DWS ON TOUR RENTA VARIABLE ! NO HAY ALTERNATIVA ! TINA - THERE IS NO ALTERNATIVE TO EQUITIES

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

DWS ON TOUR RENTA VARIABLE ………! NO HAY ALTERNATIVA ! TINA – THERE IS NO ALTERNATIVE TO EQUITIES Irene López | 11 de Febrero 2020 Barcelona For Professional Clients MiFID Directive 2014/65/EU Annex II) only. No distribution to private/retail investors. For Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)). For institutional investors only. Further distribution of this material is strictly prohibited. APAC Australia: For professional clients only.

“La Vida Comienza Donde Termina Tu Zona De Confort”

Neale Donald Walsh

“El Cambio Tiene 3 Etapas:

En La Primera, Es Imposible

En La Segunda, Es Improbable

En La Tercera, Es Inevitable”

Barak Obama

CIO VIEW 2020 For Professional Clients MiFID Directive 2014/65/EU Annex II) only. No distribution to private/retail investors. For Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)). For institutional investors only. Further distribution of this material is strictly prohibited. APAC Australia: For professional clients only.

GLOBAL ECONOMY

Not too fast – not too slow – growth is stabilizing through EM

UNITED STATES EUROZONE CHINA EMERGING MARKETS

60%

Share of

global

6.2% GDP1

5.8%

4.2% 4.4%

2.2%

1.6%

1.1% 0.9%

2019 F 2020 F 2019 F 2020 F 2019 F 2020 F 2019 F 2020 F

2020: SLOWDOWN 2020: STABILIZATION 2020: SLOWDOWN 2020: RECOVERY

↓ Impact of tax cuts fading ↓ Expected trough in exports ↓ Various trade-conflict effects ↓ Idiosyncratic risks2

/ manufacturing

↓ Economy-wide corporate ↓ High debt prevents more ↑ Fiscal / monetary support &

profits (NIPA) decreasing ↑ Fiscal stimulus in Germany monetary stimulus less dependency on the U.S.

3.1% 3.1%

2020: NO GLOBAL RECESSION EXPECTED

WORLD

↓ Economic policy uncertainty weighs on global economic decisions,

2019 F 2020 F emerging-markets recovery stabilizes

F = DWS forecast 1) IMF World Economic Outlook as of December 2019 2) In Brazil, Argentina, Chile / Forecasts are not a reliable indicator of future returns. Forecasts are based on assumptions, estimates,

opinions and hypothetical models or analysis which may prove to be incorrect. Sources: International Monetary Fund, DWS Investment GmbH as of December 2019

CIO View / Stefan Kreuzkamp / January 2020 /4

GLOBAL ECONOMY

Manufacturing dismal – service sector still keeping up its mood

PURCHASING MANAGERS‘ INDICES (PMI)

Composite Manufacturing Service

Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19

World 51.2 51.6 51.3 51.1 50.8 51.4 51.7 49.4 49.3 49.5 49.7 49.8 50.3 50.1 51.9 52.5 51.8 51.4 51.0 51.6 52.1

United States 51.5 52.6 50.7 51.0 50.9 52.0 52.7 50.6 50.4 50.3 51.1 51.3 52.6 52.4 51.5 53.0 50.7 50.9 50.6 51.6 52.8

Eurozone 52.2 51.5 51.9 50.1 50.6 50.6 50.9 47.6 46.5 47.0 45.7 45.9 46.9 46.3 53.6 53.2 53.5 51.6 52.2 51.9 52.8

France 52.7 51.9 52.9 50.8 52.6 52.1 52.0 51.9 49.7 51.1 50.1 50.7 51.7 50.4 52.9 52.6 53.4 51.1 52.9 52.2 52.4

Germany 52.6 50.9 51.7 48.5 48.9 49.4 50.2 45.0 43.2 43.5 41.7 42.1 44.1 43.7 55.8 54.5 54.8 51.4 51.6 51.7 52.9

United Kingdom 49.7 50.7 50.2 49.3 50.0 49.3 49.3 48.0 48.0 47.4 48.3 49.6 48.9 47.5 50.2 51.4 50.6 49.5 50.0 49.3 50.0

Japan 50.8 50.6 51.9 51.5 49.1 49.8 48.6 49.3 49.4 49.3 48.9 48.4 48.9 48.4 51.9 51.8 53.3 52.8 49.7 50.3 49.4

Spain 52.1 51.7 52.6 51.7 51.2 51.9 52.7 47.9 48.2 48.8 47.7 46.8 47.5 47.4 53.6 52.9 54.3 53.3 52.7 53.2 54.9

Italy 50.1 51.0 50.3 50.6 50.8 49.6 49.3 48.4 48.5 48.7 47.8 47.7 47.6 46.2 50.5 51.7 50.6 51.4 52.2 50.4 51.1

Brazil 49.0 51.6 51.9 52.5 51.8 51.8 50.9 51.0 49.9 52.5 53.4 52.2 52.9 50.2 48.2 52.2 51.4 51.8 51.2 50.9 51.0

Russia 49.2 50.2 51.5 51.4 53.3 52.9 51.8 48.6 49.3 49.1 46.3 47.2 45.6 47.5 49.7 50.4 52.1 53.6 55.8 55.6 53.1

China 50.6 50.9 51.6 51.9 52.0 53.2 52.6 49.4 49.9 50.4 51.4 51.7 51.8 51.5 52.0 51.6 52.1 51.3 51.1 53.5 52.5

India 50.8 53.9 52.6 49.8 49.6 52.7 53.7 52.1 52.5 51.4 51.4 50.6 51.2 52.7 49.6 53.8 52.4 48.7 49.2 52.7 53.3

South Korea 47.5 47.3 49.0 48.0 48.4 49.4 50.1

Taiwan 45.5 48.1 47.9 50.0 49.8 49.8 50.8

Turkey 47.9 46.7 48.0 50.0 49.0 49.5 49.5

>50 and increasing 50 and falling or unchanged

CENTRAL BANKS

Reacted to slowing economies and will stay accommodative

CENTRAL BANKS AGAIN IN CUTTING MODE 2020F: EASING BIAS BUT CB POLICY REACHING ITS LIMITS

Net number of interest rate moves, rolling 3-months average1

20

ECB MONETARY STIMULUS

15 _ QE extension (€20bn. volume/month)

_ Policy rates on hold, no cut in 2020 expected

10

5 TIERING SYSTEM

_ Two-tired system, exempting part of banks´

0 excess liquidity from negative deposit rate

-5

-10

FED MONETARY STIMULUS

-15

_ Pause after successful "insurance cuts" cycle

-20

_ On hold, no cut in 2020 expected

-25

BALANCE-SHEET EXPANSION

-30

_ Treasury-bill purchases with $60bn. at least into

2009 2011 2013 2015 2017 2019 Q2 2020 (not QE, liquidity injection)

G10 central banks Emerging-Markets central banks

1) Moving average of 3-months change in interest rates / Past performance is not a reliable indicator of future returns. Forecasts are not a reliable indicator of future returns. Forecasts are based on

assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect. Sources: Bloomberg Finance L.P., DWS Investment GmbH as of December 2019

CIO View / Stefan Kreuzkamp / January 2020 /6FISCAL STIMULUS IN EUROPE

Not much to be expected

DEBT-TO-GDP RATIOS ACROSS EU COUNTRIES

In % of GDP, 2019 GERMANY 2020 & BEYOND

133% _ Fiscal policy already supportive due to income tax relief,

99% 96% social security spending, and increased child benefits

86%

59% _ Plans to abolish the solidarity surcharge

Germany UK France Spain Italy SELF-IMPOSED RESTRICTIONS IN GERMANY

GERMANY ALREADY GENEROUS BY ITS STANDARDS _ Debt brake (constitution)

