Complete Guide To The Motley Fool Singapore's - Buying The Best Singapore REITs

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

BROUGHT TO YOU BY THE MOTLEY FOOL SINGAPORE The Motley Fool Singapore’s Complete Guide To Buying The Best Singapore REITs

All information is provided exclusively by The Motley Fool Singapore Pte Ltd, a licenced

investment advisory research provider (MAS Financial Adviser’s Licence No. FA100056-1). Any

information, commentary, recommendations or statements of opinion provided here are for

general information purposes only. It is not intended be personalised investment advice or a

solicitation for the purchase or sale of securities. Before purchasing any discussed securities, please

be sure actions are in line with your investment objectives, financial situation and particular needs.

International investors may be subject to additional risks arising from currency fluctuations and/

or local taxes or restrictions. The information contained in this publication are obtained from, or

based upon publicly available sources that we believe to reliable, but we make no warranty as to

their accuracy or usefulness of the information provided, and accepts no liability for losses incurred

by readers using research. Recommendations and opinions are subject to change without notice.

Please remember that investments can go up and down, including the possibility a stock could

lose all of its value. Past performance is not indicative of future results.

Copyright © 2018 The Motley Fool Singapore Pte. Ltd. All rights reserved. No part of this

publication may be reproduced, stored, transmitted in any form of by any means without The

Motley Fool’s prior written consent. Company Reg. No. 201227853N

All performance information was current as of the date each article was originally published,

which we’ve disclosed throughout. The articles in this publication have been reproduced from

www.Fool.sg with minimal changes.

Disclosure: The following disclosure is accurate as of the time of publication (5 September 2018).

Chin Hui Leong owns shares in Berkshire Hathaway B, CapitaLand Mall Trust, Frasers Centrepoint

Trust, Mapletree Logistics Trust, Parkway Life REIT, Singapore Exchange and Suntec REIT. Chong Ser

Jing owns shares in Berkshire Hathaway B, Frasers Commercial Trust, Mapletree Commercial Trust,

Mapletree Industrial Trust and Mapletree Logistics Trust. David Kuo owns shares in Ascott Residence

Trust, CapitaLand Commercial Trust, CapitaLand Retail China Trust, CapitaLand Mall Trust, First

REIT, Frasers Centrepoint Trust, Keppel REIT, Mapletree Commercial Trust, Mapletree Industrial Trust,

Parkway Life REIT, Singapore Exchange Limited and Starhill Global REIT. Jeremy Chia owns shares in

Berkshire Hathaway B, EC World REIT, First REIT and Keppel REIT. Sudhan owns shares in CapitaLand

Commercial Trust, CapitaLand Mall Trust and Singapore Exchange Limited. The Motley Fool Singapore

has recommendations on Ascott Residence Trust, CapitaLand Commercial Trust, CapitaLand Mall

Trust, CapitaLand Retail China Trust, First REIT, Frasers Centrepoint Trust, Mapletree Commercial Trust,

Mapletree Industrial Trust, Parkway Life REIT and Singapore Exchange Ltd.

Visit us online at www.Fool.sg

2 The Motley Fool Special Report fool.sg

Table of Contents

Introduction

What Are REITs?

• 5 Facts About Singapore-Listed REITs

• 5 Largest REITs in the Singapore Stock Market

REITs Versus Investing in Other Instruments

• Do You Know the Difference Between REITs, Property Trusts, and Stapled Securities?

• The Pros and Cons of Investing in REITs

• 8 Differences Between Investing in REITs and Physical Properties

• Why I Invest in REITs Over Treasuries and Corporate Bonds

S-REIT Regulations

• New REIT Regulations: What Investors Need to Know

REIT Structure

• What Investors Should Know About a Typical REIT Structure Using Frasers Centrepoint Trust as

an Example

Different Type of REITs Available

• 8 Different Types of REITs and Stapled Trusts Listed in Singapore

REIT Financial Statements

• How to Choose the Best REITs to Invest In?

REIT Valuation

• Valuing REITs: A Quick Primer

Choosing the Best REITs

• 3 Factors to Consider When Investing in REITs

• How to Identify REITs That Have a Portfolio That Can Appreciate in Value

• How to Sieve out the Best REITs from the Rest?

• 3 Factors to Consider When Analysing a REIT

Types of REITs to Avoid

• 4 Types of REITs to Avoid

• Three Red Flags When Investing in REITs

Risks When Investing in REITs

• Why You Shouldn’t Invest in REITs

• 3 Big Risks Investors Must Know About A Real Estate Investment Trust

REIT Exchange-Traded Funds (ETFs)

• REIT ETFs Listed in Singapore: 5 Quick Points of Comparison

• What Investors Should Know About Lion-Phillip S-REIT ETF

Commonly Used Terms in REITs Investing

• REIT Jargon Demystified: Commonly-Used Terms That REIT Investors Should Know

Bonus Contents

• REIT Investing Made Simple: A Checklist to Pick Out the Best REITs

• Are REITs Worth Considering When Rates Rise?

• 2 REITs To Buy for Your Parents

• 2 REITs That Have Increased Their Distribution Per Unit for Five Consecutive Years

• 3 Ways REITs Can Grow Their Distributions

• 2 REITs That Give Exposure to the Fast-Growing China Property Market

fool.sg Special Report The Motley Fool 3

Introduction

Dear fellow investors,

Real estate investment trusts, or REITs as they’re commonly known, are really popular

among investors in Singapore’s stock market. There’s a good reason for that. REITs

generally have high distribution yields and can thus provide a steady stream of passive

income for investors.

But, with over 40 REITs in Singapore’s stock market right now, navigating through

them can be a tricky affair. Besides, a REIT need not necessarily be a good investment

just because it has a high distribution yield. It’s for these reasons and more, that we, at The

Motley Fool Singapore, have been writing and publishing many articles on REITs at our

flagship website, Fool.sg, over the years.

In this complete Singapore REITs (S-REITs) guide, we have compiled all the best REIT-

related articles on Fool.sg. These articles touch on a wide range of topics, from the basics of

REITs, to the risks involved when investing in them.

So, sit back, and enjoy the Foolish guide we have compiled just for you. We hope you’ll

be a much savvier – and richer – REIT investor after reading our carefully-prepared guide.

Fool on!

The Motley Fool Singapore

September 2018

4 The Motley Fool Special Report fool.sgWhat Are REITs?

5 Facts About Singapore-Listed REITs

Jeremy Chia | December 21, 2017

Singaporeans love to invest in real estate. It is, 5) 3 REIT listings in Singapore this

therefore, no surprise that real estate investment

trusts (REITs) have been a popular investment year

vehicle in Singapore since its debut in 2002. Without There were a total of three new REITs that listed

further ado, here are five interesting facts about in Singapore this year. The strong performance of

REITs in Singapore. REITs in Singapore in the past and the attention it

garners from Singaporean investors have been key to

1) Singapore is the second largest attracting listings in Singapore.

