ECB Contact Group Market update

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CURRENCIES

ECB Contact Group Market update GLOBAL

CURRENCIES – November 2020

Richard Oliver Issuer of report: HSBC Bank plc

Head of EMEA FX Trading

HSBC Bank plc

richard.oliver@hsbcib.com Disclosures & Disclaimer: This report must be read with the

+44 20 7991 5082 disclosures and the analyst certifications in the Disclosure

appendix, and with the Disclaimer, which forms part of it

1. Topics of discussion in the FX market Source: Refinitiv Datastream, HSBC FX *We use a Machine Learning Process to extract key words in Reuters articles

2. Topics of discussion in the FX market excluding Election and Covid Related Themes. Source: Refinitiv Datastream, HSBC FX Research. *We use a Machine Learning Process to extract key words in Reuters articles. Our data range is from 1 January 2020 to 5 November 2020. We scanned nearly 21000 FX articles

3. The US election – now what?

Probability of Republican Senate control has shifted higher Lower volatility in financial markets should boost fund

flows into risky assets

100

Probability (%) 2.5

Cumulative flows (USD trn)

80 2.0

1.5

60 1.0

0.5

40 0.0

-0.5

20 -1.0

-1.5

0 -2.0

Jan-20 Mar-20 May-20 Jul-20 Sep-20 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19 Jan-20

President elect Biden Rep. Senate control Active Equity Funds Passive Equity Funds

Dem. Senate control Dem. Sweep Money Market Funds

Source: Bloomberg, Predictt, EFPR, HSBC4. Biden – policies and China

Clean sweeps usually see greater legislation passed but Implied tariffs on China and USD-CNY;

not always lower tariffs could boost the CNY

Percentage of legislation enacted by party

9% in the White House 7.60

Shaded areas

8% mark clean 7.40

7% sweep 7.20

6% 7.00

5% 6.80

4% 6.60

3% 6.40

2% 6.20

1% Apr-18 Oct-18 Apr-19 Oct-19 Apr-20 Oct-20

USD-CNY reference rate

0% USD-CNY spot

1978 1982 1986 1990 1994 1998 2002 2006 2010 2014 2018 Upper limit for USD-CNY spot

Carter Reagan Bush Snr. Clinton Bush Obama Trump Theoretical USD-CNY values (based only on tariffs)

Source: Predictit.org, Bloomberg, HSBC5. US-China tensions to persist

Number of China-related legislative proposals and resolutions introduced into US Congress

300 House Senate ytd by mid-Aug

250

200

150

100

50

0

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

…annualized from mid-August, 2020 China legislative proposal on track to rise

30% over 2019

Source: US Congress, HSBC6. The scarring from Covid & the recovery

Economic scarring set to be less evident in low debt countries and the US

2020 2021

110 110

GDP level, 2019 = 100

106 106

102 102

98 98

94 94

90 90

86 86

UK SP SA IT FR IN EZ JN BR GE CA US SW NZ AU NO CHF TU SK TA CH

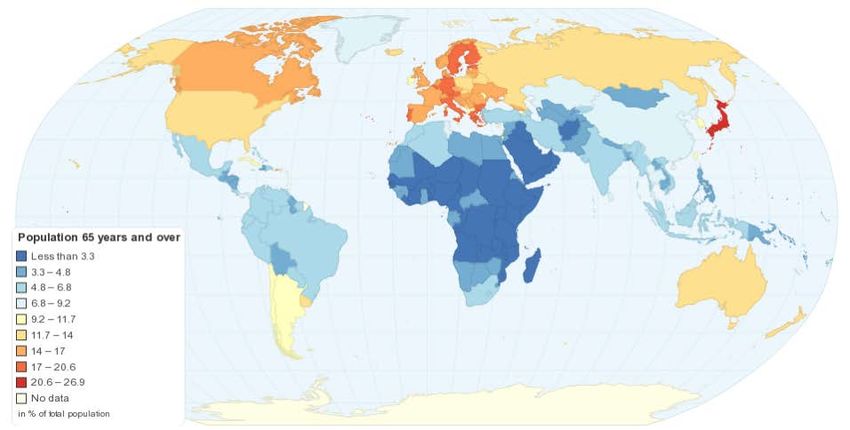

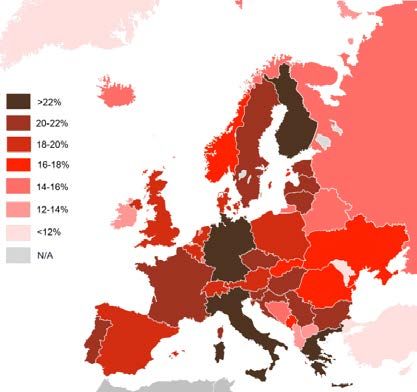

Source: Bloomberg, HSBC7. The Demographic Investment Story

Global look at populations > 65 years A closer look at Europe

Sources: http://chartsbin.com/view/1239

https://en.wikipedia.org/wiki/Ageing_of_Europe8. The EUR is in focus too

ECB references to the exchange rate have been rising lately

Source: Bloomberg, HSBCChina & the RMB

9. China’s economic recovery is broadening

China’s recovery is broadening from production China’s import demand is also broadening from

to consumption tech-led to include other products

25% % y/y

30% China imports, % y/y, 3mma

20%

15%

20%

10%

5% 10%

0%

-5% 0%

-10%

-15% -10%

-20%

-25% -20%

08 09 10 11 12 13 14 15 16 17 18 19 20 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19 Jan-20

Credit impulse IP Retail sales Tech imports Other non-oil imports

Source: Bloomberg, HSBC Source: CEIC, HSBC10. RMB – a strong current account position

