCIAL REAL ESTATE OUTLOOK: 2018.Q3

Commercial Real Estate Outlook: 2018.Q3 Download: www.nar.realtor/reports/commercial-real-estate-outlook ©2018 | NATIONAL ASSOCIATION OF REALTORS® All Rights Reserved. Reproduction, reprinting or retransmission in any form is prohibited without written permission. Although the information presented in this survey has been obtained from reliable sources, NAR does not guarantee its accuracy, and such information may be incomplete. This report is for information purposes only.

COMMERCIAL REAL ESTATE

OUTLOOK

NATIONAL ASSOCIATION OF REALTORS®

2018 LEADERSHIP TEAM

President

Elizabeth J. Mendenhall , ABR, ABRM, CIPS,

CRB, GRI, ePRO, LCI, PMN

President-Elect

John S. Smaby

First Vice President

Vince E. Malta

Treasurer

Thomas A. Riley, CCIM, CRB

Immediate Past-President

Bill E. Brown

Vice President

Colleen A. Badagliacco, CRB, CRS, ePro,

GRI, SRES

Vice President

Kenny Parcell, ABR, BB, CRS

Chief Executive Officer

Bob Goldberg

COMMERCIAL REAL ESTATE

OUTLOOK

CONTENTS

1 | Economic Overview………………………………………………………………………………… 5

2 | Commercial Real Estate Investments…………………………………………………….. 8

3 | Commercial Real Estate Fundamentals…………………………………………………… 13

4 | Outlook……………………….………………………………………………………………………….. 15

COMMERCIAL REAL ESTATE

OUTLOOK

GEORGE RATIU

Gross Domestic Product Director, Housing & Commercial Research

gratiu@realtors.org

The economy expanded at a stronger pace of 4.1

percent in 2018 Q2 (first estimate), the strongest GAY CORORATON

expansion since 2014 Q3 (4.9 percent). Growth Research Economist

strengthened due to stronger consumption, scororaton@realtors.org

exports, and government spending while

investment spending rose at a slower pace.

Exhibit 1.1: Real GDP Private non-residential fixed investment spending

6 (% Chg Annual Rate) rose 7.3 percent, a slower pace compared to the

first quarter (11.5 percent), as investments in

4 industrial equipment contracted, at -2.2 percent.

The strongest expansions were in structures (e.g.,

2 buildings), at 8.5 percent, and information

processing equipment, at 10.2 percent.

0

Private residential investment contracted 1.1

2013-Q3

2018

2012-Q1

2012-Q3

2013-Q1

2014-Q1

2014-Q3

2015-Q1

2015-Q3

2016-Q1

2016-Q3

2017-Q1

2017-Q3

2018-Q1

percent in 2018 Q2. The number of building starts—

-2 another indicator of residential investment — slightly

Source: BEA declined to a seasonalized annual rate of 1.168

million units in July 2018, down from 1.185 million

Private consumption spending—which accounts units one year ago. Labor, land, financing, and raw

for 69 percent of GDP— expanded at a stronger material costs are cited by home builders as the

pace of 4.0 percent in 2018 Q2, the strongest main headwinds facing residential construction.

pace since 2015. Compared to the pace of

change in the first quarter, spending rose at Exhibit 1.2: GDP - Real Consumer Spending

stronger pace for all types of consumer goods, & Business Investments

except for gasoline/fuel/oil/other energy. The

(% Chg Annual Rate)

Conference Board’s Consumer Confidence Index

also indicated an improvement in consumer Consumer Spending

confidence, with the index at 127.4 in July 2018, 40.0 Non-residential Private Fixed Investments

up from one year ago (120).

