Global Financial Stability Update - International ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Confidential

Confidential

January

GlobalSUMMARY

2021 EXECUTIVE Financial Stability Update

Vaccines Inoculate Markets, but Policy Support Is Still Needed

The Global Financial Stability Update at a Glance

Approval and rollout of vaccines have boosted expectations of a global recovery and lifted risk

asset prices, despite rising COVID-19 cases and persistent uncertainties surrounding the

economic outlook.

Until vaccines are widely available, the market rally and the economic recovery remain predicated

on continued monetary and fiscal policy support. Inequitable distribution of vaccines risks

exacerbating financial vulnerabilities, especially for frontier market economies.

An ongoing rebound of portfolio flows provides better financing options for emerging market

economies facing large rollover needs in 2021.

Policy accommodation has mitigated liquidity strains so far, but solvency pressures may resurface

in the near future, especially in riskier segments of credit markets and sectors hit hard by the

pandemic. Profitability challenges in the low-interest-rate environment may weigh on banks’

ability and willingness to lend in the future.

Policymakers should continue to provide support until a sustainable recovery takes hold as

underdelivery may jeopardize the healing of the global economy. However, with investors betting

on a persistent policy backstop and a sense of complacency permeating markets as asset

valuations rise further, policymakers should also be prepared for the risks of a market correction.

With monetary policy anticipated to remain accommodative in coming years, policymakers should

contain rising vulnerabilities to avoid putting growth at risk in the medium term.

A Policy Bridge to the Vaccine

Financial markets have looked beyond the global resurgence of COVID-19 cases.

Announcements and rollout of vaccines have boosted hopes of a global economic recovery in 2021

and pushed risk asset prices higher. The speed of the recovery will depend crucially on production,

distribution networks, and access to vaccines. As discussed in the January 2021 World Economic Outlook

(WEO) Update, continued monetary and fiscal support remain vital to lessen lingering uncertainties,

build a bridge to the recovery, and ensure financial stability.

Risks to the baseline could threaten financial stability in some sectors and regions. A delay in

the recovery would require prolonged accommodation, further fueling financial vulnerabilities. Uneven

vaccine distribution and asynchronous recovery could imperil capital flows to emerging market

economies, especially if advanced economies were to begin to normalize policy, and some countries

could face daunting challenges. An asset price correction, should investors suddenly reassess growth

prospects or the policy outlook, could interact with elevated vulnerabilities, creating knock-on effects

on confidence and jeopardizing macro-financial stability.

International Monetary Fund | January 2021 1GLOBAL FINANCIAL STABILITY UPDATE, JANUARY 2021

Figure 1. Equity Market Performance Finally, Some Good News

(Index; November 6, 2020 = 100)

135

Initial vaccine announcements Announcements of earlier-than-anticipated

Vaccine rotation basket

130

US small cap (Russell)

effective COVID-19 vaccines have boosted

125 EM (MSCI) market sentiment and paved the way for the

120 US

Europe global economic recovery. Industries such as

115

airlines, hospitality, and consumer services

110

rebounded in late 2020 as investors rotated into

105

these previously battered sectors in search of value

100

95

Oxford

AstraZeneca (Figure 1). Stock prices of smaller firms, including

90

Moderna

Pfizer

in clean energy, also benefitted. In advanced

85

BioNTech

economies, investment-grade and high-yield

Oct. 2020 Nov. 20 Dec. 20 Jan. 21

corporate bond spreads have tightened sharply—

Sources: Bloomberg Finance L.P.; and IMF staff calculations.

Note: Vaccine rotation basket is an equal weighted index of US hotels close to or even below pre-February 2020 levels—

and real estate and world airline equities. EM = emerging markets. while rates have reached record lows, as investors

Figure 2. US Earnings Revisions and Rate Expectations

(US dollars a share, left scale; percent, right scale) continue to reach for yield. Spreads of emerging

market sovereign debt have exhibited a similar

200 2021 EPS estimates (left scale) 2.6

compression dynamic.

