Benchmark rate reform and transition to risk free rates - Mizuho Financial Group

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Benchmark rate reform and transition to risk free rates

IBOR discontinuation and reform

Interbank Offered Rates (IBORs) are a series of benchmark interest rates, used globally for pricing

loans, debt securities and derivatives. Following recommendations made by the Financial Stability

Board in 2014, global initiatives have been undertaken to reform such benchmarks and to

commence the transition to alternative benchmark or reference rates.

Developments in the three major IBORs, as at 6th September 2021, are summarised below:

Benchmark Discontinuation / Reform measures

LIBOR The London Interbank Offered Rate (LIBOR) is a global interest rate benchmark

which is currently published across five currencies (Sterling, US Dollar, Euro, Swiss

Franc and Japanese Yen) and seven terms (ranging from overnight to 12 months).

On a number of occasions the Financial Conduct Authority (FCA) has stated that

markets should be prepared for announcements that some or all LIBOR rates will

cease after the end of 2021, or for the FCA to find that such rates are no longer

representative after the end of 2021.

On 5th March 2021, the FCA announced:

(1) immediately after December 31, 2021, publication of all seven euro LIBOR

settings, all seven Swiss franc LIBOR settings, the Spot Next, 1-week, 2-month

and 12-month Japanese yen LIBOR settings, the overnight, 1-week, 2-month

and 12-month sterling LIBOR settings, and the 1-week and 2-month US dollar

LIBOR settings will permanently cease;

(2) immediately after June 30, 2023, publication of the overnight and 12-month US

dollar LIBOR settings will permanently cease;

(3) immediately after December 31, 2021, the 1-month, 3-month and 6-month

sterling LIBOR settings will no longer be representative of the underlying market

and economic reality they are intended to measure and that representativeness

will not be restored and the FCA will consult on requiring IBA to continue to

publish these settings on a changed methodology (or ‘synthetic’) basis;

(4) immediately after December 31, 2021, the 1-month, 3-month and 6-month

Japanese yen LIBOR settings will no longer be representative of the underlying

market and economic reality they are intended to measure and that

representativeness will not be restored and the FCA will consult on requiring IBA

to continue to publish these settings on a synthetic basis for one additional year;

and

(5) immediately after June 30, 2023, the 1-month, 3-month and 6-month US dollar

LIBOR settings will cease to be provided or, subject to the FCA’s consideration

of the case, be provided on a synthetic basis and no longer be representative of

the underlying market and economic reality they are intended to measure and

that representativeness will not be restored.EURIBOR The Euro Interbank Offered Rate (EURIBOR) and the Euro Overnight Index Average

(EONIA) are the most important interest rate benchmarks within the Eurozone.

EONIA

European interest rates are subject to the EU Benchmarks Regulation (BMR) which

was introduced in January 2018 to improve the integrity of, and set a common

framework for regulation of, benchmarks across the EU. The BMR set a deadline for

critical benchmarks to meet certain regulatory standards. The BMR transition period,

after which critical benchmarks failing to meet the standards cannot be used for new

contracts, has been extended to 31 December 2023.

In July 2019, European Money Markets Institute (EMMI) was authorised as

administrator of EURIBOR under the BMR and implementation of a new hybrid

methodology for EURIBOR was completed in November 2019.

EONIA will not be reformed and has been published in parallel with the Euro Short-

Term Rate (€STR) since publication of €STR began on 2 October 2019. EONIA will

be permanently discontinued on 3 January 2022.

TIBOR Reform measures were introduced in 2017 in respect of The Tokyo Interbank

Offered Rate (TIBOR), which is widely used as an interest rate benchmark for bank

loans in Japan. It is not proposed that TIBOR be discontinued.

Further reform may be undertaken, including the potential integration of Japanese

Yen TIBOR and Euroyen TIBOR (Japanese offshore markets).

