August 2017 Month in Review - Herron Todd White

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

August 2017 Month in Review

Contents Feature – Investor interest 3 Commercial - Industrial 4 Residential 18 Rural 48 Market Indicators 56

Month in Review

August 2017

Investor interest

They’re an interesting lot, those property investors.

Your perception of a landlord might be old school - a There’s been a rise in the profile of another type Most important of all, our specialists have an opinion

rotund, cigar-smoking gent sitting atop a mound of of investor over the past decade – the non-local. on what might happen in their markets if demand

money that’s weighing down a horde of unfortunate The internet age has made it ever easier to do a from this influential mob were to slow – and in many

tenants, while he laughs maniacally at those whole mess of research without having to leave patches this may be the case. Given a tightening on

unfortunate souls unable to own their own home. your reclining easy chair. We are a big country with finance for these types of owners, it’s a reality that

a plethora of property options and buyers are no we may see less activity from this demographic in the

But dig into the numbers and you’ll find only

longer bound by state lines. future.

approximately 8% of the population invests in real

estate outside of their own home. Of that number, To take the example further afield, how about In the commercial realm, this month’s special subject

almost three quarters own just one investment. That overseas investors? Here’s an investor type who’s is industrial and it’s time to talk about rentals.

means less than 2% of the Australian population been firmly targeted in recent political dealings, and Let’s dig deep into how rents are tracking. We’re

owns more than one investment property. changes to legislation may see their interest shift in going to have our experts cover the full gamut of

the near future. the industrial rental ranges. Here, we outline what

Here’s another thought - investors come in all

various locations and standard of property are

shapes and sizes from blue-collar workers, to middle Whatever your opinion, investors are as diverse as

achieving in the rental sphere. There might even be a

class mums and dads, to young professionals of all the property options our country offers – and their

few projections on where rents are headed and how

persuasions. There’s no hard and fast rule about impact on our various markets, localities, property

you can get ready for the moves.

what an investor should look like. types and sectors can’t be ignored.

So, there you have it – a deep dive into the residential

Experience has taught us this too – most investors The fascinating thing is, what’s good for one spot,

investors psyche and how their moves might affect

aren’t in the market to try and lock everyone else isn’t necessarily a winner for another, so you need a

your local market, plus a look on industrial rentals

out of home ownership. Most are, admittedly, trying local’s view to get the real story.

and what the future holds.

to get ahead, but many would be happy to have

This month, we hone in on property investors and

just enough equity come retirement so they aren’t Please devour the wisdom within these pages but

their effect on our markets – at a nuanced level.

Feature

relying on the public purse to see them out. And don’t forget it’s most important you make time

We’ve asked our team to talk about their investor

while compulsory superannuation will help alleviate to give our team a tingle. They stand at the ready

sector. Our professionals discuss how investors tick,

our dependence on a government, most of us would to provide the right advice and ensure you aren’t

what they’re buying, what they’re selling and where

prefer to be sitting towards the pointy end of the caught out when the time comes to put your money

they’re heading next.

plane in our post-employment years. where your mouth is.

3

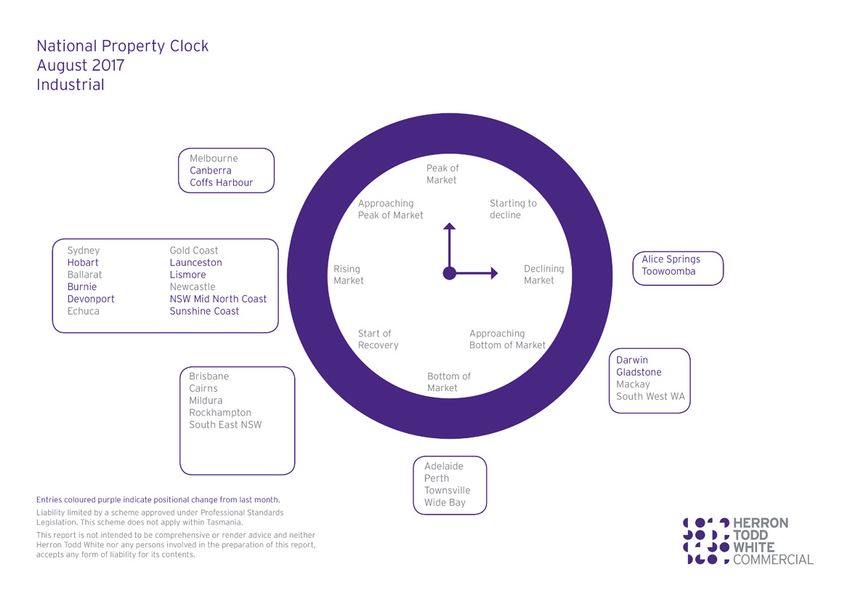

Commercial

Month in Review

August 2017

New South Wales

Overview $130 per square metre. Leases at this level of the Canberra

Rent levels are the bedrock which determine market are negotiated on a net basis, with tenants Canberra’s industrial market is concentrated in three

the success or failure of industrial investment, responsible for outgoing costs. We are noticing that main localities: Mitchell in the north; Hume in the

and having a handle on how they’re tracking is incentives have diminished with many large scale south; and Fyshwick centrally located near Canberra

imperative. operators happy to commit to long term leases of five airport. The Fyshwick market remains the most

to ten years plus options with minimal abatements popular of the three industrial areas in Canberra

This month, our team deep dive into industrial

depending on the location and improvement quality. providing a mix of small, medium and large industrial

rentals, dissecting the good from the bad and

and bulky goods use space, but activity in Mitchell

analysing movements so you can stay ahead of the In the sub 1,500 square metre bracket we note

continues to increase on the back of population

pack. rentals have also strengthened. At this level of the

growth in the Gungahlin district.

market, leases are generally negotiated on a gross

Sydney

basis with only a few agreements passing on the The ACT Government’s Four Year Indicative

