Stronger-for-longer Oil Thesis Holds, But Canadian Diffs Will Remain Challenging - Real Estate Forums

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Stronger-for-longer Oil Thesis Holds, But

Canadian Diffs Will Remain Challenging

The Global Crude Markets Continue To Look Positive, But

Canada Has Real Headwinds That Shouldn’t Be Overlooked

CIBC Capital Markets October 2018

Jon Morrison | +1 403 216 3400 | jon.morrison@cibc.com

FOR INSTITUTIONAL CLIENT USE ONLY. NOT FOR GENERAL DISTRIBUTION.

See "Important Disclosures" section at the end of this report for important required disclosures, including potential conflicts of interest.

See "Price Target Calculation" and "Key Risks to Price Target" sections at the end of this report, or at the end of each section thereof, where applicable.

Presentation Overview A Breakdown Of What Is Included In This Deck • The Global Crude Picture: A Look At Balances (Pages 3-24) • Battle Of The Barrels: A Look At Canada’s Unique Headwinds (Pages 25 – 33) − Canadian Supply/Demand: WCSB Production Versus Pipeline, Refinery And Rail Capacity (Page 30) − Crude By Rail: A Look At The CBR Loadings Needed To Clear The Market (Page 31) • IMO 2020: Road To Perdition? (Pages 34 - 37)

Macro Commodity Outlook – Crude

Crude – The Price Action Reflects Physical Realities…

WTI Strip Pricing (Past 52 Weeks)

• The last year has been an $80

interesting time for the global $75

crude markets. $70

NYMEX WTI Futures Price (US$/Bbl)

• Despite some negative data points $65

surrounding various macro events, $60

the oil tape has largely ascended $55

higher with each passing month $50

and is showing ongoing support in $45

Last Week (10/4/18)

Current Week (10/11/18)

the front-month price. $40 High (Last Week (10/4/18))

Low (10/12/17)

• The back-end of the curve has also $35

1-Oct-17 1-Mar-18 1-Aug-18 1-Jan-19 1-Jun-19 1-Nov-19 1-Apr-20 1-Sep-20 1-Feb-21 1-Jul-21

lifted and the backwardation in

the structure has been a positive Brent Strip Pricing (Past 52 Weeks)

sign of near-term tightness. $95

• December WTI barrels are trading

in the low US$70s, while Brent is $85

ICE Brent Futures Price (US$/Bbl)

in the low US$80s. As such, the

$75

price action continues to reflect

the ongoing acute tightening in $65

the physical market that we have

been emphasizing since H1/17. $55

Last Week (10/4/18)

Source: Bloomberg and CIBC World Markets Inc. $45 High (Last Week (10/4/18))

Low (10/12/17)

Current Week (10/11/18) 2

$35

1-Oct-17 1-Mar-18 1-Aug-18 1-Jan-19 1-Jun-19 1-Nov-19 1-Apr-20 1-Sep-20 1-Feb-21 1-Jul-21

The Global Crude Picture: A Look At Balances

Macro Commodity Outlook – Crude

A Look At Balances

• As we have said for the past

year, the market is tight. In fact, 103.0 2.3

acutely so. 101.0 1.9

• The chart on the right highlights 1.5

99.0

forecasted global oil/liquids

balances. 97.0

1.1

• Although we would typically see 0.7

95.0

an inventory build in the first

0.3

quarter due to seasonal

MMBbl/d

MMBbl/d 93.0

transportation demand and -0.2

refinery turnarounds, that failed 91.0

-0.6

to materialize in Q1/18 due to

89.0

the current undersupply -1.0

situation. 87.0 -1.4

• This left the market as arguably

85.0 -1.8

being 300-500 MBbl/d tighter

Q1 2010

Q2 2010

Q3 2010

Q4 2010

Q1 2011

Q2 2011

Q3 2011

Q4 2011

Q1 2012

Q2 2012

Q3 2012

Q4 2012

Q1 2013

Q2 2013

Q3 2013

Q4 2013

Q1 2014

Q2 2014

Q3 2014

Q4 2014

Q1 2015

Q2 2015

Q3 2015

Q4 2015

Q1 2016

Q2 2016

Q3 2016

Q4 2016

Q1 2017

Q2 2017

Q3 2017

Q4 2017

Q1 2018

Q2 2018

Q3 2018E

Q4 2018E

Q1 2019E

Q2 2019E

Q3 2019E

Q4 2019E

than where consensus

expectations sat at the start of Implied stock change and balance (right axis) (MMBbl/d)

the year. World production (left axis) (MMBbl/d)

World consumption (left axis) (MMBbl/d)

Source: Bloomberg and CIBC World Markets Inc.

4

Macro Commodity Outlook – Crude

OPEC Spare Capacity

• Right now OPEC has ~2.0 MMBbl/d of spare

capacity, which is defined as production

5.5%

that can come online within a month and be

delivered for upwards of a year. 5.0%

OPEC Spare Capacity, As A % Of Global Supply

• With that said, if Saudi Arabia needed to 4.5%

add another 1.0-2.0 MMBbl/d of output to 4.0%

the global market on a sustained basis, we

3.5%

believe it would require a 3-5 year

investment cycle and likely represent more 3.0%

capital than the KSA would like to be 2.5%

deploying at this stage.

2.0%

• In addition, spare capacity is typically

1.5%

tapped in times of unexpected outages and

is unlikely to want to massively draw on this 1.0%

reserve supply just yet. In fact, if Saudi 0.5%

Arabia added ~650 MBbl/d of supply to the

0.0%

global market through Q1/19, it would take

2Q18E

3Q18E

4Q18E

1Q19E

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

3Q17

4Q17

1Q18

OPEC spare capacity as a % of global

production to

Macro Commodity Outlook – Crude

Texas Output Will Remain Constrained Until H2/19

• The Midland differential

continues to be volatile and will

$5

widen back out if output is

increased in any marked way $0

before takeaway capacity

comes online. -$5

• Given this, we view there to be -$10

the potential to see Permian

US$/Bbl

activity levels contract in the -$15

coming months as there

continues to be immense -$20

congestion in crude and gas

-$25

takeaway capacity out of West

Texas/New Mexico and that -$30

isn’t likely to change until

Jan-13

Jan-14

Jan-15

Jan-16

Jan-17

Jan-18

Jul-13

Jul-14

Jul-15

Jul-16

Jul-17

Jul-18

H2/19.

• Thus, the Permian will add WTI Midland - WTI Cushing Diff WTI Midland - Gulf Coast Diff

material growth in the next 3-5

Source: Bloomberg and CIBC World Markets Inc.

years, but incremental adds

within 12 months will be more

muted.

6Macro Commodity Outlook – Crude

Texas Output Will Remain Constrained Until H2/19

8,000

7,000

6,000

5,000

MBbl/d

4,000

3,000

2,000

1,000

0

Q1/18 Q2/18 Q3/18 Q4/18 Q1/19 Q2/19 Q3/19 Q4/19 Q1/20 Q2/20 Q3/20 Q4/20 2021E 2022E 2023E 2024E 2025E

Permian Gulf Coast ("PGC") Pipeline EPD NGL Conversion Jupiter

Gray Oak Expansion EPIC pipeline Cactus II

Permian Express III phase 1 Sunrise Expansion BridgeTex Expansion

Rail Existing Pipelines Capacity Local Refinery Demand

Permian Crude Production Forecast

Source: Company reports, EIA, IEA, Bloomberg and CIBC World Markets Inc.

7Macro Commodity Outlook – Crude

200

US Crude + Product Inventories (MMBbl)

150

100

50

0

(50)

(100)

(150)

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

10 Year Range 10 Year Average 2016 2017 2018

• The above chart highlights the acute market tightening that we have been empathizing since last April as

it shows the relative changes in U.S. petroleum inventories, including crude and products.

• As can be seen, upwards of 80 MMBbls of total petroleum inventories have now been pulled from U.S.

storage tanks since the start of 2017 and U.S. crude inventories are now below the five-year average.

