Crisis, Response, and Recovery: The Federal Government and the Black/White Homeownership Gap

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

A TERNER CENTER REPORT - MARCH 2021

Crisis, Response, and Recovery:

The Federal Government and the

Black/White Homeownership Gap

AUTHOR:

CAROLINA K. REID, FACULTY RESEARCH ADVISOR

Copyright 2021 Terner Center for Housing Innovation

For more information on the Terner Center, see our website at

www.ternercenter.berkeley.edu

A TERNER CENTER REPORT - MARCH 2021

Introduction Researchers have estimated that homes in

black neighborhoods are undervalued by

Today, the median non-Hispanic White an average of $48,000, amounting to $156

household holds almost $190,000 in billion in cumulative losses.3

wealth—7.8 times that of the median Black

The Biden-Harris Administration has

household ($24,100).1 While the drivers

made racial equity one of its top priorities,

of the racial wealth gap are complex,

recognizing that systemic racism

disparities in access to homeownership,

continues to shape contemporary access

as well as in the financial benefits that

to opportunity.4 This attention to racial

homeownership confers, play a key role

inequality is long overdue, and is relevant

in shaping this inequality.2 In 2018,

to multiple policy domains, including

only 42 percent of Black households

social and labor market policies, criminal

owned a home, compared to 73 percent

justice, and education. Yet housing remains

of non-Hispanic White households. This

a central axis by which racial inequality

homeownership gap is larger than it was

is produced and sustained. Historically,

in 1968, before discrimination was legally

the federal government has played an

outlawed, demonstrating the enduring

outsized role in promoting policies that

effect of structural racism in housing and

discriminate against Black households in

mortgage markets (Figure 1). Indeed, the

housing and mortgage markets, histories

racialized history of housing policy in the

that have been powerfully illuminated in

U.S., including racial covenants, redlining,

books like The Color of Law by Richard

and discriminatory credit practices,

Rothstein and Race for Profit by Keeanga-

have shaped not only who has access to

Yamahtta Taylor, as well as in the work

homeownership, but also its returns.

Figure 1: The Black/White Homeownership Gap, 1960 - 2018

35%

30%

Difference Between White and Black

25%

Homeownership Rate

20%

15%

10%

5%

0%

1960 1970 1980 1990 2000 2010 2018

Source: Goodman, L., Zhu, J., & Pendall, P. (2017). “Are Gains in Black Homeownership History?” The Urban Institute. Retrieved from: https://

www.urban.org/urban-wire/are-gains-black-homeownership-history.

2

A TERNER CENTER REPORT - MARCH 2021

of Ta-Nehisi Coates in “The Case for These failures of government

Reparations” and Nikole Hannah-Jones

in The 1619 Project.

led to a deeply uneven recovery

for Black homeowners and

The last decade has thrown into sharp

relief the failures of federal public policy communities, widening not

to repair these harms. Disparate outcomes only the racial wealth and

for Black homeowners are not a thing of homeownership gap, but also

the past. Despite the passage of laws like

the Fair Housing Act and the Equal Oppor- fueling gentrification and

tunity Credit Act, the 2007-2010 foreclo- displacement pressures in

sure crisis and the recovery that followed some Black communities.

point vividly to the ways in which housing

and mortgage markets are still deeply

segmented by race. They also point to the and wealth gap in the future. The

limitations of the government response policies proposed by the Biden-Harris

to that crisis. Rather than stepping in Administration represent an important

boldly with direct aid to homeowners, the first step in promoting an equitable

policy response was shaped by racialized recovery, including efforts to address

narratives of who was “deserving” of aid the pandemic and provide immediate

and the unwavering belief that private financial support to households and small

actors—such as mortgage servicers and businesses. The recently passed stimulus

investors—were the best placed to provide package, which includes critical support

aid to hard-hit borrowers and communi- for renters and families with children, will

ties. These failures of government led to a do a lot to mediate the worst impacts of the

deeply uneven recovery for Black home- crisis on American families. But the goal

owners and communities, widening not of closing the racial wealth gap is going to

only the racial wealth and homeowner- need a broader set of federal interventions

ship gap, but also fueling gentrification that consider and affirmatively address

and displacement pressures in some Black the longstanding impact of discriminatory

communities. government policies on Black households

The lack of an effective government and communities.

response to the foreclosure crisis—let This paper explores how federal policy

alone one centered on principles of racial has helped forge and reinforce disparities

equity—holds important lessons for in access to homeownership and wealth

federal housing policy, particularly as the building for Black households over time.

new administration develops responses to It considers three “chapters” of major

the economic crisis caused by the novel economic downturns—the Great Depres-

coronavirus (COVID-19) pandemic. How sion, the Great Recession, and now, the

the federal government chooses to protect global COVID-19 pandemic—to show how

Black homeowners now, and whether it the federal government’s decisions about

chooses to implement policies that ensure whom to assist in the crisis, and how, has

equitable recovery for Black households broad implications for who benefits from

over the coming years, will have a profound the recovery.

impact on the racial homeownership

3

A TERNER CENTER REPORT - MARCH 2021

First, The Legacy of Redlining, reviews to rising gentrification and displacement

how the establishment of a federal housing pressures in some neighborhoods.

finance system after the Great Depression

Third, The COVID-19 Pandemic,

played a significant role in promoting the

considers the current moment, and high-

expansion of homeownership after World

lights emerging evidence that Black home-

War II. However, this expansion was pred-

owners and neighborhoods may again be

icated on a set of racist beliefs that largely

disproportionately affected by the asso-

excluded Black households from federal

ciated economic downturn. Here, poli-

subsidies (for example, through Federal

cies can still make a difference. Already,

Housing Administration (FHA) mortgage

lessons learned from the foreclosure

insurance) and prohibited them from

crisis have led to promising interventions,

buying homes in suburbanizing neighbor-

such as broadly implemented mortgage

hoods. This section of the paper—which

forbearance programs. Yet the evidence

draws largely from existing scholarship—

that COVID-19 is leading to a K-shaped

is designed to anchor the subsequent

recovery suggests that there is still more to

analysis of contemporary inequalities in

do to ensure that recovery from this crisis

these past practices of racial exclusion.

is broadly shared, and that prolonged job

The disproportionate rates of subprime

losses or unsustainable debt payment

lending to Black households and neigh-

don’t lead to additional losses among

borhoods in the 2000s, for example, are

Black homeowners.