Industrial markets have continued to show signs

costs of outgoings. This sector rarely features rentals Industrial Land Release Program is based on the

of strong growth across the whole of the Sydney

below $100 per square metre in metropolitan Sydney, current level of demand for industrial land. The

metropolitan area. Generally speaking, the

with the exception being low quality low clearance program is intended to achieve a number of

performance of the industrial market in Sydney’s

warehouses in less desirable locations. We have seen objectives, but in essence it is to increase the ACT

inner ring and particularly southern Sydney stems

the most uplift in this sector due to the affordability Government’s responsiveness to market changes

from an aggressive reduction in available stock

of most of these assets, typically at the sub by developing an inventory of land stock, where

due to the rezoning of land and conversion of

$500,000 price point. Given the population growth serviced industrial sites are available for immediate

existing stock, whilst the outer suburbs of Sydney

particularly in the north and south-west of Sydney, release. Land will be available in Hume and across

are benefiting from an unprecedented level of

many of the fringe industrial locales have seen a three new estates in Symonston (2016-17) 30,000

infrastructure investment and the on flow of owner

spike in demand from a sale and leasing perspective square metres, Fyshwick (2017-18), Hume and

occupiers and investors being priced out of industrial

as many of the existing occupiers have been pushed Symonston 55,000 square metres and Majura Valley,

precincts within close proximity of the Sydney CBD.

out of the main centres to make way for residential Hume, Symonston and Pialligo (2018-19) 42,000

Numerous local agents have reported a shortage of

redevelopment. square metres. A further 39,000 square metres will

Commercial

quality, well positioned industrial holdings.

be released in 2019-20. The program aims to release

Overall, the rental market is expected to continue to

Within the small to medium size bracket we note 166,000 square metres over the next four years.

grow due to a lack of supply together with a relatively

rentals appear to be very consistent, ranging from

healthy industrial outlook over the coming months. The land release of industrial sites has seen new

$100 to $120 per square metre per annum net

developments attract tenants from older established

plus GST and some of late have even hit as high as

sections of Fyshwick to new industrial sub division

6Month in Review

August 2017

locations. Currently rents for small units in Fyshwick Local agents report that tenant enquiry is at low have a broad range from $80 to $110 per square

range from $125 to $200 per square metre. Larger levels and those who can afford to purchase a metre gross.

premises over 1,000 square metres are letting for property are taking advantage of low interest rates

Most of the activity in the industrial market is being

$130 per square metre. and acquiring properties for long term investment.

driven by the Port of Port Kembla with logistics a

Hume rents are achieving rates of around $100 South East NSW rapidly developing sector particularly in new vehicle

per square metre for units averaging 200 to 300 The industrial property market has shown clear transportation. The tight supply and rising values

square metres and $120 per square metre for larger signs of improvement over the past two years with a and rents of industrial property in the Sydney

buildings of 1,000 square metres plus. slight increase in leasing transactions, demonstrating market is also impacting the local market, likewise

improved confidence after a prolonged period of the significant infrastructure investment in the

Mitchell properties are achieving rates of $220 per

static conditions post the GFC. south-west Sydney growth corridor most notably the

square metre for units between 100 and 300 square

proposed second airport at Badgerys Creek.

metres and $130 per square metre for over 1,000 In general, industrial rents are stable however local

square metres. agents are reporting a notable increase in enquiry Newcastle

levels, particularly for small to mid-sized efficient Location is a big factor in industrial rental growth

Industrial sales have been well located warehouse tenancies. Demand for larger around the Hunter Valley and Central Coast at

warehouse space is also increasing. Demand for older present. While we’re seeing some increase in coal

improving and are dominating the style large inefficient heavy industrial space remains mining services activity, this sector has been weak

market compared to rentals. relatively soft given the struggling manufacturing for around five years now and areas heavily reliant

and mining sectors. on mining sector activity such as Singleton and

Tenants incentives have consisted of rent free terms

Rutherford are still seeing downward pressure on

and contributions to fit out in order to move to newer Local agents are however finding that some tenants

rents across the board. Given the rental supply

locations with long term leases. (usually established businesses) prefer to purchase

and demand mismatch, rents are not expected to

rather than lease with low interest rates making

Tenant demand is low at present with tenants opting increase in the short term in these locations.

owner occupation more attractive. This is putting a

to purchase sites rather than rent due to low interest

cap on leasing activity. Mayfield West on the other hand is under stocked

Commercial

rates and good economic growth. Rents are stable

with industrial property. Local industrial leasing

and should remain so for the short term. Predicted Prime industrial rents typically range from $120 to

agents are reporting increased enquiry in this

increases in interest rates will impact the market in $150 per square metre gross. Low site coverage

locality. This is on the back of the significant

the long term and we would anticipate some rental properties with good usable handstand components

construction boom in the CBD, Mayfield West being

growth when the momentum swings back to tenant can achieve in the circa $170 to $200 per square

the closest established industrial estate to the CBD.

demand increasing and out performing sales. metre range. Second tier industrial rents tend to

7Month in Review

August 2017

Other major Hunter Valley industrial estates such as As for the remainder of the North Coast, Ballina has Incentives are common in the market with rent free

Beresfield and Thornton are indicating steady, albeit seen a slight increase in rents in industrial estates periods of one to two months, often written into

slow rental growth patterns. While stock listed for and decreased vacancies. The industrial markets in leases. Bulky Goods accommodation remains price

sale is scarce within the Beresfield estate at present, Casino, Alstonville and Goonellabah remain steady. sensitive with rental levels circa $140 to $180 per

the number of warehouses listed for lease is growing The South Lismore industrial estate has recently square metre, depending on size. We are aware of

in this ever increasing owner-occupied market sector. been affected by a major flood. There has been a 2016 leasing of circa 1,500 square metres which

anecdotal evidence that some industrial business included a 12 month rent free period over a ten year

Lismore

have packed up and moved up the hill to higher lease.

The Byron Bay industrial market has seen quite a

ground, however the majority have remained. It will

bit of action in the past six months. There has been

be some time before we can determine the effect the

high demand for industrial strata product with a lack

flood has had on the industrial market.

of available stock (both to purchase and lease). This

has resulted in increased values and premiums being Coffs Harbour

paid to secure a property. The demand is from both The rental market for smaller industrial sheds is

investors and owner-occupiers alike. The rental rates variable, demonstrating some market uncertainty,

have seen a sharp increase also for the 100 to 150 with a lower volume of recent lettings. Rental

square metre size industrial strata unit in the past six evidence displays a wide variance from $90 per

months from $150 to $180 per square metre to $230 square metre to $130 per square metre for modern

to $260 per square metre. tilt up small bays of 200 to 300 square metres in size

in prime locations.

