How Online Shoppers Pay in European Markets - JP Morgan

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

How Online Shoppers Pay in European Markets Which payment options do you need to offer in European countries? An IMRG report, supported by J.P.Morgan, looking at the importance of various payment methods across European countries. 1 | www.imrg.org Supported by: IMRG © - September 2018

A shifting landscape

A certain event beginning with a capital ‘B’ is looming, with March

2019 only a few short months away now. The exact shape the UK’s

exit from the EU takes is still very open – which might have

business ramifications around currency fluctuations, tariffs and

access to non-UK workers.

So with all this potential disruption to come (or very little – as has

ever been the case with Brexit, no-one is really sure), it wouldn’t

appear on the face of it to be a good time to be expanding

internationally.

But – demand on UK retail sites from international shoppers

actually increased following the June 2016 referendum, as sterling fell sharply against the euro,

so EU shoppers found their cents were suddenly going farther.

Now just might be a good time after all, but trading into international markets is complex. For the

purposes of this report then, we have focussed explicitly on the penetration of payment methods

across Europe to help you understand how to structure your proposition there and where things

might be going.

Andy Mulcahy, Strategy and Insight Director, IMRG

The case for Europe

Awareness of changes in consumer behaviour is essential for

companies hoping to take advantage of the opportunities the

European online retail market presents. Bricks-and-mortar retail

sales in Europe may be relatively stagnant, but as our recent reports,

‘Country Insights: The Changing Dynamic of Payments in Europe’

have made clear, the European ecommerce market is thriving.

Payment methods are constantly evolving in parallel with

increasingly sophisticated consumer demands and sentiment – a

positive sign of a healthy, dynamic market. Bolstered by numerous factors – including high levels

of internet connectivity, a boom in smartphone use, technological innovation and increasing

regulatory support for digital payments – many of the countries we assessed in our reports are

positioned for double-digit growth in online shopping over the next two years.

Now, more than ever, businesses of all sizes can embrace the opportunities afforded by cross-

border expansion, bolstered by a real insight into the payments landscape.

Shane Brodbin, Vice President, EU Product Solutions, J.P. Morgan Merchant Services

2 | www.imrg.org

IMRG © - September 2018

Unintended consequences

We track the percentage of online retail orders that go to cross-border destinations each month

in the IMRG MetaPack Cross-Border Index1. There are a number of individual countries tracked

within that index but, for reporting purposes, we also split the data by EU and non-EU volumes.

In recent years, this index has recorded a significant shift in the volume of packages being

delivered to EU countries, as shown in the chart below. This movement is likely correlative to the

post-June 2016 strength of the euro against sterling, making it a potentially rewarding time for

retailers to consider optimising their proposition for European markets while interest levels remain

high.

Since the back end of 2017, the percentage of cross-border orders going to EU destinations has

been consistently in the 65-70% range.

Breakdown of total cross-border volume Cross-Border - EU

2 years rolling Cross-Border - Non EU

80.0%

70.0%

60.0%

50.0%

40.0%

30.0%

20.0%

10.0%

0.0%

Sep-16

Mar-17

May-17

Jul-17

Mar-18

Oct-16

Jan-17

Sep-17

Oct-17

Jan-18

May-18

Jul-16

Nov-16

Nov-17

Jul-18

Aug-16

Apr-17

Aug-17

Apr-18

Jun-17

Jun-18

Feb-17

Feb-18

Dec-16

Dec-17

For the purposes of this report, we’re focussing exclusively on how customers in some of these

European countries pay for their products, for those looking to expand operations there.

Routinely sewn together into the bracket of ‘continental Europe’, you would be forgiven for thinking

that the separate countries across the Channel adhere to similar payment practices. The reality

is this: each individual market has its own payments culture which varies from country to country,

sometimes wildly so. For example, while UK customers are predominantly reliant on card

1

IMRG MetaPack Cross-Border Index, https://www.imrg.org/data-and-reports/imrg-metapack-cross-border-

indexes/

3 | www.imrg.org

IMRG © - September 2018

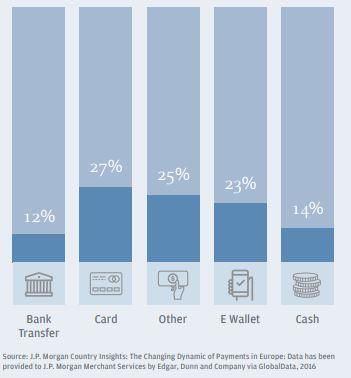

payments (54%)2, only 12%3 of shoppers in the Netherlands opt for this method, with the prevalent

choice instead being bank transfer (62%)4.

