Fashion & Luxury Private Equity and Investors Survey 2018 - Global report - Deloitte

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Fashion & Luxury Private Equity and Investors Survey 2018 Global report

Contents Preface and methodology 4 Key takeaways 7 M&A Deal Monitor 2017 9 Private Equity and Investors Survey 2018 17 Glossary and contacts 37

Fashion & Luxury Private Equity and Investors Survey 2018 | Preface and methodology Preface 2017 oversaw a global economic growth mainly driven by emerging markets. Nonetheless, there is a substantial amount of uncertainty mainly driven by a globalisation slowdown, a rise of populism in developed nations and prominent geo-political instabilities affecting the global scenario. The 2018 unstable global trading environments, however, provide a major challenge for Fashion & Luxury players, which could be reviewing their pricing strategies against significant fluctuation in exchange rates. In such a context, rising global political tensions, taxation reforms and new trade policies are expected to deeply influence the industry. The repercussions of this changing global landscape, along with the increasing presence of disruptive technologies and the digitalisation of the business and luxury worlds, are now setting the bases for changes in the industry market trends, thereby affecting its key players and their business models. In order to analyse and measure market trends and expectations on M&A activities, Deloitte has launched the third edition of the “Global Fashion & Luxury Private Equity and Investors Survey”. 4

Fashion & Luxury Private Equity and Investors Survey 2018 | Preface and methodology

Methodology and contents

The study considers ten sectors of the F&L industry, of which three are Personal Luxury Goods.

M&A Deal Monitor 2017 Private Equity and Sectors covered Market segmentation

Investors Survey 2018

Personal Luxury Goods

Price point analysis

Consumers’ perception

• Size of M&A deals by F&L • F&L market outlook

Contents

sector • Exit and investment

• Target company profiles strategies in 2018

• Investor profiles • Investors’ current Absolute

• Analysis of global deals portfolio of F&L assets

Absolute

scope

Apparel & Cosmetics & Watches &

Geo

Global Global Accessories Fragrances Jewellery Aspirational

• News and reports

Primary

• Online survey based

Primary Aspirational

from major media

Data source

data level on Computer Assisted data level

providers Web Interviewing

• Investor press (CAWI)

releases • Interviews with Private Accessible

• Company press Equity funds top

releases management

Furniture Private Jets Yachts Luxury Cars

• The study has been conducted with the support of Deloitte offices in: China,

Remarks

France, Germany, Hong Kong, Italy, Luxembourg, Singapore, Spain, Switzerland,

United Kingdom, United States.

The survey targeted senior members within investment funds, with a Fashion

•

substantial knowledge of the F&L industry. Fashion

Full secondary data Full primary data Luxury Hotels Luxury Cruises Digital Luxury

5

Fashion & Luxury Private Equity and Investors Survey 2018 | Key takeaways

Key takeaways

M&A Deal Monitor 2017

2017 Global M&A deal overview Top deals in 2017 M&A features and strategies

The Fashion & Luxury industry proved to be fertile Acquisitions of Apparel & Accessories drove numbers Of the M&A deals completed, 47 per cent were carried

soil for M&A activities with 217 deals registered in in 2017: out by strategic investors, a decrease of 43 deals

2017, presenting an increase of 6 deals compared • LVMH gained control of Christian Dior through its compared to 2016. Financial investors, on the other

to the previous year. Personal Luxury Goods deals acquisition by Bernard Arnault (~13.7B$ for 26 per cent). hand, carried out more deals compared to 2016 (+44

have increased (+5 deals versus 2016) with Apparel deals).

• Belle International by Hillhouse Capital Group (~4.7B$

& Accessories (36 per cent of total), and Cosmetics &

for 100 per cent). Strategic sellers were involved in 64 per cent of

Fragrances (13 per cent of total) increasing by 8 and 6

• Kate Spade & Co by Coach Inc (~2.4B$ for 100 per transactions (-13 percentage points versus 2016).

deals respectively. Watches & Jewellery (13 per cent of

cent). Generally, bidders’ investments focused on a buyout

total) was the only PLG presenting a decrease of 9 deals

strategy (+55 deals versus 2016).

compared to the previous year. M&A deals volumes • Jimmy Choo by Jag Acquisitions for (~1.2 B$ for 100 per

in other sectors increased, with activity in Furniture cent).

(+6 deals) and Cars (+2 deals) growing compared to

Other relevant acquisitions in 2017 involved Cosmetics

the previous year. The average deal value has shown

& Fragrances and Hotel companies:

a relevant downsize, from $449M to $230M in 2017

• Carver Korea Co by Unilever (~2.4B$ for 95 per cent).

(-49 per cent), nonetheless presenting an increase in

achieved multiples. • The Body Shop International by Natura Brasil (~1.1B$

for 100 per cent).

M&A deals in Europe strongly increased (+14 deals),

• Playa Hotels & Resorts by Pace Holdings (~1.8B$ for

while North America and Asia-Pacific remained flat.

100 per cent).

Luxury hotel deals were present in all major regions

• Hilton Garden Inn by Pandox AB (~1.0B$ for 100 per

except for Japan and the Middle East and were notable

cent).

drivers of M&A globally in 2017.

7Fashion & Luxury Private Equity and Investors Survey 2018 | Key takeaways

Private Equity and Investors Survey 2018

Fashion & Luxury market outlook Investors’ positive consensus regarding 2018 investment strategy Luxury), newcomers prefer consolidated

both Asia and the Middle East has sectors within the F&L industry (e.g.

