Carbon Trading - What Is It & How Does Ag Maximize Its Potential? - Dick Wittman, Farmer/Rancher/Timber Mgr Past President, PNW Direct Seed Assn

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Carbon Trading – What Is It &

How Does Ag Maximize Its

Potential?

Presented at

Commodity Classic Workshop

Ag Coalition on Carbon Trading

2/28/07

Dick Wittman, Farmer/Rancher/Timber Mgr

Past President, PNW Direct Seed Assn

My Background...

Former Ag Lender - FCS

Partner in diversified family farm business

Farm management consultant

Farm Family Transitions and Financial Mgmt

Industry boards/affiliations

Farm Financial Standards Council – Past President

PNW Direct Seed Assn–Founder, Past President

Commodity group and bank boards

Idaho Governors Advisory Committee – Carbon

Sequestration

Environmental Defense – Ag Advisory Committee –

Climate change

Carbon Trading Overview 2

Focus of Presentation

How PNDSA got involved in carbon trading

7 years ago

How Carbon Trading Value is created

How Ag is currently marketing carbon

Players making our markets

Trends in value of carbon credits

Ag Policy framework needed for fair price

and stable trading environment

Key policy issues needing ag definition

Strategy for building “one-voice” consensus

Handouts & PPT Available: www.wittmanconsulting.com

Carbon Trading Overview 3

Quality of Life Mission

Business

Strategic Plan Vision

Structure

“How we do it”

Succession Long Range

Planning Short-term Goals Objectives

In-source Financing Marketing

Out-Source Operating Plan-

Plan “What We Do”

Crop

Production Capital Plan Budget Rotation

Value-

Added Evaluate Action Plans

Strategic KRAs Diversification

Alliances

Environmental

Technology Stewardship

Adoption Tillage Growth

WF Version-Mike Boehlje System

Strategic Thinking Model

Carbon Trading Overview 4

PNDSA Formation

Organized in 1999

Key focus – information exchange

organization – promoting DS adoption

…coincidently, Kyoto process and

concerns about global climate

escalating at same time.

Carbon Trading Overview 5

Pacific Northwest Direct Seed Association

Partners Collaborators

Chem/Fert/Equip Commodity

Promoting economically viable

Companies Groups

and environmentally sound direct

Environmental

seed cropping systems… Educational

Groups Institutions

PNDSA

Public Agencies STEEP III

… through research

Conservation Policymakers

coordination, funding,

Organizations and information

exchange. Global Based

Energy Conservation

Companies Tillage Groups

Washington Idaho Oregon

Carbon Trading Overview 6

Key Events that Drove Carbon

Trading Market Development

Global warming concerns

Kyoto Talks

promoted caps on emissions

Proposed eligible carbon sequestration sinks and

potential for offsets

US vs. other countries’ positions – ag vs. forestry

debate

US approach – Voluntary, not mandated interest

Global trading market in “birthing stage”

New players emerging

Lots of questions re: who will the buyers and sellers

be?

Carbon Trading Overview 7

How We Got Into the Fracas

Contact from ED –

proposal to consider role as an aggregator

ED proposed role as matchmaker

Why they approached us

PNDSA policy supported programs that offered financial

incentives that encourage adoption of DS (EQIP, CSP,

PL566)

Science recognized direct seeding sequesters carbon and

builds Organic Matter

Marketing carbon credits was vehicle for monetizing

conservation benefits from DS

We had captive position with select target that made for

ideal aggregator…it was also an “IDEAL PR sell”

ED mission was to “promote market based solutions” –

didn’t want to aggregate… preferred facilitator role

Carbon Trading Overview 8

Our Learning Process…(2000-02)

Crash course on Carbon Sequestration

1st Committee: Dr Cook, Karl Kupers, Wittman

Waded through technical jungle – ERCs, RMUs,

carbon sinks, saturation, low hanging fruit, etc.

Networked with Other Experts

John Bennett, Saskatchewan Conservation

Tillage Assn, and member of Canadian

team at Kyoto

Don Reicosky, USDA-ARS, Minnesota,

internationally recognized carbon expert

Published informational document for

membership – FAQs & posted on website

Carbon Trading Overview 9

FAQs

What is carbon sequestration?

