FINANCIAL APPRAISAL - community-led housing london

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

FINANCIAL

APPRAISAL

MARCH 2020

CONTENTS

WHAT IS A FINANCIAL APPRAISAL? ................................................... 4

GROSS DEVELOPMENT VALUE ........................................................... 6

schedule of accommodation ................................................................................................................ 6

Rents and Sales Values ......................................................................................................................... 6

Affordable Housing ................................................................................................................................ 6

Transaction costs .................................................................................................................................. 7

COSTS ........................................................................................... 8

Site investigation costs.......................................................................................................................... 8

Construction costs ................................................................................................................................. 8

Contingency ............................................................................................................................................ 9

Professional fees ................................................................................................................................... 9

Planning fees, Building regulation fees ................................................................................................ 9

Planning obligations ............................................................................................................................ 10

Finance costs ....................................................................................................................................... 10

Agent’s fees and Marketing ................................................................................................................. 11

Return .................................................................................................................................................... 11

Land cost .............................................................................................................................................. 12

Site Acquisition .................................................................................................................................... 12

Tax......................................................................................................................................................... 12

CASH FLOW AND DISCOUNTED CASH FLOW ........................................ 13

LONG TERM FINANCIAL APPRAISAL .................................................. 14

UNCERTAINTY AND RISK ................................................................. 16

Planning Risk and Land Cost............................................................................................................... 16

Finance Risk and Interest .................................................................................................................... 16

Construction Risk and Cost ................................................................................................................. 17

Market Cycle Risk and Values ............................................................................................................. 17

COMPARABLE VALUATION ............................................................... 18

2GUIDE SUMMARY

In this guide, we cover development

appraisals, introduce cash flow concepts,

and cover long term financial modelling.

We talk about where the money comes from

in the guide ‘Development Finance’

HOW TO READ THIS GUIDE

Throughout the guide, there are links to

useful documents and websites for further

reading. These are highlighted in blue

We have also suggested group activities and

outputs to help you and your group work

through each stage.

If at any point you would like advice and

guidance, you can contact us at

info@communityledhousing.london

DISCLAIMER

Our team and associate Advisers encourage

groups to think openly and clearly about their

objectives and how to achieve them. The

information in this guide is for general

guidance and is not legal, financial, or

professional advice.

Community Led Housing London assumes no

responsibility for the contents of linked

websites. The inclusion of any link should not

be taken as endorsement of any kind or any

association with its operators.

You can read our full disclaimer here

3WHAT IS A FINANCIAL APPRAISAL?

A financial appraisal helps check that the different sites. The work will become more

project is viable in terms of development and resolved as more detail is added.

in the long term. For private developments,

the appraisal establishes the potential for Development appraisals look at the

profit in relation to the risks incurred. For development phase of a scheme. This may

non-profit organisations, appraisals attempt be sufficient if the intention is to sell all of the

to ensure that the costs are recoverable, and homes.

the scheme achieves what you want.

Long term financial appraisals or ‘investment

Assessing and evaluating a development is appraisals’ should be included if the

not just a one-off task, but a continuous organisation intends to hold rented units. We

process which needs constant monitoring will cover these later.

and revisions, typically on a spreadsheet.

‘Residual’ valuations use the known variables,

Different scenarios should be tested and the

or those easier to estimate, to asses an

implications of changes to assumptions

‘unknown’ value. The residual equation can

understood. It is very important to use

be rearranged depending on what you want

realistic assumptions rather than trying to

to find out. To work out a residual valuation,

make the numbers say what you want.

you will need to isolate components of the

Because the assumptions are so important, proposed development such as land price,

appraisals should be carried out by construction cost, finance cost and housing

experienced RICS valuation surveyors1 and rents/prices.

informed by the advice of your wider

In a residual land value appraisal, you assess

professional team, and the market.

whether your likely eventual income can

You need to understand what they are doing cover the costs of your development.

and how they arrived at different costs as the Whatever remains is the Residual Land Value,

decision to proceed and carry the risk, i.e. what you can pay for the land.

ultimately rests with your organisation.