REIT market in Asia The Foolish bottom line

Singapore has been a popular destination for REIT Investing in REITs in Singapore has rewarded

listings. Since its debut in 2002, the Singapore REIT shareholders handsomely in recent years. This year

market has grown to become the second largest REIT was an exceptionally good year for REITs as more

market in Asia, behind Japan. investors gained confidence in the property market

2) There are a total of 44 REITs

and property-related trusts and

securities in Singapore

There have been numerous REIT and property

related trusts listing each year. The total tally now

stands at 44. They each offer their unique value

proposition and area of specialty, giving investors a

variety of options to choose from.

3) There are 3 REIT ETFs in

Singapore

REIT exchange-traded funds (ETFs) track the

performance of a group of REITs, giving investors

exposure to a larger portfolio of properties.

4) REITs have outperformed the

Straits Times Index in recent years

A widely-used Singapore REIT index, which

consists of the 20 largest and most traded REITs in

Singapore, delivered 11.1% annually for the past

five years. The Straits Times Index (SGX: ^STI),

on the other hand, only returned 5.6% annually

during the same period.

fool.sg Special Report The Motley Fool 5What Are REITs?

5 Largest REITs in the Singapore Stock Market

Sudhan P. | April 6, 2018

Real estate investment trusts (REITs) are popular fall in distribution per unit (DPU) to 8.66

among Singaporeans. REITs are obliged to distribute cents for the full year ended 31 December

at least 90% of their taxable income to enjoy tax 2017. The fall was despite gross revenue for

benefits. Therefore, by investing in REITs, investors the year growing 13% to S$337.5 million and

can receive regular distributions, usually on a NPI going up 14.8% to S$265.5 million. An

quarterly basis. enlarged units base, which arose due to a rights

According to a recent report by Singapore issue in October 2017 to partially fund the

Exchange Limited (SGX: S68), Singapore’s five acquisition of the retail and office components

largest REITs (in terms of market capitalisation) of Asia Square Tower 2, took a significant toll

have a distribution yield of 5.6% on average. This is on the REIT’s DPU.

higher than the yield of the SPDR STI ETF (SGX: 4. Next in line is a diversified REIT, Suntec

ES3), which can be taken as a proxy to the Straits Real Estate Investment Trust (SGX: T82U),

Times Index (SGX: ^STI), at 3%. (Note: All market which owns both retail and office properties.

capitalisation and distribution yield data are as at 4 For the full year ended 31 December 2017,

April 2018.) gross revenue grew 7.8% year-on-year to

With that, let’s look at those five REITs and their S$354.2 million while NPI went up by 8.9% to

latest financial performance: S$244.5 million. The improvements were due

to the contribution from Australia’s 177 Pacific

1. With a market capitalisation of S$7.62 billion Highway, which was partially offset by lower

and topping the list is Ascendas Real Estate retail. The REIT has a market capitalisation of

Investment Trust (SGX: A17U), an industrial S$4.95 billion.

REIT. In the third quarter ended 31 December

2017, the REIT saw its gross revenue grow by 5. Last but not the least, Mapletree Commercial

4.1% year-on-year to S$217.3 million while its Trust (SGX: N2IU) takes the final spot with

net property income (NPI) rose 1.7% to S$157.6 a market capitalisation of S$4.55 billion. The

million. However, its distribution per unit (DPU) REIT, which has stakes in five office and retail

slipped 0.6% to 3.97 cents. assets in Singapore, saw its gross revenue for

the third quarter growing 0.8% year-on-year

2. Next on the list is retail REIT, CapitaLand to S$109.7 million. Meanwhile, NPI improved

Mall Trust (SGX: C38U). For the full year 1.9% to S$86.0 million. The REIT attributed

ended 31 December 2017, gross revenue the increases to higher contributions from

tumbled 1.1% year-on-year to S$682.5 VivoCity and Mapletree Business City I.

million while NPI slipped 0.3% to S$478.2

million. The declines were mainly due to the

non-contribution of Funan, which was closed

in July 2016 for redevelopment. Despite the

falls, 2017’s DPU inched up 0.3% to 11.16

cents. CapitaLand Mall Trust has a market

capitalisation of S$7.27 billion.

3. Coming in third and sporting a market

capitalisation of S$6.54 billion is CapitaLand

Commercial Trust (SGX: C61U). The

commercial REIT posted a 4.6% year-on-year

6 The Motley Fool Special Report fool.sgREITs Versus Investing in Other Instruments

Do You Know the Difference Between REITs, Property Trusts,

and Stapled Securities?

Jeremy Chia | December 27, 2017

Most of you have likely heard of real estate limits that are placed on REITs. Because of fewer

investment trusts, or REITs. But, do you know that restrictions, they do not receive the same tax benefits

there are also two other kinds of investment vehicles that REITs enjoy.

in Singapore’s stock market that are commonly

mistaken for REITs? These are property trusts and The lowdown on stapled securities

stapled securities. Stapled securities are listed property securities that

The two investment vehicles are similar to REITs in are a bundled combination of either REITs, property

many ways – even seasoned investors occasionally use investment companies, property trusts, or business

the three terms interchangeably. It is important to note trusts. This occurs when the investment vehicle wants

though, that there are fundamental differences between to apply a REIT model to a portion of its property

REITs, property trusts, and stapled securities. portfolio, but not to others. As such, only that part

of the property portfolio will be bounded by REIT

As investors, it is important that we are familiar

regulations and enjoy the associated tax benefits.

with these differences so that we can make informed

decisions. With that, here are the important Likewise, stapled trusts are obligated to pay the

differences between the three types of investment required distributions to their unitholders only for the

vehicles that you should be aware of. properties that are bound by the REIT structure.

The lowdown on REITs The Foolish bottom line

REITs are collective property investment trusts REITs, property trusts, and stapled securities, though

that pool money to invest in properties. Investors can similar, are actually bound by different regulations and

purchase units of a REIT through the stock exchange. consequently have their pros and cons.

But what makes a REIT different from a company As investors, we cannot oversimplify the

that invests in properties? Well, for one, a REIT is investment process by lumping all of them together.

bounded by more restrictions and regulations. They have their own risk-reward profile and can offer

In Singapore, REITs must pay out at least 90% of investors different value propositions. Hopefully, this

their distributable income to unitholders each year. article helps clarify the differences between the three

They are also limited to a maximum gearing ratio of and allows you to make more informed investment

45%. The restrictions can hinder a REIT’s business, decisions in the future.

but they do come with some benefits. For instance,

REITs enjoy favourable tax treatments compared to

other types of companies.