not independent from the creation of a

financial system that valued property and The final section of the paper presents

distributed credit on the basis of race. policy recommendations for the Biden-

Indeed, a growing number of studies point Harris Administration, outlining the prin-

to the enduring legacy of these maps on ciples that need to form the foundation for

contemporary racial inequality. starting to repair the harms of past gener-

ations and move the country to greater

Second, Uneven Recovery: Black Home-

racial equality in mortgage and housing

ownership after the Great Recession,

markets.

turns to the recent past to explore the

ways in which the federal response to the While the focus here is on Black house-

foreclosure crisis failed to address the holds and communities, the structural

disproportionate impact foreclosures were racism that continues to shape Black

having on Black households and neighbor- disadvantage negatively affects Hispanic/

hoods. While not explicitly “race-based” Latinx and Asian communities as well,

like the practices that shaped the recovery as evidenced by the disparate impact

out of the Great Depression, the federal of both foreclosures and the COVID-19

government’s response to the foreclosure pandemic for these groups. Tackling anti-

crisis was “race-blind,” missing the ways Black racism will benefit other structur-

in which Black households and neigh- ally marginalized populations, yet doesn’t

borhoods were particularly vulnerable preclude the need for additional research

to foreclosure. This section presents new and policies that address discrimination

analysis that demonstrates how the lack and disadvantage in other communities of

of a bold and affirmative set of policies to color.

protect Black homeowners contributed to

the widening racial wealth gap, as well as

4

A TERNER CENTER REPORT - MARCH 2021

The Legacy of Redlining homeowners—in their homes.9 The HOLC

also introduced amortizing home mort-

Much of the infrastructure and ideas that gages, which increased the affordability of

shape today’s housing finance system— home purchases and allowed homeowners

from the 30-year amortizing mortgage, to gradually build wealth in their homes

to the Federal Housing Administration, through regular, level payments that paid

to roles played by Fannie and Freddie— down their loan balance.10, 11

were established in response to the market

turmoil precipitated by the Great Depres- However, the HOLC also shaped who

sion. Before then, homeowners were in the would benefit from the recovery, estab-

minority in this country: only one out of lishing a race-based system for assessing

three households owned their home, and property values and risk. The HOLC

property ownership was limited largely to hired local real estate agents to appraise

older individuals and the wealthy. Mort- properties and determine whether they

gages required large upfront payments, would regain their value. Appraisers were

carried high interest rates, and often instructed to consider the condition of the

included a requirement to pay off the house as well as the surrounding neigh-

loan in full after five years. The real estate borhood, including its racial composi-

market was also characterized by limited tion, a practice that came to be known

lending guidelines, high price volatility as redlining (Figure 2). A neighborhood

and appraisers who used “look, spit and could be designated as “low risk” and

guess” methods of assessing property colored green if it was home to “not a

values.5 Homeowners seldom built equity, single foreigner or negro…” Conversely,

with interest-only payments common, and neighborhoods that displayed the “infil-

bore the risk and insecurity associated tration of inharmonious racial groups” or a

with short-term mortgages.6 “concentration of negro population” were

deemed “hazardous” and colored red.12

The collapse of the banking system in These maps thus codified pervasive racism

1929 revealed the fragility of the existing in the financial system and provided the

financial system, and led to broad based basis for de jure discrimination in housing

reforms to bolster the U.S. economy. and mortgage markets.13

Among those reforms (which included the

creation of the Social Security Administra- As Rothstein argues, the HOLC maps

tion and the Public Works Administration “put the federal government on record”

in other sectors)7 was the federal Home as explicitly linking Black households and

Owners Loan Corporation (HOLC), which communities to lower quality housing

was designed to respond to the rising wave and neighborhoods.14 They also created

of foreclosures confronting the nation. By a powerful financial incentive for main-

one estimate, approximately half of all taining patterns of racial segregation,

U.S. urban home mortgages were delin- one that was strengthened when the FHA

quent as of January 1, 1934.8 The HOLC adopted many of the same principles in its

purchased home mortgages that were appraisal system for mortgage insurance.15

facing foreclosure and refinanced them The FHA discouraged banks from making

with more favorable payment terms and loans on properties in redlined areas, and

schedules, keeping more than a million recommended racially restrictive cove-

people—over 10 percent of American nants on newly built suburban neighbor-

5A TERNER CENTER REPORT - MARCH 2021

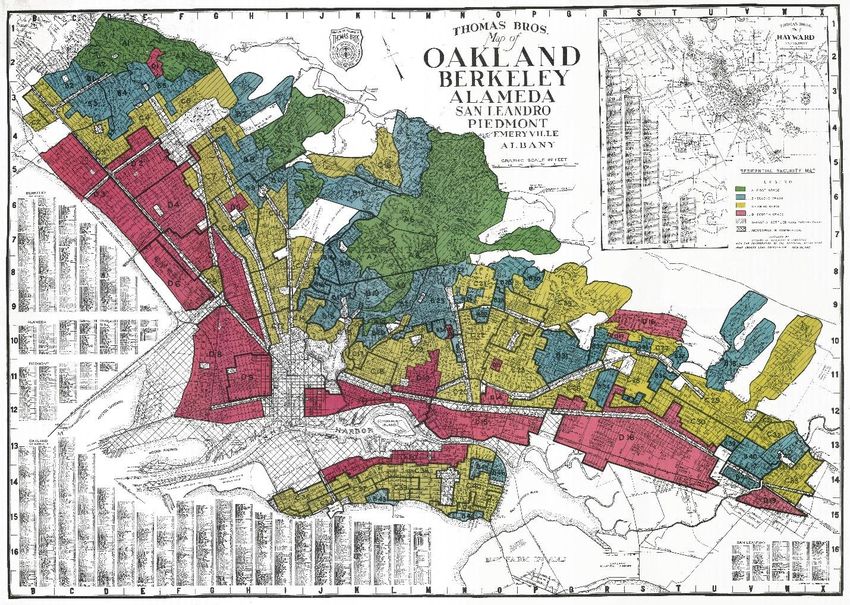

Figure 2: HOLC Redlining Map, Oakland, California

Source: Mapping Inequality: Redlining in New Deal America, University of Richmond Digital Scholarship Lab, available online at: https://dsl.

richmond.edu/panorama/redlining.