20.0

On the other hand, private fixed investment

spending expanded at a slower pace of 5.4 0.0

2006-Q4

2006-Q1

2007-Q3

2008-Q2

2009-Q1

2009-Q4

2010-Q3

2011-Q2

2012-Q1

2012-Q4

2013-Q3

2014-Q2

2015-Q1

2015-Q4

2016-Q3

2017-Q2

2018-Q1

percent as non-residential investment rose at a

-20.0

slower pace compared to the growth in Q1 and

as residential investment spending contracted. -40.0

Source: BEA, SAAR, Bil.Chn.2009$

NATIONAL ASSOCIATION of REALTORS® | RESEARCH DIVISION | www.nar.realtor/research-and-statistics 5

COMMERCIAL REAL ESTATE

OUTLOOK

Both exports and imports rose at a stronger pace in Employment

2018 Q2 compared to the pace in Q1. Exports

expanded by 9.3 percent, while imports rose at a Employment conditions remain healthy. During the

more modest pace of 0.5 percent, resulting in a 12-month period of August 2017‒July 2018, there

smaller deficit in exports of goods and services. were 2.4 million payroll jobs added, more than the

2.2 million jobs that were added in the same 12-

month period one year ago. The economy has been

Exhibit 1.3: Real Exports & Imports (%

steadily adding employment since October 2010.

Chg Annual Rate)

Exports Imports Exhibit 1.5: 12-Month Payroll

40 Employment (Change, '000)

4000

20

2000

0 0

-20 -2000

-4000

-40

-6000

2007-Q3

2015-Q4

2006-Q1

2006-Q4

2008-Q2

2009-Q1

2009-Q4

2010-Q3

2011-Q2

2012-Q1

2012-Q4

2013-Q3

2014-Q2

2015-Q1

2016-Q3

2017-Q2

2018-Q1

-8000

2009-Apr

2011-Aug

2008-Feb

2008-Sep

2013-May

2009-Nov

2011-Jan

2012-Mar

2015-Feb

2015-Sep

2016-Apr

2016-Nov

2018-Jan

2017-Jun

2006-Dec

2007-Jul

2010-Jun

2013-Dec

2014-Jul

2012-Oct

Source: BEA, SAAR, Bil.Chn.2009$

Federal and state/local consumption and Source: BLS

investment spending rose modestly by 2.1 During the 12-month period of August 2017–

percent (1.5 percent in Q1). Federal spending July 2018, employment expanded in all

rose 3.5 percent while state and local spending sectors, except information services (-21,000)

increased 1.4 percent. Government spending and utilities (-3,000). Retail trade, which has

has been a weak source of growth compared to lost jobs in the past, generated 96,000 jobs.

private consumer and investment spending and

exports. Exhibit 1.6: Payroll Employment:

12-Month Change ('000)

Exhibit 1.4: Real Government Government

Spending (% Chg Annual Rate) Leisure/Hospitality

Educ./Health

Federal State and Local Prof./Bus. Services

15.0 Financial Activities

10.0

Information

Utilities

5.0 Transp./Warehousing

Retail Trade

0.0

Wholesale Trade

-5.0 Manufacturing

Construction

-10.0

Mining/Logging

Q1/2006

Q4/2006

Q3/2007

Q2/2008

Q1/2009

Q4/2009

Q3/2010

Q2/2011

Q1/2012

Q4/2012

Q3/2013

Q2/2014

Q1/2015

Q4/2015

Q3/2016

Q2/2017

Q1/2018

-100 0 100 200 300 400 500 600

Source: BLS

Source: BEA, SAAR, Bil.Chn.2009$

NATIONAL ASSOCIATION of REALTORS® | RESEARCH DIVISION | www.nar.realtor/research-and-statistics 6

COMMERCIAL REAL ESTATE

OUTLOOK

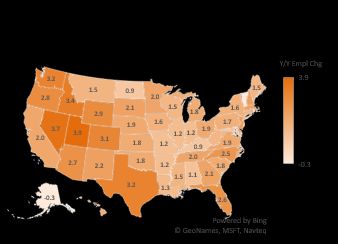

The West and South regions have Inflation and Interest Rates

experienced the strongest gains in non-farm

employment. In July 2018, employment With sustained growth, inflation has trended up. In

increased at the fastest pace from year-ago July 2018, prices for all items (CPI) rose 2.9 percent

levels in Utah, Nevada, Idaho, Texas, from the levels one year ago. Core inflation, which

