Corporate Presentation - August 2021 TSXV: ALV OTCQX: ALVOF - Alvopetro

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Corporate Presentation August 2021 TSXV: ALV OTCQX: ALVOF

Cautionary Statements

• Forward Looking Statements. This presentation contains forward-looking statements including forecasted future earnings and sales volumes, the anticipated

timing of projects, future exploration and development plans (including the timing and associated spending of such), the Company’s dividend policy and plans

for dividends and other returns to stakeholders in the future, and results from future operations. These statements are based on current assumptions and

judgments that involve numerous risks and uncertainties, which may cause actual results to differ from those anticipated. These risks include, but are not limited

to: the timing of regulatory licenses and approvals, the impact of the COVID-19 pandemic, the ability to access capital markets, the risks inherent in the oil and

gas industry, operational risks relating to exploration, development and production; potential delays or changes in plans with respect to exploration or

development projects or capital expenditures; the uncertainty of reserve estimates; the uncertainty of estimates and projections relating to production, costs

and expenses, and health, safety and environmental risks; and fluctuations in foreign currency exchange rates and commodity prices. As a consequence, actual

results may differ materially from those anticipated in the forward-looking statements. Certain of these risks are set out in more detail in our 2020 MD&A and in

our 2020 Annual Information Form all of which are available on SEDAR and can be accessed at www.sedar.com.

• Test results. There is no representation by Alvopetro that the data relating to any well test results contained in this presentation is necessarily indicative of long-

term performance or ultimate recovery. The reader is cautioned not to unduly rely on such data as such data may not be indicative of future performance of the

well or of expected production or operational results for Alvopetro in the future.

• Non-GAAP Measures. This presentation contains financial terms that are not considered measures under International Financial Reporting Standards (“IFRS”),

such as funds flow from operations, funds flow per share, operating netback, funds flow netback, net debt and net working capital (deficit) surplus. For further

information and reconciliation to these GAAP measures, see “Non-GAAP Measures” in our most recent MD&A. This presentation also refers to Net Asset Value,

Net Asset Value per Share, and Earnings Before Interest, Tax, Depreciation, and Amortization (“EBITDA”). These measures are commonly utilized in the oil and

gas industry and are considered informative for management and shareholders. Net Asset Value represents the value of the underlying assets held by the

Company less net debt and Net Asset Value per Share is used to indicate the per unit market value. See Endnote 2 at the end of this presentation for further

details as to how Net Asset Value and Net Asset Value per Share is computed. EBITDA is used to measure the Company’s operating performance and the cash

available for reinvestment and distribution to stakeholders. Its most comparable GAAP measure is the Company’s net loss and is reconciled to such by adding

back depletion and depreciation, impairment, interest and taxes, as presented on the Company’s Statement of Operations and Comprehensive Loss. The non-

GAAP measures within this presentation may not be comparable to those reported by other companies nor should they be viewed as an alternative to measures

of financial performance calculated in accordance with IFRS.

2

Cautionary Statements

• Net Present Value. The net present value of future net revenue attributable to Alvopetro’s reserves is stated without provision for interest costs and general and

administrative costs, but after providing for estimated royalties, production costs, development costs, other income, future capital expenditures, well

abandonment and reclamation costs for only those wells assigned reserves and material dedicated gathering systems and facilities for only those wells assigned

reserves by GLJ Ltd. (“GLJ”) respectively. The GLJ evaluation was dated March 8, 2021 with an effective date of December 31, 2020 (the “GLJ Report”). Full

disclosure with respect to the Alvopetro’s reserves as at December 31, 2020 is included in the annual information form which is filed on SEDAR

(www.sedar.com). It should not be assumed that the undiscounted or discounted net present value of future net revenue attributable to the Alvopetro’s

reserves estimated GLJ represent the fair market value of those reserves. Actual reserves may be greater than or less than the estimates provided herein.

