Global and Thai Economic Outlook 2021: Key Themes and Implications - Presentation for OIE Conference 26 November 2020

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Global and Thai Economic Outlook 2021: Key Themes and Implications Presentation for OIE Conference 26 November 2020

สถานการณ์เศรษฐกิจในปัจจุบัน

การฟื้นตัวของเศรษฐกิจโลกยังเผชิญความเสี่ยงจากการระบาดรอบสอง

เศรษฐกิจไทยทรุดหนักจาก Covid-19 และฟื้นตัวได้อย่างช้าๆ

การใช้จ่ายในประเทศมีความอ่อนแอและยังต้องพึ่งพามาตรการกระตุ้น

COVID update

Global daily infection is accelerating again, with new outbreaks in EU & US. The daily infection cases in Asia and

Latin America gradually drop. Fatality rate also declines as scientists find more effective drugs and treatments.

7-day moving average daily change of COVID-19 infection (by region) 7-day moving average daily change of COVID-19 infection (key country)

Unit: no. of daily confirmed patients Nov 17-23: 571,196 Unit: no. of daily confirmed patients

700,000 200,000

Infected 59,671,202

600,000 Death 1,407,542 Africa, Oceania & Caribbean Islands 13,447 US

Recovery 38,211,000

150,000

500,000 Active cases 20,052,660

400,000

Europe 250,662 EU-5*

100,000

300,000

200,000 US 177,497 50,000 India

India 89,566 Brazil

100,000

Rest of Asia Russia

Brazil China

Rest of LatAm 60,270 ASEAN ex. Thai

0 0 Thailand

29 Jan 29 Feb 31 Mar 30 Apr 31 May 30 Jun 31 Jul 31 Aug 30 Sep 31 Oct 29-Jan 29-Feb 31-Mar 30-Apr 31-May 30-Jun 31-Jul 31-Aug 30-Sep 31-Oct

100% Africa & Others

Fatality rate (%)

2% Oct 22: FDA approved Remdesivir

10%

7.2% Nov 10: FDA approved Bamlanivimab (EUA)

Europe 43%

50% 5% 2.4%

2.2%

US 31%

Asia 16% 0%

Latin America 10%

0% 29-Jan 29-Feb 31-Mar 30-Apr 31-May 30-Jun 31-Jul 31-Aug 30-Sep 31-Oct

Note: *EU-5 consists of data from France, Germany, Italy, Spain, and United Kingdom

Source: EIC analysis based on data from World Health Organization (WHO)

3

Lockdown measure

With a rebound in new cases, some countries, mostly European, have started to retighten lockdown

measures. Global economy is expected to getting worse in coming quarters before getting better when the

vaccines are distributed.

Government stringency index Real GDP growth and Government stringency index

Unit: index (100 = most stringent)

Thailand Singapore US China 10

100 France Spain Malaysia UK CN

5 TW ID VN

90 TW VN

Real GDP growth (Unit: %YOY)

US MY CN

80 SG KR KR

0 MX VN

DE PH

70 JPTW FR MY KR US

TH

-5 UK IT DE

60 FR TH SG CN ID

ES IT

UK

50 US

-10 ES

HK PH

40

DE SG

-15 Q1/2020 TH

30 M

Q2/2020 IT FR PH

MX

20 Q3/2020

-20

ES UK

10 Thailand’s index @ 3Q2020 = 46 More stringent measures,

more affected to the economy.

0 -25

0 20 40 60 80 100

Feb-20

Sep-20

Nov-20

Jan-20

Apr-20

Jul-20

Mar-20

Aug-20

Jun-20

Oct-20

May-20

Average COVID-19 government stringency index (Unit: index)

Source: EIC analysis based on data from Oxford university and CEIC

4

Stall recovery

World economy has recovered after lockdown measures have been eased. However, the recovery has

stalled following a resurgent in cases and relatively stricter measures.

Composite PMI Google mobility index: Retail and recreation

Unit: 100 Unit: % change from baseline (3 Jan- 6 Feb 2020), 7DMA

30 US UK

70

US Eurozone Japan China Global France Japan

10

Thailand World (GDP weight)

60

57.9 -10

55.3

Thailand

53.3

World

50 -30

UK

47

45.1

-50

France

40

-70

30 -90 III. Stalling Stage

I. Lockdown Stage II. Easing Stage • Re-lockdown

-110 • Rising number • Large Stimulus • Fiscal / policy cliff

20 of new cases • Infection numbers • Scarring effects

-130 • Panic spread stabilized/improved (e.g. bankruptcy &

• Pent up demand LT unemployment)

10 -150

Apr-20

Oct-20

Mar-20

Jul-20

Jan-20

Aug-20

May-20

Jun-20

Feb-20

Sep-20

Nov-20

Apr-20

Feb-20

Mar-20

Jul-20

Aug-20

Sep-20

May-20

Jun-20

Oct-20

Note: A value over 50 indicates an expansion

Source: EIC analysis based on data from CEIC and Google (Data as of 16 November 2020)

5

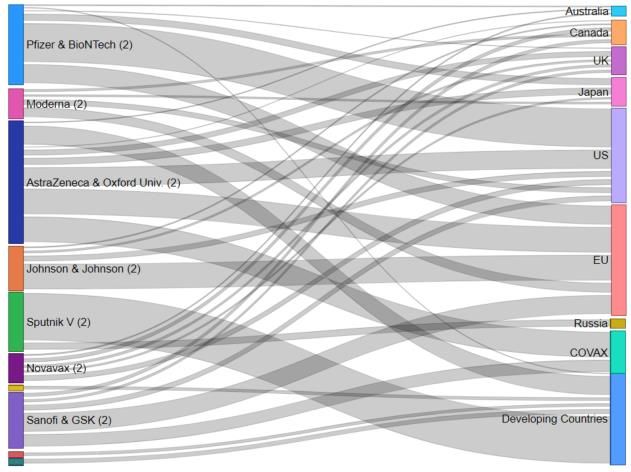

Summary of the leading COVID-19 vaccine candidates: MRNA shows high efficacy, but face logistics challenges.

Target Preliminary Latest phase-3

Vaccine Production Capacity Storage

spike Company Nationality phase-3 data vaccine efficacy Doses

platform0 (million doses) Temperature

protein analysis (minimum: 50%)

✓ Pfizer & BioNTech US/German Nov 8th 95% 2 2020: 50 / 2021: 1,300 -80 to -70˚C

mRNA

✓ Moderna US Nov 16th 94.5% 2 2020: 20 / 2021: 500 -20˚C

AstraZeneca & 1.5 dose: 90%

✓ UK Nov 23rd 1.5, 2 2021: 3,000 +2 to +8˚C

Oxford University 2 doses: 62%

Johnson & Johnson End of ‘20/

Viral vector ✓ US - 1, 2 2021: 1,000 +2 to +8˚C

(2 candidates) early ’21

✓ Gamaleya Center Russian Nov 11th 92% 2 2021: 500 -18˚C

✓ CanSinoBio Chinese - - 1 2021: 100 +2 to +8˚C

Sinovac Chinese 1st week of Dec. - 2 2020: 300 +2 to +8˚C

Inactivated Sinopharm

Chinese - - 2 2020: 220 / 2021: 1,000 +2 to +8˚C

virus (2 candidates)

Bharat Biotech Indian - - 2 2021: 200 +2 to +8˚C

✓ Novavax US Early of Q1 2021 - 2 2021: 2,000 +2 to +8˚C

✓ Medicago & GSK Canadian/UK - - 2 n.a. +2 to +8˚C

Protein

subunit ✓ Anhui Zhifei Longcom Chinese - - 2, 3 n.a. +2 to +8˚C

Sanofi & GSK

✓ French/UK H2 2021 - 2 2021: 360 +2 to +8˚C

(phase 1/2)

Source: EIC analysis based on data from WHO, US FDA, companies’ press releases

6

Vaccine update

Positive impacts of vaccine on the economy will depend on vaccine characteristics and effective

distribution. DM countries likely to get widespread vaccination in H1/2021, while EM will be H2 or later.