If you know or assume the cost of land, it can

An indicative site is often useful in order to also tell you the likely return or profit.

work up a model. This can be translated for

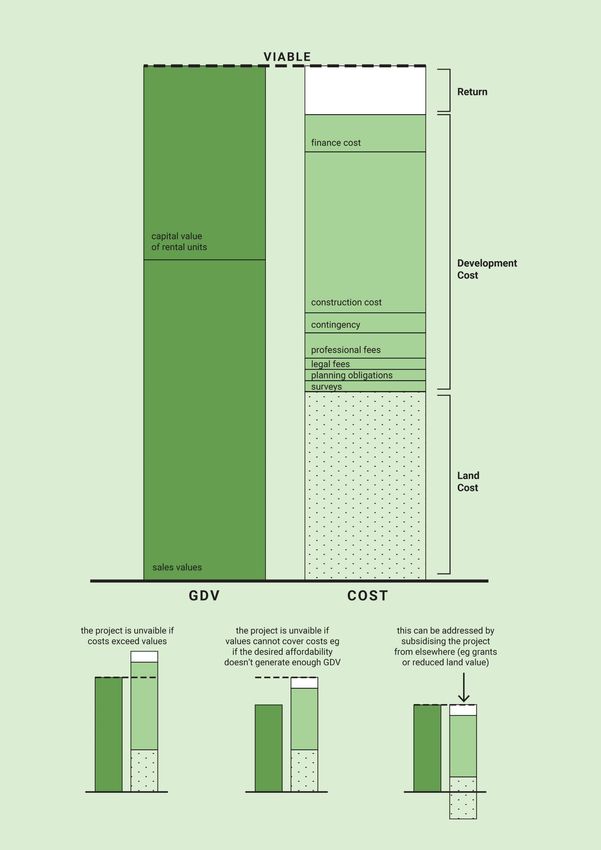

Residual Land Value Appraisal

Gross Development Development Return Residual Land

Value2

– Cost3

– Requirement

= Value

Development Return Appraisal

Gross Development Development Return

Value3

– Cost

– Cost of the Land = (on Capital or IRR)

1 The 2

professional body in the UK is the Royal Gross Development Value is the estimated value of

Institution of Chartered Surveyors (RICS), not to be the completed development.

3 Development Costs are all of the likely costs

confused with Quantity Surveyors.

involved in building the project.

45

GROSS DEVELOPMENT VALUE

The Gross Development Value (GDV) is the specification. It’s important that you base the

final capital value of the completed estimate on firm reliable evidence and careful

development. It is calculated by assessing analysis and not to rely heavily on a forecast

what the properties would be sold or rented or overestimations. The property market is

for, based on current comparable evidence4. impossible to forecast accurately so the

emphasis should be on the current market.

Annual rents and sales values are usually

SCHEDULE OF ACCOMMODATION

best analysed by reference to a rate per

To work out the GDV, you will need a

square foot (or per square meter) and are

schedule of accommodation which outlines:

based on net internal area (NIA).

• how many homes you are proposing

• their net internal area (NIA)5. Investment yield of rental property

• their tenure. The investment yield is a quick way to

It does not need to be the definitive design estimate the capital value of rental property.

but should be realistic. This is usually A snapshot of the annual rental income is

prepared by an architect, following an initial multiplied by the inverse of the yield which

capacity study of the site. For example: represents the growth in the rental income

and the risks associated with it.

→ RUSS Schedule of Accommodation

Annual Rental 1 Capital

→ OWCH Unit Mix Schedule × =

Income % Yield Value

RENTS AND SALES VALUES The yield can be obtained by comparing

Market rents and sales values are best similar recent sales of rental properties for

established with an agent or a valuer. The investment purposes. In general, the faster

estimates must be as realistic as possible the rent is expected to grow, the lower the

and based on a thorough analysis of the yield, and the higher the level of perceived

market, refering to comparable evidence, risk the higher the yield.

based on recent sales or lettings of similar

schemes in the surrounding area.

AFFORDABLE HOUSING

Information from property sites such as

Zoopla and Rightmove, collate all their The GLA set out a series of affordable

information from Land Registry and can housing products :

provide a rough starting point. • London Affordable Rent

As no two properties are identical, it is • London Living Rent

important to make adjustments to reflect • London Shared Ownership

differences in size, age, quality and

4The emphasis should be put on current and not projected values.

5The net area of the housing unit (the internal usable space excluding lifts and corridors in a block etc) needs to

be established and is known as the net internal area (NIA).