hoods to ensure white-only communities.16 further strengthened the government’s

Between 1940 and 1960, the Black-White role in ensuring equal access in credit

homeownership gap increased from 22 to markets. 18

28 percent, and in many cities, levels of

However, prohibiting discrimination is

racial segregation increased as these poli-

not the same as repairing the harm that

cies shaped differential patterns of resi-

was done by past policies, and the impact

dential mobility and housing access for

of redlining endures today. In a recent

Black and White households.17

study, Jacob Faber finds that cities that

These overt forms of de jure discrimi- were appraised by the HOLC became

nation have since been outlawed. The more segregated than those that were

Fair Housing Act of 1968, for example, not mapped, reinforcing the ways in

prohibits discrimination in the housing which systemic racism persists in shaping

market not only by race or ethnicity, but contemporary patterns of inequality.19

also based on religion, national origin, sex, Other researchers have drawn similar

disability, and family status. The Equal conclusions about the lasting legacy of

Credit Opportunity Act (1974), Home redlining, finding that neighborhoods that

Mortgage Disclosure Act (1976), and the were redlined are associated with higher

Community Reinvestment Act (1977) all rates of poverty, lower rates of economic

6A TERNER CENTER REPORT - MARCH 2021

Figure 3: Relationship between HOLC Redlining Map Assessment and Contemporary

Homeownership Rates

90

80

70

Homeownership Rate (2018)

60

50

40

30

20

10

0

A: Best (Green) B: Desirable (Blue) C: Declining (Yellow) D: Hazardous (Red)

Source: Aaronson, D., Hartley, D., &Mazumder, B. (2020). “The Effects of the 1930s HOLC ‘Redlining’ Maps.” Chicago, IL: Federal Reserve Bank of

Chicago.

mobility for children,20 reduced housing access to financial products, and the reluc-

supply, 21 lower life expectancy and higher tance of the federal government to affir-

incidence of chronic diseases,22 as well as matively further fair housing and directly

lower house values and homeownership tackle the persistent “conflation of race

rates (Figure 3).23 and risk to property values”(p. 259). As

a result, the program led to high rates of

While the HOLC maps are historical arti-

foreclosure in Black communities. Taylor

facts, the underlying ideas about prop-

terms this “predatory inclusion,” a term

erty, race, and risk persist, and have never

that could be just as easily applied to the

been sufficiently addressed by the federal

subprime boom that precipitated the next

government. Keeanga-Yamahtta Taylor’s

significant economic crisis nearly 40 years

recent book, Race for Profit: How Banks

later.

and the Real Estate Industry Undermined

Black Homeownership vividly shows the

negative consequences of not addressing

these dynamics. Through an analysis of

FHA’s efforts in the late 1960s and 1970s

to expand homeownership among Black

households, she shows how the passage of

anti-discrimination laws was insufficient

in the face of two enduring characteristics

of U.S. federal homeownership policy: the

reliance on the private sector to expand

7A TERNER CENTER REPORT - MARCH 2021

Uneven Recovery: one in four homeowners were “under-

water,” meaning their mortgage exceeded

Black Homeownership the value of their home.29

after the Great Recession This broader context of economic crisis,

however, obscures the ways in which

The Great Recession of 2007-2009 was Black communities were disproportion-

one of the deepest downturns in the ately impacted by both the labor and

U.S. economy since the Great Depres- housing market downturns. The unem-

sion, notable not only for the severity of ployment rate for Black workers reached

job losses, but also for the persistence of 16.8 percent in March 2010 (compared

weak economic conditions and slow labor to 8.7 percent for non-Hispanic White

market recovery even after the recession workers), and did not reach pre-crisis

was officially over.24 Triggered by crises in levels (7.6 percent) until May of 2017.30

the housing and financial markets,25 the Between 2007 and 2015, the Black-White

unemployment rate hit its peak in October wage gap grew to 26.7 percent, with the

2009 at 10 percent, when more than 15 average White worker making $6.73 more

million individuals were unemployed.26 an hour than the average Black worker.31

During the recession, household net worth

dropped by 18 percent, or more than $10 And, just as 40 years earlier with the

trillion.27 A significant share of this lost predatory expansion of FHA lending to

wealth was due to foreclosures and falling Black families,32 metropolitan racial and

housing values: between 2007 and 2010, ethnic segregation coupled with disparities

approximately 3.8 million households lost in credit access created the opportunity for

their home to foreclosure,28 and nearly subprime mortgage targeting, intensifying

Figure 4: The Impact of the Foreclosure Crisis by Race/Ethnicity

30

Percent of Loans at Risk of Foreclosure or

25

Foreclosed Upon, 2013

20

15

10

5

0

Non-Hispanic Black Hispanic/Latinx Asian

White

Source: Reid, C., Bocian, D., Li, W., & Quercia, R. G. (2017). “Revisiting the Subprime Crisis: The Dual Mortgage Market and Mortgage Defaults by

Race and Ethnicity.” Journal of Urban Affairs 39, no. 4: 469–87.

Note: Universe of loans includes those originated between 2004 and 2008 and tracked until January of 2013.

8A TERNER CENTER REPORT - MARCH 2021

the consequences of the American of the subprime lending boom—either had

housing bubble for Black households lost their home to foreclosure or was at

and other households of color.33 Black risk of doing so—a figure more than double

and Hispanic/Latinx borrowers were the rate of non-Hispanic White borrowers

disproportionately steered into the (Figure 4).

subprime market channel by lenders

who targeted their marketing efforts to The impacts were also spatial: neighbor-

households and neighborhoods that had hoods with more than 50 percent Black

untapped demand for credit, including residents had a foreclosure rate of twice

inner city minority neighborhoods that as high as those with less than 10 percent

had previously been redlined.34 These Black residents (Figure 5). The impact of

borrowers were charged higher interest these concentrated foreclosures in Black

rates and sold risky mortgage products neighborhoods went beyond the direct

with little consideration for whether they loss of homeownership for those families

would be able to afford the home over the experiencing default. These neighbor-

long term.35 hoods experienced much higher rates of

eviction among renters living in foreclosed

Subprime lending products and practices buildings: while data are hard to come by,

contributed directly to higher delinquency an estimated 46 percent of homes facing

and foreclosure rates among Black and foreclosure over this time period were

Hispanic/Latinx homebuyers, even after used as rental properties.37 In addition,

controlling for differences in income, these neighborhoods were more likely to

credit scores, and other observable charac- experience the negative spillover effects

teristics.36 By 2013, more than 25 percent associated with foreclosures, including

of Black homeowners who bought their lower property values and higher rates of

house between 2004 and 2007—the height crime.38

Figure 5: Neighborhood Foreclosure Rate by Percent Black Residents

Less than 10% Black

Residents

10 - 50% Black

Residents

More than 50% Black

Residents

0% 5% 10% 15% 20% 25% 30%

Percent of Loans at Risk of Foreclosure or Foreclosed Upon, 2013

Source: Data analysis based on Reid, C., Bocian, D., Li, W., & Quercia, R. G. (2017). “Revisiting the Subprime Crisis: The Dual Mortgage Market and

Mortgage Defaults by Race and Ethnicity.” Journal of Urban Affairs 39, no. 4: 469–87.

