FMG Monthly Update A Complete Roundup Across Key Assets - ATB Financial

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

FMG Monthly Update A Complete Roundup Across Key Assets

Agenda Macro Overview……………………………………………………..3 Trending Map…………………………………………………………7 Canadian Dollar………………………………………………………8 DXY and Interest Rates…………………………………............11 WTI and Canadian Crudes……………………………………..12 Natural Gas…………………………………………………………....14 USDCAD Regressions……………………………………………..15

Macro Overview

Priced for Vaccination

The Outlook At Times Seems Binary: Vaccination or Bust

2021 is off to a muddled started. Stock markets swooned in early If Israel is any indication we still have long fight ahead of us and the

January before finding their footing and rallying in unison with the path won’t be linear. Israel has vaccinated by far the largest portion

S&P 500 reaching fresh record highs by mid-month. WTI surged of its population of any country to date – a full 53% have received at

above US$53, and the Loonie traded to its best levels since 2018. least one dose compared to about 9% for the US and a paltry 2.5%

Everything was moving in the right direction, and an explosive post- for Canada. And yet even at that pace lockdowns are still required.

COVID recovery seemed assured and right at our fingertips.

The newer COVID variants move faster. Faster than the needle and

In the past two weeks or so reality has struck with its usual force. the faster than our manufacturing and supply chains. And ICU

Vaccine supplies have become scarce. Logistical rollouts have been availability still rules the day with regard to the policy response.

bottlenecked to the point where vaccine nationalism is now a thing. Early efforts will pay-off, but we may not see the immediate benefits

And stock markets were seemingly turned on their head as bands of until at least the spring time. However, there are some green shoots

retail traders took on the hedge funds and won the day. Is this the to take note of, and I for one remain optimistic on the outlook

start of another bout of extreme volatility across assets? despite the challenges in front of us. So let’s take a quick look at the

current set-up.

The strong trends in place throughout Q4 2020 are being tested –

it’s nothing catastrophic at the moment, but certainly the trend of

risk assets rallying in uniform fashion seems a bit tired and out of

place at the moment. And perhaps it should.

Highlight text in abeen

Has the recovery callout box in?

priced would

Andbeifideally

so, what

set up like this (Open Sans Bold

happens if it doesn’t show up? 12pt)

FMG Monthly Update | Feb 2021 ATB Capital Markets | 3Macro Overview

Reasons for Optimism

There Has Been Some Improvement In Hospitalization and Case Rates

It has been about 25 days since the US started to administer vaccines and there are some positive takeaways even though they are minor yet. In

the US, we note a distinct drop in the hospitalization rate as well as the number of people on ventilators. New daily case rates are also declining

in a rather sharp fashion. Most encouragingly, deaths in long term care facilities, which have received a higher rate of vaccinations than

the general population, have improved. And that last point is excellent news – there are fewer vulnerable people exposed to severe health

outcomes which is one of the keys that must be achieved before re-opening on a larger scale. These data point to an improving trend – but as

you can see the starting point was very dire to begin within and thus there is a lot of work yet to do.

US Hospitalizations and Ventilators Per Million US Daily New Cases

450 30 450,000

400 400,000

25

350 350,000

300 20 300,000

250 250,000

15

200

200,000

150 10

150,000

100

5 100,000

50

50,000

0 0

-

US Current Hospitalizations (LHS) US Currently On Ventilator (RHS) Daily New Cases 5-day Moving Average

Sources: Covid Tracking Project, Bloomberg, ATB FMG

FMG Monthly Update | Feb 2021 ATB Capital Markets | 4Macro Overview

Reasons for Caution

Vaccination Rollouts Have Been Very Slow in Some Countries…But the US is on Track

Even for developed countries the differences in vaccine availability are stark. Canada may have “secured” the most doses per capita amongst our

peers but we don’t have any manufacturing capabilities and thus are dependent on others to honour commitments. This nebulous arrangement

finally came to its logical conclusion last week when the EU effectively rolled out vaccine nationalism: Doses are now prioritized for EU member

states ahead of exports. Regardless, distribution has been slow and questions remain regarding efficacy against the newer variants with J&J’s

iteration only proving 66% effective against the South African strain – far below the ~90% threshold from earlier Pfizer and Moderna versions.