The lowdown on property trusts

Like REITs, property trusts also pool money to

invest in property. Investors can also buy units of

these trusts on the stock exchange.

The key difference between a property trust and

a REIT is that the former has no restrictions on the

amount it must distribute to its unitholders. Property

trusts are free to reinvest their money in any way

they wish. They are also not subjected to leverage

fool.sg Special Report The Motley Fool 7REITs Versus Investing in Other Instruments

The Pros and Cons of Investing in REITs

Jeremy Chia | December 12, 2017

Unsure whether to invest in real estate investment Key disadvantages as compared to stocks

trusts (REITs) or stocks? Well, before you make • Highly leveraged

a decision, it is important that you know the

differences between the two. REITs are usually highly leveraged investment

vehicles. This works as a double-edged sword.

In this article, I will run through some of the pros Leveraging allows REITs to purchase more assets

and cons of investing in REITs and stocks. than they have in unitholders’ equity. At the same

time, leverage poses additional risks as REITs

Key advantages as compared may face difficulty paying off its debt in difficult

to stocks times. As such, investors need to find REIT

• Predictable cash flow and dividends investments that have lower leverage to survive

through any exigencies.

Because REITs are required to give out 90% of

their income as dividends, investors should be • Unable to reinvest and grow

fairly certain that they would consistently get The fact that REITs are required to pay out 90%

dividends as long as the REIT continues to be of their income to unitholders works as a double-

profitable. REITs also tend to sign long-term edged sword too. Although unit holders can sleep

leases with their tenants. Because of this, easy knowing they can earn consistent dividends,

investors are able to predict the long-term REITs are not able to reinvest in their portfolio,

revenue of a REIT accurately. hence can remain stagnant for many years. The

• History of outperforming the market index two ways to grow are through issuing new units

that will dilute current unitholders’ equity or by

In the last five years, Singapore REITs as a increasing its borrowings from banks.

whole have returned more than the Straits

Times Index (SGX: ^STI). Even in the • Concentration risk

United States, REITs have had a history of Naturally, REITs, because of their focus on

outperforming the S&P 500, Dow Jones properties, will be affected when the property

Industrials and NASDAQ Composite indexes. market faces a downturn.

• REIT prices are less volatile

The Foolish bottom line

The beta of REITs, a measure of volatility, and

REITs and stocks can be good long-term

consequently, risk, has been historically much

investment vehicles for investors. However, knowing

lower than stocks at most times. This is because

the pros and cons of each instrument is important for

of the relatively predictable nature of REITs’ cash

investors who are deciding between the two.

flows and business.

• There are many types of REITs to choose from

There are 32 REITs to choose from in Singapore

that can be further divided into different

categories. These include healthcare, residential,

commercial, retail and mixed REITs. Investors

who are looking for overseas exposure also have

the option of choosing REITs that have a portfolio

of properties located outside of Singapore.

8 The Motley Fool Special Report fool.sgREITs Versus Investing in Other Instruments

8 Differences Between Investing in REITs and Physical Properties

Stanley Lim Peir Shenq, CFA | December 2017

If you are reading this, you may wonder, ‘How can its down payment, renovation costs, legal fees and

I be the next Li Ka Shing or Donald Trump when stamp duties. Let’s assume that 10% down payment

I’m just a wage earner?’ Or, perhaps, you may have is required. The legal fees and stamp duties work

accumulated some savings, and you are contemplating, out to be 5% of the property price. Thus, if the small

‘Should I start investing in a small apartment for rental apartment costs $300,000, you may need to prepare

income or build a portfolio of real estate investment a minimum of $45,000 in upfront capital to consider

trusts (REITs) that generate high dividend yields?’ the purchase. In fact, you need to prepare more as

In this article, I will share eight key differences you may need to do some minor renovation and

between investing in the two. From this, I believe service your mortgage.

it would help you to decide which of the two you What about REITs? You can start investing in REITs

should go for. with just a few hundred dollars. Of course, that is not

advisable as the transaction costs are relatively high.

Loan Eligibility It is best to invest a minimum of $3,000 to make the

This varies between banks and the country of your investment more meaningful and worthwhile. Thus, if

residence. In general, you should maintain a good you do not have much capital to start with, you may

credit score at all times so that you can qualify to consider REITs as an investment option.

get a loan to buy properties. If you are currently

eligible for a mortgage, perhaps, you should invest in Liquidity

physical properties. However, if you are not eligible Selling a physical property could be a major

for mortgages, then, your best alternative may be to decision for you. You may have to advertise and

invest in REITs. negotiate to find the right buyer who offers a good

price for your property. The whole process could take

Growth months or even years before the sale of your property

How fast are you able to grow your investment is concluded.

portfolio? Well, it depends on your financial status It is different for REITs as you can buy and sell

which impacts the maximum amount of mortgage REITs like any stock listed on the stock exchange

that you can qualify for. If you intend to borrow with just a few clicks of the button. There is usually

more, then, you need to grow your income. Thus, the always a ready buyer and a ready seller who is

ability to grow your portfolio of physical properties willing to buy your units in REITs. Here, there are no

is dependent on your ability to grow your income. advertisements, negotiations and real property gain

However, this is not the case for REITs. They tax to be incurred from the disposal of your REITs.

usually have stronger financial positions compared Thus, REITs are more liquid as the process of buying

to any individual on the street. Hence, they are more and selling the units are easier and convenient than

efficient and more capable of raising funds from banks physical properties.

and new investors to finance their acquisition of new

properties, thus, growing their portfolios. As such, Quality of Tenants

the portfolio growth in REITs is dependent on their If you invest in REITs, you will derive income

financial positions, not yours as individual investors. from a pool of commercial tenants. These tenants

vary according to the type of REITs you choose.

