Global Industrial Real Estate: Current Trends and Potential Disruptors - Brookfield Asset Management

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

PUBLIC SECURITIES GROUP i | 2018 | RE AL ES TATE

Global Industrial Real Estate: Current

Trends and Potential Disruptors

There are currently several opposing forces at work

within the industrial real estate sector. Demand drivers

like e-commerce and supply chain modernization remain

very strong. At the same time, however, new completions

and elevated company valuations require consideration.

There are also a number of potential disruptors that

could change how industrial developers and landlords

operate.

1Global Industrial Real Estate: Current

Trends and Potential Disruptors

Strong Backdrop

Industrial real estate has been among the strongest performing property types in recent years. Positive demand from

e-commerce growth has resulted in low vacancy rates and low cap rates, translating into strong returns for investors. In

both public and private markets, U.S. industrial real estate posted the highest sector-level returns over the past one-,

three- and five-year periods through December 31, 2017.

A NNUA LIZED R E TUR NS OF PRIVATE A ND PUBLIC INDUS TRIA L R E A L ES TATE

PERIOD ENDED DECEMBER 31, 2017 NCREIF PROPERTY INDEX (NPI) FTSE EPRA/NAREIT NORTH AMERICAN

INDUSTRIAL INDUSTRIAL INDEX

One-year 13.1% 23.3%

Three-year 18.1%

13.4%

Five-year 13.2% 16.4%

Source: Bloomberg, National Council of Real Estate Investment Fiduciaries. See index definitions in the disclosures section at the end of this document.

Positive performance has resulted in what we believe are elevated valuations for the public sector relative to the

broader real estate universe. The spread between the average funds-from-operations (FFO) multiple for industrial

stocks compared to that of the broader universe is wider than it has been in the past seven years.

Healthy growth in e-commerce sales has been a key driver for demand growth for industrial real estate. Total U.S.

e-commerce sales increased 16% in 2017, to $453.5 billion. We believe that double-digit growth rates will continue

globally for e-commerce. This strong demand backdrop over the last few years has been met with limited new

development deliveries, resulting in record low vacancies and strong rent growth for industrial landlords in North

America.

INDUS TRIA L PROPERT Y VA LUES A ND C A P R ATES HIS TORIC A L VA LUATION: BROA D R E A L ES TATE

VS. INDUSTRIAL SECTOR

160 10% 25x

150 9.4% 9.4%

140 9% 20x

130

131

120

8% 15x

110

100

100

7% 10x Current Spread: 5.6x

90

6.1% Average Spread: 1.9x

80

5x

70 62 5.3% 6%

60

50 5% 0x

Q1 2005

Q3 2005

Q1 2006

Q3 2006

Q1 2007

Q3 2007

Q1 2008

Q3 2008

Q1 2009

Q3 2009

Q1 2010

Q3 2010

Q1 2011

Q3 2011

Q1 2012

Q3 2012

Q1 2013

Q3 2013

Q1 2014

Q3 2014

Q1 2015

Q3 2015

Q1 2016

Q3 2016

Q1 2017

Q3 2017

Q1 2018

Mar-00

Mar-01

Mar-02

Mar-03

Mar-04

Mar-05

Mar-06

Mar-07

Mar-08

Mar-09

Mar-10

Mar-11

Mar-12

Mar-13

Mar-14

Mar-15

Mar-16

Mar-17

Commercial Property Price Index (Indexed to 100 in July '07) North American REIT Weighted Average FFO Multiple

Industrial Nominal Cap Rates (%) Industrial Sector Weighted Average FFO Multiple

Source: Green Street Advisors, November 2017. See index definitions in the Source: SNL, January 2018. See index definitions in the disclosures section

disclosures section at the end of this document. at the end of this document.

GLOBAL INDUSTRIAL REAL ESTATE: CURRENT TRENDS AND POTENTIAL DISRUPTORS 2Potential Challenges Ahead

Going forward, however, we think demand is likely to normalize and vacancy rates will move higher as completions

increase. Additionally, certain U.S. coastal infill markets have seen rent pressure as existing supply is repurposed for

other uses. This has led to strong industrial rental rate increases in recent years, but going forward, we expect that

growth to slow. Over time, we think the industry will see decreases on mark-to-market rent renewals on U.S. portfolios

and investment returns are likely to moderate.

INDUS TRIA L R E A L ES TATE M A R K E T

150 15.0%

Forecasted 14.0%

100 13.0%

12.0%

Million SF (MSF)

50 11.0%

10.0%

0 9.0%

Q1 1990

Q4 1990

Q3 1991

Q2 1992

Q1 1993

Q4 1993

Q3 1994

Q2 1995

Q1 1996

Q4 1996

Q3 1997

Q2 1998

Q1 1999

Q4 1999

Q3 2000

Q2 2001

Q1 2002

Q4 2002

Q3 2003

Q2 2004

Q1 2005

Q4 2005

Q3 2006

Q2 2007

Q1 2008

Q4 2008

Q3 2009

Q2 2010

Q1 2011

Q4 2011

Q3 2012

Q2 2013

Q1 2014

Q4 2014

Q3 2015

Q2 2016

Q1 2017

Q4 2017

Q3 2018

Q2 2019

Q1 2020

Q4 2020

Q3 2021

8.0%

-50 7.0%

6.0%

-100 5.0%

Quarterly Absorption (MSF) Quarterly Completions (MSF) Vacancy Rate (%)

Source: CBRE Econometric Advisors

Despite the overall trends in e-commerce growth, the acquisition of Whole Foods by Amazon. Other

changes in strategies among industrial tenants could examples include:

moderate demand. As retailer e-commerce platforms

• Target’s acquisition of Shipt, making same-day

mature, capital expenditures related to technology,

delivery an option at about half of its stores in early

fulfillment and distribution have been declining. This

2018

ultimately translates into slowing demand growth.