Yet if we extrapolate the current run rate for shots delivered in the US, by the beginning of September at least one shot will have been

administered to 83% of the population. The pace could increase, or it could slow, or the shots could prove less effective. A lot has to go right.

But given the current pace of administration, and the current range of variants, the US is on track to achieve herd immunity by late Q3/early Q4.

Global: Vaccine Doses Administered Per 100 People US and Canada: Shots Delivered % of Population

60 9.00%

8.18%

50 8.00%

7.00%

At the current pace, the US will have

40 delivered at least one dose to 83% of

6.00%

the population by September

30 5.00%

4.00%

20 2.42%

3.00%

10 2.00%

0 1.00%

Israel

Bahrain

Serbia

Iceland

Italy

Finland

Greece

Norway

Slovenia

Russia

Poland

Austria

Netherlands

Mexico

Ireland

Kuwait

Argentina

Guinea

Spain

Germany

Canada

Slovakia

France

Hungary

China

U.A.E.

U.K.

U.S.

Denmark

Sweden

Saudi Arabia

Czech Republic

0.00%

Dec-20 Dec-20 Dec-20 Jan-21 Jan-21 Jan-21 Jan-21

Canada USA

Sources: Covid Tracking Project, Bloomberg, ATB FMG

FMG Monthly Update | Feb 2021 ATB Capital Markets | 5Macro Overview

Conclusion: Priced for Vaccination With Little Room for Error

Global Growth Could be Set for Take Off…

This leads us to conclude that the outlook is positive. PMI’s are pointing to an expansion of activity, employment trends are improving, and

demand for commodities remains high. China’s latest 5-year plan, the 14th iteration, could be one of the most forceful for global growth since

the early 2000’s: The trend towards urbanization is not complete with the government targeting 80% urbanization over the next 15yrs compared

with 60% at present. Record fiscal and monetary stimulus have the ability to pull up incomes for the middle class, which on balance will lead to

greater aggregate demand in the coming years, especially for commodities. Yet there are risks. How much good news is left to price in?

Equity markets pay for future performance and at current 22x forward earnings there is little room for error. Earnings will have to surprise to the

upside for the rally to extend. And what if the Fed removes stimulus sooner than currently anticipated? That could lead to a rather forceful re-

pricing. But the green shoots from early vaccination results and trajectories for herd immunity give us reason for optimism.

PMI’s Are Improving, Well Above Key 50 Level… ...But Is That Enough? S&P 500 P/E Ratio Near Record

65

26.00

60 Expansion 24.00

55

22.00

50

20.00

45

P/E Ratio

Contraction 18.00

40

35 16.00

30 14.00

Jun-18

Jun-19

Jun-20

Aug-18

Aug-19

Aug-20

Feb-18

Apr-18

Oct-18

Dec-18

Feb-19

Apr-19

Oct-19

Dec-19

Feb-20

Apr-20

Oct-20

Dec-20

Feb-21

12.00

10.00

US Canada China

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

2021

Sources: Bloomberg, ATB FMG

FMG Monthly Update | Feb 2021 ATB Capital Markets | 6What’s Trending? After a Stellar Run in Q420, Markets Are Consolidating

Trending Map: Mapping January returns vs. December returns reveals a market mostly treading water heading into

February with commodities like oil and soybeans notable exceptions

12.00%

Reversing Up Trending Up

10.00%

8.00% WTI

SoyBeans

6.00%

Copper

DXY CAD

January Return

4.00%

HYG

CNY

2.00%

GBP

NOK

0.00%

AUD

-2.00% JPY TSX EUR

S&P 500

TLT

-4.00% MXN

BRL

-6.00%

Trending Down Reversing Down

-8.00%

-8.00% -6.00% -4.00% -2.00% 0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% 14.00%

December Return

Source: Bloomberg, ATB FMG

FMG Monthly Update | Feb 2021 ATB Capital Markets | 7Canadian Dollar – A Pause Before Resuming Strength?