Capital For instance, if you buy a retail REIT, you would

If you are planning to buy a small apartment, you expect to receive income from retailers. If you buy

may need to prepare a sum of capital which includes

fool.sg Special Report The Motley Fool 9hospitality-based REITs, you would expect income capital gains if their prices appreciate. It is similar

from the operations of hotels. to investing in physical properties where you

When you buy REITs, the quality of tenants is receive rental income and enjoy long-term capital

usually far more superior than one individual who appreciation.

intends to occupy your apartment. This is because The difference lies in their tax treatment. Once

they typically have stronger financial positions, again, their treatment would differ according to your

a brand and a reputation to protect. Thus, there is country of residence.

lesser risk of rental default from commercial tenants For instance, you may not need to pay income

as compared to tenants we get from renting out tax on distributions received from REITs. However,

properties. you would most likely pay income tax on rental

income from your small apartment. Hence, it is wise

Lease Periods to consider tax issues before you venture into any

Lease tenure varies according to the type of investment.

properties. For instance, it is common for retail

leases to be around three years. Meanwhile, leases The Foolish Takeaway

to the hotel and hospital operators have a duration of Should you go for a small apartment or build a

10 – 20 years. REIT portfolio? Once again, it depends on your

If you intend to rent out a small apartment, the personality, financial standing, and investment

tenancy agreement is usually for a shorter period. motives. It is prudent to explore and evaluate the pros

The duration may vary between six, 12 or 24 months, and cons of each investment vehicle before investing

subject to the common practices of the rental market to make prudent investment decisions.

in a country. The continuity of your rental income

depends on your ability to attract, retain and collect

money from your respective tenant for as long as you

possibly can.

Would you like to receive uninterrupted income

consistently from making a one-time investment in

a REIT over the next five, 10 or 20 years, or worry

about fluctuations in your rental income?

Management

I believe there are two main objectives of property

management. Firstly, it is about collecting money

from tenants as much and as efficiently as possible.

Secondly, it is about enhancing the value of the

property over the long-term. It involves continuous

maintenance of properties – from minor repairs to

major renovations and refurbishments.

If you invest in a small apartment, then, it may

certainly be helpful to have a reliable handyman or

a contractor to assist you in this area if you wish to

delegate. If you invest in REITs, you are relying on

the professional expertise of the appointed property

managers to carry out a good job to manage the

properties within the portfolio.

Tax Issues

If you invest in REITs, you will receive

distributions as a form of passive income and enjoy

10 The Motley Fool Special Report fool.sgREITs Versus Investing in Other Instruments

Why I Invest in REITs Over Treasuries and Corporate Bonds

Jeremy Chia | April 30, 2018

With interest rates set to rise this year and REITs Limited downside risks

having generally richer valuations compared to last

annum, many investors may be tempted to switch As with any publicly traded security, REITs are

from REITs to historically safer assets such as susceptible to volatility and changes in prices.

treasuries or corporate bonds. Distributions per unit may also decrease over time.

However, the long-term trend of REITs in Singapore

However, I feel that switching from REITs to bonds suggests that REITs are unlikely to underperform

may end up dragging your investment returns over for extended periods.

the longer term – even as interest rates rise. Don’t

get me wrong, I absolutely agree that treasuries and REITs in Singapore need to maintain a gearing ratio

corporate bonds are perhaps safer options than REITs. of 45%. Because of that, REIT managers, no matter

Bonds and treasuries have a stable coupon rate and how gung-ho, have to keep their balance sheet in check

the principal (if held to maturity) is more secured for the authorities. Although it may limit their growth,

than REITs. The rising interest rate environment will it means that they are unlikely to face liquidity issues.

also increase the yield on both bonds and treasuries, Real estate also tends to have a much more

while it will be a drag to a REIT’s profitability due to a consistent and stable income stream than companies.

generally higher interest expense. This means that volatility in REIT prices have

Having said that, I believe REITs still possess historically been much lower than traditional stocks.

much greater long-term potential than both treasuries

and bonds. REITs generally have a higher yield, and

Distributions growth

the property market — despite its cyclical nature Finally, and perhaps the most appealing aspect

— historically always ends up outperforming bonds about REITs, is the fact that REITs, unlike bonds are

and treasuries over the long term. So here are three able to grow its distributions each year. If a REIT

reasons why I will still choose REITs over other manages its capital well and is able to improve the

income-producing assets. yield on its properties, they can grow its distributable

income, rewarding shareholders in the process.

Higher yields For instance, some REITs listed in Singapore have

REIT prices in Singapore surged last year, as most grown its DPU by 6-7% a year. That means that

investors were bullish about the property market. in 10-12 years, its DPU would have doubled. If an

However, even at these prices, REITs still offer unit investor had initially purchased the REIT at a yield

holders a much higher yield than most bonds and of 6%, he would be enjoying a 12% yield on his

treasuries. At the time of writing, the lowest yielding investment. This is a huge upside that REITs have

REIT has a distribution yield of 4.67%, while the over bonds and treasuries, which have a fixed rate

highest is yielding 8.71%. throughout their lifespan.

The 30-year government bonds are 2.9%, while

one-year treasury bills have a yield of just 1.59%.

The Foolish bottom line

High yielding corporate bonds have a coupon rate of As an investor, I am personally always looking

3 to 5.3%. Even perpetuities, where investors do not for the best risk-reward investments. As shown from

get their principal back, have a yield of just 6%. above, I think REITs undoubtedly have a much larger

reward profile than bonds and treasuries. Furthermore,

You may be wondering how sustainable REIT’s

the limited downside risk makes them a relatively safe

yields are. Well, REITs in Singapore have historically

investment. I am confident in saying that investors

performed very well. Properties also tend to grow in

who choose REITs over bonds will most likely feel

value, meaning the REITs book value will increase

very happy about their decision over the long term.

over time. This makes it an even more attractive

proposition for investors.

fool.sg Special Report The Motley Fool 11S-REIT regulations

New REIT Regulations: What Investors Need to Know

Chong Ser Jing | July 3, 2015

Yesterday evening, the Monetary Authority of Think about it this way. Say you had 100 units of

Singapore (MAS) issued a list of changes to the a REIT in 2010 and after five years in 2015, you still

regulations affecting real estate investment trusts own the same 100 units.

(REITs) in Singapore. Over that period of time, the REIT’s distributions

The MAS had first announced back in October grew by 100% from S$100 million to S$200

2014 that it wanted to refine REIT regulations and had million; that’s a very commendable performance.

come up with a list of proposed changes. After inviting But because its unit count had doubled from

feedback from the public and thinking through them 100 million to 200 million as a result of private

for a number of months, the MAS has settled on the placements and the payment of management fees

changes, which were released yesterday evening. with new units, the REIT’s distribution per unit had

Here’re some of the important ones (along with stayed flat at S$1. And you, as the investor, would

my comments). not have any added benefits whatsoever despite the

REIT having doubled its distributions.

