Will the Renminbi replace the US Dollar as the world currency? 2013

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2013 CRISIL Young Thought Leader Competition (CYTL), 2013

Will the Renminbi

replace the US Dollar

as the world

currency?

Submitted by: Ishan Abrol

Narsee Monjee Institute of Management Studies, Bangalore

1/1/2013

Table of Contents-

Executive Summary……………………………………………………………………………..3

Historical Ascent of Dollar……………………………………………………………………...4

Historical Precedent Analysis………………………………………………………………......4

Falling Empire of Dollar………………………………………………………………………..5

Internationalization of Renminbi; Roadmap towards replacing Dollar

…………………………………………………………………………………………………….5

East Asia’s Local

Currency…………...…………………………………………………………………………….7

Critical Analysis………………………………………………………………………………….9

Conclusion………………………………………………………………………………............10

2

Executive Summary

The stellar path of the Chinese economy has led Renminbi to play a prominent role in the global

trade and its potential to replace the US Dollar. With the changes in the liberalization policies,

development of financial markets, internationalization of Renminbi and backing the currency

with real asset, Renminbi has already become the East Asia’s Local currency. But close capital

controls, competition by other currencies and less transparent government policies may make the

road bumpier for Renminbi to rise as global currency.

The analysis in this paper is divided into two sections. The first section includes Historical

Precedent analysis with the current situation of China. The analysis illustrates the dominant

position of China in the future. As compared to America in 1920, china has huge reserves which

are not backed by real asset but are denominated in Dollar which will expose China to huge

systematic risk.

In the second section, China’s policy initiatives towards promoting Renminbi as world currency

is analyzed and critical factors affecting the internationalization process are tested. Though

China has taken major steps towards internationalization but China is far behind the US in terms

of strong financial institutional reforms which are must for promoting Renminbi as the reserve

currency.

Currently with the pace of reforms for the internationalization of Renminbi, Renminbi has the

prospects to become an active international currency.

3

Ascent of Dollar

Post World War II, for the efficient international trade and stable macro economic conditions,

US pegged Dollar to gold at $35 per ounce of gold which further gave other countries an

enticement to use Dollar as reserve. This was primarily due to the acceptance of gold as the

common medium of exchange at that point of time. Furthermore, in the later half of the

nineteenth century after the World War II, all the currencies in the world were pegged to gold,

which was an advantage for the US Dollar as the gold was denominated in US dollar. Hence post

1945, rising British borrowing in American Dollars and economic weakness of the UK led to the

growing importance of Dollar in the International Trade.

This led the US Dollar to overtake sterling as suddenly every currency became denominated in

Dollar.

GDP Dominance ( 1872 ) Reserve Currency ( 1945 )

Economic Dependence ( 1914 )

Historical Precedent Analysis

Current situation of the Chinese economy overtaking the US can be compared with the Sterling-

Dollar transition phase in the 20th century to know the prospects of Renminbi to replace the US

Dollar.

GNP- In 1890, US had overtaken the British economy to become the world’s leading economy.

But it took more than 40 years for the US Dollar to dethrone the British Sterling to become the

supreme currency in 1944. Over the past decade, China has grown at an average rate of 8% and

is expected to surpass the US economy by next decade. Therefore, Renminbi has the potential to

become the sovereign currency by the next 15-20 years.

Financial Position- Post World War 1, due to the increasing borrowing by British, US became

net creditor and consequently it became the prime exporter in the world. Similarly, in the present

scenario, Chinese economy has become the largest net creditor with more than $2 trillion in

exports while US is on the opposite position. US’ situation is similar to the situation faced by UK

post World War I.

Reserve Holdings- Moreover, growing Chinese dominance in the international trade requires the

trading countries to hold their reserves in Chinese currency. However, Renminbi is not backed

by real assets. In the 20th century, other countries held Dollar because it was backed by gold; to

make Renminbi an international currency; it must be backed by some real asset. Further, it

should not erode the value of Dollar reserves held by China.

After World War II, high debt British economy fell to Americans who held the largest British

debt at that time. Currently, china is the largest creditor to the world. So, if Historical pattern is

an indicator that that the reserve currency would be replaced, then it would be Renminbi.

4

Falling Empire of the US Dollar

Despite the reserve currency status of US Dollar, the current macroeconomic and financial

instability in US is adversely affecting the future prospects of US dollar.

First of all, US accounts for 19% of the world GDP in comparison to more than 40% in 1960.