The onus, therefore, is on retailers to provide an adept payment option which coheres with the

country’s individual shopper preferences. If shoppers there do not recognise or feel comfortable

with the payment options available to them, they are unlikely to complete a purchase.

A brief overview of ecommerce in Europe

There is an essential point which needs to be addressed and borne in mind whenever cross-

border trade is being considered – which is that the payment frameworks in individual countries

should not be viewed in isolation. Each of the respective European countries are continually

oscillating on a range of factors: technological, sociological, economic, and political. Each of these

factors has a direct potential impact on payments: not only the volume of products being

purchased, but also the average basket value, demographic of purchasers, relevant regulation

and whether products are being bought in-country or externally.

Clearly, payments are only one part of any overall cross-border market strategy and, prior to

launching or ramping up activity in any country, it is recommended that you research the market

in detail to avoid making basic mistakes and give your approach the best chances of success.

IMRG provide a set of comprehensive country guides to help you with this5, but, for basic

comparison purposes here, the following table gives an overview of the most populated

ecommerce markets in Europe6:

Country GDP B2C Average online Internet Smartphone

ecommerce spend per penetration Penetration

market value person per year

UK €2.4trn €156bn €3,625 93% 65%

France €2.3trn €72bn €1,780 86% 53%

Germany €3.1trn €67.3bn €1,161 88% 55%

Spain €1.23trn €24.19bn €1,089 82% 82%

Italy €1.52trn €20bn €938 65.6% 50%

Switzerland €540bn €9.8bn €1,815 87.2% 64%

Netherlands €0.73trn €20.16bn €1,090 94% 64%

2

J.P. Morgan’s Country Insights: The Changing Dynamic of Payments in Europe – Overview,

https://www.jpmorgan.com/jpmpdf/1320745634800.pdf

3

J.P. Morgan’s Country Insights: The Changing Dynamic of Payments in Europe – The Netherlands,

https://www.jpmorgan.com/jpmpdf/1320745416256.pdf

4

Ibid.

5

IMRG Cross-Border eCommerce Trading Guides https://www.imrg.org/data-and-reports/cross-border-

ecommerce/

6

J.P. Morgan’s Country Insights: The Changing Dynamic of Payments in Europe,

https://www.jpmorgan.com/europe/merchant-services/payment-insights

4 | www.imrg.org

IMRG © - September 2018

(Continued from previous page)

Denmark €265.3bn €13.57bn €3,111 96% 68%

Norway €370.6bn €9.44bn €2,467 98% 68%

Finland €215.6bn €8bn €2,170 92.5% 55%

Sweden €0.4trn €10.44bn €1544 93% 70%

As can be seen, and as might be expected, some markets are more mature than others. However,

each can be rewarding in its own way for the right propositions, so, if one does show some degree

of promise in your particular case, how are people paying for products there?

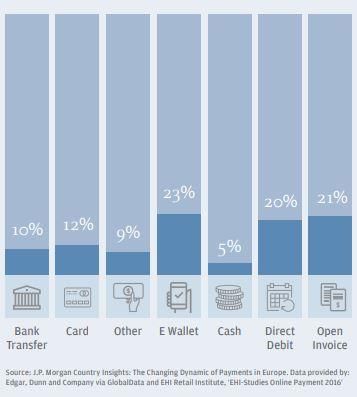

The following chart presents an immediate answer to the question, with the rest of this report

exploring the various payment methods utilised throughout Europe in more detail.

Source: J.P. Morgan’s Country Insights: The Changing Dynamic of Payments in Europe: Data has been provided to

J.P. Morgan Merchant Services by Edgar, Dunn and Company via GlobalData & IMRG, 2016

Popularity of payment methods in key markets

As mentioned in the introduction, a higher proportion of orders are now going to EU destinations

post-referendum vote. Within Europe, where are the bulk of these orders actually going?

