GLOBAL EMERGING MARKETS DYNAMIC FUND - December 2020

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

GLOBAL EMERGING MARKETS

DYNAMIC FUND

December 2020

eastspring.us/offshoreadvisor

2

LEADING ASSET MANAGER IN ASIA

LEVERAGING OUR ASIAN DNA TO CAPITALISE ON GLOBAL OPPORTUNITIES

1994 One of the

USD 248bn 300+ INVESTMENT DEEP INSIGHTS

Founded 1994 in Managing USD 248bn

PROFESSIONALS^ LARGEST INTO ASIA

Singapore (HQ) and assets on behalf of

100% owned by institutional and individual

Unrivalled on-the-ground ASIAN ASSET Our investment teams'

investment presence in Asia deep understanding of

Prudential plc (UK) investors globally MANAGERS Asian markets, provides us

and a major Asian Fixed with a unique perspective

Income player for global investments

United

Kingdom

Luxembourg

Japan

United States China* South Korea

Taiwan

India* Hong Kong*

Thailand*

Vietnam

Malaysia

Singapore

Indonesia

Investment and Sales & Client Service office

Sales & Client Service Office

Joint venture

Source: Eastspring Investments. As at 31 December 2020. ^Including joint ventures and sales offices in the US, UK and

Luxembourg. AUM size by contracted sales. Note: bn = billion.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.

3

A DIVERSIFIED AND GROWING GLOBAL ASSET MANAGER

AUM Growth (USD bn)

2% 7% 241 248

193

47% 12% CAGR 188

40% 146

131

99 121

95

81 78

51%

Fixed Income Equity Quant

Others ^ Investment Solutions (IS)

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Internal Life 56% Third Party 44%

AUM USD248bn

Source: Eastspring Investments as at 31 December 2020. AUM includes Joint Ventures AUM based on % of ownership

*Joint ventures: India - ICICI Prudential Asset Management Co Ltd, Hong Kong - Bank of China International – Prudential Asset

Management and China - CITIC-Prudential Fund Management Co Ltd. ^ Others – include Alternative assets and money market

funds. Note: bn = billion.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.

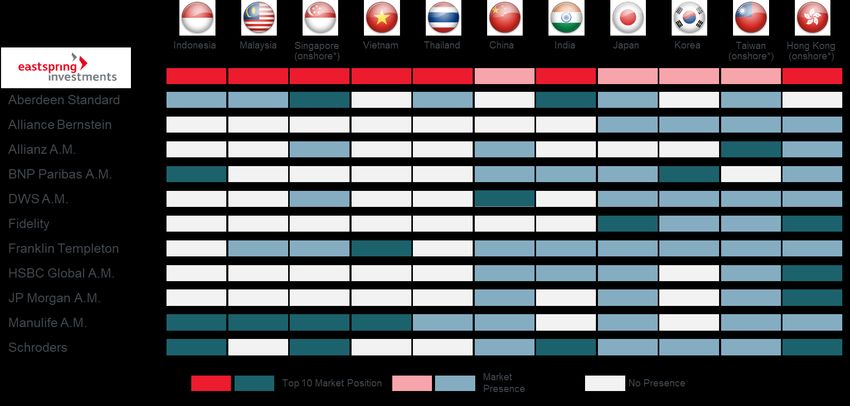

4 EXTENSIVE LOCAL PRESENCE IN ASIA ONSHORE ASSET MANAGEMENT ACROSS ASIA Sources: Singapore and Hong Kong (Morningstar), Malaysia (Lipper), Thailand (Association of Investment Management Companies), Korea (Korea Financial Investment Association), India (Association of Mutual Funds in India), Japan (Investment Trusts Association, Japan), Taiwan (Securities Investment Trust & Consulting Association of R.O.C.), China (Wind), Indonesia (Otoritas Jasa Keuangan), Vietnam (State Securities Commission of Vietnam). All markets as of December 2020. Eastspring JVs include HK, India and China. Japan reflects Publicly Offered Investment Trusts market presence. China reflects public mutual funds market presence. Vietnam reflects open-ended mutual funds market presence only. *Market presence based on whether the AMCs offer onshore domiciled mutual funds. Market ranking based on 100% shareholdings. STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.

5

INVESTMENT CAPABILITIES OVERVIEW

Fixed Investment Quantitative

Equities Income Solutions Strategies

AUM of AUM of AUM of AUM of

USD 25bn USD 62bn USD 115bn* USD 3.5bn

Key capabilities: Key capabilities: Key capabilities: Key capabilities:

GEM Concentrated Value EM Debt Multi Asset Global Low Vol

Japan Concentrated Value Asian HY Solutions Asian Low Vol

China A Growth Asia Fixed Income Multi-Factor

Greater China Asian Sustainable

Asia ex – Japan China RMB

Number of Inv. Number of Inv. Number of Inv. Number of Inv.

professionals: 31 professionals: 22 professionals: 12 professionals: 8

Avg. yrs experience: Avg. yrs experience: Avg. yrs experience: Avg. yrs experience:

18 15 14 13

Source: Eastspring Investments as at 31 December 2020. AUM for investment teams are internally calculated and includes advisory

mandates. There might be double counting of assets within the individual investment teams. The figures above do not reflect joint venture

assets under management. *Including sub-funds managed by other teams and investments into Eastspring SICAV funds. Note: bn =

billion.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.

6

FOCUSED - EQUITY INVESTMENT CAPABILITIES

Strategy Name GEM Dynamic Global Low Vol Japan Focused Value China A Shares

Primary Benchmark MSCI Emerging Markets Index MSCI ACWI Min Vol MSCI Japan Index^^ MSCI China A Net TR Index

Seeks to outperform the Seeks long-term capital growth, Seeks long-term growth of capital

Seeks to deliver higher risk-

benchmark over a full market invested in companies listed in by investing in a concentrated

adjusted returns than the broad

cycle by investing in a Japan. High conviction, portfolio of China A shares listed

Investment Objective market by targeting a low volatility

concentrated portfolio of significantly mispriced companies primarily on the Shanghai or

portfolio and avoiding undesirable

emerging market domiciled compared to long-term sustainable Shenzhen exchanges via Stock

biases

common equities. earnings. Connect.

Fundamental, benchmark- Bottom up high conviction, Top-down/bottom-up, benchmark

Quant, benchmark-aware

Investment Style aware benchmark unconstrained agnostic.

All-Cap Value Large Cap Core All-Cap Relative Value Concentrated, Quality Growth

Strategy AuM (USD) 1,594mn 551mn 1,651mn 243mn

Strategy Inception Date Oct 2010 Nov 2015 Jan 2005 Apr 2019

Ben Dunn Portfolio Manager: Jie Lu

Lead Portfolio Manager Andrew Cormie Chris Hughes Dean Cashman

Research Advisor: Michelle Qi

ESG Integration √ √+ √ √

Key Investment Parameters*

Typical No. of Holdings 40-60 350-400 30-50^^ 30-50

Expected Alpha** 2.5% 1.0% 1.5-4.0%^^ 4%

Expected Active Risk (TE) 4-6% 5-8%^ 3-8%^^ 4-10%

Typical Active Share 80-90% 80-90%^ 80-90%^^ 60-80%

Typical Beta (Historical) 1.00 0.80 NA 1.00

Max Country Weight +/-10% relative +/- 5% relative NA NA

+/-10% relative

7

WHY EASTSPRING?

Pursuit of alpha through a differentiated,

DIVERSITY OF

Asian lens OUR PEOPLE AND

PERSPECTIVES

History of operating in some of the most

diverse, illiquid and inefficient markets

positions us well for emerging and

developed markets investment

56% 40% of female

Alignment of interests and history of of our workforce representation in our

is female Executive Management

investing alongside our clients

Committee

Commitment of seed capital to innovate

new strategies and willingness to

customize solutions for clients

27

nationalities

Risk management is embedded in our

DNA with a long history of managing

liability-linked assets

As of 31 December 2020.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.