China’s trade surplus is very wide Strong exports to ‘G3’

250 USD bn USD bn

250

200 200

150 150

100 100

50

50

0

0

-50

-50 -100

-100 -150

07 08 09 10 11 12 13 14 15 16 17 18 19 20 07 08 09 10 11 12 13 14 15 16 17 18 19 20

Oil and Gas Technology G3 China+HK Asia-ex-China

Non-oil, non-tech Trade balance

ROW Trade balance

Source for both charts: CEIC, HSBC11. RMB – More sensitive to portfolio flows

Foreigners’ bond investments have increased due in Net Stock Connect flows

part to index inclusion

30 Foreign bond inflows, USD bn 15 Stock Connect flows, Inflows to China

USD bn

10

25

5

20

0

15

-5

10 -10

5 -15

0 -20 Outflows from China

-5 -25

-10 -30

Jan-15 Mar-16 May-17 Jul-18 Sep-19 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19 Jan-20

Change in Bonds held by foreigners Northbound Southbound Net flows

Source for both charts: CEIC, HSBC12. Chinese corporates & hoarding USDs

Net FX settlement for goods trade purposes in China

USD bn

80

75% conversion ratio pre "trade war" 35% conversion ratio amid "trade war" 42% during

60 'Phase 1'

40

20

0

-20

-40

-60

Jan-17 Apr-17 Jul-17 Oct-17 Jan-18 Apr-18 Jul-18 Oct-18 Jan-19 Apr-19 Jul-19 Oct-19 Jan-20 Apr-20 Jul-20 Oct-20

Net FX sales by corps (trade conversion) Trade balance

Source: CEIC, HSBC13. History of the PBoC’s counter cyclical FX policy tools

Guiding the RMB without direct intervention

110 RMB appreciation 6.1

Jan 2018 first cut

108 RMB depreciation of CCF to neutral 6.2

Sept 2017 6.3

106 first cut of

reserve ratio 6.4

104

to zero August 2018 re- 6.5

102 application of reserve Oct 2020 cut

May 2017 first 6.6

charge + CCF reserve ratio to

100 introduction of CCF 6.7

zero again

Sept 2015 6.8

98 first

introduction 6.9

96

of reserve 7.0

94 charge 7.1

92 7.2

90 7.3

Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18 Jan-19 Jul-19 Jan-20 Jul-20

CFETS RMB Index USD-CNY fix USD-CNY spot (RHS, reverse scale)

Source: Bloomberg, HSBC14. History of CNH and onshore CNY FX points and effective cost of 20%

reserve charge

Reserve charge is adjusted according to FX flow condition

4000 500

pip pip

3000 400

2000 300

1000 200

0 100

-1000 0

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18 Jan-19 Jul-19 Jan-20 Jul-20

USD-CNH 12m forward points USD-CNY 12m forward points Forex reserve charge (RHS)

Source: Bloomberg, HSBC *Note: The red line represents, for example, the additional cost of buying the one-year USD forward onshore with the 20% reserve charge; for instance, the

additional cost on 1y RHS outright forward is currently around 50pip (20%*35*6.70), assuming 1y US libor at 35bp.Asia FX liquidity

15. Top-of-book spreads during Asia hours

USDCNH USDHKD USDSGD USDTHB

5 5

Weekly median primary* top-of-book spreads during Asia hours

4 4

Spread (bps)

3 3

2 2

1 1

0 0

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20

Source: HSBC,

* EBS for USDCNH and Reuters for USDHKD, USDSGD and USDTHB16. Traded volume

USDCNH USDHKD USDTHB USDSGD

70,000 70,000

Weekly total traded volume* (millions of USD) during

60,000 Asian Hours 60,000

50,000 50,000

40,000 40,000

30,000 30,000

20,000 20,000

10,000 10,000

0 0

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20

Source: HSBC

*On EBS, Reuters, Hotspot, Currenex, LMAX, ParFX, Gain GTX and FXall17. Intraday traded FX volume

USDCNH USDHKD USDSGD USDTHB

2,500 2500

Average intraday traded volume* profiles between 2020.01.06 and 2020.11.06

2,000 2000

Volume ($M)

1,500 1500

1,000 1000

500 500

0 0

10:00

11:00

12:00

13:00

14:00

15:00

16:00

17:00

18:00

19:00

20:00

21:00

22:00

23:00

0:00

1:00

2:00

3:00

4:00

5:00

6:00

7:00

8:00

9:00

Source:

*On EBS, Reuters, Hotspot, Currenex, LMAX, ParFX, Gain GTX and FXallDISCLAIMER

The information contained in this material is intended for the sole use of the recipient and is not for general distribution. The author is a member of the sales and trading department

and not of the research department of HSBC Bank plc and/or HSBC UK Bank plc. The sales and trading department of HSBC Bank plc and/or HSBC UK Bank plc is engaged in

selling and trading in securities to which this material relates or is relevant. Accordingly, recipients of this should not regard it as an objective or independent explanation of the

matters contained in it. This has not been prepared in accordance with regulatory requirements designed to promote the independence of investment research. Any information

contained in this is not and should not be regarded as investment research for the purposes of the rules of the FCA. Any recommendations in this material are based on the individual

opinions of the sender and may be changed at any time without notice. Opinions expressed may differ from the opinions expressed by other divisions of HSBC Bank plc and/or HSBC

UK Bank plc, including its research department.

HSBC Bank plc

Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority

Registered in England No. 14259

Registered Office: 8 Canada Square, London, E14 5HQ, United Kingdom

Member HSBC GroupYou can also read