The recent growth in industrial strata titled unit

product is, advised by some agents, due to reports The industrial rental market still remains price

Byron Shire Council have relaxed their regulations sensitive with a broad range of rents being achieved,

on illegal residential occupation of industrial units. which confirms the uncertainty in the market. There

Traditionally this has always been an affordable form remains a slight oversupply of smaller industrial

Commercial

of residential accommodation within Byron Bay, bays in the lower price bracket and valuations of

with people permanently occupying industrial strata poorly leased property will invariably be lower than

units on a residential basis (albeit illegal). Part of the those with vacant possession for this owner-occupier

industrial estate is zoned B7 Business Park, which dominated market.

permits residential occupation in conjunction with

business use.

8Month in Review

August 2017

Victoria

Melbourne Incentives mostly take the form of rent free months development occurring, especially in the south,

The Melbourne industrial market performed strongly at the beginning of the lease. Standard length leases south-east and west.

in the first half of 2017. With interest rates remaining (three to five years) generally receive one to three

Echuca

low and a relatively stable economy, new industrial months rent free, which usually covers the setting

Industrial rents have been relatively static for

developments are continuing to come onto the up period of the property, whilst longer leases (five

some time, with the market generally capped at

market, especially in growth corridors where there is plus years) are seeing three to five months rent free.

the cost of construction for owner builders in the

an abundance of vacant land prime for development, This usually ends up being about 25% to 35% of the

amortized over the life of the asset in conjunction

including suburbs such as Clyde, Pakenham and commencing rental amount.

with owner-occupiers looking to take advantage of

Dandenong South in the south-east, Carrum Downs

In the south-east, in a well-regarded industrial area self managed super funds. Consequently there have

in the south, Truganina and Derrimut in the west and

such as Dandenong South, a 2,500 square metre, been limited gains in industry locally and this has also

Epping in the north.

modern office/warehouse could expect to reach been exacerbated in some regards by challenging

Industrial rents have remained relatively stable over between $70 and $90 per square metre per annum manufacturing conditions. Consequently there have

the past 12 months with the exception of the northern net plus GST, with larger properties expecting been limited gains in industry locally and this has also

industrial market, which includes Campbellfield, less and smaller properties expecting more. Older been exacerbated in some regards by challenging

Coolaroo, Somerton and Broadmeadows. This area properties and ones in inferior locales would reach manufacturing conditions.

has felt the impact of losing the Ford Motor Company between $50 and $70 per square metre per annum.

manufacturing plant in Campbellfield last October.

In the outer east in Kilsyth, we’re seeing rates of $70

to $80 per square metre per annum net plus GST

Incentives are not as prevalent for good quality large industrial properties (2,000

in the industrial sector as they square metres plus), with brand new warehouses

smaller than 500 square metres reaching up to $130

may be in other markets, however per square metre per annum net plus GST.

Commercial

are becoming more common, We expect tenant demand to remain relatively strong

especially within new industrial over the coming 12 months, however remain cautious

of oversupply given the large amount of industrial

estates.

9Month in Review

August 2017

South Australia

Adelaide When the subdued rental demand is coupled with project, comprising 12 submarines at a spend of circa

The industrial rental market is generally subdued weak investor sentiment and a low interest rate $50 billion. These projects are expected to provide

as the South Australian economy faces continued environment, it is not surprising that those left active over 2,000 jobs.

challenges. in the market are equally attracted to buy as oppose

In addition, the South Australian Government

to rent.

The market in the outer north, specifically the areas has significantly increased its expenditure on

surrounding Elizabeth South have experienced The rental market for industrial property has infrastructural projects. In 2015 to 2016 the budget

weak demand over the past 18 months due to the previously been more simplistic than other markets was $1.8 billion which has increased to $2.2 billion by

closure of Holden’s production plant and the loss of such as office space or retail where face rents and 2017 to 2018.

approximately 1,250 on-site jobs. effective rents can vary significantly. The increasing

The projects are:

use of incentives has seen the industrial market

As the 2017 departure of Holden approaches,

become more complex and less predictable. • Darlington Upgrade

there are noticeable vacancies arising throughout

• Anzac Highway to Darlington

industrial northern areas and properties are Also, the increase in outgoings has placed additional

• River Torrens to Anzac Highway

experiencing extended marketing periods given the downward pressure on net rents. It was recently

• Regency Park to Torrens Road

uncertainty surrounding the local industrial market. revealed that Adelaide has the highest power

• South Road Expressway

prices in the world, which has a particular impact

Unfortunately, GM Holden’s departure is only • Northern Connector

on industrial businesses. Although the recent

part of the bigger picture but has typified the

announcement of a raft of spending by the South The combined effect of the Defence contracts and

contraction of manufacturing in South Australia. This

Australian Government, including a 100MW battery the infrastructure expenditure is going someway to

contraction has led to an oversupply of industrial

in Jamestown, may soften the consumer electricity soften the blow, however the fall-out to the South

space throughout the market and placed downward

costs. Australian economy has been harsh.

pressure on rents.

A positive has been the securing of Defence

There is now an evident difference between renewals

construction contracts. After the completion of the

and new leases with incentives becoming more

Air Warfare Destroyer (AWD) construction contract,

Commercial

common, as has the need to reconfigure larger

the Future Frigates programme will commence in

spaces for multiple occupants.

2020 with an estimated spend of circa $35 billion.

Following this in 2022 is the Future Submarine

10Month in Review

August 2017

Queensland

Brisbane Demand in locations such as Acacia Ridge, Brendale, averages over the course of the next few years.

