Creating the Value Leader in Wireless - The Combination of T-Mobile USA and MetroPCS - SNL.com

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Creating the Value Leader in Wireless The Combination of T-Mobile USA and MetroPCS October 3, 2012

Safe harbor statement.

Additional

AdditionalInformation

Informationand

andWhere

WheretotoFind

FindItIt

This

Thisdocument

documentrelates

relatestotoaaproposed

proposedtransaction

transactionbetween

betweenMetroPCS

MetroPCSCommunications,

Communications,Inc.Inc.(“MetroPCS”)

(“MetroPCS”)and andDeutsche

DeutscheTelekom

TelekomAG AG(“Deutsche

(“DeutscheTelekom”)

Telekom”)ininconnection

connectionwithwithT-Mobile

T-MobileUSA,

USA,Inc.

Inc.(“T-

(“T-

Mobile”).

Mobile”).The

Theproposed

proposedtransaction

transactionwill

willbecome

becomethe thesubject

subjectofofaaproxy

proxystatement

statementtotobe

befiled

filedbybyMetroPCS

MetroPCSwith

withthe

theSecurities

Securitiesand

andExchange

ExchangeCommission

Commission(the (the“SEC”).

“SEC”). This

Thisdocument

documentisisnot

notaasubstitute

substitutefor

for

the

theproxy

proxystatement

statementor orany

anyother

otherdocument

documentthat thatMetroPCS

MetroPCSmaymayfile

filewith

withthe

theSEC

SECor orsend

sendtotoits

itsstockholders

stockholdersininconnection

connectionwith

withthe

theproposed

proposedtransaction.

transaction. MetroPCS’

MetroPCS’investors

investorsand

andsecurity

securityholders

holdersare

are

urged

urgedtotoread

readthe

theproxy

proxystatement

statement(including

(includingallallamendments

amendmentsand andsupplements

supplementsthereto)

thereto)and

andallallother

otherrelevant

relevantdocuments

documentsregarding

regardingthe

theproposed

proposedtransaction

transactionfiled

filedwith

withthe

theSEC

SECororsent

senttotoMetroPCS’

MetroPCS’

stockholders

stockholdersas asthey

theybecome

becomeavailable

availablebecause

becausetheytheywill

willcontain

containimportant

importantinformation

informationabout

aboutthetheproposed

proposedtransaction.

transaction. All

Alldocuments,

documents,when

whenfiled,

filed,will

willbe

beavailable

availablefree

freeofofcharge

chargeatatthe

theSEC’s

SEC’swebsite

website

(www.sec.gov).

(www.sec.gov). You Youmay

mayalsoalsoobtain

obtainthese

thesedocuments

documentsby bycontacting

contactingMetroPCS’

MetroPCS’Investor

InvestorRelations

Relationsdepartment

departmentatat+1+1(214)

(214)570-4641,

570-4641,ororvia

viae-mail

e-mailatatinvestor_relations@metropcs.com.

investor_relations@metropcs.com.This This

communication

communicationdoes doesnot

notconstitute

constituteaasolicitation

solicitationofofany

anyvote

voteor

orapproval.

approval.

Participants

Participantsininthe

theSolicitation

Solicitation

MetroPCS

MetroPCSand andits

itsdirectors

directorsand

andexecutive

executiveofficers

officerswill

willbe

bedeemed

deemedtotobe beparticipants

participantsininany

anysolicitation

solicitationofofproxies

proxiesininconnection

connectionwith

withthe

theproposed

proposedtransaction,

transaction,and

andDeutsche

DeutscheTelekom

Telekomandandits

itsdirectors

directorsand

and

executive

executiveofficers

officersmay

maybe bedeemed

deemedtotobebeparticipants

participantsininsuch

suchsolicitation.

solicitation. Information

Informationabout

aboutMetroPCS’

MetroPCS’directors

directorsand

andexecutive

executiveofficers

officersisisavailable

availableininMetroPCS’

MetroPCS’proxy

proxystatement

statementdated

datedApril

April16,

16,2012

2012for

for

its

its2012

2012Annual

AnnualMeeting

MeetingofofStockholders.

Stockholders. Other

Otherinformation

informationregarding

regardingthetheparticipants

participantsininthe

theproxy

proxysolicitation

solicitationand

andaadescription

descriptionofoftheir

theirdirect

directand

andindirect

indirectinterests,

interests,by

bysecurity

securityholdings

holdingsor

orotherwise,

otherwise,will

will

be

becontained

containedininthe

theproxy

proxystatement

statementand

andother

otherrelevant

relevantmaterials

materialstotobe

befiled

filedwith

withthe

theSEC

SECregarding

regardingthetheproposed

proposedtransaction

transactionwhen

whenthey

theybecome

becomeavailable.

available. Investors

Investorsshould

shouldread

readthe

theproxy

proxystatement

statement

carefully

carefullywhen

whenititbecomes

becomesavailable

availablebefore

beforemaking

makinganyanyvoting

votingor

orinvestment

investmentdecisions.

decisions.

