Global Currency Dollar: What Next? Is Yuan Currency to Replace or Other

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Global Currency Dollar: What Next?

Is Yuan Currency to Replace or Other

Name of Author: Rajan J.Nandola

Designation: Asst.Prof.

Organization: Thakur college of Science and Commerce.

Address: Thakur College of Science and Commerce, Thakur village, Santa Nagar, Kandivali (E),

Mumbai-400101

E-mail ID: rajan20202000@yahoo.com, rajan20202000@live.com.

Name of Co-Author: Dipti. Deshpande

E-mail ID: dipti6us@gmail.com

Abstract: The global reserve currency is the one which forms the largest proportion of the

holdings of central banks. More broadly, it is also the currency most likely to be accepted by

merchants worldwide. The debate about whether the dollar will be replaced by the yuan is a bit

of a red herring because such a shift will not occur quickly. As of 2010, about 60% of all

foreign-exchange reserves were denominated in dollars, giving the US currency a critical mass.

Investors are still comfortable with holding it; despite the country's fiscal problems, in times of

crisis, the dollar is regarded as a haven. It will take a long while for international investors to

become confident that a Communist-led government will always respect their rights. The Yuan

has the potential but it will take another decade or two if china starts promoting the currency

strongly. If we see the macro-conditions it is in favor of china but have to improve the law. Even

euro was having the same view but the current crisis going on in European countries may not be

favourable for the currency in the international market. Well this had to be look after in the

further analysis.

Purpose – The purpose of this research paper is to find out whether Yuan or any other currency

may replace dollar in terms of reserve currency or trading currency or whether the Bretton woods

system would be revisited if crisis occurs.

Design/methodology/approach –

1) The Research will be mainly based on secondary Data collection, analysis and

interpretation.

2) Use of examples, charts and tables will be made to explain the intricacies of the Concept.3) Article from Journals and Reference Books will be referred for understanding the reasons

and the facts for the depreciation of the Indian Currency.

Findings – The findings would depend upon the analysis done, but according to the literature it

is found that the dollar would remain a reserve currency more 15 to 20 years but still the opposite

could be expected.

Research limitations/implications – The limitation of this paper is that the findings may

or may not happen if the macro economic conditions of the countries change dramatically.

Practical implications – The implication of the paper is to just understand whether there

will be drastic change over an international currency market or will remain the same

Originality/value – The charts and analysis will be used by taking into consideration by

using some econometric model.

Keywords: Bretton Woods pact, multipolarity, hyper-efficient markets, etc.

Executive Summary:

The paper is apropos, if any probability of Yuan becoming the next world reserve currency?

As we know dollar has played a dominant role as a reserve currency. After the 1978 and 2007

World Crisis, dollar’s position has changed as Current account deficit and US debt has increased.

In 1980 the US debt as a percentage of GDP was 25.777% which increased to 45.936% in 1990

and in 20th century increased to 73.101% for 2010. Meanwhile, Yuan’s exports to all Asian

countries and World have increased because the labour is cheap in china and products are

exported at very lower prices. This has affected the local markets production of different

countries as Chinese products are cheap. With this GDP of china has been increasing in 1990 it

was 3.8% which increase to double in 2000 which was 8.4% and in 2011 it was 9.1% (GDP

Growth Annual, The World Bank). China’s currency Yuan or (REINMIBI) has a long way to

become a World reserve currency because even after dollar, Euro, SDRs the country has to be

politically strong, Economic size, Trade and External Financial Strength, Economic reforms also

play an important part. China’s relationship with major economies such as US, Japan, India and

Russia will also determine the success of Yuan. If China is unable to garner the support of these

economies, which are expected together constitute around 60% of World GDP in 2030, the

crowing of the Yuan as the global reserve currency would be next to impossible. (Nishant, 2010)

We will support our thought with some data and facts.

Preamble

Since 1940s, U.S. dollar has served as a main reserve currency of the world. Dollars are

used throughout the World as medium of exchange and Unit of Account, and many nations store

wealth in dollar - denominated assets such as Treasury Securities. (Carbaugh and Hedrick, 2009).

The acceptance of Global currency reserve is generally determined as one of the form, largest

proportion holdings of central bank (which is accepted by Merchants Worldwide). A reserve

currency is determined by these fundamentals – the economic size of a country – includes GDP,

trade and external financial strength – the currency’s value should be preserved through low and

stable inflation by a country i.e macroeconomic stability. Even though Switzerland is a small

country Swiss Franc is used as a reserve currency. In today’s situation China has a chance toovercome America reason being the rising US indebtness and china’s strong financial and

economic prowess. To put it other way China’s trade is large, although the economy is small, it

has become a net creditor to many nations and US has become a net debtor. As a store of value

Yuan exchange rate is expected to rise over a period of time and dollar’s value will decline.