• In addition, absent the large build in product inventories over the past six weeks due to robust refinery

runs, we have seen a relentless draw across the petroleum complex for nearly two years.

Source: Bloomberg and CIBC World Markets Inc.

8Macro Commodity Outlook – Crude

Crude – U.S. Inventory Levels Are Now Healthy…

U.S. Crude Inventories U.S. Gasoline Inventories

550,000 270,000

500,000 260,000

250,000

450,000 240,000

(000s) Bbl

(000s) Bbl

230,000

400,000

220,000

350,000 210,000

200,000

300,000

190,000

250,000 180,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

5-Yr Hi-Lo Range 2013-2017 Avg. 2016 2017 2018 5-Yr Hi-Lo Range 2013-2017 Avg. 2016 2017 2018

U.S. Distillate Inventories U.S. Jet Kerosene Inventories

200,000 55,000

180,000 50,000

160,000

45,000

(000s) Bbl

(000s) Bbl

140,000

40,000

120,000

35,000

100,000

80,000 30,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

5-Yr Hi-Lo Range 2013-2017 Avg. 2016 2017 2018 5-Yr Hi-Lo Range 2013-2017 Avg. 2016 2017 2018

Source: EIA and CIBC World Markets Inc.

9Macro Commodity Outlook

… And Look Even More Positive When Looking At Days Of Demand Cover

U.S. Gasoline Days Inventory U.S. Distillate Days Inventory

33 55

5-Yr Hi-Lo Range 5-Yr Hi-Lo Range

5 Yr Avg 5 Yr Avg

2018 2018

2017 50 2017

31 2016 2016

2015 2015

45

29

40

Days

Days

27

35

25

30

23

25

21 20

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

U.S. Crude Oil Days Inventory

37

5-Yr Hi-Lo Range

5 Yr Avg

35 2018

2017

2016

33 2015

31

29

Days

27

25

23

21

19

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Source: Bloomberg, EIA and CIBC World Markets Inc.

10Macro Commodity Outlook

Crude – OECD Inventory Levels Are Also Moving In The Right Direction…

OECD Industry Crude Oil Inventories OECD Gasoline Inventories

1,350 430

5 Yr Range 5 Yr Range

5 Yr Avg. 5 Yr Avg.

1,300 2018 420 2018

2017 2017

2016 2016

1,250 2015 410 2015

1,200 400

1,150 390

MMBbl

MMBbl

1,100 380

1,050 370

1,000 360

950 350

900 340

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

OECD Industry and Government Crude Inventories OECD Distillate Inventories

2,600 700

5 Yr Range 5 Yr Range

5 Yr Avg. 5 Yr Avg.

2,550 2018 2018

2017 2017

2016 650 2016

2015 2015

2,500

2,450

600

MMBbl

MMBbl

2,400

550

2,350

2,300

500

2,250

2,200 450

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Source: IEA and CIBC World Markets Inc.

11Macro Commodity Outlook

… And Also Look Even More Positive When Looking At Days Of Demand Cover

OECD - Crude Oil Inventories Over Daily Demand OECD - Motor Gasoline Inventories Over Daily Demand

28 31

5-Yr Range

5-Yr Avg.

27 2018

30

2017

26 2016

29 2015

25

28

24

Days

Days

23 27

22

26

21

5-Yr Range 25

20 5-Yr Avg.

2018

2017 24

19

2016

2015

18 23

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

OECD - Distillate Inventories Over Gasoil/Diesel Daily Demand

49

47

45

43

Days

41

39

5-Yr Range

37 5-Yr Avg.

2018

2017

2016

35

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Source: IEA and CIBC World Markets Inc.

12Source: IEA

Lower 48 Weekly Oil Production (MBbl/d)

7,500

8,000

8,500

9,000

9,500

10,000

10,500

11,000

Jan-15

Feb-15

Mar-15

Apr-15

May-15

Jun-15

Jul-15

Aug-15

Sep-15

Oct-15

Nov-15

Macro Commodity Outlook – Crude

Dec-15

Jan-16

Feb-16

But U.S. Supply Is Returning To Growth…

Mar-16

Apr-16

May-16

Jun-16

Jul-16

Aug-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

May-17

Jun-17

Jul-17

Aug-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

Apr-18

May-18

Jun-18

Jul-18

Aug-18

Sep-18

Oct-18

• To be clear, U.S. crude production has material growth potential, but it will be bottlenecked until H2/19.

13Macro Commodity Outlook – Crude

… But U.S. Decline Rates Are Relevant And Will Continue To Limit Some Of The Unfettered Growth

• The trailing U.S. base

decline rate has

accelerated modestly in

the past year, but

continues to sit >30%.

• Tight oil production from

the U.S. Bakken, Eagle

Ford, Niobrara and

Permian plays are the core

drivers behind this

accelerating decline curve.

• And, we continue to be of

the view that it is a low-

case probability that the

entirety of ongoing global

decline rates and rising

global oil demand can be

satisfied solely through

short-cycle U.S. shale

growth.

Source: IHS and CIBC World Markets Inc.

14Macro Commodity Outlook – Crude

Permian Update IP 90 By Month On-Production

700 5.0

Cal Day Production (All Products; Boe/d)

Gas (Boe/d) 4.5

600 Oil (Bbl/d) 4.0

500 GOR (Mcf/Bbl) 3.5

GOR (Mcf/Bbl)

400 3.0

2.5

300 2.0

200 1.5

1.0

100

• Permian well 0.5

results continue to 0 0.0

Oct-13

Oct-14

Oct-15

Oct-16

Oct-17

Jan-13

Apr-13

Jul-13

Jan-14

Apr-14

Jul-14

Jan-15

Apr-15

Jul-15

Jan-16

Apr-16

Jul-16

Jan-17

Apr-17

Jul-17

improve when one

looks at just the Month On Prod

straight peak IPs,

IP 365 By Month On-Production

IP90s, IP180s and

500 5.0

IP365s.

Cal Day Production (All Products; Boe/d)

450 Gas (Boe/d) 4.5

400 Oil (Bbl/d) 4.0

350 GOR (Mcf/Bbl) 3.5

GOR (Mcf/Bbl)

300 3.0

250 2.5

200 2.0

150 1.5

100 1.0

50 0.5

0 0.0

Oct-13

Oct-14

Oct-15

Oct-16

Jan-13

Apr-13

Jul-13

Jan-14

Apr-14

Jul-14

Jan-15

Apr-15

Jul-15

Jan-16

Apr-16

Jul-16

Jan-17

Source: IHS and CIBC World Markets Inc.

Month On Prod

15Macro Commodity Outlook – Crude

Permian Update

IP 365 By Month On-Production (Normalized by Completion Length)

300

Gas (Boe/d per 1000 meters)

Cal Day Production (All Products; Boe/d)

250 Oil (Bbl/d per 1000 meters)

• But the positive Rolling 6 Month Average

rate of change 200

diminishes once

one normalizes 150

for completion

length. 100

50

0

Jan-13

Jan-14

Jan-15

Jan-16

Jan-17

Jul-13

Jul-14

Jul-15

Jul-16

May-13

May-14

May-15

May-16

Mar-13

Sep-13

Nov-13

Mar-14

Sep-14

Nov-14

Mar-15

Sep-15

Nov-15

Mar-16

Sep-16

Nov-16

Month On Prod

Source: IHS and CIBC World Markets Inc.

16Macro Commodity Outlook – Crude

Permian Update

IP 365 By Month On-Production (Normalized by Proppant Intensity)

140

Cal Day Production (All Products; Boe/d)

120

• It diminishes 100

further if one

normalizes for 80

proppant loadings.

