Danske Banks approach to Open Banking - Kasper Sylvest Head of Group Financial Market Infrastructure and sector collaboration Danske Bank - Mobey ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Danske Banks approach to Open Banking

Kasper Sylvest

Head of Group Financial Market Infrastructure and sector collaboration

Danske Bank

1

The EU’s main purpose with PSD2 which is the trigger to Open Banking

1. Pave the way for 2. At the same time 3. Foster competition & By regulating

faster payments & focus on consumer innovation access to

harmonized rules protection with a Payment

detailed set of security accounts

requirements

2

PSD2 is expected to fundamentally change the environment

RTS Final text Parliament

released by European PSD2 approved

Commission Implementation RTS text PSD2 RTS implementation

implementation deadline, incl. API’s

NO (expected)

Nov 2017 Jan 2018 May 2018 Q1 2019 Sept 2019

Services Threats and opportunities

Financial Spend Budgeting

AIS – Account Information Services

overview overview tools

Access to customer accounts • Provides account information in a consolidated

via APIs enables the provision way This will enable a more competitive market, with

new Personal Financial Management tools and

of entirely new types of

increased payment options for consumers and

service that are regulated merchants

under PSD2 PIS – Payment Initiation Services

• Initiate payments directly on the

customers account

Recurring Mobile Cross border

payments payment transfer

3

Digital aggregators have already disrupted a number of industries, ILLUSTRATIVE

PSD2 could be the accelerator for financial service disruption

Maturity

Job search Retail Travel

Financial services

Time since disruption started

Source: Expert interviews; McKinsey FinTech Panorama data base; Team analysis 4

PSD2 has kick-started Open Banking initiatives – producing API’s beyond PSD2 started but

not well defined

Closed API’s Open API’s

Private Partner Compliance Public

Open API’s that is accessible to Open API’s that is accessible to

Closed API’s that is accessible to Open API’s that is accessible to

anyone complying with a anyone: Typically involves some

DB only preferred partners

predefined set of requirements form of basic registration

5

Danske Bank are moving from traditional integrator to ecosystem provider and ecosystem

participant

Ecosystem provider Ecosystem participant

DB

developed IOT Devices

Big Tech

services (e.g., Wearables)

DB Digital Fintechs DB APIs Retailers

(e.g., Coop &

Bank 3.0 and Services S-Group)

Partner

developed

services

Banks Loyalty

schemes

(e.g., Wrapp)

6

A number of pain points should be addressed in order to fulfil Open banking ambition and

entering into partnerships

Development capacity constraints

Rigid security architecture and approval

Complex and fragmented data landscape,

Technical foundation with limited API’s and dedicated testing environment

Heavy/inefficient iteration process between business and IT

Limited experience with partner engagement and low risk appetite

7

Our partnership with Spiir gives our Nordic customers one view of all their bank accounts in

our interface

All your banks at your

fingertips

Better overview makes better

decisions. All your bank

accounts integrated into our

mobile bank

8

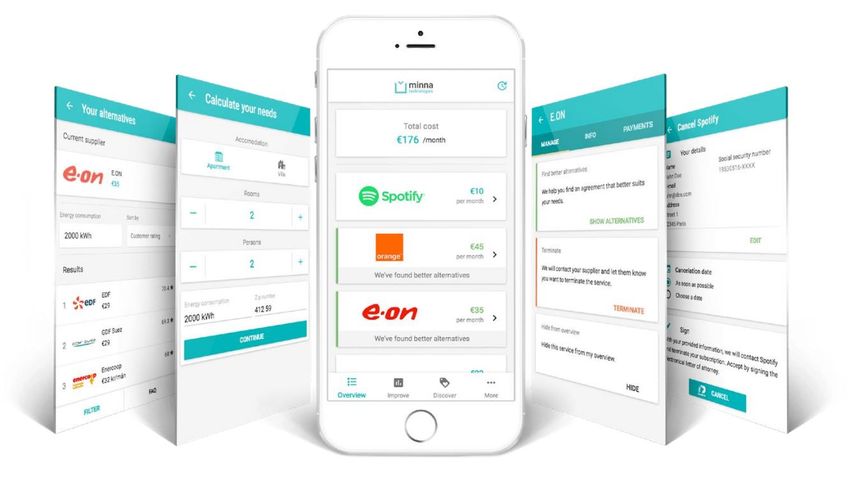

Our partnership with Minna technologies offer customers to save time and money by

enabling subscription management within the Mobilebank app

Benefits for customers

• Overview of all

subscriptions and

recurring payments

• Possibility to easily cancel

subscriptions

• Switch subscriptions to

save costs

• Save time and money

• Integrated in the Mobile

banking App

9

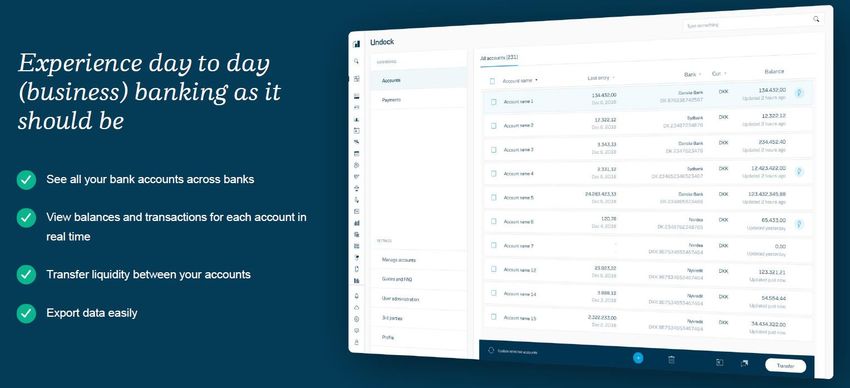

Undock – Experience day to day business banking as it should be

10District aims to provide

full financial overview

& control

• Intelligently adapts to and improves

corporate workflows

• Integrates applications from multiple

service providers to create a

financial eco-system

• Provides proactive advisory and

financial insights

11The performance of our UK Open Banking APIs are stable with most request coming from

other banks

TPP in March API Calls (AIS) API Calls (PIS)

Number of successful API calls

40 Yolt 28,818 0

Thousands

30 Ulster Bank NI Mobile Banking 6,103 0

20 Royal Bank of Scotland Mobile Banking 1,665 0

10 Tink 1,554 0

0 consents.online 521 0

Jan '19 Feb '19 Mar '19

NatWest Mobile Banking 505 0

98% 836.28 156

API avg. API avg. Number of third

availability response time parties

in milliseconds

12Key takeaways

New Partnerships are There will be no

platforms will key for future “automatic”

emerge value creation. winners

Customers don’t Open banking will

care about open accelerate the

banking – but the speed of fintech

experience. innovation.

13Thank you!

Kasper Sylvest

Head of Infrastructure and Sector Collaboration

ksy@danskebank.dk

14You can also read