1. Vaccine characteristics COVID-19 vaccine: Advanced Purchase Agreements

• Efficacy rate and no serious side effect results only include those who are

healthy excluding vulnerable groups (pre-existing conditions and elderly)

• Still uncertain if vaccine prevents or reduce transmissions to others.

mRNA

• We don't know if the vaccine prevents asymptomatic transmission

• Vaccine's efficacy declines over time, booster shot will likely be required

2. Manufacturing and Distribution

• No mRNA vaccine has ever been licensed for infectious disease, thus approval

process could take time

• mRNA is a new technology, technology-transfer to developing countries may

Viral Vector

take longer than other technology which already has production facilities in

developing countries

• Vaccines must be kept at deep freeze for storage (Pfizer’s at -70 to -80°C and

normal refrigerator temperatures for up to 5 days , Moderna at -20 °C and

normal refrigerator temperatures for up to 30 days)

3. Vaccine Availability and Acceptance

• Combined production capacity for Pfizer and Moderna in 2021: 1,800 – 2,300

million doses enough for 900 – 1,150 million people

Protein

• Population of Developed Countries* ~ 1,230 million Cansino (1)

• Astrazeneca has secured 1.3 billion does of advanced order and 2-billion

doses of manufacturing capacity

Inactivated Virus: Sinopharm (2), Sinovac (2)

*Source: EIC analysis based on data from WHO, European Commission, HHS, Companies’ websites, Press search

7

K-Shaped Recovery

Equity markets and commodity prices have recovered from their trough in Mar-Apr 2020, however, there are

disparity between sectors. Oil price is expected to slowly recover in 2021 driven by increasing oil demand.

Global stock index , by sector Key commodity 2020 price movement

Unit: Index (31 December 19 =100) Unit: Index (31 Dec ‘19 = 100)

World Energy Since Pfizer vaccine Gold (+19.1%) Oil (-28.9%)

140 Technology Financial announcement 175 Rubber (+47.3%) Sugar (+12.1%)

130 Health Care Industrial

Consumer Staples Real Estate 150 Steel (+12.3%) Copper (+15.2%)

120

Hotel and restaurant

110 125

100

100

90

80 75

70 50

60

25 2019 1Q20 2Q20 3Q20 4Q20F 2020F 2021F

50

40 K-shaped recovery 0

Brent 64 51 32 43 42 42 50

Jan-20

Apr-20

Jul-20

Jul-20

Feb-20

Mar-20

Mar-20

Sep-20

Sep-20

Nov-20

Aug-20

Dec-19

May-20

May-20

Jun-20

Oct-20

Nov-20

Feb-20

Jan-20

Apr-20

Jul-20

Sep-20

Mar-20

Dec-19

May-20

Aug-20

Jun-20

Oct-20

• Key commodity prices has bottomed out after lockdown restriction

• Stock market performance has been boosted by technology firms

has lessened and demand has gradually returned.

• The pandemic has pronounced implications for work and

• Oil price has seen a gradual rebound due to rising oil demand

consumption behavior that are expected to encourage spending on

following economic recovery after lockdown, and OPEC+ oil

new technologies.

production cut. EIC expect Brent to gradually recover in 2021F.

Source: EIC analysis based on data from Bloomberg.(data as of 24 November 2020)

Thailand’s GDP

Thailand’s GDP in Q3/20 showed a smaller contraction thanks to increasing roles of public spending.

% of % of

%YoY 2019 2019Q4 2020Q1 2020Q2 2020Q3 YTD %YoY 2019 2019Q4 2020Q1 2020Q2 2020Q3 YTD

GDP GDP

RGDP 100% 2.4% 1.5% -2.0% -12.1% -6.4% -6.7% RGDP 100% 2.4% 1.5% -2.0% -12.1% -6.4% -6.7%

Private Consumption 52.1% 4.5% 4.1% 2.7% -6.8% -0.6% -1.7% Agriculture 6.1% -0.2% -2.5% -9.8% -3.3% -0.9% -5.2%

Public Consumption 14.6% 1.4% -0.9% -2.8% 1.3% 3.4% 0.7% Manufacturing 26.4% -0.7% -2.2% -2.6% -14.6% -5.3% -7.4%

Total Investment 23.9% 2.1% 0.8% -6.5% -8.0% -2.4% -5.6% Utilities 2.9% 4.7% -1.2% 1.1% -13.3% -9.4% -7.4%

Private Investment 17.8% 2.8% 2.6% -5.4% -15.0% -10.7% -10.3% Construction 2.7% 1.9% -2.1% -9.9% 7.4% 10.5% 2.6%

Public Investment 6.0% 0.2% -5.1% -9.3% 12.5% 18.5% 7.3%

Wholesale & Retail 15.6% 5.7% 5.2% 4.8% -9.8% -5.5% -3.0%

Export G&S 71.4% -2.6% -3.4% -7.3% -27.8% -23.5% -19.4%

Transport & Storage 6.8% 3.4% 3.9% -6.0% -38.8% -23.6% -22.2%

Export Goods 54.3% -3.6% -5.1% 2.0% -15.9% -7.7% -7.2%

Hotel & Restaurant 6.2% 5.5% 6.8% -23.3% -50.2% -39.6% -37.2%

Export Services 17.2% 0.5% 1.7% -32.2% -68.0% -73.3% -56.3%

Import G&S 64.6% -4.4% -7.9% -3.1% -23.2% -20.3% -15.6% Info & Communication 5.3% 8.8% 10.6% 3.2% 2.7% 3.1% 3.0%

Import Goods 52.3% -5.5% -8.6% -0.3% -19.3% -17.0% -12.3% Finance 7.2% 2.7% 3.4% 4.5% 1.7% 1.6% 2.6%

Import Services 12.3% 0.5% -5.3% -13.0% -37.4% -32.8% -27.6% Real Estate 3.9% 3.3% 2.7% 1.7% 0.8% 1.5% 1.3%

ด้านการใช้จ่าย การฟื้นตัวที่เร็วกว่าคาดของการบริโภคภาคเอกชน และรายจ่ายภาครัฐ ด้านการผลิต ภาคเศรษฐกิจที่มีส่วนสาคัญในการพยุง GDP ในช่วงไตรมาส 3 คือ ภาค

ที่ขยายตัวเร่งขึ้น โดยเฉพาะการลงทุนภาคัรัฐ มีส่วนสาคัญที่ทาให้ GDP ในไตรมาส 3 การก่อสร้างที่ ได้รับอานิสงส์จากการก่อสร้างภาครัฐที่ขยายตัวดี และภาคการสื่อสารที่

หดตัวน้อยกว่าคาด (Bloomberg Consensus median คาดการณ์ว่า GDP Q3 จะหด ได้รับประโยชน์จาก Digital trend ขณะที่ภาคธุรกิจที่เกี่ยวกับภาคท่องเที่ยว (ภาคการ

ตัวที่ -8.8%YOY) ขนส่ง การโรงแรมและภัตตาคาร) ยังคงซบเซาต่อเนื่อง

Source: EIC analysis based on data from NESDC

9

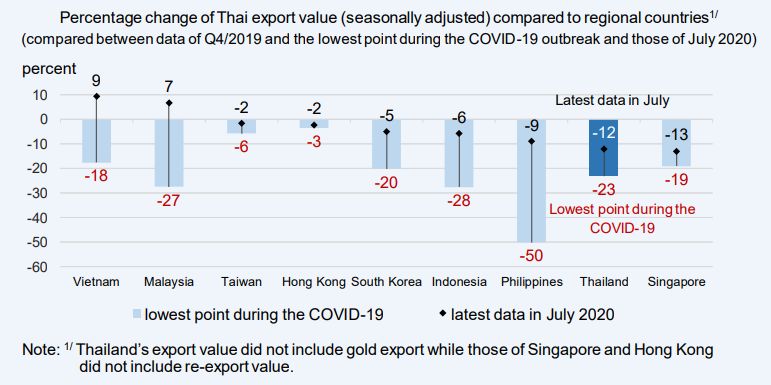

Exports

Thai exports have recovered more slowly than peers due to structural factors.

