Bank of Uganda - State of the Economy September 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Bank of Uganda

State of the Economy

September 2019

i|Page

Table of Contents

List of Figures ............................................................................................................................................... iii

List of Tables ................................................................................................................................................ iii

Acronyms and Abbreviations ........................................................................................................................ iv

Executive Summary........................................................................................................................................ v

1 Background ............................................................................................................................................ 1

2 Global Economic Environment ............................................................................................................. 1

2.1 Economic Activity ......................................................................................................................... 1

2.2 Global Commodity Prices and Inflation ......................................................................................... 2

2.3 Global Financial Markets................................................................................................................ 4

2.4 Implications for the Uganda Economy ........................................................................................... 5

3 Domestic Economic Developments ....................................................................................................... 5

3.1 Monetary Policy and Implementation ................................................................................................... 5

3.1.1 Monetary Policy Stance .............................................................................................. 5

3.1.2 Monetary Policy Implementation ............................................................................... 6

3.2 Interest Rate Developments ........................................................................................................... 7

3.2.1 Yields on Government Securities ............................................................................... 7

3.2.2 Lending and deposit Interest Rates ............................................................................ 8

3.3 Private Sector Credit ...................................................................................................................... 9

3.4 Fiscal Policy ................................................................................................................................. 12

3.4.1 Public Debt .............................................................................................................. 13

3.5 Balance of Payments and Exchange rates ..................................................................................... 14

3.5.1 Exchange Rate Developments.................................................................................. 16

3.6 Domestic Economic Activity .............................................................................................................. 18

3.7 Consumer Price Inflation.................................................................................................................... 20

3.7.1 Recent Inflation Developments ................................................................................ 20

3.7.2 Inflation Outlook ........................................................................................................... 21

4 Conclusion ........................................................................................................................................... 22

ii | P a g e

List of Figures

Figure 1: Commodity Price ............................................................................................................................ 3

Figure 2: Movement in the 10-year Government Bond Yields ..................................................................... 5

Figure 3: The 7-day Interbank Rate and Central Bank Rate .......................................................................... 7

Figure 4: Secondary Market Yields on T-bills and T-bonds ........................................................................... 8

Figure 5: Lending Rates by Sector ................................................................................................................. 9

Figure 6: Annual Growth and Contributions to Private Sector Credit ........................................................ 10

Figure 7: Sectoral Growth in Private Sector Credit ..................................................................................... 11

Figure 8: Current Account Balance and Components ................................................................................. 15

Figure 9: Developments in Overall Balance of Payments and Main Components ..................................... 16

Figure 10: Changes in the NER, Inflation Differential and REER ................................................................. 17

Figure 11: Trends of Selected EAC Partner State Exchange Rates .............................................................. 17

Figure 12: Real GDP Growth by Expenditure .............................................................................................. 19

Figure 13: Domestic Inflation Developments ............................................................................................. 21

Figure 14: Inflation Outlook ........................................................................................................................ 21

List of Tables

Table 1: Global Growth Projections .............................................................................................................. 2

Table 2: Inflation Rates in Selected Countries .............................................................................................. 4

Table 3: Non Performing Loans by sector ................................................................................................... 12

Table 4: Fiscal Operations (Shs. Billion) ...................................................................................................... 13

Table 5: Public Debt Developments ............................................................................................................ 14

iii | P a g e

Acronyms and Abbreviations AEs Advanced Economies BoP Balance of Payments BoU Bank of Uganda CA Current Account CBR Central Bank Rate CPI Consumer Price Index EU European Union EFU Energy, Fuel and Utilities EMDEs Emerging Market and Developing Economies FDI Foreign Direct Investment GDP Gross Domestic Product IFEM Interbank Foreign Exchange Market IMF International Monetary Fund NPL Non- Performing Loans OPEC Organization of Petroleum Exporting Countries PDMF Public Debt Management Framework PPs Percentage Points PSC Private Sector Credit PSI Policy Support Instrument REPOs Repurchase Agreements SSA Sub- Saharan Africa T-Bills Treasury bills T-Bonds Treasury bonds UK United Kingdom US United States WEO World Economic Outlook iv | P a g e

Executive Summary Global economic conditions continue to weaken. Declining trade and heightened uncertainty have contributed to lower global growth. Central banks are easing monetary policy to support their economies. Global growth is projected to be lower at 3.2 percent for 2019 and 3.5 percent for 2020, a 0.1 percentage point downward revision compared to April 2019 forecasts. Forecast for 2019 mostly reflects downward revision to growth in Emerging Markets and Developing Countries. Risks remain tilted to the downside, stemming mainly from escalating US tariff actions, currency wars, retaliation by trading partners, no-deal Brexit, abrupt shifts in risk sentiment and disinflationary pressures. Commodity prices have moderated in 2019, so far and remain relatively volatile owing to the impact of the still-unfolding US tariff actions. Weaker crude oil prices have been mainly driven by concerns about lower global economic growth prospects and the impact from the US-China tariff war. In the quarter to August 2019, average crude oil prices declined by 10.1 percent quarter-on-quarter, and 17.1 percent year-on-year, to USD62.1 per barrel from an average of USD71.9 per barrel in the same period of 2018. Outlook is for commodity prices to drop in 2019 owing to dimmer global economic prospects. Global inflationary pressures remain subdued and are expected to remain muted in 2019 and 2020. Among key Advanced Economies (AE), inflation remains largely below central bank targets this far in 2019, allowing major central banks not only to postpone further increases in interest rates but to cut rates or restart Quantitative Easing going forward in a bid to support growth in the face of escalating trade tensions among other downside risks to growth. While inflation is above target in some key Emerging Market Economies (EMEs), there has been some softening relative to May 2019. Outlook is for low and stable inflation among AE and EMEs in 2019/2020, in line with forecasts for lower commodity prices, however elevating risk of disinflation and further slowdown in global growth momentum. Global financial market conditions have eased further. In response to the weaker economic growth outlook and low inflation environment, several major central banks have made their monetary policies more accommodative. In July 2019, the US Fed cut the target range of the Fed Funds Rate by 0.25PPs to 2-2.25 percent. In Aug-19, Reserve Bank of New Zealand cut the Official Cash rate to 1 percent from 1.5 percent, while the Reserve Bank of Australia lowered its cash rate to 1 percent from 1.25 percent. In June 2019, the European Central Bank (ECB), in its forward guidance, undertook to provide additional stimulus if economic conditions do not improve. Similarly, although the Bank of Japan kept monetary policy steady in June 2019, it indicated it could combine interest rate cuts with bigger asset buying if needed to stimulate the economy. In the currencies market, the US Dollar continues to strengthen against major currencies this far in 2019 supported by a strong US economy. Indeed, the US Dollar index rose by 0.6 percent between Jan-19 and July 2019 and by 1.8 percent year-on-year in July 2019. In the securities markets, 10-year government bond yields continue to decline this far in 2019 consistent with outlook for lower inflation. Outlook is for intermittent episodes of financial market volatility owing to trade policy uncertainty and indecisive Brexit process. v|Page