Replacing certain IBORs with Risk Free Rates

Risk free rates ("RFRs") are generally proposed by the applicable working groups as replacements

or alternatives to IBORs, due to their transparency and limited exposure to manipulation. RFRs are

calculated on a different basis and are not like-for-like replacements for IBORs. RFRs are overnight

rates which traditionally are retrospective, i.e. they are published after the period to which they

relate, as opposed to IBORs, which are set at, or prior to, the commencement of the period to which

they relate. The differences between the two types of rate are discussed further below.

In preparation for the transition away from certain IBORs, authorities and industry working groups

have identified various RFRs as possible replacements for LIBOR and EONIA for each of the

currencies across which LIBORs are currently published:

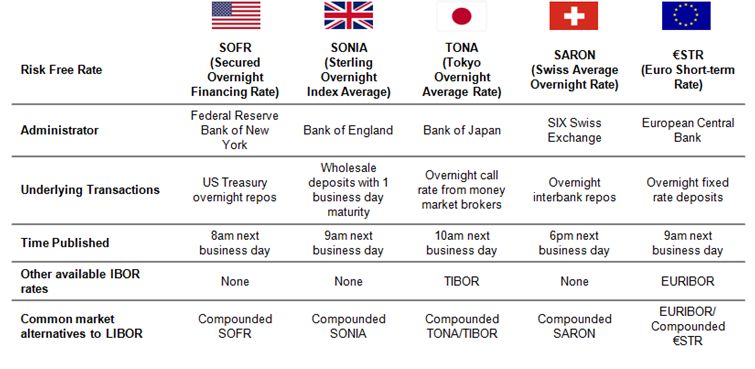

• The Bank of England’s working group has recommended reformed Sterling Overnight Index

Average (SONIA) as the preferred RFR alternative to Sterling LIBOR;

• The Federal Reserve Bank of New York, the European Central Bank, the SIX Swiss

Exchange and the Bank of Japan have also established working groups to develop risk free

rates to support the transition away from their respective currency LIBOR rates, and these

rates have now also been selected (as set out in the table below); and

• In October 2019, the European Central Bank began publishing the Euro Short-Term Rate

(€STR), a new unsecured overnight interest rate as an alternative to EONIA.As at 6th September 2021, the development of each RFR is at a different stage and they vary in a

number of ways as highlighted in the table below.

Differences between IBORs and RFRs

As set out above, RFRs are described as ‘near risk free’ and are derived from actual transactions

that have taken place in the liquid underlying markets. There are a number of differences between

IBORs and RFRs which will need to be addressed in the transition process away from certain

IBORs, including:

• Credit and Liquidity Premiums: IBORs include the cost of bank credit risk and term

liquidity risk, as they are based on the submissions of panel banks indicating where they

can borrow unsecured funds in the relevant interbank market, whereas RFRs are based on

overnight transactions. Transitioning existing contracts from IBORs to RFRs may involve

incorporating a spread into the RFR to cover the lender’s funding costs and the credit risk

premium of the borrower.

• Calculation direction: RFRs are backward looking overnight rates whereas IBORs are

forward looking term rates, meaning that for IBORs the rate of interest is fixed and publicly

available at the beginning of each interest period. Industry working groups have extensively

analysed compounding RFRs in arrears and the Working Group on Sterling Risk-Free

Reference Rates ("£RFR WG") has issued recommendations in this regard, which are

discussed further below.Points for you to consider in relation to IBOR transition

The FCA has clarified the timing of the cessation and non-representativeness of certain

benchmarks in its announcements on 5th March 2021, as described above. The £RFR WG has set

an end-Q3 2021 recommended milestone to complete active conversion of all legacy GBP LIBOR

contracts expiring after end 2021 where viable and, if not viable, ensure robust fallbacks are

adopted where possible. The changes brought about by such events may have an impact on

references to IBORs in existing products and may necessitate use of an alternative benchmark

rate, such as an RFR or an IBOR which is not being discontinued, or require fallback to a financial

institution's cost of funds.