Note: Universe of loans includes those originated between 2004 and 2008 and tracked until January of 2013. Black refers to the percent of

residents in a census tract who self-identify as Non-Hispanic Black, and does not include Hispanic Black residents or those indicating two or

more races.

9A TERNER CENTER REPORT - MARCH 2021

The Federal Government’s Three factors played into this uneven

Response to the Crisis recovery.

The U.S. government’s response to the First, the federal government failed

Great Recession included a wide range to step in with direct borrower relief

of fiscal and monetary interventions. early enough. Researchers and commu-

Ranging from the Federal Reserve’s nity members had raised concerns over

efforts to increase liquidity in the finan- the rise in predatory subprime lending—

cial markets, to the Troubled Asset especially in the refinance market—in

Relief Program (TARP), to the American Black communities as early as 1999, and

Recovery and Reinvestment Act of 2009, certainly well before 2007, there was

these interventions—while controver- evidence that foreclosures were increasing

sial—did help to reduce the severity and in minority neighborhoods.40 However, it

the length of the economic downturn. wasn’t until the crisis hit Wall Street that

Estimates suggest that, due to the fiscal federal policymakers started to take the

and financial responses of policymakers, stress in the housing market seriously. In

real GDP was 16.3 percent higher in 2011, addition, racialized narratives about who

and unemployment was almost seven was to blame for the foreclosure crisis led

percentage points lower, than it would to concerns over moral hazard and “irre-

have been without these interventions.39 sponsible” borrowers choosing to strate-

gically default rather than a focus on the

However, the policies and programs that structural factors that had led Wall Street

were designed to directly intervene to to overextend its investments in subprime

assist homeowners in distress were much mortgage-backed securities.41

less successful. Even though these inter-

ventions were not intentionally discrim- The primary form of borrower relief came

inatory (as, for example, the HOLC’s in the form of the Making Home Afford-

redlining practices coming out of the Great able (MHA) program, passed in 2009.

Depression were), they nevertheless failed MHA included both a loan modifica-

to address the disproportionate impacts of tion program (HAMP) as well as a refi-

the foreclosure crisis on Black households nance program (HARP), which encour-

and communities. As a result, efforts to aged lenders and mortgage services to

address the foreclosure crisis—such as work with borrowers in distress to rene-

the Making Home Affordable (MHA) and gotiate their loan terms. While research

the Neighborhood Stabilization Program has shown that the programs themselves

(NSP)—while on their face race-neutral, didn’t lead to differential loan modifica-

failed to address the structural reasons tion rates for Black borrowers,42 by the

why Black homeowners and communities time these programs got off the ground, a

were hardest hit, and thus benefited least significant share of Black homeowners had

from the ensuing recovery. already lost their homes to foreclosure. In

2005, for instance, more than 30 percent

10A TERNER CENTER REPORT - MARCH 2021

Figure 6: Distribution of Foreclosure Filings over Time, by Race/Ethnicity

60

50

Share of Foreclosure Filings

40

30

20

10

0

2005 2009 (Start of HAMP/HARP) 2012

Non-Hispanic White Black

Source: Data analysis based on Reid, C., Bocian, D., Li, W., & Quercia, R. G. (2017). “Revisiting the Subprime Crisis: The Dual Mortgage Market and

Mortgage Defaults by Race and Ethnicity.” Journal of Urban Affairs 39, no. 4: 469–87.

of recorded foreclosures were experi- that were keeping delinquent borrowers

enced by Black homeowners, despite the from foreclosure: insufficient incomes to

fact that they made up only 8 percent of sustain their mortgages, as well as house

outstanding mortgage liens (Figure 6). values that had plummeted well below

HAMP and HARP only went into effect their purchase price. In addition, dele-

when the share of foreclosures among gating authority to mortgage servicers

non-Hispanic White borrowers had led to considerable problems with both

grown and become more representative tracking and enforcement of relief efforts.44

of the total mortgage business. The lack Stronger federal actions—such as making

of policy maker attention to the crisis that homeowner assistance programs manda-

was hitting Black communities—one that tory or allowing borrowers to restructure

was strongly related to predatory lending their mortgages in bankruptcy—never

practices that sought to strip wealth from gained political traction. While these

Black homeowners—reinforces the not-so- limitations were true for the majority of

subtle ways that these foreclosures were borrowers in distress, the higher rates

initially ignored and then reframed as the of unemployment among Black home-

result of risky borrower decisions rather owners, coupled with greater declines in

than mortgage lending practices. house values and higher rates of negative

equity in Black communities,45 meant that

Government relief also didn’t go deep

the support that was available often did

enough.43 By focusing largely on loan

not reach Black households.

modifications and refinancing, HAMP and

HARP did not address two major factors

11A TERNER CENTER REPORT - MARCH 2021

Second, in the wake of the crisis, High credit score and down-payment

lenders greatly tightened their standards translated into a recovery in

credit standards. Some tightening—and which only the highest credit and highest

particularly more rigorous assessments of wealth borrowers could buy homes.48

a borrower’s ability to repay their mort- Black households, who on average have

gage—was long overdue. But as housing lower credit scores and wealth because of

markets softened, and as affordability historical structural barriers to accessing

increased, credit standards remained credit,49 were thus disproportionately shut

restricted so that only the highest credit out of the homeownership market at the

quality borrowers were able to get a mort- same time that home prices in many neigh-

gage. Even FHA lending—which provided borhoods were at historic lows (Figure 7).

a critical backstop and counter-cyclical Third, the federal government failed

lending role post-crisis—increasingly to adequately address the uneven

shifted toward higher-credit borrowers. distribution of foreclosures across

By 2010, nearly 74 percent of FHA loans neighborhoods. The federal govern-

went to prime or near-prime borrowers, ment sought to address the negative spill-

compared to approximately 25 percent in over effects through the Neighborhood

2000.46 The Urban Institute estimated that Stabilization Program (NSP). NSP, initially

between 2009 and 2013—a period that saw authorized by the 2008 Housing and

house prices recover in many markets— Economic Recovery Act (HERA), entailed

lenders made 4 million fewer loans than three separate rounds, directing approxi-

they would have made if credit standards mately $7 billion towards the acquisition

had been what they were in 2000, a period and redevelopment of foreclosed proper-

of reasonable lending standards. 47

Figure 7: Changes in Home Purchase Originations by Race/Ethnicity, 2004 - 2018

160

Indexed Change in Home Purchase Mortgage Originations

140

120

100

80

60

40

20

0

04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

20 20 20 20 20 20 20 20 20 20 20 20 20 20 20

Asian Black Hispanic/Latinx Non-Hispanic White

Source: Author’s calculations of HMDA Data.