Within its Private Equity Survey, Deloitte During 2017, 89 per cent of funds are

continued in 2017 as the forecast Cosmetics & Fragrances) where market

focused on understanding investors’ considering investing in a F&L asset,

continues to see these sectors knowledge is widespread.

perceptions of the potential growth in with notable interest rising in: Apparel &

stimulating the growth of the F&L

the F&L market in coming years. The Accessories (where 73 per cent intend to With respect to 2017, the continuous

industry. Expectations for North America

consensus view is that major players invest), Cosmetics & Fragrances (60 per consolidation of the F&L industry is

are positive (5-10 per cent annual

in Personal Luxury Goods (PLG) are cent), Furniture (45 per cent), Watches & moving investments towards smaller-

growth), but sentiment has decreased

projected to achieve 1.2 times their 2016 Jewellery (19 per cent) and Digital Luxury sized companies (+10 percentage

compared to 2017. Latin America

sales index by 2020 (~ +3 per cent CAGR (16 per cent), Selective Retailing (10 per points), where investors plan to

will remain stable. Finally, sentiment

FY 2016-20), while other luxury sectors cent). boost performance by implementing

regarding Japan beat expectations

are expected to achieve 1.3 times their internationalisation, performance

compared to the previous year, with Even though interest is declining

value (~ +4 per cent CAGR FY 2016-20). improvement and change management

investors foreseeing a consolidated compared to the previous year, Watches

strategies.

Within the next three years, investors growth (5-10 per cent). & Jewellery and Digital Luxury remain

forecast that the F&L industry will remarkably attractive to investors. The consensus is that forecasted returns

continue to grow by 5-10 per cent Virtualization trends in the consumer will range from 21 to 30 per cent, with

2018 exit strategy

annually. Digital Luxury and Cosmetics purchasing process are leading to Cosmetics & Fragrances and Furniture

& Fragrances are projected to The report considers potential strategies the creation of a new cluster of firms representing the top performers (>30

outperform strongly, growing by more investors will undertake in 2018 to focusing on Digital Luxury, mostly within per cent); EMEA investors expect higher

than 10 per cent per year. Apparel & enhance or disinvest their Fashion & the Cosmetics & Fragrances segment. internal rates of return (IRR) compared to

Accessories, Watches & Jewellery, Luxury portfolios. About 35 per cent of the US and China.

Despite a slowdown in the Asian market,

Hotels and Furniture are consolidating funds are considering divesting an F&L

investors’ attraction to Watches & According to respondents in 2017, 63 per

(with expected annual growth of 5-10 per asset in 2018, a slight decrease from the

Jewellery remains stable due to their cent will invest in disruptive technologies

cent), while Private Jets are projected previous year (-2 percentage points).

appeal as less volatile assets. in order to benefit from potential

to remain stable (0-5 per cent annual Generally, an investor’s exit is motivated

synergies. The Internet of Things and

growth). A decrease in Cars, Yachts and by an opportunity for high returns, the While current investors, mainly in the

Artificial intelligence will have the largest

Selective Retailing is expected. closing of the investment period, market EMEA area, are more attracted to

impact on investors’ portfolios.

trends mismatches or concerns related innovative segments (such as Digital

to the shrinking of multiples.

8Fashion & Luxury Private Equity and Investors Survey 2018 | M&A Deal Monitor 2017

M&A Deal Monitor 2017

Fashion & Luxury M&A deals

Overview of deals in 2017 by sector

211 217 +6 Top luxury deals of 2017

Value

Deals in 2016 Deals in 2017 Deals

Month Target Bidder ($m)

Sector Personal Luxury Goods 2016 2017 Growth Arnault

Jun. Christian Dior 13,673

Family

Apparel & Accessories

69 77 +8

Jul.

Belle

International

Hillhouse 4,745

Hotels

53 46 -7 Nov. Carver Korea Unilever 2,420

38 29

Kate Spade

Watches & Jewellery -9 Jul. Coach Inc. 2,380

& Co

Playa Hotels Pace

22 28

Mar. 1,863

+6 & Resorts Holdings

Cosmetics & Fragrances

Jag

Nov. Jimmy Choo 1,167

Acquisitions

Furniture

11 17 +6

Sep. The Body Shop

Natura (Brazil)

International

1,130

Private Jets

10 10 - Dec.

Hilton Garden

Hinn

Pandox AB 1,026

7 7

Sinoer Men’s Gunaghzou

Yachts - Jul. 973

Wear Cedar

Schustermann Permira

0 2

Jan. 761

& Borenstein Advisers

Cars +2

Grosvenor

Jun. GH Equity UK 740

1 1

House Hotel

Cruises -

Note: the analysis considers both closed and announced deals during 2017 | Source: Elaboration on Deloitte intelligence data

9Fashion & Luxury Private Equity and Investors Survey 2018 | M&A Deal Monitor 2017

M&A deals by region and sector

Overview of deals in 2017 by region

(number of deals)

Europe North America Key findings

+14 81 95 109 - 35 59 59 - 14 36 36

11 8 3 Europe was the only region which saw an

15 18 6 2 6

18 4 increase in Fashion & Luxury deals in

5 14 10

10 6 4

5 15 16 10 5 10 2 2017, with 14 more deals.

4 10

19 21 8 12 North America and Asia-Pacific presented

24

16 11 the same amount of deals as the previous

15 9

38 47 7 year.

