Green Bond Investor Presentation - Agder Energi

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

October 26, 2017 Green Bond Investor Presentation

Our vision: A leading Norwegian renewable energy group

Agder Energi in brief Vertically integrated utility company Fourth largest supplier of hydro power – mean production of 8.1 TWh Fourth largest network company – 195 000 customers Leading market share in retail power sales – appox. 18 TWh in end user sales Operating revenues approximately NOK 10 bn with 1 430 employees Government owned – 54.5 % by Agder municipalities and 45.5 % by Statkraft Headquarter in Kristiansand, Norway

Key credit strengths Strong market position Low cost profile and flexible producer of hydro power Monopoly position through operation of distribution grids in the Agder Counties Strong cash flow High share of price hedging next 3-5 years, robust hedge the following 10 years due to long term power sales contracts Stable and considerable cash flow from monopoly business Investment flexibility Optionality in existing project portfolio Strong and stable ownership structure 30 coordinated municipalities and Statkraft (A-), which is 100 % owned by the Norwegian state (AAA)

Core business activites

Hydro Power Network

Build and operate Build and operate

hydro power stations distribution network

Market

Energy Management and LOS: Private end user sales

Trading Otera: Infra structure contractor

Maximising profit of the Varme: District heating and cooling

hydro power portfolio,

business retail sales

Hydro power with high flexibility

River system Mean production Reservoir capacity 9.1 9.0

8.9

(TWh/year) (TWh)

8.1

Otra 3.6 2.7 7.7

Mandal 1.7 0.5

Production TWh

Arendal 1.3 0.7

Sira-Kvina 0.8 0.7

Ulla-Førre 0.3 0.5

Andre 0.4 0.1

Sum 8.1 5.3

2012 2013 2014 2015 2016

Sole network owner in Agder

• Agder Energi Nett owns and operates the regulated transmission and distribution

networks in Aust-Agder and Vest-Agder

• Stable and considerable cash flow

• Smart metering (AMS) replacement on track, investment completed in 2018

• Network capital NOK 4 101 mill

Strategic goals toward 2020 Results and value creation best in industry 20% improved profitability in existing business Develop business models and positions related to digitalization and new energy markets

Focus areas Optimizing existing business activities Positioning to offer scalable hydro power capacity Market operations posisitioning for future energy markets with flexibility and effect Posistioning for future network business Energy solutions to private consumers

Investments 2017-2021

3%

Planned investments cirka NOK 1 050 mill per

year on average in the 5 year period, of which NOK

550 mill per year is comitted and government

imposed

47% 50%

Investments include AMS and Honna, which Agder

Energi Nett has the option to sell to Statnett

Reinvestments in the network is included in the

network capital base

Flexibility in the hydro power project portfolio

Hydro Network OtherInvestments 2017-2021

Largest projects Project cost Completion

(ca, NOK mill)

Network AMS 960 2018

Hydro power Skjerka reservoirs 550 2018

Hydro power Skjerka generator 300 2019

Hydro power Åseral Nord – not approvedDividend policy NOK 400 mill plus 60 % of excess profit Based on the Group’s net income to majority according to NGAAP previous year The dividend policy is a rule of thumb, qualitative assessment annually

Financial update

Highlights second quarter 2017 Profit from operations NOK 1 329 mill (NOK 1 270 mill) in underlying EBITDA Production Power generation 4 746 GWh (5,486 GWh) Average spot price NO2 26,5 øre/KWh (21,2 øre/KWh) Other activities NetNordic Holding AS was sold in June, closing in August Agder Energi Nett is more than half way to completion of replacing the electricity meters with new digital ones (AMS)

Reservoir levels NO2

100%

80%

% of normal

60%

40%

20%

0%

jan. feb. mar. apr. may jun. jul. aug. sep. oct. nov. dec.