Fig. 1: USDCAD Broke Key Resistance ~1.3000 Fig. 2: Shanghai Deliverable Copper Inventories (Tonnes)

1.50 450,000

400,000

1.40 1.3000 Break

1.30

Should See CAD 350,000

Gains Accelerate. 300,000

Tonnes

1.20 2018 lows 250,000

1.10

Chart ~1.2550 and 200,000

1.2250 medium 150,000

1.00 term targets 100,000 Chart

50,000

0.90

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 -

2003

2003

2004

2005

2006

2007

2008

2008

2009

2010

2011

2012

2013

2013

2014

2015

2016

2017

2018

2018

2019

2020

Sources: Bloomberg, ATB FMG

Fig. 3: S&P 500 vs USDCAD Regression Sources: Bloomberg, ATB FMG

5% • The Loonie has benefited from strong commodity and equity prices: global

4% growth leads to CAD strength

y = -2.5417x + 0.0031 • Copper prices in particular are a great indicator of economic activity and

USDCAD % Change

3%

2% R² = 0.5706 demand has been strong – inventories in Shanghai are near ten year lows

1% (Fig. 2)

• The equity market has maintained a close relationship with CAD as well: a

0%

Chart 5% weekly change in the S&P 500 implies a 1% change in USDCAD (Fig. 3)

-1%

-2% • The market seems comfortable looking through weaker growth in Q1 2021

-3% to greener pastures later this year

-20% -15% -10% -5% 0% 5% 10% 15% • But vaccines are a risk: Canada’s domestic story could underperform that

S&P 500 % Change of the US if Canadian vaccine rollouts do not improve substantially

Sources: Bloomberg, ATB FMG

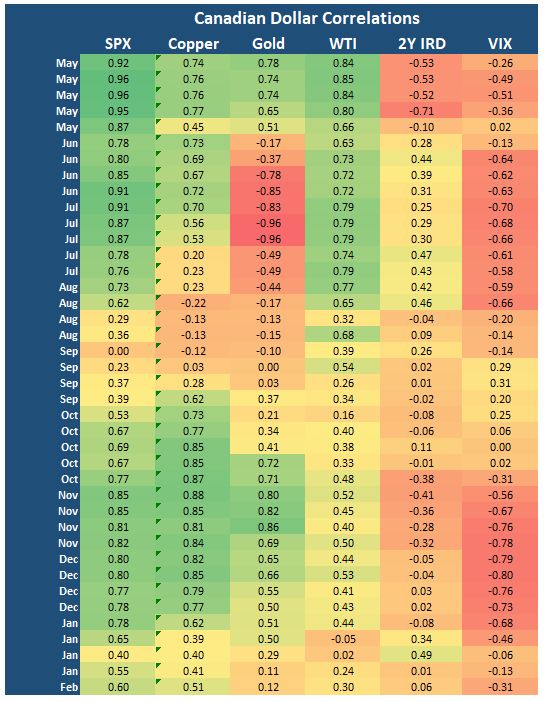

FMG Monthly Update | Feb 2021 ATB Capital Markets | 8Canadian Dollar Heat Map – What’s Driving CAD

S&P 500 and Equities Still in Drivers Seat, But Not as Clear Cut as the Past

10 Week Rolling Correlations

• CAD still maintains a strong positive correlation to

equities and copper at 0.60 and 0.51 respectively

• But you can see this is below recent highs for these

relationships ~0.85 in November

• As our Trends Map on page 7 indicated, the market

overall seems to be in a consolidation phase with

traders taking stock of how best to allocate going

forward after a strong surge across risk assets over the

past few months

• This does not imply a breakdown of the underlying

trend, just a pause

CAD Correlations largely intact, although not as

Highlight

strong as atext

fewinmonths

a callout

agobox would be ideally

set up like this (Open Sans Bold 12pt)