Cautionary

CautionaryStatement

StatementRegarding

RegardingForward-Looking

Forward-LookingStatements

Statements

This

Thisdocument

documentincludes

includes“forward-looking

“forward-lookingstatements”

statements”for

forthe

thepurpose

purposeofofthe

the“safe

“safeharbor”

harbor”provisions

provisionswithin

withinthe

themeaning

meaningofofthe

thePrivate

PrivateSecurities

SecuritiesLitigation

LitigationReform

ReformActActofof1995,

1995,as

asamended.

amended.Any Any

statements

statements made in this document that are not statements of historical fact, including statements about our beliefs, opinions, projections, and expectations, are forward-looking statementsand

made in this document that are not statements of historical fact, including statements about our beliefs, opinions, projections, and expectations, are forward-looking statements andshould

shouldbe

be

evaluated as such. These forward-looking statements often include words such as “anticipate,” “expect,” “suggests,” “plan,” “believe,” “intend,” “estimates,” “targets,” “views,” “projects,”

evaluated as such. These forward-looking statements often include words such as “anticipate,” “expect,” “suggests,” “plan,” “believe,” “intend,” “estimates,” “targets,” “views,” “projects,” “should,” “should,”

“would,”

“would,”“could,”

“could,”“may,”

“may,”“become,”

“become,”“forecast,”

“forecast,”and

andother

othersimilar

similarexpressions.

expressions.

All

Allforward-looking

forward-lookingstatements

statementsinvolve

involvesignificant

significantrisks

risksand

anduncertainties

uncertaintiesthatthatcould

couldcause

causeactual

actualresults

resultstotodiffer

differmaterially

materiallyfrom

fromthose

thoseininthe

theforward-looking

forward-lookingstatements,

statements,many manyofofwhich

whichare aregenerally

generally

outside

outside the control of MetroPCS, Deutsche Telekom and T-Mobile and are difficult to predict. Examples of such risks and uncertainties include, but are not limited to, the possibility thatthe

the control of MetroPCS, Deutsche Telekom and T-Mobile and are difficult to predict. Examples of such risks and uncertainties include, but are not limited to, the possibility that theproposed

proposed

transaction

transactionisisdelayed

delayedorordoes

doesnot

notclose,

close,including

includingdueduetotothe

thefailure

failuretotoreceive

receivethetherequired

requiredMetroPCS

MetroPCSstockholder

stockholderapprovals

approvalsor orrequired

requiredregulatory

regulatoryapprovals,

approvals,the

thetaking

takingofofgovernmental

governmentalactionaction(including

(including

the

thepassage

passageofoflegislation)

legislation)totoblock

blockthe

thetransaction,

transaction,thethefailure

failureto

tosatisfy

satisfyother

otherclosing

closingconditions,

conditions,thethepossibility

possibilitythatthatthe

theexpected

expectedsynergies

synergieswill

willnot

notbe

berealized,

realized,or

orwill

willnot

notbe

berealized

realizedwithin

withinthe

theexpected

expected

time

timeperiod,

period,the

thesignificant

significantcapital

capitalcommitments

commitmentsofofMetroPCS

MetroPCSand andT-Mobile,

T-Mobile,global

globaleconomic

economicconditions,

conditions,disruptions

disruptionstotothe

thecredit

creditand

andfinancial

financialmarkets,

markets,fluctuations

fluctuationsininexchange

exchangerates,

rates,competitive

competitiveactions

actions

taken by other companies, natural disasters, difficulties in integrating the two companies, disruption from the transaction making it more difficult to maintain business

taken by other companies, natural disasters, difficulties in integrating the two companies, disruption from the transaction making it more difficult to maintain business and operational relationships, and operational relationships,

possible

possibledisruptions

disruptionsor orintrusions

intrusionsofofMetroPCS’

MetroPCS’or orT-Mobile’s

T-Mobile’snetwork,

network,billing,

billing,operational

operationalsupport

supportand

andcustomer

customercare caresystems

systemswhich

whichmay

maylimit

limitorordisrupt

disrupttheir

theirability

abilitytotoprovide

provideservice,

service,actions

actionstaken

takenor or

conditions imposed by governmental or other regulatory authorities and the exposure to litigation. Additional factors that could cause results to differ materially from

conditions imposed by governmental or other regulatory authorities and the exposure to litigation. Additional factors that could cause results to differ materially from those described in the forward- those described in the forward-

looking

lookingstatements

statementscancanbe befound

foundininthe

theMetroPCS’

MetroPCS’20112011Annual

AnnualReport

Reporton onForm

Form10-K

10-KandandQuarterly

QuarterlyReport

Reporton onForm

Form10-Q

10-Qfor

forthe

thequarter

quarterended

endedJune June30,

30,2012

2012andandother

otherfilings

filingswith

withthe

theSEC

SECavailable

availableatat

the SEC’s website (www.sec.gov).

the SEC’s website (www.sec.gov).