6The GLA defines and publishes rents for funding from the GLA or other funders. The

differently sized units in different parts of affordable housing grant rates are fairly low

London. These can be used for your and unlikely to fully cover the gap between

appraisal, however there is still a need to market values and affordable housing.

establish market values, as this will be Established housing associations typically

needed by lenders to act as their security, use the income from unencumbered existing

and will help you work out how others would stock or build market value units to cross-

approach a residual valuation (to compare subsidise additional social units. This GLA

your valuation against). report finds that this may not continue to

Community led housing organisations can work, and greater levels of affordable

innovate in affordable housing products and housing grant are needed.

tenures, working out what affordability

means to their community, and how it can be

TRANSACTION COSTS

set. The London Community Housing Fund

Regardless of whether the you intend to hold

Prospectus has further information about the

the property to let or sell units to residents,

fixed and negotiated grant rates available.

the gross development value needs to be

expressed as a net development value to

Income from grants allow for purchaser’s costs such as stamp

Grants are usually included as another form duty, agent’s fees and legal fees (incl VAT).

of income for the scheme. This may include

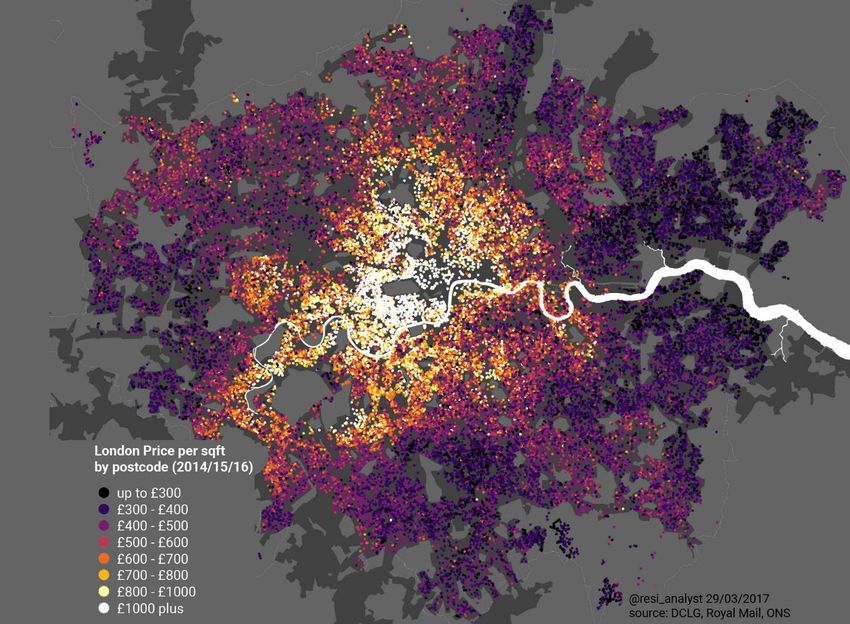

Map showing the price per sq. ft by postcode. Interactive version available here

7COSTS

SITE INVESTIGATION COSTS materials used in the building and the cost of

labour, as well as the following extra sums:

Investigations and surveys should give a

better idea of what can be built and reduce Abnormals are additional costs that may be

the risk of unexpected costs further down the required on a particular site, such as dealing

line. To begin with, you may rely on desktop with contamination, asbestos, flood risk, or

research and surveys which can be cheaper infrastructure.

to carry out. When you need more intrusive Demolition of existing property either in full

surveys, you will probably need the or partially, including.

landowner’s permission.

External works including landscaping and

A list of surveys you may want to access, such as car parking, outdoor amenity

commission are listed in our guide on space, highways, footpaths, cycle and refuse

‘Finding a Site’. storage.

While it is good practice to systematically

investigate everything about a site, it is more

Self-build is where prospective residents and

economical and efficient to focus on

volunteers contribute their labour into the

particular aspects that are likely to pose

construction. It can make some savings on

issues, so you can understand their

construction cost, although it is usually

implications better.

relatively small compared to overall

development costs (including the cost of

CONSTRUCTION COSTS land). The labour and materials cost in

construction are usually evenly split. You may

For simple appraisals, construction costs are

still require professionals to carry out more

usually estimated as a rate per square metre.

specialist and complicated work, and there

This is then multiplied by the gross external

will still be supervision and insurance costs.

area (GEA) of the proposed building6. The

It is also important to bear in mind labour

building costs are estimated at the time of

with limited training and experience may take

the proposed implementation of the

longer on site, and time spent working on

development project. Usually no allowance is

site, may mean you are not able to earn as

made for construction cost inflation, but a

much in other work. However there may be

contingency of 10% is included.

non-monetary benefits in self-build, when

Spons’ and BCIS provide average considered holistically.

construction cost data, for different building

types and construction methods.

