British Columbia's Montney play - More growth on the way Mark Oberstoetter, Generate 2017 - Clean Energy BC

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

British Columbia’s Montney play More growth on the way Mark Oberstoetter, Generate 2017 Trusted commercial intelligence woodmac.com

Building a competitive advantage

on strong foundations

Over the last 40 years, Wood Mackenzie has

evolved naturally along the energy value chain to

capture all the key components affecting global

markets. We are now a part of Verisk Analytics

(NASDAQ:VRSK).

Our integrated approach allows us to

spot trends and forecast future dynamics

before anyone else

Agenda 1 The high-level. Does the world even want gas anymore? 2 Trends and activity levels in the Montney 3 Forecasting activity by sub-play and operator

Wood Mackenzie’s base case outlook woodmac.com 4

Province-level forecast

BC Montney production surpasses 4.5 bcfd in 2025 and 5.4 bcfd in 2030

British Columbia gas production

6.0 British Columbia - conventional British Columbia - other British Columbia - Montney

5.0

Gas production bcfd

4.0

3.0

2.0

1.0

-

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Source: Wood Mackenzie – North America Gas Service

Wood Mackenzie’s base case outlook woodmac.com 5

Country-level forecast

Alberta’s Montney, Deep Basin and Duvernay contributions add to British Columbia’s

growth

Canada’s gas production

20.0 British Columbia - conventional British Columbia - other Alberta - conventional

Alberta - other Rest of Canada Alberta - Montney

18.0

British Columbia - Montney

16.0

14.0

Gas production bcfd

12.0

10.0

8.0

6.0

4.0

2.0

-

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Source: Wood Mackenzie – North America Gas Service

Wood Mackenzie’s base case outlook woodmac.com 6

North America-level forecast

Lots of competition!

North America gas production

120.0 Other US Lower 48 Marcellus / Utica Haynesville Permian Rest of Canada BC Montney

100.0

Gas production bcfd

80.0

60.0

40.0

20.0

-

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Source: Wood Mackenzie – North America Gas Service

Wood Mackenzie’s base case outlook woodmac.com 7

Together, wind and solar grow more than threefold to 2035

Emerging markets, led by China & India, will see greatest capacity build

World power output by fuel, 2017 – 2035 Global wind & solar capacity growth, 2017 – 35

35,000 2,500

30,000

2,000

25,000

Solar

1,500

20,000

TWh

GW

15,000

1,000

10,000

Wind

500

5,000

0 0

2017 2021 2025 2029 2033 2017 2021 2025 2029 2033

South America South America

Other Renewables Geothermal

Russia and Caspian Russia and Caspian

Solar Wind

North America North America

Other Solid Fuels Hydro

Middle East Middle East

Nuclear Gas

Europe Europe

Oil Coal

Asia Pacific Asia Pacific

Source: Wood Mackenzie Africa Africa

Wood Mackenzie’s base case outlook woodmac.com 8

Renewable costs are falling fast & surprising to the downside

Growth in China’s manufacturing capacity is the critical factor for solar markets

World PV bid prices vs. project size, 2009 – 2017 World solar module production, 2008 - 2016

450 50,000

2008

400 Auctioned capacity (MWdc)

2009

40,000

Average bid price (USD / MWh)

350 China 2016 panel manufacture 50%

greater than rest of world combined 2010

300

Nameplate MWdc

2016 capacity approaching 90,000 MW

30,000 2011

(vs. 50,000 MW production)

250

2012

200

20,000 2013

150

2014

100 10,000

2015

50

2016

0 0

Jul-09 Nov-10 Apr-12 Aug-13 Dec-14 May-16 Sep-17

Source: GTM Researchwoodmac.com 9 Agenda 1 The high-level. Does the world even want gas anymore? 2 Trends and activity levels in the Montney 3 Forecasting activity by sub-play and operator