The IMRG MetaPack Cross-Border Index tracks the percentage of total cross-border volume that

goes to the top 20 global destinations from UK retailers.

5 | www.imrg.org

IMRG © - September 2018

30% Feb 2018 % of total

March 2018 % of total

25% April 2018 % of total

May 2018 % of total

20% June 2018 % of total

July 2018 % of total

15%

10%

5%

0%

The top 5 European markets (besides Ireland) are France, Germany, Spain, Italy, and The

Netherlands (though the proportion does vary from month to month and sometimes Russia is in

the top 5). According to data from Edgar, Dunn & Co7, the UK, France and Germany account for

almost 60% of all ecommerce in Europe. Interestingly, the following data from Statista shows that

Germans are not big cross-border shoppers compared to other European countries, while

Spaniards and Italians do seem to be more inclined to shop in other markets, which is perhaps

reflective of the relative maturity of those online retail markets.

7

Edgar, Dunn & Company, September 2018

6 | www.imrg.org

IMRG © - September 2018

48% 48%

46% 45%

42%

37%

34% 33% 32%

29%

27%

In the next section, we look at these top 5 European markets and how the payment infrastructure

has evolved – and is evolving – in them.

France

The French ecommerce market is worth €72bn8, the second highest in Europe, only bettered by

the UK (€156bn). With the country flourishing under strong economic growth, its ecommerce

market value is expected to reach €108.53bn by 2020. This figure paints an attractive prospect

for retailers, especially when viewed in tandem with British exports, of which 18% of total cross-

border deliveries were made to France in July 2018. So how is it that French customers are paying

for goods online?

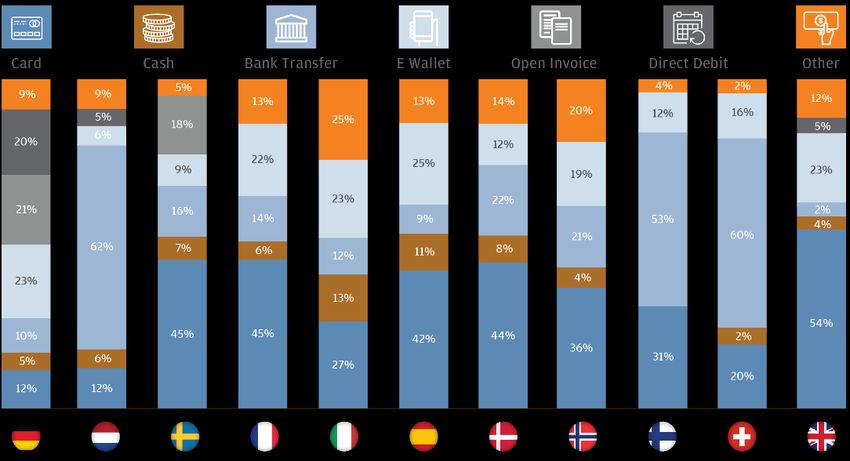

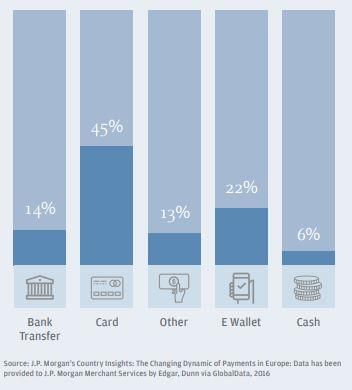

Cards are dominant. As is demonstrated by the following chart, 45% of payments in France are

made by card. This large share is likely attributed to Cartes Bancaires (CB), a well-established

interbank payment system, with the next highest payment method being e-wallets at 22%. CB

payment cards are offered in collaboration with Mastercard or Visa, which means that a merchant

can leverage their existing card acceptance from the UK for France.