12A TERNER CENTER REPORT - MARCH 2021

ties. NSP sparked significant innovation A broad set of investors stepped into the

at the local level, with city governments vacuum, purchasing foreclosed homes

and nonprofits collaborating on efforts to to convert them to rentals. As shown

establish community land trusts, develop in Figure 8, until 2006, only between 5

social enterprises, and build the capacity and 8 percent of home purchases were

of the field to manage scattered-site afford- made by investors. After 2006, however,

able rentals.50 investors made up an increasingly large

share of the home purchase market. This

However, the program faced significant included both small-scale investors (about

challenges as well, including insufficient 50 percent of the investor market), inves-

funding to match the scale of the crisis, as tors buying between 10 and 100 properties

well as a government oversight structure (30 percent) and large-scale investors (20

that made it difficult for nonprofits to move percent).

as quickly as private companies to purchase

properties.51 The quality and impact of Investor purchases were more common

NSP initiatives also varied greatly by state among lower-priced properties and in

and locale, creating a headwind against neighborhoods with a higher percentage

equity across jurisdictions. The FHA’s and of Black residents, closing off the oppor-

GSE’s bulk distressed asset sales further tunity to buy lower-cost homes. Between

limited the ability of lower-income house- 2011 and 2014, during the height of

holds and nonprofits to purchase more investor activity, nearly 1 in 4 home sales

moderately-priced properties.52 in majority Black neighborhoods went

to investors, and more than 1 in 3 lower-

priced homes did (Figure 9). 53

Figure 8: Share of Home Purchases by Investors, by Property Price Tier

25%

20%

15%

Percent of Sales

10%

5%

0%

99 000 001 002 003 004 005 006 007 008 009 010 11 012 013 014 015 016 017

19 2 2 2 2 2 2 2 2 2 2 2 20 2 2 2 2 2 2

All Home Purchases Lower-Priced Homes Mid-Priced Homes Higher-Priced Homes

Source: Author’s analysis of CoreLogic53 data.

13A TERNER CENTER REPORT - MARCH 2021

Figure 9: Neighborhood Share of Home Purchases by Investors, by Property Price Tier and Percent Black

Residents

40%

35%

30%

25%

Share of Sales

20%

15%

10%

5%

0%

Less than 10% Black Residents 10 - 50% Black Residents More than 50% Black Residents

Investor Purchases 2011-2014 Low Tier Investor Purchases 2011-2014

Source: Author’s analysis of American Community Survey, 2018 5-year estimates and CoreLogic54 data.

Note: Black refers to the percent of residents in a census tract who self-identify as Non-Hispanic Black, and does not include Hispanic Black

residents or those indicating two or more races. Investor purchase data was converted from zip codes to tracts using the Missouri Census Data

Center’s Geocorr 2018 crosswalk.

The Implications for Black failure of the U.S. government to address

Homeownership patterns of residential segregation and the

potential for capital exploitation in Black

54

The confluence of these factors—higher neighborhoods led to an uneven recovery

unemployment rates, higher foreclosures, not only in Black homeownership and

increased investor activity, and tight- wealth, but also in which neighborhoods

ened credit—all intersected to undermine experienced continued disinvestment or

Black homeownership rates (Figure 1) and intensified pressures around gentrifica-

increase the racial wealth gap. Researchers tion and displacement.

at the Urban Institute estimate that even

after controlling for differences in age and To demonstrate this, we clustered urban

educational attainment, Black families neighborhoods in the United States

lost a larger percentage of their wealth along two dimensions: the share of home

during the Great Recession than non-His- purchase loans that were made to Black

panic White families (47.6 versus 26.2 borrowers during the recovery period

percent).55 (2012-2018), as well as the change in the

share of lending to Black borrowers before

Yet these aggregate losses mask the ways and after the crisis.56 This clustering

in which the recovery was also shaped captures two dimensions of lending during

not only by who could buy homes and the recovery: overall access to mortgage

benefit from the recovery in home values credit for Black borrowers, as well as

between 2012 and 2018, but also where how much the share of lending to Black

those homes were located. The continued borrowers changed over time. The purpose

14A TERNER CENTER REPORT - MARCH 2021

of this clustering was to identify how attainment, as well as lower house values.

access to credit—and specifically, loans for These characteristics also typified the

home purchase—shifted over the period neighborhoods in which the recovery

of the recovery. The clustering process period saw increases in lending to Black

identified four different types of neighbor- households, though these neighborhoods

hoods: those that had low levels of mort- were more demographically diverse.

gage lending to Black neighborhoods both

Of particular note, however, are neighbor-

overall and during the recovery, those that

hoods that saw significant declines in their

saw declines in mortgage lending to Black

lending to Black households over the course

borrowers, those that saw increases in

of the recovery. Although they comprise a

mortgage lending to Black borrowers, and

relatively small share of neighborhoods,

those that continually have the majority of

these neighborhoods were places where

loans made to Black borrowers.

the share of mortgage lending to Black

The analysis highlights the continued households dropped to just 22.5 percent of

racial segmentation of housing markets. all purchase originations during recovery.