Possible reserves are those additional reserves that are less certain to be recovered than probable reserves. There is a 10% probability that the quantities

actually recovered will equal or exceed the sum of proved plus probable plus possible reserves.

• Prospective Resources. This presentation discloses estimates of Alvopetro’s prospective resources as evaluated by GLJ with an effective date of July 31, 2020 (as

announced by Alvopetro on September 8, 2020) and as evaluated by GLJ with an effective date of December 31, 2020 (as announced by Alvopetro on March 23,

2021). Estimates of prospective resources involve additional risks over estimates of reserves. The accuracy of any resources estimate is a function of the quality

and quantity of available data and of engineering interpretation and judgment. While resources presented herein are considered reasonable, the estimates

should be accepted with the understanding that reservoir performance subsequent to the date of the estimate may justify revision, either upward or downward.

Prospective resources have both a chance of discovery and a chance of development, which combined represent for any undiscovered accumulation its chance

of commerciality. Please refer to the noted news releases dated September 8, 2020 and March 23, 2021 for additional information as well as supplementary

information contained in the Company’s annual information form which has been filed on SEDAR.

• Contingent Resources. This news release discloses estimates of Alvopetro’s contingent resources and the net present value associated with net revenues

associated with the production of such contingent resources as evaluated by GLJ with an effective date of December 31, 2020 (as announced by the Company on

March 23, 2021). There is no certainty that it will be commercially viable to produce any portion of such contingent resources and the estimated future net

revenues do not necessarily represent the fair market value of such contingent resources. Estimates of contingent resources involve additional risks over

estimates of reserves. For additional details with respect to Alvopetro’s contingent resources, please refer to our news release dated March 23, 2021 and

supplementary information contained in Alvopetro’s annual information form for the year-ended December 31, 2020 which has been filed on SEDAR

(www.sedar.com).

• Currency. All amounts within this presentation are in U.S. dollars, unless otherwise noted.

3

Alvopetro - A Leading Brazilian Independent Gas Company

Brazil-focused integrated natural gas producer

• 9.6 mmboe 2P (88% natural gas) with focus on Caburé field & initial Gomo gas potential

• Two high impact exploration wells, best est. unrisked prospective resource of 4.6 & 5.9 mmboe(9)

• Gomo best est. risked contingent resource 3.5 mmboe & risked prospective resource 12.1 mmboe

Strategic midstream infrastructure to support growth (100% working interest)

• Gas plant and pipeline designed with 18 mmscf/d of capacity that can handle organic growth

and midstream revenue generation potential

• Only independently owned gas plant in the Basin

Stable & secure revenues with long term gas sales agreement

• Gas sales to AA-rated offtaker with price floor/ceiling of $5.52 to $9.38/mmbtu

• Q2 2021 realized price $6.06/mcf

• EBITDA margin of 71% supports organic growth and future dividends

Demonstrated ESG commitment

• Our commitment to social and environmental responsibility takes us beyond regulations

• Delivering affordable clean energy to the local community

• 53% reduction in greenhouse gas emissions when compared to fuel oil

Proven management team with successful LatAm track record

• Experience building and managing growth portfolios from 0 to 40+ kboe/d at Petrominerales

(Colombia) and Pacalta Resources (Ecuador)

• Managed successful exits of both businesses, generating ~$2.8 billion in proceeds

4

Brazil a Growing Market with Attractive Fundamentals

Largest oil producer in S. America and 9th

globally

New natural gas market. 48% of supply is

currently imported

World’s 9th largest economy

Brazil

Attractive fiscal regime with 5.5-11%

royalties & 15%-34% income tax

ANP mission to promote a stable regulatory

framework and attract new investments

Significant growth opportunities through

Petrobras divestments

Brazil is ripe for growth -- carrying out the most pro-business reforms in the past year (World Bank)

Resources:

World Bank; ANP.gov - Development Perspective presentation (May 2018), Pre-Salt Exploration presentation (May 2018), Brazilian O&G Market Revival presentation (May 2018),

ANP presentation, Pathway for Energy Transition post COVID-19 (June 2020)

5

State of Bahia – Reconcavo Basin

• Oldest producing basin in Brazil

• Reconcavo Basin: 23.9 mbopd + 2.2 e6m3/d (77 mmcf/d)

• Brazil's 4th largest city Salvador (pop 2.9 million)

• Important natural harbor All Saints Bay

• Major industrial complex Camacari

• Alvopetro SA operating in Brazil since

2006, acquired blocks in Rounds 7, 9, 11,

12, & 13

• Alvopetro produces 18% of Basin's

natural gas production

• Brazil’s 14th largest producer

• First independently owned UPGN (gas

processing facility)

• First independent gas sales agreement

with the local distribution company

6

Corporate Overview – Operating and Financial Results

Capital structure

Common shares outstanding (000’s) (1) 99,828

August 11, 2021 share price(1) C$1.02/$0.834

52 week high/low – C$/share C$1.11/C$0.54

Market cap (000’s) (1) C$101,825/$83,257

Insider ownership % (1) 9.4%

Financial & Reserves

Cash ($000’s) (3) $4,249

Q2 2021 Operating Netback

Net debt($000’s) (3),(7) $3,046

Average realized prices(3)

Natural gas ($/mcf) 6.06 Q2 2021 funds flow from operations ($000’s) (3) $5,471

NGL – condensate ($/bbl) 74.47 - Per basic/diluted share $0.05

Oil ($/bbl) 59.63

Net debt/LTM EBITDA(7) 0.17x

Total ($/boe) 38.08

Operating netback ($/boe) (3) 2P reserves (mboe) (4) 9,593

Realized sales price 38.08 2P reserve life index (years) 13.7

Royalties (2.82)

Net asset value ($000’s) (2) $192,169

Production expenses (3.68)