Fiscal impulse (EU Commission estimate), % of potential GDP _ Commitment not to run a public-sector deficit ("black

1.0 zero") is part of the coalition treaty

Forecast1

0.5

0.0

-0.5 LIMITED GROWTH IMPACT

-1.0 _ Not a real impulse that boosts private sector activity

-1.5 _ German households tend to save additional income

-2.0

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

1) Forecast EU Commission / Past performance is not a reliable indicator of future returns. Forecasts are not a reliable indicator of future returns. Forecasts are based on assumptions, estimates, opinions and

hypothetical models or analysis which may prove to be incorrect. Sources: International Monetary Fund, EU Commission, DWS Investment GmbH as of December 2019

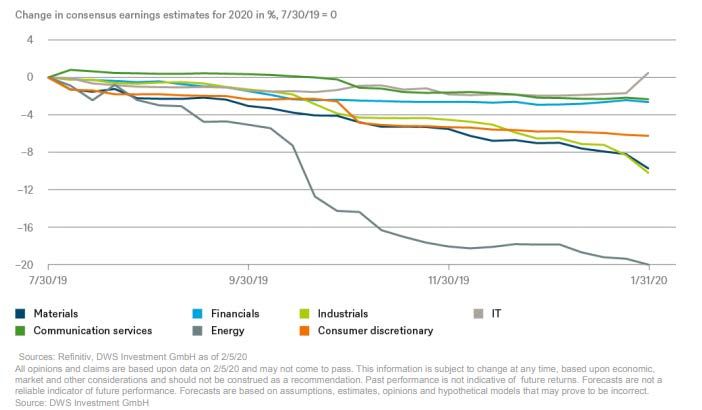

CIO View / Stefan Kreuzkamp / January 2020 /7HOW CONTAGIOUS ARE EARNINGS ESTIMATES? Change in consensus earnings estimates for 2020 Name of speaker / Name of event / Date /8

OUTLOOK 2020

Risks and opportunities

RISKS OPPORTUNITIES

PRESIDENTIAL ELECTION LOW INTEREST RATE ENVIRONMENT

Tax reform at risk: downside potential for Ongoing allocation shifts due to low or

equities negative rates

CAPITAL FLOWS

VALUATION SPREADS

Inflows in passive and active investment

Bullish sentiment, huge valuation spreads

funds as well as share buy backs

GEOPOLITICAL RISKS

LOW VOLATILITY

Middle East, Iran, Russia, Turkey gaining

Low volatility in almost every asset class

influence

RATES & INFLATION

Rise in capital market rates due to

accelerating inflation

As of: December 2019; Source: DWS International GmbH

/9OUTLOOK 2020

Peak pessimism behind us – 2020 could surprise positively

ECONOMY INFLATION CENTRAL BANKS POLITICS

Growth slowdown in DM, Close, but below CB target Globally in easing mode Tariff agreement expected

recovery in EM No inflation overshoot ECB & Fed on hold Less uncertainty from

No recession European politics

EQUITIES FIXED INCOME CURRENCIES ALTERNATIVES

Higher EPS growth Low for longer EUR/USD continue Illiquidity premium

Europe with upside potential Focus on Asian bonds sideways trading

JPY as hedge

ESG

Smart Integration of ESG criteria into the investment process

Forecasts are not a reliable indicator of future returns. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

Source: DWS Investment GmbH as of December 2019

CIO View / Stefan Kreuzkamp / January 2020 / 10ESG – THE REGULATORY PERSPECTIVE

Regulation is affecting investment management

EU COMMISSION TCFD EU COMMISSION EU COMMISSION

TASK FORCE ON

CLIMATE-RELATED

TCFD FINANCIAL

DISCLOSURES

SRD II1 GOVERNANCE & DISCLOSURE REGULATION SUSTAINABILITY IN THE

_ Requirement to report & MANAGEMENT AROUND _ Processes and policies for INVESTMENT ADVICE

track engagement activities CLIMATE-RELATED RISKS reducing sustainability risks _ Consistent product

_ Reporting to become classification based on

BaFin mandatory for PRI signatories MiFID II target market

Bundesanstalt für EU TAXONOMY

Finanzleistungsaufsicht

_ Definition of economic

BULLETIN ON INTEGRATING activities with substantial

SUSTAINABILITY RISK contribution to climate change

_ "Good practices" on

integrating sustainability risks

across the value chain

Q4 2019 Q1 2020 Q1 2021 Q4 2021 & 2022

1) Shareholder Rights Directive II / Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

Source: DWS Investment GmbH as of December 2019

CIO View / Stefan Kreuzkamp / January 2020 / 11SOLUCIONES DWS 2020 For Professional Clients MiFID Directive 2014/65/EU Annex II) only. No distribution to private/retail investors. For Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)). For institutional investors only. Further distribution of this material is strictly prohibited. APAC Australia: For professional clients only.

RENTA VARIABLE

TINA (THERE IS NO ALTERNATIVE) …. NO HAY ALTERNATIVA

MULTIACTIVO

VALUE GROWTH

DEFENSIVO CÍCLICO

ESG DIGITALIZACIÓNSOLUCIONES 2020

Investment opportunities based on sustainable growth drivers

MULTIACTIVO TEMÁTICOS

DWS Concept Kaldemorgen Industria 4.0

DWS Invest Smart Tech Industrials

Infraestructuras

DWS Invest Global Infrastructure

INCOME

DWS Invest Top Dividend Nutrición, Demografía &

Hábitos de Consumo

DWS Invest ESG Global DWS Invest

Equity Income

2020 Global Agribusiness

ESG

ALEMANIA

DWS Invest German Equities Cambio Climático & Escasez de

Recursos

DWS Deutschland

DWS Invest Climate Tech

Integración ESG & Impacto Positivo

As of: December 2019; source: DWS Investment GmbH

DWS Invest SDG Global Equities

/ 14DWS CONCEPT KALDEMORGEN CONVIRTIENDO VOLATILIDAD EN OPORTUNIDAD For Professional Clients MiFID Directive 2014/65/EU Annex II) only. No distribution to private/retail investors. For Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)). For institutional investors only. Further distribution of this material is strictly prohibited. APAC Australia: For professional clients only.

DWS CONCEPT KALDEMORGEN

Performance since inception

PERFORMANCE IN EUR SINCE INCEPTION (MAY 2, 2011)

(02.05.2011 = 100 points)

170 + 61.5%

160 (5.7% p.a.)

Vol.: 5.4%

150

140 2019

+ 12.8%

130

120

110

100

90

May-11 May-12 May-13 May-14 May-15 May-16 May-17 May-18 May-19

DWS Concept Kaldemorgen FC

Past performance is not a reliable indicator of future returns.

As of: End of December, 2019; Source: DWS International GmbH, daily figures

/ 16DWS CONCEPT KALDEMORGEN

Competitive Edge

FLEXIBILITY FOCUS ON DOWNSIDE

Unconstrained allocation RISK MANAGEMENT

across asset classes & State-of-the art

geographies without proprietary shortfall model

regional bias an integral part of the

investment process

DWS Concept

Kaldemorgen

TRACK RECORD EXPERIENCE

Robust risk-adjusted A seasoned team of

returns since 2011 across investment professionals

market cycles under strong leadership

Past performance is not a reliable estimator for future returns.

