COLUMBUS FREIGHT CHECK - Trends, Challenges and Opportunities OCTOBER 2, 2019 OCEAN MARKET PANEL DISCUSSION

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

COLUMBUS FREIGHT CHECK

OCTOBER 2, 2019

OCEAN MARKET PANEL DISCUSSION

Trends, Challenges and Opportunities

Bob Fredman, Big Lots (Moderator)

Joseph Voakes, CMA

James Setzke, Hapag Lloyd

Dan Sutton, Zim Linesle

Panel Discussion Topics IMO2020 LOW SULPHUR FUEL WINTER BLANK SAILING PROGRAM CARRIER STRATEGIES FOR SOURCING SHIFTS

New Sulphur Cap – The IMO 2020 Regulations Update September 2019

What are the IMO 2020 Fuel Regulations?

The new fuel regulations, known as “the

Sulphur Cap”, require all marine carriers

to use low sulfur fuel (up to 0.5% sulfur

content) by January 1st, 2020*

The new regulations, introduced by the

International Maritime Organization (IMO) are

aimed to reduce marine pollution and

emissions

All shipping companies will be obliged to

comply and to significantly reduce emissions

on the high seas and in coastal areas

* There are indications that a grace period for the implementation of the IMO 2020

regulations will be given till end of Q1/20

2

How will the Regulations Impact the Shipping Industry?

The new regulations will impact all the stakeholders in the industry. Compliance with

the new regulations is expected to create a significant cost impact

There are three ways for carriers to comply:

1. Buying compliant fuel at higher prices

2. Investing in and Installing new cleaning systems on board vessels (Scrubbers)

3. Deploying new type of vessels using Liquid Natural Gas (LNG)

All alternatives are expected to carry significant costs for the carriers

External sources estimate additional cost to the container shipping industry,

which can reach to a level of 20-30 Billion USD

3

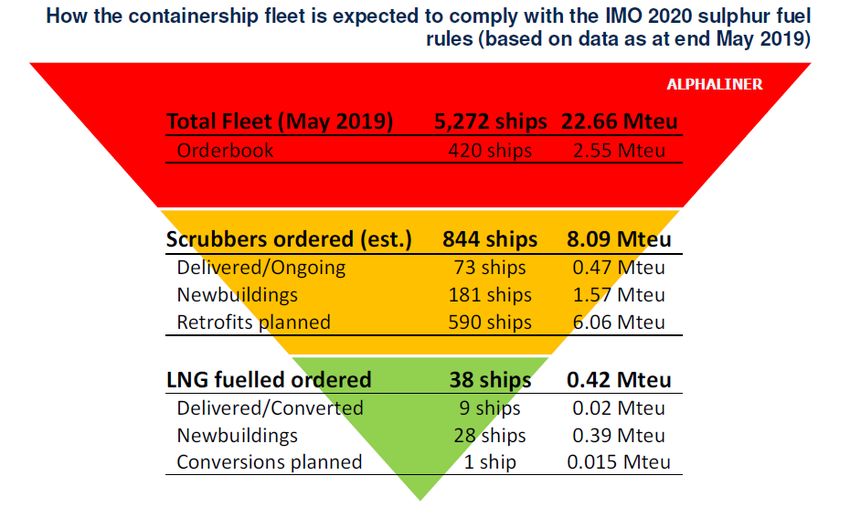

Using compliant fuels will be the dominant initial approach

to IMO2020

16% of vessels

36% of capacity

0.7% of vessels

1.9% of capacity

Source: Alphaliner Weekly Newsletter 28.05.2019

6

ZIM is well prepared for the

IMO 2020 Regulations

7

Low Sulphur IMO 2020 Regulation Caring for the future today August 2019

Low Sulphur IMO 2020 Regulation

For the benefit of:

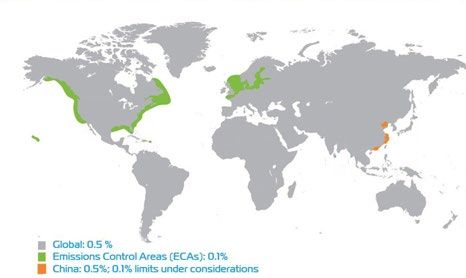

MARPOL ANNEX VI sets limits on SOx and NOx

Public Health: Environment: emissions from ship exhaust

improved air quality, reduction of acid rain,

reduction of soil erosion, Objective on January 1st, 2020

respiratory diseases acidification of oceans

Reducing average

APPLIES TO ALL SEA-GOING VESSELS WORLDWIDE:

sulphur emissions

worldwide by

~100,000 85%

2

Low Sulphur IMO 2020 RegulationWhat does this mean for our customers?

VLSFO will constitute approximately 90% of our fuel supply in 2020.

The cost of VLSFO 0.5O % is expected to be significantly higher than the present HSFO 3.50 %.

?

VLSFO 0.50% 90%

HSFO 3.50%

Low Sulphur fuels

6

Low Sulphur IMO 2020 RegulationLong-term contracts (more than 3 months validity)

For long-term contracts, BAF will be updated as of January 1st, 2020.

Fuel reference HSFO 3.50% will be replaced by VLSFO 0.50%

BAF Q1 2020 will be based on average price of VLSFO 0.50% of September/October/November 2019:

Dec 1st, Jan 1st,

Sept 19 Oct 19 Nov 19 2019 2020

Feb 20 Mar 20

Publication Application

BAF = $$ BAF = $$

average VLSFO price

BAF amounts per trade will be then updated on a quarterly basis as follows :

BAF = VLSFO 0.50% PRICE PER TON x TRADE COEFFICIENT

Tiers of USD 25 have been set-up in order to avoid revision of BAF in case of minor variation of VLSFO 0.50% price.

10

Low Sulphur IMO 2020 RegulationLong-term contracts (more than 3 months validity)

BAF simulation (for a selection of trades)*

HSFO or VLSFO price (usd/ton) 375,01 400,01 425,01 450,01 475,01 500,01 525,01 550,01 575,01 600,01 625,01 …, for each

400,00 425,00 450,00 475,00 500,00 525,00 550,00 575,00 600,00 625,00 650,00 25 usd

Far East to North Europe usd per teu 240 255 270 285 300 315 330 345 360 375 390 15,00

Far East to West Med usd per teu 240 255 270 285 300 315 330 345 360 375 390 15,00

Far East to WCNA usd per feu 405 432 459 486 513 540 567 594 621 648 675 27,00

Far East to ECNA usd per feu 660 704 748 792 836 880 924 968 1012 1056 1100 44,00

Far East to WCSA usd per teu 260 276 292 308 325 341 357 373 390 406 422 16,25

Far East to ECSA usd per teu 260 276 292 308 325 341 357 373 390 406 422 16,25

Far East to West Africa usd per teu 285 307 330 352 375 397 420 442 465 487 510 22,50

Far East to East Africa usd per teu 205 222 240 257 275 292 310 327 345 362 380 17,50

North Europe to Far East usd per teu 20 27 35 42 50 57 65 72 80 87 95 7,50

West Med to Far East usd per teu 20 27 35 42 50 57 65 72 80 87 95 7,50

WCNA to Far East usd per teu not applicable 2 5 7 10 12 15 17 2,50

ECNA to Far East usd per teu not applicable 5 10 15 20 25 30 35 5,00

WCSA to Far East usd per teu 80 85 90 95 100 105 110 115 120 125 130 5,00

ECSA to Far East usd per teu 80 85 90 95 100 105 110 115 120 125 130 5,00

West Africa to Far East usd per teu 165 177 190 202 215 227 240 252 265 277 290 12,50

East Africa to Far East usd per teu 10 18 27 36 45 53 62 71 80 88 97 8,75

*Above amounts are only given as an example of BAF quantum. Actual BAF tariffs will be communicated later on as per relevant regulations.