The Brisbane industrial market has been generally Northgate, Salisbury and Sumner is presently being

Elsewhere, suburbs such as Caboolture, Banyo,

buoyant throughout the first half of 2017 with leasing driven by owner-occupiers and we have seen capital

Hendra and Northgate are experiencing relatively

and sales activity levels within the TradeCoast values increasing within these established precincts

low levels of vacancy, with prime grade buildings and

continuing to outstrip other industrial corridors. for quality assets.

properties with exposure to motorways or arterials in

There have been record land value rates set in this

In regard to the rental market, the flight to quality high demand.

precinct over the past six months with limited supply

continues to support prime grade rents, particularly

and pent up demand driving land value rates to More broadly, many agents are reporting weak

for those locations within close proximity of major

exceed $600 per square metre of site area in some rental market conditions for buildings with 2,000

transport routes and Brisbane’s ports. With the

instances, particularly in Eagle Farm. Whilst industrial to 5,000 square metres of GLA. There has been

exception of the TradeCoast and pockets of industrial

developments remain unfeasible for the majority anecdotal evidence emerging of declining face rents

properties on the north and south sides, rental rates

of projects (due primarily to high underlying land for secondary buildings of this size and an upward

have remained stagnant throughout the greater

values, rental stagnation and rising construction trajectory in incentives - around 10% plus over the

Brisbane region. This is largely a function of weak

costs), the land market is instead being driven by initial term of a lease is becoming more and more

performance across a number of key economic

owner-occupiers seeking to purchase sites in prime common.

indicators such as inflation and growth in wages

locations with the intention of constructing purpose

and GDP. There has been some uplift in activity

built facilities for their own business purposes.

led mostly by large scale tenants (7,000 to 10,000

Looking forward, future rental

The TradeCoast has been the most sought after square metres) who took advantage of higher movement will depend on

precinct historically given its proximity to ports and incentives particularly in the northern and southern

the CBD, and is set to remain this way with several precincts as developers aimed to secure pre-

economic conditions, business

major infrastructure projects, including the doubling commitments for their developments. confidence and the future supply

of the Brisbane airport runway and the upgrade of

Kingsford Smith Drive ensuring continued growth in

In the case of Seventeen Mile Rocks, rents were of both vacant land and built

undermined 18 months ago by an unusually large

the area over the medium to long term. product.

Commercial

supply of new stock (Metrowest) coming onto the

Within the sub $5 million price range, modern stock market simultaneously in circa 2015/16. This caused Finally, leaseback agreements where the vendor sells

with strong leasing covenants continues to receive net face rents to fall $20 to $40 per square metre the property with a three to ten year commitment in

strong interest from private investors and syndicates. and from discussions with local agents, this supply place to lease the premises back from the purchaser

We have seen sub 7% yields achieved on these has finally been taken up by the market and we are common in the current market. This is primarily

transactions, however these have been in isolation. should expect to see rents return to their historical the result of businesses seeking to free up capital

11Month in Review

August 2017

or rebalance the books. The current search for yield industry. The number of vacancies has increased owner-occupiers driven by the low interest rate

amongst investors is encouraging yield compression over the past twelve months which could result in borrowings and the flat cash rate. The trend of

across the industrial landscape during a period of the tightening of rentals or the introduction of lease renters turning into owner-occupiers is mainly

sustained low interest rates. This, together with a incentives. happening in the traditional industrial precincts in

weak rental market, is making these agreements the central and southern regions which are mostly

Industrial rental rates in Toowoomba can vary from

an attractive proposition for owners of prime grade composed of small to medium sized properties that

$75 to $140 per square metre gross for warehouses

stock as a strong return on investment can be were developed to cater for the demands of local

and $120 to $200 per square metre gross for the

achieved through the sale, while simultaneously companies. The larger factories are concentrated in

office components. These rates will vary depending

locking in an affordable rent for the medium to long the Yatala Enterprise Area (YEA) in northern Gold

on factors such as size, quality of building and

term. Coast which encompasses the suburbs of Ormeau,

inclusion of overhead gantry cranes.

Yatala and Stapylton. Not surprisingly, the leasing

The inclusion of additional hardstand yard area could market is more active in the north than in the south.

South East Queensland also affect a property’s achievable rental. A standard Amongst the national companies that have set up

Property Overview Breakfast industrial property in Toowoomba will generally roots in the YEA in recent years are Caterpillar, O-I

have a site coverage of 25% to 30% with premiums Glass, Jeld-Wen and Markwell Cold Storage whilst

Register your interest here often achieved if the site coverage falls below this Aldi, Visy Industries, Harvey Norman, Stratco and

Guest speaker Mr Alan Kohler rate. Rentals of between $8 and $20 can be achieved Beulieu Carpets have stayed as prominent owners

Thursday 16 November 2017 for hardstand yards with the variances due to size, and renters.

location and type of hardstand (gravel, bitumen,

Market rents for large format industrial factories

Tickets on sale soon concrete etc).

and warehouses have stagnated despite the growing

For further information, contact Catherine Wilson

The other major factor that will affect rental rates is number of national companies setting up their

catherine.wilson@htw.com.au or 07 3353 7500

location. The western suburbs of Wilsonton, Glenvale branches in this region. As far back as 2010, active

and Torrington have always been considered more leasing agents for the area have been marketing

popular industrial precincts with suburbs such as vacant industrial space at the rental rate of $100 to

Commercial

Toowoomba

North Toowoomba, Rockville, Harlaxton and Drayton $110 per square metre per annum plus outgoings and

Industrial rentals in Toowoomba have been relatively

generally considered secondary locations. the current going rates are still the same. However

static with only modest increases over the past

the outgoings such as council rates, land tax and

two to three years. Leasing demand however has Gold Coast

cost of repairs and maintenance have been rising.

declined recently which coincides with the decrease The main thrust of the Gold Coast industrial

This has resulted in gross rental rates appearing

in activity within the Surat Basin coal seam gas market in the past few years has come from

12Month in Review

August 2017

to increase to the level of $130 to $160 per square sporadic and rental growth has been rather slow, Sunshine Coast

metre per annum. Due to keen competition, there if not stagnant. For this reason, it is still a common Over the past six to 12 months we have seen rental

have been some properties, particularly those more sight to see roadside for lease signboards in the rates continue to firm in the industrial market in

than 3,000 square metres in lettable area, being industrial estates. established estates across the Sunshine Coast.

leased at gross rates at this level, thus the actual net Vacancy levels, particularly for sub 300 square

There are however, pockets where some evidence

rates would be in the order of $90 to $100 per square metre spaces in areas such as Kunda Park, Warana

of rental increase has been seen due to diminished

metre per annum. Of course, the older sheds of and Caloundra West are limited, which has led to an

supply of serviced industrial sites coupled with a

sheet metal cladding would only command net rates increase in rental levels for these locations. Typically,

rise in land values and cost of construction. These

of $70 to $80 per square metre per annum. The rentals for these types of property range from $120

pockets are in Arundel, Southport, Helensvale,

general gross rates for small industrial units in this to $180 per square metre gross.