MARKET OVERVIEW

9

GEM DYNAMIC FUND

KEY MESSAGES

We believe our value style can generate superior long-term returns in

Global Emerging Market (“GEM”) equities.

Behavioural biases create a structural opportunity for us to exploit over

time and we have seen a substantial valuation opportunity created in GEM

equities over the last few years.

In recent months we have seen the start of a reversal in some of these

biases which has supported Value outperformance.

The Eastspring Investments - Global Emerging Markets Dynamic Fund is

well positioned to take advantage of the value opportunity over time.

Source: Eastspring Investments, 31 December 2020. This is only for information purposes. It is not intended as an offer or

solicitation for the purchase or sales of any financial instrument, investment product or service.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.

10

VALUE HAS OUTPERFORMED IN GEM EQUITIES OVER

THE LONG TERM

GEM Style Indices – Cumulative Factor Performance over the MSCI Emerging Markets Index

300%

200%

250%

150%

200%

100%

150%

50%

100%

0%

50%

-50%

0%

-100%

-50%

2009 2011 2012 2013 2014 2016 2017 2018 2019

1999 2002 2004 2007 2009 2012 2014 2016 2019

Value Momentum Quality Growth

Value Momentum Quality Growth

Source: Eastspring Investments, 31 December 2020. Market cap weighted. Returns of respective factors reflect the cumulative returns taking the

performance of the bottom quintile of stocks from the top quintile of stocks, rebalanced on a monthly basis, from 31 December 1999. The style

index described is unmanaged and not available for direct investment. Please note, there are limitations to the use of such style indices as proxies

for the past performance in the respective asset classes/sector. The historical performance or forecast presented in this slide is not indicative of,

and should not be construed as being indicative of, or otherwise used as a proxy for the future or likely performance of the Strategy.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.11 GLOBAL EMERGING MARKET ARE VERY CHEAP RELATIVE TO DEVELOPED MARKETS Source: MSCI, Refinitiv Datastream, Eastspring Investments, 31 January 2021. Notes: PB = Price-to-book. STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.

12

THERE IS STILL EXTREME VALUE DISPERSION AT A STOCK

LEVEL

3.1 GEM Valuation Dispersion

2.9

2.7

2.5

2.3

2.1

1.9

1.7

1.5

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Valuation Dispersion Average 1 Standard Deviation

2 Standard Deviations 3 Standard deviations

Source: Eastspring Investments, 31 December 2020. Valuation dispersion is defined as the Forward 12 month price to earnings ratio of the top

quintile of the research universe divided by the forward 12 month price to earnings ratio of the bottom quintile of the research universe. The

research universe is defined as the top 95% by market capitalisation of the S&P Emerging BMI. The historical performance or forecast presented

in this slide is not indicative of, and should not be construed as being indicative of, or otherwise used as a proxy for the future or likely performance

of the Strategy.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.13

QUALITY AND GROWTH NAMES ARE EXTREMELY EXPENSIVE

THIS IS AN OPPORTUNITY FOR VALUE INVESTORS

EM Quality Relative to EM Value PE EM Growth Relative to EM Value

1.5 PE

1.35

1.4 1.3

1.25

1.3

1.2

Growth Relatively

Quality Relatively Expensive

1.2 Expensive 1.15

1.1

1.1

1.05

1

1 Growth

Quality 0.95 Relatively

Relatively Cheap

0.9 Cheap 0.9

01 03 05 07 09 11 13 15 17 19 01 03 05 07 09 11 13 15 17 19

Quality PE / Value PE Average 1 SD 2 SD Growth PE / Value PE Average 1 SD 2 SD

Source: Macquarie Quantitative Research, 31 January 2021. Relative PE (price-to-earnings) of top quintile of quality (by Macquarie quality score)

versus top quintile of value (by Macquarie value score) stocks and top quintile of growth (by Macquarie growth score) versus top quintile of value

(by Macquarie value score) stocks in MSCI Emerging Markets.14 WE BELIEVE WE ARE POSITIONED TO CAPTURE THIS OPPORTUNITY POTENTIAL UPSIDE FROM HERE IS STILL LARGE Source: Refinitiv Datastream, Eastspring Investments, 31 January 2021. MSCI Emerging Markets Index. Please note that there are limitations to the use of such index as a proxy for the past performance in the respective asset classes/sector. The historical performance or forecast presented in this slide is not indicative of and should not be construed as being indicative of or otherwise used as a proxy for the future or likely performance of the Strategy. Charts are for illustrative purposes only. The index described is unmanaged and not available for direct investment. PB: Price-to- book. STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.

15

WE ARE POSITIONED IN ATTRACTIVELY VALUED STOCKS

PEERS ARE POSITIONED IN EXPENSIVE STOCKS

MSCI Emerging Markets index peers top 10 active Value Strategy top 10 active positives look cheap

positions look expensive

45

45

40 40

35 35

30 30

25 25

20 20

15 15

10 10

5 5

0 0

PB Average MSCI EM Index

PB Average

Source: Refinitiv Datastream, Eastspring Investments, 31 December 2020, Top 10 peer names sourced from BofA Merrill Lynch Global

Quantitative Strategy, MSCI FTSE, Thomson Reuters Datastream, 13F Filings, Benchmark Indices, Country Stock Exchanges. Please note

that the securities mentioned are included for illustration purposes only. It should not be considered a recommendation to purchase or sell

such securities. There is no assurance that any security discussed herein will remain in the portfolio at the time you receive this document or

that security sold has not been repurchased. The securities discussed do not represent the entire portfolio and in the aggregate may

represent only a small percentage of the portfolio holdings. PB = Price-to-book. Both sets of data are sorted by PB, with the highest PB

from the left to right.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.16

WE ARE A GOOD DIVERSIFIER TO MOST OTHER

GEM MANAGERS

Average correlation of Active Returns of eVestment

GEM Equity All Cap Universe

GEM Dynamic Strategy

Source: eVestment, Eastspring Investments, as at 31 December 2020. Correlation of active returns calculated on all eVestment Emerging equity all

cap universe (109 funds). Strategies with track records spanning December 2010 (Eastspring GEM Composite Inception) to current date specified.

Chart is for illustrative purposes only.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.PHILOSOPHY, PEOPLE & PROCESS

18

OUR FLAGSHIP GEM EQUITY STRATEGIES

GEM Dynamic GEM Fundamental Value

Concentrated stock picking Value driven

Focused on best ideas, not the Index Diversified exposure

Holistic risk management Holistic risk management

Lead portfolio manager Andrew Cormie Steven Gray / Sang Hoon Lee

Benchmark MSCI Emerging Markets Index MSCI Emerging Markets Index

Typical no. of holdings* 40 – 60 80-100

Target alpha** 2.5% 1.5%

Target tracking error 4-6% 2-4%

Country/sector range Broadly Diversified Broadly Diversified

Market capitalisation Multi Multi

Inception date 29 October 2010 1 July 2017

Strategy size USD 1594 mn USD 2,919 mn

Base currency USD USD

Fund Benchmark Active Fund Benchmark Active

PB (F12m) (x) 0.9 2.0 -1.1 1.1 2.0 -0.9

PE (FWD 12m) (x) 10.0 15.7 -5.7 10.5 15.7 -5.2

Div Yld (FWD 12m) 1.0

3.6 2.3 1.3 3.3 2.3

(%)

Number of holdings 50 1,363 - 78 1,363 -

Source: Eastspring Investments. Fund size and specification, as at 31 January 2021. *Subject to changes at the sole

discretion of the manager. **This should not be construed as a guarantee for outperformance. PB = price-to-book ratio,

PE = price-to-earnings ratio, FWD 12m = 12-month forward, Div Yld = Dividend yield.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.19

GEM EQUITY

INVESTMENT PHILOSOPHY

Price-focused process with a valuation anchor that seeks to generate

superior long-term returns

Prices frequently move more than justified due to shifts in investor risk

perception and expectations

Behavioral biases influence both investor expectations and risk appetites

True underlying value is not always reflected in price

Opportunities exist – emotional detachment, rigorous analysis and

discipline over a longer-term horizon provides opportunities

Source: Eastspring Investments, The above views are subject to change at the manager’s discretion without prior notice.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.20

WHAT IS OUR INVESTMENT EDGE?