Likewise, the huge decline in exports of goods and services raises the question whether US

Dollar should still be used as a reserve currency which accounts for 60% of the world forex

reserves.

Debt- The current US gross government debt has reached 110% of the GDP. This situation is

similar to situation in 1924 when gross debt to GDP reached to 136% due to the budget deficit,

war financing and Debt. This is reducing the credibility of the world’s largest economy.

Subprime Crisis- The 2008 subprime crisis has led the emerging market economies to

accumulate reserves other than US Dollar to diversify due to which the confidence of the global

markets is decreasing in US Dollar. Quantitative Easing by US Fed is further decreasing the

value of the Dollar foreign exchange holdings and creating a major volatility in the currency

markets.

Petrodollar Arrangement-America was the largest oil importer provided an important incentive

to other countries to peg against Dollar. Being a monopolized commodity, countries producing

oil benefit from Dollar as a reserve currency. Petrol Dollar arrangement is one of the important

reasons for Dollar dominance. However, now China is the largest importer of oil. Bilateral

agreement between UAE & China for oil purchase in Renminbi and growing trade relations with

Saudi Arabia, Russia to establish new oil refineries is challenging the Petro Dollar agreement.

The above discussion clearly illustrates that if the value of the dollar depreciates, US debt

holders will have to pay more and investments funded with US Dollar will value less. All these

factors are not a positive sign for US Dollar to retain its supremacy.

Internationalization of Renminbi; Roadmap towards replacing Dollar

Today, China is not only the world’s second largest economy but also the largest Trading

economy. However Renminbi trade settlement is meager as compared to the growing Chinese

dominance. Hence, it has become necessary for China to internationalize its currency.

5Besides comparing the Chinese Renminbi with the transition of Sterling to Dollar, another

inclination towards Renminbi as a reserve currency is the Chinese internationalization policies.

This will further help the Renminbi to become the trade & settlement currency, a financial

transaction currency and in subsequently replacing the US Dollar in the near future.

Renminbi denominated bilateral swaps- Majority of China’s trade with other countries has

started getting invoiced in the Chinese currency already. After the sub-prime crisis and in order

to internationalize its currency, PBOC (People Bank of China) has entered into Renminbi

denominated swaps worth $300 billion with more than 19 countries, further enhancing the trade

in Renminbi. Recently in October 2013, China entered into Forex Swap with Euro zone with the

transaction size of 350 billion Yuan and 45 billion Euros.

These initiatives have brought financial stability, enhancing liquidity of Renminbi in the foreign

markets, therefore enabling Yuan to become a medium of exchange.

Direct Trading and Financing in Renminbi- Previously, USD was required as an intermediary

currency to trade Renminbi with other foreign currencies but recently China launched a direct

trading platform with Japanese Yen, Australia dollar, New Zealand Dollar and Thai Baht.

Another important initiative has been to allow foreign companies to raise money in Renminbi in

securities market. Institutions such as ADB & IFC have raised money by issuing Panda Bonds

and local Foreign Multinational banks have also issue Bonds in Renminbi.

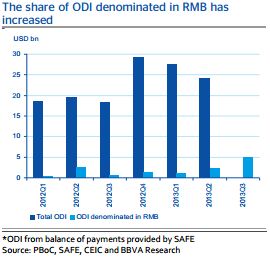

Foreign Direct Investments- Currently, China represents around more than 9% of the Global FDI

in 2013. More than 50% of the outward foreign direct investment from China is in Renminbi

which shows the paradigm shift of merely trade currency to investment currency. Renminbi

Internationalization and development of offshore Renminbi centers in Singapore, London and

Taiwan are creating more opportunities for Chinese Multinationals for outward FDI in

Renminbi.

Invoicing in Renminbi and establishing of swap contracts with other countries illustrate the

Chinese motivation to become the lender of last resort in times of crisis and liquidity crunch.

Furthermore, it will reduce the exchange rate risk faced by the Chinese companies in the global

markets.

6East Asia’s Local Currency

Recent research has shown that Renminbi has become a dominant reference currency (invoicing

in Renminbi) leading to the De-Facto Renminbi currency block in East Asia. Seven countries out

of the ten countries in East Asia are tracking Renminbi more closely than Dollar due to the rising

trade prospects with china. Emerging markets also account for 67% of the China’s imports and

56% of its exports. It is more beneficial for these countries to have a stable exchange rate with

China. So, presently Chinese Renminbi is becoming East Asia’s local currency. It is too early to

say whether or not in the near future Renminbi will replace the USD worldwide but in East Asia

it has already replaced the USD to a certain extent.