Source: BOT

10Tourism

Due to heavy reliance on foreign tourist income, Thai economy has struggled to recover. Boosting

domestic tourism has partially helped for some areas in some periods but overall occupancy remains low.

Share of Foreign Tourism, WEO No. of Thai visitors and hotel occupancy rate (Sep ’20) Hotel occupancy rate

Unit : % of 2019 GDP Unit: %YoY Unit: % of total room supply (reopening & temp. closure hotels)

No. of Thai visitors

Hotel occupancy rate

Thailand 12.0 (Overall: -34%yoy in Sep20,

(Overall: 27%)

Phillipines 8.7 -53% yoy(9M20)) 2020 actual

New Zealand 6.0 2019

Provinces

Vietnam 5.9 actual

Italy 5.5 Q1 Q2 Q3

Spain 5.4

China 4.6 Bangkok 82% 54% 11% 20%

Singapore 4.2 Chonburi 80% 50% 9% 27%

India 3.7

France 3.7 Prajuab Kirikhan 66% 49% 8% 39%

Australia 3.1 Chiang Mai 74% 56% 6% 42%

Japan 2.2

Indonesia 1.9 Phuket 76% 57% 2% 9%

South Korea 1.6

Krabi 70% 55% 1% 7%

-3 2 7 12 Phang Nga 66% 56% 5% 10%

* Thailand’s number accounts only int’l tourism >70%

0 to -20% 60.1-70% Surat Thani 72% 51% 2% 13%

-20.1 to -40% 50.1-60%

• Countries that rely more on tourism Thailand 71% 52% 7% 27%

-40.1 to -60% 40.1-50%

sector tend to suffer more from COVID-19

pandemic. -60.1 to -80% 20.1-40%

< 20%

Source: EIC analysis based on data from IMF and Ministry of Tourism & Sports

11Domestic economy

Domestic economic indicators also indicate that various sectors of Thai economy have bottomed out

thanks to several boosts, but the recovery has been uneven and stalling.

Thailand’s key economic indicators (latest data as of Sep) Despite weak purchasing power, there are supporting

factors that helps shore up domestic spending.

Unit : %YOY, index (RHS)

Oct YTD

Domestic car sales -3.9% -27.4% -3.9% Gov’t stimulus worth 500 billion THB

10% 80

passenger -25.9% -37.1%

commercial 10.4% -20.9% Public construction worth 792 billion THB,

0.0% 75

10% Domestic motorcycle sales -11.3% -13.4% 5% growing 9% from last year

1.2% 70 Precautionary saving has subsided (deposit

0% 0% -2.8% growth 11.1%YOY in July vs 8.9%YOY in Sep)

65

-10% -4.8% -3.7%

-5% Businesses have cut margin to boost sales

60 e.g. Real Estate developers (see chart)

-20% -22.0%

-10% 55

Avg. housing price changed in BMR 1H20 vs 2019 (%)

-30% 50

-15%

-0.4 1-3MB

-40% PCI-Durable 45 SDH -1.2 -0.3 3-5MB

-20% -2.7

PCI-Non Durable 40 -1.0 5-10MB

-50% -1.8

PCI-Services Private investment index SMD 0.6 >10MB

-25% -3.1

-60% Domestic car sales Manufacturing Production index 35

-1.7

Private consumption index (PCI) -30%

Inventory Index (RHS) 30 TH -0.7 1.9

-70% 0.6

Oct-19

Apr-20

Feb-20

Dec-19

Jun-19

Jun-20

Aug-19

Aug-20

-4.2

Dec-19

Apr-20

Jun-19

Jun-20

Feb-20

Oct-19

Oct-20

Aug-19

Aug-20

-3.7 -2.3 CD

-4.2

Source: EIC analysis based on data from CEIC, BOT, FTI, OIE, and Google

12Summary

EIC forecasts 2021 Thai GDP to expand by 3.8% with slow and uneven recovery, resulting from slow global

growth and more material domestic scarring effects.

2020f 2021f

Unit

Previous Now Previous Now

GDP %YOY -7.8 -6.5 3.5 3.8 2021 Risk Factors

Private Consumption %YOY -2.3 -1.1 1.9 2.0

Public Consumption %YOY 2.2 2.3 2.4 3.3 Larger & more

COVID-resurgence &

Private Investment %YOY -12.6 -10.9 4.7 4.7 effective stimulus

delay of vaccine

measures than

Public Investment %YOY 8.3 11.5 8.9 9.8 approval/ distribution

expected

Exports of Goods & Services %YOY -19.8 -20.5 6.5 7.9

Imports of Goods & Services %YOY -14.3 -15.5 5.7 8.1

Widespread

Slower global

Export values (USD, BOP) %YOY -8.0 -8.0 4.9 5.3 bankruptcies / NPL

growth hurting

Import values (USD, BOP) %YOY -15.0 -14.2 6.3 8.6 leading to higher UR

exports sector

and credit crunch

million 6.7 6.7 8.4 10.4

Number of foreign tourists

%YOY -83.1 -83.2 25.0 55.4

Political instability

Headline Inflation %YOY -0.8 -0.9 0.9 0.9

Delay in tourism affecting domestic

Core Inflation %YOY 0.3 0.3 0.2 0.3 recovery demand and foreign

Brent USD/Brl. 41.2 41.2 49.5 49.8 investor’s confidence

Policy rate (end-period) % 0.50 0.50 0.50 0.50

Source : EIC analysis

13Impacts to Industries

COVID-19 has disrupted both demand and supply-side at an unprecedented level leading to

extended and wide-spread impact to global manufacturing and supply chain

Top 5 challenges faced due to COVID-19 disruption* World manufactured goods trade by product, 2020Q2

Unit: % respondent Unit : %YOY, April May June

45

41

13 11

30 4 4 5 6

22 22

-7 -4

-11 -14 -17

-21 -24

Material Drop in Worker Cash-flow Planning issues -26

shortages demand shortages issue -42

-37

-53

Disruption Impacts

-70

• Stalled production/unfulfilled Shutdown or Automotive Footwear Industrial Precision Computers Pharmaceuticals

Supply orders reduction of products machinery instruments

Apart from pharmaceuticals,

• Lower inventory/safety stock production trade in many electronic goods

• Sharp demand reduction capacity Trade in most manufactured also outperformed most goods

Demand • Products shortages and pent-up Disruption in goods bottomed out in April as households and businesses

demand global logistics before starting to recover, but upgraded their equipment to

*responses of more than 200 manufacturing and supply-chain leaders across industries (June 2020)

the recovery was partial. adjust WFH.