We believe behavioral biases drive mis-pricing. Our structure, process

and tools deliberately and repeatedly target this mis-pricing.

As a result we…

Have a DISCIPLINED PROCESS that focuses us on VALUATION

OUTLIERS

Take a LONGER HORIZON, allowing us to focus on SUSTAINABLE

EARNINGS

Structure our TEAMS to maximise CHALLENGE and DEBATE

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.21

EQUITY TEAM

CLEARLY DEFINED RESPONSIBILITIES

ANDREW CORMIE (13/39) JOHN TSAI (4/25)

GEM AND REGIONAL ASIA VALUE EQUITY REGIONAL ASIA CORE EQUITY

CHINA-INDIA /

GLOBAL

REGIONAL ASIAN GREATER EQUITY REGIONAL

EMERGING ASEAN INDIA CORE

ASIA VALUE SMALLER CHINA INCOME ASIA CORE

MARKETS

COMPANIES

Andrew Cormie* Sundeep Bihani Krishna Kumar* John Tsai* (4/25) Pearly Yap* (10/26) Wing Kin Chow* John Tsai* (4/25) Anand Gupta*

(13/39) (13/18) (12/26) Kieron Poon (8/10) Katerina Irwan (21/25) Arthur Chai (9/24) (11/24)

Steven Gray (8/33) Andrew Cormie Yuan Yiu Tsai Bonnie Chan (5/16) (14/16) Bryan Yeong (8/19) Ding Wei Ko

Sang Hoon Lee (13/39) (3/14) Nathan Yu (3/9) Peishee Seah Jie Yang Lee (1/5) (22

EXPERIENCED GEM TEAM

GEM FOCUS

TEAM LEADER

Sang Hoon Lee Paul Chong Mandeep Sachdeva Samuel Bentley

Client Portfolio Manager

YRS 16 / EXP 25 YRS 7 / EXP 14 YRS 5 / EXP 19 YRS 12 / EXP 21

Andrew Cormie

YRS 13 / EXP 39

Steven Gray Navin Hingorani Luiz Pinho Megan Ie

YRS 8 / EXP 33 YRS 10 / EXP 21 YRS 6 / EXP 16 YRS 9 / EXP 12

Source: Eastspring Investments, 31 January 2021

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.23

POWER OF THE COMMON RESEARCH PLATFORM

GIVES ALL CLIENTS ACCESS TO THE BEST THINKING OF A DIVERSE

TEAM OF SEASONED INVESTORS

What is our Common Research Platform?

All Focus All Focus Teams All research is

Teams screen confirm if value shared across

their universe exists using a Focus Teams

to identify common company and is subject

valuation valuation model to to debate and

outliers identify underlying challenge by

value based on seasoned

sustainable investment

earnings professionals

Source: Eastspring Investments, The above views are subject to change at the manager’s discretion without prior notice.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.24

GEM EQUITY

FOCUSED TEAM APPROACH

Small, very experienced group with significant buy-in

Small, experienced, cohesive team of eight investment professionals

Deep financial industry experience

Deliberate strategy to differ from many core investment managers –

typified by large teams delivering maintenance research across the

investment universe

How do we differ?

We are a strong, centralised team that operates under a culture of

challenge and debate, equipped to maximize a creative team dynamic

We focus on best opportunities

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.25

INVESTMENT PROCESS

DISCIPLINE FOCUSES SKILL

(1)

IDEA

GENERATION

1 Identify maximum

impact opportunities

(4) (2)

2 Deepen understanding and test

RISK CONTROL FUNDAMENTAL

conviction & REVIEW ANALYSIS

3 Establish and monitor the

risk / reward relationship

4 Ensure integrity of investment (3)

process PORTFOLIO

CONSTRUCTION

Source: Eastspring Investments. The above views are subject to change at the manager’s discretion without prior notice.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.26

IDEA GENERATION

Identify episodes offering potential excess returns. The team allocates

resources to best ideas

Proprietary screens using ten years of market data; long-term valuation criteria

Identify large deviations of stocks relative to own history and universe:

PE, PE relative to the market, and relative to history

PBR, PBR relative to the market, and relative to history

FCF Yield, FCF Yield relative to the market, and relative to history

Dividend Yield, Dividend Yield relative to the market, and relative to history

Price performance

Broker sentiment and earnings revision analysis

Source: Eastspring Investments. The above views are subject to change at the manager’s discretion without prior notice.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.27

IDEA GENERATION

FOCUSING ON VALUATION OUTLIERS

We focus on the valuation outliers

300

Number of

250 Stocks

200

150

100

50

0

-1.88

-1.63

-1.38

-1.13

-0.88

-0.63

-0.38

-0.13

0.13

0.38

0.63

0.88

1.13

1.38

1.63

1.88

Frequency distribution of a Valuation Z score

Cheap Expensive

Screen on widest universe (c3,300*) to eliminate biases or sector country framing

Narrow down to an investible universe (c500) using a range of valuation metrics

This then allows for efficient allocation of research resources (c100 ‘first looks’ p.a.)

This is the first step towards fundamental analysis (c20-40 deep dives p.a.)

Source: Eastspring Investments. * Including emerging market and frontier market listed equities. The graph and information are

included for illustrative purposes only.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.28

VALUATION OUTLIERS OUTPERFORM OVER TIME

A TAILWIND FOR STOCK SELECTION

Idea Generation Screen - Composite Value Quintile Performance

4.0

3.0

2.0

%

1.0

0.0

-1.0

-2.0

1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Q1 Q2 Q3 Q4 Q5 Market Average

Source: Eastspring Investments. As at 31 December 2020. Average cumulative performance of the respective GEM Universe Screen

quintile. Q5 is the cheapest quintile and Q1 is the most expensive quintile. ‘Market Average’ is the average performance of all the 5 quintile

screens evenly weighted. Rebalanced on a monthly basis, from 31 January 1995. The style index described is unmanaged and not

available for direct investment. Please note, there are limitations to the use of such style indices as proxies for the past performance in the

respective asset classes/sector. The historical performance or forecast presented in this slide is not indicative of, and should not be

construed as being indicative of, or otherwise used as a proxy for the future or likely performance of the Strategy.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.29

FUNDAMENTAL ANALYSIS AT ITS SIMPLEST

GUARDING AGAINST BEHAVIORAL BIASES

Deep fundamental analysis by seasoned investors

Single model with absolute and relative valuation tools

a. Consensus drives the short term

b. Estimates of sustainable earnings and returns drives medium term

c. Common terminal assumptions drive the long term

Helps understand what expectations are priced by the market

Look for a significant margin of safety

Our best ideas go to the conviction list

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.30

FUNDAMENTAL ANALYSIS

CENTRAL TO OUR COMPETITIVE EDGE

Differentiated Concept of Valuation Relative to Sustainable Earnings

Profitability Market forecasts often overshoot

Sustainable

earnings

Market forecasts often

undershoot

Time

Requires deep fundamental analysis and experience

Provides clear understanding of drivers of valuation

Large differences between price and valuation provide opportunity

Source: Eastspring Investments. For illustration purposes only.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.31