The

Theforward-looking

forward-lookingstatements

statementsspeak

speakonly

onlyas

astotothe

thedate

datemade,

made,arearebased

basedon oncurrent

currentassumptions

assumptionsandandexpectations,

expectations,and

andare

aresubject

subjecttotothe

thefactors

factorsabove,

above,among

amongothers,

others,and

andinvolve

involverisks,

risks,uncertainties

uncertainties

and

andassumptions,

assumptions,many

manyofofwhich

whichare

arebeyond

beyondour

ourability

abilitytotocontrol

controlororability

abilitytotopredict.

predict.Neither

NeitherMetroPCS’

MetroPCS’investors

investorsand

andsecurity

securityholders

holdersnor

norany

anyother

otherperson

personshould

shouldplace

placeundue

unduereliance

relianceon

onthese

theseforward-

forward-

looking

lookingstatements.

statements.Neither

NeitherMetroPCS,

MetroPCS,Deutsche

DeutscheTelekom

Telekomnor norany

anyother

otherparty

partyundertake

undertakeany

anyduty

dutytotoupdate

updateany

anyforward-looking

forward-lookingstatement

statementtotoreflect

reflectevents

eventsafter

afterthe

thedate

dateofofthis

thisdocument,

document,except

exceptas

as

required

requiredby

bylaw.

law.

2

Speaker lineup.

René Obermann

– Chief Executive Officer, Deutsche Telekom

Roger Linquist

– Chairman and Chief Executive Officer, MetroPCS

John Legere

– President and Chief Executive Officer, T-Mobile USA

Braxton Carter

– Chief Financial Officer & Vice Chairman, MetroPCS

3

Creating the Value

Leader in Wireless

Leading

Leading Value

Value Carrier

Carrier in

in U.S.

U.S. Wireless

Wireless Market

Market

Strengthened

Strengthened Spectrum

Spectrum Position

Position to

to Roll-out

Roll-out 4G

4G LTE

LTE

Projected

Projected $6

$6 -- $7Bn

$7Bn Cost

Cost Synergies

Synergies from

from Enhanced

Enhanced Scale

Scale and

and Scope

Scope

Attractive

Attractive Growth

Growth Profile

Profile with

with Projected

Projected 7%

7% -- 10%

10% 5-year

5-year EBITDA

EBITDA CAGR

CAGR

4

Transaction terms and structure.

26% 74% Deutsche Telekom (DT)

MetroPCS Shareholders Ownership Ownership Equity Debt

$1.5 Bn

Cash

NewCo $15 Bn

(T-Mobile & MetroPCS) Notes

Reverse acquisition of T-Mobile by DT to nominate Board members

MetroPCS consistent with its ownership percentage

MetroPCS recapitalization with 1 NewCo Corporate

Selected consent rights for DT

for 2 stock split Governance

Increase / decrease of ownership

MetroPCS shareholders receive

Key Transaction $1.5Bn cash payment limitations for DT

Elements DT receives 74% ownership of

NewCo

MetroPCS shareholder vote expected

Combined business remains a U.S.- Conditions and

listed company late-2012/early-2013

Closing

Roll-over existing $15Bn DT Customary regulatory approvals required

Timeline

intercompany loan into notes in NewCo Expected to close in 1H 2013

5Transformational combination enhances growth and profitability.

Capture growth in industry’s fast growing no-contract services

Value Leadership

Greater customer value and choice

Greater spectrum position, network coverage and capacity

Scale Benefits Deeper LTE network deployment with path to at least 20x20 MHz

Improves marketing and purchasing scale

Projected cost synergies of $6 – $7Bn NPV (1)

Significant Synergies Clear cut technology path to one common LTE network

Straightforward integration with clear migration path for MetroPCS subscribers onto T-

Mobile network

Enhanced growth profile – projected 5-year CAGRs:

Strengthened Financials – Revenue: 3 – 5%, EBITDA: 7% – 10% and Free Cash Flow (2) 15% – 20%

Increases financial flexibility and direct capital market access for NewCo

1) NPV calculated with 9% discount rate and 38% tax rate

2) Free Cash Flow defined as EBITDA less Capital Expenditure

6Strategic rationale for Deutsche Telekom.