On changes to the fee structure So, keep an eye on whether a REIT’s Manager’s

“MAS will not intervene on the structure of fees or fees are based at least partly on growth in the REIT’s

types of fees that Managers charge, but will require per unit figures. If that’s not the case, then take a hard

them to disclose the justification for each type of look at the justifications given by the Manager and

think it if makes sense.

fees charged. Managers will also have to explain the

methodology for computing performance fees, and With all that said, it’s worth stressing that having

justify how this methodology takes into account the right incentives is no panacea for a winning

unitholders’ long-term interests.” investment. Hutchison Port Holdings Trust (SGX:

NS8U) had fee structures which are very much

Investor maestro Charlie Munger has described aligned with unitholders’ interests. Sadly though,

incentives as one of the most important forces that can its total return (including gains from reinvested

shape human behaviour. To that point, Munger once dividends) from the close of its first-day of trading

said, “I think I’ve been in the top 5% of my age cohort in March 2011 to today is a negative 10.5%. There

all my life in understanding the power of incentives, are many other important factors to consider – such

and all my life I’ve underestimated it.” as the type and quality of the properties in a REIT’s

With the right incentives in place in terms of portfolio – when making an investment.

Manager fees that are aligned with unitholders’ long-

term interests, investors in REITs can thus stand a On changes to leverage limits

better chance of having a profitable experience. “The leverage limit imposed on a REIT will be

But what should unitholders look out for? This increased from 35% to 45% of the REIT’s total assets,

ties back to what truly drives the economic value of but a REIT will no longer be allowed to leverage up to

a REIT and that is, growth in its per unit figures like 60% with a credit rating.”

its distributions and net asset value. Warren Buffett, REITs in Singapore have so far been rather

Munger’s long-time business partner and an even disciplined in terms of risk-taking. When the MAS

larger investing father-figure, once said (emphasis first announced its proposals to change REIT

mine), “We do not measure the economic significance regulations last October, it mentioned that “most

or performance of Berkshire [the conglomerate [REITs]… have kept their leverage ratios within 35%”

controlled by Buffett] by its size; we measure by even though two-thirds of them had credit ratings and

per-share progress.” could thus have geared themselves up to 60%.

12 The Motley Fool Special Report fool.sgBut, greater leverage comes with higher risks.

As such, investors may still want to keep an eye on

how the balance sheets of their REITs are changing

given that they now have more leeway to take on

more borrowings.

On changes to remuneration

policies

“Managers will be required to disclose their

remuneration policy and procedures in the REITs’

Annual Reports.”

With better disclosure, investors can then make

sounder judgements on whether the policies

are reasonable or not. This is similar to the fee

structure changes mentioned earlier in the sense

that remuneration polices which are aligned with

unitholders’ interests can help increase the odds that the

REIT will be a good investment for the latter group.

Some yellow flags to watch out for could be

remuneration policies for management personnel

which does not take into account, or only gives

little consideration to, growth in important

drivers of a REIT’s economic value such as those

mentioned earlier.

A Fool’s take

There’re a lot more to the new regulations

governing REITs and the complete list can be found

on MAS’ website. The changes to the rules will

be implemented in phases starting from 2016; in

particular, REITs will have to start adhering to the

new disclosure standards for Manager fees by the

first Annual General Meeting of the financial year

ending on or after 31 December 2015.

fool.sg Special Report The Motley Fool 13REIT Structure

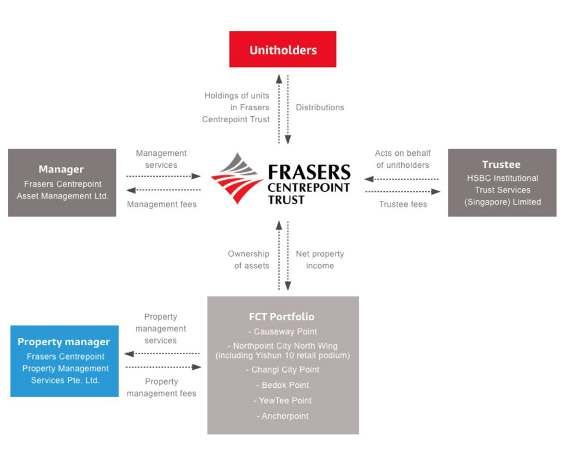

What Investors Should Know About a Typical REIT Structure

Using Frasers Centrepoint Trust as an Example

Sudhan P. | July 13, 2018

Real estate investment trusts (REITs) offer an Trustee

alternative to owning properties.

A trustee holds the underlying properties of a REIT

Under a REIT structure, investors’ (called on behalf of unitholders. The trustee’s role is to ensure

unitholders) money is pooled together to invest in that the REIT is complying with all applicable laws,

a portfolio of income-generating real estate such as and that the rights of unitholders are protected. In

offices, hotels, hospitals, and shopping malls. Just exchange for providing the services, the trustee is paid

like stocks, they can be bought and sold on a stock a fee. For Frasers Centrepoint Trust, the trustee’s fee is

exchange. In return for their capital, unitholders 0.1% per year of the value of the REIT’s properties.

receive regular distributions from the REITs.

The first Singapore REIT, CapitaLand Mall Trust Manager (or REIT manager)

(SGX: C38U), was listed in July 2002. It is also the The REIT manager is a separate company set

largest retail REIT by market capitalisation of S$7.4 up to run the REIT. It is usually a wholly-owned

billion, as at 31 March 2018. It retail peer would be or partly-owned subsidiary of a REIT’s sponsor

Frasers Centrepoint Trust (SGX: J69U), which is (more on sponsors later). The chief executive officer

also a retail REIT that owns shopping malls such as (CEO) of a REIT manager is just like the CEO of

Causeway Point and Changi City Point. any listed company.

Since REITs have a structure that is different from The central role of a REIT manager is to set the

listed companies, it would be useful to go through strategic direction for the REIT, and enhance the

a typical trust structure to help investors better REIT’s property value to maximise rental income,

understand REITs. which leads to higher distributions for unitholders.

Let’s use Frasers Centrepoint Trust’s structure as an A REIT manager also supervises a property

example here. manager (explained below) in its day-to-day

management of the assets.

REIT managers are paid recurring management

fees for their services. Frasers Centrepoint Trust’s

manager receives a base fee of 0.3% per annum of

the value of the REIT’s properties and a performance

fee of 5% per year of the net property income (NPI).

The manager can choose to receive the payments in

cash or units, or both.

Frasers Centrepoint Trust’s manager is also entitled

to receive an acquisition fee of 1% of the acquisition

price and a divestment fee of 0.5% of the sale price on

all acquisitions or disposals of assets.

Property manager

The property manager takes care of the day-to-day

operations of the properties in the REIT’s portfolio.