FMG Monthly Update | Feb 2021 ATB Capital Markets | 9Canadian Dollar Forecast

We Still See CAD Gaining on Strong Global Growth Trends

Outlook Supportive

ATB FMG USDCAD FORECAST 2021-2022

1.4500

1.4000 Positive:

1.3500 • Record QE and low rates to fuel growth + improved vaccine ramp could

accelerate re-opening trades

1.3000

• Commodities could be on verge of a super-cycle

1.2500

• Early stage build out of EV fleet and greener grid supportive of raw

1.2000 materials and energy prices in near/medium term

1.1500

• Technically, USDCAD not near oversold territory on longer term scales

Q120 Q220 Q320 Q420 Q121 Q221 Q321 Q421 2022 • Does the Canadian economy really need a 30% discount against the USD

to compete?

Historical Mean High Low ATB FMG

Negative:

Date Mean High Low ATB FMG • It’s still a pandemic, we are tethered to vaccine efficacy + logistics

Q1 2021 1.2800 1.3400 1.2500 1.2800 • Have equities and commodities (key drivers of CAD strength) priced in

Q2 2021 1.2800 1.3600 1.2400 1.2700 too much good news?

Highlight Correlations

text in a callout box intact,

would although

be ideallynot as

Q3 2021 1.2700 1.3600 1.2300 1.2500

• US yieldCAD curve steeping could largely

lead to upward pressure on front end yields

Q4 2021 1.2700 1.3600 1.2200 1.2500 set up like this

strong a(Open

asbe few Sans Bold

months ago 12pt)

which would likely supportive of USD strength

2022 1.2700 1.3900 1.2000 1.2300

• Moral suasion from the BoC: Will they draw a line in the sand regarding

CAD strength?

FMG Monthly Update | Feb 2021 ATB Capital Markets | 10DXY and Interest Rates – USD Pressured; When Will Fed Move?

Fig. 1: DXY Consolidating, Downtrend Still Intact Fig. 2: US Twin Deficits Imply a Weaker USD

105.00 0 0

100.00 -10

Testing Major

Budget Deficit % of GDP

Trade Deficit Billions

-20 -5

95.00 Support:

Structurally weaker

-30

90.00

USD narrative -40 -10

85.00

Chart intact. Market -50

consolidating at -60 -15

Chart

80.00

75.00 major support -70

~89-91 -80 -20

70.00 2016 2017 2018 2019 2020

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Sources: Bloomberg, ATB FMG Trade Deficit (USD Billions) Budget Deficit % of GDP

Fig. 3: Inflation Expectations May Force Fed’s Hand? Sources: Bloomberg, ATB FMG

3.00 US 10y Breakevens are • The trade weighted US dollar index (DXY) has been in a consolidation

already back above 2% - pattern in the very near term but the overall trend remains lower

• Over the long term the USD faces major headwinds from twin US deficits:

2.50

2.00 Record trade and budget imbalances will put sustained pressure on the

greenback

Inflation %

1.50

• Treasury Secretary Janet Yellen has essentially brushed aside a return to

Chart the longstanding official “Strong USD Policy” , and during her time as Fed

1.00 GFC

Covid chair she highlighted a strong greenback as hurting the US economic

0.50

recovery from the GFC

0.00 • That type of thinking may mean lower for longer…but long-run inflation

2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021 expectations are already above 2% – the Fed may have to follow the

Sources: Bloomberg, ATB FMG market sooner than anticipated and start tapering

FMG Monthly Update | Feb 2021 ATB Capital Markets | 11WTI Crude Oil – Bullish Fundamental Backdrop

Fig. 1: US Stockpiles Fell 64mm bbls Since June Peak Fig. 2: Supply Restraint From OPEC and US Shale