Strengthens DT’s Enhances platform for credible challenger position in the U.S. wireless market

Strategic Position in Leading player in fast growing no-contract services

Attractive U.S. Market

Increases scale and positions NewCo for growth and value creation

Compelling Total projected cost synergies with NPV of $6 – $7Bn (1)

Value Strongly enhances asset value compared to SOTP valuations without deploying more

Opportunity capital

Increased Financial NewCo is publicly listed entity; equivalent to an accelerated IPO with synergies

Flexibility Creates path towards self-funding platform in the U.S. with direct access to capital markets

DT’s Commitment to No impact to shareholder remuneration policy

Shareholders

Unchanged No changes to guidance for 2012

1) NPV calculated with 9% discount rate and 38% tax rate

7Strategic rationale and financial benefits for MetroPCS.

Addresses need for spectrum by increasing average depth from 22 to 83 MHz in

MetroPCS’s major metro areas

Strengthens Strategic Ability to expand MetroPCS model into new geographies providing new growth platform

Position Stronger value proposition to customers powered by broader coverage and deeper

spectrum

Increased scale and access to nationwide platform

Shareholders to Shareholders receive cash payment of approximately $4.09 per share

Receive Attractive Mix Shareholders receive 26% ownership stake in NewCo and significant participation in

of Cash and Stock NewCo’s growth and value creation, including projected cost synergies

Combined entity reduces MetroPCS’s standalone business risk

Enhances Stability and Increases flexibility to pursue future opportunities

Flexibility

Allows MetroPCS customers to gain access to full range of contract and no-contract

services

8NewCo: The Wireless Value Leader

NewCo leadership in place.

Brings Together Seasoned Executive Leadership with Significant Industry Expertise

John Legere J. Braxton Carter

President and Chief Chief Financial Officer

Executive Officer

Jim Alling Thomas C. Keys

COO of T-Mobile COO of MetroPCS

Customer Unit Customer Unit

10NewCo: The premier challenger in the U.S. wireless market.

Simplicity, unlimited data, and “No Surprises” for both contract and no-contract customers

Combined spectrum resources enabling at least 20x20 MHz LTE in major metro areas

Growth platform delivering projected 7% - 10% EBITDA growth

and 15% - 20% FCF (1) growth (5-year CAGR)

Led by proven management team committed to growth and cost leadership

1) Free Cash Flow defined as EBITDA less Capital Expenditure

11Increasing our momentum.

AT&T Network Verizon Tower MetroPCS

spectrum modernization spectrum transaction Combination

swap

$4Bn LTE More Attractive

investment efficient financial structure Creating the

AWS spectrum

including site network and while maintaining leading value

received

upgrades and deeper LTE operational carrier

spectrum rollout flexibility

re-farming

12Enhanced spectrum position.

Spectrum Transactions Significantly Improved T-Mobile's Spectrum Depth

Total Spectrum in Top 100 Major Metro Areas

MHz (1)

75 11 72

6

61 4

2

52 7

50 41

35

26

25

31

26 26

0

T-Mobile (Dec 2011) AT&T Spectrum VZW Spectrum T-Mobile (Oct 2012) MetroPCS NewCo

PCS Spectrum AWS Spectrum

1) Totals do not reconcile due to rounding

13NewCo: an enhanced competitor.

Total Spectrum in Top 25 Major Metro Areas Subscribers

MHz 2Q-2012, Millions

76 48 42.5

75 63 33.2

36 9.3 6.6

6.6 14.6

50 24 5.3

25 12 21.3 21.3

13

0

0

NewCo

NewCo (1)

Branded Contract Branded No-Contract Wholesale

Total Revenue EBITDA

$Bn, 2012E (2) $Bn, 2012E (2)

9

30 5.1 1.4 6.3

24.8 4.9

19.7 6

20

3

10 0

(3)

0 NewCo

% Margin of

NewCo Service 28.2% 30.3% 28.6%

Revenue (4)

1) Includes MVNO and M2M

2) 2012E based on equity research consensus; presented as US GAAP

3) Pre stock-based compensation

14

4) Based on 2012E equity research consensus T-Mobile service revenue of $17.3Bn, MetroPCS service revenue of $4.6Bn and NewCo service revenue of $21.9BnAccelerates Challenger Strategy.