This includes daily upkeep of the properties, running

Source: Frasers Centrepoint Trust corporate website marketing events to attract tenants or shoppers (in the

14 The Motley Fool Special Report fool.sgcase of shopping malls), and ensuring the best tenancy mix to maximise rental income. In return, the property manager is paid a property management fee. For Frasers Centrepoint Trust, the property management fees are 2% per annum of gross revenue, and 2% to 2.5% per year of NPI. Sponsor (not present in all REITs) One thing missing from the flowchart above is the sponsor. In Frasers Centrepoint Trust’s case, the sponsor is Frasers Property Ltd (SGX: TQ5). Not all REITs have a sponsor. A sponsor typically supplies the properties to be placed into the REIT’s initial portfolio, and may continue to provide a pipeline of assets for the REIT. Most of the time, the sponsor also owns large stakes in the REIT manager, and the REIT. Frasers Property, which has full ownership of five retail malls in Singapore, except for one, could inject these properties into Frasers Centrepoint Trust’s portfolio in the future. The five properties are Northpoint City South Wing, Robertson Walk, Valley Point, The Centrepoint, and Waterway Point (33.3% ownership). As of 24 November 2017, Frasers Property had a 41.86% stake in Frasers Centrepoint Trust. The Foolish takeaway Understanding the different players in typical REIT structure helps investors to better appreciate how REITs function. Armed with this knowledge, they can make a more informed decision when investing in REITs. Some REITs with overseas properties may have additional layers, but the main trust structure is usually the same as what we have seen above. fool.sg Special Report The Motley Fool 15

Different Type of REITs Available

8 Different Types of REITs and Stapled Trusts Listed in Singapore

Sudhan P. | July 12, 2018

There are around 40 real estate investment trusts Industrial

(REITs) and stapled trusts in Singapore currently.

The REITs and six stapled trusts had an average The industrial sub-segment covers properties

distribution yield of 6.7%, as of 6 July 2018. The such as factories, warehouses and business parks.

figure is an average, so some REITs will have an Singapore’s largest REIT in terms of market

above-average yield while others will be below- capitalisation comes from this sub-sector, and

average. A REIT’s distribution yield can be affected that is Ascendas Real Estate Investment Trust

by a number of factors; one such factor is the sub- (SGX: A17U). Industrial REITs usually have high

segment in which the REIT operates in. distribution yields due to the short 30-year leases

that most Singapore industrial properties have as

With that in mind, let’s look at the various compared to retail or office real estate.

sub-segments a REIT or stapled trust operate in, as

categorised by the Global Industry Classification Others industrial REITs include AIMS AMP

Standard (GICS). Capital Industrial REIT (SGX: O5RU), Cache

Logistics Trust (SGX: K2LU), Mapletree Industrial

Retail Trust (SGX: ME8U) and Mapletree Logistics Trust

(SGX: M44U).

This sub-segment holds real estate used for retail

activities such as shopping centres, something that Office

most investors would be familiar with. To know if

a certain shopping mall is doing well, investors can This sub-segment owns properties that are used

simply walk into the mall and observe the shopper for office or commercial purposes. The largest office

traffic, the type of tenants, and whether the mall REIT listed here is CapitaLand Commercial Trust

is fully occupied with tenants. The popularity of (SGX: C61U). In recent times, the distribution yields

retail REITs could be why it tends to provide lower for some office REITs have been falling due to higher

distribution yields as compared to other REIT REIT unit prices resulting from a pickup in the

sub-segments. commercial sector.

Retail REITs with assets solely in Singapore Other listed commercial REITs include Frasers

include CapitaLand Mall Trust (SGX: C38U), Commercial Trust (SGX: ND8U), Keppel REIT

Frasers Centrepoint Trust (SGX: J69U) and SPH (SGX: K71U) and Manulife US Real Estate

REIT (SGX: SK6U). Investment Trust (SGX: BTOU).

Retails REITs such as CapitaLand Retail China Hotel & Resort

Trust (SGX: AU8U), Lippo Malls Indonesia Retail

This sub-segment hosts hospitality-related properties

Trust (SGX: D5IU) and BHG Retail REIT (SGX:

such as hotels and serviced residences. The entities

BMGU) hold overseas retail properties.

in this sub-segment are often structured as a stapled

Starhill Global Real Estate Investment Trust trust. Stapled trusts in the hotel and resort sub-sector

(SGX: P40U) owns a mix of both local and include CDL Hospitality Trusts (SGX: J85), Frasers

overseas properties. Hospitality Trust (SGX: ACV) and OUE Hospitality

Mapletree Commercial Trust (SGX: N2IU), which Trust (SGX: SK7).

owns both retail and office properties, is classified

as a retail REIT under the GICS. The trust owns five Healthcare

properties, including VivoCity, Singapore’s largest REITs in this sub-segment hold healthcare-

retail mall, and Mapletree Business City. related assets such as hospitals and nursing homes.

16 The Motley Fool Special Report fool.sgDue to their resilient and stable nature, healthcare REITs are popular among investors. Therefore, such REITs usually offer lower distribution yields and trade at a premium to their book values as compared to other REITs. REITs in the healthcare sub-segment are First Real Estate Investment Trust (SGX: AW9U) and Parkway Life REIT (SGX: C2PU). Others: Specialized, Diversified and Residential There are other REITs and stapled trusts that do not fall into the sub-segments discussed above. Keppel DC REIT (SGX: AJBU), which owns data centres, falls under the specialized sub-sector. Mapletree North Asia Commercial Trust (SGX: RW0U), formerly known as Mapletree Greater China Commercial Trust, is a diversified REIT. REITs such as Viva Industrial Trust (SGX: T8B) and Suntec Real Estate Investment Trust (SGX: T82U) are also classified as diversified REITs. Meanwhile, Ascott Residence Trust (SGX: A68U) is a residential REIT. fool.sg Special Report The Motley Fool 17

REIT Financial Statements

How to Choose the Best REITs to Invest In?

Sudhan P. | June 26, 2018

When it comes to investing in real estate

investment trusts (REITs), most investors look at the

distribution yield as part of their decision-making

process. However, the distribution yield of a REIT

tells us nothing about the sustainability of its

distributions, nor the strengths or weaknesses of the

REIT’s business.

Instead of focusing solely on a REIT’s

distribution yield, REITs investors should also look

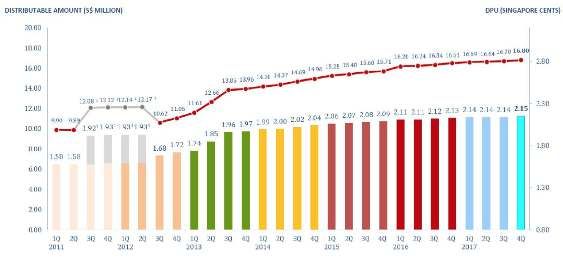

at other factors. Only then can they make a more Source: First REIT 2017 earnings presentation

informed investing decision with a REIT. Here are

I also look at whether a REIT’s distributable

the important factors I look at.

amount and distribution per unit (DPU) are

improving consistently every year, apart from its

Growth in the basic numbers gross revenue and NPI. Taking First REIT as an

Firstly, I like to investigate whether a REIT’s example again, its distributable amount and DPU

gross revenue, net property income (NPI), and can be seen to be rising steadily from 2011 to 2017

distribution to unitholders are growing consistently from the following chart:

on an annual basis.