8

J.P. Morgan’s Country Insights: The Changing Dynamic of Payments in Europe – France,

https://www.jpmorgan.com/jpmpdf/1320745162989.pdf

7 | www.imrg.org

IMRG © - September 2018

The popularity of e-wallets is increasing; the smartphone-optimised payment method accounted for €15.8bn of transactions in 2016, an increase of 25% from the year before. And this number needs to be viewed alongside smartphone growth in France: with a current smartphone penetration of only 53%, mobile is the fastest-growing channel in the country, expanding at three- times the rate of the overall ecommerce sector. E-wallet transactions should be expected to increase in line with this and, in this regard, PayPal is the provider of choice as the leading e- wallet in the country. Bank transfers are also on the rise, owing to the increase in digital-only banks. In 2016 the payment method grew by 90%, while card growth plateaued. Further to this, telecoms provider Orange launched Orange Bank in November 2017, an online-only banking service which allows customers to pay, check balances, and talk with advisers from their smartphones 24/7. According to IMRG-MetaPack data, France is the largest cross-border recipient of UK goods in the world, besides the US. Cards remain the primary payment method which UK retailers should look to optimise when launching in the country, but with the nation currently undergoing a period of technological innovation, smartphone payment methods are not to be discounted. Commentary from Shane Brodbin, J.P. Morgan “Currency is also worth mentioning: easily overlooked, retailers need to ensure that the prices of their products are displayed in the currency native to whichever country they’re looking to establish themselves within. This could increase the conversion rate from those particular populations.” 8 | www.imrg.org IMRG © - September 2018

Germany Despite having the largest GDP in Europe, Germany is only the third-biggest ecommerce nation, accounting for €67.3bn of online sales9. The German populace are traditionally low-spenders, with the average online spend per-person 25% below the European average. Further to this, Germans appear relatively hesitant when it comes to cross-border ecommerce, likely influenced by the established ‘try before you buy’ principle in Germany: Germany has one of the largest returns rates in Europe, and therefore any retailer would do well to ensure their returns offering is strong when establishing a foothold in the country. In contrast to France, Germany has a relatively low card usage (12%), as shown in the graph below, and in 2016, card payments fell by 41% in value terms. The domestic debit card, Girocard, is not enabled for ecommerce, and therefore German customers turn to other payment methods to conduct online transactions. Open invoices, where the customer pays after reception of the goods, are one of the most widely used payment methods in Germany. While potentially presenting a challenge to retailers in terms of reconciliation, its popularity doesn’t seem to be slowing down or being overtaken by alternative methods: open invoices grew in value by 58.2% year-on-year in 2016. The Swedish online bank Klarna is also now available in Germany, which can handle the tracking of invoices on behalf of retailers. 9 J.P. Morgan’s Country Insights: The Changing Dynamic of Payments in Europe – Germany, https://www.jpmorgan.com/jpmpdf/1320745272912.pdf 9 | www.imrg.org IMRG © - September 2018

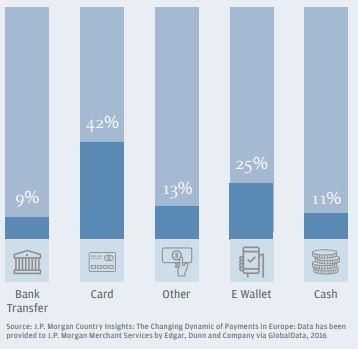

Two other payment methods experiencing strong growth are direct debit and bank transfer, partly driven by the establishment of the Single Euro Payments Area (SEPA). The implementation of this catch-all, continent-wide innovation has streamlined the ease with which online payments can be made, and SEPA direct debits already account for 20% of the payment market in Germany. The most popular bank transfer methods for Germans are GiroPay and Sofort. The last payment method worthy of mention is the e-wallet, of which the German population have been early adopters. The country has one of the highest usage rates of mobile for ecommerce, and an estimated 38% of online shopping is completed by mobile, this potentially explaining the popularity of e-wallets. Of the e-wallet methods available, PayPal is once again dominant, accounting for 20% of the market. Germany is an affluent nation, with an increasing lean towards ecommerce as the sector becomes more optimised. Retailers looking to establish a presence in the country should look to offer an array of payment methods and ensure that their returns policy is clear and efficient. Spain eCommerce in Spain is only now taking root10. In 2016, just 4.1% of retail sales were made online, perhaps owing to years of economic difficulties, high unemployment, and a culture which encourages shopping and socialising outside of the home. However, rather than intending to dissuade, the rising rate of ecommerce presents an opportunity for retailers; Spaniards look to overseas outlets for a vast proportion of their purchases (46.6%), and many leading brands have yet to establish a presence in the country. As a population, the Spanish have a general lack of trust in financial security. Likely owing to this, card payments are the preferred payment method at 42% of online transactions, as they are easily traceable and often offer payment protections. As shown in the following chart, the next highest payment method is the e-wallet at 25%. The total value of e-wallet transactions grew 170% between 2014 and 2016, with PayPal once again being the dominant provider, taking 20% of the market. This figure correlates with Spanish smartphone habits: Spaniards are becoming on-the-move shoppers, with 31% browsing stores on their mobile devices though only 7% finalising purchases via their smartphones. 10 J.P. Morgan’s Country Insights: The Changing Dynamic of Payments in Europe – Spain, https://www.jpmorgan.com/jpmpdf/1320745127975.pdf 10 | www.imrg.org IMRG © - September 2018