Source: EIC analysis based on information from PWC, McKinseyIn Thailand, shortage of cashflows resulting from lower demand & financing difficulties have posed the biggest impact to firms, with small-size and low-tech firms suffered the most. Main challenges faced by Thai firms Main causes of challenges Remarks: “GVC firms” refer to producing intermediate inputs and sell a large share to foreign customers or domestically located MNCs , subsidiaries of MNCs with a large proportion of exports and/or imports and two-way traders, while “domestic upstream” refers to non-GVC firms that sell intermediate goods, whereas the “domestic downstream” indicates non-GVC firms that sell finished goods Source: United Nations Industrial Development Organization, Thailand (UNIDO), online survey of impact assessment of COVID-19 on Thai Industrial during 15 Apr-15 May 2020, N=320, June 2020)

Uneven trend is also witnessed in Thai manufacturing product sales

Manufacturing Products sale values by type (domestic and exports)

Unit: %YTD (9 months/2020)

Work from home and

10% health concerns

Petro Refinery

Pharma

0%

Rubber&Plastic Comp & Elec

Paper products

Furniture

Metal products Electricals

-10% Durables and Delayables

Export sales

Chemicals Food products

Machines Others non-Metal products

-20% Wearing apparel

Leather Motorcycles Basic metals Beverages

-30% Textile

-40%

Automotives

-50%

-50% -40% -30% -20% -10% 0% 10%

Domestic sales

Source: EIC analysis based on data from OIE

17Weaker growth Supply chain rearrangement

• Lower private demand and • Greater emphasis on security

deteriorating balance sheet and resiliency

• Long-term unemployment and • Shorter, more diversified and

underemployment localized supply chain

• Lower investment

Accelerated tech adoption Increasing focus on ESG

• Consumer behavior change

and the rise of contact-free

Themes for • More scrutiny on climate change

and social inequality risks

economy

• Business transformation lead

Post-COVID • Increased importance of

by more investment in digital

technology

World stakeholder engagement as part

of corporate strategy

Market concentration Expanding role of government

• Widespread firm exits lead to more • Higher public spending and

concentrated market more liquidity injection

• Distressed financial status • More active role in business

encourages higher M&A activities sector

• Digital disruption trends favor

companies with ability to adapt

Source: EIC analysis based on data from Moody’s, McKinsey

18The global economy will continue to evolve toward a tripolar system with US, China, and EU as its

pillars. These shifts will have ramifications for trade & supply chains, regulatory standards, technology,

and the role of government, with widespread implications across countries and sectors.

1. Post-pandemic focus on economic

self-sufficiency will heighten

rivalries and lower productivity

2. The interests of the three pillars will

increasingly diverge.

3. Closer intraregional trade

connections will partly offset

slowing interregional flows.

4. More competition in emerging

technologies will lead to

governments playing a more

prominent role.

5. Political considerations will

influence global investment and

capital flows.

Dual circulation strategy

19Global supply chain rearrangement

Thailand will face both opportunities and challenges from global supply chain rearrangement.

Drivers Broad strategies Impacts Implications to ASEAN & Thailand

Trade war-Tech war

1.Diversification • Shorter & less just in time Potential benefits from China + 1

supply chain strategy with ASEAN advantages in

COVID-19 • More regional & FDI openness and relatively low

2. Regionalization/ fragmented trade operation costs.

Localization (Reshoring) Potential negative impacts from

• Close to market reshoring esp. critical sectors such as

Digital technology production base medical supplies, F&B and Hi-tech.

e.g. 3D printing, • Rise in digital services &

Blockchain, IOT 3. Digital Supply Chain (DSC)

infrastructure

Policy recommendations:

• Strengthen fundamentals to

attract more strategic FDI

including improving human

capital, reducing political

uncertainty and regulatory

hindrances.

• FTA and regional integration will

lessen reshoring strains as well as

promote regional trade and

investment blocs.

Source: EIC analysis based on data from McKinsey, Moody’s

20Scarring effects

1

Rising trend of market concentration is likely to accelerate as a result of economic slowdown and more

intense competition both from domestic large firms and global tech firms, which are better adapt to

digital disruption compared to SME.

Market concentration has risen steadily over the past 2 decades. The On top of concentrated share in big domestic firms, global tech firms

trend should continue as COVID impact disproportionately affect small (FAANG+) are also gaining shares in many industries from media to

firms. commerce.

Market concentration (top1%), all firms Stock price index

Unit: % of total revenue Unit: index (Dec 31, 2019 = 100)

75 73.7 180 SET index

160 S&P500 (excl. FAANG)

70 FAANG 146

140

120

65

100 99

59.5

60 80 77

• Top 1% in 2018 = 4,464 firms 60 Oct 27, 2020

55 • Total firms in 2018 = 446,444 firms

40

20

50

2018

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

0

Dec-19 Feb-20 Apr-20 Jun-20 Aug-20

Source : EIC analysis based on data from DBD, SET, and IMF

21In 2021, government stimulus and investment policies, demand recovery of necessities and new normal trends will

support recovery of particular businesses such as construction, F&B, healthcare and logistic services

Key drivers Descriptions Potential sectors

▪ Government subsidized scheme to stimulate domestic tourism: the "We

Travel Together" scheme, reopen the border for 1,200 long-stay tourists

▪ Royal decree to borrow 1 trillion baht to stimulate and rehabilitate the

economy

▪ Newly awarded/bid transport mega projects e.g. high-speed rail, urban Hotel in popular Public Building material

Government electric train, seaport destination located construction (long steel

near Bangkok contractors and cement)

stimulus policy

▪ Demand for essential products will be less sensitive to economic

slowdown

▪ Demand recovery, especially consumer products like food, will fuel

demand for logistics and transportation services

Fresh fruits Modern Logistic Shelf-stable Crude palm oil

and cassava grocery service food and for biodiesel

Demand recovery starch retail providers cheapest protein production

of necessities

▪ Health and food safety concerns, and demand for wellness lifestyle

▪ Work from home, entertainment at home, and online

e-learning increase demand and change the pattern of internet usage

▪ E-commerce and home delivery service (esp. food)

▪ New hobbies such as cooking, gardening will support demand for related Healthcare Rubber Fixed broadband HDD & Parcel Food

product gloves internet service Semi- delivery ingredients

New normal products for medical providers conductors providers

trendsSlow recovery of global demand and domestic demand for durable goods as well as key structural changes

will continue to adversely impact some businesses especially hotel, airline, automotive and real estate

Key challenges Descriptions Impacted sectors

▪ Easing tourism restriction but caution remain will continue to pressure

on global tourism and related businesses

▪ Gradual economic recovery will still weigh on demand from our trading

partners and weakens Thailand’s export outlook, esp. those that are

export-oriented Hotels in locations Airline Refinery Cars Luxury F&B

that rely on revenue exports products

Slow recovery of from foreign tourists

global trade & tourism

▪ Lower purchasing power of consumers will continue to hurt demand for

residential property and affect on developers to postpone the new

projects

▪ Slow domestic recovery, high HH debt and more prudent lending policy

will lower demand for big-ticket items and durable goods Residential Auto makers, part suppliers

Persistent low estate and auto dealers

purchasing power of

domestic consumers

▪ Supply chain rearrangement will create both positive impact in bringing FDI

and negative impact in withdrawing production facilities from the country

▪ Gradual change of technologies; a shift towards more energy-efficient

and environmentally friendly vehicle (like EVs and hybrid) will negatively Desktop PC ICE Car makers Midstream rubber

impact those producing old, obsolete technologies/products exporters

Structural changes ▪ Heightened competition from new, potential competitors

and disruptive technologyThe COVID-19 outbreak has widely impacted businesses. Businesses related to tourism and the sales of durable

goods were significantly affected and will take longer time to recover.