Washington, and Colorado, with employment measures the change in prices other than food and

growing at above three percent. Employment energy, rose to 2.4 percent. The Federal Open

increased in all states except Alaska. Market Operations Committee (FOMC) seeks to

Nationally, non-farm employment rose two keep inflation at two percent when setting the

percent in July 2018 from the level one year federal funds rate target. FOMC has raised the

ago level, federal funds target range twice this year, to a range

of 1.75 to two percent in June 2018, an increase of

50 basis points since January 2018. With the higher

target, the 30-year fixed rate for mortgages rose to

an average of 4.53 percent in July 2018 (3.97

percent in July 2017).

Exhibit 1.9: Inflation

All Items All Items, Less Food and Energy

6.0

4.0

2.0

0.0

-2.0

-4.0

Jul/2005

Jul/2016

Jun/2006

Apr/2008

Jun/2017

Nov/2001

May/2007

Sep/2003

Nov/2012

May/2018

Jan/2000

Dec/2000

Mar/2009

Aug/2004

Feb/2010

Jan/2011

Dec/2011

Sep/2014

Aug/2015

Oct/2013

Oct/2002

The labor market continues to tighten. The

unemployment rate dropped below four

percent, to 3.9 percent in July 2018. The Source: BLS

unemployment rate has hovered at four

percent since April 2018. Exhibit 1.10: Interest Rates

Federal Funds Rate (Midpoint)

Exhibit 1.8: Unemployment 10.0000

12 30-Year Fixed Rate for Mortgages

10 8.0000

8 6.0000

6

4.0000

4

2 2.0000

0 0.0000

2008-Sep

2012-Sep

2006-Sep

2007-May

2009-May

2010-Sep

2011-May

2013-May

2014-Sep

2015-May

2016-Sep

2017-May

2006-Jan

2008-Jan

2010-Jan

2012-Jan

2014-Jan

2016-Jan

2018-Jan

Jan/2018

Jan/2000

Jan/2001

Jan/2002

Jan/2003

Jan/2004

Jan/2005

Jan/2006

Jan/2007

Jan/2008

Jan/2009

Jan/2010

Jan/2011

Jan/2012

Jan/2013

Jan/2014

Jan/2015

Jan/2016

Jan/2017

Source: BLS Source: FRB, Freddie Mac

NATIONAL ASSOCIATION of REALTORS® | RESEARCH DIVISION | www.nar.realtor/research-and-statistics 7

COMMERCIAL REAL ESTATE

OUTLOOK

Commercial space is concentrated in large After the two-year decline in sales volume,

buildings, yet large buildings are a relatively small investments in LCRE markets posted increases in

number of the overall stock of commercial buildings. both the first and second quarters of this year.

Based on Energy Information Administration data

approximately 72 percent of commercial buildings Exhibit 2.1: CRE Sales Volume ($2.5M+)

are less than 10,000 square feet in size.1 An

Individual Portfolio Entity

additional eight percent of commercial buildings are

$200

less than 17,000 square feet in size. In short, the

Billions

commercial real estate market is bifurcated, with the $180

majority of buildings (81 percent) relatively small

$160

(SCRE), but with the bulk of commercial space (71

percent) in larger buildings (LCRE). $140

$120

Likewise, commercial sales transactions are

measured and reported based on deal value. $100

Commercial deals at the higher end—$2.5 million

$80

and above—comprise a large share of investment

sales, and generally receive most of the press $60

coverage. Smaller commercial transactions tend to

$40

be obscured given their values. However, these

smaller properties comprise the backbone of daily $20

economic activity—e.g. neighborhood shopping $-

centers, warehouses, small offices, supermarkets,

15Q2

07Q1

07Q4

08Q3

09Q2

10Q1

10Q4

11Q3

12Q2

13Q1

13Q4

14Q3

16Q1

16Q4

17Q3

18Q2

etc. Given the importance of these buildings to local

communities, and REALTORS®’ active roles in Source: Real Capital Analytics

serving these markets, this report focuses on

illuminating trends in both large and small markets.