Spain is an upcoming player in the European ecommerce market. Internet penetration has increased by more than 20% in the last eight years, and with national debt rallying, the data points towards an increase in the Spanish population’s overall expenditure. With there already being a significant interest in foreign brands, Spain may become a worthwhile foothold in the coming years. Italy At only 3% of their total retail market, Italy has one of the smallest ecommerce markets in Europe11. The figure can be somewhat attributed to the internet penetration rate in the region, which is one of the lowest on the continent at 65.6%. However, in spite of this, the number of ecommerce customers doubled from 2011 to 2016 to 18.8 million, meaning there is still an argument for retailers to consider this market as one of potential. Repeated financial crises and an attitude of mistrust towards major banks have caused a general boycott of cards among the Italian populace, and in corroboration of that, 8 million Italians are unbanked. What this means is that the major payment method in Italy is not affiliated with banking: a large proportion of the population instead opt for prepaid cards, which can be purchased with cash and then used for online shopping. To date, more than 25 million prepaid cards have been issued, making Italy the world’s biggest market for the payment method. 11 J.P. Morgan’s Country Insights: The Changing Dynamic of Payments in Europe – Italy, https://www.jpmorgan.com/jpmpdf/1320745128271.pdf 11 | www.imrg.org IMRG © - September 2018

Of equal interest is the usage of e-wallets in the region. While by value the method sits below cards, as shown in the chart below, by volume, the payment method is leagues beyond the rest. In 2016, there were 203.54 million transactions made by e-wallet, while only 70.68 million purchases were made online by cards. This is perhaps reflected in Italy’s smartphone usage, where 30% of all ecommerce payments are made by mobile. PayPal is once again dominant in this area, accounting for around 17% of the Italian ecommerce market. Cash is an interesting figure to mention. Italy has one of the highest cash usages in Europe, perhaps demonstrating their reluctance for technological innovation. Despite the Italian association CashlessWay implementing a ‘No Cash Day’ initiative, cash has remained resilient in the country. This presents something of a challenge to online retailers, particularly with operational functions such as collection of funds. Italy, while not being a leading ecommerce player in Europe as of yet, nevertheless accounts for a significant portion of UK exports. What this represents is an opportunity for retailers to establish themselves at the crest of Italy’s ecommerce growth, and online merchants rising to the challenge should concentrate on payment methods optimised for smartphone. 12 | www.imrg.org IMRG © - September 2018