FUNDAMENTAL ANALYSIS

WHEN ASSESSING MARKET RISKS ESG IS INCORPORATED

Assessing material risks to sustainable earnings:

Incorporate governance, social behavior and environmental impacts

Monitor company development over time

Actively engage companies to promote shareholder value realisation

We will actively promote changes when necessary

Active and informed voting policy

Additional tools used:

MSCI – identification of potential ESG risks

ISS – for Proxy analysis

Source: Eastspring Investments. The above views are subject to change at the fund manager’s discretion without prior notice.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.32 FUNDAMENTAL ANALYSIS GUARDING AGAINST BEHAVIORAL BIASES Lenovo Group Ltd 992 HK Target 7.51 90.6% Forecasts 5 Year AVG Mar-19 Mar-20 Mar-21 Mar-22 Mar-23 CAGR Sales 43,660 47,387 48,697 50,568 53,057 56,240 4.4% Sales growth 6.0% 4.5% 2.8% 3.8% 4.9% 6.0% EBITDA margin 3.1% 3.1% 3.4% 3.5% 3.7% 3.8% 3.5% OP growth -12.0% 66.1% 32.3% 16.3% 16.0% 16.0% OP margin 1.7% 1.6% 2.0% 2.2% 2.5% 2.7% Net Profit 384 517 735 605 727 868 -245.0% PER (current & fwd to fye) 985.0 11.7 8.2 10.0 8.3 6.9 PBR (current & fwd to fye) 13.2 1.6 1.5 1.5 1.4 1.3 Dividend Yield 6.2% 5.0% 8.5% 7.0% 8.4% 10.1% ROE 12.4% 14.2% 19.1% 15.0% 17.1% 19.4% 17.0% Adjusted ROE -1.2% 18.8% 25.1% 19.6% 22.5% 24.8% 22.1% Net Debt (Cash) / Equity -2.4% 35.3% 20.1% 6.4% -8.2% -23.5% EV/EBITDA (current & fwd to fye) 5.8 5.8 4.8 4.2 3.5 2.9 Implied Valuation FW PER FW PBR FW DY FW EV/EBITDA At Current Share Price 10.4 1.6 6.0 5.8 At Valuation Target 19.8 3.0 3.1 9.5 Equilibrium assumptions Equilibrium 5 Year AVG Used Blend Target Share Price 7.51 Inflation 2.4% 2.4% Real growth 5.1% 3.6% Absolute Value 7.51 Discount rate 10.5% 10.5% DCF Model 10.29 ROE 17.2% 12.4% 17.2% Residual Income Model 6.09 Non-cash ROE 21.0% -1.2% 21.0% DDM Model 6.15 Equilibrium outputs Equilib mult Median mult Used Relative Value Market mult FWD #s 6.70 Fwd EY 5.79% 6.91% 12m fwd. EY 9.64% FWD DY 3.91% 2.22% 3.91% 12m fwd DPS 5.96% 0.03 6.00 FWD PER 17.3 14.5 17.3 12m fwd EPS 10.4 0.05 6.56 FWD PBR 3.0 3.5 3.0 12m fwd BPS 1.6 0.32 7.54 Source: Eastspring Investments. The table and information is included for illustrative purposes only. Data shown as of date of research. It should not be considered a recommendation to purchase or sell any security. STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.

33

FUNDAMENTAL ANALYSIS

CALIBRATING CONVICTION AND UPSIDE

High Upside %

Stocks allocated to a “list” –

reflecting combination of Upside

and Conviction Conviction

Active List

Conviction list: best ideas of List

high upside and shared

Low Conviction

High Conviction

team conviction

Active list: lower upside and

/ or shared team conviction

Risk list: Not used for Risk List Active List

Dynamic strategy. Only

used for lower risk

mandates.

Low Upside %

Source: Eastspring Investments. The above views are subject to change at the fund manager’s discretion without prior notice.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.34

PORTFOLIO CONSTRUCTION

GETTING OUR HIGH CONVICTION IDEAS INTO THE PORTFOLIO

Clear and separate discipline, our portfolios are more than a collection of

good ideas

Portfolios are predominantly populated with stocks from our conviction list

Positions are scaled around valuation upside and conviction

Before investing in highly correlated stocks, we seek conviction that we will

get rewarded for accepting the additional risk

We identify and seek to manage unintended risks

This all combines to produce price sensitive and patient portfolios of high

conviction stocks

Source: Eastspring Investments. The above views are subject to change at the fund manager’s discretion without prior notice

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.35

PORTFOLIO CONSTRUCTION ILLUSTRATION

ACTIVE POSITION SIZE DRIVEN BY RISK AND EXPECTED RETURN

GEM Dynamic Risk Return

150%

130%

Add to uncorrelated high

upside stocks

110% No risk

positions

90%

Upside* %

70%

Review / Rotate to higher

upside stocks

50%

30%

10% Sell low upside stocks

0.00% 0.20% 0.40% 0.60% 0.80% 1.00% 1.20% 1.40%

-10%

Stock Contribution To Active Risk %

Source: Eastspring Investments. As at 30 October 2020. *Upside adjusted to maximum 150%. The plotted points represent holdings in

the strategy. The above views are subject to change at the fund manager’s discretion without prior notice. Past performance is not

necessarily indicative of the future or likely performance of strategies adopting the same strategy mentioned above.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.36

RISK CONTROL AND REVIEW

TESTING CONSISTENCY OF PORTFOLIO WITH MANDATE AND RISK

Monitoring of positions relative to valuation and risk contribution aids review and sell discipline

Weekly portfolio review meeting: All portfolios subject to team scrutiny

Test consistency of views and portfolio positions

Quantitative Portfolio Strategy (QPS) Team - ongoing test of process consistency and allocation

of capital in accordance with mandate

Head of Eastspring Portfolio Strategies (EPS) utilises risk framework in supervision and

oversight

Risk oversight – scrutiny of risk characteristics and risk budget supported by independent

Investment Risk Management Team

Head of EPS

Head of EPS Head of EPS

Quarterly Quarterly

/ Group

Monthly one Strategy Performance Strategy Risk CRO

on one

Performance Reviews Performance Oversight

Strategy risk

Review Review

Oversight

Source: Eastspring Investments. The above views are subject to change at the manager’s discretion without prior notice,

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.37

TEAM’S SUSTAINABLE EDGE

POSITIONED FOR SUSTAINABLE LONG-TERM PERFORMANCE

Competitive edge based our understanding of behavioural sources of mispricing

Price-focused process with a valuation anchor

Experienced; small; dynamic; focused on “best ideas”

Rigorous research supported by peer review

Research output plus risk understanding provides clear link to portfolio construction

Ongoing review supports process integrity and sell discipline

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.ENVIRONMENTAL, SOCIAL & GOVERNANCE

39

ASSESSING ALL MATERIAL RISKS TO

SUSTAINABLE EARNINGS

Ongoing level of engagement with companies around material risks include but

not limited to:

Board structure: discussions around board structure and its appropriateness to their strategy.

We always vote and will vote against the board and engage with the company if appropriate.

Minority shareholder return focus: discussions with management to monitor whether change in

this area is in line with expectations.

Structure of management KPIs: are they aligned with targeting capital efficiency / ROE or other.

We will engage and monitor for change.

Complex ownership: we will engage with companies and monitor for improvements.

Managing environmental risks: discuss the processes in place at companies with significant

environmental risks to building clarity around the risks to earnings.