Source: DWS International GmbH, May 2019

/ 17DEDICATED INVESTMENT TEAM

Boutique-style approach combined with resources of a global player

MULTI ASSET TOTAL RETURN TEAM

Portfolio Manager

37 37

Klaus Kaldemorgen

Co-Head Multi Asset Total Return Teams

Managing Director

Co-Manager

14 14 11 11

Henning Potstada Christoph Schmidt, CFA

Co-Head Multi Asset Total Return Team Global Sector Focus:

Global Sector focus: Energy, Materials | Global Convertibles Industrials, Health Care

Portfolio Management

Risk Management & Data Analytics

Equities & Sector Gatekeeper Fixed Income & Currencies Gatekeeper

Dr. Gunnar 22 22 Stefan 26 15 Bernhard 31 19 Stefanie 23 3 Heike 30 17 Thomas 6 6

Friede, Flasdick Falk Holtze-Jen Fornefett Graby

CEFA CIIA

Global Sector Focus: Global Sector Focus: Fixed Income Currencies Risk Management, Performance- Risk Management, Performance-

IT, Telekom., Utilities, Consumers Contribution, Portfolio Analytics Contribution, Portfolio Analytics

ESG

Sascha 19 19 Tanja 8 8

Halicki, Siegrist, CFA

CEFA, CIIA

Industry experience (years) with DWS (years)

Institutional Mandates Fixed Income & Institutional

Mandates

DWS GLOBAL RESEARCH NETWORK

Equities Core Fixed Income Credit Alternatives Fund Selection

Sector/ Geo Coverage Sovereign IG, HY, EM, Hybrids Hedge funds, infrastructure,

convertibles, commodities

125 59 70 220 14

As of: September 2019; Source: DWS International GmbH

/ 18DWS CONCEPT KALDEMORGEN

Risk/Return profile of DWS Concept Kaldemorgen over time

ANNUAL PERFORMANCE, VOLATILITY AND DRAWDOWNS* SINCE INCEPTION (MAY, 2011)

15%

12.84%

11.87%

10%

8.16% 7.65%

6.42%

5% 3.55%

1.56%

0.46%

0%

-2.23%

-5%

-10%

2011 2012 2013 2014 2015 2016 2017 2018 2019

(partial,

inception May

Performance Max Drawdown Volatility

2011)

Inception date: May, 2011

DWS Concept Kaldemorgen FC share class; Calculation of performance is based on the time-weighted return and excludes front-end fees. Individual costs for funds such as

management / performance fee, commissions and other charges have been included in this presentation. Past performance is not a reliable indicator of future returns.

* On a calendar year basis

As of: December 2019; Source: DWS International GmbH, daily figures

/ 19ASSET CLASS STEERING DURING THE YEAR

With success through different market phases thanks to flexibility

ASSET ALLOCATION

100% 100%

90% 90%

80% 80%

70% 70%

60% 60%

50% 50%

40% 40%

30% 30%

20% 20%

10% 10%

0% 0%

12/18 01/19 02/19 03/19 04/19 05/19 06/19 07/19 08/19 09/19 10/19 11/19 12/19

Cash Gold Certificates Government Bonds Corporate Bonds Equities Net Exposure Equities (RS)

Past performance is not a reliable indicator of future returns. Allocations are subject to change without prior notice.

As of: end of December 2019; Source: DWS International GmbH, Thomson Reuters Datastream.

/ 20DWS CONCEPT KALDEMORGEN

Contribution overview (before costs)

PERFORMANCE CONTRIBUTION – YTD

All asset classes in positive territory in 2019:

Equities (local) 10.9%

_ Equity as the major performance contributor in

H1

Equity index futures (local) -1.3%

_ Increase in corporate bond allocation paying off

Corporate bonds (local) 2.2%

_ Profits from government bonds in the US, Russia

Government bonds (local) 0.9% and Turkey

_ Gold with a positive contribution especially in Q2

Bond index futures (local) 0.0%

_ FX also contributing positively, mainly due to

Gold (local) 1.4% strengthening of the USD, GBP and RUB

Cash/MM (local) -0.1%

FX 1.3%

TOP 3 CONTRIBUTORS YTD

FX Forwards -0.4% AT&T INC 83 BP

TAIWAN SEMICONDUCTOR MAN. 62 BP

ALPHABET INC 57 BP

Past performance is not a reliable indicator of future returns.

As of end of December 2019, Source: DWS International GmbH

/ 21DWS CONCEPT KALDEMORGEN

Navigating markets effectively

NET EQUITY NET DURATION NET EUR-POSITION

50% 5 120%

4

40%

100%

3

30% 2

80%

1

20%

0 60%

10%

-1

40%

0% -2

-3

-10% 20%

-4

-20% -5 0%

05/11

05/12

05/13

05/14

05/15

05/16

05/17

05/18

05/19

05/11

05/12

05/13

05/14

05/15

05/16

05/17

05/18

05/19

05/11

05/12

05/13

05/14

05/15

05/16

05/17

05/18

05/19

Allocations are subject to change without notice.

As of: Dezember 2019; Source: DWS International GmbH

/ 22OUTLOOK 2020

Peak pessimism behind us – 2020 could surprise positively

ECONOMY INFLATION CENTRAL BANKS POLITICS

Growth slowdown in DM, Close, but below CB target Globally in easing mode Tariff agreement expected

recovery in EM No inflation overshoot ECB & Fed on hold Less uncertainty from

No recession European politics

EQUITIES FIXED INCOME CURRENCIES ALTERNATIVES

Higher EPS growth Low for longer EUR/USD continue Illiquidity premium

Europe with upside potential Focus on Asian bonds sideways trading

JPY as hedge

ESG

Smart Integration of ESG criteria into the investment process

Forecasts are not a reliable indicator of future returns. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

Source: DWS Investment GmbH as of December 2019

CIO View / Stefan Kreuzkamp / January 2020 / 23OUTLOOK 2020

Structural trends and changes

DIGITALIZATION CLIMATE CHANGE

Almost every sector affected! Big driver for ESG / sustainable

Disruptive in particular for financial investments

and automobile sector

As of: December 2019; Source: DWS International GmbH

/ 24OUTLOOK 2020

Increase of asset classes with low or negative correlation to equities

ASSET CLASS EXPOSURE IN 2020 DIVERSIFIERS

50%

Equity Listed Residential Property, stable dividend stocks

31%

18%

Government Bonds US Treasuries, Norway Government, EM Government

12%

13% Reduction of Corporate Bonds high correlation with

Corporate Bonds

26% equities

9% Diversification benefits, profit from geopolitical risks &

Gold

7% low/negative interest rates

10%

Cash Avoid negative interests

24%

28% Increase of „Safe Haven“ currencies (USD, CHF, JPY),

Foreign Currencies

24% NOK, strategic short position in GBP

2020 Beginning 2019

Allocations are subject to change without prior warning

Source: DWS International GmbH, as of: January 2020

/ 25DWS CONCEPT KALDEMORGEN

Current portfolio positioning – Equity

BREAKDOWN BY REGION BREAKDOWN BY SECTOR

Eurozone 19.5% Health Care 12.3%

Comm. Services 7.5%

North America 15.8% InfoTech 5.8%

Financials 4.1%

United Kingdom 3.2%

Consumer Discretionary 3.9%

Asia ex. Japan 3.1% Energy 2.8%

Real Estate 2.6%

Switzerland 2.6%

Consumer Staples 1.8%

Japan 1.0% Industrials 1.7%

Utilities 1.7%

EM/Others 0.6% Materials 1.6%

KEY RATIOS*

Dividend Yield (12M Forward) 3.25% Net Debt to Equity 66.81%

EV/EBITDA (12M Forward) 9.28 EPS Growth (12M Forward) 4.97%

Data shown in % of fund volume. Allocations are subject to change without notice.

* Data based on the equity part of the fund.