Large Cap Commercial Real Estate Markets

The first half of the year confirmed the maturation of

the current real estate cycle. Investors have become

more disciplined in the acquisition process, as rising

interest rates are squeezing the spread between

cap rates and long-term bonds. In addition, faced

with declining sales, sellers have been adjusting

their price expectations and have started to close

the noticeable pricing gap of the past two years.

1Smith and Ratiu, (2015), "Small Commercial Real Estate Market,"

National Association of REALTORS®

NATIONAL ASSOCIATION of REALTORS® | RESEARCH DIVISION | www.nar.realtor/research-and-statistics 8COMMERCIAL REAL ESTATE

OUTLOOK

Investment volume in the large cap space reached Office properties accounted for almost one-in-four

$236.1 billion in transactions by the midpoint of this transactions during the quarter, with $28.8 billion in

year, a 4.1 percent advance compared with the sales. However, office investment volume faltered,

same period in 2017, according to Real Capital with a 17 percent decline. The sector seemed to be

Analytics (RCA). Deal volume proved mixed across undergoing a rebalancing, with Central Business

property types, with momentum shifting further District properties experiencing waning interest,

toward industrial and apartment properties in both while suburban office properties regained their

major and secondary markets. attractiveness.

Apartment sales accounted for the largest share of The retail sector closed $20.7 billion in sales during

transactions—29 percent—with $34.5 billion in the second quarter, an increase from the same

closed transactions, based on RCA data. However, period in 2017. However, the advance was mostly

the second quarter of the year saw apartment deal driven by Unibail Rodamco’s acquisition of the

volume post a seven percent decline year-over- Westfield portfolio, as single asset sales mirrored

year. investor concern over the general direction of the

retail space. Industrial properties remained on a

strong upward trend, with sales totaling $18.2 billion

Exhibit 2.2: Sector Momentum - Major vs in the second quarter, up 17 percent from the prior

Non-Major Metros year.

15% Exhibit 2.3: Commercial Property Price

NMM

Apartment Indices

NCREIF Green Street Advisors

10% 6MM

Real Capital Analytics Federal Reserve

Price (RCA CPPI) YoY Chg

NMM Office - Industrial

Sub 6MM

350.0

6MM OfficeApartment

-

Sub

NMM 300.0

5% NMM Hotel

Industrial

NMM Office -

CBD 250.0

6MM Hotel

NMM Retail 200.0

6MM Retail

0%

150.0

100.0

-5%

50.0

-40% -20% 0% 20% 40%

Volume YoY Chg (trailing 12-month) 0.0

Source: Real Capital Analytics

2006-Q1

2001-Q1

2002-Q1

2003-Q1

2004-Q1

2005-Q1

2007-Q1

2008-Q1

2009-Q1

2010-Q1

2011-Q1

2012-Q1

2013-Q1

2014-Q1

2015-Q1

2016-Q1

2017-Q1

2018-Q1

NATIONAL ASSOCIATION of REALTORS® | RESEARCH DIVISION | www.nar.realtor/research-and-statistics 9COMMERCIAL REAL ESTATE

OUTLOOK

Prices in LCRE markets advanced 6.5 percent year- Other commercial real estate price indices posted

over-year in the second quarter of 2018, according mixed trends. The Green Street Advisors

to RCA’s Commercial Property Price Index. All Commercial Property Price Index—focused on large

property types posted higher prices during the cap properties—was virtually flat, with a 0.4 percent

quarter, with the apartment and industrial properties gain on a yearly basis during the second quarter, at

recording higher comparative gains of 11.6 percent a value of 126.3. The GSA index has flattened for

and 6.5 percent, respectively. the past several quarters. The National Council of

Real Estate Investment Fiduciaries (NCREIF) Price

Exhibit 2.4: NCREIF Property Index Returns— Index increased 8.5 percent on a yearly basis during

2018.Q2 the second quarter, accelerating from the prior

quarter’s 7.1 percent gain.

