CONSOLIDATION OF THE EUROPEAN AUTOMOTIVE AFTERMARKET - Hugues Archambault Founding Partner - The Bridge presentation

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CONSOLIDATION

OF THE EUROPEAN

AUTOMOTIVE AFTERMARKET

Hugues Archambault

Founding Partner

Brazil Aftermarket Workshop – Automechanika Frankfurt – Sept. 12th, 2018

THE BRIDGE: INTRODUCTION

The Bridge Corporate Finance advises entrepreneurs and companies

on all their strategic and capitalistic projects

THE BRIDGE HELPS YOU THE BRIDGE WORKS WITH

§ Define your strategy

§ Acquire a business

§ Divest a business

§ Optimize your long-term

financial structure

§ Adjust your equity/

shareholder base

EUROPE: KEY FACTS • Countries: >50 • Area: 10 million km2 (Brazil: 8.5) • Population: 750 million (Brazil: 200) • GDP: $23 trillion (Brazil: 2.1) • # of cars(1): 325 million (Brazil: 35) FRANKFURT • # of CVs(1): 55 million (Brazil: 7) Sources: UN Department of Economic and Social Affairs 2017, IMF 2018, ACEA Vehicles in Use Report 2017, OICA 2015 Notes: (1) Incl. Russia, Turkey and the Ukraine. EU countries marked in yellow

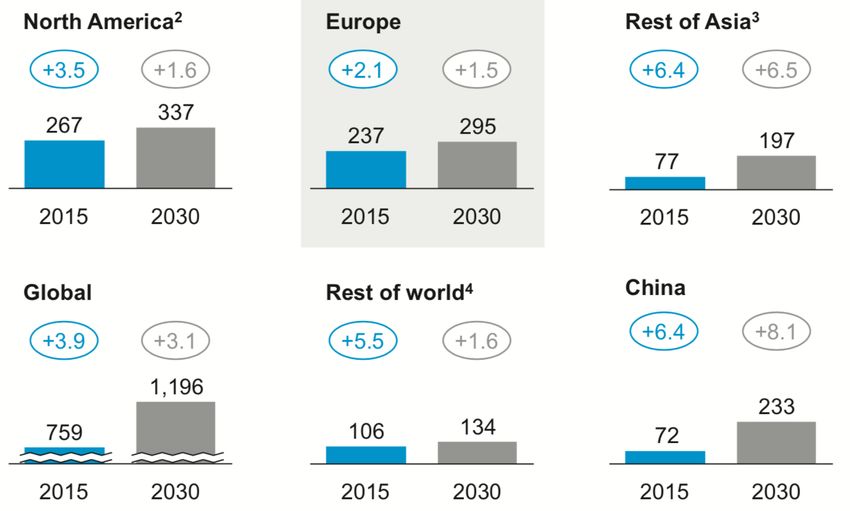

THE AUTOMOTIVE AFTERMARKET: SIZE The European aftermarket represents c. $240 billion, i.e. c. 31% of the world’s Sources: McKinsey market model; expert survey among CLEPA members (February 2017) Notes: Figures in $ billion including parts, labor, maintenance, and crash-related revenues 2 US, Canada, and Mexico 3 Incl. India 4 South America, Africa, and Oceania

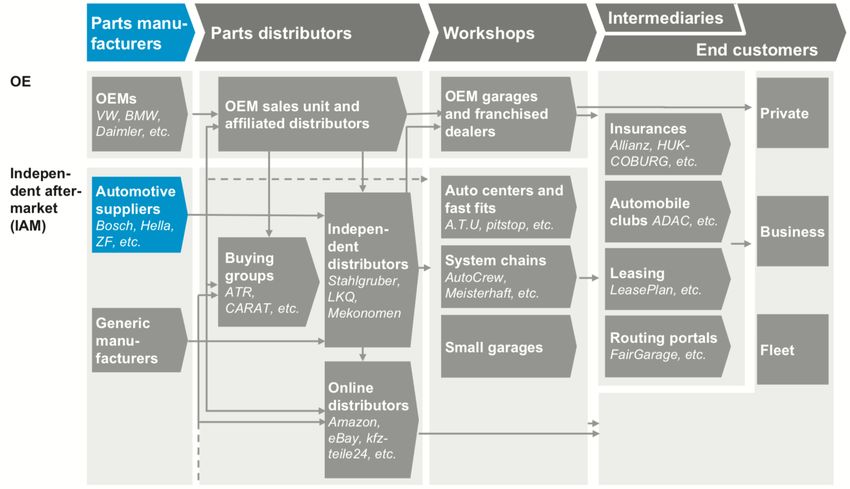

THE AUTOMOTIVE AFTERMARKET: VALUE CHAIN

The IAM accounts for 50-75% of the European aftermarket depending on the strength of