Operating netback 31.58 Net asset value per share (2) C$2.41/$1.92

Funds flow netback(3) 25.46

All reference to “$” refer to U.S. dollars. C$ refers to Canadian dollars

7

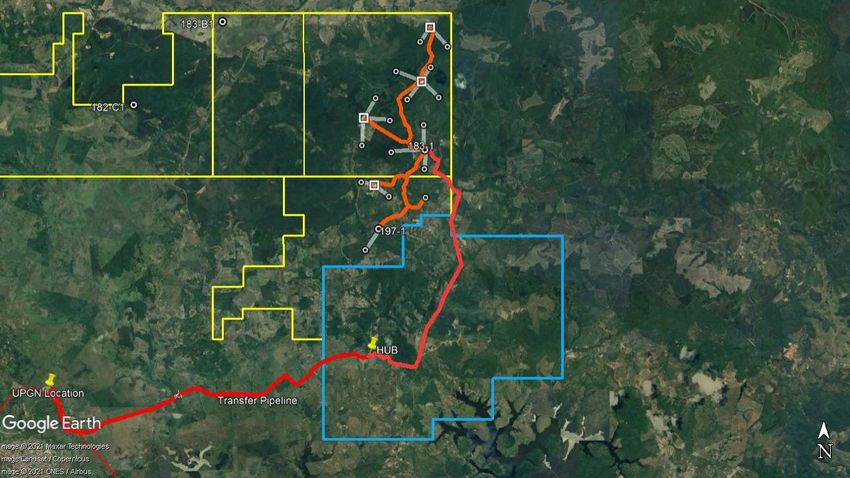

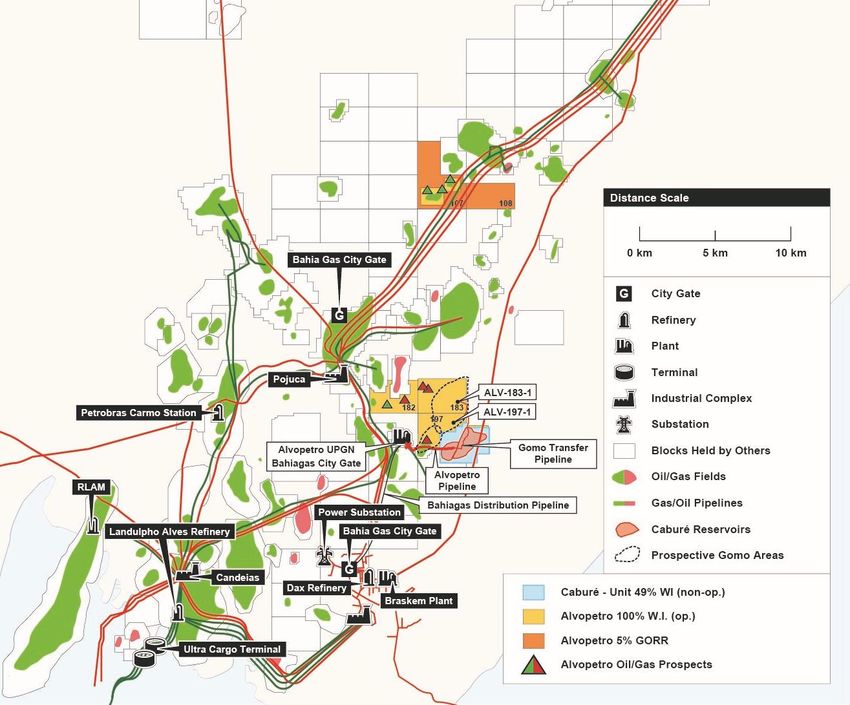

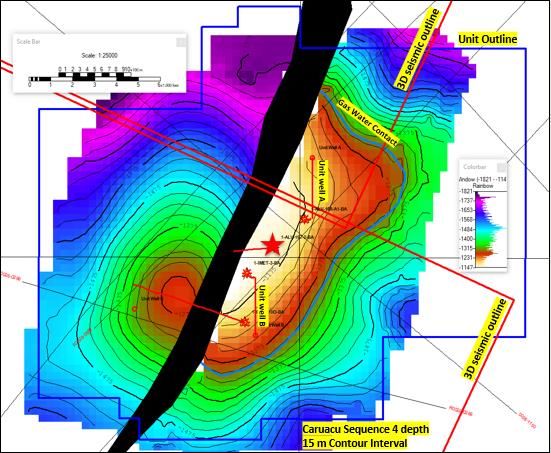

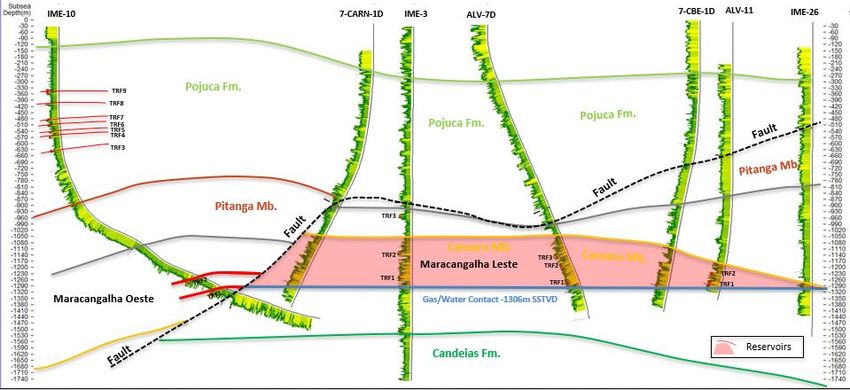

Caburé – Asset Overview (49.1% ALV)

• Upstream – core asset is a joint development of a conventional

natural gas discovery - ALV 49.1% (light blue )