NATIONAL 1.81%

OFFICE 1.54% Cap rates spent the first half of the year continuing

on a sideways trend, in a narrow range of 6.7-6.8

INDUSTRIAL 3.58%

percent, according to RCA. Apartments continued

RETAIL 1.32% experiencing slight cap rate compression, with an

APARTMENT 1.54%

average of 5.5 percent in the second quarter.

Industrial transactions also posted a minor decline in

Source: National Council of Real Estate Investment Fiduciaries cap rates, at an average of 6.4 percent. Office and

hotel sales saw increases in average cap rates,

while retail deals retained an average rate of 6.5

percent in the second quarter, on par with last year.

NATIONAL ASSOCIATION of REALTORS® | RESEARCH DIVISION | www.nar.realtor/research-and-statistics 10COMMERCIAL REAL ESTATE

OUTLOOK

Small Cap Commercial Real Estate Markets Exhibit 2.6: Sales Prices (YoY % Chg)

The second quarter of the year marked a slowdown Real Capital Analytics CRE Markets

in investment volume gains in the small cap space. REALTOR® CRE Markets

Commercial real estate sales in SCRE markets

increased by 0.5 percent from the same quarter in 15.0%

2017. The slight advance stood in contrast to the 4.9

percent average second-quarter increase typical of 10.0%

the previous five years.

5.0%

The figure may portend a broader slowdown,

mirroring the LCRE markets trend, with a two-year 0.0%

lag. The shortage of available commercial inventory

2014.Q1

2008.Q4

2009.Q3

2010.Q2

2011.Q1

2011.Q4

2012.Q3

2013.Q2

2014.Q4

2015.Q3

2016.Q2

2017.Q1

2017.Q4

remained ranked as the top concern for -5.0%

REALTORS®, likely impacting deal volume. Almost

half of respondents to a market survey ranked tight -10.0%

inventory as the number one issue affecting their

markets.

-15.0%

Exhibit 2.5: Sales Volume (YoY % Chg) -20.0%

Real Capital Analytics CRE Markets

-25.0% Sources: National Association of REALTORS®, Real Capital Analytics

REALTOR® CRE Markets

The inventory squeeze continued exerting upward

200%

pressure on prices in SCRE markets, to the tune of

a 5.1 percent yearly advance in the second quarter

150% of this year. In turn, the pricing gap between buyers

and sellers proved the second highest ranked

concern for commercial practitioners, reported by

100% about one-in-five members.

Capitalization rates in SCRE markets moved

50% sideways in the second quarter of 2018, at an

average of 6.8 percent. Compared with the prior

year, cap rates declined 46 basis points.

0%

2016.Q2

2008.Q4

2009.Q3

2010.Q2

2011.Q1

2011.Q4

2012.Q3

2013.Q2

2014.Q1

2014.Q4

2015.Q3

2017.Q1

2017.Q4

-50%

-100% Sources: National Association of REALTORS®, Real Capital Analytics

NATIONAL ASSOCIATION of REALTORS® | RESEARCH DIVISION | www.nar.realtor/research-and-statistics 11COMMERCIAL REAL ESTATE

OUTLOOK

International transactions remained a fixture in year at 2.6 percent, and rose to 2.9 percent by

REALTORS®’ CRE markets in the final quarter of August of this year. As the Federal Reserve is

the year, accounting for 12.0 percent of responses expected to continue raising the short-term rate,

to a survey. The average international sale price longer termed bonds should continue feeling upward

was $2.5 million in the second quarter of the year. pressure. The upward trajectory of 10-year