Nations like Nigeria and Chile want to use Yuan as a reserve not only as asset but want to satisfy

private – public sector demand.

China will take some 10 – 15 years to become a reserve currency, as it has to create a market

environment and policy to have Yuan as a global currency. Capital account is closed and that is

why Yuan is still not convertible and freely available. The financial system is repressed and

government controlled, with this the financial markets lack the sophistication to provide liquidity

for currency to be attractive.

Many economists are commenting that there are chances of Yuan appreciating by 1% and others

are arguing that if would depreciate by 1% for year 2012.

Dollar Dominance as a Global Currency:

The transition of dollar – pound, where US had started focusing on imports of raw materials and

exports of manufactured goods. Pound was playing the role of international reserve currency

built on the gold standard. After the World War I pound became very weak and Federal Reserve

was established in 1914. At that time US had high hopes of replacing Pound, but the aftermath

might have affected the overall stability of countries holding Pound as the reserve currency. In

1924 and 1927 US had helped Britain to restore the gold standard by lowering its discount rate.

The interest rate change was done to open the gap between dollar and Pound. With this interest

changes Britain could return to Gold Standard at Pre – war Parity in 1925 and 1927. The reason

for The Great Depression (1929 – 1933) was because of Stock market crash as Britain could not

maintain the convertibility of pound, for this reason it left the gold standard in 1930. The fear of

dollar devaluing increased the conversion of dollar into gold by different countries. US

abandoned gold standard in 1933.

In the year 1934 dollar was most attractive currency because it was convertible in gold. In 1944

the Bretton Woods System was formed and dollar became the major reserve currency. According

to Mundell, the Bretton Woods System was neither a gold standard nor a dollar standard

(Mundell, 2003) it was both. When different nations started using dollar as a comfortable

exchange reserve currency dollar became stronger than any other currencies. About 64 percent of

World’s official foreign exchange reserves are held in dollars, and about 86 percent of daily

foreign exchange trades involves dollar (Bank of International Settlements, 2007).

The question is why was US eager to replace Pound?

Firstly, Compared to the 19th century US economy had relatively started opening in the 20th

Century. The involvement in World Trade and Capital markets increased.

Secondly, for dollar as a World dominant currency it was very convenient and cheap to get the

resources in its own currency. The concept of Seignorage {Seignorage is the revenue that the

government makes from the gap between the cost of printing notes and minting coins and there

nominal value. (Mc Neill, 2005)}. This means the risk of exchange rate fluctuation and

transaction cost for third party transactions.

Does Yuan have a chance of becoming next global currency?

In the developing countries China has performed well and a decade it will become a high income

country. The GDP growth is be almost same at US. From the fiscal management point China hasalready performed similar or more than Europe and US. China’s economic prominence may shift from exports to domestic consumption, as it has wealth has educed. China should float its currency to have major economic power. During the 1997/1998 Asian Crisis and the 2007- 2010 World Financial Crisis and Economic Crisis, China has proved to be stabilizer for East Asia and the World (Gunther Schnabl, 2010). Global Financial Crisis gave a fair chance of cross – border use of Yuan. Currency used internationally provides lots of advantages. Firstly, it reduces the risk of exchange for private and public sectors and transactions of domestic currency can be done internationally. Secondly, financing of debt can be done by issuing its own currency. As the World’s banker, it can also borrow “Short “at low rates and lend “long” at higher yields, earning the spread, while as the world’s “venture capitalist”(Gourinchans P – O & H Rey, 2005), it can sell liquid, domestic - currency – denominated high - debt domestic grade to finance (domestic – currency – denominated) illiquid high return assets (Hausmann & Sturzenegger, 2006). Sustainability of net debtor position could be achieved in long run. Thirdly, International competitiveness could be beneficial by increasing the no of investors in financial market. Fourthly, the international use of reserve currency benefits as the value purchased per unit of commodity is raised. Comparison of China and US: The inspiration of US and China is the same. In the past, switching of the reserve currency from Pound to dollar shows a guideline, that chances of Yuan becoming reserve currency are by the mid of 20th century. In the year 1870 Britain lost its position to US as a largest economy and largest exporter. After this scenario, US became the net creditor and Britain became the net debtor. In 1945, dollar became the World reserve currency replacing the Pound. Comparing to the past at the time of Britain Pound and US dollar transition similar case is now with China being the net creditor and US has become the net debtor. China is on its way to become the largest exporter. The historic correlation doesn’t say that the addition of Yuan as a reserve currency is not mind – boggling. As the capital markets and foreign investment are concerned China’s opening has to be done, which is already done by US and Britain way back. China has to make currency fully convertible for transactions, by decreasing the restrictions on money entering and leaving the country. Continuing with the domestic financial reforms and making bond markets more liquid. In 2009, selected companies used Yuan to settle transactions in Hong Kong, Macau and Asian countries. China and Russia have entered in bilateral agreement for increasing the use of their currencies. Countries like Malaysia, South Korea, Indonesia and Hong Kong have made currency swap – agreements with China for making the import payments. The US General government net debt Figure 1 which is percentage of GDP indicates the healthy state of the economy. The debt – GDP ratio was 25.777 % in 1980 and in 2009 the debt – GDP ratio was 58.83% by the year 2017 it is estimated to increase about 88.422 %, according the IMF. The long term soundness of US debt is a question because the fiscal pressures are increased. The international role of dollar has become uncertain due to the fiscal bearings. Large scale deficits are there because under the perception of US treasury securities that dollar is the World’s only safe and liquid asset. This is the reason why there is long – term unemployment and hindered the progress of fiscal reforms. After a period US treasury will be less attractive in the market because of such reasons.