60

• In fact, IP365s are

slipping once 40 Gas (Boe/d per 1000 tons)

normalizing for

Oil (Bbl/d per 1000 tons)

well size/proppant 20

loadings. Rolling 6 Month Average

0

Jan-13

Jan-14

Jan-15

Jan-16

Jan-17

Mar-13

May-13

Jul-13

Mar-14

May-14

Jul-14

Mar-15

May-15

Jul-15

Mar-16

May-16

Jul-16

Sep-13

Sep-14

Sep-15

Sep-16

Nov-13

Nov-14

Nov-15

Nov-16

Month On Prod

Source: IHS and CIBC World Markets Inc.

17Macro Commodity Outlook – Crude

Eagle Ford Update IP 90 By Month On-Production

700 5.0

Gas (Boe/d) 4.5

Cal Day Production (All Products; Boe/d)

600

Oil (Bbl/d)

4.0

500 GOR (Mcf/Bbl)

3.5

GOR (Mcf/Bbl)

3.0

400

2.5

300

2.0

200 1.5

1.0

• Eagle Ford well 100

0.5

results also 0 0.0

Jan-13

Apr-13

Jul-13

Oct-13

Jan-14

Apr-14

Jul-14

Oct-14

Jan-15

Apr-15

Jul-15

Oct-15

Jan-16

Apr-16

Jul-16

Oct-16

Jan-17

Apr-17

Jul-17

Oct-17

continue to

improve when one Month On Prod

looks at just the IP 365 By Month On-Production

straight peak IPs, 500 5.0

IP90s, IP180s and 450 Gas (Boe/d) 4.5

Cal Day Production (All Products; Boe/d)

IP365s. 400

Oil (Bbl/d)

4.0

GOR (Mcf/Bbl)

350 3.5

GOR (Mcf/Bbl)

300 3.0

250 2.5

200 2.0

150 1.5

100 1.0

50 0.5

0 0.0

Source: IHS and CIBC World Markets Inc.

Jan-13

Jan-14

Jan-15

Jan-16

Jan-17

Apr-13

Jul-13

Apr-14

Jul-14

Apr-15

Jul-15

Apr-16

Jul-16

Oct-13

Oct-14

Oct-15

Oct-16

Month On Prod

18Macro Commodity Outlook – Crude

Eagle Ford Update

IP 365 By Month On-Production (Normalized by Completion Length)

300

Gas (Boe/d per 1000 meters)

Cal Day Production (All Products; Boe/d)

250 Oil (Bbl/d per 1000 meters)

Rolling 6 Month Average

• But the positive

rate of change 200

diminishes once

one normalizes 150

for completion

length.

100

50

0

May-13

May-14

May-15

May-16

Jul-13

Nov-13

Jul-14

Nov-14

Jul-15

Nov-15

Jul-16

Nov-16

Jan-13

Jan-14

Jan-15

Jan-16

Jan-17

Mar-13

Mar-14

Mar-15

Mar-16

Sep-13

Sep-14

Sep-15

Sep-16

Month On Prod

Source: IHS and CIBC World Markets Inc.

19Macro Commodity Outlook – Crude

Eagle Ford Update

IP 365 By Month On-Production (Normalized by Proppant Intensity)

140

Cal Day Production (All Products; Boe/d)

120

• It diminishes 100

further if one

normalizes for 80

proppant loadings.

60

• In fact, IP365s are

slipping once

40 Gas (Boe/d per 1000 tons)

normalizing for

well size/proppant Oil (Bbl/d per 1000 tons)

20

loadings. Rolling 6 Month Average

0

Jul-13

Jul-14

Jul-15

Jul-16

Jan-13

Jan-14

Jan-15

Jan-16

Jan-17

May-13

May-14

May-15

May-16

Sep-13

Nov-13

Sep-14

Nov-14

Sep-15

Nov-15

Sep-16

Nov-16

Mar-13

Mar-14

Mar-15

Mar-16

Month On Prod

Source: IHS and CIBC World Markets Inc.

20Macro Commodity Outlook – Crude

Outside Of The U.S. There Are Few Other Supply Growth Markets Expected In 2018 - 2020

$35.0

Canada $30.0

WCSB Oil Sands Capital Spending ($ Billions)

• Canadian oil sands spending declined for the third $25.0

consecutive year in 2017, with total annual capex $20.0

expected to be down nearly 60% from the 2014

peak. $15.0

$10.0

• Although there were eight projects sanctioned in

2016, this was materially below the recent $5.0

annual growth trend. $0.0

2017E

2018E

2019E

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Brazil 2,800,000

2,600,000

• Following three years of robust production adds

Brazilian Crude Production (Bbl/d)

2,400,000

from pre-salt development, Brazil’s growth is 2,200,000

likely to stall out in 2018 with 10% Y/Y and forward development 1,000,000

plans require greater capital spending, which

will be a challenge for Petrobras given its tight

balance sheet and debt repayment plans.

Source: CAPP, PSAC, IHS, ANP, company reports and CIBC World Markets Inc.

21Macro Commodity Outlook – Crude

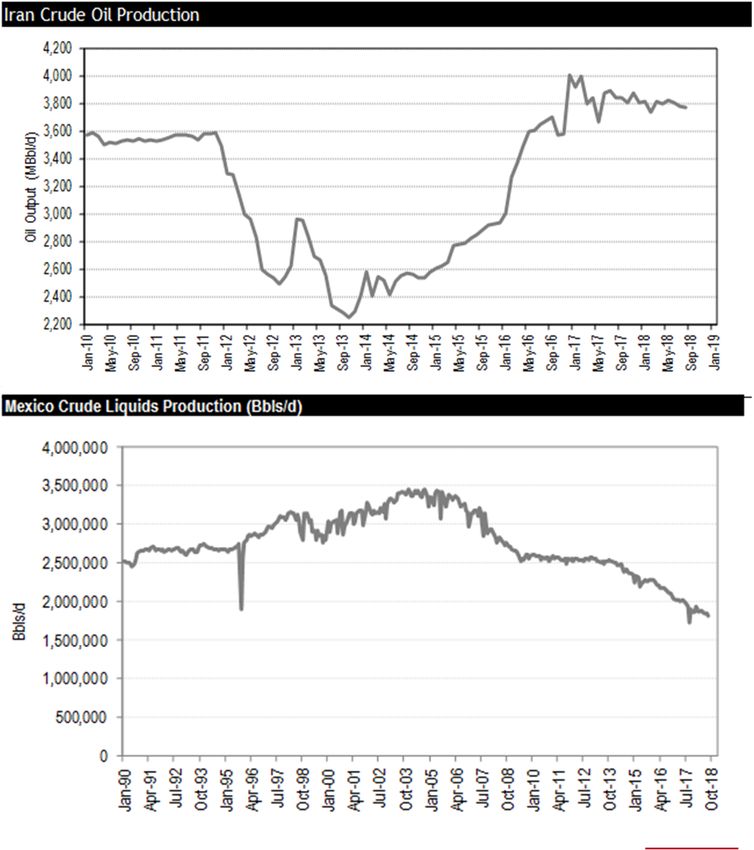

Crude – Other Key Global Supply Markets

• Iran: Iran has shown material growth since

the original sanctions have been lifted,

but the country needs material

investments to continue its growth.

• Specifically, there are critical investments

needed in energy infrastructure and

oilfield services capacity - both of which

are challenged in the current macro

environment and further handicapped by

the current U.S. Administration.

Incremental U.S. sanctions only

deteriorate this outlook.

• Mexico: Production continues to fade

every month, with base spending and

activity levels being materially below the

level needed to have flat output.

• Other Offshore Mega Projects Are

Largely Shelved: GoM is completing the

last major project sanctions. North Sea is

fairly lethargic outside UK maintenance

work and offshore Africa is largely at a

standstill.