Any such changes may impact the loans, debt securities and derivatives you currently hold (and

those you enter into in future), including:

• requiring the application of fallback provisions in the contract which provide for an

alternative mechanism for calculating the relevant payment amount, such as when IBOR

rates are not available, or the amendment of contracts to (i) replace existing fallback

provisions with more robust fallback provisions, or (ii) to include fallback provisions;

• potential changes to the interest and other provisions of existing contracts, to provide for

the transition to an alternative reference rate;

• the potential for a material mismatch between products in your portfolio (such as loans and

corresponding hedges), which currently refer to the same benchmark rate;

• an impact on the value or pricing or cost to you of the product;

• potential accounting and tax issues, as many businesses use IBORs for derivative and

other valuation purposes; and

• potential operational implications, such as changes to systems or processes (such as the

impact on cashflow forecasting, when moving from forward looking to backward looking

rates).

We recommend you keep up to date with the latest industry developments and consider whether

you require independent professional advice (whether legal, accountancy, tax or other advice) in

relation to IBOR transition and keep your position under review.Next steps

Loans

The FCA announcement on 5th March 2021 confirmed that the following 26 LIBOR settings will

cease to be published from 31 December 2021.

LIBOR Tenor

EUR LIBOR all tenors

CHF LIBOR all tenors

JPY LIBOR spot next, 1 week, 2 month and 12 month

GBP LIBOR overnight, 1 week, 2 month and 12 month

USD LIBOR 1 week and 2 month

The FCA announcement also confirmed that even if the remaining 9 LIBOR settings were to

continue to be published on a synthetic basis, they will no longer be representative of the underlying

market or economic reality that they are intended to measure.

LIBOR Tenor

JPY LIBOR 1, 3 and 6 months

GBP LIBOR 1, 3 and 6 months

USD LIBOR 1, 3 and 6 months

Parties to facility agreements which contain any version of the LMA’s “Replacement of Screen Rate”

clause should consider whether the FCA announcement constitutes a “Screen Rate Replacement

Event” and whether they wish to begin the optional amendment process this clause offers in such

circumstances. Parties to facility agreements containing the LMA’s rate switch provisions in the

form of those in the LMA Recommended Forms (defined below) should consider whether the FCA

announcement constitutes a “Rate Switch Trigger Event” in their agreements. The £RFR WG

published a paper in August 2020 outlining how, by the end of Q3 2020, lenders should be in a

position to offer non-LIBOR linked products to borrowers and must include clear contractual

arrangements (through pre-agreed conversion terms or an agreed process for re-negotiation) in

new and re-financed sterling LIBOR loans to convert to alternative rates by year end-2021. In

compliance with these requirements Mizuho is able to offer non-LIBOR linked products and, where

relevant, will include clear contractual arrangements for conversion in in-scope agreements.

Also, in light of the recommended milestones set by the £RFR WG, from 1st April 2021 all new or

refinanced GBP lending entered into by Mizuho which expires after end 2021 has been and will

continue to be based on SONIA or other non-LIBOR alternatives.

In September 2020, the £RFR WG also recommended the use of a Five Banking Days Lookback

without Observation Shift as the standard approach for SONIA. A "Lookback" period allows for

payment certainty for borrowers when using an 'in arrears' rate such as SONIA, as the actual rate

is known to the borrower five days before interest is payable (rather than at the beginning of the

interest period, as with LIBOR). Although the £RFR WG has recommended a standard Lookback

period of five Business Days, the length of the Lookback period can be varied based on

borrower/lender needs.