What is the unit that is traded?

Carbon Sequestration Credits

Emission Reduction Units

How much can be sequestered from

direct seeding?

How is sequestration measured?

Who are potential buyers?

Carbon Trading Overview 10FAQs (cont’d)

What drives value of Offset per T C?

Range $2.50/t US Æ$25-30/T Europe

Kinsella-$29.85Corn; $9.85 Soy; $17.85 Wheat

What are risks of selling credits?

To buyer… & to seller

How does risk impact price of ERUs?

What is duration of proposed sequestration

agreements?

What are advantages of leasing vs. selling?

Carbon Trading Overview 11…let’s start with some basics about

Carbon Sequestration

Carbon Trading Overview 12What is sequestration?

Net result of photosynthesis, plant respiration,

& tillage/residue mgmt/rotation practices

Photosynthesis:

CO2 + nutrients + sunlight + water = O + carbohydrates

Plant respiration:

O + Carbs convert to CO2, water, and energy

Results:

When photosynthesis > respiration

CO2 removed from atmosphere & stored in plant cells

…then we add impacts of tillage, residue mgmt,

rotation diversity

Carbon Trading Overview 13Where does Ag Fit as carbon sink?

4 types of sinks - atmosphere,

terrestrial biosphere (soil & plants),

oceans, and subterranean sediments

Agriculture & forestry sequestration

activity deals with terrestrial

sequestration

Carbon Trading Overview 14Terrestrial Sequestration

• Converting CO2 into biomass

– Increase soil carbon

– Rehabilitate range land

– Grow trees

– Grow microbes

• Cost effective “low hanging

fruit”

24 October 2006Economic Cost Comparisons

• Relative costs of Carbon Sequestration Solutions

– Geologic Price

– Terrestrial

• Aforestation

• Agricultural soils

Geologic

Forestry

Crop soils

Carbon

24 October 2006Why Direct Seeding/NT Getting Attention

as Global Warming Solution? Benefits

Solution to economic and

environmental sustainability:

Sequesters CO2 Æ.5T/acre/yr

Can Ç OM 0.1%/Yr.

Improves air & water quality

Improves wildlife habitat

Lower fossil fuel use

↓ 3.5gal/acre per USDA

Increases economic viability

Solution to global warming

through emission reductions and

carbon sequestration Æ 20-25%

Kyoto goalTillage leads to soil erosion (wind, water) & carbon release

…also causes degradation of air, water and wildlife quality

Å CO2 going into

atmosphere = ↓ OM

Å Habitat is GONE– both above & below ground!M = Mobile

R. = Research

MR. GEM

G = Gas

E = Exchange

M = Machine

Invisible effects of invisible forces!

Carbon Trading Overview 19Tillage + Erosion + Unhealthy Rotations Î 50% Loss Soil Organic Matter

Example: Kansas soils had native organic matter 1-4%

…current levels = 0.5 – 2%

Carbon Trading Overview 20Key Issue to Qualify for Emissions Offsets: ÆMinimal soil disturbance ÆRetention of residue on soil surface

Other Impacts of Reduced

Tillage on CO2 Emissions

Reverse tillage based emissions (3.7 tons of CO2 are released/ton of carbon that

is lost from tillage and erosion).

CO2 emissions lowered by 75% in reduced-tillage farming systems and 93% in

no-till and strip-till systems.

Reduced fuel use (est. 3-5 gal/ac) provides fossil fuel emission reductions

Æreduce 22.38# CO2 emissions/gal saved

Can raise soil organic matter (SOM) by 0.1%/year. Continuous NT/Direct Seed

could reach equilibrium in 15-20 years.

Minimizes breakdown of humus Æ increases water holding capacity and ability

to sustain soil micro-biological activity

Worldwide, 48 million hectares direct seeding at turn of century

Æ results in 134

…estimated we million tons million

need 620 of reduced CO2 per

tonnes year. (Tebrugge)

to meet Kyoto .

Æ NT/DS can solve 1/5 of problem!