More than 20% Hotels

Determinants for recovery

High revenue contraction Thai Airlines

1 Economic conditions and purchasing

Automotive

power Thai GDP is expected to recover

Industrial Estates Commercial RE Car Dealers

Restaurants in 2022. Foreign spending will depend

(land sales) Retail oil Residential RE

on COVID-19 containment, fiscal

Impact to 2020 revenue compared to 2019

Refinery

Rubber stimulus, and economic structure of

each country.

10-20% revenue 2 Social distancing without

contraction vaccine, revenue from businesses

Marine Transport that rely on social interactions, esp.

Private Steel

(Thai ships) tourism will continue to be

Building Materials Construction Petrochemical

Non-grocery W&R impacted from social distancing

Trucking Sugar

Electric train measures

Plastic product

3 Structural change e.g. consumer

behavior change, technology

Less than 10% adoption, and supply chain

revenue contraction rearrangement

Medical services Home Appliances * Impact and recovery within industry

Mobile operator Grocery W&R Overall F&B Rice may be uneven depending the business’s

Low Palm Oil Cassava ability to adapt. Desirable strategies are

such as establishing online presence,

prioritizing financial stability, and

2H 2020 1H 2021 2H 2021 1H 2022 2H 2022 After 2022 adapting to consumer behavior.

Time for quarterly revenue to recover to 2019 average Source : EIC analysis

24แนวโน้มของเศรษฐกิจในอีก 1-2 ปีข้างหน้า เศรษฐกิจไทยมีแนวโน้มฟื้นตัวช้า จากแนวโน้มภาคท่องเที่ยว จะกลับมาได้ช้าและผลพวงจาก 3 แผลเป็นทางเศรษฐกิจ

Global economic projection

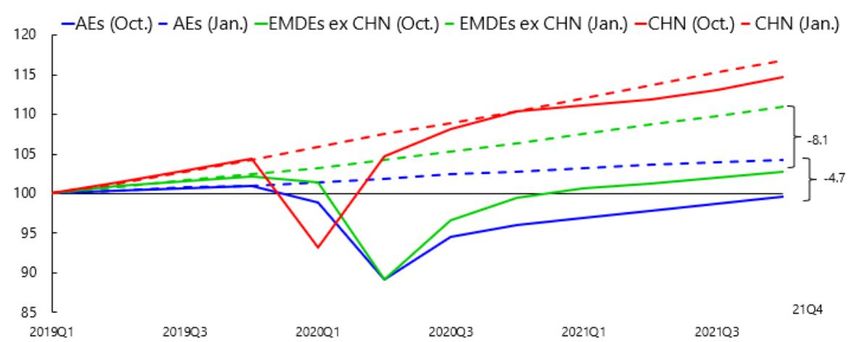

EIC projects the world economy to contract by -4.1% in 2020 and a 5.4% recovery in 2021. Excluding

China, most economies will remain below 2019 levels in 2021.

EIC ‘s GDP Forecasts Path to recovery, by IMF’s WEO

Unit : %YOY Unit: %YOY

GDP growth (%YOY)

Country

(% of world GDP, PPP basis) -2.0

2019 2020F 2021F

World 2.8% -4.1% 5.4% -8.1

US (15.9) 2.2% -3.6% 3.5% -4.7

Euro (15.4) 1.3% -7.3% 4.5%

Ger (3.5) 0.6% -5.0% 3.2%

Fra (2.4) 1.5% -8.8% 5.0%

Japan (4.1) 0.7% -5.0% 2.5%

Factors determining global recovery in 2021

S. Kor (1.7) 2.0% -1.5% 3.4%

1• Development of vaccine and higher efficacy rate

India (7.1) 4.2% -9.3% 9.5%

2• Government stimulus to be implemented in early 2021

China (17.4) 6.1% 2.0% 8.3%

3• Future trade volume and FDI are expected to remain slow

ASEAN-5 4.9% -4.5% 5.8%

4• Increasing business bankruptcies and elevated

unemployment are expected

Source: EIC analysis based on data from IMF WEO (October 2020)

26Global economic projection

Global recovery in 2021 is expected to be gradual as future trade volume and FDI are expected to remain

slow, business bankruptcies may continue to rise, and unemployment is expected to stay elevated.

Global trade volume, Outward FDI, and world GDP growth Growth and business bankruptcies Unemployment rate, by WEO

Unit : %YOY Unit : %

Global trade volume (IMF; goods and services)

15 60

China

Global outward FDI (UNCTAD) rhs 3.64.2

IMF 2021f = 8.3%

10 40 Korea 3.64.1

5 20 Japan 3

2.8

UK 4.8

0 0 7.4

Euro Area 8.3

-5 -20 9.1

US

5.5 6.9

-10 -40

0 2 4 6 8 10

IMF 2020f = -10.4%

-15 -60 2019 2020F 2021F

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

• IMF projected global trade volume to decline by -10.4% • Bankruptcies are higher in years when • Unemployment rate is expected to remain

in 2020 to reflect weaker demand across the world, real GDP growth is low, as firms’ high across both AE and EM.

trade restriction, and supply chain disruptions. revenues decline. • Lower labor force participation is expected

• Expect shifts in supply chain as firms re-shore their • BIS forecasts bankruptcies across AEs to continue following the exit of

productions to reduce risks from reliance on foreign to increase by 19–55% in 2020 and by discouraged workers. Resource mismatches

producers. an average of about 20% by 2021. could have impacts on productivity.

Source: EIC analysis based on data from IMF WEO (October 2020), Fed (for US unemployment rate 2021), World Bank, BIS

27Tourism

EIC revises up 2021F foreign tourists slightly from 8.4 to 10.4 million to reflect positive news about vaccine

efficacy. However, most of tourists will be in H2 and the outlook remains highly uncertain.

Foreign tourist arrivals Factors to monitor for foreign tourism in 2021

Unit: million

+ Supporting factors

2020 forecast 2021 forecast • Vaccine(s) likely to get approval for general use

8 6.7 million tourists 10.4 million tourists in Q1/21

• Rising tourism demand in H2/21 after

7 6.7 widespread vaccination in the US, UK, EU during

5.9 H1/21; have time to plan trips in H2

6 Old Current • Low local infection and effective containment

Vaccine(s) 5.3

Approved • Long-stay tourists from Special Tourist Visa (STV)

5

for general use scheme likely to increase in number

In Thailand

4

Vaccine(s) 2.9 - Challenges & Risks

3 Approved

2.0 • Lower purchasing power among potential tourists

for general use

2 In DM due to global recession

1.1 • intense competition from other top destinations

1 0.8

0.4 0.5 • Higher costs for commercial flights

0.0 0.0 0.0 • Sentiments among Thai public with regards to

0

Q1/20 Q2/20 Q3/20 Q4/20 Q1/21 Q2/21 Q3/21 Q4/21 opening to foreign tourists before widespread

vaccinations in Thailand

• Vaccine uncertainty: deep-freeze logistics,

• Tourists from Asia and Oceania will kick off the recovery, followed by EU and US tourists duration of how long immunogenicity will last

• Share of younger and FIT tourists will rise at the beginning of recovery • Political unrest

Source: EIC analysis based on data from Ministry of Tourism & Sports

28Exports

Thai exports sector is predicted to slowly recover in 2021, following weak global trade projection and

low proportion of products that are on global demand (electronics).