Collaborating with other investors: we will work with other minority shareholder to communicate

with boards on specific issues when appropriate.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.40

GLOBAL EMERGING MARKETS DYNAMIC STRATEGY

ESG SUMMARY PROFILE (AS OF 31 JANUARY 2021)

Company Fund Company Fund

Company name GICS Industry Company name GICS Industry

Rating Weight Rating Weight

Lenovo Group Ltd. Technology Hardware, Storage & Peripherals AA 3.9% Cosco Shipping Energy Oil, Gas & Consumable Fuels CCC 1.0%

Fubon Financial Holding Insurance AA 1.3% Petrochina Co Ltd Oil, Gas & Consumable Fuels CCC 1.3%

Absa Group Ltd Banks AA 1.0% Sinopec Engineering Group Construction & Engineering B 1.9%

Banco Bradesco Pref Banks AA 2.6% Cosco Shipping Ports Transportation Infrastructure B 1.3%

Life Healthcare Group Health Care Providers & Services A 1.4% Kunlun Energy Co. Gas Utilities B 2.0%

Naspers Ltd N Internet & Direct Marketing Retail A 3.8% E-mart Co. Ltd Food & Staples Retailing B 1.9%

Estacio Participacoes S.a. Diversified Consumer Services A 2.2% Hyundai Mobis Auto Components B 3.5%

Samsung Electronics Co Technology Hardware, Storage & Peripherals A 8.5% China Petroleum & Oil, Gas & Consumable Fuels B 1.2%

Independent Power & Renewable Electricity

China Longyuan Power A 1.5% Tingyi (cayman Islands) Food Products B 1.2%

Producers

Electronic Equipment, Instruments &

Lg Display Co A 1.8% Grupo Televisa Sab Media B 1.5%

Components

Source: Eastspring Investments, MSCI ratings , 31 January 2021. BM: Benchmark. Benchmark/Index: MSCI Emerging Markets Index. The graphs

and information are included for illustrative purposes only.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.GEM DYNAMIC STRATEGY

42

GLOBAL EMERGING MARKETS DYNAMIC STRATEGY

PERFORMANCE AS AT 31 DECEMBER 2020

Performance – Class A Relative To MSCI EM Index

%

40.0

29.7

30.0

19.7 18.3 18.3

20.0 12.8

10.0 10.0 9.7

10.0 7.4 6.3 6.3 6.2 6.0

2.6 1.1 2.2

0.0

-10.0 -5.1 -3.1 -3.8

-20.0 -12.0 -12.0

1M 3M YTD 1 Yr 3 Yrs (p.a.) 5 Yrs (p.a.) Since Inception

(p.a.)

Net (%) Benchmark Return (%) Relative (%)

Performance – Class A Relative To MSCI EM Value Index

%

35.0

29.7

30.0

25.0

19.0

20.0

15.0 12.8

10.0 10.7 9.2 9.7

10.0 6.3 6.3 6.8

4.0 2.9

5.0 2.3 1.1 0.4 0.7 2.2 1.2 1.0

0.0

-5.0 -2.8

-2.8

1M 3M YTD 1 Yr 3 Yrs (p.a.) 5 Yrs (p.a.) Since Inception

(p.a.)

Net (%) MSCI Emerging Markets Value (%) Relative (%)

Source: Eastspring Investments, 31 December 2020, NAV-Net Class A. Returns are based in share class currency and computed using the NAV price on

bid-bid basis with net income reinvested . The NAV price is net of all fees, expenses and withholding taxes. Calendar year returns are based on the share

class performance for the year and if the share class is incepted during a particular year, the returns shown relate to the performance of the share class since

its inception till end of that calendar year. Fees and expenses vary among share classes, further information is available in the Prospectus. Benchmark: MSCI

Emerging Markets Index. This is for information purposes only. It is not intended as an offer or solicitation for the purchase or sale of any financial

instrument, investment product, security or service. Inception date: 15 May 2014. Past performance is not necessarily indicative of the future or likely

performance.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.43

GLOBAL EMERGING MARKETS DYNAMIC STRATEGY

CALENDAR YEAR PERFORMANCE AS AT 31 DECEMBER 2020

% Performance – Class A Relative To MSCI EM Index

50.0

37.3

40.0 30.4

30.0

18.3 18.4 18.1

20.0 12.7 11.2

6.3 6.9

10.0 0.7

0.0

-10.0 -5.8 -2.8

-6.9

-20.0 -12.0 -13.9 -14.6

-17.7 -14.9

-30.0

2020 2019 2018 2017 2016 2015

Net (%) Benchmark Return (%) Relative (%)

% Performance – Class A Relative To MSCI EM Value Index

40.0

30.4 28.2

30.0

18.1

20.0 12.7 11.9 14.9

6.3 9.2

10.0 0.7 2.2 3.2 0.9

0.0

-10.0 -2.8 -3.1

-20.0 -10.7

-13.9

-17.7 -18.6

-30.0

2020 2019 2018 2017 2016 2015

Net (%) MSCI Emerging Markets Value (%) Relative (%)

Source: Eastspring Investments, 31 December 2020, NAV-Net Class A. Returns are based in share class currency and computed using the NAV price on

bid-bid basis with net income reinvested . The NAV price is net of all fees, expenses and withholding taxes. Calendar year returns are based on the share

class performance for the year and if the share class is incepted during a particular year, the returns shown relate to the performance of the share class since

its inception till end of that calendar year. Fees and expenses vary among share classes, further information is available in the Prospectus. Benchmark: MSCI

Emerging Markets Index. This is for information purposes only. It is not intended as an offer or solicitation for the purchase or sale of any financial

instrument, investment product, security or service. Inception date: 15 May 2014. Past performance is not necessarily indicative of the future or likely

performance.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.44

GLOBAL EMERGING MARKETS DYNAMIC STRATEGY

Performance Relative To MSCI Emerging Markets Net Div (%)

10.0 6.9

3.7 3.9

5.0 0.7

%

0.0

-5.0 -2.8 -3.7

-10.0 -6.9 -5.8 -6.5

-9.1

-15.0 -12.0

-20.0

-25.0 -21.1

2015 2016 2017 2018 2019 2020

Fund relative to MSCI EM Net Div Value Index relative to MSCI EM Net Div

0.0

-2.0

-4.0

-3.1 -3.8

-6.0 -4.8

-5.1 -5.8

-8.0 -6.0

%

-10.0 -8.9

-12.0

-14.0 -12.0

-16.0 -14.3

-15.2

1 year 2 years (p.a.) 3 years (p.a.) 5 years (p.a.) Since Inception (p.a.)

Fund relative to MSCI EM Net Div Value Index relative to MSCI EM Net Div

Source: Eastspring Investments, 31 December 2020, NAV-Net Class A. Returns are based in share class currency and computed using the NAV price on

bid-bid basis with net income reinvested . The NAV price is net of all fees, expenses and withholding taxes. Calendar year returns are based on the share

class performance for the year and if the share class is incepted during a particular year, the returns shown relate to the performance of the share class

since its inception till end of that calendar year. Fees and expenses vary among share classes, further information is available in the Prospectus.

Benchmark: MSCI Emerging Markets Index. This is for information purposes only. It is not intended as an offer or solicitation for the purchase or sale of

any financial instrument, investment product, security or service. Inception date: 15 May 2014. Past performance is not necessarily indicative of future

performance.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.45 GLOBAL EMERGING MARKETS DYNAMIC STRATEGY PORTOFLIO CHARACTERISTICS (AS OF 31 DECEMBER 2020) Source: Eastspring Investments. As at 31 December 2020. Benchmark/Index: MSCI Emerging Markets Index. The information provided herein are subject to change at the discretion of the Investment Manager without prior notice. STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.

46 RISK CONTROL & REVIEW Source: Eastspring Investments, 31 December 2020. Charts above reflect the change in underlying risk model effective from 1 July 2020. We made this change from Axioma model version 2 to version 4 to benefit from their updated risk mode The graphs and information are included for illustrative purposes only. STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.