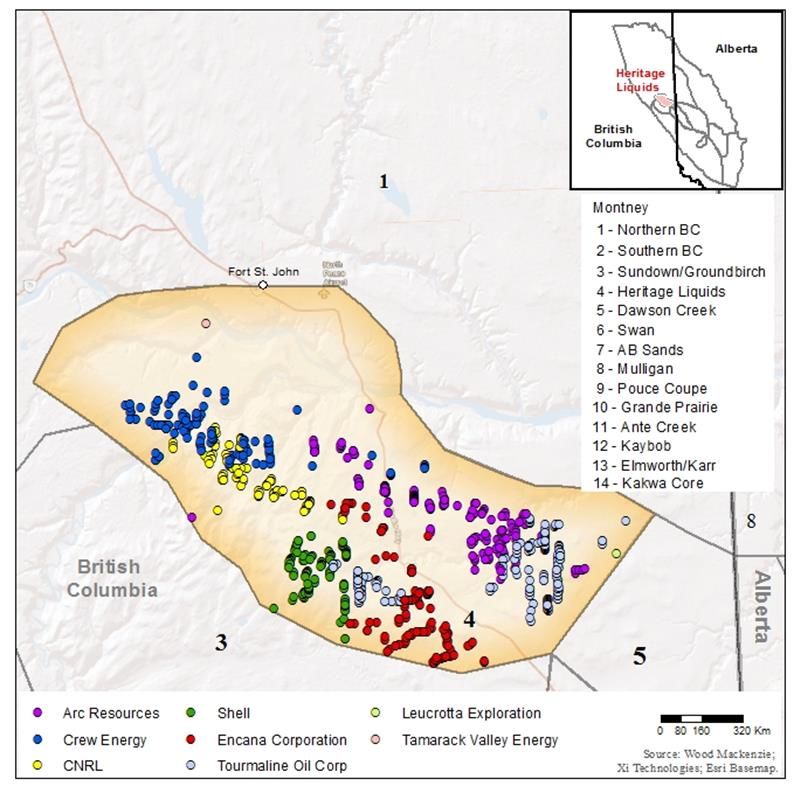

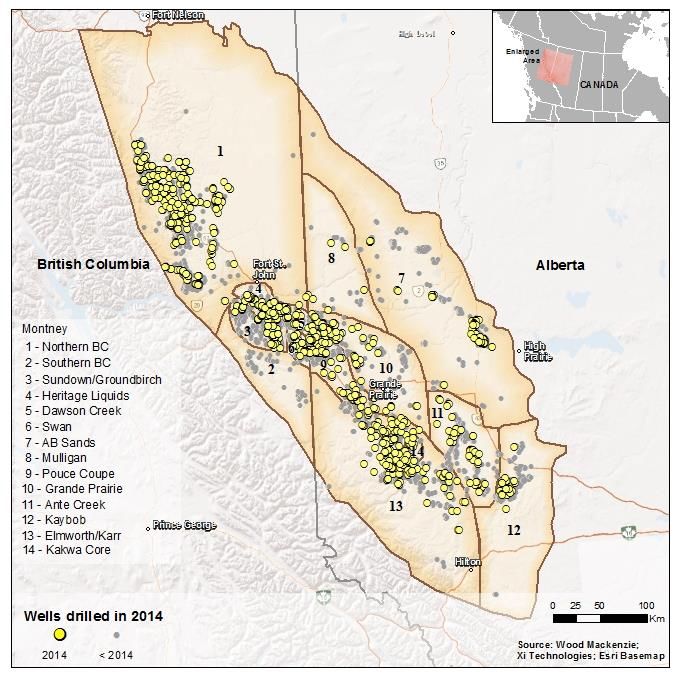

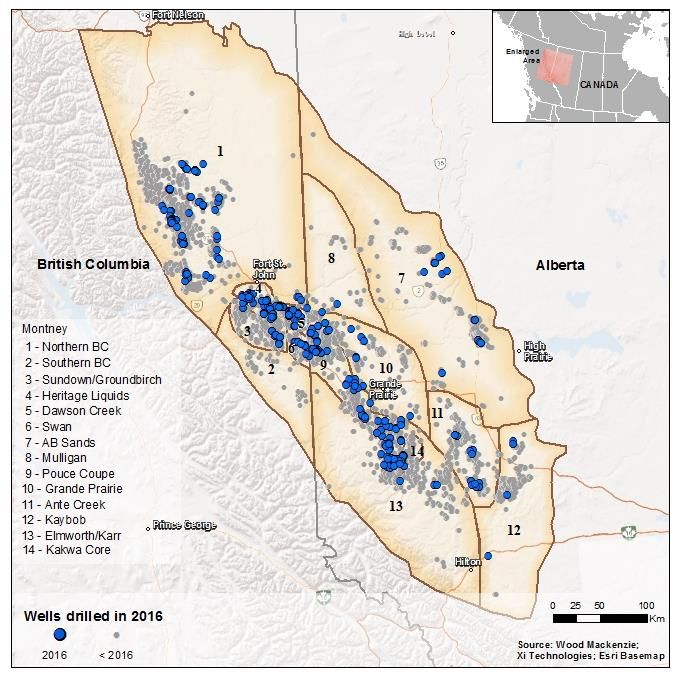

Trends and activity levels in the Montney woodmac.com 10 Montney by vintage year: 2014 vs. 2016 2014 marked the peak of drilling activity thus far, led by Northern BC LNG-aspirants and increased activity due to strong commodity prices 2014 well locations 2016 well locations Source: Wood Mackenzie

Trends and activity levels in the Montney woodmac.com 11 Operators have refined drilling and completion techniques All or a combination of increased proppant placement, longer laterals and a greater number of more targeted frac stages has resulted in significantly improved recoveries

Trends and activity levels in the Montney woodmac.com 12

The trend of longer laterals

Operator preference and geology is responsible for the varying lengths of laterals

Lateral lengths by year

2011 2012 2013 2014 2015 2016

3,500

3,000

Lateral length (metres)

2,500

2,000

1,500

1,000

500

Montney Duvernay

0

Pembina

Dry Gas

Kakwa Core

Dawson Creek

Mulligan

Swan

AB Sands

Northern BC

Southern BC

Pouce Coupe

Kaybob Simonette

Oil

Ante Creek

Grand Prairie

Kaybob

Elmworth/Karr

Sundown Groundbirch

Heritage Liquids

Kaybob West North

Kaybob Fox Creek

Source: Wood MackenzieTrends and activity levels in the Montney woodmac.com 13

Frac stages, the more the better?

Refined completion techniques have seen a marked increase in frac stages per well