195 Average short-term rate expected over next 2.4

10 years (right scale)

190 2.2 Financial markets have shrugged off the most

185

2.0 recent softening in economic activity. The surge

180

1.8 of COVID-19 infections and associated stringency

175

1.6 measures since late 2020 have adversely affected

170

165 1.4 economic activity in many countries, pointing to a

160 1.2 possible slowdown in the fourth quarter (see the

155 1.0 January 2021 WEO Update). Yet, despite persistent

uncertainties surrounding the economic outlook,

investors appear to remain confident about growth

Source: IMF staff calculations. prospects in 2021, betting that continued policy

Note: Earnings per share (EPS) based on Thomson Reuters

Datastream IBES for the S&P 500; average expected short-term rates support will offset any possible near-term

derived from Treasury bonds and Adrian, Crump, and Moench model.

disappointment. The much discussed disconnect

Figure 3. COVID-19 Infections and Vaccine Preorders

between financial markets and the economy

persists. Despite the recent rise in US long-end

rates, market participants point to expectations of

very low rates over coming years and upward

revisions in earnings expectations since the vaccine

announcements as justification for the market rally

(Figure 2).

Vaccine access is likely to be uneven, and

equitable distribution may take time. Many

advanced economies, such as Canada, some

Source: Duke Global Health Innovation Center. European Union countries, the United Kingdom,

Note: Vaccine preorders refers to confirmed doses as of January 19,

2021. EU = European Union. Data labels use International and the United States, have prepurchased vaccines,

Organization for Standardization (ISO) country codes.

2 International Monetary Fund | January 2021GLOBAL FINANCIAL STABILITY UPDATE, JANUARY 2021

Figure 4. Emerging Market Sovereign Bond Issuance with large per capita coverage. By contrast,

(Billions of US dollars; share in percent)

procurement of vaccine doses for emerging market

B

50

BB BBB A or above Share of HY issuance (3 month moving average, right scale)

50

and developing economies via direct negotiation or

45 45 through the multilateral COVAX pillar lag

40 40

significantly.1 The need for access to vaccines is

35 35

30 30 particularly urgent in countries where cases have

25 25 accelerated recently or remain very high (Figure 3).

20 20

15 15 No Global Financial Crisis to Date: Don’t Turn

10 10

It into One!

5 5

0 0

Delayed access to comprehensive health care

solutions could mean an incomplete global

Sources: Bondradar; and IMF staff calculations. recovery and endanger the global financial

Note: Refers to international hard currency bond issuance. January

2021 is partial data through January 20. HY = high yield. system. With emerging market economies

Figure 5. Portfolio Flows to Emerging Markets accounting for about 65 percent of global growth

(US billions) (about 40 percent excluding China) over 2017–19,

75 Debt Equity

delays in tackling the pandemic in such countries

50

may bode ill for the global economy. Supply chain

25

disruptions could affect corporate profitability even

0

in regions where the pandemic is under control.

-25

And because growth is a crucial ingredient for

-50

financial stability, an uneven and partial recovery

-75

risks jeopardizing the health of the financial system.

-100

Emerging markets have large financing needs.

Large and persistent fiscal deficits in most

Sources: Institute of International Finance; and IMF staff calculations.

emerging and frontier market economies are likely

Figure 6. 2021 Gross External Financing Needs

(Percent of GDP) to persist in 2021, albeit to a smaller extent than in

40

Short-term debt (by remaining maturity) 2020. In the baseline WEO scenario of continued

Current account deficit

36 Total easy financial conditions, market financing will

32

28

remain a significant source of funding, as it has

24 been in recent months (Figure 4). The resumption

20

16 of portfolio flows is central to the stability of many

12 emerging market economies (Figure 5); retaining

8

4 market access is essential. An uneven global

0

-4

economic recovery because of delayed health care

and vaccine solutions may present a formidable

UKR

BRA

PHL

IND

IDN

PER

TUN

TUR

KEN

THA

PAK

ZAF

COL

ROU

MEX

EGY

Investment grade Sub-investment grade challenge for emerging and frontier economies.