Indicating a likely preference for safety of capital Treasuries, coupled with a flat cap rate movement,

over returns, the average cap rate for SCRE has begun to narrow the spread between the two. In

international deals was 6.7 percent. the second quarter, the spread dropped below 400

basis points, a noticeable decline from the over 570

Longer-dated bond yields advanced over the first basis points registered in 2012.

half of 2018. The Treasury 10-year note started the

Exhibit 2.7: Cap Rates - 2018.Q2 Exhibit 2.8: CRE Spreads: Cap Rates to 10-

Yr. T-Notes (bps)

RCA Markets REALTOR® Markets

8.0% RCA Cap Rates REALTORS® Cap Rates

1200

7.0%

1000

6.0%

5.0% 800

4.0% 600

3.0% 400

2.0%

200

1.0%

0

0.0%

11Q3

13Q1

10Q1

10Q3

11Q1

12Q1

12Q3

13Q3

14Q1

14Q3

15Q1

15Q3

16Q1

16Q3

17Q1

17Q3

18Q1

Office Industrial Retail Apartment

Sources: National Association of REALTORS®, Real Capital Analytics Sources: National Association of REALTORS®, Real Capital Analytics

NATIONAL ASSOCIATION of REALTORS® | RESEARCH DIVISION | www.nar.realtor/research-and-statistics 12COMMERCIAL REAL ESTATE

OUTLOOK

Large Cap Commercial Real Estate Markets

The commercial fundamentals in LCRE markets translated into a net of 4.5 million square feet of

continued to provide solid performance during the retail space absorbed during the second quarter,

second quarter of 2018, benefitting from strong according to CBRE. The figure was slightly lower

economic tailwinds. While demand maintained than the first quarter, as store closures continued to

course, market metrics were more nuanced across affect the mall landscape. Retail construction activity

the core property sectors. declined to the lowest level since the first quarter of

2012, as completions totaled 7.0 million square feet.

The second quarter of 2018 witnessed solid demand The retail availability rate moved sideways, at 6.5

for office space, driven by continued employment percent in the fourth quarter, as asking retail rents

gains in office-using industries. Net absorption of reached $17.37 per square foot, a 5.1 percent

office spaces totaled 15.5 million square feet during increase year-over-year.

the quarter, according to CBRE. On the supply side,

completions remained strong, with over 10 million An improving employment environment and growing

square feet of new space finished during the population continue to favor demand for housing.

quarter. According to CBRE, a majority of newly- With residential pricing remaining strong and a

finished space was preleased, as tenants continue market influenced by tight inventory, the apartment

to seek quality work accommodations. Reflecting sector continued to experience favorable conditions

the demand-supply balance, the office vacancy rate in the second quarter of the year. Net absorption of

slid to 13.0 percent. The asking rent for office space multifamily space totaled 249,000 units over the 12

nationally averaged $32.58 per square foot, a 1.3 months ending in June 2018, according to CBRE.

percent increase from a year ago. Construction of multifamily properties maintained

momentum, with 276,000 units delivered over the

Boosted by strong consumer spending and trade, same period. The national vacancy rate inched up

the industrial sector experienced another quarter of 10 basis points from a year ago, to an average of

gains in fundamentals. Industrial net absorption 4.7 percent. Apartment effective rents rose 2.0

totaled 58.8 million square feet during the second percent year-over-year, to an average of $1,685 per

quarter, according to CBRE data. The solid demand month during the quarter.

outpaced new deliveries, even as new supply rose

7.5 percent from the second quarter of 2017.

Completions totaled 48.9 million square feet, leading

to a decline in the vacancy rate, to 4.4 percent.

Industrial asking rents advanced in the second

quarter to $7.11 per square foot, a 5.5 percent year-

over-year increase, and the highest level since

1989.