Figure 1

Source: IMF,

In the year 1980 the current account balance of US was 0.083 % which increased to – 4.184 % in

the year 2000 and is expected to be – 3.53% by the year 2017, according to IMF. The reason is

US had spent more on imports compared to exports. Broadly speaking there are two main

theoretical explanations for the persistence of this deficit, as well as diverging views of its

seriousness. One focuses on the rise of export – oriented economies in Asia and the desirability

of investment in US capital markets. This explanation posits that there is a “global saving glut”

which sees emerging economies wishing to park their export revenues in a stable and liquid

currency, creating a surplus of capital inflows that must necessarily mirrored by a matching

deficit in the current account. The other main explanation focuses on the high level of US

government debt and dis – saving by US households, arguing that the current account deficit is

driven by profligate household spending that will persist in the absence of policy reforms (World

Economic Forum , 2012)

Figure 2Source: IMF

The International Investment Position shows the direct investment abroad has increased. The

dollar diplomacy was achieved by US as it became the net creditor in the 19th century.

International Investment Position (End-Period Stocks)

In millions of U.S. dollars

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Assets

Direct investment abroad 66,655 70,758 76,850 84,096 91,265 103,332 122,727 151,157 163,530 170,021 190,803 213,062

Portfolio investment 28,682 38,601 58,200 101,568 122,057 147,342 197,791 248,951 188,909 253,016 315,934 314,906

Equity securities 12,478 18,516 22,895 38,466 40,127 46,350 89,251 138,580 70,296 119,306 150,981 137,036

Debt securities 16,204 20,085 35,305 63,102 81,930 100,992 108,540 110,371 118,613 133,710 164,953 177,870

Financial derivatives 1 - - 20 117 2,531 1,949 3,555 13,606 10,089 11,359 9,090

Other investment 67,343 73,944 68,727 72,686 109,340 128,564 149,038 180,399 191,273 206,076 220,390 259,573

Monetary authorities …. …. …. …. …. …. …. …. …. …. …. ….

General government 260 250 249 218 187 185 189 178 181 182 225 210

Banks 45,257 52,022 45,644 49,667 57,563 57,922 64,204 77,222 97,474 98,934 99,504 123,936

Other sectors 21,826 21,672 22,834 22,801 51,590 70,457 84,645 102,999 93,618 106,960 120,661 135,427

Reserve assets 111,370 126,572 166,046 211,139 246,561 257,952 270,840 275,027 296,389 352,967 387,206 390,590

Total assets 274,051 309,875 369,823 469,509 569,340 639,721 742,345 859,089 853,707 992,169 1,125,692 1,187,221

Liabilities

Direct investment in R.O.C.(Taiwan) 19,521 34,746 30,069 37,262 38,283 43,175 50,211 48,640 45,458 55,756 64,203 56,154

Portfolio investment 30,064 43,014 38,237 81,390 100,805 141,605 189,749 215,235 110,114 203,000 253,475 195,669

Equity securities 25,716 38,599 32,091 71,175 89,236 134,132 183,160 209,425 104,408 197,540 243,469 186,258

Debt securities 4,348 4,415 6,146 10,215 11,569 7,473 6,589 5,810 5,706 5,460 10,006 9,411

Financial derivatives 5 - - - 84 3,126 2,504 3,850 15,250 9,890 10,139 10,000

Other investment 31,972 35,448 43,208 54,752 89,817 106,929 114,605 122,977 119,439 122,055 152,225 184,814

Monetary authorities …. …. …. …. 4,476 13,727 10,416 3,116 - - - -

General government 23 16 10 4 3 3 2 2 1 1 - -

Banks 26,396 27,311 34,205 46,985 60,619 58,843 62,491 77,978 78,243 68,708 85,607 107,038