27 15 14 12

4 8

Luxury hotel deals were present in all

2015 2016 2017 major regions except for Japan and the

2015 2016 2017 2015 2016 2017

Middle East and were notable drivers of

M&A globally in 2017.

Japan Middle East Rest of World Japan presented a slight decrease in F&L

-4 6 8 4 -2 2 5 3 -2 3 8 6

deals since 2016 with 75 per cent of its

1 1 deals driven by Watches & Jewellery.

1

2 1 1

1 2 1 Although deals in Fashion and Luxury in the

3 5 Middle East decreased, the region saw an

2 1 4 increase in deals relative to the Apparel &

5 2 2 Accessories sector.

1 2

2 3

1 1

2015 2016 2017 2015 2016 2017 2015 2016 2017

Cosmetics & Fragrances Hotels Other Private Jets

Watches & Jewellery Apparel & Accessories Yachts # Variance 2016-17

Source: Elaboration on Deloitte intelligence data

10Fashion & Luxury Private Equity and Investors Survey 2018 | M&A Deal Monitor 2017

Size of main M&A deals

The F&L soil has been fertile with 217 M&A deals in 2017, showing a 2.8 per cent increase from 2016. Personal Luxury Goods

(+3.8 per cent YoY) represent 62 per cent of all deals.

Number of deals in 2017 - Breakdown by sector

(number of deals, percentage)

7 2 1 217 Key findings

10

PLG YoY 2016 -17 +5 17

83

Other Watches & Jewellery

luxury

( 38%) registered 9 deals less

markets

46

compared to 2016.

Apparel & Accessories and

28

Cosmetics & Fragrances

29 deals increased by 8 and 6

Personal deals respectively.

134

Luxury

( 62%) Furniture, and Cars have

Goods

77 become more attractive to

investors during 2017.

Apparel & Watches Cosmetics & Hotels Furniture Private Jets Yachts Cars Cruises Total Fashion

Accessories & Jewellery Fragrances & Luxury

Sector

breakdown 35.5% 13.4% 12.9% 21.2% 7.8% 4.6% 3.2% 0.9% 0.5% 100%

Var. #

deals +8 -9 +6 -7 +6 - - +2 - +6

2016-17

Source: Elaboration on Deloitte intelligence data

11Fashion & Luxury Private Equity and Investors Survey 2018 | M&A Deal Monitor 2017

Average value of main deals by sector

Deals related to the Cosmetics & Fragrances industry were the largest in 2017 with an average value of $390m.

The average deal value of PLG’s in 2017 was $293m.

Average value per deal in 2017 – Breakdown by sector

($m, percentage)

697

Personal Luxury Goods Other luxury sectors F&L average Key findings

The deal value of Christian Dior’s

acquisition by LVMH is not

considered in the perimeter

of the analysis Hotels and Watches & Jewellery

341 saw the average deal value fall in

2017.

Apparel & Accessories, Cosmetics

390 & Fragrances, Furniture, Yachts

and Private Jets recorded increases

(+9 per cent, +26 per cent, +102 per

Avg. PLG

$293m cent, +513 per cent and +64 per

230

cent respectively).

163

356 133 119

62

55 44

N/A

Apparel & Cosmetics F&L Hotels Watches Furniture Cars Yachts Private Jets Cruises

Accessories & Fragrances Average & Jewellery

513%

102%

64%

9% 26% N/A N/A

YoY 2016/17

(%)

-49% -37%

-80%

Notes: The average deal value has been calculated based upon data of disclosed transactions | Source: Elaboration on Deloitte intelligence data

12Fashion & Luxury Private Equity and Investors Survey 2018 | M&A Deal Monitor 2017

Target company features

Compared to the previous year, funds increased the number of deals related to smaller sized firms, delivering on

average higher multiples (41 per cent of deals with a >15x EV/EBITDA multiple). The increase in acquisitions of smaller

firms positively correlates with a higher average multiplier, showing how the F&L industry can be profitable even for

mid-sized investors.

Target company features - Sales class and multiples

(percentage, enterprise value - EV/EBITDA multiples)

Key findings

TARGET COMPANIES SALES CLASS CAGR Deal EV/EBITDA multiple CAGR

15-17 15-17 In 2017, investors were mostly oriented

100% 100% 100% 100% 100% 100% towards lower-sized firms ($0-$50m)

which accounted for 55 per cent of deals

Big Size

21% 16% (> $250m) -13% in the year, compared to 40 per cent in

28% % 2016.

42% 37% 41% > 15x -1%

There was a marked decrease in deals

Medium Size

29% -1% involving players of sizes larger than

($51-$250m)

30% $250m (-13 per cent CAGR 2015-17).

32% % Deals involving multiples superior to 15

34% times EBITDA increased, while there was

31% 31% 11 - 15x - a decline in deals positioned on EBITDA

multiples of 11–15 times.

Small size

55% +5%

49% ($0-$50 m)

40% % 20%

19% 17% 5 - 10x -5%

8% 9% 10% < 5x +16%

2015 2016 2017 2015 2016 2017

Notes: The target sales class has been calculated for all companies with financial data which is publicly available | Source: Elaboration on Deloitte intelligence data

13Fashion & Luxury Private Equity and Investors Survey 2018 | M&A Deal Monitor 2017

Investor profiles

Financial investors were 53 per cent of total bidders with Private Equity/Venture Capital representing 55 per cent of

them. 45 per cent of Strategic investors were involved in an Apparel & Accessories or Hotels related deal in 2017.