On the domestic scene, The Bank of Uganda (BoU), in August 2019, maintained the Central Bank Rate (CBR) at 10 percent. The band on the CBR was maintained at +/-3 percentage points (PPs) and the margin on the rediscount rate at 4 PPs on the CBR, placing the rediscount rate and the bank rate at 14 percent and 15 percent, respectively. BoU continued to use Repurchase Agreements (REPOs)/reverse REPOs and deposit auctions to align liquidity conditions in the domestic interbank market with the desired monetary policy stance. In line with the unchanged monetary policy stance, money market rates remained relatively stable in the three months to August 2019. The weighted average 7-day interbank money market rate averaged 10.3 percent between the quarters to May and to August 2019. Average yields on government securities continued to decline in the three months to August 2019, partly on account of the accommodative monetary policy stance. Yields have been declining since the start of 2019. In the three months to August 2019, average yields on Treasury bills declined by an average of 0.2 percentage points (PPs) across all tenors to 9.4 percent (91-day) and 11.5 percent (364-day) compared to an average decline of 0.9 PPs registered in the three months to May 2019. The 182-day paper, which is mostly used in pricing commercial bank lending rates, remained relatively stable at 10.9 percent. Over the same period, yields on Treasury Bonds also declined by an average of 0.7 PPs across all tenors. Notably, there was a larger decline of 1.4 PPs to 14.9 percent for the 15 year Treasury bond which could be a reflection of the lower withholding tax on securities with ten years or more to maturity. In addition, there was a relatively high demand for Government securities, evidenced by huge oversubscriptions in the auctions. Commercial bank lending interest rates generally declined since the beginning of 2019. The gradual decline in the shilling lending rate is reflective of the accommodative monetary policy stance. In the quarter to July 2019, commercial bank lending interest rates remained relatively stable, averaging 20.0 percent compared to an average of 20.2 percent in the quarter to April 2019. However, in July 2019, the Shilling lending rate increased to 21.4 percent from 19 percent in June 2019. Average lending rates on US dollar-denominated loans remained largely stable at 7.0 percent during the quarter ended July 2019. Over the same period, the weighted average shilling deposit rate also remained stable at 10.3 percent; while the foreign currency deposit rate averaged 2.8 percent, lower than the 3.4 percent registered in the quarter to April 2019. Growth in private sector credit (PSC) continued to strengthen, largely supported by continued improvement in economic activity, an accommodative monetary policy stance, and improvement in asset quality (as reflected in lower non-performing loans (NPLs)). The year-on-year growth in PSC averaged 12.6 percent in FY2018/19, almost doubling the 6.8 percent recorded in FY2017/18. The growth in PSC was largely driven by shilling denominated loans, which grew by 18.8 percent in FY 2018/19, from 10.9 percent in the previous year. Foreign currency denominated loans also recovered, recording year- on-year growth of 2.4 percent, compared to 0.5 percent in FY 2017/18. On a quarter-on-quarter basis, PSC also grew strongly at 4.2 percent in the three months to July 2019, compared to 2.1 percent in the three months to April 2019. Going forward, credit to the private sector is poised to improve further on account of lower risk aversion (reflected in the decline in NPLs), strong economic activity and lower cost of borrowing. The vi | P a g e

Business lending survey (BLS) for June 2019 showed that commercial banks expected to maintain their lending rates, while some banks anticipated a decrease in the subsequent quarter. Commercial banks also expected a decrease in default rates on loans to enterprises linked to aggressive recovery measures and the expected injection of funds by the Government to clear arrears. There was likelihood that banks would ease the terms and conditions for loans to enterprises and prime borrowers. Furthermore, the passing of the movable assets bill was expected to pave the way for increased access to financial services by small borrowers, which in turn is likely to provide more support to credit growth. However, there were some downside risks to the anticipated growth in the growth of PSC, which include the implementation of IFRS9, which could limit the availability of loanable funds. In addition, the high operational and funding costs related to the effects of past commitments, like long term fixed deposits and the depreciated shilling, remain factors behind the slow reduction in lending interest rates and could increase the cost of foreign currency borrowing for banks. The BLS also indicated a risk of an increase in default rates on loans to households and individuals in the three months ahead linked to delayed Government releases, impacting specifically salary loans coupled with seasonal effects usually registered in the first quarter where obligations outweigh incomes. These factors could keep lending rates elevated and limit further credit growth. However, on the flipside, operational costs are expected to reduce as banks leverage technology. Fiscal operations were less expansionary than programmed in FY 2018/19. Indeed, the projected fiscal deficit including grants was 5.8 percent of GDP, lower than the budget by 0.8 percent of GDP over the same period. The implementation of the budget was supported by a surplus in domestic revenue but faced constraints from lower-than-target external financing (loans & grants) and slow execution of infrastructural projects. Fiscal Policy is projected to be expansionary in FY 2019/20 with a deficit to GDP of 8.7 percent. Financing this deficit could be challenging. Moreover, Government revenue (including grants) in the first month of FY2019/20 was lower than the approved budget by Shs. 307.8 billion to Shs 1.27 trillion. Fiscal consolidation is projected from FY2020/21 but unlikely given the infrastructure projects in the pipeline and other social spending needs and also the usual slow implementation of the projects. The provisional total public debt stock as at end July 2019 stood at Shs. 47,109 billion (43 percent of GDP), corresponding to year-on-year growth of 14.5 percent. The growth in the stock of total public debt was mainly due to a 16.1 percent increase in the public domestic debt. The public external debt grew by 13.7 percent from USD 7.3 billion to USD 8.3 billion, representing a dominant share of 65.5 percent of the total public debt. In the quarter ended July 2019, the external sector recorded an overall deficit balance of US$59.9 million which was a USD10.7 million contraction from a deficit of USD70.6 million recorded in the quarter to April 2019. Preliminary data indicates that, the current account deficit improved by US$93.9 million to a deficit of USD 811.1 million during the quarter ended July 2019. The trade balance, which continues to be a major component of the current account, improved by US$ 5.3 million to a deficit of USD 717.2 million during the quarter ended July 2019. The financial account surplus was insufficient to finance the deficit balance on the Current and Capital accounts; consequently, there was a drawdown in Reserve of US$ 59.9 million during the quarter to July 2019. vii | P a g e

The outlook for the BOP in the short term is for the current account deficit to widen in FY2019/20

compared to the previous period. The current account deficit is expected to remain weak on account of

continued pickup in imports by the government and private sector. Similarly, the financial account

surplus is projected to widen, as inflows of capital through FDI and project loans are expected to

increase.