22

Source: Energy Intelligence and PemexMacro Commodity Outlook – Crude

Other Key Global Supply Markets

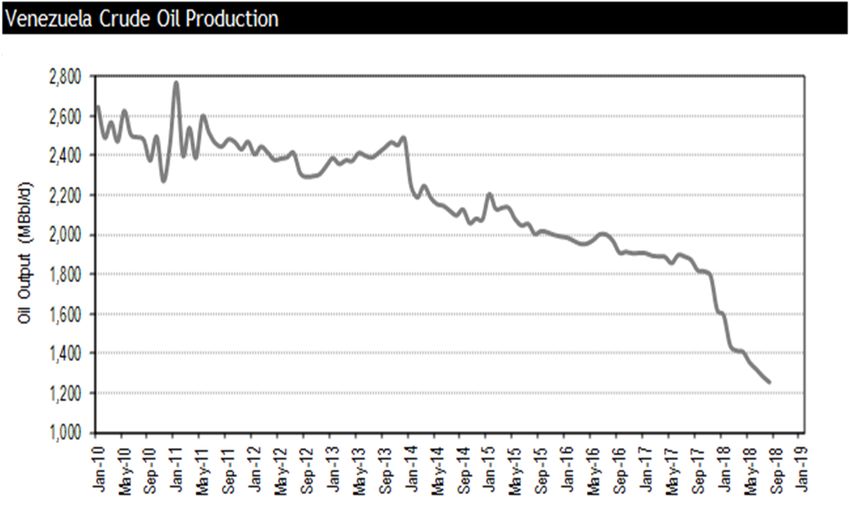

• Venezuela: The geopolitical risk in

Venezuela continues to deteriorate by the

day. January crude output sat at ~1.5

MMBbl/d and current production may be

closer to 1.3 MMBbl/d or 1.4 MMBbl/d, or

perhaps even lower. This very unfortunate

situation is driving downside risk to global

supply balances and should the current state

of the union continue, there is considerable

upside risk to global oil prices.

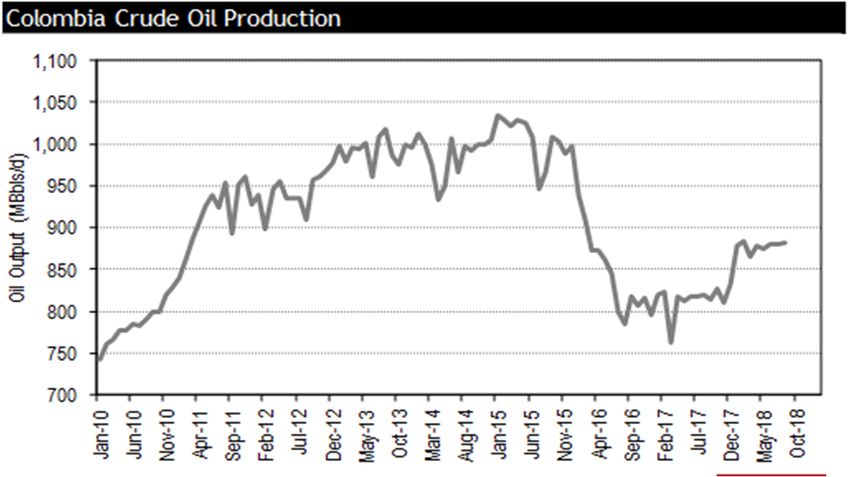

• Colombia: Capital spending levels and

development plans have been materially

trimmed in the face of trailing oil price

volatility and there is no reason to believe

upward momentum is on the come, from a

country-wide perspective.

• Markets That Will Grow Outside Of North

America: Kuwait, Kazakhstan, Russia and

possibly Iraq, depending on IOC development

plans.

Source: Energy Intelligence and OPEC

23Macro Commodity Outlook – Crude

• Further, we have highlighted $160

this multiple times in the

past, but we’ll harp on it $140

Dec. 2008

once more. While the

forward strip is a great tool $120

May. 2012

to hedge risk as either a

$100

producer or consumer of Dec. 2007

crude/products, it’s a poor May. 2014

$US/Bbl

$80

predictor of forward prices. Dec. 2014

Sep.2018

• In fact, the long-term $60 Jan. 2009

Jun.2018

correlation between the

Sept. 2017 Mar. 2017

forward strip looking 12 $40

Dec. 2004

Jan. 2016

months ahead and realized

crude prices over the past 20 $20

Dec. 2003

years has an R2 of 0.17. But

to be honest, we probably $0

didn’t even need to run that

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

statistical analysis.

Source: Bloomberg and CIBC World Markets Inc.

24Battle Of The Barrels: A Look At Canada’s Unique Headwinds

Battle Of The Barrels: A Look At The Price Action

• Canada light and heavy oil diffs have been both under pressure and volatile lately.

• Specifically, Ed Par/Mixed Sweet Blend (MSW) pricing has moved from trading at a traditional

~US$4/Bbl discount relative to WTI and a ~US$6/Bbl discount relative to U.S. Gulf Coast prices to

recent peaks of ~US$33/Bbl and ~US$40/Bbl over the past month, respectively.

• We have also seen Canadian Synthetic Crude Oil (SCO) move from historically pricing in line to a

modest premium to WTI, to a peak discount of US$31/Bbl in the past week.

• Western Canadian Select (WCS) pricing has also moved from trading at a traditional ~US$15/Bbl

discount relative to WTI to a recent peak of ~US$50/Bbl over the past week.

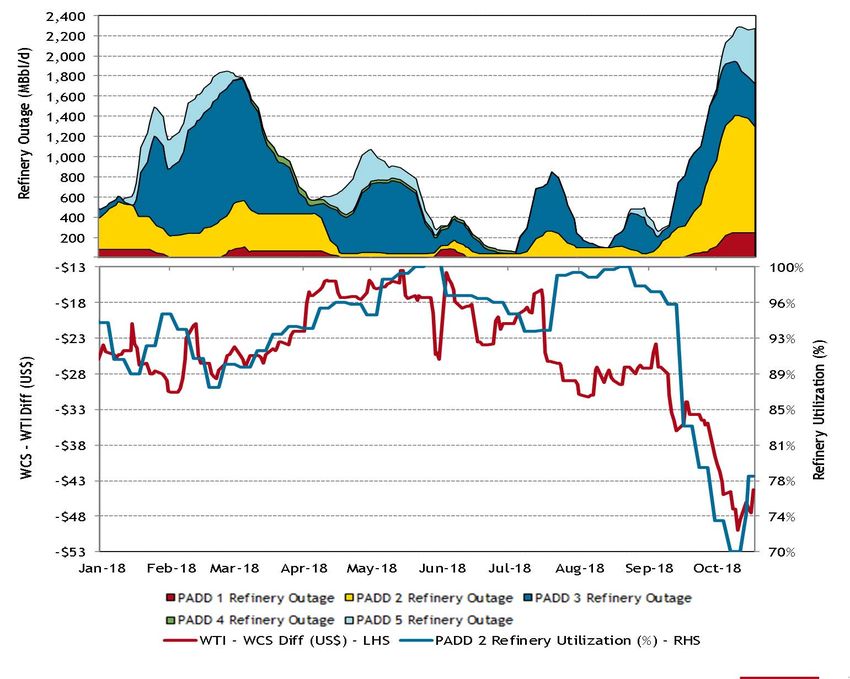

• Naturally, these spreads will tighten up as select PADD II refineries move out of maintenance in the

coming weeks, but there are structural takeaway capacity issues that shouldn’t be glazed over.

26Battle Of The Barrels: A Look At The Price Action

YTD North American Crude Benchmarks (US$/Bbl) YTD Canadian Crudes Relative To LLS (US$/Bbl)

$80 $10

$70

$0

($10)

$60

($20)

• This price

US$/Bbl

$50

US$/Bbl

($30)

action can be

$40 ($40)

seen in the

($50)

spreads to the $30

($60)

right. $20

($70)

• Despite a

robust global Ed Mixed Sweet Syncrude Blend

Western Canadian Select West Texas Intermediate Ed Mixed Sweet - LLS Syncrude - LLS WCS - LLS

market,

Canadian YTD Canadian Crudes Relative To WTI (US$/Bbl) YTD Canadian Crudes Relative To MEH (US$/Bbl)

crude prices $10 $10

have been

$0 $0

collapsing.