– Unitized development area 7 existing wells & all production

facilities completed

• Designed gross production plateau 15.9 mmcf/d (450 e3m3)

Mmscf/d Bcf

12.0

Caburé ALV Gas Production profile (Case: 2P)*

37.5

9.0 30.0

22.5

6.0

15.0

3.0

7.5

- -

1 2 3 4 5 6 7 8 9 10 11

Average daily production Cumulative production

(mmcf/d) (Bcf)

*Caburé only, ALV company working interest, based on

Virtual Field Tour:

GLJ 12/31/20 reserve report forecast 8

https://www.youtube.com/watch?v=p1AvDNX0YXk&t=16s

Midstream - Infrastructure & Marketing (100% ALV) • ALV owned 11-km transfer pipeline from the Unit (red ) • ALV Gas Plant (UPGN) constructed by Enerflex with 18 mmcfpd capacity • Bahiagás 15-km pipeline (black ) & 70 mmcfpd citygate at our plant site completed in July 2020 • The first non-Petrobras gas plant in state of Bahia capable of delivering ANP sales specified natural gas • Gas deliveries commenced on July 5, 2020 • Precedent setting long-term GSA signed with Bahiagas gas distribution company (majority owned by Mitsui – Fitch AA rating) • Gas price floor of US$5.52/mmbtu and cap of US$9.38/mmbtu (indexed to US CPI) as of August 1, 2021 • August 1, 2021 – January 31, 2022 natural gas price of BRL$1.31/m3 (+24%), US$7.72/mcf(5) • Highly strategic legacy asset that positions ALV to unlock remaining natural gas potential *Forecasted natural gas prices will be impacted by fluctuations in BRL/USD currency exchange. Gas volumes are heat-content adjusted so that Alvopetro receives payments on an energy basis. 9

Caburé – Unit Development HUB

N

10Gas Treatment Facility and City Gate

N

11ESG – First Year of Caburé Operations

12Disciplined Reinvestment & Stakeholder Return Model –

Caburé & Gomo 2P Reserves

Stakeholders

Reinvestment

• Significant cash generating capacity just from development of Caburé & Gomo 2P reserves

• Floor pricing protects free cash flow. 2021 Forecasted EBITDA, from Caburé alone, is >$20 million (8)

• Funds returns to stakeholders (50%) and high impact upstream reinvestment (50%)

• Assumes consistent debt at current level and cumulative stakeholder returns (debt repayments and/or dividends) of C$1.30/share

• Does not reflect any upside from >$111 million (C$1.39/share) of unallocated capital available for upstream reinvestment

Assumptions: Caburé & Gomo 2P reserves, Q2/2021 GLJ Pricing Scenario with July 30, 2021 flat 5.12BRL/USD exchange rate, less forecast G&A(8); Stakeholder

returns starting in 2022 (debt repayment/dividends) = (EBITDA-Income Tax) * 50% less interest, UPGN integrated service fee, and debt interest. 13Growth Plan (100% working interest)

Objective is to fully utilize our strategic

midstream assets (18 mmcfpd)

• Highly under-explored prospective land base (23,527 acres,

100% working interest)

• Eight exploration prospects identified, supported by high

quality reprocessed seismic

• 2021 exploration program with unrisked prospective

resource evaluated by GLJ (best estimate)(9):

• ALV-182-C1 4.6 mmboe

• ALV-183-B1 5.9 mmboe

• Gomo/Murucututu tight gas play

– Declared commerciality, 2 existing wells

– 183(1) tie-in by end of 2021

– Broader development plan starting in 2022

• Petrobras divesting all onshore production

• Midstream processing opportunities

142021 Natural Gas Exploration Drilling Program (100% ALV)

Fazenda Belem

Tie Miranga

Agua Grande

Biriba

Sussuarana

Rio Pojuca

ALV-183-B1

A

ALV-182-C1

A’

• ALV-182-C1 & ALV-183-B1 Pre-Rift natural gas

prospects (100% WI)