QoLEvolution of Carbon Trading

PNDSA Early Experiences – Leasing

Other Early Players across globe

…BEWARE of taking ownership of bragging rights!

Somebody somewhere has done it before!!!

Current Aggregators Active in Ag

Carbon Trading Overview 23Early players in Carbon Trading

Australia/NZ

Major players early on; now almost self-

sufficient in meeting Kyoto protocol

Central & South America –

Numerous grants, small projects to promote

conservation improvement

Canada/US

GEMCO/IGR - 500,000 tons ’99 (priced at $2-

6/Ton…growers netted $.37/T)

Europe

Actively trading emissions credits

Carbon Trading Overview 24PNDSA Strategy - Carbon Trading

Educate first…negotiate deals later!

Key Policy Stance: Lease…don’t

sell…especially until we know what

we’re doing!

Result: Participated in first global

carbon lease arrangement for carbon

credits

Carbon Trading Overview 25Why Lease vs. Sale

Fixed term –

Lease allows seller to put deadline on

liability for performance

Outright sale involves indefinite time

frame to deliver performance obligation

Allows for change in conditions

Lease allows farming practices to change

if conditions warrant

Permanent sale may bind farm to current

management practices

Carbon Trading Overview 26Why Lease vs. Sell? (cont’d)

If measurement shows over time you are

an emitter, may be forced to buy credits to

deliver sequestration benefit sold.

Leasing avoids permanent conservation

easement that could reduce the future

value of the land.

From STEWARDSHIP standpoint, leasing

creates incentive for emitters to fix the

problem…vs. selling buyers a permanent

right to pollute. (Moral high ground!)

Carbon Trading Overview 27Soil Carbon Sequestration: A working contract A LEASE contract between Northwest no- till farmers and a Louisiana energy company, Entergy (4th largest energy co in US)

What the PNDSA desired:

Contract where money actually

changed hands

Cash up front

Lease arrangement

Opportunities and incentives for:

Developing future contracts

Stimulating measurement research

Financial incentives to increase

adoption of DS cropping systems

Carbon Trading Overview 29What Entergy wanted

Get Kyoto ready before mandate

comes in 2008

Long term contract: 10 year

Low price

Emission Reduction Credits in

addition to carbon sequestration

credits

Carbon Trading Overview 30The Process

ED made initial proposal to PNDSA

Agreed on Conceptual Model for lease

arrangement

ED circulated 1-page offer sheet to

potential customers desiring emissions

reductions

Entergy Co – “…let’s make a deal”

“Looking toward tomorrow”

Building an offset forest

Promoting a stewardship image with

constituents

Carbon Trading Overview 31Process (cont’d)

PNDSA developed contract with growers

Definition of DS; requirements and penalties

Eligible acres: DS before 2002; CRP excluded

Grower contracts completed by November

2002

Money transferred to producers through

PNDSA

Annual verifications performed by NRCS

Carbon Trading Overview 32Eligibility & Protocols*

#1 - Must be member of PNDSA

* Acres meet definition of direct seeding

Planting and fertilizing with no prior

tillage to prepare soil

Can be one or two pass

* No burning during lease term

* Pay back feature if tilled before 2012

* If leased acres out of compliance,

could substitute other acreage

Carbon Trading Overview 33What we negotiated

10 yr lease - 3000 tons CO2 credits/year through

direct seed production practices

Total of 30,000 tons (1T CO2/3.67 = T C)