($10) ($10)

($20) ($20)

US$/Bbl

US$/Bbl

($30)

($30)

($40)

($40)

($50)

($50)

($60)

($60)

Ed Mixed Sweet - WTI Syncrude - WTI WCS - WTI

Ed Mixed Sweet - MEH Syncrude - MEH WCS - MEH

Source: Bloomberg and CIBC World Markets Inc. 27Battle Of The Barrels: U.S. Refinery Maintenance Has Been

An Issue

• It’s important to note that

some of this Canadian

price action is driven by

U.S. refinery turnarounds

caused by seasonally

reduced physical demand

for Canadian barrels.

• Specifically, BP Whiting

(~413 MBbl/d nameplate)

will be off until later this

week. Marathon’s Detroit

(~139 MBbl/d nameplate)

is set to come back online

today. And Holly Frontier’s

El Dorado refinery (~160

MBbl/d nameplate) will be

offline until mid-

November.

• As such, while some price

reprieve is on the way,

there are also structural

issues working against

Canada.

Source: Bloomberg and CIBC World Markets Inc.

28Battle Of The Barrels: U.S. Refinery Maintenance

• Despite this negative price action and

the decline in demand for Canadian

crude feedstock into the U.S. refining

market, Canadian flows into PADD II and

III remain steady.

• And it isn’t resulting in any material

outsized ballooning in crude stocks in

these storage markets. Specifically, U.S. PADD 3. U.S. Gulf Coast Crude Inventories

crude export draws have remained 300000

healthy while U.S. production is starting 280000

to flat line due to crude takeaway 260000

challenges. 240000

220000

(000s) Bbl

200000

180000

160000

140000

120000

Source: EIA, Bloomberg and CIBC World Markets Inc. Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

5-Yr Hi-Lo Range 2013-2017 Avg. 2016 29

2017 2018Battle Of The Barrels: Structural Takeaway Capacity Issues Exist

8,000

7,000

6,000

5,000

MBbl/d

4,000

3,000

2,000

1,000

0

2017A 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

Other Proposed Pipelines (Keystone XL and TMX) Enbridge Line 3 Replacement

Enbridge Mainline Optimization + BEP Repurposing Rail

Existing Pipelines Western Canada Refineries

WCSB Crude Supply (CAPP Forecast) WCSB Crude Supply (CIBC Forecast)

CIBC Crude Supply (Bull Case)

• Within the exhibit above, we stack our current base and bull-case WCSB production forecasts along with

those of the CAPP against current and forecasted WCSB takeaway capacity. As can be seen, the market

looks very tight.

Source: CAPP, NEB, geoSCOUT, company reports and CIBC World Markets Inc.

30Battle Of The Barrels: A Look At CRB Needed To Clear The Market

600 -$48

550 -$44

500 -$40

CBR Loading (MBbl/d)

450 -$36

WCS - WTI Diff ($/Bbl)

400 -$32

350 -$28

300 -$24

250 -$20

200 -$16

150 -$12

100 -$8

50 -$4

0 $0

Oct-17

Oct-18

Oct-19

Mar-17

Mar-18

Mar-19

Nov-17

Nov-18

Nov-19

Feb-17

Apr-17

Jun-17

Jul-17

Aug-17

Sep-17

Dec-17

Feb-18

Apr-18

Jun-18

Jul-18

Aug-18

Sep-18

Dec-18

Feb-19

Apr-19

Jun-19

Jul-19

Aug-19

Sep-19

Dec-19

Jan-17

Jan-18

Jan-19

May-17

May-18

May-19

High Case CBR Loadings Needed Base Case CBR Loadings Needed

Low Case CBR Loadings Needed Actual CBR Loadings

Expected CBR Export Capacity by ~2018 YE WCS - WTI Diff (RHS)

WCS - WTI Diff Strip (RHS)

Source: NEB, Bloomberg, CN, CP, CAPP, company reports and CIBC World Markets Inc.

• Moreover, as we highlight in the exhibit above, we believe the industry is going to need to

materially ramp CBR loadings over the coming six months. This will include the need to take

CBR shipments to a level that we have never seen before.

• And while we take comfort that Canada should be running upwards of ~450 MBbl/d of CBR

loadings by 2018 YE based on comments from CP and CN, the margin for error is small and

the industry will need to exercise extreme pragmatism in not overproducing, even under our

dampened growth expectations. 31Battle Of The Barrels: Key Takeaways

• Canada can no longer be a growth market until long-term egress issues are achieved: The reality is

that we do not believe individual Canadian company growth plans are achievable in the context of the

current takeaway constraints. Simply said, we believe producers will need to shut in production to

keep the spreads reasonable at various points in time over the coming year.

• This comes despite field-level economics likely still indicating that it makes sense to keep drilling and

adding output for select companies in select plays.

• Canadian producers will need to be logical and pragmatic: While we are operating under the

assumption that companies will be rational when it comes to a decision of maximizing production

versus cash flow, this is effectively a game of “prisoners dilemma” and sometime prices need to do all

of the work before the industry responds as it should.

• With that said, as we witnessed from Cenovus in H1/18, should the diff blow out and it makes sense to

dial back production by 1%-2% to increase cash flow by 5%-10%, we believe the latter should take

place, eventually.

• Canadian light volumes face other headwinds: The MSW/SCO barrel has rising competition from the

Permian, Oklahoma, Rockies and U.S. Bakken, which all sell into the PADD II/PADD III market and are

ramping up production. And until there are enhanced egress options to move more production from

these markets (particularly the Permian) to the Gulf Coast, this will create crude-on-crude

competition that is likely to remain in place for upwards of the next 18 months.

• MSW volumes are also being backed out of WCSB refineries: There is ~760 MBbl/d of nameplate

refining capacity in Western Canada, of which upwards of 75% of the historical feedstock that has

typically been run through these facilities is a Canadian light barrel (i.e., a MSW type of grade). But

these refineries are consistently trying to increase running synthetic or heavy oil sands barrels in order

to maximize profits and have strong physical integration with their upstream output.

32Battle Of The Barrels: Key Takeaways

• A look at the path forward:

• Limit unfettered Canadian light volume growth and be cognizant of these structural issues

ahead.

• Wait for full Enbridge Mainline expansion/optimization to unfold.

• Look at alternative markets to clear output at this juncture, including using CBR into the

Eastern Canadian refining market to back out international imports and then into the U.S.

Gulf Coast – although there will likely be export bottlenecks arriving due to export capacity.

• The industry needs to push other long-term ways to get more production to tidewater.

2015 - Present Brent - Ed Mixed Sweet (US$/Bbl)

$100 $45

$90 $40

Brent‐MSW Diff (US$/Bbl)

$80 $35

$70 $30

$60

$25

US$/Bbl

$50

$20

$40

$30 $15

$20 $10

$10 $5

$0 $0

Series1 Brent Ed Mixed Sweet

Source: Bloomberg and CIBC World Markets Inc.

33IMO 2020: Road To Perdition?

IMO 2020: The Regulation Will Challenge Heavy Sour Pricing,

But The Canadian Large-caps Should Fare Well

• We believe IMO 2020 has the potential to be one of the larger events in the oil market this decade. The

regulation will have broad impacts on pricing for various crude slates and will require tens of billions of

dollars of capex to be spread across the refining and maritime shipping industries. Depending on how

industry responds to the price action that follows, it also has the potential to cause material inflation

globally as middle distillates are effectively the lifeblood of the global economy. If left unchecked,

rising diesel prices will act as a tax on economic growth and come with negative consequences.

• Although the regulation does not officially take effect until January 1, 2020 and the global shipping

industry will likely continue to burn high sulphur fuel oil (HSFO) in vessels until New Year’s Eve 2019,

the spot market for HSFO will drop like a stone before this date. Specifically, anyone that traffics or

trades in the HSFO market will be keen to destock their inventories and offload their exposure before

the music stops on January 1, 2020. This price action can already be seen in the forward curve between

diesel and HSFO, but likely has further to go from here (see the below exhibit).