Caburé • Unrisked prospective resource evaluated by

Remanso

GLJ (best estimate)(9)

Mata Sao Joao

• ALV-182-C1 4.6 mmboe (47% COS)

Riacho Sao Pedro • ALV-183-B1 5.9 mmboe (44% COS)

• Prospects defined on reprocessed 3D seismic

data

• Key analog fields

Jaquipe • Biriba OGIP 55 BCF (9.2 mmboe)

• Sussuarana OGIP 26 BCF (4.3 mmboe)

15Gomo Deep Basin Natural Gas Resource (100% ALV)

A A’

Jan2 197- 183-

1 1

3275m

3550m

• 5,460-acre tight gas resource Tested Gas

• Confirmed natural gas resource in 197-1 and 183-1 wells

• Environmental permit for 8-km tie-in approved. Initiated installation.

• 2P reserves 3.3mmboe (19.7 Bcfe) (4) including two development locations at 183-1

• Best Estimate Risked Contingent Resource 3.5mmboe (20.7Bcfe)(10)

• Best Estimate Risked Prospective Resource 12.1mmboe (72.4Bcfe)(10)

• Planning “fit for purpose” development wells

16Indicative Gomo/Murucututu Development Plan

17Gomo Development Plan – Reserves and Resource

Development Plans

• Reserves: Pipeline to current well locations. 2 development wells

• Contingent Resource: 4 additional development wells from the current well locations

• Prospective Resource: 10 additional wellbores from 3 future multi-well development

locations. Additional pipeline capacity for increased production.

18Reserves & Resources

Reserves (mboe) 1P 2P 3P Reserves NPV10BT ($000’s) 1P 2P 3P

Caburé 4,098 6,018 7,668 Caburé 107,524 146,901 177,496

Gomo 843 3,276 5,951 Gomo 8,047 44,389 88,751

Other 167 300 589 Other 893 3,925 8,569

Total Company Reserves(4) 5,108 9,593 14,209 Total Company Reserves(4) 116,463 195,215 274,816

Resource (mboe) Low Best High Resource NPV10BT ($000’s) Low Best High

Risked Contingent – Gomo(10) 2,874 3,451 5,665 Risked Contingent - Gomo(10) 31,329 37,711 70,937

Risked Prospective - Gomo(10) 6,555 12,072 17,827 Risked Prospective - Gomo(10) 65,565 144,784 220,437

Unrisked Prospective – 183-B1(9) 2,065 5,901 13,429

Unrisked Prospective – 182-C1(9) 1,168 4,618 16,757

Risked Prospective – 183-B1(9) 901 2,574 5,859

Risked Prospective – 182-C1(9) 545 2,157 7,825

19Track Record of Delivery

April-May 2018 October 2018 Through June 2019 September 2019 Mid 2019 - May 2020 July 5, 2020>

Caburé Unitization Equity Support for Award Development Project Financing Portfolio First

& Signed GSA Project Development Contracts Secured Growth Caburé Gas

$1.10

• The unitization • Completed a private • UPGN facility & operating • Entered into a $15mm • Unit facilities construction • Q3 2020: 1,764 boepd

agreement at Cabure

+483%

placement for aggregate agreement Credit Agreement with & development drilling • Q4 2020: 1,950 boepd

$1.00 encompasses 4 existing • 11km transfer pipeline

gross proceeds of Cordiant Capital increased 2P reserves by • Q1 2021: 2,175 boepd

wells the first of which C$5.2mm ($4.0mm) contract award • The Facility is secured by 30% to 7.9 mmboe • Q2 2021: 2,361 boepd

$0.90 was drilled in 2014 • The Placement was priced • Environmental licenses all of Alvopetro's assets, • Completed final • July 2021: 2,412 boepd

• After considerable time at C$0.45/sh ($0.35/sh), and ANP authorizations matures in 3 years and construction of Caburé • Repaid 50% of project