2017 2016 Avg. 10 yrsPower prices NO2

40

35

30

25

Øre/KWh

20

15

10

5

0

jan. feb. mar. apr. may jun. jul. aug. sep. oct. nov. dec.

Spot/forward price 2017 Spot price 2016Revenues and EBITDA per segment

Revenues (NOK mill) EBITDA (NOK mill)

12 000 3 000

2 531 2 537

10 000 2 500 2 440

2 194

8 000 2 000

1 500 1 377

6 000

4 000 1 000

2 000 500

0 0

2013 2014 2015 2016 2017H1 2013 2014 2015 2016 2017H1

Hydro Network Market Hydro Network MarketSolid cash flow providing financial strength

Cash Flow (NOK mill) FFO*/Net Debt

2 000 1 779

30%

1 486 1 512 1 502

1 500 25,1%

25%

21,8%

1 000

19,4%

20% 18,4%

500

0 15%

-500

10%

-1 000

5%

-1 500

-2 000 0%

2013 2014 2015 2016 2013 2014 2015 2016

Operational CF Net investments Dividends FFO*/Net Debt

*Unadjusted, adjustments are made in rating. Interest bearing debt on 4 quarters rolling basisRobust funding structure and diverse maturity profile

Funding sources Maturity profile (NOK mill)

1 600

1 400

7%

7% 1 200

1 000

800

54%

600

33%

400

200

0

2017 2019 2021 2023 2025 2027+

Bonds EUR Loans USPP CP

Bonds EUR Loans USPP CP

Unutilized credit facilities NOK 1 500 mill to support short term funding and refinancing risk, overdraft facility

NOK 1 000 mill for operational liquidity and Nasdaq cash requirementObtained Scope credit rating in Aug-17 Vertically integrated business model with monopolistic power distribution, strong position of hydro power generation in the merit system and leading retail sales business Profitable and environmentally-friendly hydro power production with substantial hedging agreements and sizeable reservoir capacity Long-term, committed majority owners that are jointly organized and show ability and willingness for potential parent support

Agder Energi Green Bonds Agder Energi: God kraft-godt klima

Renewable hydro power in context of emissions

1 200 Grams CO2/KWh

1 000 Hydro power part of future ambitions of low

emissions

800 ‒ Rule of thumb conventional coal fired plants

1 000 x higher CO2 emissions than hydro power

600

‒ Source: Eurelectric, LCA figures

400

Green Certificates

200 ‒ Norwegian-Swedish political initiative to increase

renewable power production by 28 TWh by 2021

- ‒ Agder Energi build profitable hydro power

projects with granted concessionAgder Energi’s Green Bond Framework

Eligible Projects

Project

• Renewable Energy – hydro power (wind power) and

pool

related infrastructure

• Energy Efficiency – connection of renewable energy

to transmission networks, upgrading of transmission

and distribution networks, energy storage, energy

recovery and smart grids

Selection of projects

• Cooperation treasury, relevant business unit and

environmental advisor

Use of Green Bond Proceeds

• The green bond proceeds may be used to purchase or

develop new eligible projects as well as to renovate,

upgrade and refinance existing eligible projects Eligible ProjectsCICERO - an independent provider of second opinions

Assessment Begins Draft Second Opinion Final Second Opinion

Green Bond

Framework

Green Bond Climate

Principles Science

Clarifications with

Sustainability the Issuer as needed

Strategy and

Reports

Relevant

✓ Use of proceeds

standards

✓ Management of proceeds

Other relevant ✓ Governance and Transparency

documentation

✓ Impact Reporting

Input from Issuer Week 1-2 Week 3 Second OpinionCICERO’s second opinion of Agder Energi’s Green Bond Framework

“Based on the assessment of the project types that will be financed by the green

bond, and the assessment of policies and reporting standards, Agder Energi’s

Green Bond Framework receives a Dark Green shading”

Strengths: Weaknesses:

• HSE risk assessment established across all • Environmental overview of supply chain is

operations insufficient

• Environmental risk analysis on a project level

through Miljøoppfølgingsprogrammet

(“MOP”)

• Focus on environmental concerns in hydro

power projects

• Good reporting standardsAgder Energi’s environmental policy

Agder Energi’s Corporate Social Responsibility policy

‒ Based on national and international laws regulations with focus on human

rights, labour rights, environment and anti-corruption

‒ Subsidiaries are responsible for monitoring and reporting risks, group CRS

reporting on CO2 and NOx emissions

Agder Energi Vannkraft’s environmental strategy

‒ Production within concessions and national and international laws and

regulations

‒ Work pro-actively and systematically to reduce negative environmental

impacts from operations within any given concession

‒ Waste Management

‒ Hydrology / Biology / Natural Resources

‒ Maintain high knowledge on environment where the company is operating

‒ New projects are monitored under a separate environmental

management plan, setting targets and requirements to the contractorsExtensive NVE concession process

AE produces OED produces

AE produces NVE to decide

impact study NVE produce proposition to

note of comprehensive

and send proposition to the national

intention to -ness of impact

application to OED assembly for

NVE study

NVE final decision

‒ Process takes normally 5-10 years before final concession is granted

‒ Througout the process, there are several open public hearings

‒ Independent expertise do separate studies within different focus

areas, such as local environmental impact on fishing, farming, natural

environment, emissions etc

‒ NVE does the professional evaluation of the project

‒ OED does the professional and political evalutation and arrives at a

positive conclusion if the advantages outnumber the disadvantagesIveland II, Otra river system

Iveland II – new renewable hydro power production

‒ Increased annual production 140 GWh (150 GWh qualify for

green certificates)

‒ Applicaton 2007, concession 2012, completed in 2016

‒ Installed capacity increased by 45 MW

‒ Total investment of NOK 700 mill

‒ Reduction of 275 tons of CO2 due to utilization of non-standard

concrete

‒ Option in new project to utilize non-standard concrete

‒ 140 GWh hydro power capacity compare to more than 130 000

tons of CO2 emissions from a conventional coal power plant

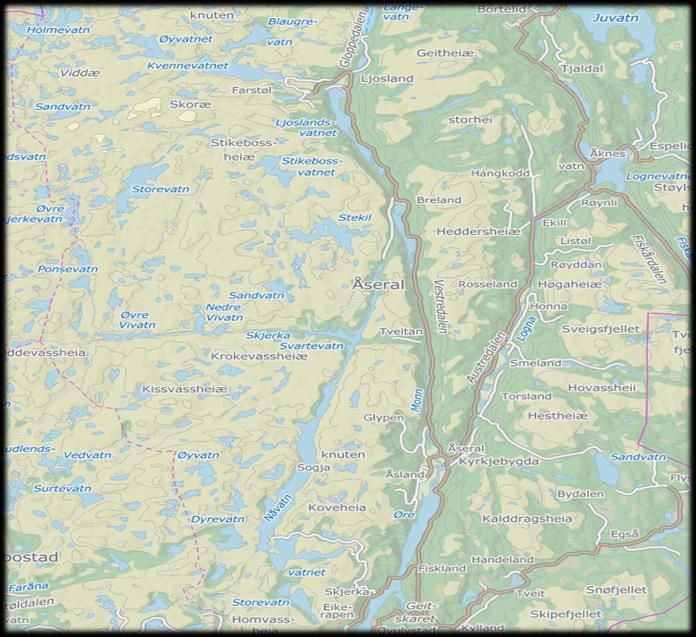

‒ NIB issued a green bond based on financing part of IvelandÅseral Projects, Mandal river system