47

EASTSPRING INVESTMENTS – GLOBAL EMERGING

MARKETS DYNAMIC STRATEGY

COUNTRY ATTRIBUTION – 3 YEARS TO 31 DECEMBER 2020

Asset

Country Strategy Weight Ending (%) Index Weight Ending (%) Security Selection(%) Total Effect (%)

Allocation(%)

Total 100.0 100.0 0.0 -9.8 -9.8

Asia 71.9 80.0 -0.2 -14.7 -14.9

India 5.6 9.2 0.1 2.6 2.8

Philippines 3.9 0.7 -0.6 0.7 0.1

Pakistan 0.0 0.0 0.0 0.0 0.0

Hong Kong 0.0 0.0 0.0 0.0 0.0

Thailand 1.2 1.8 0.4 -0.8 -0.4

Malaysia 1.0 1.5 0.3 -0.8 -0.6

Indonesia 1.6 1.3 -0.1 -0.7 -0.8

Taiwan 6.0 12.8 -0.5 -2.0 -2.5

South Korea 18.8 13.5 0.5 -6.3 -5.8

China 33.8 39.1 -0.3 -7.5 -7.8

EMEA 13.2 12.1 0.6 1.7 2.4

South Africa 6.4 3.5 -0.9 3.1 2.2

Saudi Arabia 0.0 2.4 1.0 0.0 1.0

Poland 0.0 0.7 0.5 0.1 0.6

Greece 0.0 0.1 0.1 0.2 0.3

Hungary 0.0 0.2 0.0 0.0 0.1

Czech Republic 0.0 0.1 0.0 0.0 0.0

Kuwait 0.0 0.5 0.0 0.0 0.0

Qatar 0.0 0.7 0.0 0.0 0.0

Russia 3.0 3.0 0.8 -0.9 -0.1

United Arab Emirates 1.5 0.5 -0.2 0.1 -0.1

Egypt 1.1 0.1 -0.3 -0.1 -0.4

Turkey 1.2 0.4 -0.3 -0.9 -1.2

LATAM 12.8 7.9 0.3 3.4 3.7

Brazil 7.7 5.1 0.5 1.9 2.4

Chile 0.0 0.5 0.5 0.2 0.7

Mexico 5.1 1.7 -0.9 1.2 0.3

Argentina 0.0 0.1 0.1 0.0 0.1

Colombia 0.0 0.2 0.0 0.1 0.1

Peru 0.0 0.2 0.1 0.0 0.1

Europe 0.0 0.0 -0.2 0.0 -0.2

Netherlands 0.0 0.0 -0.2 0.0 -0.2

Cash and Equivalents 2.2 0.0 -0.5 -0.3 -0.8

Source: Eastspring Investments. 3 Years to 31 December 2020. Benchmark/Index: MSCI Emerging Markets Index. Past

performance is not necessarily indicative of future performance. The information provided herein is subject to change at the

discretion of the Investment Manager without prior notice.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.48

EASTSPRING INVESTMENTS – GLOBAL EMERGING

MARKETS DYNAMIC STRATEGY

SECTOR ATTRIBUTION – 3 YEARS TO 31 DECEMBER 2020

Strategy Benchmark Active Stock Selection

Sector Sector Effect (%) Total Effect (%)

(%) (%) (%) Effect (%)

Total 100.0 100.0 0.0 -5.6 -4.2 -9.8

Financials 24.3 18.0 6.4 -0.6 2.0 1.4

Materials 5.5 7.6 -2.1 0.3 0.8 1.1

Consumer Staples 3.1 5.9 -2.8 0.1 0.4 0.5

Utilities 5.8 2.0 3.8 -1.6 1.9 0.3

Information Technology 19.0 20.5 -1.4 0.4 -0.3 0.2

Communication Services 11.2 11.6 -0.5 -1.0 1.1 0.1

Health Care 0.7 4.7 -4.0 0.4 -0.4 0.1

Real Estate 1.9 2.1 -0.2 0.0 -0.9 -0.8

Cash and Equivalents 2.2 0.0 2.2 -0.7 -0.2 -0.9

Industrials 7.4 4.3 3.1 -0.5 -2.6 -3.2

Energy 7.0 5.0 2.0 -0.7 -2.5 -3.3

Consumer Discretionary 11.8 18.3 -6.5 -1.7 -3.6 -5.3

Source: Eastspring Investments, 3 Years to 31 December 2020. Past performance is not necessarily indicative of the future or likely performance of

mandates adopting the same strategy mentioned above. Please note that the securities mentioned are for illustrative purposes only. It should not be

considered as a recommendation to purchase or sell such securities. There is no assurance that any security discussed herein will remain in the

portfolio at the time you receive this document or that security sold has not been repurchased. The securities discussed do not represent the entire

portfolio and in the aggregate may represent only a small percentage of the portfolio holdings.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.49

EASTSPRING INVESTMENTS – GLOBAL EMERGING

MARKETS DYNAMIC STRATEGY

CONTRIBUTORS AND DETRACTORS – 3 YEARS TO 31 DECEMBER 2020

Benchmark Benchmark

Strategy End Contribution Strategy End Contribution

Contributors End Weight Detractors End Weight

Weight (%) (%) Weight (%) (%)

(%) (%)

China Resources Cement

0.0 0.0 1.7 Petrochina Co Ltd-H 1.4 0.1 -2.0

Holdings

ICICI Bank Ltd 3.5 0.5 1.5 Embraer 0.0 0.0 -1.8

CCR SA 0.0 0.0 1.5 Petrobras Petroleo Brasil^ 2.3 0.6 -1.5

Samsung Electronics Co Bank Negara Indonesia

8.9 5.2 1.5 1.6 0.0 -1.5

Ltd^ (Persero)

Banco Do Brasil 0.0 0.1 1.3 Emart Co Ltd 1.8 0.0 -1.4

China Overseas Land &

Cosan -A 0.0 0.0 1.2 1.9 0.1 -1.3

Investment

Sinopec Engineering

Infosys Ltd^ 0.0 0.7 1.2 1.9 0.0 -1.3

Group-H

JBS 0.0 0.1 1.0 LG Display 1.5 0.1 -1.2

China Longyuan Power

2.5 0.0 0.8 Bangkok Bank^ 1.2 0.0 -1.2

Group-H

Lenovo Group 4.1 0.1 0.8 Hana Financial Group 0.0 0.1 -1.2

Source: Eastspring Investments. 3 Years to 31 December 2020. Benchmark/Index: MSCI Emerging Markets Index. Past performance is not necessarily indicative of

future performance. Please note that the securities mentioned are for illustrative purposes only. It should not be considered as a recommendation to purchase or sell

such securities. There is no assurance that any security discussed herein will remain in the portfolio at the time you receive this document or that security sold has not

been repurchased. The securities discussed do not represent the entire portfolio and in the aggregate may represent only a small percentage of the portfolio holdings.

The information provided herein is subject to change at the discretion of the Investment Manager without prior notice. ^Includes all share classes.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.50 EASTSPRING INVESTMENTS – GLOBAL EMERGING MARKETS DYNAMIC STRATEGY COUNTRY POSITIONING - AS AT 31 DECEMBER 2020 Country Strategy Weight (%) Benchmark Weight (%) Relative (%) South Korea 18.8 13.5 5.3 Mexico 5.1 1.7 3.4 Philippines 3.9 0.7 3.2 South Africa 6.4 3.5 3.0 Brazil 7.7 5.1 2.6 Cash and Equivalents 2.2 0.0 2.2 Egypt 1.1 0.1 1.0 United Arab Emirates 1.5 0.5 1.0 Turkey 1.2 0.4 0.8 Indonesia 1.6 1.3 0.2 Russia 3.0 3.0 0.0 Pakistan 0.0 0.0 0.0 Czech Republic 0.0 0.1 -0.1 Greece 0.0 0.1 -0.1 Argentina 0.0 0.1 -0.1 Colombia 0.0 0.2 -0.2 Hungary 0.0 0.2 -0.2 Peru 0.0 0.2 -0.2 Kuwait 0.0 0.5 -0.5 Chile 0.0 0.5 -0.5 Malaysia 1.0 1.5 -0.5 Thailand 1.2 1.8 -0.6 Poland 0.0 0.7 -0.7 Qatar 0.0 0.7 -0.7 Saudi Arabia 0.0 2.4 -2.4 India 5.6 9.2 -3.6 China 33.8 39.1 -5.3 Taiwan 6.0 12.8 -6.8 Source: Eastspring Investments. 31 December 2020. Benchmark/Index: MSCI Emerging Markets Index. The information provided herein is subject to change at the discretion of the Investment Manager without prior notice. STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.