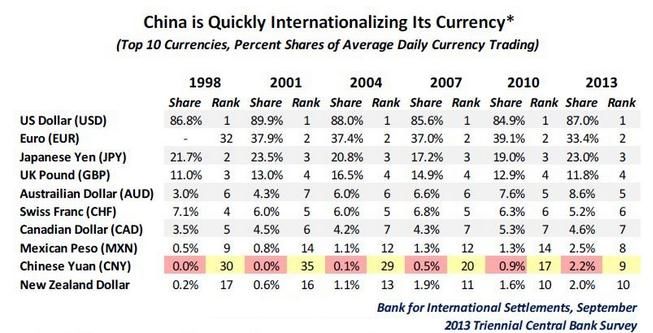

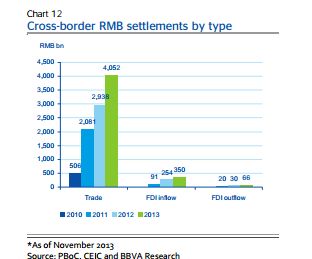

Post 2010, 18% of China’s exports has been settled in Renminbi. Renminbi has become world’s

9th most traded currency in the world in just three years but this number can take a giant forward

leap if china adopts the floating rate currency regime.

7Now, more than 10,000 banks worldwide are offering their customers to settle their trade

transactions with China in Renminbi in comparison to 900 Banks in 2011. The pool of offshore

Renminbi settlement is around $143 billion dollars which has been into existence since 2010.

Now more than 16% of the Chinese trade is settled in Renminbi. Strikingly, Chinese bond

market has grown exponentially from 69 billion Renminbi to 405 billion Renminbi. This

paradigm shift shows the potential of Renminbi to replace the dollar in the long term.

Since 2012, the Chinese Currency market (CNY Market) has become one of the fastest growing

markets worldwide.

Despite being the world’s largest trading nation and the second largest economy, Renminbi’s

share in the global trade compared to major currencies is insignificant. Growing CNY market

and importance of Renminbi in trade settlement are long term initiatives of China to create an

alternative to US Dollar as the world currency.

8Critical Analysis-

The most important question that Chinese policymakers have to answer is: Would the Chinese

Government have more benefits in bringing flexibility in controls in exchange for

internationalization of Renminbi?

China is aggressively trying to internationalize its currency but the policies adopted to do full

internationalization are daunting for a conventional Chinese policymaker. Cost of being a reserve

currency will be higher for China as compared to US or UK because once China liberalizes the

capital controls; it will lead Renminbi to appreciate significantly. It was different in case of US

because being a consumption driven economy and leader in technology exports faced less

currency appreciation pressure. Unlike US, China has a long way before it can become a leader

in technology exports.

China’s export comprises of 48% of the GDP and Chinese Renminbi appreciation will adversely

affect the competitiveness of its export sector and economic growth.

China’s Trilemma- In 1960, Noble prize winner Robert Mundell inferred that a country at one

time can’t have an open capital account, along with control over interest rates and currency. For

a country like China which is having a fixed currency rate and restricted capital conversion, it

will be a very tough task to decide on the tradeoff between giving up of the controls and

Internationalization of Currency.

China needs to have higher financial stability and economic integration than those of US to

replace Dollar.

Apart from the above impediments, there are other roadblocks for Renminbi to become the

reserve currency which can be imputed to the following factors-

1. Dollar as Safe Asset- Post subprime crisis, USD is regarded as the safe haven as it global

turnover increase from 2007 to 2013. But in 1940, post crisis Pound weakened and its

global share also reduces. This further explains the strong belief of the global investors in

the USD.

2. Competition- Earlier US Dollar had no competition other than Pound but Renminbi is

facing competition from the Euro and the SDR (Special Drawing Rights). Euro is the

second largest reserve currency with 23.8% share in the global reserves. Growing

importance of SDR will also challenge the dominance of Renminbi

3. Dollar Dilemma-. To replace the dollar as a reserve currency it is very important for the

Chinese Central Bank to exonerate the Dollar reserves with less volatility in the forex

market.

4. Low Inflation and Macroeconomic stability- To have the macroeconomic stability and

low inflation for the support of reserve currency, a country should have full currency

convertibility and free floating exchange rate.

9It will be a long term goal for Chinese officials to regulate the capital controls because in

a short span, the pegged exchange rate and stringent capital control will lead to the

unsustainable monetary imbalances in the Chinese economy.