560,000 540,722 13,500 36,000

Inventories peaked

OPEC Production 000's bpd

540,000 34,000

US Production 000's bpd

at 540mm bbls in 12,500

520,000 32,000

June & have drawn

000’s bbls

500,000 11,500

30,000

480,000

an avg of 2.06mm

10,500 28,000

460,000

bbls/week since

26,000

440,000 then…but still sit 9,500

24,000

5% above the 5yr

420,000

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb avg for this time of

8,500

Chart 22,000

7,500 20,000

year

US Commercial Inventories 2014 2015 2016 2017 2018 2019 2020

US Oil Production OPEC Oil Production

Sources: Bloomberg, ATB FMG

Fig. 3: WTI 1st-12th Month Timespreads Remain Strong Sources: Bloomberg, ATB FMG

4.00 • WTI prices have been supported by record OPEC+ supply cuts along with a

3.00 renewed commitment to supply restraint from US shale as well

2.00 • The mantra from investors and management alike has been “shareholder

+US$7.44/bbl (+179%)

1.00 returns ahead of production growth”, and that theme finally seems to be

sticking

US$ / bbl

0.00

-1.00 • US commercial oil inventories have drawn -8mm bbls already this year and

-2.00 US production is 10.9mm bpd – well below the 13.1mm bpd peak 1year

-3.00 ago

-4.00 • The setup is favourable as a result with the curve pointing to a tight

-5.00 market throughout 2021 and prices looking poised to rally once again

Aug Sep Oct Nov Dec Jan Feb towards US$60 ahead of the next OPEC meeting in March

Sources: Bloomberg, ATB FMG

FMG Monthly Update | Feb 2021 ATB Capital Markets | 12Canadian Crude – Outlook Positive Despite Keystone Disappointment

Fig. 1: Canadian Differentials to WTI Relatively Strong Fig. 2: US Imports of Canadian Crude Improving

$10.00 4,100

$5.00 3,900

$0.00 3,700

-$5.00

US$/bbl

WCS 3,500

-$10.00

3,300

-$15.00 MSW

3,100

-$20.00 C5 CFT 2,900

-$25.00

2,700

Chart

-$30.00

2,500

Feb-19 May-19 Aug-19 Nov-19 Feb-20 May-20 Aug-20 Nov-20

Sources: Bloomberg, ATB FMG 000's bbl per day 4-Wk Average

Fig. 3: Low Crude by Rail Volume = Tighter Differentials Sources: Bloomberg, ATB FMG

450,000 • Canadian crude prices continue to fair quite well, buoyed by rebounding

400,000 demand from the US and a lower call on crude by rail which is helping to

350,000 support differentials to WTI

300,000

• The debottlenecking out of the WCSB is set to continue with most major

bbl per day

250,000

200,000

producers rather optimistic on differentials over the next 2-3 years

150,000 • Enbridge’s Line 3 replacement and the TMX expansion could add up to

100,000 960k bpd of egress due to new pipe and optimizations on existing

50,000 infrastructure

• While Keystone XL is a disappointment, the continued demand from US

0

Aug-16

Aug-17

Aug-18

Aug-19

Aug-20

Feb-16

Feb-17

Feb-18

Feb-19

Feb-20

May-16

Nov-16

May-17

Nov-17

May-18

Nov-18

May-19

Nov-19

May-20

Nov-20

refiners and lack of greenfield heavy oil projects, along with a structurally

short Canadian refined products market, will help to support producers

Sources: Bloomberg, ATB FMG over the coming cycle

FMG Monthly Update | Feb 2021 ATB Capital Markets | 13Natural Gas – February Cold Snap Could Have Summer Implications

Fig. 1: US Natural Gas Inventories Near 5yr Avg Fig. 2: Low Rigs Could Mean Tighter Supply in 2022

4,500 210

4,000 190

3,500 170

3,000 150

2,500 130

2,000

110

1,500

90

1,000

70

500

50

0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

5yr Range 5yr Avg 2021 2020

Sources: Bloomberg, ATB FMG US Gas Rigs

Fig. 3: Backwardated Above $3 Should Incentivize Drilling Sources: Bloomberg, ATB FMG