As the unemployment rate and rising wages have

buoyed consumer optimism, retail spending

registered a noticeable gain. Some of that spending

NATIONAL ASSOCIATION of REALTORS® | RESEARCH DIVISION | www.nar.realtor/research-and-statistics 13COMMERCIAL REAL ESTATE

OUTLOOK

Small Cap Commercial Real Estate Markets

Commercial fundamentals in REALTORS®’ markets Vacancy rates reflected the mixed conditions of the

notched a quarter of gains, following a softer first core property types. The office and industrial

quarter. Leasing volume advanced by 5.9 percent vacancy rates declined 30 basis points and 140

from the preceding quarter, as demand for space basis points, respectively, from a year ago. Retail

remained solid in small cap markets. New properties experienced higher vacancies, averaging

construction rose by 2.2 percent from the prior 12.0 percent in the second quarter. Multifamily

quarter, as developers in SCRE markets faced spaces contended with rising supply, which pushed

rising construction costs. Leasing rates increased by vacancy rates up 30 basis points, to 6.1 percent.

1.8 percent, as concessions declined 2.8 percent.

Exhibit 3.1: REALTORS® Fundamentals Exhibit 3.2: REALTORS® Commercial

Vacancy Rates

New Construction Leasing Volume

Office Industrial Retail

15%

Multifamily Hotel

10% 30.0%

5% 25.0%

% Change, Quarter-over-quarter

0%

20.0%

2009.Q2

2010.Q1

2010.Q4

2011.Q3

2012.Q2

2013.Q1

2013.Q4

2014.Q3

2015.Q2

2016.Q1

2016.Q4

2017.Q3

2018.Q2

-5%

15.0%

-10%

10.0%

-15%

-20% 5.0%

-25%

0.0%

2018.Q1

2010.Q1

2010.Q3

2011.Q1

2011.Q3

2012.Q1

2012.Q3

2013.Q1

2013.Q3

2014.Q1

2014.Q3

2015.Q1

2015.Q3

2016.Q1

2016.Q3

2017.Q1

2017.Q3

-30%

Source: National Association of Realtors®

Tenants in REALTORS®’ markets remained Source: National Association of Realtors®

focused on smaller footprints. In the second quarter,

the ‘5,000 square feet and below’ segment

accounted for 75.0 percent of activity. The ‘5,000 –

7,499 square feet’ segment accounted for 5.0

percent of activity during the quarter, similarly to the

‘10,000 – 49,999 square feet’ segment’s 6.0

percent. The ‘50,000 square feet and above’

segment comprised 4.0 percent of total activity.

NATIONAL ASSOCIATION of REALTORS® | RESEARCH DIVISION | www.nar.realtor/research-and-statistics 14COMMERCIAL REAL ESTATE

OUTLOOK

Economy

NAR forecasts economic output to expand at a

stronger pace of 3.0 percent in 2018. This forecast 2016 2017 2018 2019

factors in the increased consumer and investment Annual Growth Rate, %

spending arising from the tax changes under the Real GDP 1.6 2.2 3.0 2.7

Tax Cuts and Jobs Act, which includes a reduction Nonfarm Payroll Employment 1.8 1.6 1.7 1.5

in the corporate tax rate from 35 percent to 21 Consumer Prices 1.3 2.1 2.9 2.7

percent. Payroll employment is projected to Level

increase 1.7 percent for the year, which would Consumer Confidence 100 121 127 125.0

push the unemployment rate down to 3.9 percent. Percent

Inflation is expected to accelerate to 2.9 percent, Unemployment 4.9 4.4 3.9 3.9

as the economy continues to reach its full capacity Fed Funds Rate 0.4 1.0 1.8 2.6

and as oil prices continue to recover. NAR 3-Month T-bill Rate 0.3 1.0 1.9 2.5

forecasts the prime rate to hit 4.9 percent and the Prime Rate 3.5 4.1 4.9 5.6

30-year government bond rate to move up to 3.2 10-Year Gov’t Bond 1.8 2.3 3.0 3.5

30-Year Gov’t Bond 2.6 2.9 3.2 3.7

percent for the year. NAR expects monetary policy

to continue to tighten in 2019, but at a cautious

Source: National Association of REALTORS®

pace.