200

Fuel Oil (3.5% Sulphur) Fuel Oil Futures

180 Diesel (ULSD) Diesel (ULSD) Futures Although the HSFO futures market

160 Heavy Fuel Oil vs. ULSD Diff ($/Bbl) is showing a ~US$20/Bbl decline

over H1/19 - Q1/20, we believe

140

more pressure is set to arrive...

US$/Bbl

120

100

80

60

40

20

0

Jan-08

Jan-09

Jan-10

Jan-11

Jan-12

Jan-13

Jan-14

Jan-15

Jan-16

Jan-17

Jan-18

Jan-19

Jan-20

Jan-21

Jan-22

Jan-23

Jan-24

Jul-08

Jul-09

Jul-10

Jul-11

Jul-12

Jul-13

Jul-14

Jul-15

Jul-16

Jul-17

Jul-18

Jul-19

Jul-20

Jul-21

Jul-22

Jul-23

35

Source: Bloomberg and CIBC World Markets Inc.IMO 2020: The Regulation Will Challenge Heavy Sour Pricing,

But The Canadian Large-caps Should Fare Well

• The key thing to note is that it would be a mistake to take the simplistic view that the regulation

will be negative for heavy sours and neutral for everything else. As we have been harping on for the

past 18 months, the global oil market has been going through an acute tightening and after years of

delivering a number of large global supply projects that were sanctioned prior to the H2/14

downturn, the forward landscape for incremental production growth around the world is soft

outside of the U.S. in 2020+ and that is not going to change anytime soon, in our view.

• The reality is that the world is longing for more crude and while one impact of IMO 2020 will be

price dislocation for heavy sours, the market will still need every one of those barrels to keep

clearing the market in order to keep the world’s crude supply and demand in some form of a

relative check. While heavy sour diffs will widen on the back of IMO 2020, the global reference

point will also rise and it’s not inconceivable (maybe even fairly likely) that pricing for WCS and

other heavy sour grades will actually increase on the back of the regulation in absolute terms. As

such, should the equity markets start to massively discount Canadian heavy oil and oil sands

producers as we march into H2/19 and those producers have solid market access to keep clearing

their production (i.e., like the vast majority of Canadian Large-caps/Integrateds have), then that

might end up presenting a solid buying opportunity for such equities.

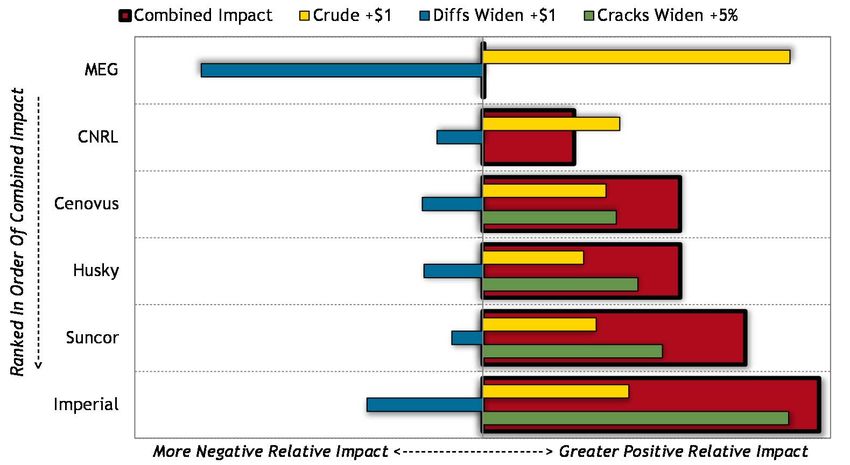

• Within our Canadian Large-cap E&P and Integrateds coverage universe, there will be varying

degrees of impact from the implementation of IMO 2020. Specifically, we would highlight that we

expect the regulation to likely be the most positive for Imperial, Suncor and Husky, then less

positive for Cenovus and Canadian Natural (but still likely a positive tailwind for both companies)

and then neutral to possibly somewhat negative for MEG, on a relative basis.

36IMO 2020: The Regulation Will Challenge Heavy Sour Pricing,

But The Canadian Large-caps Should Fare Well

The exhibit below highlights the 2020 directional impact that a US$1/Bbl wider WCS-WTI diff, a

US$1/Bbl increase in the WTI price and a 5% widening in crack spreads would have to each company’s

cash flows. You’ll notice there isn’t a legend here and there is good reason for this – this isn’t a linear

relationship and we didn’t want to publish a thousand different sensitivities, but felt the chart below

gives a better directional read on how to think about impacts outside of our base-case forecasts,

which naturally incorporate our IMO 2020 and other market views.

Source: Company reports and CIBC World Markets Inc.

37Price Forecast

2018E 2019E 2020E

Current Current Current

Crude Oil

Brent (US$/Bbl) $74.00 $85.00 $85.00

Brent - WTI Differential (US$/Bbl) ($5.50) ($10.00) ($9.00)

WTI Oil (US$/Bbl) $68.50 $75.00 $76.00

WTI - Ed. Par Differential (US$/Bbl) ($7.86) ($11.00) ($8.75)

Forex - US$/C$ $0.780 $0.780 $0.780

Ed. Par (C$/Bbl) $77.74 $82.05 $86.22

Light Heavy Differential vs. C$ WTI (%) (36%) (36%) (39%)

Light Heavy Differential vs. US$ WTI (US$/Bbl) ($25.00) ($27.00) ($30.00)

Western Canada Select (C$/Bbl) $55.77 $61.54 $58.97

Natural Gas

NYMEX (US$/Mcf) $3.04 $2.69 $2.62

NYMEX - AECO Differential (US$/Mcf) ($1.79) ($1.55) ($1.50)

AECO 30+ Day Spot (C$/Mcf) $1.60 $1.46 $1.44

Dawn Gas (US$/Mcf) $3.02 $2.59 $2.52

Dawn Gas Premium/(Discount) to HH (US$/Mcf) ($0.02) ($0.10) ($0.10)

Station 2 Gas (US$/Mcf) $1.18 $0.99 $0.98

Station 2 Gas Premium/(Discount) to HH (US$/Mcf) ($1.87) ($1.70) ($1.65)

Chicago Gas (US$/Mcf) $2.91 $2.54 $2.48

Chicago Gas Premium/(Discount) to HH (US$/Mcf) ($0.13) ($0.15) ($0.15)

Sumas Gas (US$/Mcf) $2.23 $1.94 $1.88

Sumas Gas Premium/(Discount) to HH (US$/Mcf) ($0.81) ($0.75) ($0.75)

Malin Gas (US$/Mcf) $2.48 $2.09 $2.03

Malin Gas Premium/(Discount) to HH (US$/Mcf) ($0.57) ($0.60) ($0.60)

Waha Gas (US$/Mcf) $2.32 $2.19 $2.13

Waha Gas Premium/(Discount) to HH (US$/Mcf) ($0.72) ($0.50) ($0.50)

Source: Company reports and CIBC World Markets Inc.

38I

Oil Update - October 18, 2018

IMPORTANT DISCLOSURES:

Analyst Certification: Each CIBC World Markets Corp./Inc. research analyst named on the front page of this research report, or at the beginning of any

subsection hereof, hereby certifies that (i) the recommendations and opinions expressed herein accurately reflect such research analyst's personal views

about the company and securities that are the subject of this report and all other companies and securities mentioned in this report that are covered by

such research analyst and (ii) no part of the research analyst's compensation was, is, or will be, directly or indirectly, related to the specific

recommendations or views expressed by such research analyst in this report.

Analysts employed outside the U.S. are not registered as research analysts with FINRA. These analysts may not be associated persons of CIBC World Markets

Corp. and therefore may not be subject to FINRA Rule 2241 restrictions on communications with a subject company, public appearances and trading

securities held by a research analyst account.