Initiatives Underway Benefits with MetroPCS

$4Bn network modernization Complementary spectrum position

Amazing 4G Services 20% coverage improvement Path to at least 20x20 MHz LTE

>200MM pops LTE in 2013 Improved urban and in-building coverage

Unlimited 4G data

Geographic expansion opportunities

Value Leader First with contract handset financing and

Expanded customer choice

Bring Your Own Device

Brand re-launch Signals “staying power”

Trusted

Trusted Brand

Brand 1,400 store refresh Improved customer experience

Ramping B2B salesforce by 1,000

Leading value carrier

Multi-Segment Player Monthly4G growth of ~75% YoY

~70,000 total points of distribution

Rich MVNO pipeline

Business re-structuring Projected 20 - 25% increase in network

Challenger Business asset utilization

Cost discipline yielding $900MM savings Projected $6 - 7Bn NPV (1) value of

Model Branded contract churn improvement of synergies

50Bps YoY Cost leadership culture

1) NPV calculated with 9% discount rate and 38% tax rate

15$4Bn network modernization well underway.

Amazing

4G

Services

$4Bn Total Investment

37,000 sites upgraded over three years with:

– Multi-mode radios

Antennas with integrated

– Tower-top electronics radios

– New antennas with integrated radios

Enables technology enhancements:

– HSPA+ introduction in PCS spectrum

band in 2012 BTS

– LTE >200MM POPs by end of year

Coax Card

2013 Fiber

– Approximately 20% projected improved

in-building coverage

16MetroPCS enables deeper LTE spectrum in top areas. Amazing

4G

Services

Spectrum depth enhances LTE in key metro areas (1) = T-Mobile AWS Spectrum

= Additional AWS spectrum

from transaction

Key Areas Post-Transaction LTE Spectrum (MHz) Average LTE Spectrum in Key Areas (MHz)

New York 50

60

Los Angeles 50

14 50

50

Dallas 60

Philadelphia 40 40 36

Detroit 50

30

Boston 50

San Francisco 50 20

Tampa 50

10

Sacramento 50

0

Las Vegas 50

NewCo

Orlando 50

1) Assumes AWS spectrum fully deployed as LTE spectrum over time

17Delivers greater network scale. Amazing

4G

Services

Cell Sites and DAS Nodes Subscribers per Cell Site*

Thousands

Enhanced

Enhanced spectrum

spectrum position

position

60 765

52

633 664

MetroPCS

MetroPCS DAS

DAS site

site consolidation

consolidation

enhances

enhances network

network density

density

18

Greater

Greater equipment

equipment purchasing

purchasing

* scale

NewCo* NewCo scale

*Note: Includes DAS Nodes and Macro Sites *Note: Includes M2M subscribers;

cell sites adjusted for DAS Nodes

Total Spectrum BRS (Clearwire)

MHz, top 25 major metro areas

109 106

97

76

63 52

54 13 9

NewCo

18T-Mobile network ready to accommodate MetroPCS Amazing

4G

subscribers. Services

Favorable Dynamics Integration Plan

T-Mobile’s

T-Mobile’s 40-60

40-60 MHzMHz HSPA+

HSPA+ // LTE

LTE will

will Transition

Transition MetroPCS’s

MetroPCS’s subscribers

subscribers to

to T-

T-

have

have capacity

capacity to

to allow

allow MetroPCS

MetroPCS Mobile

Mobile // NewCo

NewCo network

network through

through upgrade

upgrade

customers

customers to

to begin

begin migration

migration at

at time

time of

of cycles

cycles

close

close

Re-farm

Re-farm MetroPCS

MetroPCS spectrum

spectrum to

to create

create

Rapid

Rapid handset

handset turnover

turnover (60%

(60% -- 65%

65% per

per

capacity

capacity for

for increasing

increasing demand

demand forfor

year)

year) facilitates

facilitates MetroPCS

MetroPCS customer

customer

migration

migration increased

increased LTE

LTE bandwidth

bandwidth

Coverage

Coverage and

and performance

performance for

for MetroPCS

MetroPCS Decommission

Decommission redundant

redundant sites

sites and

and

customers

customers improves

improves dramatically

dramatically in

in integrate

integrate selected

selected MetroPCS

MetroPCS assets

assets in

in

transition

transition minimizing

minimizing any

any potential

potential churn

churn dense

dense metro

metro areas

areas

GSM

GSM ecosystem

ecosystem handsets

handsets equivalent

equivalent or

or MetroPCS

MetroPCS customers

customers anticipated

anticipated to

to be

be

more

more capable

capable at

at each

each price

price point

point completely

completely migrated

migrated to

to NewCo

NewCo byby 2H

2H 2015

2015

19Straightforward spectrum migration strategy. Amazing

4G

Services

GSM Dallas Region Case Study

GSM remains

remains “universal”