• Wal-Mart’s plans to double the number of in-store

Additionally, retailers are facing pressures related to

pickup locations

shipping costs (both deliveries and returns), which have

been driven higher primarily by a shortage of labor. • Zara’s use of robots to fulfill in-store pickups, which

These costs make up more than 50% of retailers’ cost account for one-third of the company’s global online

structures and are growing. sales

We see a move toward a “buy online/pick up in store” Although retailers are experiencing double-digit sales

model. More online shoppers are embracing this option, growth in e-commerce channels, rising cost pressures

citing speed as the top reason. Retailers prefer the option associated with these growing digital platforms are

as it reduces expenses related to fulfillment centers and forcing these companies to optimize distribution

shipping costs. channels. Ultimately this could result in slowing demand

and deceleration of rent growth in the industrial real

This is particularly important in the grocery space where

estate market.

competition is heating up in the online channel following

GLOBAL INDUSTRIAL REAL ESTATE: CURRENT TRENDS AND POTENTIAL DISRUPTORS 3INDUSTRIAL PROPERT Y VALUES AND YIELDS

International Spotlight – U.K. and Japan

Outside the U.S. market, we think a number of current

trends are worth watching. Despite uncertainty

related to Brexit trade negotiations in the U.K., the

region’s industrial real estate sector has been resilient.

Property values have meaningfully risen over the last

few years as net initial yields (cap rates) have declined.

The underlying fundamentals in the U.K. continue

to be strong. Online penetration is higher in the U.K.

compared to the U.S., but valuations in public markets

appear to reflect this currently.

U.K. Industrial Property Prices (Indexed to 100 July ’06)

U.K. Net Initial Yield (%)

Source: Green Street Advisors, November 2017

The Japanese industrial market has undergone a significant transition. The supply chain was typically fragmented with

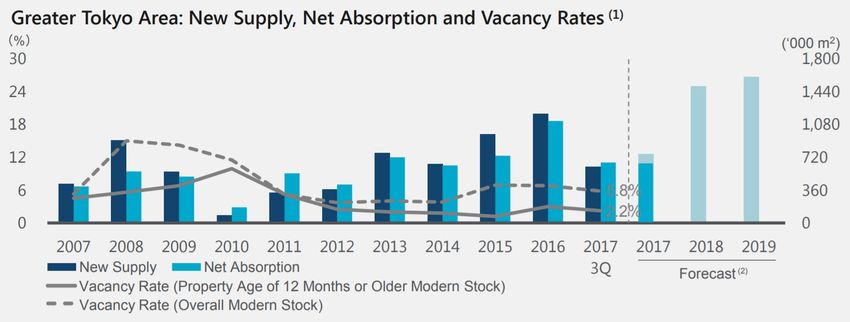

multiple layers, but modernization has resulted in consolidation. The amount of advanced logistics facilities as a percentage

of total industrial supply has more than doubled over the past five years (from 1.9% to 3.9%), according to CBRE. These

modern logistics facilities are taller buildings with multiple stories, increasing the usable square footage without increasing

the footprint.

We believe that new deliveries of advanced logistics facilities will outpace demand in 2018 as deliveries are forecasted to be

7.5% of the current existing supply. In general, we believe the first movers in this wave of new supply have received attractive

return on capital, but we are cautious going forward as new supply begins to outpace demand.

Source: CBRE Research

GLOBAL INDUSTRIAL REAL ESTATE: CURRENT TRENDS AND POTENTIAL DISRUPTORS 4Potential Disruptors

We see several potential disruptors on the horizon that are worth considering as we forecast growth rates for industrial real

estate.

The first is the adoption of autonomous vehicles. The value of industrial real estate could be significantly impacted as

autonomous vehicles and commercial vehicle fleets reduce congestion and travel times. We would expect to see a shift in

relative values of industrial real estate, likely slowing rent growth in infill markets and driving growth higher in nearby low-rent

markets.

Source: Brookfield Investment Management Inc.

Additionally, driverless fleets will help alleviate pressures in the trucking industry, which has struggled to keep pace with

demand amid a shortage of drivers. We believe this may result in additional shadow supply of industrial product in the form

of more trucks on the road transporting goods.

On the positive side for industrial real estate, autonomous vehicles will dramatically reduce the cost structure for shippers,

as half of these expenses are related to wages and benefits. This could make online shopping and delivery a more cost

competitive option to in-store retailing.