Coomera and certain parts of Burleigh Heads where

region have also levelled at $120 to $140 per square

rental rates at $140 to $180 per square metre per Within secondary industrial locations we have

metre per annum.

annum gross are common. However, these rates seen a reduction in vacancy levels which has led

Further to the north of the YEA, the less significant appear to apply to modern units and freestanding to some rental growth, however it’s still common

established industrial estates of Beenleigh, Bethania industrial buildings whilst older style premises still for incentives to be offered to attract prospective

and Logan Village at the fringe of Brisbane’s south prevalent today appear to be less affected, with the tenants, which has led to some inconstancy with

are experiencing very low leasing demand and general level mostly falling at the old rates of $120 rental levels. A summary of the rental levels for the

consequently, rental rates are staying at a low level. to $160 per square metre. With outgoings currently sub 300 square metre market is as follows:

There are hardly any large format industrial factories falling between $30 and $50 per square metre of

available for lease due to a lack of demand and even lettable floor area, the net rates have remained at Location Rental Range (per sqm gross)

small industrial units are only achieving rental levels around $90 to $110 per square metre.

Kunda Park $120 to $145

of $70 to $110 per square metre per annum gross.

There are early talks of an imminent interest rate

Warana $130 to $160

The same owner-occupier dominated market rise, the only uncertainty being when. Any rise in the

scenario is occurring in the central and southern lending rates could be a game changer. Landlords Caloundra West $130 to $180

Commercial

industrial regions, although the market levels are at would be looking to pass on any increase in cost to

Bells Creek $120 to $140

higher levels of $110 to $150 per square metre per tenants, however, is the market demand capable of

annum gross. Due to a limited supply of industrial absorbing the increase? Property is a very inelastic Coolum Beach $100 to $130

sites, there has been very few new stock added to commodity and it will take many months for the

Noosaville $130 to $180

the market, which translates into limited new stock market to adjust to any change in the cash rate and

available for lease. However due to a preference to any projections of rental increase or yield increase in

own rather than to lease, leasing demand has been the short term would be rather presumptuous at this

time.

13Month in Review

August 2017

These primary industrial areas still note vacancy Incentives are common as part of these negotiations, achievable rental rate seems to be the local versus

in the 300 square metre to 1,500 square metre generally taking the form of rent free periods or national tenancies with national tenants tending to be

sector, though have also begun to drop over the contributions to tenant fit out. able to afford slightly higher rates per square metre.

past 12 months, which has led to some rental growth We are aware of four recent leases of large industrial

There has been some activity on the industrial sales

dependant on specific property attributes. We note properties in Parkhurst of between 1,685 and 2,300

front in the past 12 months, with two significant sales

that rental rates for good quality larger industrial square metres, which have been leased at between

to local owner-occupiers, both at $1.9 million. These

properties vary from $110 to $140 per square metre $90 and $138 per square metre gross. We consider

are large industrial complexes both in Callemondah

gross for warehouse, $140 to $180 per square metre these rentals provide the best recent evidence of

Drive. There is also the notable sale of the RCR

gross for office components and $15 to $35 per market rentals for large industrial premises.

Tomlinson workshop in Ganley Street that sold for

square metre for hardstand components.

$6.2 million, reflecting an analysed market yield of There appears to be an increasing tendency for

Gladstone about 9.75%. There was close to ten years remaining shorter lease terms, with potential uncertainty for

The industrial rental market in Gladstone has on the lease term. the medium term direction of rental rates. Owner-

continued at a relatively slow pace with limited occupiers continue to remain active in the market,

Rockhampton

activity. New rental negotiations in the past 12 to 24 with most activity in the $750,000 to $1.5 million

The Rockhampton market benefits from a fairly

months have shown reductions in excess of 50% price bracket.

diverse economy which has somewhat cushioned

from peak market conditions. It appears that these

the impact that the downturn in the resources A 1,122 square metre warehouse recently sold

rentals however have perhaps started to flatten

sector has had on the industrial lease market. in Alexandra Street for $1.3 million to an owner-

out with no notable further reductions in recent

There has however been a slight softening of the occupier, reflecting $1,159 per square metre of

months. Rental evidence shows rentals generally

industrial market in Rockhampton in the past 12 to 18 lettable area. We anticipate that owner-occupier

falling between $90 and $150 per square metre

months (mostly for larger industrial premises) and activity will continue in the medium term as a result

gross, depending on a variety of factors, particularly

the current supply of leased industrial properties of low interest rates and current market conditions.

condition and nature of improvements, site coverage

exceeds demand.

and crane availability. In terms of rental variance Mackay

and location, higher rentals are generally achieved Rates per square metre for industrial leases tend to The industrial rental market in Mackay has

Commercial

in the industrial precincts around Callemondah. fall within the $100 to $140 per square metre range, experienced a significant downward correction in

Lower rentals and generally higher vacancies exist but it is not uncommon for rentals to be negotiated rental levels as a result of the coal mining downturn.

in secondary industrial locations around South Trees outside of this range. Properties at the upper end of Based on a fairly limited number of reported new

and the South Gladstone area. Given the high level this range are generally located within established leases, we believe that rents are down by 30% to

of supply relative to demand, tenants continue to industrial precincts and provide quality workshop 40% from the peak in 2011/12. The market features

have bargaining power in new lease negotiations. and office areas. Another contributing factor in the high levels of vacancy and weak levels of demand.