Sources: National authorities; and IMF staff calculations. With some countries already constrained by limited

Note: Brazil, Romania, South Africa, Thailand, and Ukraine report

intercompany lending in their gross external financing needs.

1COVAX—the vaccine-focused pillar of the Access to COVID-19 Tools Accelerator, a partnership of the World Health Organization, the European

Commission, and France—is tasked with developing and providing innovative and equitable access to COVID-19 vaccines to all participating countries. It

was launched in April 2020 in response to the pandemic, and it aims to make 2 billion doses available by the end of 2021.

International Monetary Fund | January 2021 3GLOBAL FINANCIAL STABILITY UPDATE, JANUARY 2021

Figure 7. US High-Yield Spreads policy space, especially where access to capital

(Percent)

markets is still not fully restored, the prospect of

25 25

higher long-term rates in advanced economies as

Transportation central banks find themselves closer to policy

20 20

Consumer cyclical normalization may jeopardize the rollover of large

Technology

15 15

external financing needs (Figure 6).

Energy

While solvency pressures have been limited so

10 10 far, risks in the nonfinancial corporate sector

remain. Reflecting unprecedented policy support,

5 5 spreads have recovered almost entirely, even in the

sub-investment-grade sector, although sectoral

0 0 differences persist (Figure 7). Default rates at large

Jan. 2020 Apr. 20 Jul. 20 Oct. 20 Jan. 21

firms have remained well below previous peaks,

Sources: S&P Global; and IMF staff calculations.

Figure 8. Evolution of Potential “Fallen Angels”

and bankruptcies among smaller firms have stayed

(Count, left scale; US billions, right scale) low or even declined in some cases. However,

140 Global count of potential fallen angels (left scale) 250 challenges remain. For example, the number of

120

US fallen angels outstanding (right scale)

potential “fallen angels” (that is, firms with a BBB

Europe fallen angels outstanding (right scale)

200

minus rating and negative outlook) has tripled

100

globally since the beginning of the pandemic, and

150

80 in some jurisdictions (for example, the European

60

100

Union and the United States) the potential for

40

further downgrades is elevated (Figure 8). In China,

50 defaults by state-owned enterprises in the last

20

quarter of 2020 suggest that addressing financial

0 0 vulnerabilities continues to be a priority. Ultimately,

2008 09 10 11 12 13 14 15 16 17 18 19 20

Sources: ICE BAML; S&P Global; and IMF staff calculations.

the health of the global corporate sector will

Note: See text for definition of “fallen angel” companies. depend critically on the evolution of the pandemic

Figure 9. European Bank Performance Metrics and on the extent and duration of policy support.

(Percent)

Should investors reassess the prospects for

21

COVID-19 Vaccine economic growth and the outlook for monetary

19 outbreak announcement

and fiscal policy, liquidity pressures, and the risk of

17

COE (Cost of equity) such pressures morphing into insolvencies, may

15 ROE (Return on equity)

resurface.

13

Household debt may rise, on the back of

11

accommodative financial conditions. So far,

9

strains in the household sectors have been

7

mitigated by significant government support and

5

relief programs as well as by declines in interest

rates, which have reduced the debt service load.

But poorer and marginalized households have been

Sources: Bloomberg Finance L.P.; and IMF staff calculations.

Note: 2022 consensus EPS forecasts are used for the market-implied

substantially more affected than others. This

cost of equity, with consensus expectations used for ROE.

4 International Monetary Fund | January 2021GLOBAL FINANCIAL STABILITY UPDATE, JANUARY 2021

Figure 10. Bank Lending Standards, Nonfinancial Firms suggests that vulnerabilities are unevenly

(Standard deviations from mean; higher is tighter; Q3 2020)

4

distributed among some households, and financial

stress may rise if policy support is withdrawn too

3

early or there is an incomplete economic recovery.

2

Banks have not been part of the problem so far.