$2.50/ton paid up front => $75,000 total

Annual verification by local Conservation District

employees - visual inspection of direct seed

methodology

Emission reduction credits from reduced fossil fuel

usage in DS

22.38# CO2 reduction/gal diesel saved

Aggregation fee of 20% paid to PNDSA

Contract signed May 2002; started aggregating

credits in September 2002

Carbon Trading Overview 34PNDSA / aggregator contract

with farmers

100 acre maximum @.55ton CO2/acre/year of DS

Designed to give more farmers a chance

Create interest in future contracts

Insure actuarially sound

Total acres to meet contract: 54,500 ac-yrs

Total acres signed up: 6,240ac…113% of min. regmt

1 Acre Example:

6yrs DS x .55T CO2/yr x $2.50/T = $8.25/ac

Grower@$2.00/TÆ$6.60/ac; PNDSA@$.50/TÆ$1.65/ac

Æ Not the money that counts…

Ten year term

Payback criteria if revert back to tillage during term

of contract

Carbon Trading Overview 35Working on New Generation

Contract

Significant expansion in acres –

scoping potential acreage available

Targets: 100-200,000T CO2/yr => 2-400,000ac

Higher values for sequestration

Variable compensation based on

rainfall/rotations

Growers to receive value for fossil fuel

reductions + sequestration

Tougher protocols administration

Scoping other third party verifiers

Compensation for verification

Carbon Trading Overview 36Part II – 3 Basics of Marketing Your

Carbon

Define & measure what we have to sell

Assure a fair price

Assess market supply, demand and equilibrium

price levels

Assure ag access to the market – legislation,

regulation, protocols, and market exchanges

Develop a marketing strategy

Inventory saleable product & get “certified”

Identify viable market outlets

Decide on market timing & price objectives

Execute the plan

Carbon Trading Overview 37Two Different Products to Market

Carbon Sequestration

Emission Reductions

From tillage reductions

From reductions in fossil fuel reductions

Carbon Trading Overview 38Intensive Tillage NT/Direct Seed/Zero Till

Carbon Trade Products Created by Transition to NT/DS:

ÆNet Carbon Sequestered from reduced tillage =

0.55 tons CO2 per acre/year

…doesn’t count benefits to soil, water & habitat quality from

reduced erosion

ÆEmissions eliminated from reduction in fossil fuel consumption

4 gal fuel x 22.38# CO2 ↓/gal saved = 90# Æ .045T CO2/ac/yr

Total Carbon Emission Offsets = .55 + .05 = .60THow do we measure this…

Players active in measurement

CASMGS – 8 Land Grants; K-State (Rice)

2003 Measurement & Monitoring conference

National Soil Tilth Laboratory – Ames, IA

North Central Soil Conservation Research

Laboratory – Morris, MN (Reicosky)

Predictive measurement models

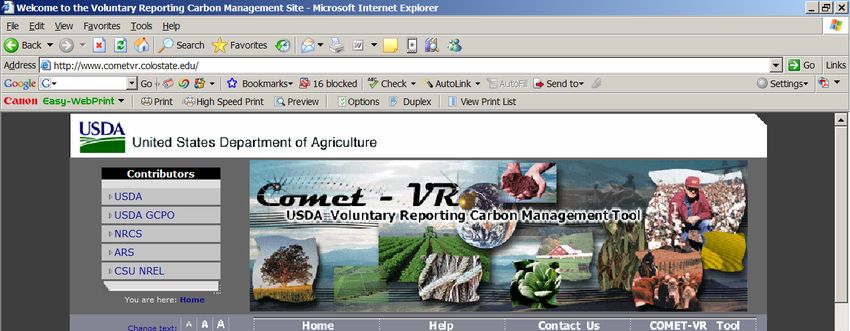

COMET (CENTURY) www.cometvr.colostate.edu/

C-Lock (CENTURY) – So Dakota St.

CROP-SYST ARS-Pullman, WA

SEQUESTER – Pendleton, OR

Other tools: Veris Mapping

Carbon Trading Overview 40Voluntary Reporting Carbon Management Tool COMET-VR (Beta)

Go to | Reset | State | County | Parcel | Soil | Rotation | Tillage | Submit | Summary |

Values are valid for 2005 through 2015 assuming that no change in management occurs.

The default values, or your specified values for soil carbon, may be reported in the 1605(b) system. We recommend that you

print this page and save a copy of this report to a file on your computer system. Use the button "Write File" on the Next

page to save this report.