Other sectors 5,553 8,121 8,993 7,763 24,719 34,356 41,696 41,881 41,195 53,346 66,618 77,776

Total liabilities 81,562 113,208 111,514 173,404 228,989 294,835 357,069 390,702 290,261 390,701 480,042 446,637

Net International Investment Position 192,489 196,667 258,309 296,105 340,351 344,886 385,276 468,387 563,446 601,468 645,650 740,584

Chinese Government's Official Web Portal

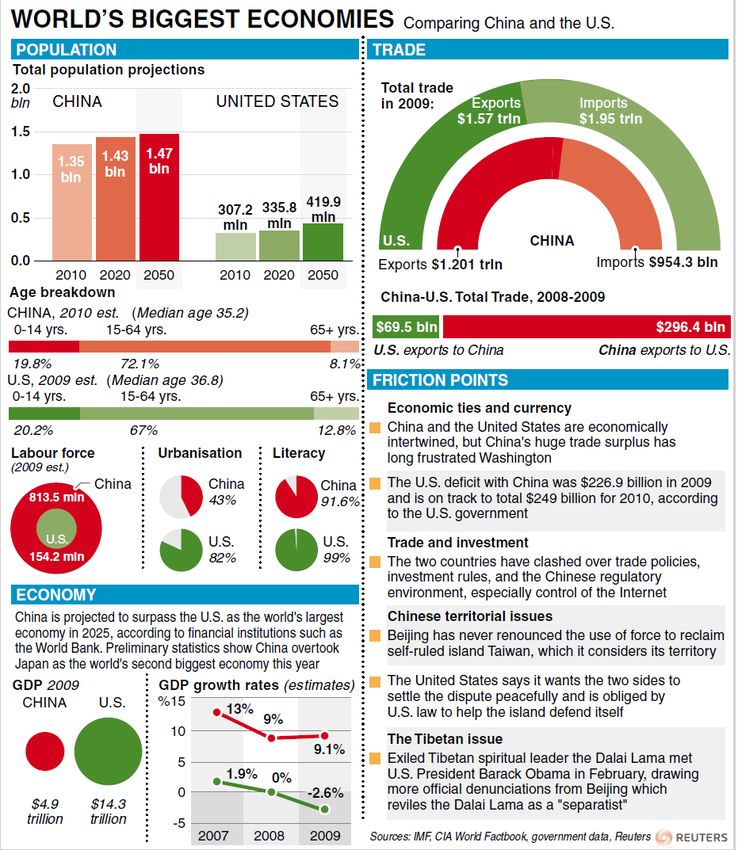

This diagram shows even though the position of population which will increase to about 1.47

billion in 2050 and for US it would be 419.9 million. From the trade point of view exports was

1.201 trillion for china which is still less than the exports of US. The imports are also less for

China. But a persistent growth in the economic reforms and politically strong relations with

different Asian and Developed countries would give a chance of Yuan replacing the dollar.Source: Returers 2010

Conclusion:

If the United States continues to spend and borrow at its present pace, and the Federal

Reserve maintains an easy monetary policy with low interest rates, the dollar’s status as a reserve

currency likely will continue to erode. When the world’s growing demand for liquidity subsidesas economic conditions return to normal, the United States could eventually lose the privilege of

being able to have the world’s main reserve currency. In spite of these uncertainties, there is a

shortage of currencies that could replace the dollar as the main reserve currency. To retain the

dollar’s reserve status, the Federal Reserve must be prepared to tighten its monetary reins. Doing

so will not be easy, particularly since large federal deficits probably will force lawmakers to

increase taxes, thus slowing future investment and growth. The demand for reserve currency has

increased over a decade and dollar doesn’t have a dominant role. Still China has a long way to

become the global currency.

Bibliography

Reports and Articles

1. Will Chinese Yuan be the next reserve currency? Nishant

2. Cost and benefits of running an international currency, by Papaiouannou and Portes

3. The Yuan charge, by Reuters

4. Yuan as reserve currency, by DB Research

5. Will the dollar be dethroned as main reserve currency? , Global Economic Journal,

Robert J. Carbaugh and David W. Hedrick

6. The future of reserve currencies, by Benjamin J. Cohen, Professor of International

Political Economy at the University of California, Santa Barbara

7. China’s Yuan: The next reserve currency? , by Steve Le Vine

8. CRS Report for congress China’s currency : Economic Issues and Options for U.S Trade

Policy, Wayne M. Morrison and Marc Labonte

Websites and databases

1. International monetary fund, IMF

2. World Trade Organization, WTO

3. World Bank

4. Bank of International Settlements, BIS

5. Social Science Research Network, SSRN

6. HIS Global InsightYou can also read