The Uganda Shilling remains largely stable with a bias towards appreciation. On a quarterly basis, the

Shilling strengthened by 0.8 percent against the US Dollar, to an average midrate of Shs 3,706.4/USD in

the three months to August 2019, compared to the weakening by 1.1 percent observed in the quarter

ended May 2019. Similarly, on a month-on-month basis, the Shilling strengthened by 0.1 in August 2019

and 1.0 percent year- on-year to a mid-rate of Shs. 3,693.7/ USD, driven largely by Strong inflows

mainly from of strong inflows mainly from NGOs and Financial Institutions and export proceeds. On

trade weighted basis (Nominal Effective Exchange Rate – NEER), the exchange rate appreciated by 1.4

percent quarter on quarter, and 4.4 percent year-on-year in the quarter ended August 2019.

In the last two Financial Years (FY) Uganda’s economy has grown on average by 6.1 percent from a

growth of 3.9 percent in FY2016/17. Investor surveys suggest that business conditions and sentiments

are strong. Credit to the private sector has improved, helped by an accommodative monetary policy

stance.

The economy is expected to maintain this growth momentum and is projected to grow between 6.0 and

6.3 percent in FY 2019/20 and between 6.5 and 7.0 percent in the medium term. The growth prospects

are supported by private sector credit growth, on the back of accommodative monetary policy; public

investment in infrastructure; higher agricultural output due to favourable weather and government

efforts in improving agriculture; improved regional security (South Sudan and DRC) which could boost

Uganda’s exports.

There are downside risks to growth including: Lower external demand due to a depressed global

economy; political and policy uncertainty which are very elevated in several major economies with global

growth continuing to be biased downwards. Already, odds for a global recession are very high; weather

conditions remain a risk for agriculture sector; continued low absorption by government is likely to

moderate the expected support from government investment and multiplier effect on growth; widening

fiscal deficits and associated financing risks given the fact that Government had borrowed Shs.1.5 billion

from BoU by August 2019, moreover if the revenue shortfall observed in July 2019 persists, this could

hinder growth; persistently high non-performing loans in agricultural sector which have potential to

curtail further investment in the sector, and in effect moderate anticipated strong GDP growth; the

decision to postpone the Financial Investment Decision(FID) could have an impact on the investment

in the oil sector which could hinder economic growth in the outer years.

Domestic inflation remains subdued, with annual headline and core inflation averaging 2.7 percent and

3.7 percent, respectively in the quarter to August 2019. Low inflation protects the purchasing power of

Ugandans, importantly poor households.

Even though the inflation projections for August 2019 round of forecast indicate inflation to be higher

in the near term by 0.6 percentage point, outlook for inflation is still soft. However, there are risks to the

inflation forecast: global economic conditions are expected to continue dampening domestic growth and

viii | P a g einflation; the future direction of food crops prices; momentum of domestic demand; widening fiscal deficit and financing; election cycle and associated sentiments and risks. Inflation outlook is favourable, with inflation projected to stabilize around the 5.0 percent target in the medium term. Given the current inflation outlook, BoU has kept the policy rate on hold since October 2018.The evaluation of the macroeconomic developments, current information set and outlook suggests that at the current CBR, monetary policy stance is accommodative, and that inflation will converge to the target in the medium term while supporting growth. ix | P a g e

1 Background This report presents domestic and external economic developments in the period to August 2019. It assesses the future prospects for the global and domestic economy, including economic growth and inflation. It also presents the risks to the domestic economic outlook, the policy challenges in the medium term and the implications of the domestic economic outlook on the future direction of monetary policy. 2 Global Economic Environment 2.1 Economic Activity Global economic conditions continued to weaken during the first half of 2019, on the back of declining trade and heightened uncertainty. While growth was buoyant in Advanced Economies (AEs), activity in Emerging Market and Developing Economies (EM&DEs) was lower than anticipated. At 0.9 percent and 2.7 percent, Q1 2019 growth in the United States and Japan remained resilient, and the temporary factors which had hurt growth in the Euro area in 2018 waned, keeping quarterly growth stable at 1.2 percent. On the other hand, the quarterly growth data out of China, Argentina, Brazil, and India point to weakening activity. According to the IMF July 2019 WEO, global growth is projected at 3.2 percent in 2019 and 3.5 percent in 2020, 0.1 PPs downward revision from the April 2019 forecast. As highlighted in Table 1, the lower forecasts for 2019 mostly reflect downward revision to growth in EM&DEs. The revision arises mainly from the impact of escalating tariffs on an already slowing Chinese economy and lower expected domestic demand growth in India; weak sentiment and policy uncertainty in key Latin American economies mainly in Brazil, Mexico and Venezuela; and softer growth in Sub-Saharan Africa (SSA), mainly dragged down by subdued activity in South Africa arising from the stronger adverse impact of strikes, energy supply constraints in the mining sector, and weak agricultural production. Growth is expected to pick up in 2020 on the assumption that global financial markets remain accommodative; that temporary drags on growth continue to dissipate; and that stressed emerging market economies stabilise. Risks to global growth outlook remain tilted to the downside, stemming mainly from the escalating trade tensions that have the potential of undoing the central banks’ policy stimuli, a no-deal Brexit, abrupt shifts in risk sentiment, and disinflationary pressures. 1|Page

Table 1: Global Growth Projections Source: IMF - WEO April 2019, Economist Intelligence Unit – World Economic Summary May 2019 2.2 Global Commodity Prices and Inflation 2.2.1 Commodity Prices Commodity prices have moderated in 2019, so far and remain relatively volatile owing to the impact of the still-unfolding US tariff actions. Weaker crude oil prices have been mainly driven by concerns about lower global economic growth prospects and the impact from the US-China tariff war. In the quarter to August 2019, average crude oil prices declined by 10.1 percent quarter-on-quarter, and 17.1 percent year-on-year, to USD62.1 per barrel from an average of USD71.9 per barrel in the same period of 2018. The FAO food price index, a measure of global food prices, indicated that average food prices rose by 2.4 percent on a quarterly basis, and 1.6 percent on a yearly basis, in the quarter to July 2019. However, month-on-month, prices declined by 1.1 percent in July 2019, subdued by large export supplies of some cereals and expectation of high sugarcane yields in India. The outlook is for commodity prices to drop in 2019, owing to dimmer global economic prospects. According to the IMF WEO July 2019, average crude oil prices are projected to fall by 4.1 percent to USD65.5 in 2019 and by 2.5 percent in 2020. The US Energy Information Administration (EIA) projects West Texas Intermediate (WTI) spot prices to drop by 10 percent to USD57.9 per barrel in 2019 but pick up by 2.8 percent in 2020. Agricultural commodity prices are projected to generally decline in 2019 and recover slightly in 2020. The global commodity price developments are depicted in Figure 1. 2|Page