As of: December 2019; source: DWS International GmbH

/ 26DWS CONCEPT KALDEMORGEN

Current portfolio positioning – Fixed Income

BREAKDOWN BY MARKET SEGMENTS BREAKDOWN BY REGIONS BREAKDOWN BY SECTORS

North America 14.3% Comm. Services 2.7%

Emerging Markets 9.1%

Industrials 2.5%

Europe ex Eurozone 6.3% Energy 2.5%

Sovereigns 8.6% Health Care 2.3%

Eurozone 4.7% Consumer Staples 1.4%

InfoTech 0.9%

HY Corporates 8.0% Latin America 2.2%

Financials* 0.9%

Others Materials 0.5%

1.2%

IG Corporates 2.1% Consumer Disc. 0.2%

Asia ex Japan 0.1% Real Estate 0.1%

Utilities 0.1%

Convertibles 0.9%

Japan 0.0% None 0.0%

KEY RATIOS*

Average Bond Rating BBB Duration excl. Derivatives (years) 3.84

Ø Coupon excl. Derivatives 4.29% Duration incl. Derivatives (years) 3.81

Ø Yield-to-maturity excl. Derivatives 3.42%

Data shown in % of fund volume. Allocations are subject to change without notice.

* Data based on the fixed income part of the fund.

As of: December 2019; source: DWS International GmbH

/ 27ALLOCATION TO EMERGING MARKETS

Select opportunities paying off

FIXED INCOME

RUSSIAN GOVERNMENT BOND (01.01.2019 = 100)

_ Profits from the appreciation of the Russian

Ruble as well as from positions in the equity and 112

fixed income buckets in Russia 110

108 +11.2%

_ Increase of Mexican corporate bonds exposure 106

(carry) 104

_ Turkish government bonds in hard currency (EUR 102

and USD) 100

98

RUSSIAN RUBLE APPRECIATION (EUR/RUB) EXPOSURE IN THE FIXED INCOME PORTFOLIO

80 4,0%

78

3,0%

76

RUB loses

74

+13.7% 2,0%

RUB gains 72

70

1,0%

68

0,0%

Brazil Mexico Russia Turkey

Past performance is not a reliable indicator of future returns. Allocations are subject to change without prior notice.

As of: end of December 2019; Source: DWS International GmbH, Bloomberg

/ 28DWS CONCEPT KALDEMORGEN

Current portfolio positioning – Currency

BREAKDOWN BY CURRENCY*

EUR 66.7%

42.7%

USD 17.7%

34.7%

GBP -1.8%

5.2%

CHF 2.6%

2.6%

JPY 1.5%

1.5%

TWD 1.5%

1.5%

Gold 6.9%

6.9%

RUB 2.2%

2.2%

HKD 1.4%

1.4%

Others 1.3%

1.3%

-10% 0% 10% 20% 30% 40% 50% 60% 70% 80%

Net Gross

Allocations are subject to change without notice.

* refers to foreign currency accounts and securities held in the respective currency .

As of: December 2019; source: DWS International GmbH, BarraOne

/ 29ESTRATEGIAS INCOME DWS INVEST TOP DIVIDEND DWS INVEST ESG EQUITY INCOME For Professional Clients MiFID Directive 2014/65/EU Annex II) only. No distribution to private/retail investors. For Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)). For institutional investors only. Further distribution of this material is strictly prohibited. APAC Australia: For professional clients only.

CONSERVATIVE EQUITY INVESTMENT

The stock market year 2018 as an example

INVESTOR: EQUITIES GLOBAL1 INVESTOR: DWS TOP DIVIDENDE

Recession?

Distribution

„Interest „Interest

fears“? fears“?

1 measured by the MSCI World Index

As of: End of December 2019. Source: DWS International GmbH

/ 31WHAT SHOULD BE THE VALUE OF A

DIVIDEND STRATEGY IN THE LONG-TERM?

1 Real asset (“inflation hedge”)

2 High dividend yield and regular income

3 Asymmetric risk return profile

4 Less volatile than “traditional” equity investments

5 Superior risk-adjusted returns

Source: DWS International GmbH

/ 32DIVIDENDS – WHERE ELSE IS THERE YIELD?

Dividend yield

Bond yield (5Y.) Company

(current)

2.2 % PFIZER 3.7 %

2.6 % VERIZON 4.1 %

0.0 % UNILEVER 3.3 %

0.0 % ALLIANZ 4.1 %

-0.1 % TOTAL 5.2 %

For illustrative purposes only.

As of: End of December 2019; source: DWS International GmbH, Bloomberg, www.euwax.de

/ 33DWS TOP DIVIDENDE LD

Attractive and regular income

AVERAGE DISTRIBUTION YIELDS CLEARLY HIGHER THAN INFLATION RATES

Distribution per share DWS Top Dividende LD in EUR:

1.101 2.50 2.90 2.90 2.90 2.65 2.65 2.65 2.75 2.75 2.80 2.90 3.00 3.10 3.20 3.40 3.60

6%

5% 4,8%

4,3%

4,1% 4,0%

4% 3,6% 3,6% 3,5%

3,2% 3,1% 3,3% 3,1%

3,0% 2,9% 2,9%

3% 2,7% 2,7% 2,6%

2%

1%

0%

1

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Distribution yield per share DWS Top Dividende2 Inflation rate Eurozone

Past performance is not a reliable indicator of future returns.

1 Short fiscal year (04/28/2003 – 09/30/2003)

2 Based on the average NAV of the fiscal year (10/01 – 09/30)

3 Based on the average NAV of DWS Top Dividende since inception (04/28/2003 – 09/30/2019), Inception date: 04/28/2003

As of: End of December 2019; source: DWS International GmbH, Refinitiv Datastream

/ 34HIGH DIVIDEND YIELD IS NOT ALWAYS BETTER

DIVIDEND YIELD

ESTIMATED VERSUS REALIZED YIELD BY DIVIDEND YIELD (IBES CONSENSUS FTSE WORLD SINCE 1995)

(in %)

25

Realized yield (clearly) below

Our preferred investment universe

expected yield

20

Dividend yield (%)

15

10

5

0DWS TOP DIVIDENDE

Clearly lower downside risk and volatility

DWS TOP DIVIDENDE LD – SINCE INCEPTION*

100%

81%

Down

Up

-65%

-100%

DWS Top Dividende LD MSCI World (RI)-Index**

Past performance is not a reliable indicator of future returns. Upside Capture Ratio measures a manager's performance in up markets relative to the market (benchmark) itself. It is

calculated by taking the security’s upside capture return and dividing it by the benchmark’s upside capture return. Downside Capture Ratio measures manager's performance in down

markets. A down-market is defined as those periods (months or quarters) in which market return is less than 0. In essence, it tells you what percentage of the down market was

captured by the manager. For example, if the ratio is 110 %, the manager has captured 110 % of the down-market and therefore underperformed the market on the Downside.

As of: End of December 2019; * April 28th, 2003 ** No official benchmark

Source: DWS International GmbH

/ 36THE GOLDEN RULES OF DIVIDEND INVESTING –

TIPS AND HINTS

1. Stick to your STYLE

especially in growth/momentum driven

markets

2. PATIENCE and DISCIPLINE are key

Dividend investing is not a sprint, it´s a marathon

3. DON´T GET TOO GREEDY

Avoid dividend cutter

4. FOCUS ON CAPITAL PRESERVATION

Winning more by losing less

5. SUSTAINABLE BUSINESS MODEL

Stability of revenues/earnings, strong balance

sheet

Forecasts are based on assumptions, estimates, views and hypothetical models or analyses, which might prove inaccurate or incorrect.