Main bidders’ profile

(percentage, number of deals)

Key findings

Financial investors +44 -43 Strategic investors Change in

number of Deals conducted by strategic investors,

100% 100% deals YoY

2016-17 mainly operating in the Apparel &

+24 Other Accessories, Hotels and Cosmetics &

26% 23% industries +6

O ther investors Fragrances sectors, represent 58 per

Yachts -1 cent of total deals. Nonetheless, there

4%

4% Furniture -3

+18 Watches was a notable decrease in deals driven

Financial Services 19% 10% -3

& Jewellery by strategic investors compared to the

47% 13% Cosmetics -13 previous year (-43 deals).

53% & Fragrances

There was a relevant increase in deals

Apparel conducted by financial investors (+44

+2 21%

& Accessories

-15

Private Equity/ 55% deals compared to 2016).

Venture Capital

24% Hotels -14

Breakdown by Breakdown by investor

investor type core industry

Source: Elaboration on Deloitte intelligence data

14Fashion & Luxury Private Equity and Investors Survey 2018 | M&A Deal Monitor 2017

Portfolio exit strategies

In 2017 there has been an increase in financial sellers (36 per cent vs 23 per cent of 2016), with the majority of

acquisitions carried out through buyouts (+55 YoY 2016-17).

Exit types vs investment strategies

(percentage, number of deals)

Exit types patterns Investment strategy by bidder type YoY 2016-17

Key findings

(deals)

100% 100% 100% 100% 100% 1% 100% Other -24

3% 2% 2% Turnarounds There was a slight decrease in M&A

Sponsor 7% 4% 3% -41

13% operations carried out by "strategic"

to sponsor 3% 10% 6% Consolidations -10

25% sellers in 2017 (64 per cent). In 2016 77

16% 10% 10% Acquisition

Financial 9% -9

Sponsor capital per cent of investors were "strategic".

20% Seller

to strategic

11% 36% 29%

19% 24%

Growth

capital

+1

Furthermore, the exit patterns of

25% financial investors increased from 23 per

cent in 2016 to 36 per cent in 2017.

Strategic

to sponsor

38% There was a strong growth in

39%

investments through a buyout (+55

Strategic deals). Strategic turnaround oriented

Seller 59%

52% 51% 54% Buyouts +55 deals, decreased sharply.

Strategic

64%

29% 25%

to strategic

2015 2016 2017 Financial Strategic Total

investor investor

Notes: The deal strategy analysis has been performed based upon data of disclosed transactions | Source: Elaboration on Deloitte intelligence data

15Fashion & Luxury Private Equity and Investors Survey 2018 | M&A Deal Monitor 2017

Bidders’ investment stake

Deals in the Personal Luxury Goods segments decreased by 11 percentage points, up front a general

reduction of majority stake deals, which account on average for 66 per cent of M&A activities in the F&L

sector.

Investment stakes by sector

(percentage)

76 28 25 17 11 9 7 1 1 175

21% 18% 18% 14%

34% Minority

36% 33%

45%

100% 100%

79% 82% 82% 86%

67% 66% Majority

64%

55%

Apparel & Watches Cosmetics & Furniture Hotels Private Jets Yachts Cruises Cars Total F&L

Accessories & Jewellery Fragrances

PERSONAL LUXURY GOODS OTHER LUXURY SECTORS

62% Majority 76% Majority

-11% pts Decrease -1 % pts Decrease

Notes: Undisclosed investment stakes deals have been excluded from the analysis | Source: Elaboration on Deloitte intelligence data

16Fashion & Luxury Private Equity and Investors Survey 2018 | Private Equity and Investors Survey 2018

Private Equity and Investors Survey 2018

Fashion & Luxury market outlook

Market outlook: FY2017-20 F&L sales index outlook

(index on sales 2010=100)

rising sales forecast Index

280

PLG idx growth: 1.2x

Investors expect PLG top players to achieve 1.2 260

Other lux idx growth: 1.3x

times the 2016 sales index by 2020, (~ 3 per cent

240

16-20 CAGR). Other luxury sectors are expected to 230

be at 1.3 times the 2016 value (~ 4 per cent 16-20 220 216

CAGR). 200

180 177

180

CAGR

160 2016-20F

140 Personal

Luxury Goods

~2.7%

120 Other luxury

sectors ~3.6%

100 Forecast

80

2010 2011 2012 2013 2014 2015 2016 2017 2020F

Notes: Values reported at constant exchange rates | Source: Elaboration on Company Financial Report data and Deloitte survey

17Fashion & Luxury Private Equity and Investors Survey 2018 | Private Equity and Investors Survey 2018

Market outlook: trend by F&L sector

In the next three years investors expect a sound growth in the Cosmetics & Fragrances and Digital Luxury

industries, confirming last years trend. A solid, but limited growth is also expected in the Apparel &

Accessories, Watches & Jewellery, Hotels and Furniture industries, while investors forecast Cars, Yachts and

Retailing as shrinking.

Expected F&L market trends for the next 3 years – Breakdown by sector

(index on responses)

Key findings

Strong Private Equity funds expect the F&L industry to grow by

Increase around 5-10 per cent annually in the next three years,

(>10% per

year) confirming last year’s sentiment.

The main sectors that will drive this growth are

Cosmetics & Fragrances and Digital Luxury, with growth

Increase

(5-10% per rates higher than 10 per cent and a continuously

year) improving sentiment. A slower trend is predicted for

Apparel & Accessories, Watches & Jewellery, Hotels

Stable

and Furniture (between 5-10 per cent annually), while

Decrease Private Jets will remain stable.