Of the approximately 47,000 urban This, despite the fact that Black house-

neighborhoods considered for this anal- holds made up approximately 50 percent

ysis (census tracts), more than 95 percent of the population in these neighborhoods.

originated less than 4.2 percent of loans to These neighborhoods also saw higher

Black borrowers. This represents a decline rates of investor purchases in both 2009

in lending to Black borrowers since 2004, and 2014, and a higher share of single-

but only slightly, emphasizing the chal- family homes being used as rental homes.

lenges Black households face in accessing These neighborhoods were also the ones

housing in a broad range of metropolitan that experienced the most dramatic price

neighborhoods. These neighborhoods are gains during the recovery (Figure 10),

predominantly non-Hispanic White, and highlighting the interconnections between

have higher incomes, higher house values, subprime lending, foreclosures, and the

and higher levels of educational attain- shifts in who benefitted from the recovery

ment than other neighborhoods, all of at the neighborhood scale. Neighborhoods

which work to further determine who has that saw declines in mortgage lending to

access to resources and privilege (Table 1). Black borrowers during the recovery saw

an increase in average property values

In contrast, the clustering analysis from $210,000 at the bottom of the

also identified neighborhoods in which market to over $300,000 in 2018, with

Black borrowers comprised a larger these gains accruing disproportionately

share of lending—over two-thirds of all to investors and non-Black households.

purchase mortgages. Lending patterns These neighborhoods were also more

in these neighborhoods did not change likely to be in cities experiencing gentrifi-

much over the course of the recovery cation pressures, including the San Fran-

either. Yet, in these neighborhoods, the cisco Bay Area, Los Angeles, Washington

long-term consequences of residential DC, Atlanta, and Nashville.

segregation manifest in lower household

incomes, lower rates of educational

15A TERNER CENTER REPORT - MARCH 2021

Table 1: Characteristics of Neighborhoods by Lending Clusters, 2019

Declines in

Low Levels Increases High Share

Mortgage

of Lending in Lending of Lending

Lending

to Black to Black to Black

to Black

Borrowers Borrowers Borrowers

Borrowers

Percent of Home Mortgage

Purchase Loans, Black Households 5.1 57.0 32.9 71.5

(2004)

Percent of Home Mortgage

Purchase Loans, Black Households 4.2 22.5 45.6 69.5

(2012-2018)

Neighborhood Socio-Economic

Characteristics (2019)

Percent Non-Hispanic White 66.5 29.4 31.8 15.1

Percent Asian 6.0 3.4 3.5 2.0

Percent Black 7.5 49.5 46.5 71.9

Percent Hispanic/Latinx 16.6 14.1 14.8 8.0

Percent with a BA or Higher 34.8 28.3 24.7 23.8

Unemployment Rate 4.8 7.0 6.7 8.3

Median Income $78,588 $55,946 $60,349 $58,922

Housing Market

Percent of Loans Seriously

13.2 18.9 20.0 21.8

Delinquent (2013)

Percent of Subprime Originations

24.7 39.1 36.1 39.6

(2004-2008)

Share of Investor Purchases (2009) 6.3 11.4 8.4 10.9

Share of Investor Purchases (2014) 12.9 18.9 16.5 18.2

Percent Single-Family Rentals

17.4 27.9 21.4 22.2

(2019)

Median House Value (2019) $339,604 $302,122 $195,775 $196,411

Number of Neighborhoods 44,622 275 890 1,259

Source: Author’s analysis of American Community Survey and Home Mortgage Disclosure Act Data, 2004 – 2018. Analysis limited to census tracts

with at least 100 home purchase loans between 2010 and 2018. Black share of loans calculated as a percent of loans with race data reported. 16A TERNER CENTER REPORT - MARCH 2021

Figure 10: House Price Recovery, by Lending Clusters

140

130

120

Zillow House Value Index (2004=100)

110

100

90

80

70

60

50

40

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

High Share of Lending to Black Borrowers Increases in Lending to Black Borrowers

Low Levels of Lending to Black Borrowers Declines in Lending to Black Borrowers

Source: Author’s calculations of Zillow House Price Index, adjusted for inflation and normalized to 2004 values.

It is difficult to estimate the consequences reveals the continued stark differences in

of these trends on Black wealth, since the access to credit and wealth building across

counterfactual is far from clear. But to neighborhoods.

illustrate the longstanding consequences

Black households who were able to enter

of residential segregation and differential

homeownership over this time period did

access to credit on wealth, we estimated

build equity—an estimated $44 billion.

the amount of equity that homeowners

But had they received mortgages based on

who bought their homes between 2012

their share of the population (13.4 percent),

and 2018 gained, based on the year

they would have gained an additional $93

they bought their home and the house

billion in equity. Almost all of those gains

price appreciation that occurred in their

would have come from increased access

neighborhood through the end of 2018

to neighborhoods with very low levels of

(Figure 11). This vastly underestimates

lending to Black households (Figure 11).

differences in wealth accumulation over

While largely illustrative, this analysis

this time period, since it does not account

nevertheless demonstrates that in order to

for those who already owned homes, or

close the wealth gap, policies need to tackle

the equity accrued to those who purchased

both access to credit and racial exclusion.

the property without a mortgage. Yet it

17A TERNER CENTER REPORT - MARCH 2021

Figure 11: Racial Disparities in Homebuyer Equity Accumulation, 2012-2018

Declines in Mortgage Lending to Black Borrowers

Increases in Lending to Black Borrowers

High Share of Lending to Black Borrowers

Low Levels of Lending to Black Borrowers

0 20 40 60 80 100 120 140 160

Increase in Housing Equity (Billions $2019)

Equity Accumulated by Black Borrowers, 2012-2018

Alternate 1: Equity if Lending Share was Same as in 2004

Alternate 2: Equity Share if Lending Equal to Black Population in Neighborhood

Alternate 3: Equity Share if Lending Equal to Share of Black Population Nationally

Source: Author’s calculations of HMDA and Zillow Data.

The COVID-19 Pandemic employment since March, compared to

43 percent of non-Hispanic White adults.