As of end of December 2019; source: DWS International GmbH

/ 37INCOME STRATEGIES

Characteristics, Investment rationale and Investment strategy

“Consistent dividend growers”:

Strong track record of

Dividend growing dividends

“Defensive yield”: Defensive champions / combined with decent

stocks with higher yield but Aristocrats dividend yield

lower growth (mature

business models)

(Dividend) growth at a

Dividend Dividend

reasonable yield

Strong balance sheet and free yielders growers

cash flow, low

net debt / good credit rating

Quality

Our Global equity income strategy focusing on companies with above average dividend yield, reasonable dividend growth

and sustainable dividend coverage.

© 2019 Morningstar, Inc. All rights reserved. The information contained herein:

(1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor

its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

* (vs. peers in global equity income category by Morningstar and broad market combined with top rankings and ratings )

Note: Not all Deutsche AM products and services are offered in all jurisdictions and availability is subject to local regulatory restrictions and requirements. Past performance is not

necessarily indicative of future returns.

Source: DWS International GmbH

/ 38SIMILARITIES & DIFFERENCES

DWS Invest Top Dividend & DWS Invest ESG Equity Income

DWS Invest Top Dividend DWS Invest ESG Equity Income

Morningstar Peer group Global Equity Income Global Equity Income

Benchmark None None

Use of derivatives / FX

Generally not Generally not

hedging

Focus on large caps,

Focus on mega / large caps

Market capitalization partially mid caps

(Ø market cap: 103 bn EUR)

(Ø market cap: 97 bn EUR)

Number of holdings 60 – 100 60 – 100

Single stock weight 1–3% 1–4%

Sector restrictions / None – focus on defensive None – focus on ESG conform

sector bias dividend payer defensive dividend payer

Regional restrictions None None

Liquidity ~ 7% ~ 5%

Ø Current dividend yield Ø 3.9% Ø 3.2%

Ø Median dividend

7.0% 8.7%

growth 1 year

Turnover Ratio ~ 20 % p.a. < 50 % p.a.

Past performance is no guarantee of future results..

AuM EUR 24 bn

As of: End of December 2019; source: DWS International GmbH, Aladdin Research

EUR 293 mn

No assurance can be given that investment objective or any target will be achieved. © 2020 Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not

be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

/ 39DWS ESG CONSENSUS RATING

scanning for cross-vendor concordance in ESG assessments

DISCRETIONARY BEST-IN-CLASS

APPROACH

100 points

A ESG true leaders

concordant rank order ►

B ESG leaders

C ESG upper midfield

D ESG lower midfield

DWS is licensed user of the data from

those ESG-data-vendors.

0 points E ESG laggards

F ESG true laggards

HARD EXCLUSIONS

DWS’ ESG Consensus Ratings seek to identify the true ESG leaders and ESG laggards by peer group, consistently assessed as such by the top ESG agencies in a 360 degree

review.

As of: December 2019; source: DWS International GmbH

/ 40DETAILING OUR MINIMUM ESG STANDARDS (MESGS)

Exclusion and best-in-class criteria that apply to all ESG labeled DWS mutual funds

Sector screens Norm screen and Best-in-Class ranking

Controversial weapons UNGC Norm Compliance

_ Nuclear weapons _ Human rights

_ Cluster munitions _ Child / forced labor

_ Anti personnel mines _ Work conditions

_ Depleted uranium _ Environmental impact

_ Business ethics

Ownership and production of

Rating: A – E2

weapons and components

Controversial sectors

_ Tobacco

X

Exclusion

Climate Transition Risk

Investment

_ Military defense

Rating: A – E3 universe

_ Adult entertainment

_ Gambling Security selection

_ Nuclear power from those issuers

_ Coal* ESG overall SynRating that meet all

requirements

Max. revenue threshold

Rating: A – D4

≤ 5%

1 Max. revenue threshold: ≤ 25%, 2 max. 5% E in portfolio, 3 E max 5%, F excluded 4 ESG SynRating: max. 15% D in portfolio; max. 5% unrated

As of: December 2019; source: DWS Investment GmbH

/ 41DWS INVEST ESG EQUITY INCOME

Sector and country allocation – absolute to DWS Top Dividende

Portfolio

overlap

SECTOR ALLOCATION approx. COUNTRY ALLOCATION

16,9%

1/2 - 2/3 USA 33,3%

Financials 15,2% 36,1%

15,3% Germany 9,5%

Health Care 14,5% 7,4%

Great Britain 6,6%

IT 12,8% 5,6%

7,1% 6,2%

9,2% Exclusion of

Netherlands 5,9%

Consumer Staples 12,4% tobacco e.g. 5,2%

Canada 6,3%

Utilities 7,6% Greener European Utilities vs.

8,6% coal intensive US utilities

Japan 5,0%

7,6% 5,7%

Communication 9,0% 4,5%

Norway 4,0%

Industrials 7,0%

5,5% 4,4%

Denmark 0,0%

Materials 6,5% Chemical sector vs. Mining 3,6% In general overweight in Europe due to better

4,7% Switzerland

Companies 5,4% ESG data availability, better transparency and

pioneering role of Europe in the field of ESG

Consumer Disc. 4,0% 3,3%

1,6% France 5,4%

Energy 3,3% Primarily indirect oil exposure 2,7%

11,3% Finland 1,4%

vs. European Oil Majors

Real Estate 0,0% 5,8%

0,5% Other Countries 7,3%

ESG Equity Income DWS Top Dividende ESG Equity Income DWS Top Dividende

In % of fund volume. Allocations are subject to change without notice.

As of: End of December 2019; source: DWS International GmbH, Report Finder

/ 42DWS INVEST ESG EQUITY INCOME

ESG quality versus DWS Top Dividende and MSCI World

ESG Best in Class Exclusion

50% 42%

39%

40% 34%

30% 25% 27%

23% 20%

19%

20% 14%11%

8% 8% 10%10%

10%

0% 0% 0% 0% 1% 2%

0%

A B C D E F Kasse

Ø SynRating: B Ø SynRating: C Ø SynRating: C

ESG-Score: 77 ESG-Score: 68 ESG-Score: 61

DWS Invest ESG DWS

MSCI Welt

Equity Income Top Dividende

Especially ESG Equity Income scores best within the Morningstar Peer Group “Global Equity Income”. It is

leading on the first rank and has 5 out of 5 sustainability globes.

ESG SynScore and ESG SynRating are based on proprietary ESG Engine.

No assurance can be given that investment objective or any target will be achieved. © 2019 Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to

Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers

are responsible for any damages or losses arising from any use of this information.

As of: End of December 2019; source: DWS International GmbH, Aladdin Research, Update Quarterly

/ 43ESG GLOBAL EQUITY INCOME MANDATE

Performance since inception (May 27, 2013)

PERFORMANCE SINCE INCEPTION1 OF “ESG GLOBAL EQUITY INCOME” MANDATE VS. MARKET

100 + 94.9%

Vola 12.5%

80 SR: 0.88

+ 82.3%

60 Vola 8.8%

SR: 1.11

40 + 80.1%

Vola 8.8%

20 SR: 1.08

+ 73.9%

0

Vola 11.1%

SR: 0.81

-20

05/13 11/13 05/14 11/14 05/15 11/15 05/16 11/16 05/17 11/17 05/18 11/18 05/19

MSCI World TR Net (EUR) ESG Global Equity Income Mandat

MSCI World High Dividend Yield TR Net (EUR) DWS Top Dividende (brutto)

1) May 27th, 2013

Past performance is no guarantee of future results. Calculation of performance is based on the time-weighted return and excludes front-end fees. Individual costs such as fees,

commissions and other charges have not been included in this presentation and would have an adverse impact on returns if they were included. Sharpe Ratio (SR) = measure to

calculate risk-adjusted return

As of: End of September 2019; source: DWS International GmbH, monthly data, update quartely

/ 44RENTA VARIABLE ALEMANA DWS INVEST GERMAN EQUITIES / DWS DEUTSCHLAND For Professional Clients MiFID Directive 2014/65/EU Annex II) only. No distribution to private/retail investors. For Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)). For institutional investors only. Further distribution of this material is strictly prohibited. APAC Australia: For professional clients only.