“universal” technology

technology

5x5 MHz Blocks

for

for roaming,

roaming, M2M

M2M and

and legacy

legacy devices

devices CDMA / EVDO GSM HSPA+ LTE

2H2013 1H2014 2H2014 1H2015 2H2015

MetroPCS

MetroPCS PCS

PCS spectrum

spectrum migrated

migrated to

to

HSPA+

HSPA+

T-Mobile

T-Mobile

T-Mobile AWS

AWS repurposed

repurposed from

from

AWS

HSPA+

HSPA+ to

to LTE

LTE over

over time

time

Available

Available MetroPCS

MetroPCS AWS

AWS spectrum

spectrum MetroPCS

migrates

migrates to

to LTE

LTE

AWS

AWS becoming

becoming primary

primary LTE

LTE band

band PCS

T-Mobile

across

across Americas

Americas

20Creates the value leader in wireless. Value

Leader

Best Value in the U.S. Market

Contract Services No-contract Services

Brands

Partner Brands (MVNO)

Consumer

Customer

B2B Consumer

Segments M2M

Primary Channel National / Direct National / Indirect Local / Indirect

~70,000

~70,000 total

total points

points ofof distribution

distribution

Distribution

~7,500

~7,500 branded

branded doors

doors // ~10,000

~10,000 33rdrd-party

-party doors

doors // ~50,000

~50,000 national

national retail

retail doors

doors

Network 4G

4G network

network with

with LTE/HSPA+

LTE/HSPA+ delivers

delivers fast

fast and

and reliable

reliable coverage

coverage

21Improves customer experience. Trusted

Brand

Benefits to NewCo Customers

Better service and faster speeds driven by: Greatly expands on-net domestic

coverage

Network Increased network density

Coverage Broader coverage area International roaming options

Additional capacity in major metro areas

Deeper LTE coverage in major metro Faster, broader, higher capacity 4G

LTE

areas such as NY, LA and Dallas HSPA+ and LTE network

Expands handset availability Wider handset choice and lower costs

Devices

Leverage MetroPCS automation and National footprint subs not forced to

Distribution self service to improve service levels leave MetroPCS when they move

and Service

22Leader in fast growing no-contract offerings. Multi-

Segment

Player

North America Industry Growth Branded No-contract Subscribers (1) Branded No-contract Revenue

% Subscribers CAGR (2012-2017) Q2-2012, Millions Q2-2012, $Bn

21.3 1.0

Total 3% - 5% 15.4 1.2

NewCo 14.6 NewCo 1.6

9.3 1.2

No-Contract 9% - 10%

7.5 Not Reported

5.9 0.8

Contract 2% - 3% 5.3 Not Reported

5.3 0.4

Source: Independent Market Research (OVUM)

1) Facilities-based carriers exclude wholesale

23MetroPCS expands footprint.

Multi-

Segment

Player

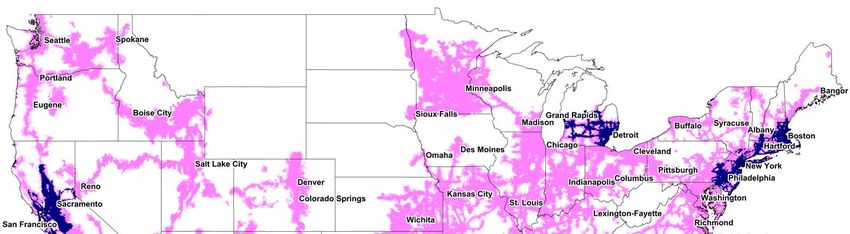

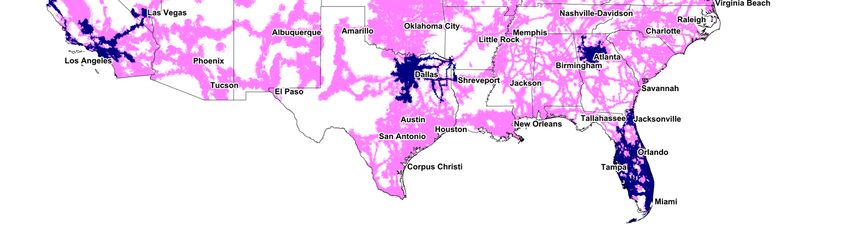

NewCo’s Spectrum and Network Broadens MetroPCS’s Potential Reach

MetroPCS Network

T-Mobile Network

Addressable

Addressable POPs

POPs coverage

coverage increases

increases from

from 105MM

105MM to

to more

more than

than 280MM

280MM

24Transaction accelerates momentum in contract offerings.

Multi-

Segment

Player

Powerful signal to customers that NewCo is here to compete in contract offerings

Network improvements contribute to improving churn metrics

Improves 4G LTE depth in major metro areas

Additional spectrum supports Unlimited as key differentiator

Signals staying power to B2B customers

Providing Contract Customers a More Compelling Product Offering

25Poised for growth.