Operator reported frac stages per well British Columbia’s top performing wells based

on IP30 rates

2013 2017 Bottom 75% Top 25% Top 10%

100 10,000

Average number of frac stages per well

90 9,000

80 8,000

70

7,000

60

Proppant (tonnes)

6,000

50

5,000

40

30 4,000

20 3,000

10

2,000

0

1,000

-

- 20 40 60 80 100

Number of frac stages

Source: Wood Mackenzie Source: Wood Mackenzie, BCOCG, IPS ranged by mmcfeTrends and activity levels in the Montney woodmac.com 14

Fewer rigs are drilling more productive and cheaper Montney wells

Lowered costs are due to structural shifts in drilling and completion techniques, along with

depressed service costs

Rig counts versus total gas production Movements in well costs since 2012

20 Seven Generations Delphi

80 BC gas production BC rig count 5.0 Cequence Black Swan

Tourmaline Birchcliff (compl. cost only)

18

4.5 Storm Resources

70

Company cited well cost (Cdn$mm)

16

4.0

Average monthly rig count

60

Production (bcfd)

14

3.5

50 12

3.0

10

40 2.5

2.0 8

30

1.5 6

20

1.0 4

10

0.5 2

0 0.0 0

2014

2012

2013

2015

2016

2017

2017

2014

2015

2016

Source: Wood Mackenzie, Nickles RigLocatorTrends and activity levels in the Montney woodmac.com 15

Montney and Deep Basin hold significant low-cost gas resource

At a wellhead breakeven, WCSB production is competitive with the Marcellus and Utica,

but top tier areas lack in repeatability

4.00 Montney Deep Basin Marcellus Utica

Bluesky AB

3.50

Northern wet gas

Local hub breakeven (US $/mmbtu)