GERMAN GDP IS HEALTHIER THAN SOME MAY THINK

125

120

115

110

105

100

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Germany United States

GDP per capita, index: 2000 = 100

The information herein reflects our current views only, are subject to change, and are not intended to be promissory or relied upon by the reader. There can be no certainty that events will turn out as we have

opined herein. Forecasts are not a reliable indicator of future returns. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analysis which may prove to be incorrect.

*+: high expected market impact; O: neutral expected market impact; -: low expected market impact // Source: Bloomberg Finance L.P., DWS Investment GmbH as of January 2020

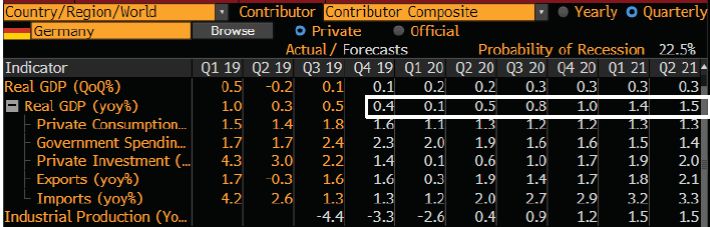

CIO Office / Market Outlook Slides / January 2020 / 46GERMANY BOTTOMING Key Economic Indicators Consensus expects strong rebound in growth in 2020 Source: Bloomberg CIO Office / Market Outlook Slides / January 2020 / 47

DWS INVEST GERMAN EQUITIES / DWS DEUTSCHLAND

Characteristics, Investment rationale and Investment strategy

CHARACTERISTICS & INVESTMENT RATIONALE

_ Investment style: Blend INVESTMENT STRATEGY

_ Investment approach: Bottom-up/stock picking _ German equity strategy focusing on firms sustainable business models and

_ Benchmark: CDAX Index strong balance sheets.

_ Tracking error: No formal tracking error target

CDAX UNIVERSE (minimum 500mn € market cap)

_ Holdings: 40 – 60 stocks

Investment focus Quality Fundamentals Sustainability

_ Market capitalization: Large-Caps and flexible addition

of high quality Small/Mid Caps (30% on average)

_ Combination of value and _ Earnings quality _ Growth at a reasonable _ ESG aspects

growth stocks _ Management track record price

_ Use of derivatives: 1) DAX futures for active steering of _ Flexible addition of _ Attractive dividend yield

_ Strong balance sheets

investment ratio to tactically benefit from short term small/mid caps

market movements and to manage risk as well as

Opportunistic “blend” approach

2) options to generate premium intakes (max. 3% of

portfolio delta adjusted)

DWS Deutschland / DWS Invest German Equities

_ ~60 stocks

_ One of the largest and most experienced German

Monitoring Risk Management

equity teams with direct access and close long-term

relationships to the most important German companies.

_ Excellent stock picking expertise with a focus on High Conviction German equity portfolios

structural growth and positive earnings momentum

Note: Not all Deutsche AM products and services are offered in all jurisdictions and availability is subject to local regulatory restrictions and requirements.

Source: DWS International GmbH

/ 48DWS INVEST GERMAN EQUITIES / DWS DEUTSCHLAND

Portfolio allocation

BY SECTORS / ASSET CLASSES* BY MARKET CAPITALIZATION*

IT Mega caps

Financials (> 10 bn .)

Industr ials

Consumer Disc. Larg e cap s

(> 5 bn. < 10 bn.)

Materials

Por tfolio

Health Ca re Por tfolio

Mid cap s

Commu nicatio n Ben chmar k

(> 1 bn. < 5 b n.)

Real Estate

Utili ties Small caps

Consumer Sta ples (< 1 bn.)

0% 5% 10% 15% 20% 25% 30%

0% 20% 40% 60% 80% 100 %

BY TOP TEN*

Allia nz SE

SAP S E

Wirecard AG

Siemen s AG

Adid as AG

Muenchen er… Por tfolio

Infin eon…

KION G roup AG

BAS F SE

Fresenius SE…

0% 2% 4% 6% 8% 10% 12%

This allocation data comprises a mutual fund benchmarked against CDAX (RI).

* In % of fund volume; Reference index: 100% CDAX

Allocations are subject to change without notice.

As of: December 30, 2019; source: DWS International GmbH, Report Finder FIS XP

/ 49DWS INVEST GERMAN EQUITIES / DWS DEUTSCHLAND

Performance & risk figures

CALENDAR YEAR PERFORMANCE 7-YEAR CUMULATIVE PERFORMANCE

40% 250 108.09%

30%

220 84.05%

20%

10% 190

0% 160

-10%

130

-20%

-30% 100

Yea r to 201 9 201 8 201 7 201 6 201 5 201 4 201 3 201 2

Date Strategy Ben chmar k Strategy Ben chmar k

YTD 2019 2018 2017 2016 2015 2014 2013 2012 12/14 - 12/15 12/15 - 12/16 12/16 - 12/17 12/17 - 12/18 12/18 - 12/19

Strategy 25.78% 25.78% -23.03% 20.03% 9.52% 17.54% 5.25% 32.19% 37.97% Strategy 17.54% 9.52% 20.03% -23.03% 25.78%

Benchmark 25.08% 25.08% -18.11% 15.98% 6.50% 11.33% 3.09% 26.75% 29.26%

Spread

Benchmark 11.33% 6.50% 15.98% -18.11% 25.08%

0.70% 0.70% -4.92% 4.05% 3.01% 6.21% 2.15% 5.44% 8.71%

ANNUALISED PERFORMANCE STATISTICS

Return p.a. Annualised volatility (p.a.)

Strategy Benchmark Spread Strategy Benchmark Tracking error Information ratio Sharpe ratio Max Drawdown Beta Var (99%/10day/1y)

1 Year 25.78% 25.08% 0.70% 15.65% 12.83% 3.28 0.21 1.67 6.91 1.21 10.53%

3 Years 5.13% 5.90% -0.78% 15.52% 12.41% 3.45 -0.23 0.35 25.24 1.24 -

5 Years 8.38% 7.09% 1.29% 17.69% 15.14% 3.31 0.39 0.49 25.24 1.16 -

7 Years 11.03% 9.10% 1.93% 16.20% 14.02% 3.01 0.64 0.69 25.24 1.14 -

This data comprises a mutual fund benchmarked against CDAX (RI). Calculation of performance is based on the time-weighted return. Possible previous benchmark changes have

already been reflected in benchmark performance. Individual costs such as fees, commissions and other charges have not been included in this presentation and would have an

adverse impact on returns if they were included. Past performance is not a reliable indicator of future returns.

Reference index: 100% CDAX

As of: December 30, 2019; source: DWS International GmbH

/ 50TEMÁTICOS For Professional Clients MiFID Directive 2014/65/EU Annex II) only. No distribution to private/retail investors. For Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)). For institutional investors only. Further distribution of this material is strictly prohibited. APAC Australia: For professional clients only.