Figure 1: Commodity Price

Avg Crude Oil Prices, US$/Brl 50%

40%

Price Indices, 2010=100

Quarterly % Changes

30%

20%

10%

0%

-10%

-20%

-30%

-40%

2016Q4

2017Q1

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

2016Q2

2016Q3

2017Q2

2017Q3

2017Q4

2018Q1

2018Q2

2018Q3

2018Q4

2019Q1

2019Q2

Energy Prices Non Energy Prices Avg. Crude oil price FAO Food Price

Source: World Bank & FAO

2.2.2 Global Inflation

Global inflationary pressures remained subdued, and are expected to remain mute in 2019 and

2020. Among key AEs, inflation remains largely below the average central bank target of 2

percent this far in 2019. This development allowed room for major central banks not only to

postpone further increases in interest rates but to cut rates or restart quantitative easing going

forward, in the face of the downside risks to growth. Average inflation fell in July 2019, to 0.5

percent in Japan, 1.0 percent in the Euro Area, and 1.8 per cent in the US from respective rates

of 0.9 percent, 1.7 percent, and 2.0 percent in April 2019. Inflation remained stable at 2.0

percent in the UK. However, while inflation in key Emerging Market Economies (EMEs) was

relatively elevated and close to or above the average 4 percent central bank target, there has

been a general softening since May 2019. Inflation developments in selected countries are

shown in Table 2.

The outlook is for low or stable inflation among AEs and EMEs in 2019/2020, in line with the

projections of lower commodity prices and a further slowdown in in global growth momentum.

In AEs, inflation is projected to drop to 1.6 percent in 2019 from 2.0 percent in 2018, but rise

to 2.0 percent in 2020. In EMDEs, inflation is projected to remain stable at 4.8 percent in 2019

before decreasing slightly to 4.7 percent in 2020. Inflation outlook for EMDEs is driven largely

by idiosyncratic factors in a few countries especially in Latin America.

3|PageTable 2: Inflation Rates in Selected Countries

Quarterly Monthly

Q2- Q3- Q4- Q1- Q2- Jan- Feb- Mar- Apr- May- Jun- Jul-

2018 2018 2018 2019 2019 2019 2019 2019 2019 2019 2019 2019

Japan 0.6 1.1 0.9 0.3 0.8 0.2 0.2 0.5 0.9 0.7 0.7 0.5

UK 2.2 2.3 2.1 1.8 2.0 1.8 1.8 1.8 2.0 1.9 1.9 2.0

US 2.7 2.6 2.2 1.6 1.8 1.6 1.5 1.9 2.0 1.8 1.6 1.8

Euro area 1.7 2.1 1.9 1.4 1.4 1.4 1.5 1.4 1.7 1.2 1.3 1.0

Brazil 3.3 4.4 4.1 4.1 4.3 3.8 3.9 4.6 4.9 4.7 3.4 3.2

China 1.8 2.3 2.2 1.8 2.6 1.7 1.5 2.3 2.5 2.7 2.7 2.8

India 4.0 5.6 5.1 7.1 8.5 6.6 7.0 7.7 8.3 8.7 8.6 6.0

Russia 2.4 3.0 3.9 5.2 5.0 5.0 5.2 5.3 5.2 5.1 4.7 4.6

South Africa 4.3 4.9 4.8 4.2 4.4 3.9 4.1 4.5 4.4 4.4 4.5 4.0

Source: OECD Statistics

2.3 Global Financial Markets

Global financial market conditions have eased further. In response to the weaker economic

growth outlook and low inflation environment, several major central banks have made their

monetary policies more accommodative. In July 2019, the US Fed cut the target range of the

Fed Funds Rate by 0.25PPs to 2-2.25 percent. In Aug-19, Reserve Bank of New Zealand cut the

Official Cash rate to 1 percent from 1.5 percent, while the Reserve Bank of Australia lowered its

cash rate to 1 percent from 1.25 percent. In June 2019, the European Central Bank (ECB), in its

forward guidance, undertook to provide additional stimulus if economic conditions do not

improve. Similarly, although the Bank of Japan kept monetary policy steady in June 2019, it

indicated it could combine interest rate cuts with bigger asset buying if needed to stimulate the

economy.

In the securities markets, sovereign 10-year bond yields subsequently declined further – in many

cases to historical lows – and credit spreads remain narrower than a year ago (Figure 2). In the

currencies market, the US Dollar continues to strengthen against major currencies this far in

2019 supported by a strong US economy. The US Dollar Index rose by 1.3 percent between

January 2019 and August 2019 and by 2.1 percent year-on-year in August 2019.

Despite the easing global financial conditions, intermittent episodes of financial market volatility

are expected owing to trade policy uncertainty and an indecisive Brexit process.

4|PageFigure 2: Movement in the 10-year Government Bond Yields Source: Thomas Reuters Eikon 2.4 Implications for the Uganda Economy Global economic conditions have weakened further, on the back of declining trade and heightened uncertainty. Given that more than half of Uganda’s exports go to Sub-Saharan Africa whose growth is now projected to be lower, Uganda’s GDP growth may be moderated in 2019, with some improvement in 2020. Global inflationary pressures are muted in line with largely lower commodity prices in 2019. This implies low imported inflation which will support low domestic inflation in 2019. The unease in global financial markets could reduce investor risk appetite lowering capital flows to EMDEs including Uganda, with dampening effect on investment and domestic growth. Changes in capital flows could also lead to exchange rate volatility. 3 Domestic Economic Developments 3.1 Monetary Policy and Implementation 3.1.1 Monetary Policy Stance The Bank of Uganda (BoU), in August 2019, maintained the Central Bank Rate (CBR) at 10 percent. The band on the CBR was maintained at +/-3 percentage points (PPs) and the margin on the rediscount rate at 4 PPs on the CBR, placing the rediscount rate and the bank rate at 14 percent and 15 percent, respectively. 5|Page