(< 0% per App&Acc Wat&Jew Cos&Fra Cars Hotels Yachts Private Furniture Retailing Digital Total

year) Jets Luxury F&L Forecasts are less favourable for Cars, Yachts and

Selective Retailing, where the growth rates might be

Personal Luxury Goods Other luxury sectors

negative and Private Equity sentiment is weakening

2017-18 change markedly.

in sentiment

Source: Elaboration on Deloitte survey

18Fashion & Luxury Private Equity and Investors Survey 2018 | Private Equity and Investors Survey 2018

Market outlook: trend by geographical area

Investors expect the Asian and the Middle Eastern areas to stimulate growth of the F&L industry, also

affecting the expectations on Japan, which has notably increased since the previous year. Latin America is

expected to consolidate even though sentiment has improved.

Expected F&L market trends for the next 3 years – Breakdown by region

(index on responses)

Key findings

Strong

increase

(> 10%

per year) Asia and the Middle East Fashion and Luxury markets

will drive the industry’s growth in the coming three

Increase years, with growth rates which might exceed 10 per

(5-10%

per year)

cent on an annual base.

Latin America is expected to consolidate even though

Stable

investor sentiment has seen a slight improve since the

Decrease previous year.

(< 0%

per year) Sentiment towards Japan has notably improved with

Europe North Latin Japan Asia Middle Rest of Total positive trends expected for the next 3 years.

America America East the world F&L

2017-18

change in

sentiment

Source: Elaboration on Deloitte survey

19Fashion & Luxury Private Equity and Investors Survey 2018 | Private Equity and Investors Survey 2018

2018 Exit and Investment Strategy

Funds’ F&L exit strategy for 2018

Funds considering divesting an F&L asset in 2018 are decreasing in number. The main drivers of exit are the

prospect of high returns, closing of the investment period and market trend mismatches, which are affecting

smaller multiples expected by investors.

Funds that are going to divest at least one asset in 2018

(percentage of respondents)

Key findings

-2%

pts 35 per cent of funds participating in the

35% survey project at least one disinvestment

within their F&L portfolio, a slight decrease

compared to the results of the survey

Exit drivers Exit strategies Exit multiple carried out last year (-2 percentage points).

(percentage of respondents) (percentage of respondents) (percentage of respondents)

The main drivers that will influence exits

100% 100% 100%

Other drivers

100% 100% 100% 100% 100% 100% will be: High Returns Opportunities (35 per

11% 6%

13% Other

18% Closing of the 20% cent), Market trends mismatches (35 per

24% investment 38% > 10x

26% 19% Second 44% (EV/EBITDA) cent) and Closing of the investment period

period 55%

29% 20% buyout

11%

Market trends

8% 19%

73% (24 per cent).

35% mismatch IPO

12% expectations In 50 per cent of cases, the exit will be

54% 60% Trade 56%

< 10x completed through operations of trade

52% High returns 50% 45% (EV/EBITDA)

41% 35% sale

sales, in which 44 per cent of investors will

opportunity 27%

pay an EBITDA multiple higher than 10x,

2016 2017 2018 2016 2017 2018 2016 2017 2018 a strong decrease compared to 2017’s

expectations when 55 per cent expected

multiples greater than 10x.

Source: Elaboration on Deloitte survey

20Fashion & Luxury Private Equity and Investors Survey 2018 | Preface and methodology

Expected new investments in 2018

Personal Luxury Goods remain the most attractive sectors for investors, with Apparel & Accessories and Cosmetics &

Fragrances becoming even more prominent. The relevant trend of Digital Luxury is stabilising.

100%

11% No

Most attractive sectors for investors Change in 2017-18

(percentage of respondents) (percentage points) Key findings

A pparel &

73% 5

Accessories The sectors considered to be most

Cosmetics & attractive based on survey respondents

60% 11

89 % Fragrances are: Apparel & Accessories (73 per cent),

of PE Yes Cosmetics & Fragrances (60 per cent),

Furniture 45% 18

funds Furniture (45 per cent) and Watches &

Watches Jewellery (19 per cent).

& Jewellery 19% -2

Interest in Watches & Jewellery is

Digital however slightly declining compared to

Luxury 16% -1

the 2017, with 2 percentage points less.

Selective Digital Luxury attracted 16 per cent of

Retailing 10% -21

Will your fund investors.

acquire an F&L Personal Luxury Goods Other F&L sectors

asset in 2018?

Source: Elaboration on Deloitte survey

21Fashion & Luxury Private Equity and Investors Survey 2018 | Private Equity and Investors Survey 2018

F&L sector attractiveness

Both Apparel & Accessories and Cosmetics & Fragrances are remarkably attractive to

investors. Furniture has shown a notable increase since 2017, becoming a star sector for

potential investment in the coming year.

Map of investor attraction in F&L sectors

25

Key findings

20

Virtualization trends in the consumer purchasing process are

15 Furniture leading to the creation of a new cluster of firms focusing on

Digital Luxury, mainly in the Cosmetics & Fragrances sector.

10 Cosmetics

& Fragrances The attraction towards the Watches & Jewellery and Digital

luxury sectors remains stable. Investors are attracted to less

Change in 2017-18

5

(percentage points)

Apparel volatile assets.

& Accessories

0 The appeal of Apparel & Accessories has fallen, yet the sector

Digital Watches remains the primary choice for investors, attracted by higher

-5

& Jewellery margin performances.