Pre-fabrication and off-site manufacture is

As designs develop a Quantity Surveyor will

not necessarily much cheaper for smaller

come on board and work alongside other

schemes where economies of scale may not

consultants to provide further resolution.

be possible, and where tight sites require

They will look at a detailed breakdown of the

creative design responses to optimise

6 Gross area of the building can be measured in a perimeter walls, or the centre line of the party wall. It

number of ways. For construction cost, you measure does not include open balconies, external fire

the Gross External Area (GEA) includes the whole are escapes, parking areas, terraces, gardens or covered

of the building up to the external face of the walkways.

8housing density, rather than units with This includes the architect, the quantity

standard dimensions. It is important to surveyor, the structural engineer, the

establish what is included in quotes from off- mechanical and electrical engineers and the

site manufacturers, as foundations and project manager. It may also include

groundworks are not often included and are environmental and planning consultants,

significant proportion of construction costs. landscape architects, traffic engineers,

Although it may actually be more expensive acoustic consultants, party wall surveyors

on a per square meter rate, off-site and other specialists. Community led housing

manufacture can make the overall projects may also want to make special

construction time period shorter and may allowances for a deeper co-design processes

provide cost certainty compared to traditional than conventional schemes.

construction methods. It is usually better to The total cost of professional fees is

ask your professional team to explore the normally estimated around 12–18% of the

role of pre-fabrication in your project, without ‘hard’ construction cost. The actual rates can

being fixed on something that may not be the vary with the size of the project and

best suited for your particular site or project. complexity of the task.

External works, such as landscaping and They are either calculated on a ‘flat fee’ basis

highways, are often treated separately with or a negotiated percentage. The agreed fee

different square meter rates or fixed sums. may depend your relationship with each

professional. Small refurbishment schemes

normally attract higher percentages than

CONTINGENCY larger development projects. If professionals

Developments never stick entirely to the perceive your scheme to be high profile or

initial budget forecast. It is important to innovative in some way, they may compete to

include a development or construction be a part of the project and reduce their

contingency to cover unexpected costs. rates.

Contingency typically ranges up to 10%

depending on the complexity of the

development and usually covers the potential PLANNING FEES, BUILDING

increases costs such as labour, construction REGULATION FEES

or unanticipated delays. These fees are paid to the local authority in

The actual contingency itself depends on making a planning application and are based

your ability to plan and execute: on the scale and nature of the scheme. A list

of fees can be found on local authority

• an accurate development plan

websites.

• the associated time period

• the level of risk and return built into the If obtaining planning permission proves

proposal difficult, or in the event of an appeal, you may

have to allow for planning consultant fees,

solicitors, counsel and expert witnesses. The

PROFESSIONAL FEES extra time period involved will need to be

These fees are normally calculated as a reflected in the finance costs too.

percentage of the ‘hard’ construction costs Building regulation fees are on a sliding scale

and include all fees for professional services based on the final building cost. Details are

employed in the development.

9available from the council’s building control rate that a developer would be offered for

department or other approved inspectors. senior debt. However, the actual cost of the

finance is affected by many factors which

can include:

PLANNING OBLIGATIONS

• varying underlying interest rates

These are payments made to the Local

• refinancing of loans on differing terms

Authority and GLA to account for the impact

• amortisation (reducing or paying off a

of development on the surrounding area.

debt with regular payments)

Community Infrastructure Levy (CIL) is a set • the risk in the development

rate per meter square of development • the relationship between the borrower

collected by Local Authorities to fund and the financier

transport, schools, open spaces and other • the risk that the borrowed funds will be

infrastructure across the borough. It is set paid in full by the due date

differently in different places and for different

kinds of development, and you need to check

Different lenders will lend on different criteria

planning policy documents.

but they will all look closely at security value

Affordable housing doesn’t usually require and asset cover:

CIL payments to be made, although planners

will have to accept your proposals meet their

affordable housing definitions and policies. Security Value is the value that a lender can

expect to recover should the borrower default

Self-build and custom-build is also exempt

on a loan and the lender must repossess the

from CIL, and most community-led housing

property. This tends to be below the price of

should fall within this definition even if there

a new home, to reflect that if it were

is no physical construction work by residents.

repossessed, it would by that time be second

Section 106 agreements are negotiated on a hand, and the lender would wish to sell it

scheme by scheme basis, and place quickly and would also incur costs in selling it

obligations on the development including again.

payments for individual site-specific items.