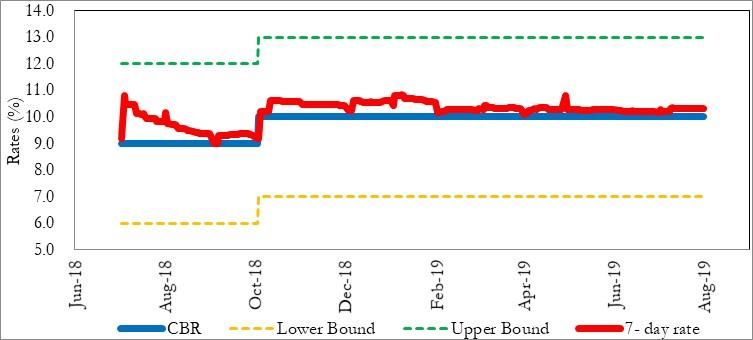

During the August 2019 forecast round, the inflation outlook remained relatively unchanged from the previous period. Core inflation was projected to rise slightly in the near term and stay close to the 5 percent target in the course of next four quarters before peaking at 6.4 in the third quarter of 2020. Similarly, headline inflation was forecast to rise slightly in the near term before returning to 5 percent in the medium term. The risks to inflation were relatively well balanced including, the future path of the exchange rate, higher fiscal stimulus, adverse weather conditions that could lead to a rise in inflation. Economic growth was estimated at 6.3 percent in the financial year (FY) 2019/20, and over 6 percent in the medium term supported by strengthening private sector activity, public investment in infrastructure; higher agricultural output due to favourable weather and government efforts in improving agriculture; improved regional security (South Sudan and the Democratic republic of Congo (DRC)) which could boost Uganda’s exports. However, risks to economic growth remained including the widening fiscal deficit, persistently high non- performing loans in agricultural sector, vagaries of weather, rising global trade tensions, the political and security situation in the run-up to the 2021 general elections, further delays in the start of oil production, spreading of Ebola from DRC, and security concerns and political tensions which could dampen confidence. 3.1.2 Monetary Policy Implementation BoU continued to use Repurchase Agreements (REPOs)/reverse REPOs and deposit auctions to align liquidity conditions in the domestic interbank market with the desired monetary policy stance. The net outstanding stock of REPOs and deposit auctions as at end August 2019 was Shs. 946 billion and Shs. 512.3 billion, respectively. In line with the unchanged monetary policy stance, money market rates remained relatively stable in the three months to August 2019. The weighted average 7-day interbank money market rate averaged 10.3 percent between the quarters to May and to August 2019. The CBR continued to anchor movements in the 7-day money market rate as depicted below in Figure 3. 6|Page

Figure 3: The 7-day Interbank Rate and Central Bank Rate Source: Bank of Uganda 3.2 Interest Rate Developments 3.2.1 Yields on Government Securities Average yields on government securities continued to decline in the three months to August 2019, partly on account of the accommodative monetary policy stance. Yields have been declining since the start of 2019. In the three months to August 2019, average yields on Treasury bills declined by an average of 0.2 percentage points (PPs) across all tenors to 9.4 percent (91-day) and 11.5 percent (364-day) compared to an average decline of 0.9 PPs registered in the three months to May 2019. The 182-day paper, which is mostly used in pricing commercial bank lending rates, remained relatively stable at 10.9 percent. Over the same period, yields on Treasury Bonds also declined by an average of 0.7 PPs across all tenors. Notably, there was a larger decline of 1.4 PPs to 14.9 percent for the 15 year Treasury bond which could be a reflection of the lower withholding tax on securities with ten years or more to maturity. In addition, there was a relatively high demand for Government securities, evidenced by huge oversubscriptions in the auctions. In line with movements in the primary market, there was a continued downward shift in the yield curve across the maturity spectrum in the secondary market. The declining yields are indicative of lower inflation expectations. Figure 4 shows the trend in the secondary market yields on government securities since the three months to February 2019. 7|Page

Figure 4: Secondary Market Yields on T-bills and T-bonds

18.0

Secondary Market Rates

Annualised Yields (%)

15.0

Steady decline from

Q-Jan'19 to Q-Aug'19

12.0

9.0

91-days 182-days 364-days 2-years 3-years 5-years 10-years 15-years

Q-Feb'19 10.6 12.1 12.4 15.9 16.5 16.8 17.3 17.6

Q-May'19 9.5 10.6 11.1 13.4 14.9 15.4 15.8 16.4

Q-Aug'19 9.2 10.4 10.7 12.5 13.7 14.6 15.3 15.6

Source: Bank of Uganda

3.2.2 Lending and deposit Interest Rates

Bank lending to households and businesses remains an important channel through which

monetary policy affects the economy. Commercial bank lending interest rates generally declined

since the beginning of 2019. The gradual decline in the shilling lending rate is reflective of the

accommodative monetary policy stance. In the quarter to July 2019, commercial bank lending

interest rates remained relatively stable, averaging 20.0 percent compared to an average of 20.2

percent in the quarter to April 2019. However, in July 2019, the Shilling lending rate increased

to 21.4 percent from 19 percent in June 2019. Average lending rates on US dollar-denominated

loans remained largely stable at 7.0 percent during the quarter ended July 2019. Over the same

period, the weighted average shilling deposit rate also remained stable at 10.3 percent; while the

foreign currency deposit rate averaged 2.8 percent, lower than the 3.4 percent registered in the

quarter to April 2019.

A decomposition of lending rates by sector for the quarter ended July 2019 showed a slight

increase in lending rates to the key sectors of trade, agriculture and building, construction and

real estate by 0.6 PPs, 0.3 PPs and 1.1 PPs, respectively, to an average of 19.2 percent, 21.4

percent and 21.2 percent, while the personal and household loans declined by 0.2 PPs in the

three months to July 2019 to an average of 21.9 percent. The lending rates by sector are

depicted in Figure 5.

8|PageFigure 5: Lending Rates by Sector Source: Bank of Uganda 3.3 Private Sector Credit Growth in private sector credit (PSC) continued to strengthen, largely supported by continued improvement in economic activity, an accommodative monetary policy stance, and improvement in asset quality (as reflected in lower non-performing loans (NPLs)). The year- on-year growth in PSC averaged 12.6 percent in FY2018/19, almost doubling the 6.8 percent recorded in FY2017/18. The growth in PSC was largely driven by shilling denominated loans, which grew by 18.8 percent in FY 2018/19, from 10.9 percent in the previous year. Foreign currency denominated loans also recovered, recording year-on-year growth of 2.4 percent, compared to 0.5 percent in FY 2017/18. On a quarter-on-quarter basis, PSC also grew strongly at 4.2 percent in the three months to July 2019, compared to 2.1 percent in the three months to April 2019. Net of valuation changes on account of exchange rate movements, the average annual PSC grew by 14.8 percent in the quarter to July 2019, higher than the 14.0 percent growth recorded in the quarter to April 2019 and 10.9 percent in the quarter to July 2018. Specifically, foreign currency denominated loans grew by 7 percent, doubling from the 3.5 percent growth registered in the quarter to April 2019. Developments in private sector credit are shown in Figure 6. 9|Page

Figure 6: Annual Growth and Contributions to Private Sector Credit

22.0

18.0

14.0

10.0

Percent

6.0

2.0

-2.0

-6.0

Jan-17

May-17

Jan-18

May-18

Jan-19

May-19

Sep-17

Sep-18

Nov-18

Jul-17

Jul-18

Mar-19

Jul-19

Mar-17

Nov-17

Mar-18

PSC Shs. PSC fx Total PSC PSC (Net Revaluation)

Source: Bank of Uganda

Credit growth remains robust across most sectors supported by strong economic growth and

lower non-performing loans (NPLs) as depicted by the sectoral decomposition in Figure 7.