Potential Conflicts of Interest: Equity research analysts employed by CIBC World Markets Corp./Inc. are compensated from revenues generated by various

CIBC World Markets Corp./Inc. businesses, including the CIBC World Markets Investment Banking Department. Research analysts do not receive

compensation based upon revenues from specific investment banking transactions. CIBC World Markets Corp./Inc. generally prohibits any research analyst

and any member of his or her household from executing trades in the securities of a company that such research analyst covers. Additionally, CIBC World

Markets Corp./Inc. generally prohibits any research analyst from serving as an officer, director or advisory board member of a company that such analyst

covers.

In addition to 1% ownership positions in covered companies that are required to be specifically disclosed in this report, CIBC World Markets Corp./Inc. may

have a long position of less than 1% or a short position or deal as principal in the securities discussed herein, related securities or in options, futures or other

derivative instruments based thereon.

Recipients of this report are advised that any or all of the foregoing arrangements, as well as more specific disclosures set forth below, may at times give

rise to potential conflicts of interest.

1Oil Update - October 18, 2018 Important Disclosure Footnotes for Companies Mentioned in this Report that Are Covered by CIBC World Markets Corp./Inc.: Stock Prices as of 10/18/2018: Canadian Natural Resources Ltd. (2a, 2b, 2g, 7) (CNQ-TSX, C$37.31) Cenovus Energy Inc. (2g, 7, 9) (CVE-TSX, C$11.29) Husky Energy Inc. (2g) (HSE-TSX, C$19.83) Imperial Oil Limited (2g) (IMO-TSX, C$43.96) MEG Energy Corp. (2g) (MEG-TSX, C$10.79) Suncor Energy Inc. (2a, 2e, 2g, 7) (SU-TSX, C$47.17) Important disclosure footnotes that correspond to the footnotes in this table may be found in the "Key to Important Disclosure Footnotes" section of this report.

Oil Update - October 18, 2018

Key to Important Disclosure Footnotes:

1a CIBC WM Corp. makes a market in the securities of this company.

1b CIBC WM Inc. makes a market in the securities of this company.

1c CIBC WM Plc. makes a market in the securities of this company.

2a This company is a client for which a CIBC World Markets company has performed investment banking services in the past 12

months.

2b CIBC World Markets Corp. has managed or co-managed a public offering of securities for this company in the past 12

months.

2c CIBC World Markets Inc. has managed or co-managed a public offering of securities for this company in the past 12 months.

2d CIBC World Markets Corp. has received compensation for investment banking services from this company in the past 12

months.

2e CIBC World Markets Inc. has received compensation for investment banking services from this company in the past 12

months.

2f CIBC World Markets Corp. expects to receive or intends to seek compensation for investment banking services from this

company in the next 3 months.

2g CIBC World Markets Inc. expects to receive or intends to seek compensation for investment banking services from this

company in the next 3 months.

3a This company is a client for which a CIBC World Markets company has performed non-investment banking, securities-related

services in the past 12 months.

3b CIBC World Markets Corp. has received compensation for non-investment banking, securities-related services from this

company in the past 12 months.

3c CIBC World Markets Inc. has received compensation for non-investment banking, securities-related services from this

company in the past 12 months.

4a This company is a client for which a CIBC World Markets company has performed non-investment banking, non-securities-

related services in the past 12 months.

4b CIBC World Markets Corp. has received compensation for non-investment banking, non-securities-related services from this

company in the past 12 months.

4c CIBC World Markets Inc. has received compensation for non-investment banking, non-securities-related services from this

company in the past 12 months.

5a The CIBC World Markets Corp. analyst(s) who covers this company also has a long position in its common equity securities.

5b A member of the household of a CIBC World Markets Corp. research analyst who covers this company has a long position in

the common equity securities of this company.

6a The CIBC World Markets Inc. fundamental analyst(s) who covers this company also has a long position in its common equity

securities.

6b A member of the household of a CIBC World Markets Inc. fundamental research analyst who covers this company has a long

position in the common equity securities of this company.

7 CIBC World Markets Corp., CIBC World Markets Inc., and their affiliates, in the aggregate, beneficially own 1% or more of a

class of equity securities issued by this company.Oil Update - October 18, 2018

Key to Important Disclosure Footnotes: (Continued)

8 An executive of CIBC World Markets Inc. or any analyst involved in the preparation of this research report has provided

services to this company for remuneration in the past 12 months.

9 An executive committee member or director of Canadian Imperial Bank of Commerce (“CIBC”), the parent company to CIBC

World Markets Inc. and CIBC World Markets Corp., or a member of his/her household is an officer, director or advisory

board member of this company or one of its subsidiaries.

10 Canadian Imperial Bank of Commerce ("CIBC"), the parent company to CIBC World Markets Inc. and CIBC World Markets

Corp., has a significant credit relationship with this company.

11 The equity securities of this company are restricted voting shares.

12 The equity securities of this company are subordinate voting shares.

13 The equity securities of this company are non-voting shares.

14 The equity securities of this company are limited voting shares.V

Oil Update - October 18, 2018

CIBC World Markets Corp./Inc. Price Chart

For price and performance charts required under NYSE and NASD rules, please visit CIBC on the web at http://apps.cibcwm.com/pricecharts/ or write to CIBC World Markets

Corp., 425 Lexington Avenue, New York, NY 10017 (212-856-4000) or CIBC world Markets Inc., 161 Bay Street, 4th Floor, Toronto, ON M5H 2S8, Attn: Research Disclosure Chart

Request.

CIBC World Markets Corp./Inc. Stock Rating System

Abbreviation Rating Description

Stock Ratings

OP Outperformer Stock is expected to outperform similar stocks in the coverage universe during the next 12-18

months.

NT Neutral Stock is expected to perform in line with similar stocks in the coverage universe during the

next 12-18 months.

UN Underperformer Stock is expected to underperform similar stocks in the coverage universe during the next 12-

18 months.

NR Not Rated CIBC World Markets does not maintain an investment recommendation on the stock.

R Restricted CIBC World Markets is restricted (due to potential conflict of interest) from rating the stock.

Stock Ratings Prior To December 09, 2016

SO Sector Outperformer Stock is expected to outperform the sector during the next 12-18 months.

SP Sector Performer Stock is expected to perform in line with the sector during the next 12-18 months.

SU Sector Underperformer Stock is expected to underperform the sector during the next 12-18 months.

NR Not Rated CIBC World Markets does not maintain an investment recommendation on the stock.

R Restricted CIBC World Markets is restricted (due to potential conflict of interest) from rating the stock.

Sector Ratings (note: Broader market averages refer to S&P 500 in the U.S. and S&P/TSX Composite in Canada.)

O Overweight Sector is expected to outperform the broader market averages.

M Marketweight Sector is expected to equal the performance of the broader market averages.

U Underweight Sector is expected to underperform the broader market averages.

NA None Sector rating is not applicable.

"Speculative" indicates that an investment in this security involves a high amount of risk due to volatility and/or liquidity issues.VI

Oil Update - October 18, 2018

Ratings Distribution*: CIBC World Markets Corp./Inc. Coverage Universe

(as of 18 Oct 2018) Count Percent Inv. Banking Relationships Count Percent

Outperformer (Buy) 159 47.6% Outperformer (Buy) 142 89.3%

Neutral (Hold/Neutral) 155 46.4% Neutral (Hold/Neutral) 131 84.5%

Underperformer (Sell) 8 2.4% Underperformer (Sell) 8 100.0%

Restricted 11 3.3% Restricted 11 100.0%

*Although the investment recommendations within the three-tiered,relative stock rating system utilized by CIBC World Markets Corp./Inc.do not

correlate to buy, hold and sell recommendations, for the purposes of complying with FINRA rules, CIBC World Markets Corp./Inc. has assigned buy

ratings to securities rated Outperformer, hold ratings to securities rated Neutral, and sell ratings to securities rated Underperformer. The

distributions above reflect the combined historical ratings of CIBC World Markets Corp. and CIBC World Markets Inc.