These could include contributions towards

affordable housing if it is not being provided Asset Cover is a test to determine an

on site. organisation’s ability to cover its debt

obligations with its assets, after all liabilities

have been met. In effect it determines if, in a

FINANCE COSTS worst-case scenario, an organisation has

Very rarely will a developer cover the enough assets that can be sold to repay its

development costs entirely with their own loans. Funders cover this issue by lending up

money. Normally finance is arranged through to a set percentage of overall value of the

a funder who will lend a proportion of the development. This is called the Loan to Value

costs for a return on the loan. This is the ratio. Thus, if the value of the site was £1m

interest rate charged on the loan for the and the Loan to Value (LTV) percentage was

‘term’, or duration of the loan, which is a 70%, the maximum debt that could be raised

further cost for the development. would be £700k.

In the residual calculation, the interest rate on

costs traditionally takes the market interest

10It is usual for lenders to stipulate their The finance cost is therefore divided in half

desired level of Asset Cover and Interest and the interest is calculated on that sum

Cover in the loan documentation and over the whole construction period.

agreements. These are known as Loan In order to calculate compound interest on a

Covenants and will be clearly outlined in any quarterly basis the annual interest rate is

term sheets. divided by 4 to obtain the quarterly rate (say

Finance is needed over a period of time. 2%).

Interest is only paid on funds drawn down. This produces a compound interest formula

The drawdown of funds, and therefore of (1.02)n, where ‘n’ represents the number of

distribution of finance costs are not incurred quarters over which the interest is calculated.

at once, or even in a linear manner. In order to

calculate the interest costs, it is common to

Finance fees

estimate the total length of the development,

These fees are related to the costs

when expenditure will stop and cash inflows

associated with arranging development

will occur (when the homes are sold, or let

finance. For example, you will need to pay the

and refinanced).

bank’s arrangement fees, solicitor’s fee and

surveyor’s fee. Fees can be negotiated, but

Pre-development usually reflect the size of the required loan

Typically, you might assume a 12-18 month and may be anything between 3-10% of the

pre-development period where you obtain value of the loan.

planning permission and prepare for start on

site8. Costs prior to site acquisition, such as

searching for potential sites, are usually not AGENT’S FEES AND MARKETING

considered to be substantial enough that you

Agent fees are what a developer would pay

will need to borrow.

an estate agent to sell or let individual units.

Most developers will also make an allowance

Development to spend on promoting and marketing the

The site acquisition is usually the first project. This may not be needed to the same

commitment that requires a major outlay and, extent for community led housing projects,

therefore, interest is calculated on all site which may have a ready pool of people

acquisition costs over the entire development looking to move in. However, it may be a

period. good idea to make an allowance for running

You would assume 18-24 months of allocation and selection processes and

construction time, plus any time after checking eligibility for sub-market housing.

construction completes before income

comes in7. Many developers try to defer the

RETURN

payment for the land until later to reduce the

interest payments. The return requirement8 in your model

depends on the risks involved with the

A ‘rule of thumb’ assumes that costs are

scheme, a higher level of risk will need a

incurred evenly over the construction period.

7These are assumptions and do not take into on site, can add a significant amount of time into the

account the scale or complexity of the project. pre-development and construction time.

8 Also known as Developer’s Profit

Delays in the project such as planning or abnormals

11higher level of return. So this can also be the landowner in order to achieve a target

interpreted as a ‘risk allowance’. rate of return through the Residual Land

Return is usually expressed as a percentage Valuation (see page 4).

of the total development costs in

straightforward or simple projects.

SITE ACQUISITION

It is difficult to generalise but often

Site acquisition costs and fees usually

developers will seek between a 15% and 25%

include: legal fees between 0.25–0.5% of the

of the total cost as return, the percentage

land price, depending on the complexity of

rising with perceived risk. You may also

the deal, and agent’s introduction fee

include contingencies within your return,

normally agreed at 1–2% of the land price.

rather than a separate allowance for

These have to be set aside from what can be

contingencies as discussed below.

offered to the landowner.

For projects with greater complexity, for

example larger developments that will take a

long and make be built in phases, return may TAX

also be expressed as the profit on GDV. More Stamp duty is paid as a percentage of the

sophisticated developers will consider the land price. You can look up stamp duty rates,

Internal Rate of Return (IRR) calculated using as well as reliefs and exemptions, and other

a Discounted Cash Flow (DCF) model (see information. Stamp duty will also have to be

page 16). This allows a better comparison set aside from what can be offered to the

between different projects of different landowner.

lengths.