-10

-15

Personal Luxury Goods

Selective

-20 Other General investor propensity

Retailing

-25

0 10 % 20 % 30 % 40 % 50 % 60% 70% 80%

Investment propensity 2018

(percentage of respondents)

Source: Elaboration on Deloitte survey

22Fashion & Luxury Private Equity and Investors Survey 2018 | Private Equity and Investors Survey 2018

Sector attractiveness: current vs potential investors

While current investors are more attracted to diversify their investments towards innovative

segments such as Digital Luxury, newcomers prefer to invest in more traditional and

established F&L sectors.

Map of investor attraction in F&L sectors – Current vs potential investors

100 %

Attractive sectors for Key findings

90 % new investors

80 % Apparel As the most established sector, Apparel & Accessories remains

& Accessories the main target for all investors.

New F&L investors’ propensity

70 %

Funds with higher specialization in the industry tend to be more

Cosmetics

(percentage of respondents)

60 % & Fragrances attracted to innovative sectors such as Digital Luxury.

New potential investors focus on more traditional sectors such

50 % as Apparel & Accessories and Cosmetics & Fragrances.

Furniture has become an extremely attractive sector for

40 %

potential investors in 2018.

Furniture

30 %

Selective

Retailing

20 %

Watches

10 % & Jewellery

Attractive sectors for Personal Luxury Goods

0% Digital

current investors General investor propensity

-10 %

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Current F&L investors’ propensity

(percentage of respondents)

Source: Elaboration on Deloitte survey

23Fashion & Luxury Private Equity and Investors Survey 2018 | Private Equity and Investors Survey 2018

Growth strategies for the F&L portfolio

Performance improvement and change management are becoming important drivers of F&L portfolios

growth strategies, combined with Internationalisation that is less accounted for as a strategy.

Main adopted strategic drivers for the F&L portfolio

(percentage of respondents)

44% Key findings

41%

38%

Internationalisation is now the main strategic lever (44 per

cent) adopted by F&L investors to grow their asset value.

89%

25% Even though it’s adoption has weakened since the previous

22% year, investors still see Digital Strategy Design (16 per

cent) as a relevant topic for F&L companies seeking faster

16%

growth.

Frequently, funds acquire underperforming companies,

aiming to bring sales growth and margins up to the average

sector performance.

International. Performance Change New distribution New production Digital strategy

improvement management channel development design

Change

in % points -23 +16 +19 -5 -2 -6

2017-18

Source: Elaboration on Deloitte survey

24Fashion & Luxury Private Equity and Investors Survey 2018 | Private Equity and Investors Survey 2018

Size of potential investment in F&L

The F&L industry is polarizing on investors looking to acquire small sized firms and industry giants,

through the acquisition of minority stakes.

Average sales of potential target companies

(percentage of respondents)

Key findings

100% 100% 100% 100% 100% 100% 100%

Investors are typically attracted to small (52 per cent)

16% 17% 18% 14% 18% +6 and medium-sized (30 per cent) businesses.

21%

89% 26%

Investments in 2017 oriented towards larger

21% companies has remained stable due to the continuous

9% 25% 30% -2

33% 35% 43% consolidation of the F&L industry.

Target companies in Apparel & Accessories, Cosmetics

& Fragrances, Watches & Jewellery and Furniture tend

65% 63% to be smaller ( $250m) Medium ($50-$250m) Small (< $50m) Change in 2017-18 (% points)

Source: Elaboration on Deloitte survey

25Fashion & Luxury Private Equity and Investors Survey 2018 | Private Equity and Investors Survey 2018

Main features of the M&A deal

The preferred deal strategies are Leveraged Buyout (LBO), Expansion Capital and Management Buyout (MBO), financed

mostly through senior debt, aimed at acquiring a majority stake in the targeted companies.

Structure of the new F&L investment deals

(percentage of respondents)

Key findings

Deal type Funding Stake

The main deal strategies adopted by

89% investors in 2017 are: LBO/Replacement

100% 100% 100% 100% 100% 100% 100% 100% 100%

(28 per cent), Expansion Capital (26 per

18% 13%

22% Other cent) and Support to the MBO (24 per

32% 30% Other

39% cent).

26% 29% Support

24% to MBO/MB Operations financed through senior

73%

23% Shareholders’ 81% 83% Majority debt have been increasing (47 per cent).

24% 15% loan

Shareholder’s loan has become one of

28% 25% Expansion

26% capital the most used sources.

Most deals focus on acquisitions of

46% 47% Senior debt

44% majority stakes.

33% LBO/

28% 28% Replacement 27%

19% 17% Minority

2016 2017 2018 2016 2017 2018 2016 2017 2018

Source: Elaboration on Deloitte survey

26Fashion & Luxury Private Equity and Investors Survey 2018 | Private Equity and Investors Survey 2018

Return expected from new investments

Investors forecast rates of return from their assets ranging from 21 per cent to 30 per cent, with Selective

Retailing and Apparel & Accessories expected as top performers (>30 per cent).

Internal Rate of Return (IRR) expected from new F&L investments

(percentage of respondents)

Key findings

100% 100% 100% 100% 100% 100%

5% 7%

14% 13% +3%

On average, funds expect an IRR from their investments

20%

89% ranging from 21 per cent to 30 per cent, while 13 per

cent forecast a higher performance (>30 per cent).