HSFO 2019 prices range. 11

Assumed VLSFO 2020 prices range - based on the factors available at the date of the publication of this document.

Low Sulphur IMO 2020 RegulationCMA CGM: fully compliant as of January 1st, 2020

Use Low Sulphur Fuel Oil

with 0.50% Sulphur

Install Advanced Air Quality Systems*

onboard our vessels will be

compliant

January 1st, 2020

Use LNG-powered vessels

* Exhaust Gas Cleaning Systems

5

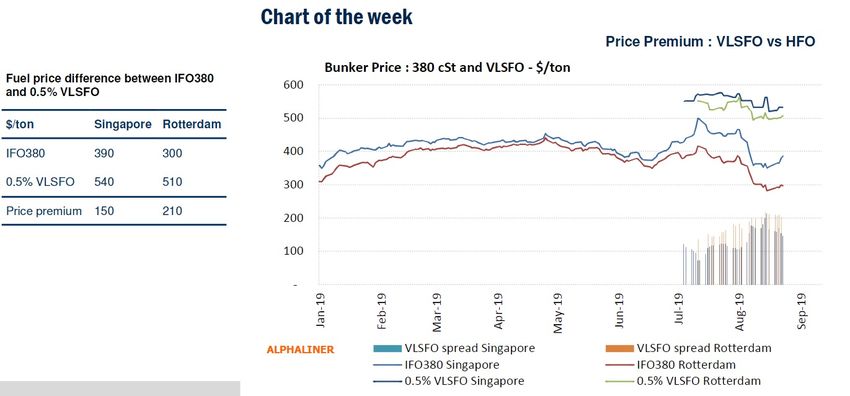

Low Sulphur IMO 2020 RegulationAlphaliner Price Spreads between IFO380 and 0.5% VLSFO

For greener shipping

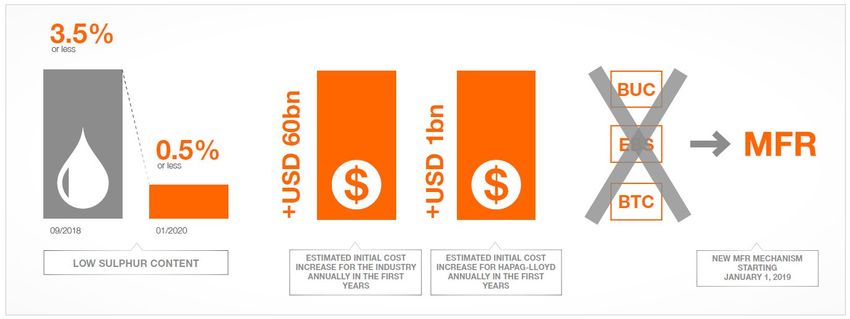

Financial Impact of IMO2020 for the Shipping Industry

Complying with the new low sulphur regulation will make the industry significantly greener, but

compliance will have a significant cost impact on the industry

To comply with the regulation, the industry will have to either start using low sulphur fuels or invest in new technologies that have yet to be thoroughly tested in

practice

In either case the costs will go up, because compliant fuels as well as investments to new technologies will be expensive

Experts are estimating an additional initial fuel cost of USD 60bn for the entire industry annually in the first years

Hapag-Lloyd is estimating its additional initial costs to amount up to USD 1bn for the company annually in the first years, based on the assumption that the spread

between HSFO and LSFO 0.5% will be USD 250

To recover fuel related costs caused by the IMO2020, Hapag-Lloyd is introducing a transparent and fair Marine Fuel Recovery (MFR) mechanism