There are usually VAT implications to be

It is important not to confuse the not-for- factored into the development appraisal.

profit nature of community led housing Different types of developers and different

projects, and assume a profit margin does types of schemes all have different VAT

not need to be included in the appraisal. Not- implications including standard, reduced and

for-profit housing associations typically seek zero-rated VAT scenarios. Even if VAT is

an Internal Rate of Return (IRR) of 7%. This recovered, there may be a cash flow

ensures there is some money to keep the implication between the payment of VAT and

organisation going to the next scheme. its recovery.

Stamp duty and particularly VAT are complex,

LAND COST and you should get a relevant accountant or

tax adviser on board, to structure the

The price to be paid for the land may already

development in the best way.

be agreed or sought by the landowner

(vendor). In most cases the developer has to

establish a land price that can be offered to

12CASH FLOW AND DISCOUNTED CASH FLOW

Cash Flow appraisals allow the timing of Discounted Cash Flow (DCF) models

costs and income to be spread over the examine the different cash flows, but they are

development period, or the long term, to give all discounted back (using a present value

a better assessment of finance costs. While formula) to a common point in time to allow

Residual Valuations are relatively simple, they an even comparison.

are not very flexible in handling the timing of The DCF approach is a method of valuing an

costs and income. asset using the concepts of the time value of

In practice, some of the development costs money. It is an explicit approach where all

are incurred before the start of the building future cash flows are estimated and

contract, e.g. finance fees and much of the discounted to their present value. The

professional fees. The construction costs discount rate reflects the time value of

usually follow an S-curve of cumulative money and a risk premium, representing

expenditure. The final 3% of construction compensation for the risk inherent in future

costs is usually held back as a ‘retention’ cash flows that are uncertain.

under the building contract. There may also In simple terms, the time value of money can

be a gap between completion of the be considered to represent interest foregone.

construction until the full letting, sale or re-

The discounting acknowledges the

finance. Quantity surveyors and project

relationship between time and money. The

managers can estimate the timing of costs.

“time value of money” can be explained by

In the cash flow model, interest is calculated thinking about if you’d prefer £100 now or

on the outstanding balance (including £100 in a years’ time. Clearly you’d prefer it

interest) at the end of each month at a now. If you’re offered £100 now and £200 in

monthly rate equivalent to the effective a years’ time you’d choose £200 in a years’

annual rate (EAR). Adjusting the pattern of time, as it is unlikely you will more than

expenditure, may lower the total interest double the money in that time. Somewhere

figure. The cash flow method is particularly between those figures is a figure that will

useful where receipts come in before the make you equally happy either way. Say £120

completion of the full scheme, e.g. a phased in a years’ time is equivalent for you to £100

development. The model also allows you to now. So £120 in a years’ time is worth 83% of

adjust for changes in interest rates over the its value in today’s money. ( 100 / 120 = .83)

development period or for different sources

This allows a calculation of the ‘internal rate

of finance within the appraisal.

of return’ (IRR), which considers both the

A cash flow appraisal will be required to timing and the size of each cash flow. This

satisfy potential lenders with a detailed can be used instead of a percentage return

business case. You may use both techniques on cost and is ideal for comparing different

together, using the cash flow method to potential projects. However, the DCF method

calculate the interest cost and put this into a does not show the outstanding debt at a

conventional residual appraisal for clear particular time. It shows the profit in today’s

presentation. The cash flow method will be value rather than the actual sum that will be

used throughout the development to evaluate received at the end of the development.

the project as costs are incurred and

influencing variables change.

13LONG TERM FINANCIAL APPRAISAL

Long term modelling considers the life of the annual income. Simply being a community

scheme after the development period. A 30- led organisation is unlikely to reduce voids.

40-year cash flow analysis will be required Similarly, an assumption must be made for

where you intend to hold property to let. This rent and service charges which are not paid

may integrate with your development by tenants who fall into arears. This is usually

appraisal, or if you are buying homes built by around 2% of annual income but may be

another developer it can establish what price greater if specialist groups with multiple

you can afford to pay for the homes. needs are to be housed.

A long-term financial model will establish

whether a single development will be Management costs

financially viable after it is built and can be Management costs will be influenced by the

managed and maintained at agreed model of management chosen, for example;

standards. volunteer, employee, agency, or a

If this is the only scheme of a new combination of these. Typically, these are

organisation, it must also ensure that it can assumed at around £500 per property per

sustain itself over the long term. Existing year. Management costs may include office

organisations will adapt their financial plans costs and other associated overheads,

to include the new scheme and ensure that it employee or managing agency costs,

does not place an unreasonable burden or recruitment or procurement costs and

drain on existing residents or other activities, contract management costs.

and that the organisation is viable over the

long term.