Tioga County

3.00

Ohio

Southern wet gas

Southern BC

Lycoming Area Northern BC

2.50

Falher AB

Greene Dry Gas Area Lean Gas SWPA

Dawson Creek BC

WV Rich Gas Northeast PA

2.00 Notikewin AB Sundown Groundbirch BC Lean gas core

Swan BC

Spirit River Tier 1

Kaybob AB Southwest Rich Gas

1.50

Pouce Coupe AB

Bradford Area

Susquehanna Core

1.00

Heritage Liquids BC

Kakwa Core AB

0.50 Grande Prairie AB

Dunvegan AB

Elmworth/Karr AB

0.00

-1,000 1,000 Ante Creek AB 3,000 5,000 7,000 9,000 11,000 13,000

-0.50 Remaining well locations

Source: Wood Mackenziewoodmac.com 16 Agenda 1 The high-level. Does the world even want gas anymore? 2 Trends and activity levels in the Montney 3 Forecasting activity by sub-play and operator

Forecasting activity by sub-play and operator woodmac.com 17

Wood Mackenzie’s Montney sub-plays

NPV split by sub-play

Remaining value split 50/50 between AB and BC

Liquids-rich gas areas including Kakwa Core, Heritage

Liquids and Pouce Coupe hold 53% of remaining value

Northern BC (1),

Kakwa Core (14), Cdn$6.72 bn

Cdn$8.34 bn

Sundown

Groundbirch (3),

Elmworth Karr (13), Cdn$3.87 bn

Cdn$4.54 bn

Kaybob (12),

Cdn$1.14 bn

Ante Creek (11),

Cdn$2.43 bn

Grande Prairie (10), Heritage Liquids

Cdn$2.54 bn (4), Cdn$13.32 bn

Pouce Coupe (9),

Cdn$6.29 bn Dawson Creek (5),

Cdn$0.71 bn

Swan (6),

AB Sands (7),

Cdn$2.48 bn

Cdn$0.49 bn

Southern BC (2), Cdn$0

Mulligan (8), Cdn$0

Source: Wood MackenzieForecasting activity by sub-play and operator woodmac.com 18

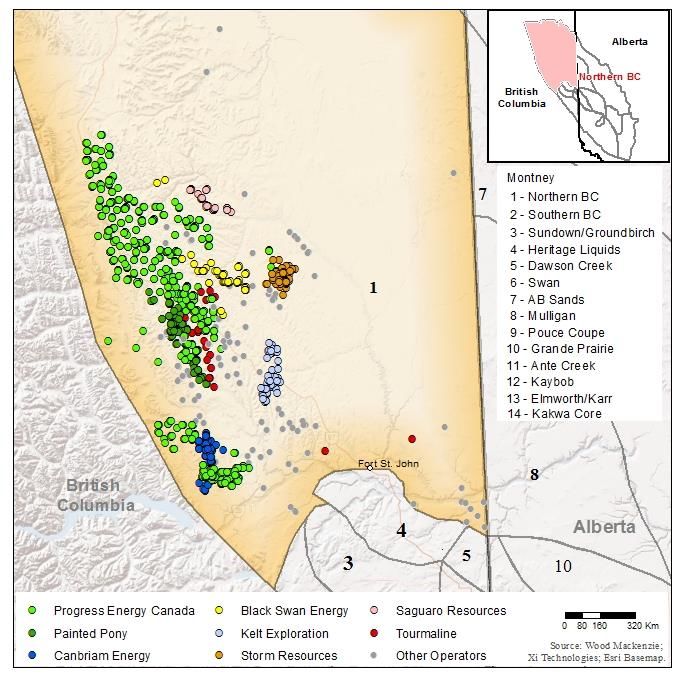

Sub-play area 1 – Northern BC

Activity has shifted from LNG linked drilling to pure-play producers

» Near-term growth driven by investments in processing infrastructure

Gas

Gas Oil/condensate

Oil/condensate NGLs Wells

Wellsdrilled

drilled

5,000

3,000 300

350

(mmcfe/d)

production(mmcfe/d)