The manufacturing sector continued to register strong growth averaging 21.2 percent in the

quarter to July 2019, slightly lower than the 22.5 percent growth registered in the quarter to

April 2019. There was an improvement in growth in credit to the agriculture sector at 18.8

percent in the quarter to July 2019 compared to 13.9 percent and 14.6 percent in the quarters to

April and January 2019, respectively. Growth in credit to the building, mortgage, construction &

real estate sectors, which has generally remained below average the industry average, recorded a

recovery, growing at 12.9 percent in the quarter to July 2019 compared to 9.9 percent and 9.1

percent respectively in the quarters to April and January 2019. Over the same period however,

growth in credit to the trade sector declined to an average of 14.8 percent from 16.1 percent

recorded in the previous period.

Going forward, credit to the private sector is poised to improve further on account of lower

risk aversion (reflected in the decline in NPLs), strong economic activity and lower cost of

borrowing. The Business lending survey (BLS) for June 2019 showed that commercial banks

expected to maintain their lending rates, while some banks anticipated a decrease in the

subsequent quarter. Commercial banks also expected a decrease in default rates on loans to

enterprises linked to aggressive recovery measures and the expected injection of funds by the

Government to clear arrears. There was likelihood that banks would ease the terms and

conditions for loans to enterprises and prime borrowers. Furthermore, the passing of the

movable assets bill was expected to pave the way for increased access to financial services by

small borrowers, which in turn is likely to provide more support to credit growth.

10 | P a g eHowever, there were some downside risks to the anticipated growth in the growth of PSC, which include the implementation of IFRS9, which could limit the availability of loanable funds. In addition, the high operational and funding costs related to the effects of past commitments, like long term fixed deposits and the depreciated shilling, remain factors behind the slow reduction in lending interest rates and could increase the cost of foreign currency borrowing for banks. The BLS also indicated a risk of an increase in default rates on loans to households and individuals in the three months ahead linked to delayed Government releases, impacting specifically salary loans coupled with seasonal effects usually registered in the first quarter where obligations outweigh incomes. These factors could keep lending rates elevated and limit further credit growth. However, on the flipside, operational costs are expected to reduce as banks leverage technology. Figure 7: Sectoral Growth in Private Sector Credit Source: Bank of Uganda In terms of asset quality, non-performing loans (NPLs) remained relatively low in the quarter to June 2019. As a percentage of total loans, NPLs remained at 3.8 percent in the quarter to June 2019 as in the preceding quarter (Table 3). The ratio of NPLs to total loans in the building, construction and real estate sector, which has a gross loan share of 20.1 percent, increased by 0.5 percent to 3 percent in the quarter to June 2019, while NPLs in the trade and commerce sector, with a 19.1 percent share of gross loans, have been on a steady decline from June 2018. The agriculture and services sectors were the most risky sectors as at June 2019, registering sectoral NPL ratios of 9.1 and 7.6, way above the industry average. Going forward, Banks are 11 | P a g e

expected to further ease overall credit standards as the asset quality continues to improve. This

will in turn boost private sector credit and enhance economic growth.

Table 3: Non Performing Loans by sector

Jun-18 Sep-18 Dec-18 Mar-19 Jun-19 Gross Loan

Non-Performing Loans as a share of Total

Share as at

Loans by sector

Jun' 19

BUILDING, CONSTRUCTION & REAL ESTATE 3.4 3.9 2.2 2.5 3.0 20.1

TRADE & COMMERCE 5.2 6.3 4.0 3.6 3.2 19.1

Breakdown by sector

PERSONAL AND HOUSEHOLD LOANS 2.8 3.3 2.6 2.8 2.6 18.3

MANUFACTURING 1.4 1.9 2.3 2.9 2.7 14.3

AGRICULTURE 11.0 9.8 7.9 9.7 9.1 12.6

BUSINESS SERVICES 6.1 3.7 2.7 3.1 2.8 4.6

TRANSPORT & COMMUNICATION 3.1 4.3 2.6 1.5 3.4 4.4

COMMUNITY, SOCIAL AND OTHER SERVICES 5.8 3.8 3.0 8.0 7.6 3.2

ELECTICITY & WATER 0.1 0.1 0.0 0.1 0.3 2.0

OTHER ACTIVITIES 14.3 21.8 8.6 6.7 4.0 0.9

MINING & QUARRYING 5.2 4.7 0.4 0.3 0.8 0.6

5 Banks with a large share ( >8%) 4.1 4.3 3.0 3.1 3.1 62.0

Category

of Banks

14 Banks with a moderate share (1-8%) 4.8 5.2 4.0 4.9 4.4 35.0

5 Banks with a small share (underperformance in the external loan disbursements may in part be attributed to slow

absorption by Government projects.

The developments in government revenue and expenditure resulted in a fiscal deficit inclusive

of grants of Shs. 6,243.4 billion, which was lower than the approved budget deficit by Shs.

1,184.1 billion. The fiscal operations are depicted in Table 4.

Table 4: Fiscal Operations (Shs. Billion)

July’17- Prel. July'18- Approved Budget

Variation

June’18 June’19 July’18-June’19

Revenue & Grants 15,281.1 17,262.5 18,046.2 -783.7

Revenue 14,506.9 16,637.8 16,358.8 279.0

Grants 774.2 624.7 1,687.4 -1,062.7

Expenditure & Lending 20,183.4 23,505.9 25,473.7 -1,967.8

Current Expenditure 10,916.0 12,092.8 12,249.6 -156.8

Development Expenditure 7,566.1 9,707.5 11,912.7 -2,205.2

Net lending/repayments1 1,396.5 1,286.7 1,050.8 235.9

Domestic arrears 304.9 418.9 260.6 158.3

Deficit (excluding grants)

repayment -5,676.5 -6,868.1 (9,114.9) 2,246.8

Deficit (including grants) -4,902.3 -6,243.4 (7,427.6) 1,184.1

Financing (net) 4,902.3 6,243.4 7,427.6 -1,184.1

External Financing (net) 3,496.2 3,632.4 5,442.1 -1,809.7

Domestic Financing (net) 1,358.1 2,464.2 1,985.4 478.8

Errors & Omissions 48.0 146.9 0.0

% of GDP

Revenue & Grants 15.2 15.4 16.1 -0.7

Expenditure & Lending 20.1 21.0 22.7 -1.7

Deficit (including grants) 4.9 5.6 6.6 -1.0

Source: Ministry of Finance, Planning and Economic Development (MOFPED)

Fiscal Policy is projected to be expansionary in FY 2019/20 with a deficit to GDP of 8.7

percent. Financing this level of deficit will be challenging. Moreover, this is premised on

domestic revenue to GDP of 16.3 percent, which is an increase of 1.2 percentage points

compared to FY2018/19. Indeed, government revenue (including grants) in the first month of

FY2019/20 was lower than the approved budget by Shs. 307.8 billion. Fiscal consolidation is

projected from FY2020/21 but this is unlikely given the numerous infrastructure projects in the

pipeline and other social spending needs and also the usual slow implementation of the projects.