Maintenance and servicing

Whilst a yield can be used as a quick way to There will be an expected annual cost of

establish the capital value of rented homes, maintaining the landlord’s fixtures and

long term modelling should consider the fittings in each property. Whilst day to day

following in more detail: repairs should be low in the early years after

construction or refurbishment, the costs are

Rent inflation or growth rate likely to rise over the medium and long term.

As well as knowing the rent, long term The maintenance of common parts and the

appraisals must make assumptions on how landlord’s structural elements should also be

much the rent will be increased each year considered. The cost of servicing the scheme

over the long term. If the community led will be present throughout.

housing organisation is a Registered Provider

(RP), or the homes are being managed by Asset management

one, the Rent Standard will place restrictions A costed asset management plan should

on rental increases. inform the financial plan regarding the long-

term costs of major works programmes and

Void and bad debt levels cyclical maintenance (such as lifts every 15

Rent and service charge income will be lost years for example). Enough funds should be

due to periods when homes are ‘void’ or set aside over several years.

untenanted. Usually assumed around 2% of

14Governance costs

Running the organisation brings on going

costs including meetings, member expenses,

consultation and involvement, comms and

marketing, insurance, annual return fees,

accountancy and audit costs and legal fees.

Cost inflation assumptions

All costs increase over time as inflation

impacts on the initial cost base. However,

cost inflation is not uniform and realistic

assumptions must be made for different

costs such as materials, wages, insurance,

utilities and professional fees. Unrealistic

assumptions about cost inflation when

compounded over the long term can be

catastrophic to financial viability.

Tax liabilities

The taxation implications for long term

models should also be considered, including

VAT, Corporation Tax, Annual Taxation on

Enveloped Dwellings and employer tax

liabilities, where relevant.

Financing or net borrowing costs

The remaining rental income after

management and maintenance etc must be

able to pay down any debt outstanding when

a development is completed (ie development

finance that is not paid back though the sales

of homes). This may require assumptions

over long term financing and interest rates.

Typically, the first 5-10 years are most

challenging as rents will not grow

significantly. A healthy margin of error for

‘interest cover’ during this time will be key.

Interest rates will also apply to reserves

accumulated over the long term, although

this will likely be lower.

15UNCERTAINTY AND RISK

Risk is an inherent part of the property PLANNING RISK AND LAND COST

development process and needs to be

Planning risk refers to the risk in a change of

assessed as part of this process. You can

use, or detailed design consent for the

reduce elements of risk at a cost. The degree

development, or other relevant government

of risk is usually related to the complexity

consents required to progress to the

and scale of the proposed development.

construction phase of the development.

It is important that the inputs as reliable as

The purchase price of the land is usually the

possible and based on the experience of

first major financial commitment (page 11).

professional advice and/or robust sources of

In order to reduce risk, it is common to try to

information.

agree an ‘option’ or negotiate a purchase that

You should avoid getting caught up with is subject to obtaining a satisfactory planning

making an appraisal “work”, if it means you consent, when the detailed construction cost

are being unrealistic or over optimistic about is also clearer.

assumptions. It is also good to test scenarios

The greater the possibility that planning and

to understand what things are more sensitive,

related permissions will be denied, or

and to make sure your project can cope with

complicated and time consuming to achieve,

a margin of error. Sensitivity analysis can be

the greater the assessed planning risk. This

built in the appraisal to clearly identify

translates into a higher developer’s risk

changes in inputs.

required, and likely lower land value.

The two major types of risk are systematic

Once planning consent has been obtained,

(wider market context) risk or unsystematic

the value of the scheme is clearer. Before a

(property specific) risk.

planning consent it is unclear what exactly

Rental and sales values and construction you will be able to get permission for, and

costs are usually the most sensitive variables how long that will take. Further applications

and are subject to fluctuations outside your may be made after a site is purchased.

control. However, planning applications take time and

Over the development process, your any potential increase in value needs to be

commitment to the scheme increases and it balanced against the cost of holding the site.

becomes more difficult to change course,

even if things around you are changing. At

FINANCE RISK AND INTEREST

the same time risks reduce over the

development period, as they either emerge, or Funding arrangements need to be in place

as pass away. For example, a project very before any major commitment is made. In

close to completion will not have any obtaining the necessary finance to acquire

planning risk, minimal construction risk and the land and build the scheme, you will be

very little market cycle risk, hence the exposed to any fluctuations in interest rates

developer’s profit required in taking such a during the development period. However, at a

scheme on at the valuation date will be a cost, you can either fix or cap the interest

much lower percentage of profit on cost than rate. The terms of long-term finance

a scheme without planning permission. negotiated before the development are likely

to be less favourable than those that can be

16negotiated upon completion, although you local or global economy, the higher the risk

can secure both together. that the market could change to the

developer’s detriment before the delivery of

the scheme.