14Month in Review

August 2017

In some cases, new lease rentals are subject to $1 million range and largely catering to intending Cairns

confidentiality clauses and cannot be reported. This owner-occupiers. There are occasional high The industrial sector in Cairns is relatively small with

is a new characteristic which has probably occurred end syndication or trust purchases, but only for areas close to the CBD showing stronger demand.

to suppress the full extent of the market correction properties with strong lease profiles. Though we now perceive the industrial market to

and to protect the market from a more severe be entering a recovery phase, industrial property

Industrial rents have been on a declining trend and

outcome. development remains slow.

appear to have reached a level that is being accepted

Rental rates are yet to consolidate at new lower by the market. As a result of softening rents, Prices per square metre for established strata titled

levels and new rentals have been negotiated within a incentives also appear to have settled to reflect rent industrial units have been steady at around the

fairly broad and inconsistent range. A recent example free periods of around three months. $1,250 to $1,500 mark for some time. Commercial

is a modern warehouse at Caterpillar Drive, Paget of agents advise limited availability of good quality

Broadly speaking, a large portion of mainstream

over 1,000 square metres in lettable area which was stand alone warehouse stock with slow to reasonable

industrial property falls within the $90 to $110 per

leased at $81 per square metre per annum net which demand for this type of premises. Strata titled

square metre rental range. Within the lower end of

is considered reflective of the market. industrial warehouses are also limited in numbers to

this range is typically smaller older light industrial

both sell and lease with similar limited demand.

Rental incentives in the form of rent free periods or properties in Garbutt with small office components.

lower rent in the first lease year were fairly common Larger better quality mainstream industrial Industrial property rents range from $100 to $150

throughout 2016. This has not been as common in properties in Garbutt and Bohle generally fall within per square metre per annum gross depending on

2017. the mid to higher end range depending on the office size, location and quality. A lack of new stock should

size component and hardstand areas. Industrial see availability tighten as we move through 2017.

The market has been most active at total annual

property exhibiting large office components and

rental ranges of $30,000 to $65,000 per annum There is good investor demand for leased industrial

extensive hardstand areas can reflect rents up to

net. The highest recent rental was struck at properties across all price ranges of the market,

above $140 per square metre.

approximately $210,000 per annum net in August from small stratas through to large showrooms.

2016. At the peak of the market, total annual rents Overall rents are flat with the market continuing However there is very limited quality investment

for large premises exceeded this level. The market is to exhibit a balanced to oversupply of property stock available for purchase. This will tend to support

Commercial

approaching its cyclical trough. available relative to current demand. This is likely to values for well leased properties over the short

see downward pressure remain on rental rates until to medium term. The market has been gradually

Townsville

such time as the rental vacancy situation improves. consolidating over the past 12 to 18 months and the

The industrial market remains flat with current

outlook is for stable conditions as we move through

market activity being largely confined to affordable

2017. A recovery in the vacant industrial land market

properties that tick all the right boxes in the sub

in Cairns will continue to depend on more widespread

recovery in the local economy.

15Month in Review

August 2017

Northern Territory

Darwin (zoned LI or GI), compared to 79 in the corresponding

A short drive through any of Darwin’s industrial period in 2014. This is a 40% reduction in sales

areas, such as Winnellie or Berrimah, will confirm the volume which is fairly consistent with other property

prevalence of for lease and for sale signs scattered at types in the Greater Darwin area.

regular intervals across all property types.

Demand for industrial property in Darwin is closely

In such an environment, tenants have the upper linked to domestic demand for goods and services.

hand when negotiating new rentals or renewing their Therefore, until we see prolonged population growth

existing arrangements. Many of these tenants are here, it is unlikely we will see a sustained recovery in

experiencing difficult trading conditions anyway and the industrial property market

renegotiation of rents can be a matter of economic

survival, rather than just a cost cutting exercise.

Inevitably, this is leading to downward pressure on

rents and sometimes an increase in rental incentives

such as rent free periods. In the current market,

it is not unheard of for rental reductions of 20%

to be negotiated in the industrial property market,

especially for older style stock where the rent was

set close to the 2014 peak.

Sale transactions have also slowed. For this calendar

year to June, there have been a total of 47 sales of

industrial properties across Darwin and Palmerston

Commercial

16Month in Review

August 2017

Western Australia

Perth that enquiries for larger space above 10,000 square appears to be more positive. There are a number of

In these times when demand is low as a result of the metres is low, the requirements for space below quiet murmurs with regard to resource projects and

maligned resources sector, the flight to quality is 10,000 square metres has increased. the general consensus in the market is that we have

prevalent in the industrial eastern corridors of Perth reached the bottom.

Prime industrial rents at present typically range

such as Kewdale, Welshpool, Hazelmere, Forrestfield

from $70 to $100 per square metre per annum net in On average these requirements have been for

and to some extent Maddington. The dynamic shift

the north, between $70 and $100 per square metre between 7,000 and 8,000 square metre buildings

in the state’s economy as a result of the mining

per annum net in the core, between $60 and $90 on large sites, which in some cases have offered the

downturn creates a number of opportunities for

per square metre per annum net in the south and potential for expansion at a later date. It is likely this

occupiers in this core industrial circle which has

between $70 and $100 per square metre per annum trend will continue in the short to medium term.

historically been tightly held.

net in the east.

Challenges do persist for secondary and older style

Although some companies Secondary industrial rents at present are typically industrial space and heavy discounts to previously

15% to 20% below prime industrial rents. achieved rents are required to at least attract any

have been rationalising space enquiry.

Leasing enquiry is expected to remain positive

requirements, other businesses in the short term, mostly for opportunities in the

have used this as an opportunity to traditional, more established precincts, with a steady

increase in transactional activity likely as a result.

upgrade or relocate to alternative, It is anticipated that this demand will be mostly in

often larger industrial space the sub 10,000 square metre segment. Although

major pre-commitment leasing demand (greater than

that better suits their long-term 10,000 square metres) has appeared to soften in

business needs. comparison to previous years, there are a number of

active requirements in the market which may lead to

As tenants have relocated this has also created

an increase in this activity in the medium term.