4,500

year

2,500 300

250

year

4,000

per

3,500 250

per

2,000 200

drilled

Sub-playproduction

3,000 200

drilled

1,500

2,500 150

Wells

2,000 150

Wells

1,000 100

Sub-play

1,500 100

1,000

500 50

50

500

0 0

2010 2014 2018 2022 2026 2030 2034

mmcfe/d IP Average gas well IP

16 boe/d IP Average oil well IP 1,800

IP30 rate (boe/d)

IP30 rate (mmcfe/d)

14 1,600

12 1,400

10 1,165 1,200

1,000

8

6.5 6.1 800

6 5.9 5.9 5.2 600

4 4.7 4.7 4.5 4.3 4.3 3.5

3.2 400

2

2.8 200

0 0

CNRL

Suncor

Progress

Canbriam

Painted Pony

Crew

Kelt Exploration

Saguaro Res.

Todd Energy

Black Swan

Storm Res.

Chinook Energy

Unconventional

Energy

Res.

Source: Wood Mackenzie, XI TechnologiesForecasting activity by sub-play and operator woodmac.com 19

Sub-play area 4 – Heritage Liquids

High value British Columbia acreage given condensate and NGL yields

» Highest IRR (post-tax) of British Columbia sub-plays at 62%

Gas Oil/condensate NGLs Wells drilled

5,000 300

Sub-play production (mmcfe/d)

4,500

250

Wells drilled per year

4,000

3,500

200

3,000

2,500 150

2,000

100

1,500

1,000

50

500

0 0

2010 2014 2018 2022 2026 2030 2034

86

$4.3

295

EUR (mmboe) Oil

NGL

$21.5

$14.6 Gas

Revenue (C$M))

1,094

Source: Wood Mackenzie, XI TechnologiesForecasting activity by sub-play and operator woodmac.com 20

Over 6,790 wells have been drilled in the Montney since 2013

We forecast over 10,000 more will be drilled in 2018-2026. Four areas stand out –

Northern BC, Heritage Liquids, Kakwa and Pouce Coupe

Sub-play drilling history and forecast

Northern BC (1) Southern BC (2) Sundown Groundbirch (3) Heritage Liquids (4)

Dawson Creek (5) Swan (6) AB Sands (7) Mulligan (8)

1,400 Pouce Coupe (9) Grande Prairie (10) Ante Creek (11) Kaybob (12)

Elmworth Karr (13) Kakwa Core (14)

1,200

1,000

Wells drilled

800

600

400

200

0

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

Source: Wood Mackenzie, XI Technologies. Note this is our Canada Upstream unconstrained outlook, our markets teams take a risked view on these development levels.woodmac.com 21 Disclaimer Strictly Private & Confidential This report has been prepared by Wood Mackenzie Limited. The report is intended solely for the benefit of its subscribers and its contents and conclusions are confidential and may not be disclosed to any other persons or companies without Wood Mackenzie’s prior written permission. The information upon which this report is based has either been supplied to us by public sources or comes from our own experience, knowledge and databases. The opinions expressed in this report are those of Wood Mackenzie. They have been arrived at following careful consideration and enquiry but we do not guarantee their fairness, completeness or accuracy. The opinions, as of this date, are subject to change. We do not accept any liability for your reliance upon them.

Europe +44 131 243 4400 Americas +1 713 470 1600 Asia Pacific +65 6518 0800 Email contactus@woodmac.com Website www.woodmac.com Wood Mackenzie™, a Verisk Analytics business, is a trusted source of commercial intelligence for the world's natural resources sector. We empower clients to make better strategic decisions, providing objective analysis and advice on assets, companies and markets. For more information visit: www.woodmac.com WOOD MACKENZIE is a trade mark of Wood Mackenzie Limited and is the subject of trade mark registrations and/or applications in the European Community, the USA and other countries around the world.

You can also read