WTO expects global trade WTO World merchandise trade volume Export value forecast (USD, BOP basis)

volume to recover slowly, Unit : Index (2015 = 100) Unit : %YOY

shrinking by -9.2% in 2020 120 9.5% 7.5%

5.3%

and then expanding only

100

7.2% in 2021 due to:

• Global trade recovery 80

tend to slow again after -3.3%

pent up demand has 60 -8.0%

expired, following the 40

slow recovery of global 2017 2018 2019 2020f 2021f

economy that still has Good prospect

various risk factors. • Food & Beverage (Necessity products for daily livings)

• Protectionism trend that Unit : %YOY • Electronics related to data center/cloud

began to increase in 2020 • Health & wellness products

10

many countries, which 7.2

2021 • Oil price related products benefit from higher crude price (EIC expects

may affect the world 5 Brent to avg. 49.5 in 2021 vs 42 USD/Brl in 2020)

trade conditions

• The risk of global trade is Sluggish

0

still high if COVID-19 • Automotive and related products - durable goods is expected to slowly

resurgences occur. recover, affecting to other products in supply chain such as rubber

-5

sheet, tire

• Electricals – slow global recovery would bring about sluggish demand

-10 -9.2

in electrical appliances

Source: EIC analysis based on data from WTO and BOT

29Thai baht

THB appreciation since end-Oct 2020 has outpaced other regional currencies. The appreciation was a

result of USD weakness and improved investors’ confidence. EIC expects 29.5-30.5 THB/USD by end 2021.

Change in regional exchange rates against US dollar

Unit: % (data as of 17 Nov 2020)

USD is expected to weaken due to the following

8%

4.1% 3.3%

2.6% 2.1% 1.8% 1. Global economic recovery

3% 1.2% 0.5% 0.3% 0.2% 0.1%

-2% 2. US fiscal deficit and lower trade uncertainty

-1.5% -0.5%-1.5%

-7% YTD Since end of October 3. Relatively low rate of return (carry) from USD.

Thailand

Europe

Malaysia

Taiwan

Japan

India

USD index

Indonesia

South korea

China

Philippines

Vietnam

Other factors contributing to THB appreciation

USDTHB, NEER, and Dollar index 1. CA surplus and low money recycling abroad

Unit: index (data as of 17 Nov 2020) Unit: baht per USD 2. Capital inflows to EM, including Thailand thanks to

NEER THB/USD 27 positive news on vaccine, net EM bond issuance, and

155 Since Jan 2014 18.7% 9.5%

30.2 rapid economic recovery in China

2020YTD -4.3% -1.5%

135 31

Since end of Oct 2020 - 3.3% 121.2

115 Weakening factors for THB

95 35

NEER THB/USD (rhs) 1. Worse-than-expected global economy

75

2. Delay of vaccine distribution

2014

2015

2016

2017

2018

2019

2020

3. Stumble Thai economic recovery or Thai political unrest

Source: EIC analysis based on data from Bloomberg, SET, and Thai BMA.

30Thai baht

Consistent and sustained Baht appreciation resulted from 1) high CA surplus and 2) home bias of investment.

Recent BOT’s measures to relax outflows restriction will help reduce Baht pressure in the long run, but likely

have limited impacts in the short run.

Current account to GDP and NEER International assets to GDP in 2019

Unit: % to GDP

25% 1200% Reserve Direct investment Portfolio Others* 1135%

Change in NEER from Jan 2014 to August 2020

= Appreciation

20% Thailand 1000%

Switzerland

15% 772%

800%

Japan

10%

600% 516%

Singapore

5% Korea

400%

Philippines 255% 275%

0% Germany 198%

Indonesia 200% 152%

-5% India 99% 103% 119%

33% 52%

Australia 0%

-10% United 35% 45% 41% 24% 24% 3% 13% 2% 2% 1% 16% 7%

Kingdom Canada Malaysia

Australia

Malaysia

Canada

Thailand

Korea

Japan

UK

Singapore

Germany

Switzerlan

Indonesia

Philippines

-15%

New Zealand

d

-20%

-7% -2% 3% 8% 13% 18%

Blue figures refer to percent of reserves to total international asset

Average current account to GDP from Jan 2014 to Aug 2020 *Financial derivatives (other than reserves) and employee stock options

Source: EIC analysis based on data from BIS, and IMF

31Scarring effects

3 Scarring effects to limit 2021 Thailand economic growth

These 3 effects also have feedback impacts on each other, thus create higher negative pressure on economic growth ahead

1 Worsened business 2 Slow labor market recovery

High unemployment and lower work

3 Balance sheet restoration

Both businesses and HH need to

dynamics

Less entry and higher exit of hours imply lower income. Job recovery restore their b/s. This will in turn

firms leads to lower employment is expected to be slow due to lead to sluggish spending and new

and low investment growth deteriorated business financial position loan growth

Firm closures lead to more unemployment Lower income and higher debt

Lower HH income slows spending which hurts firms Business deleveraging limits new employment

HH & Business deleveraging and higher presence of zombie firms limits new spending & investment as well as efficient resource reallocation

Expected impact to the economy

Slower productivity growth

Sluggish job and Higher market

and lower potential long-

economic recovery concentration

term growth

32Scarring effects

1

For the first 10 months of 2020, business dynamics worsened as firm entry dropped and firm exit rose.

Newly-registered firms Change in newly-registered and dissolved firm during 10M/20

Unit: firms Unit: %YOY

2018 2019 2020

8,000 Newly-registered firms Firms dissolved

6,000 EE -23.3% 27.3%

Auto -31.1% 25.8%

4,000 Number of new firms dropped

again after a short recovery. Restaurant -14.1% 21.6%

2,000

Manu - other -23.6% 18.9%

Lower number reflects worse situation

0 Service - other -6.4% 9.9%

jan feb mar apr may jun jul aug sep oct nov dec

Total -12.3% 7.7%

WR -10.5% 7.6%

Firms dissolved

Real-estate -21.6% 4.8%

Unit: firms

Number of firms dissolved Hotel-37.8% 4.5%

4,000 Higher number reflects worse situation increased 34.8%YOY Petchem -10.5% 3.2%

during Sep-Oct

3,000 Contruction -14.6% 1.5%

2,000 FB -26.1% -13.4%

1,000 Agri -16.2% -21.2%

0

jan feb mar apr may jun jul aug sep oct nov dec

Source : EIC analysis based on data from DBD

33Scarring effects

2

Unemployment rate rose again in Oct’20 while work hours remained poor compared to pre-Covid despite

some improvement. Uncertainty remains high; unemployment rate could still rise as more firms go out of

business.

Unemployment rate No. of employed persons by hours worked

Change in job type reflects higher business closures and

Unit: % of labor force Unit: million Unit: %YOY

more informal works which tend to earn lower income.

workers with 0 work hrs (furlough) workers with 1-34 work hrs

Total unemployment 4.4%

(NSO survey) 3.9% %YOY of both (RHS)

Unemployment under 3.7% 12 100% %change in Oct’20

social security system

68.7% Job type

10 48.1% 43.4% from Mar ‘20

2.5

0.6

2.8% 8 29.8% 50%

0.4

19.7%

0.3

0.7

0.4

0.4

0.3

0.4

0.4

6

0.5

2.2%

4 0%

Employer (2.2% of total

1.5% 1.4% 2 employment) -1.1%

6.4

6.0

5.8

6.0

6.3

8.2

7.6

6.8

7.4

7.1

6.2

2.1% 1.3% 2.0%

2.1% 2.1% • income = 22.6k THB/month

1.9% 1.8% 0 -50%

full-time workers OT workers %YOY of both (RHS)

0.9% 1.0% 1.0% Self-employed (48.3% of total

40

35 -2.5% -1.6% -0.6% 5% employment) +3.3%

-3.3%

Peak pre-COVID

Q1/20

Q2/20

Aug 2020

Avg. 2013-18

Oct 2020

Jul 2020

Sep 2020

2019

30 0% • income = 11.6k THB/month

-6.9% -6.0%

25 -5%

20 22.3

-10%

23.9

15

22.6

23.2

22.5

24.7

23.4

Employee (31.9% of total

24.8

24.1

24.6

22.4

10 -15%

5 -15.2% -2.4%

9.7

8.6

employment)

8.1

7.8

7.4

7.3

0 -20%

2020Q2 6.0

Oct-20 5.8

Aug-20 5.7

Sep-20 5.5

Jul-204.5

• income = 14.2k THB/month

2015

2016

2017

2018

2019

2020Q1

*income by job type is from SES data

Unemployed persons (NSO), Oct = 810k

- Youth group (age 15-24y) registered

highest unemployment rate at 8.9% Labor market continued to worsen (underemployment rose and

Unemployed persons (SSO), Sep = 488k higher-hour jobs dropped) but the rate of change slowly improved.