Top of Form

CASCADE County, Montana Century's Dynamic Carbon Database COMET-VR Summary:

Voluntary Reporting Carbon Management Tool COMET-VR

Carbon Storage Report

Report Year: 2005

Parcel Description Parcel Management History

Parcel Name: Parcel 1 Historic: irrigation (pre 1970's)

Parcel Size: 600 Acres 70's to dryland: spring wheat-mechanical

90's: fallow; No Till Tillage

Location: CASCADE, Montana

Current: CRP, 100% grass; No Till Tillage

Soil: Non-hydric Silt Loam

Report

CRP, 100% grass; No Till Tillage

Period:

Predicted Change in Soil Carbon for the Parcel

Annual Change for 2005

0.15T/Ac

Change in Carbon % Uncertainty

Total Tons Carbon per year: 25 8.87

Total Tons CO2 Equivalent per year: 91 8.87

Values recorded in English units. One ton of carbon is equivalent to 3.664 tons of carbon

dioxide.

Carbon Trading Overview 42

http://www.cometvr.colostate.edu/C-Lock Model Results

Accrued CO2-equivalent offsets and credits summed over each 10-year period of the simulation of three

management scenarios, compared to a BAU case of conventional tillage of a corn-wheat-soybean rotation.

Net credits are the sum of credits and offsets.

1991–2000 2001–2010 2011–2020 2021–2030

Mg CO2 equivalent per hectare

TOTAL

Crop – Reduced Tillage

Offsets 4.8 2.6 3.9 2.3

Credits 2.1 0.1 -1.1 1.1

Net Credits 6.9 2.6 2.8 3.4 15.7

Crop – No Tillage

Offsets 5.5 4.2 6.6 4.9

Credits 12.8 7.9 4.4 6.8

Net Credits 18.2 12.1 11.0 11.7 53.1

CRP

Offsets 5.5 4.2 6.6 4.9

Credits 15.5 17.2 12.6 14.2

Net Credits 21.0 21.4 19.2 19.1 80.7

Source: “C-Lock…” South Dakota School of Mines and Technology, Karen Updegraff et alChallenges with Modeling

Diverse micro-climates

Weather – temperature, rainfall

Soil properties

Diversity of management practices

Rotation

Tillage Practices

Nutrient Management

Historical land use–(requires LT records)

Getting academics/researchers to form

consensus

Carbon Trading Overview 44Potential C Sequestration of

1# C Æ 3.7# CO2

Management Practices

• No-tillage (direct-seeding): 100 to 700

lbs C/ac per year over 10-30 years Å370 - 2,590#/yr

– BUT, dependent on crop rotation,

fertilization

• Returning crop residues and roots: Soil

C gain is proportional to C inputs

– Perennials > annuals; Wheat > peas >

summer fallow

• Perennial grasses (CRP): 500 to 1000

lbs C/ac per year

Å1850 - 3700#/yr

.

.

CT

Model predictions of soil organic C change under

various agricultural systems

Annual increases of 250 to 1000 lbs soil C/ac

.

.At what price should carbon sell?

Using “cost accounting” valuing GHG offsets

Kinsella–value of nutrients; price needed to encourage Ç soil quality

through adoption of NT Æ $75-100/t C

Chuck Rice: N,P,K + H20 in kg humus = $.20

Æ Converts to $1100/ac with 1% SOM @0.6% carbon

Æ If increase SOM 0.1% Æ C is worth $110 value/acre

Legal Costs/Transition Costs - not cheap; give up flexibility in tillage,

rotations, burning, etc.

Using “supply/demand” approach

Demand = function of:

Voluntary vs. mandated trading market

Minimum price = “bottom fruit” selling now to voluntary buyers

Maximum price = What the fine is to sin!;

Level at which Caps are set (i.e. setting lower increases value of credits)

Costs to reduce emissions (i.e. severity of emission taxes or permits

imposed (i.e. $.05 Fuel tax/litre equals $20.15/tonne of carbon.)

Supply: depends on who will be eligible to market

What is best buy: emissions reduction? … or sequestration?

Who is an eligible offset? Ag, Forestry, other GHG reduction projects

How do ag vs non-ag offset projects/practices compete (quality, price)?