OE networks in each country

Parts manu-

facturers

Automotive

suppliers

Bosch, Indepen-

Valeo, ZF dent

Buying distributors

groups Autodis,

ATR, Nexus, LKQ,

Carat Wessels+

Müller

Source: McKinsey

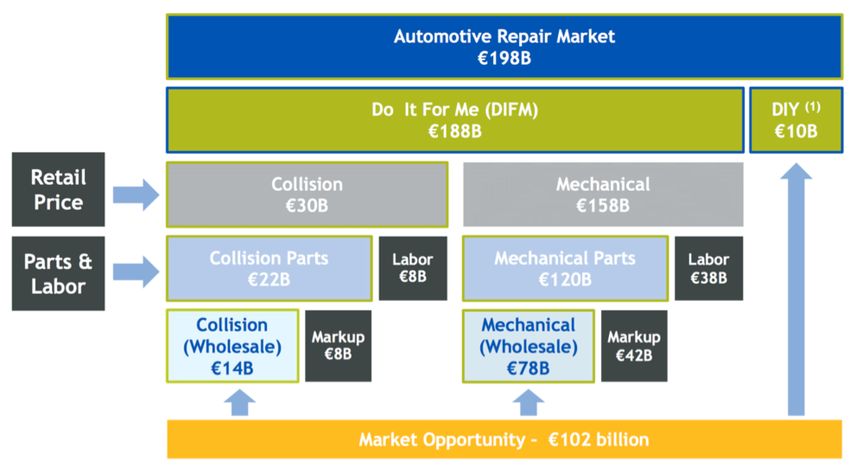

THE EUROPEAN AFTERMARKET: SEGMENTATION

The addressable market for independent distributors represents c. $120 billion

Sources: 2014 Datamonitor, LKQ

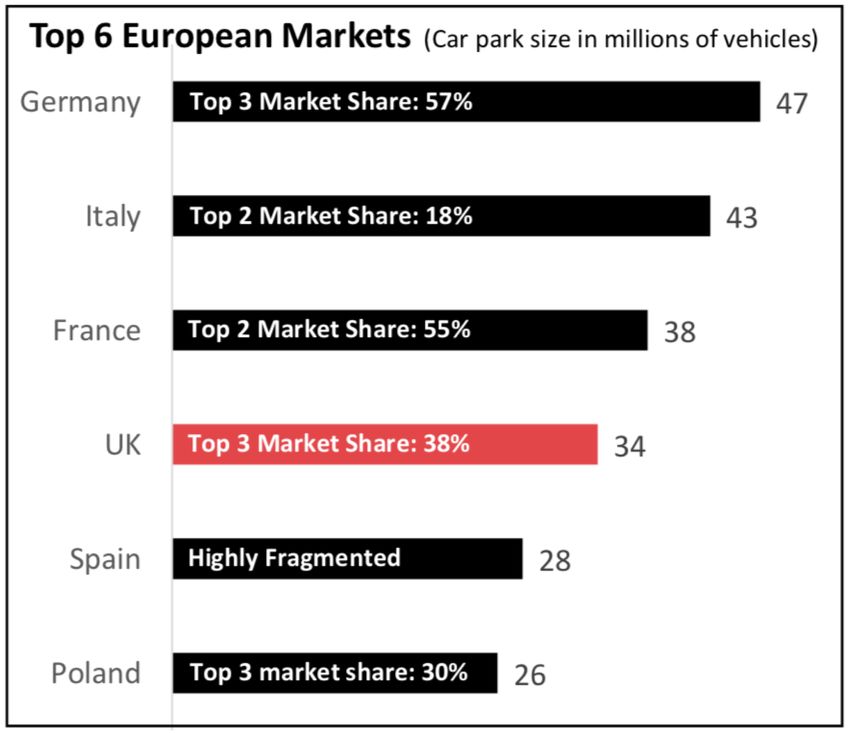

(1) Do-It-yourself e-commerce onlyTHE EUROPEAN AFTERMARKET: CONSOLIDATION LEVEL BY COUNTRY

Consolidation is well advanced in

Germany, France, Benelux and Top 3 Market Share: 58%

Scandinavia...

...but large markets such as Italy, Spain Top 3 Market Share: 19%

and Poland are still very fragmented

Top 2 Market Share: 55%

Top 3 Market Share: 39%

Highly fragmented

Top 3 Market Share: 30%

Sources: Uni-Select, The Bridge Corporate FinanceTHE EUROPEAN AFTERMARKET: THE LEADING DISTRIBUTION GROUPS

A handful of distributors generate revenues in excess of €1 billion

The largest, LKQ only holds c. 6% of the European market !

Leaders usually derive 50% or more of their revenues from acquisitions !

Turnover 1,1

(€’billion)

4,7

1,7 1,7 1,6 1,4

1,1

0,8

0,5

0,3

Turnover LKQ Europe GPC/AAG Inter-Cars W+M Autodis Mekonomen SAG Europart Uni-Select/TPA

acquired (%) 100% 100% 0% 50% 40% 75% 50% 25% 100%

Sources: Company reports and presentations, The Bridge Corporate Finance estimates

8CONSOLIDATION IN EUROPE: WHY?

Consolidation boosts the bottom line even more than top line!

n Market share gain

Expansion n Geographical expansion

n Vertical and horizontal integration

n Premium products

Lower procurement costs

n Private label products

n Back-office

Reduced overhead costs n IT

n Catalogue

n Higher visibility

Brand economies of scale

n Mutualized brand costs

n Asian sourcing

Logistics & warehousing n Slow movers

n Distribution to clientsVALUATION IN M&A TRANSACTIONS

Financial investors have created a lot of value from consolidation !

Trade buyers Financial investors

12,3x 12,1x

11,7x

Average

9,7x 10,0x 9,7x

EV/EBITDA: 9,0x

10x

7,6x

6,2x

Oct. 2011 Oct. 2013 Aug. 2014 Oct. 2015 Dec. 2015 Aug. 2017 Nov. 2017 May 2018 Sep. 2018

Target

Target country

Buyer

Buyer country

Enterprise

256 560 440 615 1,040 235 1,695 1,500 395

Value (€’m)

Sources: Company information, Mergermarket, press articles, The Bridge Corporate Finance intelligenceWHAT CAN WE EXPECT ?

M&A activity will continue to be intense with more focus on post-deal activities

Further consolidation of n LV ++

traditional distribution n CV +

n E-commerce ?

Vertical integration n Repair services ?

n Technologies +

Horizontal integration n Car makers -

n Inbound +

Transatlantic deals

n Outbound -

n Deliver synergies ++

Focus on integration

n Create real groups ++THANK YOU FOR LISTENING !

You can also read