Source : EIC analysis based on data from NSO and SSO

34Scarring effects

3

HH debt to GDP in Q2/20 made its record high as GDP plummeted despite the slowdown in outstanding

debt. Thailand’s HH debt ratio is the highest among EM countries, and would reach the threshold that could

impede growth significantly. Elevated debt overhang will require HH to deleverage and repair its B/S.

HH debt to GDP (BOT) & HH debt to income (NSO) HH debt to GDP and GDP per capita by country

Unit : % of GDP (BOT), % of HH income (NSO) Unit : % of GDP

Covid shock to income 160

110%

will likely make the

98.5% Thailand’s HH debt ratio is the highest

96.1% ratio exceed 100%

Household debt to GDP (%, Q1/20)

100% 140 among EM countries.

88.3% 87.1% CHE

90% 83.2%

80.3% 120 AUS

88.1%

80% 83.8% DNK

81.2% 79.9% 80.1% CAN NLD NOR

78.1% 100 KOR

70% 76.6%

NZL

THA (BOT-Q2/20) GBP SWE

60% 66.2%

80 HKG

THA (BOT-Q1/20) USA

57.9%

50% MYS

60 JPN

40% %growth 2009-18 2019 Q1/20 Q2/20 EMU

HH debt 9.7% 5.1% 3.9% 3.8% 40 ZAF

30% BRA POL IRL

GDP 6.0% 3.1% 1.7% -2.8% CZE

20%

20 IDNCOLRUS

HUN

2020Q2

2009

2011

2013

2015

2017

2019

2020Q1

end-20 (F)

SAU High income countries

TUR MEX

IND ARG Non-high-income countries

0

0 20,000 40,000 60,000 80,000 100,000

GDP per capita (USD, 2019)

Source : EIC analysis based on data from BOT, NESDC, NSO, BIS, IMF, and World Bank

35Summary

EIC forecasts 2021 Thai GDP to expand by 3.8% with slow and uneven recovery, resulting from slow global

growth and more material domestic scarring effects.

2020f 2021f

Unit

Previous Now Previous Now

GDP %YOY -7.8 -6.5 3.5 3.8 2021 Risk Factors

Private Consumption %YOY -2.3 -1.1 1.9 2.0

Public Consumption %YOY 2.2 2.3 2.4 3.3 Larger & more

COVID-resurgence &

Private Investment %YOY -12.6 -10.9 4.7 4.7 effective stimulus

delay of vaccine

measures than

Public Investment %YOY 8.3 11.5 8.9 9.8 approval/ distribution

expected

Exports of Goods & Services %YOY -19.8 -20.5 6.5 7.9

Imports of Goods & Services %YOY -14.3 -15.5 5.7 8.1

Widespread

Slower global

Export values (USD, BOP) %YOY -8.0 -8.0 4.9 5.3 bankruptcies / NPL

growth hurting

Import values (USD, BOP) %YOY -15.0 -14.2 6.3 8.6 leading to higher UR

exports sector

and credit crunch

million 6.7 6.7 8.4 10.4

Number of foreign tourists

%YOY -83.1 -83.2 25.0 55.4

Political instability

Headline Inflation %YOY -0.8 -0.9 0.9 0.9

Delay in tourism affecting domestic

Core Inflation %YOY 0.3 0.3 0.2 0.3 recovery demand and foreign

Brent USD/Brl. 41.2 41.2 49.5 49.8 investor’s confidence

Policy rate (end-period) % 0.50 0.50 0.50 0.50

Source : EIC analysis

36Summary

Although we revise GDP growth upwardly for 2020 and 2021, Thai economy would still have a gradual

recovery with challenges from scarring effects, while risks turned more balanced.

Thailand’s real GDP level

Unit: Index, Q4/19 = 100 4Q GDP get back

%YOY 2020E 2021F 2022F

to 2019 level

Current Base Better Worse

106

Better -6.2 4.9 4.3 2021Q3-2022Q2

104

Base -6.5 3.8 3.6 2022Q1-Q4

102

Worse -7.1 1.8 2.7 2023Q1-Q4

100

98

96 Assumptions

94 Better – no major recurrence, vaccine is found in Q4/2020 and

widely available in TH by H1/2021

92 Base -- Vaccine is found in Q1/2021 and available in TH by

90 H2/2021. Rises in NPL, but with relatively orderly financial

adjustment.

88

Worse – New outbreak in Q4/2020 and 2021, vaccine is found in

86 H2/2021 & severe scarring effects leading to financial stress, sharp

2018Q1

2018Q2

2018Q3

2018Q4

2019Q1

2019Q2

2019Q4

2020Q1

2020Q2

2020Q3

2020Q4

2021Q1

2021Q3

2021Q4

2022Q1

2022Q2

2022Q3

2022Q4

2019Q3

2021Q2

fall in demand & credit crunch.

Source: EIC analysis

37Policy Recommendations

& Business Strategy

38Key events in 2020:

The passing of the baton in tech leadership and the geopolitical frontline of the future

39Lower supply of labor and skill gaps from technology disruption are exacerbating the global talent

shortage resulting in increasing unrealized output over the next 10 years.

Total global labor deficit as a % of Total global labor deficit as a % of

workforce 2020 workforce 2030 Talent deficit in Asia Pacific

Unit: % Labor deficit Unit: %

Labor deficit

3% 11%

Global unrealized Global unrealized

output due to labor output due to labor

deficit deficit

$2.1 trillion USD $8.5 trillion USD

97% 89%

Workforce Workforce The acuteness of an

economy’s deficit is based the

The forecast accounts for demographic, migration into and out of the country, labor- absolute number of worker

shortage

force participation rate, education levels of the population and industry demand.

Note: Calculation based on three knowledge intensive sectors: Financial and business services, Technology, media, and telecommunications, and Manufacturing

Source: Korn Ferry

40COVID-19 has propelled talent to the top risk for many businesses. Since the pandemic, CEOs ranked

talent as the most significant threat to their businesses up 10 places from January.

In the context of COVID-19 losing key employees and attracting specialized talent can have critical impact on growth. New digital talents are needed to

meet changing customer behaviors and needs. In addition many leadership teams are concerned about the mental and physical wellbeing of their staff.