Carbon Trading Overview 46$38US

$20US

$11US

$9.50US

$5US

2005-06 Euro vs US dollar

Currency exchange rates:

ÆLow: $1.16

ÆHigh: $1.35MARKET DATA (Click here for

live data)

CCX Carbon Financial Instruments,

2006 RECAP

Summary of trade

Vinta 2006

High Low Close Historic Volume

ge Volume

2003 $5.30 $1.50 $4.10 827,500 1,677,800

2004 $4.90 $1.55 $3.95 825,700 1,889,800

2005 $4.80 $1.55 $4.05 966,100 2,310,600

2006 $4.75 $1.60 $4.00 1,326,000 2,299,800

2007 $5.00 $3.00 $3.75 1,523,600 1,523,600

2008 $4.65 $3.00 $3.75 1,520,200 1,520,200

2009 $4.60 $3.10 $3.75 1,590,300 1,590,300

2010 $4.60 $3.10 $4.00 1,707,000 1,707,000

14,519,100

10,316,40 Price Units: Per metric ton of CO2

Totals

0 Volume Units: metric tons of CO2

Source: Iowa Farm Bureau websiteWhere can you sell your carbon?

Direct Sale Aggregators

Direct Sellers: PNDSA

Aggregate/re-sell: CCX, GEMCO/IGF

X-Chg Aggregators (a growing list…)

Illinois Conservation and Climate Initiative

Iowa Farm Bureau

National Carbon Offset Coalition

National Farmers Union

Northern Plains Environmental, Inc

Others

Foreign Markets ???

Carbon Trading Overview 49Contract Protocols - Key Issue for

Offsets to be Validated

CCX traded contracts

CCX developed protocols working with

aggregators

Emissions standards: 1605 compliance

Sequestration standards: still “work-in-progress”

Direct Sale contracts

What ever the buyer & seller agree upon

Issue: Will existing protocols be recognized

by state, national, international bodies if:

cap & trade is passed

rules are legislated for what constitutes eligible

offsets

Carbon Trading Overview 50Common Protocols – NT/DS

Member of aggregating entity

Practices comply with DS/NT/ST

definitions

NRCS 329 standards – Beware of the

devil in the details (Definition of NT/DS)

No burning or residue removal

Substitutability

1605(B) – covers emissions side…

doesn’t address sequestration projects

Carbon Trading Overview 51Protocol – Considerations

Rate of carbon sequestration

Volatility – ability to withstand

environmental disasters (fire, insects,

disease, floods)

Permanence

Leakage

Additionality

Predictability

Conversion to other sink forms

Net emissions/sequestration balance – CO2

emitted to generation CO2 seq. project

Carbon Trading Overview 52Quality Measurements / Standards

Gold Standard – branding,

certification process (Duke University)

King formula – quality measure

“Carbon Credited” Brands program -

maps carbon footprint – Michael

Kiely, Australia)

Carbon Trading Overview 53$$$ at Stake

Producers – value added revenue source

86mm acres corn

57mm acres wheat

CRP; forests

Grasslands, methane capture, renewable fuels

Aggregators - service to members/profit

Revenue source 10-20% of offset value

Administrative Cost

Emitters – looking for offsets to meet caps

Looking for least cost/highest quality

Buying time until can improve efficiency

Carbon Trading Overview 54Illustrative Ranking of Carbon as a Crop in U.S.

Per Proposed GHG Limits in

Senate Bill 280 (Lieberman-McCain) 1/12/07

Carbon at $10/MT CO2e,

25

Production Value ($B)

20

15

10

5

0

orn

s

ON

nes

to

ns

ns

s

hay

pes

ton

es

s

eat

es

rice

es

uce

ond

nge

oat

ma

ato

cuk

bea

bea

dat

in c

wh

tari

gra

cot

RB

lett

alm

ora

h to

pot

soy

gra

CA

nec

fres

[Crop Source: USDA - National Agricultural Statistics Service – US Crop 55

Rankings - 1997 Production Year Ranking Based on Value of Production]Marketing Question: Sell now…or

wait?

Issues

Climate change legislation/regulation?

How position farm to maximize value?

How long will game be in town?

Getting “carbon credited” – Be Ready!

Inventory offsets available to market

Do it yourself? …or Hire experts? (i.e. “Carbon

Credited” Brands program, mapping carbon footprint –

Michael Kiely, Australia)

Big Question: will “stamped” projects and

offsets bring premiums or better market access?