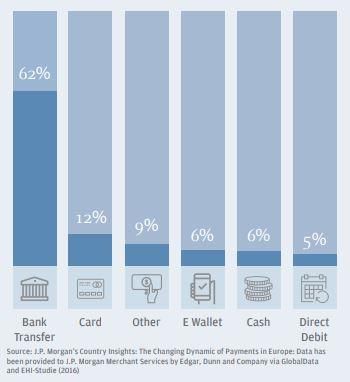

The Netherlands The Dutch population are a people who have fully embraced ecommerce12. 95% of the adult population shopped online in 2016, with almost 40% conducting transactions on their smartphones. Further to this, the B2C ecommerce value increased by 22.6% year-on-year in 2016 to €20.16bn, demonstrating a surging market in which online merchants may find potential for their brands. The Dutch are unique in their overwhelming preference for one particular payment method: the bank transfer. As displayed in the chart below, bank transfers account for 62% of ecommerce transactions, a sizeable 50% higher than the next closest payment method, card, at 12%. The popularity of bank transfers can be attributed to the home-grown service iDEAL, which accounts for 56% of the market by value. iDEAL has a large breadth of shopper coverage and the service is also enabled for mobile transactions, underpinning its position as the singular payment method of choice. Its ubiquity, coupled with the fact that Maestro / V-Pay cards cannot be used online in the country, means that any online retailer looking to establish themselves in the Netherlands needs a payment method optimised for iDEAL as a matter of necessity. 12 J.P. Morgan’s Country Insights: The Changing Dynamic of Payments in Europe – The Netherlands, https://www.jpmorgan.com/jpmpdf/1320745416256.pdf 13 | www.imrg.org IMRG © - September 2018

Commentary from Shane Brodbin, J.P. Morgan “The payments market in Europe is undergoing a period of great transformation. The continuing growth of the ecommerce sector, technological innovation and an evolving regulatory environment are combining to fundamentally change the way people pay for goods and services. The customer of today wants fast, convenient and secure payment options, available on demand and on their device of choice. As a result, online merchants are having to expand the payment methods they work with. To be successful, retailers have to find a way to continue to extend their brand into the digital space, based on consumer-defined, behavioural frameworks that are still emerging.” Conclusion Since 2016, the EU has been the dominant destination for UK online retail cross-border trade. The strength of the euro against sterling has evidently created a surge of European interest in UK goods. Each country has its own culture, and intrinsic to that culture is a certain attitude towards the various ways in which people can pay. While cards are still the most prolific payment option in Europe, some methods have achieved good penetration, and subtle changes in technology and user expectation can create notable shifts in usage. Nevertheless, each individual European country is its own entity. Ultimately, payments are not governed by the options provided, but by the economic, social, political, and technological mindset of the population. Further to this, merchants need to assess each market, as the different payment methods may pose additional costs and challenges to a merchant. In order to gain insight into this changing landscape, J.P. Morgan Merchant Services conducted a survey of eleven different markets in Europe, taking an in-depth look at how the ecommerce sector is developing across the region and examining the changing dynamics of the payments space. You can read all eleven reports at www.jpmorgan.com/europe/merchant- services/payment-insights. 14 | www.imrg.org IMRG © - September 2018

About IMRG For over 20 years, IMRG (Interactive Media in Retail Group) has been the voice of e-retail in the UK. We are a membership community comprising businesses of all sizes – multichannel and pureplay, SME and multinational, and solution providers to industry. We support our members through a range of activities – including market tracking and insight, benchmarking and best practice sharing. Our indexes provide in-depth intelligence on online sales, mobile sales, delivery trends and over 60 additional KPIs. Our goal is to ensure our members have the information and resources they need to succeed in rapidly-evolving markets – both domestically and internationally. www.imrg.org About J.P. Morgan Merchant Services is the payment acceptance and merchant acquiring business of JPMorgan Chase & Co. – a global financial services firm with assets of $2.5 trillion and operations worldwide. It is a leading provider of payment, fraud management and data security solutions, capable of authorising payment transactions in more than 130 currencies. J.P. Morgan, through its Merchant Services business, has uniquely combined proven payment technology with a long legacy of merchant advocacy that creates quantifiable value for ecommerce companies. Its processing platforms provide integrated solutions for all major credit and debit card payments as well as mobile payments and processed more than $1 trillion in payment transaction volume worldwide in 2017. According to The Nilson Report, it is also the top merchant acquirer of ecommerce transactions in Europe 1. Source: 1 The Nilson Report, #1132, May 2018. Chase Paymentech Europe Limited, trading as J.P. Morgan is regulated by the Central Bank of Ireland. The information herein or any document attached hereto does not take into account individual client circumstances, objectives or needs and is not intended as a recommendation of a particular product or strategy to particular clients and any recipient of this document shall make its own independent decision. Information in this document has been obtained from sources believed to be reliable, but neither Chase Paymentech Europe Limited nor any of its affiliates warrant the completeness or accuracy of the information contained herein. 15 | www.imrg.org IMRG © - September 2018

You can also read