Gross revenue is the income that a REIT earns

through rent, operation of car parks, and so on. After

deducting property-related expenses such as property

management fees, property taxes, and maintenance

expenses, we arrive at the NPI figure.

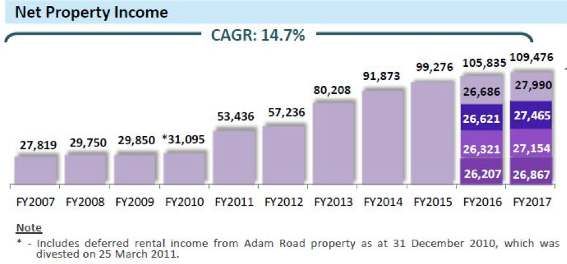

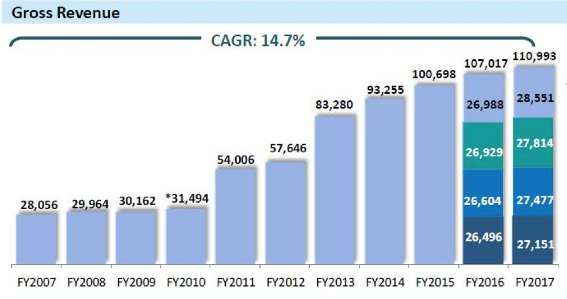

The chart below is an example from First Real

Estate Investment Trust (SGX: AW9U) that shows

growth of its gross revenue and NPI from 2007 to

2017. First REIT is a healthcare-focused REIT. Source: First REIT 2017 earnings presentation

Property yield

The property yield is the NPI divided by the

valuation of the properties held in a REIT’s

portfolio. This metric reveals the intrinsic strength

of the REIT’s underlying properties, and is more

critical than calculating the REIT’s distribution

yield (as the distribution yield is a function of the

REIT’s unit price).

In 2017, First REIT had an NPI of S$109.5

million and S$1.35 billion in investment

18 The Motley Fool Special Report fool.sgproperties. This equates to a property yield of which is a valuation metric. Other valuation metrics

8.1%. Property yields in the range of 5% to 9% are involve looking at the REIT’s capitalisation rate, net

great, in my opinion. asset value, or replacement cost.

The property yield can then be compared on

either a yearly basis to look for trends, or with other

The Foolish takeaway

REITs operating in the same industry. For example, Recently, my Foolish colleague, Jeremy Chia,

Parkway Life REIT (SGX: C2PU), another highlighted in his article that Cache Logistics

healthcare REIT, only had a property yield of 5.9% Trust (SGX: K2LU) had a distribution yield of

in 2017. In another instance, the two retail REITs, 8.3%. This is one of the highest yields in the

CapitaLand Mall Trust (SGX: C38U) and Frasers Singapore stock market.

Centrepoint Trust (SGX: J69U), had property However, after digging a little deeper, investors

yields of 5.8% and 4.9%, respectively, in 2017. would realise that the REIT has a relatively high

gearing ratio, and an unhealthy interest coverage

Gearing and interest coverage ratios ratio. These factors could ultimately put Cache

The gearing ratio and interest coverage ratio reveal Logistics Trust’s DPU at risk. Therefore, Foolish

the strength of a REIT’s balance sheet. investors should always look beyond distribution

The gearing ratio is calculated by dividing the yields when buying REITs.

total debt of a REIT by its total assets. As of 31

December 2017, Parkway Life REIT had a gearing

ratio of 36.4%. REITs in Singapore have a gearing

limit of 45%, as required by the Monetary Authority

of Singapore.

The interest coverage ratio is derived by dividing

a REIT’s NPI by its finance costs. At the end of

2017, Parkway Life REIT had an interest coverage

ratio of over 10. This shows that even if the REIT’s

NPI were to decline by 60%, it would still be able

to service its debt. I like to look for an interest cover

ratio that is above 4.

Other metrics to look at

Investors must also look at general operating

metrics such as the REIT’s portfolio occupancy

rate, and other metrics specific to a REIT. Two

REIT-specific metrics for retail REITs would be

shopper traffic numbers and tenants’ sales. For

hospitality REITs, investors can look at the revenue

per available room and average daily rate.

I also like to look at a REIT’s funds from

operations (FFO) and adjusted funds from

operations (AFFO). FFO strips off cost-accounting

methods such as depreciation of investment

properties that may inaccurately distort a REIT’s

cash-generating ability. The FFO is akin to the

operating cash flow of a company, while the AFFO

is like a company’s free cash flow.

Only after looking at all the factors mentioned

above do I look at the distribution yield of a REIT,

fool.sg Special Report The Motley Fool 19REIT Valuation

Valuing REITs: A Quick Primer

Sudhan P. | July 25, 2018

Real estate investment trusts (REITs) cannot As of 30 March 2018, Lippo Malls Indonesia

be valued by the typical price-to-earnings (P/E) Retail Trust had a NAV of S$0.30 per unit. This

ratio as their earnings are distorted by revaluation means that at a unit price of S$0.32, it is trading

of investment properties, change in fair value of at a P/B ratio of 1.07 ((S$0.32/S$0.30) x 100%).

derivatives, and so on. In other words, it means that investors who invest

How else can REITs be valued then? Let’s look at in Lippo Malls Indonesia Retail Trust are paying

some common ways of evaluating them. S$1.07 for S$1 worth of the REIT’s net assets.

Some REITs trade at a massive premium to their

Distribution yield NAV as the market perceives them to be safer or to

The distribution yield shows how much an possess strong fundamentals.

investor receives in distribution per unit (DPU)

for the unit price paid for a REIT. Since REITs are

Capitalisation rate

required to distribute at least 90% of their taxable Capitalisation rate, or cap rate, is a measure of the

income to their unitholders in order to enjoy tax return on investment of a property. It is derived by

benefits, many REITs have high distribution yields. taking the net property income (NPI) of a property

As of 6 July 2018, the average distribution yield for and dividing it by its value. For example, in 2017,

Singapore REITs was 6.7%. CapitaLand Mall Trust’s (SGX: C38U) Tampines

Mall had a valuation of S$1.05 billion and an NPI

Let’s go through a simple example to learn

of S$58.3 million. Therefore, its cap rate was 5.6%.

how to calculate a REIT’s distribution yield.