Commercial

backfill opportunity in properties which have

previously been tightly held for many years. Agents In recent months there has been an increase in pre-

advise of an increase in tenant enquiry, mostly for commitment activity in the east precinct, including

core or east located properties. Whilst they do admit Jandakot airport and Maddington. The market

17Residential

Month in Review

August 2017

Overview affordability a recurring media topic, the federal Another example of an investor hot spot is the area

Investors are sometimes a hard-put-upon group, but government has introduced initiatives to help the known as Kings Cross. Kings Cross is one of Sydney’s

there’s no denying they have a huge effect on our first home buyer and limit the overall buying power highest density precincts and covers the suburbs

property markets. of the investor. Whilst it is still too early to track of Potts Point, Elizabeth Bay and Rushcutters Bay.

the success of these initiatives introduced on 1 July It is well established, being within two kilometres of

This month, our offices discuss how investors are

2017, the tightening of lending ratios and terms for the CBD, and has a train station, light commercial

operating in their markets, and what an investor

investors has been slowly occurring since early this buildings and retail spaces. Recent changes to laws

slowdown might mean in their service area.

year and our queries with both agents and brokers governing the opening hours of entertainment

Sydney are telling us that the impact is starting to take establishments in the area has allowed the precinct

It has been well documented that the Sydney market effect. Whether the restrictions will have a long term to begin to shed its reputation as a somewhat unsafe

has gone from strength to strength over the past effect on the market is currently unknown. nightlife district allowing it to become increasingly

number of years due primarily to a supply versus popular with investors. Investors targeting this

Historically investors have been attracted to areas

demand imbalance as more and more players look area in the past have been seeking the strong

that offer strong rental demand and the possibility

to enter the market and maximise strong capital rental returns offered by the many small studio and

for solid future capital growth. Traditionally these

appreciation opportunities. With record low cash 1-bedroom units. It seems to be the trend however

areas tend to be located within close commuting

rates, strong employment opportunities and a wide that many small studio units have lower levels of

distance of the CBD and around universities,

range of property types, the Sydney market has capital growth than standard 2-bedroom units for

hospitals and areas with good infrastructure and

property at a price point to suit many. example which we assume is also due to the broader

public transport options. To meet this demand, there

market appeal.

Sydney has long been a favourite for investors, has been a significant change in the town planning

whether local, interstate or overseas. Corelogic data requirements which has been driven by the state In western Sydney the new apartment market

from April 2017 indicates that 55.3% of mortgage government. Sydney is fast becoming a vertical city, continues in various degrees throughout all major

demand that month in Sydney was from investors. If with a change in buyer expectations and a surge regional zones with the Liverpool/Fairfield areas as

one in two mortgages is being driven by the investor in demand for apartment living. Modern, medium well as Parramatta and The Hills district in particular

pool, it stands to reason that this important segment to high density zones are becoming increasingly seeing substantial development. The Norwest

Residential

has had much influence on the overall position of the common with many notable precincts springing up Railway line currently under construction from Rouse

market. across the city including Green Square at Zetland, Hill to Epping has resulted in a significant increase in

Harold Park at Forest Lodge, Discovery Point at unit developments approved or under construction

Sub $1 million dollars is still a driver for the broad

Wolli Creek, Central Park in Chippendale as well as in what is typically considered the burbs, with

market and in this segment the investor is really

developing precincts in Erskineville and Camperdown unprecedented construction occurring particularly

competing against the first home buyer. With housing

(to name a few). in Kellyville. This list in western Sydney is continually

21Month in Review

August 2017

growing with a record number of unit approvals This not only adds value to their existing investment begins to plateau and banks continue to tighten

passed over recent years. What these areas have but can also increase yield substantially with a lending criteria and increase interest rates.

in common is that they all appear to have a high dual income when configured correctly. The areas

The best advice we could offer to future investors

investor contingent although the future of some that appear to have a high proportion of granny

is to do your research. Important aspects

will depend heavily on an unknown tenant pool with flats are generally the outer rings of western

include good access to services and low levels of

oversupply perhaps becoming a future issue. Sydney particularly within the LGAs of Penrith and

unemployment. Check your suburb profile, speak

Campbelltown. The comparatively lower initial entry

With Liverpool being the CBD of the south- to local rental agents about demand, check if any

point for the main dwelling, larger sized allotments

west region, it has seen a large number of new major changes are on the cards such as future large

suitable for granny flats and consistent rental

developments completed in recent years. An example scale infrastructure projects, re-zoning etc. Is it an

demand in the area make these locations popular.

of this includes the 30-level Sky Haus development area tipped for gentrification? Check the history

Currently rental yields are approximately 2.9% within

in Liverpool (420 Macquarie Street) which includes of the developer – have their other developments

greater Sydney (as per CoreLogic Housing Market

dual-key units selling on high yields of over 6% in proven to be popular with second buyers if you

and Economic Update July 2017), however our own

some cases. Investors is this area commonly seek must sell quickly? Whilst investments are generally

market knowledge indicates that dual occupancy

above average returns however it comes with limited not as emotionally driven as the purchase of an

properties (main dwelling and granny flats) in these

capital growth in comparison to superior locations individual’s home, be conscious that if you want a

outer ring suburbs have been selling at yields of

closer to Sydney or the Parramatta CBD. Many see tenant to live there, it has to be appealing especially

approximately 5% in recent times. The granny flat

it as an area of future potential however given its if the tenant pool has plenty of options. Sunlight,

trend has really gained momentum over the past five

proximity to Parramatta, the M5 and M7 motorways privacy and aspect in large scale unit developments

years with owners initially achieving higher returns

and of course the future second airport at Badgerys could be crucial to getting a long term tenant which

but due to strong capital growth for the parent parcel

Creek. A good entry point for investors in the is a benefit to maximise your overall investment

and relatively stable rentals, yields in these areas

Liverpool/Fairfield unit market can usually be found strategy. Be thorough with your research and focus

have compressed.

between $400,000 and $600,000. on a strong rental yield with a view to a longer term

While the positive cash flow provided by a strong investment as the days of annual capital growth

Another popular option for yield is always a benefit, in the past year returns from exceeding 15% are no longer expected.