3.4.1 Public Debt

13 | P a g eThe provisional total public debt stock as at end July 2019 stood at Shs. 47,109 billion (43

percent of GDP), corresponding to year-on-year growth of 14.5 percent. The growth in the

stock of total public debt was mainly due to a 16.1 percent increase in the public domestic debt.

The public external debt grew by 13.7 percent from USD 7.3 billion to USD 8.3 billion,

representing a dominant share of 65.5 percent of the total public debt. With the exception of

the ratio of the stock of government securities to the stock of private sector credit which stands

at 102.1 percent, above the benchmark of 75 percent, all the public domestic debt risk

indicators were within the Public Debt Management Framework (PDMF 2013) medium term

benchmarks (Table 5).

Table 5: Public Debt Developments

PDMF Jun’17 Jun’18 Jun’19

Percent maturing in 1 year 3Yrs 3.7 3.8 3.9

(ATM) (years)

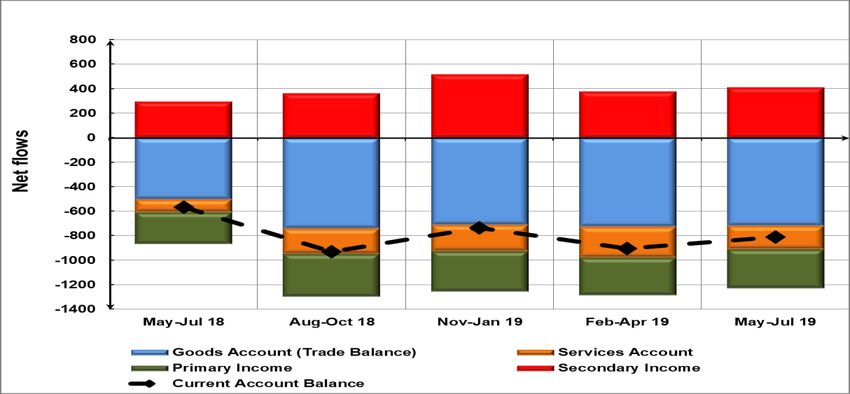

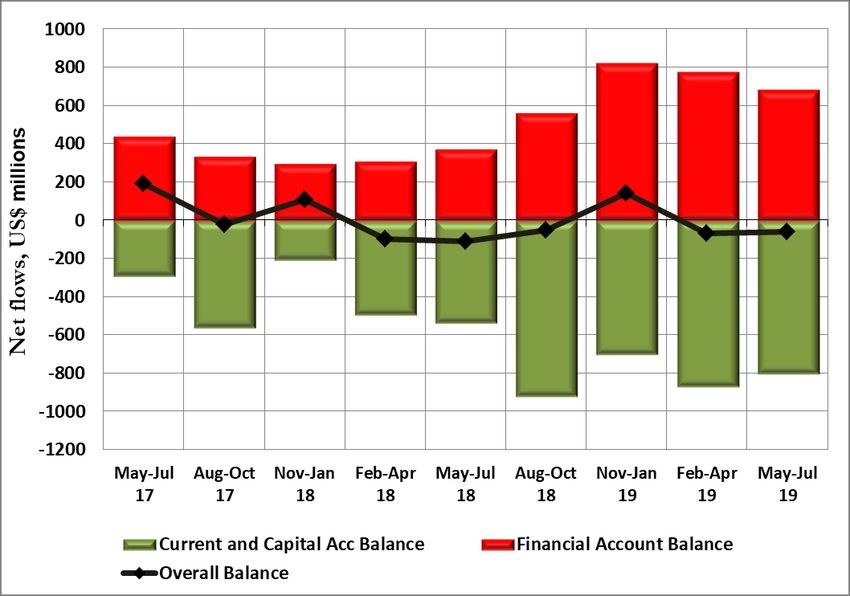

Total Stock/PSCtransport. Over the same period, the primary income balance deteriorated by USD 8.1 million to a deficit of USD316.3 million during the quarter ended July 2019, owing to higher income payable to foreign investors. On the other hand, the secondary income balance improved by USD36.4 million to a surplus of USD414.3 million, on account of a USD56.4 million increase in NGO’s receipts. Figure 8: Current Account Balance and Components The capital account balance deteriorated by USD28.4 million in the quarter ended July 2019 to USD7.6 million from USD36.0 million in the previous quarter. The developments in the current and capital account yielded a net borrowing balance of USD803.5 million, a decline of USD65.5 million relative to the quarter ended April 2019. Capital inflows of USD686.9 million were received in the quarter to July 2019, down from inflows of USD778.0 million in the previous quarter. This was driven by lower loan disbursements for public investments in the period under review. However, on an annual basis, the financial account inflows increased by USD 1531.3 million in the 12 months to July 2019 mainly on account of FDI inflows, higher loan disbursements and lower portfolio investment outflows. The financial account surplus was insufficient to finance the deficit balance on the Current and Capital accounts; consequently, there was a drawdown in Reserve of US$ 59.9 million during the quarter to July 2019 as depicted in Figure 9. Similarly, on an annual basis, the financial account surplus was insufficient to finance the current and capital account, leading to a drawdown of reserves by USD 41.4 million. The stock of reserves as at the end of July 2019 was estimated at USD3,342.4 million (including valuation changes), equivalent to 4.1 months of future imports of goods and services, a decline from USD3,434.3 million (4.3 months of import 15 | P a g e

cover) as at end April 2019. Figure 9: Developments in Overall Balance of Payments and Main Components Source: Bank of Uganda The outlook for the BOP in the short term is for the current account deficit to widen in FY2019/20 compared to the previous period. The current account deficit is expected to remain weak on account of continued pickup in imports by the government and private sector. Similarly, the financial account surplus is projected to widen, as inflows of capital through FDI and project loans are expected to increase. 3.5.1 Exchange Rate Developments The Uganda Shilling remains largely stable with a bias towards appreciation. On a quarterly basis, the Shilling strengthened by 0.8 percent against the US Dollar, to an average midrate of Shs 3,706.4/USD in the three months to August 2019, compared to the weakening by 1.1 percent observed in the quarter ended May 2019. Similarly, on a month-on-month basis, the Shilling strengthened by 0.1 in August 2019 and 1.0 percent year- on-year to a mid-rate of Shs. 3,693.7/ USD, driven largely by Strong inflows mainly from of strong inflows mainly from NGOs and Financial Institutions and export proceeds. On trade weighted basis (Nominal Effective Exchange Rate – NEER), the exchange rate appreciated by 1.4 percent quarter on quarter, and 4.4 percent year-on-year in the quarter ended 16 | P a g e

August 2019. On monthly basis the NEER also appreciated by 1.1 percent in August 2019 and

3.5 percent year-on-year. Taking inflation into account, the real effective exchange rate (REER)

appreciated by 0.3 percent month on month and 4.7 percent year on year on in July 2019.