$3.60 • Nymex gas prices have been on a wild ride lately with front month prices

rising 53cents since Jan. 22 to hit US$2.95/mmBtu as we went to press

$3.50

$3.40

$3.30

$3.20 • Weather has been above seasonal for much of the winter, but the coming

cold blast across North American could bring inventories below the 5-yr

$3.10

$3.00

$2.90

$2.80 average just as we start to think about a challenging spring/summer

$2.70 injection season amid lower than normal drilling activity

$2.60

$2.50

$2.40

• While stockpiles may be elevated at present, there is an argument to be

$2.30 made that 2022 balances are on track to be rather tight, and this could

$2.20

lead to a sustained rally in the medium term in order to incentivize further

Apr-21

Oct-21

Apr-22

Oct-22

Apr-23

Oct-23

Apr-24

Oct-24

Apr-25

Oct-25

Jan-21

Jul-21

Jan-22

Jul-22

Jan-23

Jul-23

Jan-24

Jul-24

Jan-25

Jul-25

drilling

Today 3-Months Ago

• LNG is also a bullish caveat with US exports still tracking right at capacity

Sources: Bloomberg, ATB FMG for ~11Bcf per day on a strong Asia and Europe arb

FMG Monthly Update | Feb 2021 ATB Capital Markets | 14USDCAD Regressions – Key Weekly Regressions For CAD 2018-2021

USDCAD vs Copper USDCAD vs WTI

5.00% 5.00%

4.00% 4.00%

y = -0.1797x + 0.0004

y = -0.1387x + 0.0003

3.00% R² = 0.2536 3.00% R² = 0.3652

USDCAD % Change

USDCAD % Change

2.00% 2.00%

Charts are placed here.

The box outline is not required

1.00% 1.00%

0.00% 0.00%

-1.00% -1.00%

-2.00% -2.00%

-3.00% -3.00%

-15.00% -10.00% -5.00% 0.00% 5.00% 10.00% -20.00% -15.00% -10.00% -5.00% 0.00% 5.00% 10.00% 15.00%

Copper % Change WTI % Change

USDCAD vs DXY

5.00%

4.00%

3.00%

y = 0.6934x + 0.005

R² = 0.4631

USDCAD % Change

2.00%

1.00%

0.00%

-1.00%

-2.00%

-3.00%

-4.00%

-5.00% -4.00% -3.00% -2.00% -1.00% 0.00% 1.00% 2.00% 3.00% 4.00% 5.00%

Sources: Bloomberg, ATB FMG FMG Monthly Update | Feb 2021 ATB Capital Markets | 15

DXY % ChangeATB Financial Markets Contacts

FMG Desk Contacts

Rob Laird

Managing Director

ATB Financial Markets Group

403-974-3582

rlaird@atb.com

Foreign Exchange Commodities Interest Rates Trading

Janek Guminski, CFA Chris Fricke, MBA Shane Hawryluk Dan Noble Mark Johnson, MBA Bennett Cheung, CFA

Sr. Director FX Sales Director FX Sales Director Commodity Sales Director Commodity Sales Director Interest Rates Sales Director FX Trading

403-974-3580 403-974-3580 403-974-3582 403-974-33582 403-974-3582 403-974-3583

jguminski@atb.com cfricke@atb.com shawryluk@atb.com dnoble2@atb.com mjohnson4@atb.com bcheung@atb.com

Cynthia Chan Mike Gee, MBA Mark Engelking, CFA

Associate Director FX Sales Director ATBFX Director FX Trading

780-392-7070 403-869-8526 403-974-3583

cchan@atb.com mgee2@atb.com mengelking@atb.com

Bill Dahmer

Director FX Initiatives

780-408-7237

wdahmer@atb.com

Analyst Business Management

JP Dore Kim Campbell

Analyst, FMG Sr. Business Manager

403-888-5342 403-554-3963

jdore@atb.com kcampbell2@atb.com

FMG Monthly Update | Feb 2021 ATB Capital Markets | 16You can also read