Greatest risk to growth Jul/Aug 2020 Greatest risk to growth Jan/Feb 2020

Unit: % of respondent Unit: % of respondent

Talent risk 21 Environmental/climate change risk 22

Supply chain risk 18 Return to territorialism 19

Return to territorialism 14 Cyber security Risk 15

Environmental/climate change risk 12 Emerging/disruptive technology risk 11

Cyber security Risk 10 Operational risk 11

Emerging/disruptive technology risk 7 Regulatory risk 8

Operational risk 5 Reputational risk 6

Regulatory risk 5 Interest rate risk 3

Tax risk 4 Supply chain risk 2

Interest rate risk 2 Tax risk 2

Reputational risk 2 Internal unethical culture risk 1

Internal unethical culture risk 1 Talent risk 1

Note: Responses from 1,300 CEOs in Jan/Feb 2020; 315 CEOs in Jul/Aug 2020 globally

Source: EIC analysis based on data from KPMG 2020 CEO Outlook COVID-19 Special Edition

41Perception on firms’ ability to adopt new technology has held steady for the past 3 years;

however, ranking has slipped in multiple dimensions

Perception toward firms’ technology adoption effort Perception toward firms’ technology adoption effort

Unit: Survey score 0-10 (best) Unit: rank (63 countries in 2020)

2018 2019 2020 2018 2019 2020

Companies are very

Companies are very good at using digital

good at using digital tools

tools 0

10

10

8 5.7

Digital transformation 20

Digital transformation 6

in companies is 4

in companies is 30 39

Companies are agile Companies are agile

generally well 5.9 5.9 generally well 29 40 36

2 implemented

implemented 0 50

35

34

Flexibility and 5.0 Companies are very Flexibility and Companies are very

6.8

adaptability of people good at using big data adaptability of people good at using big data

are high when faced to support decision- are high when faced to support decision-

with new challenges making with new challenges making

Source: EIC analysis based on data from IMD

42Based on international standards, Thai entrepreneurs assessed that the efficiency of large

businesses is quite high. However, the efficiency of SMEs is relatively low.

Large corporations are efficient by international standards SMEs are efficient by international standards

Unit: Survey score 0-10 (best) Unit: rank (63 countries in 2020) Unit: Survey score 0-10 (best) Unit: rank (63 countries in 2020)

10 0 10 0

Score Ranking (rhs) Score Ranking (rhs)

9 9

15 10 10

8 8

7 20 7 20

6 6

5 30 5 30

4 4

40 40

3 3

50

2 50 2 50

1 1

60 60

0 0

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Source : EIC analysis based on data from IMD

43An improvement in education and labor market score has been sluggish. As a result, Thailand

is ranked at a bottom half in this area.

Education system and labor market Education system and labor market

Unit: score 0-10 (best) Unit: rank (63 countries in 2020)

2010 2015 2020 2010 2015 2020

The educational system The educational system

meets the needs of a meets the needs of a

competitive economy* competitive economy*

10 0

8 10

6 4.5 20

Management education Attracting and Management education 30 46 Attracting and retaining

meets the needs of the 6.4 4 meets the needs of the 40 talents is a priority in

2 7.0 retaining talents is a 27

business community priority in companies business community 50 companies

0 34 60

47

University education 6.0 5.0 Language skills are University education 38 Language skills are

meets the needs of a meeting the needs of meets the needs of a meeting the needs of

competitive economy enterprises competitive economy enterprises

Note: * Use data 2018 instead of 2020.

Source: EIC analysis based on data from IMD

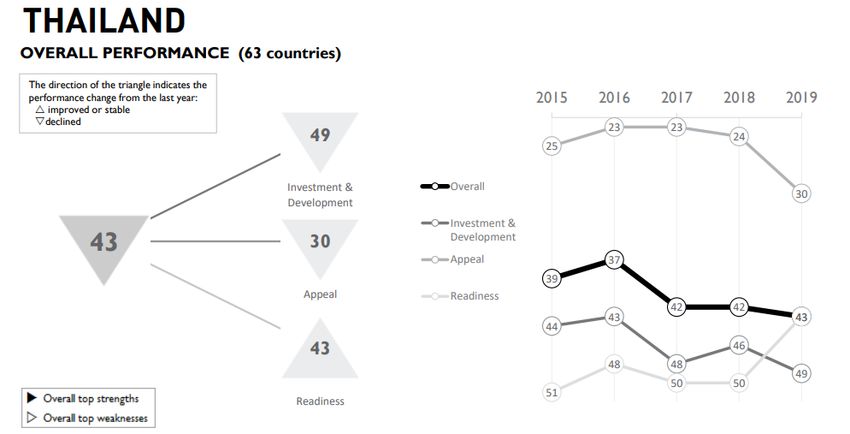

44Thailand stands at 43rd (out of 63 countries) in IMD’s World Talent Ranking 2019, lower from the

previous year as ranks for Appeal and Investment & Development dropped.

World’s Best 2019

Appeal Switzerland

Overall, Switzerland

Readiness Singapore

Investment &

Denmark

Development

Source: IMD

45Winning the future will require digital-first strategy & talent development through public-

private collaboration

Focus Area Actions for Private Sector Leaders Actions for Public Sector Leaders

• Deploy productivity-boosting technology -

Enhance productivity • Build digital infrastructure

digitize processes and focus on analytics

• Raise digital capabilities in companies esp. for SMEs

through digital • Adopt technology to manage supply chain (e.g.

• Digitalize government processes to encourage adoption by

technology and blockchain) and increase agility (e.g. 3D printing)

companies and citizens

infrastructure • Install new-normal working model designed for

• Ensure data privacy, security, ownership and interoperability

speed (flatter, more flexible, and agile)

• Compile skill gap map to facilitate training & job matching

• Drive national reskilling and lifelong learning program (e.g.

• Leverage strategic workforce planning Singapore’s SkillsFuture, EU’s Upskilling Pathways)

• Develop targeted Upskill/Reskill on a large scale • Reform curriculum by collaborating with employers and global

Invest in reskilling • Align education curricula with skills needs leaders as well as support teacher’s training

• Transform culture and org. structure to attract • Attract foreign talents with clear plan and accountability

& keep talent as well as promote lifelong learning • Improve social support program to address changing needs

e.g. worker job transition program, social safety net for gig

workers & independent contractors

Source: EIC analysis based on data from Moody’s, McKinsey, EU, BCG

46Singapore Adapt and Grow Initiative: An initiative by Workforce Singapore, a private-public partnership, launched in 2016 to help Singaporeans adapt to changing job demands, re-skill for new careers, and stay agile for new opportunities. Source: Workforce Singapore 47

Survey results from people aged 15-35 years found that 31% of Thai people think current knowledge

and skills will last a lifetime, the most in ASEAN.

Survey of knowledge and skills

Unit: %

100%

7%

my current education and skill are already

8% 11% 9% 9% 9%

90%

13% out-of-date

80%

70% 43%

50% 44% 52% 52%

my current education and skill will need to be

53%

60% constantly updated

69%

50%

14%

40% my current education and skill will last for 5y

15% 17% 5% 14%

before I need to retrain

30% 16% 20%

7% 7% my current education and skill will last for

20% 6%

6% 8% 31%

8% another 10y before I need to retain

10% 21% 4%

14%

19%

11%

19% my current education and skill will last for

10%

0% most of my life

Indonesia Malaysia Phiippines Singapore Thailand Vietnam Asean

Source: WEF and Sea group

48“Live as if you were to die tomorrow.

Learn as if you were to live forever”

Mahatma GandhiDisclaimer

The information contained in this report has been Any opinions presented herein represent our

obtained from sources believed to be reliable. subjective views and our current estimates and

However, neither we nor any of our respective judgments based on various assumptions that

affiliates, employees or representatives make any may be subject to change without notice, and may

representation or warranty, express or implied, as not prove to be correct.

to the accuracy or completeness of any of the

information contained in this report, and we and This report is for the recipient’s information only.

our respective affiliates, employees or It does not represent or constitute any advice,

representatives expressly disclaim any and all offer, recommendation, or solicitation by us and

liability relating to or resulting from the use of this should not be relied upon as such. We, or any of

report or such information by the recipient or other our associates, may also have an interest in the

persons in whatever manner. companies mentioned herein.You can also read