NATIONAL ASSOCIATION of REALTORS® | RESEARCH DIVISION | www.nar.realtor/research-and-statistics 15COMMERCIAL REAL ESTATE

OUTLOOK

Commercial Real Estate

Exhibit 4.2: Commercial Real Estate Vacancy Forecast (%)

2017.Q2 2017.Q3 2017.Q4 2018.Q1 2018.Q2 2018.Q3 2018.Q4 2019.Q1 2019.Q2 2019.Q3 2019.Q4 2020.Q1 2017 2018 2019

Office 12.7 12.7 12.0 12.7 12.4 13.2 13.2 13.1 13.0 12.8 12.8 12.7 12.8 12.9 12.9

Industrial 9.1 8.9 7.8 7.4 7.7 7.5 7.4 7.2 6.9 6.7 6.5 6.7 8.8 7.5 6.8

Retail 10.4 12.1 11.4 12.0 12.0 12.0 12.1 12.1 11.9 12.1 12.3 11.7 11.8 12.0 12.1

Multifamily 5.8 5.3 5.0 5.5 6.1 6.3 6.4 6.3 6.4 6.5 6.6 5.4 5.5 6.1 6.4

Source: National Association of REALTORS®

With economic output and employment trends

continuing on an expansionary path, commercial

fundamentals are expected to exhibit solid demand

and increasing cash flows. Vacancy rates will likely

provide mixed results, with multifamily undergoing

growing availability from an expanding supply

pipeline. Office and retail properties will likely see

vacancies move sideways, while industrial spaces

will find rent growth advancing at a steady pace.

On the investment side, rising interest rates will

continue to add upward pressure on investment

yields. The Federal Reserve has indicated that it is

committed to unwinding its balance sheet and, as

consumer prices rose by close to 3.0 percent in

August, will continue with several rate increases in

2018 and 2019. Most analysts are expecting

another two rate hikes this year, and three-to-four

next year.

For commercial investments, the trends have

already shown in pricing. Cap rates seem to have

found a floor, and for some property types, have

already begun to turn upward. In SCRE markets,

price gains will likely continue during the latter half

of 2018, mostly due to the inventory shortage.

However, the momentum is moderating, and

beginning to converge toward that of LCRE markets.

NATIONAL ASSOCIATION of REALTORS® | RESEARCH DIVISION | www.nar.realtor/research-and-statistics 16COMMERCIAL REAL ESTATE

OUTLOOK

The National Association of REALTORS®, “The Voice for Real Estate,” is America’s largest trade

association, representing 1.3 million members, including NAR’s institutes, societies and

councils, involved in all aspects of the real estate industry. NAR membership includes brokers,

salespeople, property managers, appraisers, counselors and others engaged in both residential

and commercial real estate. The term REALTOR® is a registered collective membership mark

that identifies a real estate professional who is a member of the National Association of

REALTORS® and subscribes to its strict Code of Ethics. Working for America's property owners,

the National Association provides a facility for professional development, research and

exchange of information among its members and to the public and government for the purpose

of preserving the free enterprise system and the right to own real property.

NATIONAL ASSOCIATION OF REALTORS®

RESEARCH GROUP

The Mission of the NATIONAL ASSOCIATION OF REALTORS® Research Group is to produce

timely, data-driven market analysis and authoritative business intelligence to serve members,

and inform consumers, policymakers and the media in a professional and accessible manner.

To find out about other products from NAR’s Research, visit

www.nar.realtor/research-and-statistics

NATIONAL ASSOCIATION OF REALTORS®

RESEARCH GROUP

500 New Jersey Avenue, NW

Washington, DC 20001

202.383.1000COMMERCIAL REAL ESTATE OUTLOOK | 2018.Q3

You can also read