2Hapag-Lloyd Marine Fuel Recovery

Simplify rate structure and will replace all existing

fuel charges with a new Marine Fuel Recovery (MFR)

mechanism

Marine Fuel Recovery Mechanism will be gradually implemented

from 1 January 2019

Transparent and easy-to-understand

It helps our customers predict and plan the price increases for

their trade routes

The MFR aiming at recovering costs arising from stricter

regulation

The calculation is based on average market data

3Transparent and easy-to-understand: The MFR mechanism is

based on a set of variables and average market data

The MFR is based on market data and derived out of averages for Market Class Vessels

Fuel consumption (per ton) Carried TEU

Based on Market Class Vessels, representing a typical service in the market on a Estimation of the carried TEUs per round voyage consists of

specific trade the nominal size of a market class vessel (eeSea) and

utilization based on Clean Cargo Working Group data

Considered per round voyage at average speed (CCWG)

Differentiation between days spent at sea and at port (eeSea data)

Example: East Asia – North Europe trade

19 different services per week considered

For each service its average vessel is determined

and considered in the calculation

A market class vessel for this trade is ~14,300 TEU

based on vessel size data from eeSea

14,000 – 22,000 TEU: 10 services

10,000 – 14,000 TEU: 5 services

8,000 – 10,000 TEU: 2 services

4,000 – 6,000 TEU: 2 services

Fuel price (per ton)

70% utilization based on the global average utilization

Based on market prices for different fuel types (source: Platts) outlined by CCWG

Fuel types included: HSFO or LSFO 0.5% and LSFO 0.1% 14,300 x 0.7 = 10, 010 TEU

4B l ank S ai l i ng s – F rom We e k 4 0 to 4 4

Sum of Vessel Capacity in TEU's Week

Alliance Service Vessel Name 40 41 42 44

OCEAN AASP/Soth China 2 COSCO VENICE 4,365

East Coast Express (ECX1)/China AW Loop2 (AW2) OOCL Chongqing 13,200

East Coast Express (ECX2)/China AW Loop1 (AW1) CMA CGM Adams 14,414

Gulf Coast China 1(GCC1)/ Pacific Gulf 6(PG6) APL California 6,350

Gulf Coast China 2(GCC2) COSCO Auckland 4,249

Pacific China Central 2(PCC2) /HRX/Yangste KOTA PURI 11,923

Pacific China Central1 (PCC1)/Hibiscus Express OOCL LUXEMBURG 8,063

Pacific China North1(PCN1)/bohai COSCO Italy 13,386

Pacific China South 2(PCS2) EVER Ursula 5,652

Pacific North West 1(PNW1)/Dhalia/ Pacific Northwest Loop

4(NP4) OOCL Vancouver 5,888

Pacific Northwest Pendulum (PNW2) APL Southampton 10,800

CMA CGM Aquila 11,356

Pacific Northwest Pendulum (PNW4) CSCL Bohai Sea 10,036

CMA CGM

PRX/AAS2/Pacific China South 1(PCS1)/South China Loop1(SC1) Bougainville 18,000

THE East Coast Loop2(EC2) Seaspand Hudson 10,000

East Coast Loop3(EC3) Houston Bridge 9,600

YM Uniform 8,626

Pacific North Loop1(PN1) MOL Creation 8,110

ONE Contribution 8,560

Pacific North Loop3(PN3) YM Ultimate 8,204

Pacific South Loop4(PS4) YM Milestone 6,589

Pacific South Loop5(PS5) ONE Commitment 8,560

YM Utmost 8,200

Pacific South Loop6(PS6) NYK Adonis 9,592

Pacific South Loop7(PS7) Aristomenis 9,954

2M PEARL TBA 0

Yulan/TP3 TBA 0

2M + Zim AMBERJACK/ZCP/TP10 TBA 0

ORIENT/ZP8/TP8 GUNVOUR Maersk 6,600

PELICAN/ZGX/TP88 TBA 0

Others PN2 TBA 0

PNS AS MORGANA 4,255

SCHUBERT 4,255

27 September Grand Total Copyright © 2017 Yusen Logistics. All rights reserved 81,129 99,363 54,443 13,852 1

2019You can also read