Ratings Distribution: Energy Coverage Universe

(as of 18 Oct 2018) Count Percent Inv. Banking Relationships Count Percent

Outperformer (Buy) 35 50.7% Outperformer (Buy) 35 100.0%

Neutral (Hold/Neutral) 29 42.0% Neutral (Hold/Neutral) 28 96.6%

Underperformer (Sell) 2 2.9% Underperformer (Sell) 2 100.0%

Restricted 3 4.3% Restricted 3 100.0%

Important disclosures required by applicable rules can be obtained by visiting CIBC World Markets on the web at http://researchcentral.cibcwm.com/. Important disclosures

for each issuer can be found using the "Coverage" tab on the top left of the Research Central home page. Access to the system for rating investment opportunities and our

dissemination policy can be found at the bottom of each page on the Research Central website. These important disclosures can also be obtained by writing to CIBC World

Markets Corp., 425 Lexington Avenue, New York, NY 10017 (212-856-4000) or CIBC World Markets Inc.,161 Bay Street, 4th Floor, Toronto, ON M5H 2S8, Attention: Research

Disclosures Request.VII

Oil Update - October 18, 2018

Legal Disclaimer

Not for Distribution: This marketing presentation is issued and approved by CIBC World Markets Inc. solely for distribution to institutional investor clients and

not with a view toward public distribution as a research report. This presentation is provided to such institutional investor clients for informational purposes

only, and does not constitute an offer or solicitation to buy or sell any securities discussed herein in any jurisdiction where such offer or solicitation is

prohibited.

This presentation is issued and approved for distribution by (a) in Canada, CIBC World Markets Inc., a member of the Investment Industry Regulatory

Organization of Canada (“IIROC”), the Toronto Stock Exchange, the TSX Venture Exchange and a Member of the Canadian Investor Protection Fund, (b) in the

United Kingdom, CIBC World Markets plc, is Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the

Prudential Regulation Authority, (c) in Australia to wholesale clients only, CIBC Australia Ltd, a company regulated by the ASIC with AFSL license number

240603 and ACN 000 067 256, and (d) in Japan, CIBC World Markets (Japan) Inc., a registered Type 1 Financial product provider with the registration number

Director General of Kanto Finance Bureau #218 (collectively, “CIBC World Markets”) and (e) in the United States either by (i) CIBC World Markets Inc. for

distribution only to U.S. Major Institutional Investors (“MII”) (as such term is defined in SEC Rule 15a-6) or (ii) CIBC World Markets Corp., a member of the

Financial Industry Regulatory Authority (“FINRA”). U.S. MIIs receiving this presentation from CIBC World Markets Inc. (the Canadian broker-dealer) are

required to effect transactions (other than negotiating their terms) in securities discussed in the presentation through CIBC World Markets Corp. (the U.S.

broker-dealer).

This presentation is provided, for informational purposes only, to institutional investor and retail clients of CIBC World Markets in Canada, and does not

constitute an offer or solicitation to buy or sell any securities discussed herein in any jurisdiction where such offer or solicitation would be prohibited. This

document and any of the products and information contained herein are not intended for the use of private investors in the United Kingdom. Such investors

will not be able to enter into agreements or purchase products mentioned herein from CIBC World Markets plc. The comments and views expressed in this

document are meant for the general interests of wholesale clients of CIBC Australia Limited.

This presentation has been prepared by the CIBC group and is issued in Hong Kong by Canadian Imperial Bank of Commerce, Hong Kong Branch, a registered

institution under the Securities and Futures Ordinance, Cap 571 (the “SFO”). This presentation is intended for “professional investors” only (within the

meaning of the SFO) and has been prepared for general circulation and does not take into account the objectives, financial situation or needs of any

recipient. Any recipient in Hong Kong who has any questions or requires further information on any matter arising from or relating to this presentation should

contact Canadian Imperial Bank of Commerce, Hong Kong Branch at Suite 3602, Cheung Kong Centre, 2 Queen’s Road Central, Hong Kong (telephone number:

+852 2841 6111). Orders for Hong Kong listed securities will be executed by Canadian Imperial Bank of Commerce, Hong Kong Branch. Canadian Imperial

Bank of Commerce, Hong Kong Branch has entered into an arrangement with its broker-dealer affiliates worldwide to execute orders for securities listed

outside of Hong Kong for Hong Kong clients.

This presentation is intended for distribution in Singapore solely to “institutional investors” (within the meanings of the Financial Advisers Act (Chapter 110

of Singapore)).

The securities mentioned in this presentation may not be suitable for all types of investors. This presentation does not take into account the investment

objectives, financial situation or specific needs of any particular client of CIBC World Markets. Recipients should consider this presentation as only a single

factor in making an investment decision and should not rely solely on investment recommendations contained herein, if any, as a substitution for the

exercise of independent judgment of the merits and risks of investments. The analyst writing the presentation is not a person or company with actual,

implied or apparent authority to act on behalf of any issuer mentioned in the presentation. Before making an investment decision with respect to any

security recommended in this presentation, the recipient should consider whether such recommendation is appropriate given the recipient's particular

investment needs, objectives and financial circumstances. CIBC World Markets suggests that, prior to acting on any of the recommendations herein,

Canadian retail clients of CIBC World Markets contact one of our client advisers in your jurisdiction to discuss your particular circumstances.

Non-client recipients of this presentation who are not institutional investor clients of CIBC World Markets should consult with an independent financial

advisor prior to making any investment decision based on this presentation or for any necessary explanation of its contents. CIBC World Markets will not treatVIII

Oil Update - October 18, 2018

Legal Disclaimer (Continued)

non-client recipients as its clients solely by virtue of their receiving this presentation.

Past performance is not a guarantee of future results, and no representation or warranty, express or implied, is made regarding future performance of any

security mentioned in this presentation. The price of the securities mentioned in this presentation and the income they produce may fluctuate and/or be

adversely affected by exchange rates, and investors may realize losses on investments in such securities, including the loss of investment principal. CIBC

World Markets accepts no liability for any loss arising from the use of information contained in this presentation, except to the extent that liability may arise

under specific statutes or regulations applicable to CIBC World Markets.

Information, opinions and statistical data contained in this presentation were obtained or derived from sources believed to be reliable, but CIBC World

Markets does not represent that any such information, opinion or statistical data is accurate or complete (with the exception of information contained in the

Important Disclosures section of this presentation provided by CIBC World Markets or individual research analysts), and they should not be relied upon as

such. All estimates, opinions and recommendations expressed herein constitute judgments as of the date of this presentation and are subject to change

without notice.

Nothing in this presentation constitutes legal, accounting or tax advice. Since the levels and bases of taxation can change, any reference in this presentation

to the impact of taxation should not be construed as offering tax advice on the tax consequences of investments. As with any investment having potential

tax implications, clients should consult with their own independent tax adviser.

This presentation may provide addresses of, or contain hyperlinks to, Internet web sites. CIBC World Markets has not reviewed the linked Internet web site of

any third party and takes no responsibility for the contents thereof. Each such address or hyperlink is provided solely for the recipient's convenience and

information, and the content of linked third-party web sites is not in any way incorporated into this document. Recipients who choose to access such third-

party web sites or follow such hyperlinks do so at their own risk.

Although each company issuing this presentation is a wholly owned subsidiary of Canadian Imperial Bank of Commerce (“CIBC”), each is solely responsible for

its contractual obligations and commitments, and any securities products offered or recommended to or purchased or sold in any client accounts (i) will not

be insured by the Federal Deposit Insurance Corporation (“FDIC”), the Canada Deposit Insurance Corporation or other similar deposit insurance, (ii) will not

be deposits or other obligations of CIBC, (iii) will not be endorsed or guaranteed by CIBC, and (iv) will be subject to investment risks, including possible loss

of the principal invested. The CIBC trademark is used under license.

© 2018 CIBC World Markets Inc. All rights reserved. Unauthorized use, distribution, duplication or disclosure without the prior written permission of CIBC

World Markets is prohibited by law and may result in prosecution.You can also read