In relation to syndicated loans, the Loan Market Association (LMA) has now published

recommended versions of its forms of facility agreement for loans referencing RFRs as part of its

library of recommended forms (the LMA Recommended Forms). The LMA Recommended Forms

(which were previously in circulation as exposure drafts) reflect the recommendations of the £RFRWG and are being widely adopted by the loan market. The LMA Recommended Forms are being used for both term and revolving loans (in sterling and other currencies) and are also being adapted for use in bilateral transactions. In the majority of cases, the LMA Recommended Forms are being adopted with minimal amendments, which indicates that lenders are becoming broadly comfortable with the LMA’s approach. The publication of the LMA Recommended Forms occurred on 30 March 2021, just prior to the £RFR WG milestone for the cessation of new sterling LIBOR products on 1 April 2021. The syndicated loan market does not have a protocol system (i.e. a multi-lateral method) for amendments (such as that which is operated by ISDA) given the multilateral nature of syndicated loans and so loan agreements referencing LIBOR may need to be individually amended to refer to a replacement rate. On 25th October 2019 the LMA, to help streamline the amendment process, published an exposure draft reference rate selection agreement for use in relation to legacy transactions transitioning from LIBOR to an RFR. The LMA published this draft reference rate selections agreement as a recommended form on 4 June 2021. The Federal Reserve Board, the Office of the Comptroller of the Currency, and the Federal Deposit Insurance Corporation have issued supervisory guidance encouraging banks to “cease entering into new contracts that use USD LIBOR as a reference rate as soon as practicable and in any event by December 31, 2021”, noting that new USD LIBOR issuance after 2021 would create safety and soundness risks. Foreign regulators have stated that they are considering similar steps. The Loan Syndication and Trading Association has published a concept credit agreement describing a term loan referencing daily simple SOFR or daily compounded SOFR (using a "compound the balance" approach). Consistent with the ARRC's recommended conventions, the concept document includes a lookback with no observation shift. On 29 July 2021, the ARRC announced that it was formally recommending the CME Group’s SOFR forward looking Term Rates. On 9 August 2021, the LSTA published a Draft Term SOFR Concept Document which reflects the ARRC’s recommended conventions, but also includes some additional convention options. Derivatives and other trading products The International Swaps and Derivatives Association (ISDA) launched the IBOR Fallbacks Protocol (the Protocol) on 23rd October 2020 for adhering parties, which is a multilateral method to amend legacy derivatives (and certain other trading contracts), and the IBOR Fallbacks Supplement (Supplement 70) to the 2006 ISDA Definitions (the Definitions) to implement robust fallbacks to IBORs into transactions. The Protocol and Supplement 70 took effect on 25th January 2021. Mizuho Bank, Ltd. and Mizuho International plc have both signed up to the Protocol. The announcement made by the FCA on 5th March 2021 constitutes an “Index Cessation Event” for all LIBOR settings under the Supplement and the Protocol, and as a result the fallback spread adjustment will be fixed as of 5 March 2021 for all euro, sterling, Swiss franc, US dollar and yen LIBOR tenors. In respect of the ISDA Benchmarks Supplement, at the time of the Index Cessation Event the LIBOR Floating Rate Options, as referenced in transactions incorporating the terms of the IBOR Fallbacks or the Protocol, include a reference to a concept defined or otherwise described as an “index cessation event” which in effect means that a “Priority Fallback” of the ISDA Benchmarks Supplement will apply to the relevant transactions. “Consequences of a Benchmark Trigger Event” of the ISDA Benchmarks Supplement will apply only to the extent the “Priority Fallback” fails to provide a means of determining the index level.

Timely adherence to the Protocol is being encouraged by national working groups, including the

ARRC, as well as international bodies such as the Financial Stability Board.

Please note that the £RFR WG has recommended the following best practice milestones:

i) from 1 April 2021, cease initiation of new GBP LIBOR linked derivatives, bonds and

securitisations that expire after the end of 2021;

ii) from 1 July 2021, cease initiation of new GBP LIBOR-linked non-linear derivatives

that expire after the end of 2021; and

iii) by end Q3 2021, complete active conversion where viable.

However, the £RFR WG recognises that there will be limited circumstances when it may be

appropriate to enter into new GBP LIBOR-linked derivative contracts that expire after the end of

2021, for risk management of existing positions (or exposure resulting from existing contracts, and

to support active conversion). More details are available here.

Further best practice cessation milestones have also been published by regulatory bodies and

industry working groups in advance of LIBOR discontinuation:

• JPY LIBOR – A sub-committee of the Bank of Japan has issued a milestone to ‘cease

initiation of JPY LIBOR referencing interest rate swaps expiring after 2021’ by September

end.