Carbon Trading Overview 56Part III – Defining an Ag Policy Framework

– Underpinning Access to Carbon Market

Issues where Ag

needs to weigh in

Strategies for

building consensus

Caution: Be sensitive

to constituents who

don’t get to play

Carbon Trading Overview 5710 Policy Issues – Carbon Trading

Cap and trade federal legislation

Limits on Agriculture as eligible

carbon sink/emissions offset

U S position on national/international

protocols limiting emissions

Eligibility to market emissions

reductions as well as sequestration

credits

Where should baselines be set?

Carbon Trading Overview 58Issues (cont’d)

Financial additionality – eligibility to

receive compensation from multiple

parties for same practices

Research funding for terrestrial

sequestration

Fixing value of carbon legislatively

Establishing state/federal protocols

Preferred role of USDA in carbon

trading

Carbon Trading Overview 59The “Carbon bus has left…are we on

the bus, or running to catch up?”

Megafirms pushing for 10-30%

emissions reduction next 15 yrs

(utilities, manufacturing,

chemicals, financial services,

environmental groups)

Buyers coming… Example:

10 MMT offsets (5 utilities)

Æ 4mm NT acres for 5 years

6 bills in hopper to regulate

climate, carbon…& counting

ÆCan agriculture say where we

stand?

Carbon Trading Overview 60Strategy for Resolving Policy

Debates

Form collaborative effort across all

commodity and conservation groups

Formalize networks/communication

with select environmental groups who

share common goals with agriculture

Carbon Trading Overview 61Threats from inaction & ignorance

Ag will have no say in policy formulation

Mandated caps on price of carbon

Producers will sell carbon credits too cheap

Existing contracts could lose value due to

measurement rules

Ag sector could be penalized for emissions*

State regulations lock Ag sector out of

marketing carbon-friendly practices (CA)

Non-US competitors imposing opinions on

what we should do

Carbon Trading Overview 62Examples: Daily threats & attitude shifts

“Agriculture sector should be penalized for GHG

emissions…farmers and livestock breeders that produce

excess greenhouse gas emissions should be punished for

their negative impact on the environment.” U K Environment

Secretary, David Miliband – Oxford Farming Conference, Greenwire, January 4, 2007

“Companies that see climate change coming, recognize it for

what it is, do the relevant R&D and inculcate a positive

attitude to change …do very well. A company that

doesn’t believe it and doesn’t encourage it managers to

take it seriously is going to get rolled over.” John Llewellyn,

Lehman Bros as quoted in Financial Times 2-1-07 re: Exxon shifting its position on climate

change.

“…some large, rich countries still must be convinced…they

are refusing to accept the consequences of their acts.”

French President Jacques Chirac comments referring to the U. S., one of 113 nations who

approved the release of Intergovernmental Panel on Climate Change report.

Carbon Trading Overview 63Information Sources

Climate Information

Carbon Trading Information Overload!!!

Experts

Aggregators

Trading Exchanges

Conservation

Organizations

See Handouts

Surf the web

sources…follow the

Linkages

Carbon Trading Overview 64Great source – Links to climate reports

Information Sources

Great Linkages… Æ Climate change Æ Cons Organizations

Summary “The so-called and long-overstated debate about global warming is over.

It’s time now to hear from the world’s policymakers.” Tim Wirth, President, United Nations Foundation

Time for change in agriculture’s image re: climate impact

Traditionally: seen as part of problem

Opportunity ahead: be key part of solution

Be at the table: …”if don’t will be on menu” (Sara)

Identify, engage & agree on carbon trading policy issues

Engage in protocol definitions; keep them simple

RE: Marketing Carbon

Insure producers are EDUCATED before

selling…experimenting with small acreage is good tool

Understand opportunities & risks; be prepared to deliver

benefits we contract to sell

Encourage professional marketing approach

Assess what have to sell; don’t sell too cheap; beware of

snake oil salesmen “picking the bottom fruit”

Carbon Trading Overview 68Time for Questions...

Carbon Trading Overview 69You can also read