The second disruptor is Amazon’s rethinking of the supply chain. The company recently launched a trial program in an

effort to shrink inventories and shorten delivery times (and therefore reduce costs). In the company’s current Fulfillment by

Amazon process, goods are shipped from merchants to Amazon warehouses. Amazon is then compensated for storing,

packing and delivering items once they are ordered by customers.

Under its trial program, Amazon is making its shipping and logistics software available to third-party vendors; and will

manage the pick up and delivery of merchants’ goods from third-party warehouses. This essentially allows Amazon to ship to

consumers directly from third-party facilities, eliminating the need for an Amazon sorting facility and therefore reducing its

logistical footprint.

Investment Implications

While the fundamental, long-term demand drivers for the sector remain positive, we currently have a cautious view on the

industrial sector in the public markets. We see some challenges that are more near term and concrete, while others are

longer term and more abstract. We are considering all these risk factors as we seek to identify companies in the sector with

the best growth prospects at the best valuations.

GLOBAL INDUSTRIAL REAL ESTATE: CURRENT TRENDS AND POTENTIAL DISRUPTORS 5DISCLOSURES

As of March 29, 2018. © Brookfield Investment Management Inc. Brookfield Investment Management Inc. (“Brookfield”) is an SEC-registered investment adviser and

represents the Public Securities platform of Brookfield Asset Management Inc. (“BAM”), providing global listed real assets strategies including real estate equities,

infrastructure equities, multi-strategy real asset solutions and real asset debt. BIM is a wholly owned subsidiary of BAM.

The information in this report is not and is not intended as investment advice or prediction of investment performance. This information is deemed to be from reliable

sources; however, Brookfield does not warrant its completeness or accuracy. Brookfield disclaims any duty or obligation to update any information provided in this

report. This report is not intended to and does not constitute an offer or solicitation to sell or a solicitation of an offer to buy any security, product or service (nor shall

any security, product or service be offered or sold) in any jurisdiction in which Brookfield is not licensed to conduct business, and/or an offer, solicitation, purchase or

sale would be unavailable or unlawful. Past performance is not indicative of future results.

Performance shown in USD unless otherwise noted. Opinions, if any, expressed herein are current opinions of Brookfield Investment Management Inc. and are

subject to change without notice. The mention of specific securities, if any, is not a recommendation or solicitation for any person to buy, sell or hold any particular

security. Any outlooks or forecasts presented herein are as of the date appearing on this report only and are also subject to change without notice.

Information herein contains, includes or is based upon forward-looking statements within the meaning of the federal securities laws, specifically Section 21E of

the Securities Exchange Act of 1934, as amended. Forward-looking statements include all statements, other than statements of historical fact, that address future

activities, events, or developments, including without limitation, business or investment strategy or measures to implement strategy, competitive strengths, goals,

expansion and growth of our business, plans, prospects and references to our future success. You can identify these statements by the fact that they do not relate

strictly to historical or current facts. Words such as “anticipate,” “estimate,” “expect,” “project,” “intend,” “plan,” “believe,” and other similar words are intended to identify

these forward-looking statements. Forward-looking statements can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. Many

such factors will be important in determining our actual future results or outcomes. Consequently, no forward-looking statement can be guaranteed. Our actual

results or outcomes may vary materially. Given these uncertainties, you should not place undue reliance on these forward-looking statements.

The quoted indexes within this report do not reflect deductions for fees, expenses or taxes. These indexes are unmanaged and cannot be purchased directly by

investors. Index performance is shown for illustrative purposes only and does not predict or depict the performance of any investment. There may be material factors

relevant to any such comparison such as differences in the volatility, and regulatory and legal restrictions between the indexes shown and the strategy.

For Institutional Use Only and may not be reproduced, shown, quoted to, or used with members of the public.

DEFINITIONS

The NCREIF Property Index (NPI) is a quarterly, unleveraged composite total return index for private commercial real estate properties held for investment purposes

only. The capital value component of return is predominately the product of property appraisals.

The FTSE EPRA/NAREIT North America Index is designed to track the performance of listed real estate companies and REITs in North American markets.

Green Street’s Commercial Property Price Index is a time series of unleveraged U.S. commercial property values that captures the prices at which commercial real

estate transactions are currently being negotiated and contracted.

Nominal cap rates calculated as the difference between revenues and operating expenses, as a percentage of property value.

An FFO multiple is the multiple of funds from operations (FFO) per share of a company. FFO measures net income, excluding gains or losses from sales of property and

adding back real estate depreciation.

Infill industrial developments are typically situated in established markets, where new supply cannot be easily added due to geographical or other constraints.

ENDNOTES

i. The Public Securities Group (Brookfield Investment Management Inc.)

is a wholly owned subsidiary of Brookfield Asset Management Inc.

CONTAC T US

Telephone: 1-855-777-8001

Email: publicsecurities.enquiries@brookfield.com

Or visit our website at www.brookfield.com

© 2018 Brookfield Investment Management Inc.

RE_03-18

GLOBAL INDUSTRIAL REAL ESTATE: CURRENT TRENDS AND POTENTIAL DISRUPTORS 6You can also read