Translating global challenges into investable themes

Investment opportunities based on sustainable growth drivers

Technolical breakthrough Climate Change and resource scarcity

DWS Invest Artificial DWS Invest Climate Tech

Intelligence

Interconnectivity of tech Nutrition, demography and

themes and globalisation Global eating habbits

DWS (Invest) Smart Megatrends DWS Invest Global

Industrial Technologies Agribusiness

ESG and positive impact investing

Urbanisation, demography and

modernisation

DWS Invest SDG Global

Equities

DWS Invest Global

Infrastructure

As of: December 2019; source: DWS Investment GmbH

/ 52For Professional Clients (MiFID Directive 2014/65/EC Annex II) only. No distribution to private/retail customers.

For Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)).

Thematic Equities – Smart Technologies

DWS Invest Smart Industrial Technologies

Automation & Digitalization are only two megatrends that shape our current world. The fund invests in

industrial companies that drive these changes. “Smart Tech” operates in various fields: Automation,

Digitalization, Energy Efficiency, Global Trade, MedTech and Infrastructure. The fund management team

has a strong focus on growth stocks while ensuring risk diversification on a portfolio level.

Automation & Robotics Infrastructure

More use of software & robotics to High demand for infrastructure due to

improve efficiency, quality and to allow demographic trends and

a higher degree of customization modernization requirements

E-Commerce & Global trade Digitalisation & Cyber Security

Increasing air travel and freight Demand for software applications to

volumes because of globalization improve efficiency and to distinguish

and demographic trends products and services

Smart Energy Medical Technology

Reduction of energy costs and emissions Rapidly rising health care costs,

to fulfill global emission standards leads healthier lifestyle and appearance of

to “Smart Cities” and “Smart homes” Millennials are influencing changes in

consumer behavior.

As of: December 2019

Source: DWS International GmbH

/ 53For Professional Clients (MiFID Directive 2014/65/EC Annex II) only. No distribution to private/retail customers.

For Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)).

Thematic Equities – Impact Investing & ESG Integration

DWS (Invest) SDG Global Equities

We seek exposure to companies which operate in SDG-related business sectors and have a meaningful

positive impact on the United Nations Sustainable Development Goals (SDGs). Comprehensive analysis

and evaluation of the SDG impact is based on our proprietary ESG-Engine. The average proportion of

SDG-related revenue of the companies in the fund must be more than 50%.

Measuring what matters Making a positive impact

Integrating the UN SDGs into

investment portfolios through our

proprietary SDG-Rating.

Stocks are only eligible for the fund´s

investment universe if they are

relative and absolute SDG-

Champions.

The SDGs at an investor level Application of ESG standards

Achieving the SDGs may require up to Consideration of ESG aspects (Best-in-Class-

$7tn in investment each year from 2015 to Approach, Exclusion, Norm Compliance,

2030 – of which up to $6tn is reliant on the Carbon Rating, Engagement) based on the

unique ESG Engine.

private sector.

Excellent proprietary ESG engine, which

received the Insurance ERM Award 2017

As of: December 2018

Source: DWS International GmbH

/ 54DWS INVEST SDG GLOBAL EQUITIES

High positive link to UN SDGs versus MSCI World

DWS Invest SDG Global Equities MSCI World

50% 9%

SDG related revenues SDG related revenues

More than every Only about every

second euro invested twentieth euro invested

is aligned with is aligned with

the UN SDGs the UN SDGs

Forecasts are not a reliable indicator of future returns. Forecasts are based on assumptions, estimates, views and hypothetical models or analyses, which might prove inaccurate or

incorrect. Number is average of SDG related revenue contribution since inception of the fund.

As of: December 2019; source: DWS International GmbH, quarterly updated

/ 55DWS INVEST SDG GLOBAL EQUITIES

Allocation

Portfolio allocation by SDG related revenues and by SDG theme (in %)

13 23,2%

3 10,5%

6 6,6%

12 4,7%

4 3,0%

2 2,0%

11 0,3%

8 0,1%

More than every second euro invested is aligned with the UN SDGs

Pictures illustrative purposes only.

As of: December 2019; source: DWS International GmbH; quarterly updated

/ 56Thematic Equities – Agribusiness

DWS Invest Global Agribusiness

We need to improve the efficiency in Agribusiness and invest in solutions to feed the planet. A two-

pronged investment approach via equity both upstream and downstream holds the key to generate a

superb risk-return profile for investors in our strategy.

Upstream Downstream

_ Fertilizer companies _ Protein producers (beef, chicken, pork)

_ Agricultural chemicals, _ Fishery & Aquaculture

_ Seed producers _ Packaged foods

_ Farm equipment _ Retail foods

_ machinery

_ Breweries and soft drink producers,

_ Restaurants

_ Supermarkets

Agribusiness Tech

Midstream

_ Data management (field monitoring)

_ Processors

_ Monitoring and communication

_ Distributors technology

_ Railways _ GPS Tracking

_ Port operators _ Precision AG (Irrigation, Planting,

Spraying)

As of: December 2019

Source: DWS International GmbH

/ 57For Professional Clients (MiFID Directive 2014/65/EC Annex II) only. No distribution to private/retail customers.

For Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)).

Thematic Equities – Climate Technology

DWS Invest Climate Tech

We need to address the global climate change and invest in solutions that mitigate and adapt its

implications on the planet. A versatile investment approach via listed equity focusing on proprietary

climate change sector universe holds the key to generate a superb risk-return profile for investors.

Climate Change Impact Management Consumption of Energy

Health: Diseases/pest control, air Industry: Combined heat and power,

quality, environmental sensing advanced boilers, pumps, compressors

Agribusiness: Precision Ag, drip Buildings: Thermal insulation, building

irrigation, drought resistance plants automation, lighting systems

Water: Re-use/desalination, leak Vehicles: Hybrid & electric vehicles,

detection, Smart Water infrastructure battery technology, improved

Disaster Prevention/Recovery combustion engine technology

Transportation of Energy

Generation of Energy

Electricity transmission and distribution

Solar poly, wafer, module, inverter

Smart grid / Energy storage

Solar and wind farm developers/owners

Data management

Wind turbine manufacturers

Monitoring/communication technology

Hydro value chain / Waste-to-Energy

New Materials

As of: December 2018

Source: DWS International GmbH

/ 58Thematic Equities – Infrastructure

DWS Invest Global Infrastructure

Historical underinvestment and future investment gaps in infrastructure spending coupled with significant

structural drivers create investment opportunities. Infrastructure securities are backed by tangible

assets with sustainable inflation-linked underlying cash flows that can effectively diversify a multi-assets

portfolio. We invest in listed infrastructure companies that generates at least 70% of the operational cash

flow is from owning or leasing hard infrastructure assets.

The Opportunity “Pure-Play” Focus

_ Strong tailwinds from investor and “real world” _ Regulated Utilities: e.g. Water, electricity

demand networks

_ Communications: e.g. Mobile Towers, Satellites

_ Invest with the pioneer of the asset class – _ Energy: e.g. Oil and gas pipelines

“Pure Play” infrastructure

_ Ports: e.g. Sea ports, airports

_ Transportation: e.g. Rail roads, toll roads

Characteristics of Pure-Play

The Benefits Assets

_ “Pure play” infrastructure allows “smart access” to _ Focus on hard assets that provide efficient

the asset class movement of people and products

_ Stable & inflation linked cash flows and attractive _ Low pricing risk owing to fixed, contracted, or

income regulated revenue models

_ Perfect fit in a Multi-Asset-Portfolio _ Provision of essentials services such as water or

_ Complement to direct investments, allowing for power result in highly inelastic demand profiles

instant diversification & capital deployment _ Long-dated assets with perpetual lives, low

_ Long duration assets & cash flows operating costs which leads to high operating

margins

_ Sustainable performance and alpha

_ Inflation protection from inflation-adjusted

As of: December 2019 revenues

Source: DWS International GmbH

/ 59APÉNDICE For Professional Clients MiFID Directive 2014/65/EU Annex II) only. No distribution to private/retail investors. For Qualified Investors (Art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)). For institutional investors only. Further distribution of this material is strictly prohibited. APAC Australia: For professional clients only.