• USD LIBOR – The Federal Reserve Board, the Office of the Comptroller of the Currency,

and the Federal Deposit Insurance Corporation have issued supervisory guidance

encouraging banks to “cease entering into new contracts that use USD LIBOR as a

reference rate as soon as practicable and in any event by December 31, 2021”.

Mizuho expects clients to take these milestones into account when requesting to transact in new

LIBOR-linked linear derivatives with us.

In May 2021 ISDA published Supplement 74 to the 2006 ISDA Definitions for stand-alone overnight

RFR Rate Options for SONIA, SOFR, €STR, TONA, SARON, AONIA, CORRA, HONIA, SORA,

THOR, NZOIA and NOWA and Supplement 75 approaches to compounding/averaging to provide

for new RFR definitions and adopt conventions that more closely match the conventions adopted

by the loan market.

The FCA and £RFR WG are encouraging a broad-based transition to SONIA by the end of 2021

as the primary method to ensure contractual certainty and retain economic control. You can find

further information here and here.

Further information and resources

If you would like any further information, please contact your relationship manager or in relation to

Mizuho Bank, Ltd. email MHBK.IBOR.enquiries@mhcb.co.uk and in relation to Mizuho

International plc email MHI.IBOR.enquiries@uk.mizuho-sc.com.

For further information on the impact of the FCA recent announcement on the cessation of LIBOR

benchmarks, please see the Future Cessation and Non-Representativeness Guidance published

by ISDA.

You can find further information from the USD Alternative Reference Rates Committee (ARCC)

here, the Working Group on Sterling Risk-Free Reference Rates here, the Cross-Industry

Committee on Japanese Yen Interest Rate Benchmarks here and the EURRFR Working Group

here. You can also find publications from the LMA here and from ISDA here.This document has been prepared by Mizuho Bank, Ltd. and Mizuho International plc (together Mizuho) solely for the purpose of supplying information to Mizuho clients. It is not intended for persons who are retail clients within the meaning of the United Kingdom’s Financial Conduct Authority rules nor for persons who are restricted in accordance with US, Japanese or any other applicable securities laws. It must not be distributed, in whole or in part, to any person without the prior consent of Mizuho. This document has been prepared by Mizuho solely from publicly available information. Information contained herein and the data underlying it have been obtained from, or based upon, sources believed by us to be reliable, but no assurance can be given that the information, data or any computations based thereon are accurate or complete. The content of this document is subject to change without notice. We do not accept any obligation to any recipient to update or correct this information. This document is not intended to be investment research and has not been prepared in accordance with requirements to promote the independence of investment research. This document is not independent from Mizuho’s interests. Mizuho may reference benchmarks for internal purposes or in respect of products and transactions which we execute with clients. Any views, opinions or forecasts expressed in this document are not intended to be and should not be viewed as advice or recommendations. It is not and should not be construed as a recommendation or an offer or solicitation to buy or sell any financial instrument or any interest in any financial instrument or enter into any transaction. Mizuho makes no representation and provides no advice in respect of legal, regulatory, tax or accounting matters in any applicable jurisdiction. You should form your own independent judgement and consider seeking your own independent advice (whether legal, financial or other) as to the applicability and relevance of the information contained herein. Mizuho is not responsible for and accepts no liability with respect to the use of this document or of its contents. Mizuho Bank, Ltd., London Branch – Registered office: Mizuho House, 30 Old Bailey, London, EC4M 7AU, Tel: 020 7012 4000. Mizuho Bank, Ltd., London Branch, is authorised by the Prudential Regulation Authority and is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. Details about the extent of our regulation by the Prudential Regulation Authority are available upon request. Mizuho International plc - Registered Office: Mizuho House, 30 Old Bailey, London EC4M 7AU, Tel: 020 7236 1090. Mizuho International plc is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority and is a member of The London Stock Exchange.

You can also read