51

EASTSPRING INVESTMENTS – GLOBAL EMERGING

MARKETS DYNAMIC STRATEGY

SECTOR POSITIONING AS AT 31 DECEMBER 2020

Strategy Active

Sector Benchmark (%)

(%) (%)

Financials 24.3 18.0 6.4

Utilities 5.8 2.0 3.8

Industrials 7.4 4.3 3.1

Cash and Equivalents 2.2 0.0 2.2

Energy 7.0 5.0 2.0

Real Estate 1.9 2.1 -0.2

Communication Services 11.2 11.6 -0.5

Information Technology 19.0 20.5 -1.4

Materials 5.5 7.6 -2.1

Consumer Staples 3.1 5.9 -2.8

Health Care 0.7 4.7 -4.0

Consumer Discretionary 11.8 18.3 -6.5

Source: Eastspring Investments. 31 December 2020. Benchmark/Index: MSCI Emerging Markets Index. The information provided herein is subject

to change at the discretion of the Investment Manager without prior notice.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.52

EASTSPRING INVESTMENTS – GLOBAL EMERGING

MARKETS DYNAMIC STRATEGY

OVERWEIGHTS AND UNDERWEIGHTS AS AT 31 DECEMBER 2020

Benchmark Benchmark

Strategy End Relative Strategy End Relative

Overweights End Weight Underweights End Weight

Weight (%) (%) Weight (%) (%)

(%) (%)

Taiwan Semiconductor

Baidu Inc 5.5 0.7 4.7 0.0 5.9 -5.9

Manufacturing

Lenovo Group Ltd 4.1 0.1 4.0 Alibaba Group Holding Ltd 0.0 5.6 -5.6

Samsung Electronics Co

8.9 5.2 3.7 Tencent Holdings Ltd 0.0 5.3 -5.3

Ltd^

ICICI Bank Ltd 3.5 0.5 3.0 Meituan-Class B 0.0 1.7 -1.7

Hon Hai Precision Industry 3.4 0.5 2.9 Reliance Industries Ltd 0.0 1.0 -1.0

Banco Bradesco^ 3.2 0.4 2.9 JD.com Inc 0.0 1.0 -1.0

Hyundai Mobis Co Ltd 3.0 0.2 2.8 Ping An Insurance- H 0.0 0.9 -0.9

Naspers Ltd-N 3.6 1.1 2.5 Pinduoduo Inc - ADR 0.0 0.9 -0.9

China Longyuan Power

2.5 0.0 2.4 NIO Inc - ADR 0.0 0.8 -0.8

Group-H

China Pacific Insurance

2.4 0.1 2.2 Vale SA 0.0 0.8 -0.8

Group

Source: Eastspring Investments, 31 December 2020. Benchmark: MSCI Emerging Markets Index. Please note that the securities mentioned are included for

illustration purposes only. It should not be considered a recommendation to purchase or sell such securities. There is no assurance that any security discussed

herein will remain in the portfolio at the time you receive this document or that securities sold have not been repurchased. The securities discussed do not

represent the entire portfolio and in the aggregate may represent only a small percentage of the portfolio holdings. The information provided herein are subject

to change at the discretion of the Investment Manager without prior notice. ^Includes all share classes.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.APPENDIX

54

EASTSPRING INVESTMENTS – GLOBAL EMERGING

MARKETS DYNAMIC FUND

SHARE CLASSES AVAILABLE FOR INVESTMENT

*Minimum *Minimum

Class Currency Bloomberg ISIN Inception initial subsequent

ticker date investment investment

Class A USD IOEMDAU LX LU0640798160 15-May-14 USD500 USD50

Class R USD EGEMDRU LX LU2199555702 15-July-20 USD500 USD50

Initial sales Annual Annual admin Initial sales Annual Annual Ongoing

Class charges% management fee% (max) charges% management admin fee% charges %

(max) fee% (max) (current) fee% (current) (current)

Class A 5.000 2.000 0.500 5.000 1.500 0.300 1.920

Class R None 1.000 0.500 None 0.750 0.300 1.180

Annual Ongoing charges vary from year to year and do not include portfolio transaction cost.

Distribution Dividend per Ongoing charges are based on annualized expenses for the year ending December

Class Ex-date dividend 2019 for Share Class A; Ongoing charges are based on estimated expenses of another

frequency share yield % share class for Share Class R.

R-class shares are not sold directly to investors, but to financial intermediaries that

serve investors. The intermediary executes the purchase of the funds on behalf of the

Class A N.A N.A N.A N.A investor, as well as the sale and exchange. The Sales Charge may be modified for

certain financial intermediaries who submit trades on behalf of eligible investors. As

allowed in the Prospectus, Eastspring and the financial intermediaries have agreed to

Class R N.A N.A N.A N.A

waive the Sales Charge for all purchases for the fee-based R share class. Always

consult your financial adviser. For more about charges, see the Prospectus.

Distributions are not guaranteed and may fluctuate. Past distributions are not necessarily indicative of future trends, which may be lower. Distribution payouts and its

frequency are determined by the Board of Directors, and can be made out of (a) income; or (b) net capital gains; or (c) capital of the Fund or a combination of any of (a)

and/or (b) and/or (c). The payment of distributions should not be confused with the Fund’s performance, rate of return or yield. Any payment of distributions by the Fund

may result in an immediate decrease in the net asset value per share. Funds with Monthly and Quarterly Distribution Frequency: Annualised Dividend yield = (Dividend

per share / Reference NAV at start of distribution period) x (No. of calendar days in a year / No. of calendar days in distribution period) x 100%. Funds with Yearly

Distribution Frequency: Annualised Dividend Yield = (Dividend amount / Total Net Assets) x (No. of calendar days in a year / No. of calendar days in distribution period)

x 100%. *Or their near equivalent in any major freely convertible currency of the amounts specified. "N.A.": This share class does not distribute dividends.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.55

EASTSPRING INVESTMENTS – GLOBAL EMERGING

MARKETS DYNAMIC

COMPOSITE DECEMBER 2020 (USD)

Annualised figures

Calendar Year Data 2020 2019 2018 2017 2016 2015 2014 2013 2012 2011

2 3 4 5 6 7 8 9 10

Rolling Results 1M 1Y S.I

Yrs Yrs Yrs Yrs Yrs Yrs Yrs Yrs Yrs

Composite Return - Net (%) 8.0 14.2 -12.3 31.1 19.1 -17.0 -9.6 -0.6 24.1 -21.3

Composite Return - Net (%) 10.4 8.0 11.1 2.7 9.1 11.1 5.8 3.5 2.9 5.1 2.1 2.9

Composite Return - Gross (%) 8.8 15.2 -11.5 32.2 20.2 -16.3 -8.8 0.2 25.2 -20.6

Composite Return - Gross (%) 10.5 8.8 12.0 3.5 10.1 12.0 6.7 4.3 3.8 6.0 3.0 3.8

Benchmark Return (%) 18.7 18.9 -14.3 37.3 11.2 -14.9 -2.2 -2.6 18.2 -18.4

Benchmark Return (%) 7.4 18.7 18.8 6.5 13.5 13.0 7.8 6.3 5.2 6.5 3.7 4.4

Relative to Gross (%) -9.9 -3.7 2.8 -5.0 9.0 -1.3 -6.6 2.8 6.9 -2.2

Relative to Gross (%) 3.1 -9.9 -6.8 -3.0 -3.4 -1.0 -1.1 -2.0 -1.3 -0.5 -0.8 -0.7

Composite 3-Year Annualised

Composite Annualised Volatility (%) N/A 30.6 24.9 21.8 19.4 19.3 19.7 19.1 18.4 18.8 19.7 19.8 21.8 14.6 14.9 17.6 18.8 16.4 17.0 21.2 N/A N/A