Retail REIT Lippo Malls Indonesia Retail Trust The cap rate can also be calculated on a portfolio

(SGX: D5IU)has a DPU of S$0.0322 for the last level and is sometimes known as the property yield.

12 months. At its unit price of S$0.32 at the time During the same year, CapitaLand Mall Trust had

of writing, it has a distribution yield of 10.1% an NPI of S$478.2 million and a portfolio value of

((S$0.0322/S$0.32) x 100%). S$8.31 billion, giving a capitalisation rate of 5.8%.

Most investors are usually enticed by a high Cap rates should be compared between REITs of

distribution yield. However, there are many reasons the same type to give an apple-to-apple comparison.

for a REIT’s yield to be higher than that of another

REIT. For one, poor economic fundamentals The Foolish takeaway

surrounding a REIT could cause its unit price to fall, The distribution yield, P/B ratio, and cap rate are

increasing its distribution yield as a result. not the only valuation methods that investors can use.

We should focus on a REIT’s DPU track record There are other ways of valuing REITs, such as the

instead of its distribution yield alone. price-to-funds-from-operations ratio, the replacement

cost method, and comparable sales method.

Price-to-book ratio However, investors should not be too hard up on

The price-to-book (P/B) ratio is computed by any particular valuation method as valuing a stock

taking a REIT’s current market price and dividing it or a REIT is more art than science. Sticking to

by the REIT’s latest reported net asset value (NAV) simple valuation methods mentioned in the article

per unit. The NAV of a REIT is calculated with the should do the trick.

simple equation of total assets minus total liabilities.

A P/B ratio below 1 shows that a REIT is trading at

a discount to its NAV.

20 The Motley Fool Special Report fool.sgChoosing the Best REITs

3 Factors to Consider When Investing in REITs

Jeremy Chia | December 27, 2017

Real estate investment trusts (REITs) have been management team is reliable and skilled?

performing well in the last five years, beating the

A good way to assess a management team is to

broader stock market index by around five percentage

simply do a quick Internet search on the members

points. However, not all REITs have performed

of the team and look out for any red flags, such

equally well. Some have lagged behind their peers,

as previous misdeeds or fraud. Good indicators

while others have outperformed considerably. As

of a strong manager are having experience in the

investors, we are always striving to find the best

industry, having a clean track record and having a

investment to grow our wealth and looking for these

proven ability to grow the REIT.

outperformers can make a huge difference.

With that in mind, I would like to point to three The Foolish bottom line

characteristics of a REIT that I look for when On average, REITs in Singapore have performed

investing. admirably. However, not all REITs have done

equally well. Some have only returned 5% a year,

Consistently high occupancy rate while others have returned more than 20% a year.

A high occupancy rate means that the REIT Obviously, that is a huge difference and finding the

can lease out most of its leasable area and can high performing gems can make a big difference to

maximise the return on its properties. A REIT that our portfolio. Hopefully, this article gives us a good

can consistently maintain a high occupancy rate over stepping stone to finding those REIT darlings that

many years shows the strength of the management can help grow our portfolio even more.

team in utilising its assets and maintaining a healthy

relationship with its tenants.

The stable occupancy rate also makes revenue

more predictable, and investors can be assured of

sustainable and stable dividends.

Price-to-book ratio below one

The price-to-book ratio compares the price of

a unit of a REIT with the book value per unit. As

investors, we should look for REITs that are trading

below its book value.

Because the book value of REITs is mostly made

up of properties, it is a good indicator of how much

unitholders would get back should the REIT decide

to liquidate its assets. A low price-to-book ratio will

reduce the risk of any losses should the REIT fold.

A strong management team

Managing a REIT takes skill and experience. As

such, not every management team can do a good job.

As investors, we need to ensure that our investments

are in safe hands. However, how do we know if the

fool.sg Special Report The Motley Fool 21Choosing the Best REITs

How to Identify REITs That Have a Portfolio That Can Appreciate

in Value

Sudhan P. | July 25, 2018

A REIT with a portfolio of properties that can Assets located in high-growth

appreciate in value over the long term can reward

unitholders in two ways. markets

Firstly, it can unlock unitholder value when it REITs that have assets that are strategically

sells the asset at a profit. Secondly, a portfolio that located in high-growth areas are also more likely to

appreciates in value increases the book value of experience asset revaluations.

the REIT, thereby giving it a larger asset base to Take CapitaLand Retail China Trust (SGX:

increase its debt load to fund further acquisitions; AU8U) for example. The REIT owns a portfolio

this could, in turn, increase the REIT’s distributions of 11 retail malls in China. I will take one of its

to unitholders. properties – CapitaMall WangJing – as a point of

So, how can investors identify REITs that have reference. CapitaMall WangJing is a shopping mall

portfolios that could potentially grow in value? Here located in the densely populated residential suburb

are two things to look at. of Wangjing in Beijing.

Because the property is located in such an

Free-hold or long land-lease optimal market, it has seen positive revaluations

tenures consistently over the past few years; its value has

grown from RMB 1.43 billion in June 2011 to RMB

The length of the land-lease tenures of a REIT’s 2.38 billion currently. The growth has happened

property portfolio is crucial in predicting its likelihood despite the fact that the property sits on a piece of

to appreciate in value. Properties that sit on land that land with a relatively short lease (expiry is in 2043).

are free-hold are more likely to increase in value over

time, whereas properties that are on land with short The Foolish bottom line

lease tenures are likely to start depreciating in value as

the land-lease maturity date approaches. Positive revaluations of a REIT’s properties

may not directly lead to cash inflows for the REIT.

A case in point is Parkway Life REIT However, it is still essential that investors do not

(SGX:C2PU), which has properties that are either on underestimate the importance of such revaluation

free-hold land, or land with long leases. Partly because gains. Not only can the REIT realise its gains in

of this strategy, the REIT has managed to report the future, but it is also important in improving the

valuation gains in its portfolio on a very consistent REITs ability to take on more borrowings, which

basis. For instance, its properties had a valuation gain can fuel future growth.

of S$26 million in 2017, S$18.2 million in 2016, S5.7

million in 2015, and S$45 million in 2014.

This consistent growth in the value of Parkway Life

REIT’s portfolio provides a larger asset base on which

it can borrow more to further expand its portfolio.

On the point about borrowing, REITs have a

regulatory gearing limit of 45%, where the gearing

ratio is calculated by dividing total debt by total assets.

From this, you can see that having a high asset base

enables more debt to be taken on by a REIT.

22 The Motley Fool Special Report fool.sgYou can also read