Residential

capital gains have been significantly more profitable

investors in western Sydney is for investors who have the option of using the growth

Canberra

Recent changes to lending and legislation, aimed

adding a granny flat to the rear of in equity to fund an additional investment property.

at enabling first home buyers to enter the market,

In the future however, it may be wiser for investors

the allotment. to seek out strong rental returns as capital growth

has had an effect on property investors looking

to expand their portfolios. These measures were

22Month in Review

August 2017

introduced in an effort to allow first home buyers to Rental yields in detached housing have remained tenancies. The last investor type is a more prominent

be more competitive in a heated market. As a result, steady but like other capital cities, capital growth individual or group interested in cash flow and their

property investors looking for an asset with good has been very strong. An option for investors in the portfolio will comprise larger unit blocks held in one

yield and growth will have to do their research and ACT may be to purchase a vacant block through line. They can be either local, from a capital city such

be willing to go the extra mile to secure a profitable the Mr Fluffy Asbestos Removal Scheme. There as Sydney or from overseas and the price points for

investment. are several hundred blocks being introduced to the their investments are often in the $1 million to $3

market most of which are in sought after established million range.

Unlike other states, the ACT has not introduced

areas. Land banking one of these blocks and either

a scheme which cuts stamp duty for first home The investor market has been particularly active in

selling or developing later may be a profitable option

buyers. There are some incentives available via the the past three to four years throughout the Illawarra.

providing investors are able to cover the initial costs.

government and private developers however nothing Changes to self managed superannuation fund

However, developers should be wary of the changes

similar to those in New Sourth Wales and Victoria. regulations and historically low interest rates have

to the Lease Variation Charge which took effect on

been the driving force behind this along with rising

With the increased supply of apartments coming the 1st of July 2017. These changes have significantly

property values allowing mum and dad investors

onto the market over the next year, the ACT has increased the fee required to build multiple units on

to use the equity in their owner occupied property

seen relatively slow growth for this style of property residential blocks.

to invest elsewhere. Residential rental prices have

with some properties loosing value. However, rental

Illawarra not been increasing at the same proportion as

demand for apartments has remained strong despite

We see a few different investor types who look to property values and therefore yields have dropped

the increase of supply. If property investors are

invest in residential property. One is the mum and during this period. Some examples of recent larger

chasing yields and not capital growth, purchasing

dad style investor who is either using spare cash or style unit block sales in the Illawarra and their

a new apartment may be a good option. This is

their self-managed superannuation fund to invest gross yields are as follows: ten x 2-bedroom villas

particularly relevant for apartments in the CBD

in a single residential property. This can either be in Bomaderry recently exchanged for $2.35 million

and district centres such as Woden, Tuggeranong,

a dwelling or a unit and their price point can be and at an estimated market rental of $275 per week

Belconnen and Gungahlin. Apartments in proximity

anywhere from $350,000 through to $1 million per villa, the sale price shows a gross yield of 6.1%.

to University of Canberra and Australian National

depending on the amount they have to invest. In Corrimal, a complex comprising five x 3-bedroom

Residential

University also offer good investment opportunities.

Another type is a local investor who has multiple townhouses recently exchanged for $2.27 million

It should be noted that new apartments in Molonglo

properties generating income for them. Most of their and this shows a gross yield of 4.9% at the assessed

Valley, Gungahlin and Tuggeranong may experience

properties are lower end units or dwellings (typically weekly rental of $2,150.

low to no capital growth over the next few years due

purchased for sub $750,000) and they can often

to increasing supply. We understand that investors are significant

include properties converted to allow for multiple

players in the residential property market and

23Month in Review

August 2017

are contributing to rising property prices and the The hamlets of Colo Vale and Hilltop have seen an This may not be the case in the Lower Hunter

recent boom in construction of unit complexes in increase in medium term investor activity, with those however; in fact it will probably buck the trend.

Wollongong. As new units continue to be released to locations being close to the freeway and producing Newcastle is still an enticing prospect for investors

the Wollongong market (along with more on campus strong rental returns. due its close proximity to Sydney, its affordability

accommodation at Wollongong University) there is a compared to the capital cities and an excellent rental

Likewise, across the Southern Tablelands there

real threat of an over supply and heightened risk of market with a current vacancy rate of just 2.3%.

has been a modest amount of speculative investor

vacancy rates rising. As always we would recommend

activity in the new subdivisions close in to Goulburn With Newcastle being a university city there is

that investors complete proper due diligence prior

as well as some of the northern fringe locations of a high investor involvement in good rental yield

to purchasing and understand the rental history of

the region such as Marulan, where investors have suburbs close to the university such as Jesmond and

their potential purchase along with any surrounding

purchased blocks, constructed dwellings and on sold. Wallsend. However investors are also looking at inner

development or infrastructure changes that may

city and coastal suburbs such as Cooks Hill, Wickham

impact. Newcastle

and Adamstown for higher capital gains.

Owning your own home is the great Australian

Southern Highlands/Tablelands

dream, but what about owning two homes, three

With the continuing ripple effect from the Sydney

homes or even more? Investing in real estate has

The Newcastle CBD is undergoing

market buoying the local market, there has been

a noticeable increase in the speculative investor

always been a popular way of earning an extra a makeover and with the

income in Australia and with over 50% of residential

type of individual. This is most evident in the recent

sales in the Lower Hunter in the past financial year

construction of not only a new

release of Retford Park subdivision close to the

township of Bowral which has seen a flurry of vacant

being to investors, this region is certainly a hot spot university campus but also

for property investment.

land lots coming to market. Notably these pre sales numerous apartments, the area is

were effected in quarter 4 of 2015 and quarter 1 The number of investment home loans has

of 2016, with the market having strengthened a dropped nationally over the past year and this

sure to see an influx of investment

minimum 10% since this period. Some of these trend is predicted to continue due to the regulatory in the near future.

purchasers are of the mindset to take the gain clampdowns that have been imposed. These

Residential

Strong rental returns, larger blocks, competitive

now rather than proceed with construction of a regulations and the government’s efforts to cool

capital gains and the ability to find low maintenance

dwelling and bring it to market, albeit that is the the housing market especially in major cities

2- to 3-bedroom properties for under $500,000

strategy of some investors in areas such as Renwick, would suggest that investment should slow down

means the region offers plenty of good investment

(Mittagong) Darraby (Moss Vale), continuing to ride nationwide.

opportunities for those who can’t afford the larger

the wave from the Sydney market.

capital cities, especially Sydney.

24You can also read