Volatility (%)

Highest Return in Composite (%) 10.5 9.0 12.1 3.6 10.1 12.0 6.7 4.4 3.8 6.0 3.0 3.8 Benchmark 3-Year Annualised

19.9 14.4 14.8 15.6 16.3 14.3 15.2 19.3 N/A N/A

Lowest Return in Composite (%) 10.5 8.7 11.9 3.6 10.1 12.0 6.7 4.4 3.8 6.0 3.0 3.8 Volatility (%)

Tracking Error (%) N/A 9.5 7.2 6.4 5.9 5.6 5.5 5.3 5.1 4.9 4.8 4.8 Number of Portfolios 3 2 1 1 1 1 1 1 1 1

Information Ratio N/A -1.0 -0.9 -0.5 -0.6 -0.2 -0.2 -0.4 -0.3 -0.1 -0.2 -0.1 Market Value at End, USD (bn) 1.54 0.95 0.47 0.52 1.73 0.46 0.48 0.12 0.02 0.02

Eastspring Investments claims compliance with Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. To receive a complete list and description the composites and/or a presentation that adheres to

the GIPS standards, contact the relevant sales representatives or email institutional@eastspring.com.

The Firm is defined as all portfolios, except those that are predominantly Private Equity portfolios, of Eastspring Investments (Singapore) Limited and Eastspring Investments (Hong-Kong) Limited (collectively referred to as "Eastspring Investments"), which are business units within the

Prudential Plc Group.

This composite includes a single portfolio that invest primarily in GEM Dynamic equities and managed to MSCI Emerging Mkts Index.

This Composite was created on 1 Dec 10 and Composite Performance starts from 1 Dec 10. A full List of the Firm's Composites is available upon request.

From 1 May 2018, benchmark was changed to MSCI Emerging Mkts Gross Div Index from Net Div Index.

Eastspring Investments has been independently verified for the periods 1 Jan 98 - 31 Dec 09. The verification report(s) is/are available upon request. Verification assesses whether (1) the firm has complied with all the composite construction requirements of the GIPS standards on a

firm-wide basis and (2) the firms policies and procedures are designed to calculate and present performance in compliance with the GIPS standards. Verification does not ensure the accuracy of any specific composite presentation.

The minimum fund size requirement for a fund to be included in a composite is USD3 million.

All returns are presented in Dollar. Market Values are presented in Dollar.

Policies for valuing portfolios, calculating performance and preparing compliant presentations are available upon request.

Performance results are presented gross of investment management fees and net of trading expenses. Treatment of other fees and withholding tax on dividends, interest income and capital gains varies for the underlying portfolios. Additional information on other fees treatment are

available upon request.

Portfolios within the composite has no or minimal derivatives exposure

If a fund has a cash flow or in-specie transfer (either in or out) that is greater than 10% of the opening balance of the fund, then the impact on portfolio performance has to be assessed to determine whether it should be held out-of-structure. If the impact on performance is equal to or

greater than 20 basis points, then the fund can be excluded from composite performance until it is back in structure. Additional information regarding the treatment of significant cash flows is available upon request.

The highest % of management fee charged are as per below:

Equity Strategies : 2.00% per annum

Fixed Income Strategies : 1.25% per annum

Additional information regarding policies for calculating and reporting returns is available on request

The Firm total assets under management as of 31 December 2019 was USD125 billion.

Net composite returns shown do not represent actual net returns of underlying portfolios but are calculated net of the highest band fee (net down by 0.75% p.a.) in the tiered management fee schedule applicable to an institutional investor investing in such a strategy. However, the firm

reserves the right to change this fee structure and hence net composite returns might change without prior or subsequent notifications to current or potential investors

Effective 1st November 2018, Information Ratio is calculated as (Annualized Fund Return - Annualized Bench Return) / Tracking Error.

Prior to 1st November 2018, Information Ratio was calculated as (Average Annualized Excess Return / Tracking Error).

Source: Eastspring Investments, 31 December 2020 (C0208). Benchmark: MSCI Emerging Markets Index. This is for information

purposes only. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, investment product,

security or service.

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.56

Andrew leads Eastspring Investments’ Funds Management Pty Limited and, before

Global Emerging Markets and Regional Asia this, he was a Managing Director, heading

Value equity team, responsible for the firm’s up the Global Equity Team of JP Morgan

GEM and Asia equity value offering Investment Management, London, for ten

(including China-India funds). He was years. He also worked at JP Morgan

appointed to this position in June 2020. Investment Management, Melbourne,

Andrew is also the Lead Portfolio Manager latterly as their Director, responsible for the

for the GEM Dynamic strategy. Australian Equity and Balanced business.

Andrew began his investment career with

With more than 39 years’ investment

National Mutual Life Association.

experience, Andrew has been with

Andrew Cormie, CFA Eastspring since he joined as a Portfolio Andrew is a CFA charterholder and holds a

Portfolio Manager Manager in 2008. Bachelor’s degree in Business

Administration from the Griffith University,

Prior to joining Eastspring, Andrew was the

Brisbane and a diploma from the Securities

Founding Partner and Director of Voyager

Institute of Australia.

Source: Eastspring Investments, 31 January 2021

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.57

Sang Hoon Lee joined Eastspring Fidelity Investment Management (Hong

Investments as Portfolio Manager Kong) Ltd. He was also an Equity Analyst

in January 2005. at Dresdner Kleinwort Benson and Seoul

Securities, Korea. Sang Hoon has over

Sang Hoon is part of the Equity team and 25 years of financial industry experience.

is a member of the Global Emerging

Markets (GEM) focus team. He is also Sang Hoon is a CFA charterholder and

Lead Manager of the GEM Core strategy. holds a Bachelor’s degree in Business

Administration from Seoul National

Prior to joining Eastspring Investments, University and a Master degree of Business

Sang Hoon Lee, CFA, MBA Sang Hoon was an Investment Analyst at Administration from The Wharton School,

University of Pennsylvania.

Portfolio Manager

Luiz Pinho joined Eastspring Investments Brazil. This followed several years at UBS

as Portfolio Manager in December 2014. Investment Bank as a Research Analyst

covering the Brazilian oil & gas and utilities

He is part of the Equity team and is a sectors. Before that, Luiz was an Equity

member of the Global Emerging Markets Analyst at Schroders and had done private

(GEM) focus team. He is also the Lead equity research for GP Investments. Luiz

Portfolio Manager for the Brazil Equity has more than 18 years of financial industry

strategy. experience.

Luiz holds a Bachelor of Business

Prior to joining Eastspring Investments, Luiz

Luiz Pinho Administration from Universidade de Sao

was a Brazilian Equities Specialist providing

Paulo (FEA USP) and a Masters Degree

Portfolio Manager portfolio management support to the GEM

in Finance and Accounting from Umeå

CIO division at UBS Wealth Management in

University, Sweden.

Source: Eastspring Investments, 31 January 2021

STRICTLY PRIVATE AND CONFIDENTIAL. FOR PROFESSIONAL INVESTORS ONLY.You can also read