Dam Langevatn Åseral Projects – maintain existing and build

Kvernevatn

new hydro power capacity

‒ Several separate projects with individual

investment decision

‒ New dam Langevatn,

Øygard ‒ New tunnel Langevatn/Nåvatn 13 km

‒ Kvernevatn and Øygard hydro power stations

‒ Skjerka generator 2

‒ Concessions granted

Åseral Nord – maintain hydro power infra

structure

Skjerka 2 ‒ Replacing Langevatn dam, government imposed

‒ Regulation increases by 10 meters/14%

‒ New tunnel

‒ Investment total (not approved, to be deceded)

‒ Ongoing procurement process

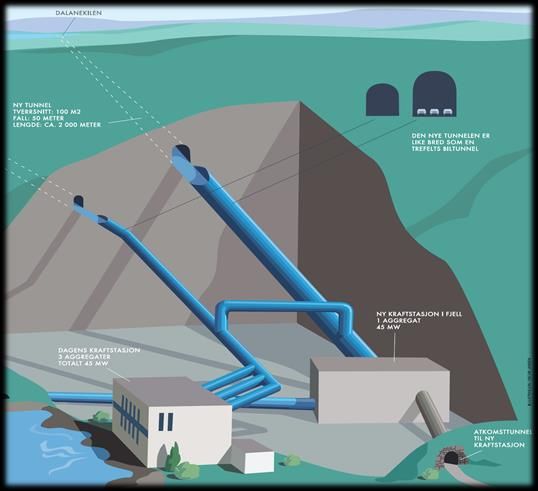

‒ Expected completion 2021Skjerka generator and dams, Mandal river system

Skjerka 2 – safeguard existing and increase

production capacity

‒ Existing generator 650 GWh

‒ A 2nd generator reduces production risk, loss at

maintenance, increases flexibility premium

‒ Increase production of 18 GWh

‒ Investment of NOK 300 mill

‒ Expected completion 2019

‒ Production site prepared for a 2nd generator

Skjerka dams – maintain hydro power

infrastructure

‒ 2 new dams replacing 5

‒ Increase production of 40 GWh

‒ Lifting water level of Skjerkevann by 23 meters

‒ Investment of NOK 550 mill

‒ Expected completion 2018

‒ Government imposedAnnual Green Bond Report

Agder Energi will provide an annual

investor letter covering:

‒ Projects financed (eligible projects are

defined together with environmental advisor)

‒ Impact reporting

‒ Use of proceeds from the ear marked

account

Annual Green Bond Report

2018Summary

Agder Energi is a Norwegian vertically integrated utility company owned

by 30 municipalities and Statkraft (A-)

‒ Highly competitive and flexible producer of renewable hydro power

‒ Mean production 8.1 TWh, 5.6 TWh reservoir capacity

‒ 4th largest grid company with 195 000 customers

‒ Strong and stable cash flow, high share of price hedging

‒ Scope rating of BBB+

The Green Bond Framework will primarily finance renewable energy

‒ Examples of eligible projects Iveland, Skjerka and Åseral Nord totaling

approximately NOK 2.3 bn in investments

‒ Received the highest possible rating by CICERO – Dark Green

‒ Green Bonds natural funding source for hydro power investments

‒ Adds to the diversification of funding sourcesDisclaimer This document has been prepared by Agder Energi AS (“The Company”). This document is not to be reproduced or distributed, in whole or in part, by any person other than the Company. The Company takes no responsibility for the use of these materials by any person. The information contained in this document has not been subject to independent verification and no representation, warranty or undertaking, express or implied, is made as to, and no reliance may be placed on, the fairness, accuracy, completeness or correctness of the information or opinions contained herein. Neither the Company nor its shareholders, its advisors, its representatives or any other person shall be held liable for any loss arising from any use of this document or its contents or otherwise arising in connection with this document. In the event of any discrepancies between the information contained in this document and the public documents, the latter shall prevail. This document does not constitute an offer to sell or an invitation or solicitation of an offer to subscribe for or purchase any securities, and this shall not form the basis for or be used for any such offer or invitation or other contract or engagement in any jurisdiction.

You can also read