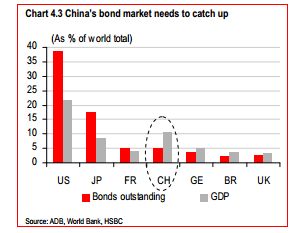

5. Depth of Financial Markets- Chinese Securities and Bond market are in its nascent stage.

In spite of the broad steps taken by the Chinese policymakers such as creation of high

yield junk bond markets, introduction of collateral debt swap transaction for private

sector, Chinese bond and securities market is far behind than the developed countries

capital markets. Further, Chinese policy makers also have to take a step to strengthen its

derivative market. Moreover, Global investors are not allowed to take part in the

derivatives or the money markets.

The above factors such as strong political, economic, social stability factors can only make

US economy and Dollar stronger as compared to the Chinese economy. China has to make

major restructuring changes in its whole system to challenge the USD. Furthermore, USD

can be called as the English language of the Forex Markets because most commodities such

as oil are priced in US Dollar just like most people interact in English with each other.

Conclusion-

A conventional wisdom proposes that any successful internationalization process should also

complement with the open policies of the government, relax capital controls, flexibility of

exchange rate and depth of financial reforms. Presently, China is not ready to replace USD in the

near term and if history is any guide, then possibly by the Year 2040, Oil prices reaching 600

CNY/Barrel causing inflationary pressure in countries like India. The MSCI World Index, all the

commodities and Trade will be denominated in the world’s most traded currency.

Internationalization of currency is a multi-stage process which begins with promoting local

currency as a trade currency than the investment currency before becoming the reserve currency.

China is at stage one where it is establishing itself as a trade currency. Thereafter, in the medium

term it will be an addition to the other reserve currency or basket of currencies before dethroning

the US Dollar. Renminbi will become an important reserve currency within the next decade but

prospects of surpassing the Dollar as the reserve currency in the near term doesn’t look so much

probable.

10Bibliography

Arvind Subramanian, M. K. (2012, October). China's Currency Rises in the US Backyard.

Financial Times.

Arvind Subramanian, M. K. (2013). The Renminbi Bloc Is Here: Asia Down, Rest of the World

to Go? Pterson's Institute of International Economics.

BBVA Research. (2013). China’s outward FDI reaches new highs on strong growth in 2012-13.

China Economic Watch.

BBVA Research. (2013, May 27). China’s RMB Bilateral Swap Agreements: What explains the

choice of countries?

Bowles, P. (2011). Renminbi Internationalization: A Journey to Where?

Chuling Chen, R. Y. (n.d.). RMB as an Anchor Currency in ASEAN, China, Japan and Korea

Region1.

DBS Group Research. (2013, March). A global RMB: inventing the necessary.

Dr Zhou Xiaochuan. (2009, March 23). Reform the international monetary system. Bank of

International Settlement.

Eswar Prasad, L. (. (2013). The Renminbi’s Role in the Global Monetary System. Global

Economy and Development at Brookings.

Eswar Prasad, L. Y. (2013). The Renminbi’s Prospects as a Global Reserve Currency. Cato

Journal.

HSBC Global Research . (2013, March). The rise of the redback II. HSBC Global Research.

Lee, J.-W. (2010). Will the Renminbi Emerge as an International Reserve Currency? Asian

Development Bank.

R. Sean Craig, C. H. (2013). Development of the Renminbi Market in Hong Kong SAR:

Assessing Onshore-Offshore Market Integration. IMF Working Paper.

Robert N McCauley, P. M. (2009). Dollar appreciation in 2008: safe haven, carry trades, dollar

shortage and overhedging. Bank of International Settlement.

Ryan, J. (n.d.). China, the Eurozone and Global Reserve Currencies. Centre for Economic

Policy.

Schenk, C. R. (2009). The Retirement of Sterling as a Reserve Currency after 1945: Lessons for

the US Dollar? International Monetory Fund.

UBS Investment Research. (2012, August). From Here To Eternity.

11Vass, T. E. (2013, Feburary 22). The Uncertain Future Of The US Dollar as The Global Reserve

Currency.

Yukon Huang, C. L. (2013). Does Internationalizing the RMB Make Sense for China? Cato

Journal.

Websites and Database

World Trade organization, WTO

International Monetary Fund, IMF

People’s Bank of China, PBC

Seekingalpha.com

Financial Times, FT.com

Forbes.com

12You can also read