$0.80 and effort, that equal to the 5-day VWAP received bears a 9.5% interest rate, development debt financing

agreement was finalized • The transaction brought payable monthly • Stimulated and tested • Year 1 funds flow from

between all commercial in strategic US investors • The net proceeds funded: 183(1) Gomo well operations $18.1 million

$0.70 and regulatory • Underpinned listing on exploration drilling; • Supports shareholder

participants, paving the OTCQX" Cabure Transfer Pipeline; returns, and organic

$0.60 way for the eventual Gas Treatment Facility; growth

monetization of the asset Caburé & Gomo • Increased 2P reserves by

$0.50 development costs 21% to 9.6 mmboe

$0.40

$0.30

$0.20

$0.10

$0.00

Consistent growth and execution has generated a 483% (1) shareholder return since 2018

20Why Invest?

• Stable production profile with little to no maintenance capital and a 13.7-year

reserve life index

• Highly strategic infrastructure in heart of the Basin near major industrial demand

• Attractive long-term gas sales agreement with $5.52/mmbtu floor price

• High margin production – Q2 2021 operating netback of $31.58/boe and funds flow

from operations of $5.5 million ($0.05 per basic and diluted share)

• Low leverage with net debt to EBITDA of just 0.17 times(7)

• Disciplined & balanced stakeholder return and reinvestment model

• Plan to commence dividend payment by Q1 2022

• Strong organic growth plan

• Near-term, high-impact exploration catalysts + Gomo development upside

• Attractive valuation – trading at 42% of 2P NAV

Virtual Field Tour: https://www.youtube.com/watch?v=p1AvDNX0YXk&t=16s

21TSXV: ALV

OTCQX: ALVOF Calgary, Canada:

Alvopetro Energy Ltd.

Suite 1920, 215 – 9th Avenue SW

Calgary, Alberta, Canada

T2P 1K3

Tel: (587) 794-4224

Email: info@alvopetro.com

Salvador, Brazil:

Alvopetro S/A Extração de Petróleo e Gás Natural

Rua Ewerton Visco, 290, Boulevard Side Empresarial,

Sala 2004, Caminho das Árvores, Salvador-BA

CEP 41.820-022

Tel: + 55 (71) 3432-0917

Email: info@alvopetro.com

www.alvopetro.com

Follow Alvopetro on our social media channels:

Twitter - https://twitter.com/AlvopetroEnergy

Instagram - https://www.instagram.com/alvopetro/

LinkedIn - https://www.linkedin.com/company/alvopetro-energy-ltd

YouTube: https://www.youtube.com/channel/UCgDn_igrQgdlj-maR6fWB0w

22Endnotes

1. As of August 11, 2021. C$ share price and C$ market cap (TSXV), $ share price and $ market cap (OTCQX). Share price return 2018-2020 YTD from December

29, 2017 to August 11, 2021(TSXV).

2. Net Asset Value of $192.2 million ($1.92/share, C$2.41/share) includes; 2P NPV10 before tax of $195.2 million of reserves as evaluated by GLJ as at 12/31/20

less net debt of $3.0 million as of June 30, 2021. Per share value based on 99,828,295 shares outstanding as of August 11, 2021. C$/share based on August 11,

2021 exchange rate of C$1.2506/$1US.

3. Cash balance and Net Debt as of June 30, 2021. Operating netback and funds flow from operations for three months ended June 30, 2021.

4. Proved (“1P”) reserves, proved plus probable (“2P”) reserves, and proved plus probable plus possible (“3P”) reserves evaluated by GLJ as of December 31,

2020.

5. The natural gas price is set semi-annually in Brazilian Real/m3. Forecasted US$ price of $7.34/mcf as of August 1, 2021 based on average heat content to date

of 7% and July 30, 2021 foreign exchange rate of 5.12.