TACTICAL VIEW(2) & STRATEGIC FORECAST(3)

Level Tactical View Dec '20 F -1W YTD

Rates percentage points

GER 2yr -0.66 -0.60 -0.05 -0.06

GER 10yr -0.41 -0.35 -0.08 -0.23

GER 30yr 0.09 0.15 -0.10 -0.26

UK 10yr 0.52 0.95 -0.04 -0.34

UST 2yr 1.39 1.50 -0.11 -0.18

UST 10yr 1.56 1.85 -0.13 -0.32

UST 30yr 2.02 2.25 -0.11 -0.31

JGB 10yr -0.07 -0.10 -0.05 -0.06

Spreads basis points

EUR IG Corp 104 90 3 1

EUR HY 350 360 26 36

US IG Corp 96 110 4 5

US HY 382 400 26 52

EM Credit 317 320 10 9

EM Sovereign 313 320 11 17

Italy 10yr 135 150 -22 -25

Spain 10yr 68 70 0 2

Currencies

EUR vs USD 1.10 1.15 0.00 -0.02

USD vs JPY 108.90 105.00 -0.38 0.02

EUR vs GBP 0.84 0.89 0.00 -0.01

EUR vs JPY 120.12 121.00 -0.37 -1.84

GBP vs USD 1.31 1.29 0.00 0.00

USD vs CNY 6.94 7.10 0.00 -0.04

Equity* & Commodities

S&P 500 3,284 3,300 -0.4% 1.9%

Stoxx 600 414 420 -2.3% -0.6%

Euro Stoxx 50 3,674 3,770 -2.8% -2.0%

DAX 30 13,120 14,000 -3.4% -1.0%

SMI 10,734 10,450 -1.1% 1.1%

FTSE 100 7,321 7,510 -3.5% -3.5%

MSCI EM 1,073 1,120 -4.2% -4.1%

MSCI AC Asia xJ 662 700 -4.5% -4.1%

MSCI Australia 1,407 1,355 -1.1% 3.3%

MSCI Japan 1,015 1,060 -3.1% -2.2%

Gold 1,581 - 1,550 0.6% 4.3%

Crude Oil (WTI) 52 - 54 -3.7% -15.5%

The information herein reflects our current views only, is subject to change, and is not intended to be promissory or relied upon by the reader. There can be no certainty that events will turn out as we have

opined herein. Past performance is not a reliable indicator of future returns. Forecasts are not a reliable indicator of future returns. Forecasts are based on assumptions, estimates, opinions and hypothetical

models or analysis which may prove to be incorrect. *Relative to MSCI World Index, Sources: Bloomberg Finance L.P., DWS Investment GmbH as of 1/31/20 // (1) Outcome: A - above expectations, B - below

expectations, O - on expectations (2) = underweight; = neutral; = overweight // (3) F = Forecast

61DWS CONCEPT KALDEMORGEN

OPPORTUNITIES RISKS

_ Market, industry and company-specific price increases

on the equity markets.

+ _ At any time, the price of the shares can fall below the price

at which the investor acquired them (up to the risk of total loss).

-

_ Drops in yields or increases in prices in the bond markets and/or _ Market, industry and company-specific price fluctuations on the equity

reductions in yield spreads for high-yield securities. markets.

_ Opportunities for additional income through the use of derivative _ Interest rate, price and currency fluctuations in the bond markets. A

investment instruments. creditworthiness risk exists with regard to the issuers of bonds. In

general terms, this is the risk of over-indebtedness or insolvency, i.e.

the potential temporary or permanent inability to fulfil interest and/or

repayment obligations on schedule. This can have a negative impact

on the fund's performance.

_ Asset-backed securities may be less liquid than corporate debt; in

addition, there is the risk of early repayment, which can lead to

fluctuations in the unit price.

_ The use of derivatives involves counterparty risks, i.e. the

creditworthiness risk of the counterparties (see the above risk notice

on creditworthiness risk). Derivatives are subject neither to statutory

nor voluntary deposit insurance.

_ Investments in the commodities sector may be associated with illiquid

markets and high volatility.

_ The fund has the option of achieving leverage through the use of

derivatives. The use of leverage can result in the increase in potential

losses.

_ The fund can invest in assets with different currencies. This gives rise

to exchange rate risks, which may be hedged.

Source: DWS International GmbH

/ 62DWS TOP DIVIDENDE / DWS INVEST TOP DIVIDEND

OPPORTUNITIES RISKS

_ Market-, sector- and company-specific price gains + _ Market-, sector- and company-specific -

price volatility

_ Possible exchange- rate chances

_ Possible exchange-rate risk

_ Above-average dividend yields

_ Possible dividend cuts

_ Because of its composition or the techniques used by its

managers, the fund is subject to heightened volatility.

Consequently, unit prices may fluctuate sharply in either

direction within short periods of time.

_ The value of the fund's shares may fall below the price at

which the client originally bought them

Source: DWS International GmbH

/ 63DWS INVEST ESG EQUITY INCOME /

DWS TOP DIVIDENDE

OPPORTUNITIES RISKS

_ Market-, sector- and company-specific _ Market-, sector- and company-specific

price gains price volatility

_ Possible exchange- rate chances _ Possible exchange-rate risk

_ Above-average dividend yields _ Possible dividend cuts

_ Because of its composition or the techniques used by its

managers, the

fund is subject to heightened volatility. Consequently, unit

prices may fluctuate sharply in either direction within short

periods of time.

_ The value of the fund's shares may fall below the price at

which the client originally bought them.

Source: DWS International GmbH

/ 64DWS INVEST GLOBAL INFRASTRUCTURE

Opportunities and risks

OPPORTUNITIES RISKS

_ Increase in demand for infrastructure due + _ Market, industry and business-related price losses

-

to rising world population and urbanization

_ Exchange rate losses

_ Trends in increased mobile data use in developed countries-

particularly in the United States _ Stronger regulation in the field of infrastructure worldwide

_ Increased demand for the transport of goods, energy and _ Weakening of underlying trends (urbanization/mobile data

people; Due to economic growth and new technologies in use/higher transport needs of people and goods or of energy)

energy production _ Concentration risk: By concentrating on shares in the

_ Market, industry and business-related price increases infrastructure sector, there is a limited diversification within the

fund.

_ Exchange rate gains

_ The fund includes a significant amount of derivative

transactions with various Contracting Parties. If a Contracting

Party does not make any payments, for example due to

insolvency, this may cause the investment to suffer a loss.

Financial derivatives are not subject to the statutory or

voluntary deposit guarantee

_ Due to its composition/the techniques used by the fund

management, the Special Fund has a significantly increased

volatility, i.e., the share prices may also be subject to

significant fluctuations downwards or upward within a short

period of time.

_ The share value may at any time fall below the purchase price

at which the client has acquired the share.

Source: DWS International GmbH, as of: end of December 2019

/ 65DWS INVEST GLOBAL AGRIBUSINESS

Opportunities and risks

OPPORTUNITIES RISKS

_ Market, sector and company-specific _ Market, sector and company-specific

price gains price volatility

_ Possible exchange-rate risk

_ Because of its composition or the techniques used by its

managers, the fund is subject to heightened volatility.

Consequently, unit prices may fluctuate sharply in either

direction within short periods of time

_ The value of the fund's shares may fall below the price at

which the client originally bought them

As of: September 2019; source: DWS International GmbH

/ 66You can also read