1 Banks entered the pandemic with a large amount of

capital and high liquidity buffers and have shown

0

resilience so far, and unprecedented policy support

-1 has helped maintain the flow of credit to

households and firms. However, profitability

-2

POL PHL ESP USA CZE EA DEU CAN GBR JPN HUN KOR THA ITA TUR challenges in the low-interest rate environment call

Sources: CEIC; Haver Analytics; and IMF staff calculations. into question banks’ ability or willingness to

Figure 11. Bank Loan Growth

(Percent)

continue to lend in coming quarters. Banks may be

10 10

concerned about rising credit exposures and

Corporate Household

increasing nonperforming loans once policy

Loan growth 2020:Q3 (quarter on quarter)

8 8

6 6 support measures end, especially where the

4 4 recovery may be delayed or incomplete. Banks may

2 2

also face challenges in generating returns above the

0 0

cost of equity amid continued compression of net

-2 -2

-4 -4

interest margins, a development long evident in

-6 AE -6 Japan and Europe (Figure 9). Underwriting

-8

EM

-8 standards for nonfinancial firms have tightened in

-5 0 5 10 15 20 -5 0 5 10 15 20

Loan growth in 2020:H1 from 2019:Q4

some instances (Figure 10) and bank loan growth in

Sources: Haver Analytics; and IMF staff calculations.

many countries has remained low or slowed in

Note: AE = advanced economy; EM = emerging market. recent months (Figure 11).

Figure 12. Flows into Global Investment Funds

(Billions of US dollars, cumulative since March 2020) Inflows to investment funds have resumed on

Money market Fixed income the back of improving market sentiment. The

1,200

imperative to put cash to work in a buoyant market

1,000

environment have driven investors to reach for

800

yield. Between March and November 2020, fixed

600

income funds registered cumulative inflows of

400

200

about $280 billion, $230 billion of which poured in

0

since the beginning of September (Figure 12).

-200 However, vulnerabilities in investment funds

-400 continue to be a concern: stretched asset valuations

-600 expose investment funds to the risk of a price

correction, and liquidity and maturity mismatches

remain largely unaddressed.2

Source: Morningstar.

2 See Chapter 1 of the October 2020 Global Financial Stability Report and the FSB holistic review.

International Monetary Fund | January 2021 5GLOBAL FINANCIAL STABILITY UPDATE, JANUARY 2021

Figure 13. Global Sustainable Debt Issuance Capital markets are gaining importance as a

(Billions of US dollars)

source of funding to combat climate change

700

Green bond and achieve social goals, and they can play a

600 Green loan

crucial role in greening the recovery. Greater

Social bond

500

Sustainability bond awareness of the need for social spending, likely

400 Sustainability-linked bond

related to efforts to fight the pandemic, led to a

Sustainability-linked loan

300 very large increase in social bond issuance in 2020.

200 Debtors have tapped into sustainable finance

100

sources, with sustainable debt issuance in 2020 set

to surpass the 2019 record at more than

0

2010 11 12 13 14 15 16 17 18 19 20 $650 billion (Figure 13).

Sources: BloombergNEF; and IMF staff calculations.

Note: 2020 is partial data as of November 30. Once More Unto the Breach

Figure 14. Market-Implied Probability of Inflation

Outcomes

Ongoing policy support remains necessary

(Percent, over five years) until a sustainable recovery takes hold to

100%

Less than 1% Between 1% and 2% Greater than 2% prevent the pandemic crisis from posing a

threat to the global financial system. The global

80%

community should strive for multilateral

60%

cooperation in equitable vaccine development and

40% delivery across the world to ensure an even and

20%

complete economic recovery. Policymakers should

safeguard the progress made so far and build on

0%

Jan. 2020 Oct. 20 Latest Jan. 2020 Oct. 20 Latest the rollout of vaccines to return to sustainable

United States European Union

growth. A bridge to the point where vaccines are

Sources: Bloomberg L.P.; and IMF staff calculations. widely available requires preserving monetary