6. Based on EIA & EPA average energy and emissions intensities.

7. Net Debt is computed as the carrying amount of the Credit Facility, decreased by net working capital surplus or increased by net working capital deficit. As of

June 30, 2021, Alvopetro’s Net debt is $3.0 million. Net Debt/LTM (Last Twelve Months) EBITDA is based on Net Debt of $3.0 million as of June 30, 2021 and

EBITDA for the period July 1, 2020 to June 30, 2021 of $18.4 million.

8. Forecasted production and EBITDA based on Caburé 2P reserves, 04/01/21 GLJ Pricing Scenario, less forecasted G/A. See GLJ’s price forecast

https://www.gljpc.com/sites/default/files/pricing/apr21.pdf. The forecasted natural gas price may be below the floor price as a result of forecast foreign

currency fluctuations.

9. Undiscovered Petroleum Initially in Place (“UPIIP”) and Prospective Resources evaluated by GLJ with an effective date of July 31, 2020. See Alvopetro press

release dated September 8, 2020 for further details. UPIIP values do not include an implied truncation for minimum economic field size. Prospective resources

have been truncated for minimum economic field size of 2.2 BCF. Prospective resources have both a chance of discovery and a chance of development, which

combined represent for any undiscovered accumulation its chance of commerciality. For the 182-C1 prospect, the chance of discovery is 0.48, with a chance of

development of 0.98, for an overall chance of commerciality of 0.47. For the 183-B1 prospect, the chance of discovery is 0.44, with a chance of development

of 1.00, for a chance of commerciality of 0.44. The chance of commerciality has been included in the estimation of the risked prospective resources.

10. Contingent and Prospective Resources on Alvopetro’s Gomo property as evaluated by GLJ with an effective date of December 31, 2020. See Alvopetro press

release dated March 23, 2021, for further details and supplementary information contained in the Company’s annual information form which has been filed on

SEDAR (www.sedar.com).

23Appendix Additional Technical Materials

ALV-183-B1 Pre-Rift Agua Grande/Sergi Gas Prospect

A A A” A

’ 182-C1 Block

183-B1 Block

Biriba Sussuarana

A’

A”

• 3100 meters TVD (100% WI)

• Gas prospect defined on

reprocessed 3D seismic

Basement Basement

• 1300-acre Pre-Rift prospect

• GLJ independent prospective resource assessment, gross lease • Seal potential for Agua Grande

unrisked prospective resource 5.9 mmboe(9) Fm and Sergi Fm similar to the

• 44% chance of discovery, 100% chance of development fault set up for the offsetting

Biriba analog gas field

• Sand/sand juxtaposition in

analogs indicates sealing faults

25ALV-182-C1 Agua Grande/Sergi Gas Prospect

NW SE

• 2900 meters TVD (100% WI)

• 780-acre pre-rift prospect, maximum

Pitanga column height 135m

• Gas prospect defined on reprocessed

3FBL 0007 BA well projected

9km (closest well to

3D seismic

• Seal potential is excellent for Sergi Fm

penetrate below Sergi)

juxtaposed against basement. Agua

Sergi

Grande Fm is juxtaposed against

Afligidos shale

Basement

• GLJ independent prospective resource

Sergi

assessment gross lease unrisked

prospective resource 4.6 mmboe(9)

• 48% chance of discovery, 98%

Basement

chance of development

26Gomo Development: Single Well Economics

2P assessment (GLJ):

• 5.2Bcf sales gas+129mbbls

of condensate = 1.0 mmboe

• Year 1 average production rate:

1.34 mmcfpd, 257 boepd

(including condensate)

• Field condensate rate is

24bbl/mmcf. Sales based on

field heat content (no

assumption for UPGN

condensate yield)

• Capex: $5.8MM

• F&D: $5.80/boe

• First year NOI: $3.5MM

• Full cycle IRR: 45%

• Simple payout: 1.8 years

27You can also read