60% Lower expected rates of return for Watches & Jewellery

59% 74% 71% 59% -10%

do not play a major role in investors’ strategies, due to

57%

the lower volatility of this segment.

Selective Retailing and Apparel & Accessories are

expected to guarantee investors a higher IRR.

27% 40% 28%

21% 23% 22% +6%

App & Acc Cos & Fra Wat & Jew Retailing Furniture Total F&L

> 30% 21-30% 10-20% Change in 2017-18 (% points)

Source: Elaboration on Deloitte survey

27Fashion & Luxury Private Equity and Investors Survey 2018 | Private Equity and Investors Survey 2018

Return from new investments: small yields more

Respondents confirm the existence of a correlation between a target firm’s size and the expected rate of

return from investment. A return greater than 20 per cent is more likely from mid-sized and small firms, in

line with the investment plans of the surveyed investors.

IRR expected from new F&L investments – Breakdown by target company size

(percentage)

72% 28%

Big company

23% (> $250m)

30%

Target Turnover Size

Medium company

13% 29%

(percentage)

($50-$250m )

57%

48%

Small company

(< $50m)

< 20% > 20%

Expected IRR

(percentage)

Source: Elaboration on Deloitte survey

28Fashion & Luxury Private Equity and Investors Survey 2018 | Private Equity and Investors Survey 2018

Disruptive technologies in Fashion & Luxury

63 per cent of respondents will invest in disruptive technologies in order to benefit from potential synergies.

Internet of Things and Artificial Intelligence will have the largest impact on investors’ portfolios according to

respondents in 2017.

Fund likelihood Impact of disruptive technology based on portfolio type

of Investment (percentage)

in disruptive

technologies firms Key findings

(percentage)

Personal Luxury Goods (PLG)

13% 100%

9% The disruptive technologies considered to be of most

10%

19% impact on portfolios relevant to Personal Luxury

22% Goods are: Internet of Things (27 per cent), Big Data

27% & Analytics (22 per cent), Artificial Intelligence (19 per

cent), Healthtech (10 per cent) and Robotics (9 per

Internet of Big Data & Artificial Health Robotics Other Total PLG

cent) .

37% Things Analytics Intelligence Tech Considering other luxury sectors, the main disruptive

technologies perceived by F&L investors are: Internet

63% of Things (26 per cent), Artificial Intelligence (24 per

Other luxury sectors

10% 100% cent), Big Data & Analytics (22 per cent), Blockchain (11

11%

7% per cent) and Robotics (7 per cent).

22%

24%

Will probably invest 26%

in disruptive technologies

Internet of Artificial Big Data & Blockchain Robotics Other Other luxury

Things Intelligence Analytics sectors

Source: Elaboration on Deloitte survey

29Fashion & Luxury Private Equity and Investors Survey 2018 | Private Equity and Investors Survey 2018

Profile of survey respondents

Funds’ key features Fund strategy 100%

The main strategic 19% Other Fund core industries

approach of the involved

28% Growth

83 per cent of survey participants are medium-large funds is: buyout (53 per The main industries

cent) and growth (28 per represented in investors’

Private Equity Funds. In 22 per cent of cases, they

cent) strategies portfolios are: F&L (23 per

hold a portfolio of net assets greater than $1bn. 53% Buyout cent), Retail & Consumer

(21 per cent), Industrial (19

% of

per cent), and Healthcare

respondents (14 per cent)

Investor type

% of respondents

100%

Other types

Fund net assets 23% Other

17% 14% Healthcare

31 per cent of funds

participating in the 100% 19% Industrial

survey have net assets 83% Retail, Consumer

22% > $1bn 21%

ranging from $100-500m, & Leisure

while 22 per cent have 19% $501m -$1bn 23% Fashion&Luxury

full net assets greater Private Equity Fund

than $1bn 31% $100m - $500m % of

repondents

28% < $100m

% of

respondents

Note: (1) Other investors: Family offices, Luxury Holdings and Sovereign Wealth funds | Source: Elaboration on Deloitte survey

31Fashion & Luxury Private Equity and Investors Survey 2018 | Private Equity and Investors Survey 2018

Profile of survey respondents

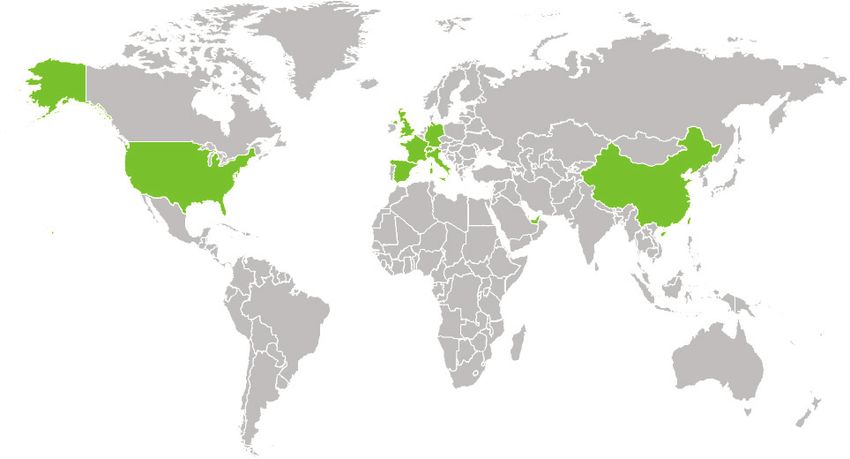

Respondents are senior members of their funds, with an in-depth knowledge of F&L industry.