Developments in the exchange rate are depicted in Figure 10.

Figure 10: Changes in the NER, Inflation Differential and REER

9

7

5

3

1

-1

Per cent

-3

-5

-7

-9

Jun-18

Jun-19

Jan-18

Feb-18

May-18

Jan-19

Feb-19

May-19

Jul-17

Jul-18

Jul-19

Oct-17

Nov-17

Oct-18

Nov-18

Sep-17

Apr-18

Sep-18

Dec-18

Apr-19

Aug-17

Dec-17

Mar-18

Aug-18

Mar-19

Y-o-Y UGX/USD Change Inflation Differential Y-O-Y REER Change

Source: Bank of Uganda

Developments in regional exchange rates were mixed during the three months to August 2019,

with the Uganda Shilling appreciating, the Tanzania Shilling remaining largely stable and the

Kenya Shilling and Rwanda Franc depreciating slightly against the US dollar (Figure 11). The

Kenya Shilling appreciated by 1.8 percent to average KES 102.7/US$, the Tanzania Shilling

depreciated by 0.01 percent to average TZS 2,300.5/US$, while the Rwanda Franc depreciated

by 1.1 percent to average RWF 900.2/US$ in the quarter ended August 2019 compared to the

previous quarter ended May 2019.

Figure 11: Trends of Selected EAC Partner State Exchange Rates

4% UGX/USD KES/USD RWF/USD TZShs/USD

3%

2%

1%

Monthly Percentage

0%

Changes

-1%

-2%

-3%

2017 M11

2017 M01

2017 M02

2017 M03

2017 M04

2017 M05

2017 M06

2017 M07

2017 M08

2017 M09

2017 M10

2017 M12

2018 M01

2018 M02

2018 M03

2018 M04

2018 M05

2018 M06

2018 M07

2018 M08

2018 M09

2018 M10

2018 M11

2018 M12

2019 M01

2019 M02

2019 M03

2019 M04

2019 M05

2019 M06

2019 M07

2019 M08

Source: Bank of Uganda

17 | P a g eConditions in the IFEM enabled BoU to boost foreign exchange reserves. Indeed, in the three months to August 2019, the BoU purchased US$ 249.9 million for reserve build-up and sold US$35.4 million in targeted sales, as a result the net foreign currency purchased in the IFEM for reserve build-up was US$ 214.5 million. In the short to the medium term, the exchange rate may depreciate on account of strong government and private sector import demand as more projects get underway and economic activity continues to strengthen. 3.6 Domestic Economic Activity In line with previous estimates of 6.0 - 6.5 percent growth for the FY 2018/19, Uganda Bureau of Statistics (UBOS) estimates indicate that the economy expanded at 6.1 percent, 0.1 PPs lower than the growth in FY2017/18, at 6.2 percent. The estimation is consistent with the BoU’s high frequency indicator of economic activity – the composite index of economic activity (CIEA) data, where annual growth was projected at about 5.9 percent, with a positive growth outlook in all economic sectors. On a quarterly basis, UBOS data indicated a lower GDP growth rate of 0.8 percent in the quarter to March 2019, pointing to a slowdown in economic activity. Similarly, the BoU’s CIEA estimated growth at 1.1 percent in the quarter to June 2019, compared to 1.7 percent growth in the preceding quarter, driven by lower growth in the agriculture, industry and the services sectors of 0.3, 0.6 and 1.4 percent relative to 0.5, 2.1 and 1.0 percent, respectively in the quarter to March 2019. If the projected slowdown is to materialise, there is likelihood that the 6.2 percent growth projected for FY 2018/19 might not be realised. Stanbic bank’s Purchasing Managers Index (PMI) grew to 57.5 in August 2019, from 58.2 in the preceding month, signalling a decline in business conditions in the private sector but still above the average. The index moved in line with business confidence indices, which remained in the optimistic territory in the quarter to July 2019. Notwithstanding the continued optimism by businesses, confidence indices were less upbeat across all sectors, save for the agriculture and manufacturing sectors but with a less buoyant outlook. On the other hand, consumer sentiments on the economy improved, albeit still in the pessimistic zone, with expectations and current economic conditions sub-components registering an improvement. Figure 12 depicts the growth in GDP and CIEA. 18 | P a g e

Figure 12: Real GDP Growth by Expenditure

4.00

3.50

3.00

percent

2.50

2.00

1.50

1.00

0.50

-

Quarterly changes-CIEA UBOS GDP

Source: Uganda Bureau of Statistics

Looking forward, the Ugandan economy is projected to continue on its growth trajectory, as it’s

estimated to grow between 6 and 6.3 percent in FY 2019/20, and between 6.5 and 7.0 percent

over the medium term. Growth prospects are expected to emanate from strengthening private

sector activity; public investment in infrastructure; higher agricultural output due to favourable

weather and government efforts in improving agriculture. In addition, improvements in regional

security particularly in the Democratic Republic of Congo and South Sudan following the

signing of the revitalised peace agreement could provide an impetus to Uganda’s exports, and in

turn, boost growth. The start of oil production will provide additional boost to overall GDP.

Continued strong growth in services, industry, and construction will provide the needed

impetus to sustain strong overall growth. Growth in services (7-7.5 percent a year) will continue

to rely on strong performance in information and communication, transport, and tourism.

Industrial growth (5 percent) will be supported by the expansion of industrial parks, while

construction (7-8 percent) will be driven by public investment projects. Agriculture is expected

to grow on average 3 percent a year and is facing downside risks from the increasing severity

and frequency of unfavourable weather events.

The growth outlook, however, remains subject to downside risks, which include:

a) continued slow execution of public investments could moderate the expected support

from Government investment and the multiplier effect on growth;

b) political and policy uncertainty which are very elevated in several major economies with

global growth continuing to be biased downwards. Already, odds for a global recession

are very high. Heightened uncertainty and declining international trade that have

19 | P a g eYou can also read