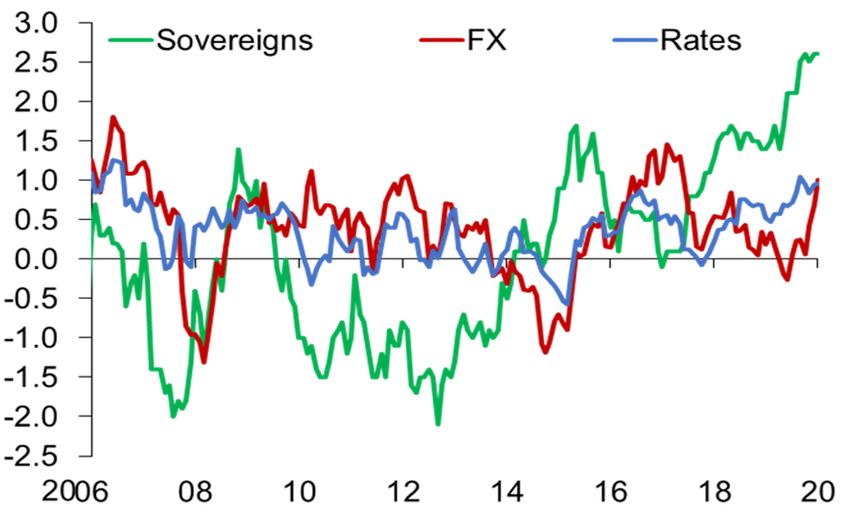

Figure 15. Investor Positioning in Emerging Market policy accommodation, ensuring liquidity support

Assets to households and firms, and keeping financial

(Reported investment position in excess of average in units of

standard deviation) risks at bay.3 Underdelivering on policy action risks

jeopardizing the recovery, and the IMF and other

multilateral institutions stand ready to provider

further support should further downside risks

materialize.

However, policymakers should also be

cognizant of the risks of a market correction

should investors suddenly reassess growth

prospects or the policy outlook. With the

recovery still nascent, and inflation still expected to

Source: J.P. Morgan emerging markets client survey as of December

10, 2020. Note: FX = foreign exchange. be subdued, monetary policy is anticipated to

remain accommodative for years to come

3 See the October 2020 Global Financial Stability Report for a discussion of monetary, fiscal, and financial policies to support the recovery and the policy

priorities once the pandemic is under control.

6 International Monetary Fund | January 2021GLOBAL FINANCIAL STABILITY UPDATE, JANUARY 2021

Figure 16. Financial Conditions Indices (Figure 14). Asset valuations appear to be stretched

(Standard deviations from mean)

in several markets. A sense of complacency

Interest rates House prices Corporate valuations

EM external costs Index

Other

permeating financial markets as investors seem to

United Euro Other

2.5 China

States area advanced emerging bet on a persistent policy backstop and uniform

2.0 market views raise the risk of a price correction

1.5 (Figure 15). A sudden sharp tightening of financial

1.0 conditions from current very low levels—for

0.5

example, as a result of a persistent increase in long-

term interest rates—could be particularly

0.0

pernicious should such tightening interact with

-0.5

financial vulnerabilities (Figure 16).

-1.0

Financial stability risks are in check so far, but

Jun

Jun

Jun

Jun

Jun

Dec

Mar

Dec

Dec

Mar

Dec

Dec

Mar

Dec

Dec

Mar

Dec

Dec

Mar

Dec

Sep

Sep

Sep

Sep

Source: IMF staff calculations. Sep action is needed to address financial

Note: Higher indicates tighter financial conditions. EM = emerging vulnerabilities exposed by the crisis.

market. Series begins December 2019 and ends December 2020.

Policymakers face an intertemporal policy trade-off

between continuing to support the recovery until

Note for all charts where applicable: Data labels use International

Organization for Standardization (ISO) country codes. sustainable growth takes hold and addressing

financial vulnerabilities that were evident before the

pandemic or have emerged since it began. These

include rising corporate debt, fragilities in the

nonbank financial institutions sector, increasing

sovereign debt, market access challenges for some

developing economies, and declining profitability in

some banking systems. Employing macroprudential

policies to tackle these vulnerabilities is crucial to

avoid putting growth at risk in the medium term.

International Monetary Fund | January 2021 7You can also read