RESPONDENTS’ LOCATIONS RESPONDENTS’ ROLES

(percentage of respondents)

Other

Director

and/or

Principal 6%

13%

Investment 16%

66%

manager

GLOBAL Managing Director

and/ or Partner

Main countries

Source: Elaboration on Deloitte survey

32Fashion & Luxury Private Equity and Investors Survey 2018 | Private Equity and Investors Survey 2018

Funds’ current F&L portfolio: main sectors

Investors mainly manage assets in Apparel & Accessories (66 per cent) and Cosmetics & Fragrances (28

per cent), Watches & Jewellery (25 per cent), Furniture (25 per cent) and Selective Retailing (16 per cent).

Main F&L assets managed by investors

(percentage of respondents)

66% 78% of investors have a Fashion & Luxury asset in their portfolio

56%

28%

25% 25%

16%

Apparel Cosmetics Watches Furniture Selective Other

& Accessories & Fragrances & Jewellery Retailing F&L sectors 1

Note: (1) “Other F&L Sectors” includes mainly: Digital Luxury (16 per cent), Hotels (16 per cent), Yachts (9 per cent), Cars (6 per cent) | Source: Elaboration on Deloitte survey

33Fashion & Luxury Private Equity and Investors Survey 2018 | Private Equity and Investors Survey 2018

Funds’ current F&L portfolio: structure

77 per cent of current F&L investors focus 25 per cent or less of their overall portfolio on the F&L industry. Investors usually hold

their F&L assets for less than 5 years, mostly with a majority stake (71 per cent).

Portfolio focus in F&L industry Portfolio equity stake and duration

(percentage of respondents) (percentage of respondents)

High focus

(>25% of AuM)

Minority > 5 years

+13

23% Medium focus 29%

(5 - 25% of AuM)

Equity 39%

-14 Duration

54% stake

61%

71%

23%

Low focus

(< 5% of AuM)

Majority < 5 years

+1

Change in 2017-18

(% points)

78% of investors have a Fashion & Luxury asset in their portfolio

Source: Elaboration on Deloitte survey

34Fashion & Luxury Private Equity and Investors Survey 2018 | Private Equity and Investors Survey 2018

Funds’ current F&L portfolio: average asset size

40 per cent of respondents have assets with an average turnover which is less than $50m. Large-sized assets (>$250m)

represent 30 per cent of the average portfolio.

Average turnover of F&L assets in investors’ portfolio

(percentage of respondents)

100%

10%

Large

30% assets

20%

17%

30% Medium

assets

13%

25%

40%

Small

assets

15%

< $25m $25-$50m $51-$100m $101-$250m $251m-$500m $501m-$1B Total F&L

investors

Source: Elaboration on Deloitte survey

35Fashion & Luxury Private Equity and Investors Survey 2018 | Glossary

Glossary

Main terms and abbreviations

Personal Luxury Goods Personal Luxury Goods include the following

sectors: Apparel & Accessories, Cosmetics &

Fragrances and Watches & Jewellery

App&Acc Abbreviation for Apparel & Accessories

AuM Acronym for Assets Under Management

CAGR Acronym for Compound Annual Growth Rate

Cos&Fra Abbreviation for Cosmetics & Fragrances

F&L Abbreviation for Fashion & Luxury

IRR Acronym for Internal Rate of Return

PE Acronym for Private Equity

PLG Acronym for Personal Luxury Goods

RoW Acronym for Rest of the World

Wat&Jew Abbreviation for Watches & Jewellery

37Fashion & Luxury Private Equity and Investors Survey 2018 | Glossary

Contacts

Deloitte Fashion & Luxury Leaders Deloitte Financial Advisory & Corporate Finance contacts

EMEA Fashion & Spain EMEA Corporate Italy Switzerland

Luxury Leader Juan José Peso Finance Consumer Elio Milantoni Stephan Bruecher

Patrizia Arienti Jpeso@deloitte.es Business Leader emilantoni@deloitte.it sbruecher@deloitte.ch

parienti@deloitte.it Elio Milantoni Tommaso Nastasi Howard Da Silva

Switzerland emilantoni@deloitte.it tnastasi@deloitte.it hdasilva@deloitte.ch

France Karine Szegedi

Benedicte Sabadie kszegedi@deloitte.ch China Japan UK

bsabadiefaure@deloitte.fr Ivan Man Kit Wong Satoshi Yokota Phillip Lane

Turkey ivawong@deloitte.com.hk satoshi.yokota@tohmatsu.co.jp plane@deloitte.co.uk

Germany Hakan Gol Ryukichi Sakuta Richard Lloyd-Owen

Philip Beil hgol@deloitte.com France rysakuta@deloitte.co.uk rlloydowen@deloitte.co.uk

pbeil@deloitte.de Claire Deguerry

UK cdeguerry@deloitte.fr Singapore USA

Italy Sundeep Khanna Lucile Regnault Jiak See Ng Lorin DeMordaunt

sundeepkhanna@deloitte.co.uk lregnault@deloitte.fr jsng@deloitte.com ldemordaunt@deloitte.com

Patrizia Arienti

parienti@deloitte.it

Germany Spain

Alexander Bielig Tomas De Heredia

abielig@deloitte.de tdeheredia@deloitte.es

Karsten Hollasch

Khollasch@deloitte.de

38This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this communication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this communication. Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms. © 2018 Deloitte Italy S.p.A. Graphic Department - Italy | SG.065.18

You can also read