The COVID-19 pandemic and associated There is also evidence that Black workers

economic recession presents a new threat are more likely to have experienced perma-

to the well-being of Black homeowners, nent layoffs.58

and has the potential to further exacer-

These disparities have increased housing

bate these racial inequalities in wealth.

insecurity for both Black renters and

Although the impacts of the pandemic

homeowners. Nearly one in five Black

have been widespread, Black workers face

homeowners is behind on their mort-

a double burden: they are more likely to

gage payments, compared to less than 10

be employed in the essential workforce

percent of non-Hispanic White house-

and thus susceptible to the virus,57 yet at

holds (Figure 12).

the same time they are also more likely to

have experienced a loss of income since The systems that are in place to support

March. Based on the Census Household homeowners in arrears are also likely

Pulse Survey, 55 percent of Black adults to be less helpful for Black households,

have experienced a loss of income or reinforcing the ways in which structural

18A TERNER CENTER REPORT - MARCH 2021

Figure 12: Homeowners Behind on Mortgage Payments, by Race/Ethnicity, November/December 2020

25%

Percent of Owner Households with a Mortgage

20%

15%

10%

5%

0%

Non-Hispanic White Black Hispanic/Latinx Asian Other

Source: U.S. Census Household Pulse Survey, November 25-December 7, 2020.

disadvantage manifests in multiple ways. their mortgage payments will be able to

For example, Black households who sell their homes rather than go into default.

applied for unemployment benefits were While certainly better than a foreclosure

less likely to receive them than non-His- (for both the borrower and the broader

panic White adults, and on average, their housing market), this nevertheless raises

unemployment checks were lower (even significant racial equity concerns, particu-

for workers who earn the same salary) larly if Black homeowners are more likely

due to state differences in benefit cover- to be forced to sell due to financial insecu-

age.59 In addition, while homeowners with rity coming out of the pandemic.

federally backed mortgages have some

reprieve thanks to forbearance options, All of this—coupled with research that

a Fannie Mae survey showed that half of shows that the severity and distress of a

homeowners do not know about forbear- recession falls hardest on households of

ance options and that the knowledge gap color—demands that the administration

is particularly acute for lower-income and take both immediate and deliberate action

minority homeowners.60 to ensure a more equitable recovery out of

this crisis than the last. This will require

The current market conditions suggest that both short-term relief actions, as well as

we will not see the same wave of foreclo- a more intentional set of policies for the

sures as we did during the last recession, in recovery that recognize and address the

part due to the fact that house prices have structural inequalities that have produced

been largely stable and/or rising. This and sustained racial inequalities in

means that homeowners unable to make housing and credit markets.

19A TERNER CENTER REPORT - MARCH 2021

Policy Implications that disproportionately benefited those

with capital, including investors and

The election has ushered in a new admin- higher wealth households.

istration, one that has the mandate and

Undoing the legacy of housing and mort-

the responsibility to lead the country out

gage discrimination and redistributing

of the COVID-19 pandemic and associated

the risks and rewards of homeownership

economic downturn. Those actions must

will require a much stronger role for the

be bold and focus on relief that is likely to

federal government going forward. The

have the greatest impact on lower-income

lessons from past periods of crisis point

and households of color. For example,

to two, twin principles that can guide this

expanding housing assistance for renters

agenda: first, develop policies that expand

and ensuring that the crisis doesn’t lead to

access to credit in meaningful and respon-

widespread evictions and increased home-

sible ways to underserved borrowers

lessness is fundamental to reducing racial

and communities, and second, explicitly

inequality, given the high share of Black

confront the systems that work to perpet-

households who are renters. There also

uate residential segregation and that

needs to be explicit policies focused on

exclude or displace lower-income house-

helping households facing accumulated

holds of color from the neighborhoods

rental or mortgage debt.

they want to call home. These two need to

However, these emergency actions are be pursued in tandem, and supported by

insufficient to address the larger systemic federal funding, attention to oversight and

inequalities that Black households face in implementation, and consumer protection.

the homeownership market, during the

The first principle goes back to the long-

recovery period and beyond. For too long,

term repercussions of redlining and the

housing policy has reinforced the legacy of

systemic denial of credit to Black house-

redlining by focusing on the deficiencies

holds. At the heart of this challenge is

of Black neighborhoods, rather than on

the way in which the lending industry

the structures that produced them. The

assesses and prices credit risk. Struc-

lessons from the last recession suggest

tural racism, both past and present, is

that if policies are not explicitly focused on

baked into how the financial system eval-

addressing the structural vulnerabilities

uates a borrower’s creditworthiness. Not

facing Black households, the benefits of

surprisingly, researchers have found that

the recovery will largely accrue to higher-

Black borrowers have a significantly lower

income households, furthering racial

median FICO score (626) compared to

inequalities in the housing market. As

non-Hispanic White borrowers (751). They

Ta-Nahesi Coates argues in “The Case for

are also more likely to have no credit score:

Reparations,” failing to address the roots

an estimated 21 percent of the Black popu-

of residential segregation merely sets

lation has no credit score, compared to

up recurring opportunities for capital to

12 percent of non-Hispanic White house-

extract wealth from Black communities.

holds.61 The rise of Fintech lending, as well

The data presented here show that these

as innovations in credit scoring algorithms

are not dynamics relegated to the past;

and the use of big data, all have the poten-

the subprime crisis—coupled with the

tial to further embed racial differences in

lack of federal attention to addressing

the assessment of risk.62

the conditions for Black families and

neighborhoods—contributed to a recovery

20A TERNER CENTER REPORT - MARCH 2021

Failing to confront these disparities However, the Biden-Harris Adminis-

means that the system will continue to tration should also seek to develop new

produce unequal outcomes. Studies have programs in which the government explic-

consistently shown that Black borrowers itly helps lower-credit score and lower-

are more likely to be denied a mortgage, wealth borrowers overcome the conditions

receive a loan with a higher interest rate, created by historical discrimination. Down

and face greater constraints to refinancing payment programs—while important

to a lower cost product.63 These inequal- in overcoming collateral constraints for

ities translate into material differences some first-time homebuyers—aren’t suffi-

in wealth: A recent paper estimates that cient on their own. Ultimately, reducing

mortgage discrimination costs Black and the Black/White homeownership gap will

Hispanic/Latinx borrowers 7.9 basis require more affirmative credit programs,

points more in interest on their home and a meaningful intent to overcome the

mortgages. Although this difference may legacy of discrimination in housing and

seem small, this “tax” adds up, costing an credit markets. The Community Reinvest-

estimated $765 million in extra interest ment Act is an example of such an affirma-

per year.64 Other researchers have esti- tive obligation, and should be modernized

mated that the average interest rate for to increase its effectiveness at redressing

Black homeowners is 33 basis points racial inequalities.66 The federal govern-

higher than for non-Hispanic White ment has other tools at its disposal as well.

homeowners, translating into an extra For instance, the Equal Credit Opportu-

$743 in mortgage interest costs a year.65 nity Act includes a provision for Special