CONSTRUCTION RISK AND COST

Rental values for affordable housing tend to

The construction cost is the second major

be well defined and increase in line with set

financial commitment.

formulas or local incomes etc, rather than the

Construction risk refers to the risk that speculative property market. However values

construction will be delayed potentially due may be more closely linked to the property

to variations or late information, labour market (for example as a percentage of

becoming unavailable, labour and materials market values)

costs rising during the course of works

It is essential to obtain the most reliable, up-

(partly due to inflation) or that unexpected

to-date value estimates. Due to the

events cause sudden escalations in the cost.

complexity of the property market, valuers

The more technically demanding, large, are unable to predict future changes in

complex and long the build programme is, property values with a high degree of

the higher the risk. certainty. You therefore shouldn’t try to

There are some ways of making the predict future values, even when construction

construction cost more certain by passing all costs in the appraisal grow at current

or some of the risk and design responsibility inflation rates, as this would expose you to

onto the contractor, although greater more risk. It cannot always be assumed that

certainty of cost usually means a higher cost rises in construction costs during a

overall. Good project management is vital to development, will be saved by rises in values.

preventing increases in cost and time delays. However, the level of uncertainty associated

You should question every aspect of the with achieving an estimated sales value can

building contract in order to manage any be removed if a pre-sales or off-plan sales

problems as they arise. can be achieved.

The benefit of a pre-sale reducing risk has to

MARKET CYCLE RISK AND VALUES be weighed against the opportunity costs of

achieving a potentially higher value in a rising

Market cycle risk is the risk that during the

market. Although there may be an advantage

course of the development market demand

in reducing void periods before income is

for the development changes. The longer the

received, as the building will be handed over

development programme, the more

on completion without further interest

uncertainty there is in the prevailing market,

payments.

17COMPARABLE VALUATION

Although the residual method is usually took place 2 years ago may not be

preferred for development projects, the relevant to a valuation where the market

comparable method of valuation is has changed significantly over that

commonly used by valuers for other property period).

valuations. The above list is not exhaustive. It gives an

The comparable method is typically adopted indication of the thinking adopted by valuers.

in markets with enough recent evidence of Other factors may need to be considered

similar transactions. It involves searching for depending on the value drivers for the type of

recent transactions that give an indication of development. For example when assessing

the price the market would pay. land value for a retail development or an

Land transactions that can act as office development.

comparable guides to the price that can be After establishing relevant comparables, the

achieved on a site, should be similar to the valuer usually adjusts the sale prices

site in the following ways: evidenced by these transactions to reflect

• situated nearby or in a similar type of differences between the comparable land’s

location to the subject site value driving factors/characteristics and

those of the subject land. This is often

• of the same planning category or

practically achieved either:

permissions as the subject land (e.g. both

sites have planning permission for • through an implicit adjustment to the

industrial use); prices achieved on the comparable sales

by an experienced valuer; or

• identical or similar in respect of the

utilities present or near the site (e.g. both • through a more explicit process of listing

sites have water, electricity and gas each value factor and applying a premium

present and capped on site or access at or discount to the comparable price

the edge of the site); achieved to reflect an adjustment due to

differences between the comparable and

• topographically like the subject site (e.g.

the land/site being valued.

both sites are flat and have vegetation);

• with similar access to transport links (e.g.

Valuing land with the comparable method

both sites have direct highway access);

can be tricky as it is difficult to find suitable

• surrounded by similar infrastructure (e.g. comparables and any attempt to 'equalise'

both sites are situated in the town centre the differences can become a fruitless and

with good access to the surrounding retail, unverifiable exercise. Land transactions also

leisure and town centre amenities); lack the transparency of other property

• situated in a position with access to a transactions. It is not easy to find out how the

similar socio-demographic profile as the deal was structured and influencing factors.

subject site (e.g. both sites are situated The residual method usually offers a more

close to small towns with affluent rational alternative as to what a potential

catchments); purchaser ought to pay, although the

• not too historic to be irrelevant to the comparable method may be used to

current valuation (e.g. a transaction that determine GDV.

18Contact us

7-14 Great Dover Street

London

SE1 4YR

020 3096 7769

info@communityledhousing.london

Follow us on social media

@CLHLondon

19You can also read