Challenger

Business

Model

Expected 5-year Growth

% CAGR Capture

Capture Scale

Scale Benefits

Benefits

Achievable

Achievable projected

projected cost

cost synergy

synergy realization

realization

Revenue 3% - 5% with

with run-rate

run-rate of

of $1.2

$1.2 –– $1.5Bn

$1.5Bn

EBITDA 7% - 10% – Projected

Projected EBITDA

EBITDA run-rate

run-rate of

of $0.8

$0.8 ––

$1.0Bn

$1.0Bn

Free Cash

15% - 20%

Flow (1) – Reduction

Reduction in

in capex

capex with

with projected

projected run-

run-

rate

rate savings

savings of

of $0.4

$0.4 –– $0.5Bn

$0.5Bn

Target Profitability

% of service revenue

Upside

Upside from

from geographic

geographic expansion

expansion of

of

EBITDA

34% - 36% MetroPCS

MetroPCS brand

brand

Margin

1) Free Cash Flow defined as EBITDA less Capital Expenditure

26Synergies turbocharge the Challenger business model. Challenger

Business

Model

T-Mobile’s network capacity accelerates MetroPCS customer transition

Rapid Transition to Highly complementary spectrum allows for greater LTE bandwidth

a Single Network

Projected $5 - $6Bn NPV (1)

Rapid handset turnover facilitates network migration

Decommission redundant sites and retain selected MetroPCS network assets

Capture Economies Realize efficiencies in common support functions

of Scale

Estimated ~$1Bn NPV (1)

Maximize scale benefits with handset and other partners

Expanding MetroPCS’s brand into new major metro areas

Drive MetroPCS

Increase distribution density and customer convenience

Geographic Expansion

Provide strong dealer community

1) NPV calculated with 9% discount rate and 38% tax rate

27Cost synergies yield projected $6 - $7 billion NPV (1). Challenger

Business

Model

Year 1 Year 2 Year 3 Year 4 Year 5 Description

Network ($MM)

Reduction in operating expenses

Operating

Opex Savings -

($0-$50) $100-$200

($0-$50) $200-$300

$0-$100 $500-$600

$300-$400 $600-$700 related to tower, backhaul and

roaming

Savings in capacity and expansion

Capex Savings $100-$200 $300-$400 $400-$500 $450-$550 $400-$450

capex

Site upgrades and

One - Time Costs ($600-$700) ($0 - $50) ($700-$800) ($800-$900) -

decommissioning

Non - Network ($MM)

HSPA+ cost advantage over CDMA

Opex Savings $0-$50

- $100-$200 $150-$250 $150-$250 $200-$300 Procurement and back office

efficiencies

Capex Savings $100-$200

- $0-$50 $0-$50 $0-$50 $0-$50 Common platform efficiencies

Customer transition and business

One – Time Costs ($150-$250) ($0-$100) ($0-$100) - -

integration

1) NPV calculated with 9% discount rate and 38% tax rate

28NewCo’s strong financial profile. Challenger

Business

Model

Total Revenue EBITDA

$Bn, 2012E (1) $Bn, 2012E (1)

9

30 5.1 24.8 1.4 6.3

19.7 6 4.9

20

3

10

0

0 (2)

NewCo

NewCo % Margin of

Service 28.2% 30.3% 28.6%

Revenue (3)

Capital Expenditure Free Cash Flow (4)

$Bn, 2012E (1) $Bn, 2012E (1)

6 4

0.9 4.2 3

4 3.2 0.5 2.1

2 1.6

2

1

0 0

NewCo NewCo

% Capital % Margin of

Intensity 18.8% 20.2% 19.1% Service 9.4% 10.1% 9.6%

of Service Revenue (3)

Revenue (3)

1) 2012E based on equity research consensus; presented as US GAAP

2) Pre stock-based compensation

3) Based on 2012E equity research consensus T-Mobile service revenue of $17.3Bn, MetroPCS service revenue of $4.6Bn and NewCo service revenue of $21.9Bn

29

4) Free Cash Flow defined as EBITDA less Capital ExpenditureNewCo’s attractive and flexible capital structure. Challenger

Business

Model

NewCo Debt

NewCo

NewCo Financial

Financial Strategy

Strategy $Bn, 2012E (1)

NewCo

NewCo will

will have

have significant

significant financial

financial resources,

resources, $20.4

$18.6

stability

stability and

and access

access to

to capital

capital

– Strong

Strong credit

credit profile

profile will

will reduce

reduce cost

cost of

of

capital

capital

Total Debt Net Debt

– Target

Target credit

credit rating

rating of

of Ba2/BB

Ba2/BB to

to Ba3/BB-

Ba3/BB-

NewCo Post-Synergy EBITDA Leverage Ratio

Deutsche

Deutsche Telekom

Telekom will

will be

be the

the largest

largest holder

holder of

of x 2012E EBITDA (2)