More broadly, the impacts of how lenders Purpose Credit Programs (SPCPs) that

evaluate and price risk go beyond home- would allow a targeted lending program

ownership, affecting wide-ranging sectors on the basis of a protected class such as

such as job and rental applications, as well race or national origin without violating

as auto, life, and homeowners insurance. other federal antidiscrimination statutes,

such as the Fair Housing Act.67

The significance of credit scores for

everyday life means that there needs to GSE reform should also prioritize their

be much stronger oversight of risk assess- public mission of providing increased

ment practices, and greater transpar- credit access for affordable housing

ency into how credit scores are calculated and homeownership. The GSEs have a

and used. The Biden-Harris Adminis- long history of developing underwriting

tration should leverage the authority guidelines and products, making invest-

of the Consumer Financial Protection ments and developing partnerships that

Bureau to ensure that algorithms used have safely expanded credit to under-

to predict credit risk include expanded served communities. Indeed, the GSE

data on consumer payments (e.g., utility “Duty to Serve” principle is broader than

payments), increase the transparency and fair lending, and involves taking affirma-

quality of credit score calculations, and tive steps to reach out to communities

pursue disparate impact cases under the traditionally underserved by the housing

Equal Credit Opportunity Act and Fair finance market.68 Duty to Serve obliga-

Housing Act. tions, coupled with public funds to subsi-

21A TERNER CENTER REPORT - MARCH 2021

dize mortgage programs for lower-income income requirements, to better assess and

and lower-wealth households, could help mitigate risk while extending credit to

to overcome the different “starting line” borrowers who don’t qualify for a conven-

for Black households with limited assets tional loan.71 While more work is needed

or lower credit scores. to identify which products may be the

most beneficial for Black and other lower-

There are models to build on, that have wealth, the FHA and/or the GSEs are in a

demonstrated it is possible to expand unique position to analyze data and eval-

access to credit and homeownership uate pilot programs to identify potential

in responsible ways. For example, the responsible, scalable models.

Community Advantage Program, a joint

effort of the Ford Foundation, Fannie Policymakers also need to place greater

Mae, and Self-Help Credit Union, used emphasis on post-purchase intervention

a $50 million grant as a credit enhance- and support. There is increasing evidence

ment, which leveraged $4.74 billion in that income volatility and risk among

financing for low-interest-rate mortgages lower-income households is growing.72

to nearly 52,000 low-income home- Lower-income homeowners have a smaller

owners across the country.69 While the financial cushion with which to withstand

serious delinquency rate for these loans the impact of negative life events, such as

during the height of the foreclosure crisis unemployment or serious illness, or to

was higher than that for prime loans (10 meet unanticipated repair costs, and by

percent compared to 5 percent for prime virtue of their limited housing choices,

fixed-rate loans), it was substantially they are more likely to buy houses in need

lower than those for prime adjustable-rate of repair. Research has shown that access

loans, subprime fixed-rate loans, and to savings to cover 2-3 months of mortgage

subprime adjustable-rate loans, which payments leads to lower default rates than

exhibited serious delinquency rates of 18, equity support through down payment

22, and 43 percent, respectively.70 Given assistance.73 Structuring an insurance

the growth and increased capacity of the or savings program—for example, a

community development finance industry, “post-purchase” Individual Development

a new federal fund to provide credit Account that would set money aside for

enhancement capacity to expand this home improvements or shortfalls in mort-

program and bring the number of assisted gage payments funded in part by a share

households to scale could be significant in of the monthly loan payments—could help

mediating inequalities in access to credit improve the sustainability of homeown-

and homeownership. Another potential ership, especially for Black homeowners

remedy would be to look to the Veteran who may face greater precarity in the labor

Administration’s underwriting practices, market.74

including their loan-to-value and residual

22A TERNER CENTER REPORT - MARCH 2021

Second, the Biden-Harris Administra- on mobility strategies alone obscures the

tion needs to center neighborhoods and important ties individuals have to place,

place-based policy-making as part of its and ignores the voices of Black residents

racial equity strategy. The persistence of and organizers who are making claims for

policies and practices that reinforce racial the right to stay in their community.

and ethnic segregation means that Black

households continue to live in different A renewed role for the federal government

neighborhoods than their non-Hispanic in community development could help to

White counterparts. The Administration address the longstanding harms of resi-

has already taken important steps in that dential segregation by providing funding

direction, recommitting to the Affirma- to increase investment in Black commu-

tively Furthering Fair Housing (AFFH) nities through localized strategies, rather

rule and the disparate impact standard.75 than real estate speculation. Especially

Yet there is more to be done to tackle resi- with the likely long-term repercussions of

dential segregation, and the ways in which COVID-19 in lower-income and communi-

not only federal but also local zoning laws ties of color, the federal government could

continue to shape patterns of exclusion. In play a vital role in ensuring that mission-

California, recent legislation has reinforced driven entities have access to funding and

the goals of AFFH, requiring that each city technical assistance to ensure that the

and county include an analysis and action recovery doesn’t merely benefit those with

plan to combat housing discrimination as access to liquid capital. For example, a

part of its General Plan.76 Requiring this of governmental backstop or guarantee (e.g.,

more jurisdictions, as well as expanding through FHA or the GSEs) could be made

the capacity of jurisdictions to assess and available to mission-driven entities to

address barriers to fair housing, could help purchase properties at risk of speculative

to support more inclusive zoning practices flipping in exchange for long-term restric-

which would allow for greater housing tions on rents.79 Others have proposed

choices across metropolitan regions.77 the creation of a “Social Housing Devel-

opment Authority,” which could acquire

However, the framework for implementing distressed properties and then convey

fair housing also needs to account for the them to nonprofit housing organizations,

trends that are reshaping the geography of tenant groups, or other mission-driven

opportunity in many cities and metropol- groups.80

itan areas. Gentrification, displacement,

and the suburbanization of poverty are In addition, the federal government should

creating new patterns of racial exclusion. support the expansion of community

In addition, scholars are increasingly land trusts and cooperative ownership

pointing to the ways in which policies that models, which to date have been limited in

seek to promote integration can reinforce scale due to lack of funding and technical

the devaluation of Black neighborhoods.78 capacity. These models have the potential

What is needed are intentional efforts to build wealth and preserve affordability

to both open up exclusionary neighbor- over the long-term. In cities across the

hoods (urban and suburban) as well as country, community-led initiatives—

invest in community development and often led by Black community members—

the preservation of affordable housing in have been developing and sustaining

lower-income neighborhoods. The focus cooperative models of land ownership

23You can also read