NewCo

NewCo equity

equity and

and debt

debt 2.9x

2.6x

– DT

DT maintains

maintains an

an investment

investment grade

grade credit

credit

rating

rating (Baa1

(Baa1 // BBB+)

BBB+)

– DT

DT to

to roll-over

roll-over existing

existing $15Bn

$15Bn inter-company

inter-company

Total Leverage Net Leverage

loan

loan into

into NewCo

NewCo senior

senior unsecured

unsecured notes

notes

1) Projected total debt of $20.4Bn and net debt of $18.6Bn assuming $1.8Bn of cash at close; excludes $2.4Bn tower financing obligation and $0.4Bn MetroPCS capital leases

2) Based on equity research consensus EBITDA of $7.1Bn (pro forma 2012E EBITDA of $6.3Bn and $0.9Bn of run-rate cost synergies)

30NewCo’s detailed capital structure.

Challenger

Business

Model

Capital Structure

1 Deutsche

Deutsche Telekom

Telekom Financing

Financing $Bn (1)

$15Bn

$15Bn of

of rollover

rollover notes

notes

DT Financing $15.0

–– Average

Average tenor

tenor of

of 8.5

8.5 years

years 1

DT Revolving Credit Facility (Undrawn) 0.0

–– Projected

Projected weighted

weighted average

average yield

yield of

of 8%

8%

Existing MetroPCS Bank Loan 2.5

$0.5Bn

$0.5Bn Revolving

Revolving Credit

Credit Facility

Facility 2

Existing MetroPCS Unsecured Notes 2.0

$5.5Bn

$5.5Bn backstop

backstop (existing

(existing MetroPCS

MetroPCS debt

debt and

and new

new

third

third party

party debt)

debt)

New Third Party Financing 1.0 3

2 Existing Total NewCo Debt $20.4

Existing MetroPCS

MetroPCS Debt

Debt

$2.5Bn

$2.5Bn bank

bank debt

debt (subject

(subject to

to waiver

waiver or

or refinance)

refinance) T-Mobile Tower Leasing Obligation 2.4

–– Variable

Variable rate

rate with

with weighted

weighted average

average ofof 4.6%

4.6% as

as MetroPCS Capital Leasing Obligations 0.4

of

of 6/30/12

6/30/12 and

and maturity

maturity range

range of

of 2013-2018

2013-2018 Total Adjusted NewCo Debt $23.2

$2Bn

$2Bn unsecured

unsecured notes

notes

–– 7.875%

7.875% notes

notes due

due 2018

2018 Less: Expected Cash at Closing (1.8)

–– 6.625%

6.625% notes

notes due

due 2020

2020 Total NewCo Net Debt $18.6

3 New

New 33rdrd Party

Party Debt

Debt Total Adjusted NewCo Net Debt $21.4

$1Bn

$1Bn new

new third

third party

party debt

debt

1) Totals do not reconcile due to rounding

31Creating the Value

Leader in Wireless

Leading

Leading Value

Value Carrier

Carrier in

in U.S.

U.S. Wireless

Wireless Market

Market

Strengthened

Strengthened Spectrum

Spectrum Position

Position to

to Roll-out

Roll-out 4G

4G LTE

LTE

Projected

Projected $6

$6 -- $7Bn

$7Bn Cost

Cost Synergies

Synergies from

from Enhanced

Enhanced Scale

Scale and

and Scope

Scope

Attractive

Attractive Growth

Growth Profile

Profile with

with Projected

Projected 7%

7% -- 10%

10% 5-year

5-year EBITDA

EBITDA CAGR

CAGR

32Back-Up

Estimated Deutsche Telekom group impact from MetroPCS

transaction.

Major Financial Key Performance Indicators (KPIs) 2013

Revenue EBITDA (adj.) ROCE FCF EPS (adj.)

Delta

€ 4.2 Bn € 1.1 Bn 0.4 p.p. € -0.3 Bn € 0.02

Other

Other Effects

Effects

One

One time

time effect

effect 2012:

2012: estimated

estimated negative

negative net

net income

income effect

effect of

of €€ 77 -- 88 Bn

Bn due

due to

to goodwill

goodwill and

and asset

asset

impairment

impairment on

on T-Mobile

T-Mobile asset

asset

FCF

FCF in

in 2013

2013 will

will include

include integration

integration expenses

expenses of

of €€ 0.6

0.6 to

to €€ 0.7

0.7 Bn.

Bn. Positive

Positive accretion

accretion including

including integration

integration

expenses

expenses expected

expected from

from 2014

2014 onwards

onwards

Rating

Rating debt:

debt: the

the transaction

transaction has

has aa non-significant

non-significant impact

impact on

on DT

DT Debt/EBITDA

Debt/EBITDA ratio

ratio

34You can also read