Indigo Paints Limited - Issue Opens - Progressive Share Brokers

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Indigo Paints Limited

Issue Opens Wednesday, January 20, 2021

Issue Closes Friday, January 22, 2021

Price Band (in Rs) 1488/1490

Bid Lot 10 shares and multiples thereafter

IPO UPDATE

Indigo Paints Limited

Indian Paint Industry Overview: SNAPSHOT

The Indian paint industry is valued at approximately Rs545bn and is expected Issue Opens Wednesday, January 20,2021

to grow to Rs971bn by 2024. There is a strong co-relation between the

Friday, January 22, 2021

Indian paint industry and the GDP growth of India. It has historically almost Issue Closes

doubled India's GDP growth rate. The industry has registered a CAGR of

approximately 11% during FY14 to FY19. Price Band (Rs) 1488/1490

The Paint industry has a three-stage setup comprising of raw material 10 shares and multiples

Bid Lot

supplier, manufacturers and sellers. Most sales are driven through dealer thereafter

and distributor networks, which sell onwards to local buyers. Hardware Face Value Rs10

stores are usually the retailers in the paint and coating industry, while the

other major retailers may have paint and coating segments within their Listing BSE & NSE

broad range of offerings. Direct sales are a minor component of overall sales.

Type of Issue Offer for Sale & Fresh Issue

India Per Capita Paint Consumption: Fresh Issue 3,000

India's per capita paint consumption increased by a CAGR of 6.8% in the last

Offer Size (Rs Mn) OFS 8,702

seven years from 2.6kg in FY12 to 4.1kg in FY19. Compared to the global

average consumption of approximately 14kg to 15kg per capita, the per Total 11,702

capita consumption of paints and coatings in India is low, indicating a *Implied Market Cap

significant opportunity for market penetration in India. 70,878

(Rs Mn)

Exhibit 01: India’s Per Capita Consumption of Paints & Coatings v/s key P/E (based on FY20 Earnings)* 148.2

Global Economies (in kg), 2019

*Note: Implied Market Cap & P/E are calculated at upper price

band of Rs1490

Issue Allocation

Reservations % of Net Issue

QIB 50

NIB 15

Retail 35

Total 100

Employee Reservation: Upto 70,000 Equity Shares

Employee Discount: Rs148/- per share

Object of the Offer

Source: Company RHP, Progressive Research

Funding capital expenditure for expansion of

existing manufacturing facility at Pudukkottai,

Exhibit 02: Per Capita Consumption of Paints & Coatings India

Tamil Nadu by setting-up an additional unit

adjacent to the existing facility

Purchase of tinting machines and gyroshakers

Repayment/prepayment of all or certain of the

borrowings

General corporate purposes

Source: Company RHP

Please Turn Over Page No 1IPO UPDATE

Indigo Paints Limited

Industry: (contd.)

Exhibit 03: Market size of the Indian paints market by product type, in value (Rsbn) and in volume (MMT), for 2014, 2019

and 2024 (forecast)

Source: Company RHP

The high growth trajectory and shift of preference towards odour free, dust and water resistant paints can be attributed to the

rise in urbanization, growth in the popularity of branded paints, shortening of the re-painting cycle and robust pricing power

prevalent in the paint industry. An increase in demand is expected for both the decorative and industrial paints with massive

infrastructure initiatives by the Government of India.

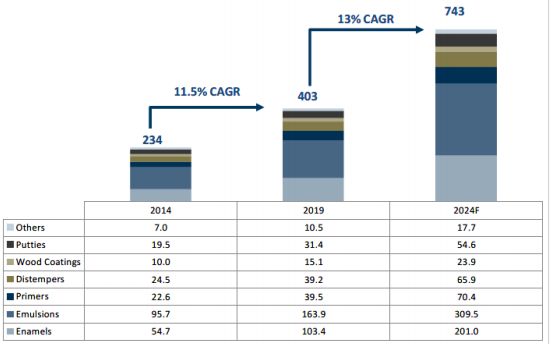

The decorative segment has grown at a CAGR of 11.5% from FY14 to FY19, driven by the increase in consumption of paints in

Tier 2-4 cities, that account for nearly half the total sales. The decorative paints segment represents around 74% of the overall

paint market in India and includes wall finishes for interior and exterior use, enamels, wood finishes and ancillary products such

as primers and putties. Over the past five years, the share of decorative paints has increased from 67% to 74% (FY19).

Exhibit 04: Market size of Indian decorative paints market, in value (Rsbn) & in volume (MMT), for 2014, 2019 & 2024

(forecast)

Source: Company RHP

The Indian decorative paints market is expected to growth at a CAGR of approximately 13% in terms of value and 10.2% in terms

of volume through 2024 driven by a number of factors including increase in the disposable income of individuals and families and

various housing schemes. The Government schemes and policies like ‘Housing for All’ will also be a major driver for growth of

fresh painting. With more such initiatives targeted for the regional population, the demand from smaller cities and towns is

estimated to grow faster benefitting companies like Indigo Paints, which already has an established presence in these

geographies.

Please Turn Over Page No 2IPO UPDATE

Indigo Paints Limited

Industry: (contd.)

Exhibit 05: Indian decorative paints industry, segmented based on sub-product type, in terms of value (Rsbn), for 2014, 2019

and 2024 (forecast)

Source: Company RHP

Entry Barriers:

The Indian decorative paint industry has significant entry barriers. These market entry barriers include the development of an

extensive distribution network through long-term relationships with dealers, the ability to set up tinting machines with dealers,

as well as significant marketing costs and the establishment of a distinct brand to gain product acceptance.

About the Company:

Indigo Paints Limited (Indigo Paints) is engaged in the business of manufacturing paints and is the fastest growing amongst the

top five paint companies in India. It is the fifth largest company in the Indian decorative paint industry in terms of revenue from

operations for FY20. It manufactures the complete range of decorative paints including emulsions, enamels, wood coatings,

distempers, primers, putties and cement paints. It is the first company that started manufacturing certain differentiated products

like Metallic Emulsions, Bright Ceiling Coat Emulsions, Tile Coat Emulsions, Dirtproof & Waterproof Exterior Laminate, Floor Coat

Emulsions, Exterior and Interior Acrylic Laminate and PU Super Gloss Enamel. The multipronged approach by the company

includes introducing differentiated products to create a distinct market in the paint industry, building brand equity for the

primary consumer brand, creating an extensive distribution network and installing tinting machines across the dealer network.

The company sells its products under the brand of 'Indigo', through its distribution network across 27 states and seven union

territories (as on September 2020). Indian cricketer Mahendra Singh Dhoni is its brand ambassador.

Business Operations:

The portfolio of decorative paint products comprises emulsion paints, enamels, wood coatings, distempers, primers, putties and

cement paints. The company manufactures and sells most of its products under the “Indigo” brand of paints. The products are

categorised into four price points namely Platinum Series, Gold Series, Silver Series and Bronze Series. The portfolio of Indigo

Differentiated Products comprises category-creator products and value-added products and are differentiated from other paint

products based on their properties and the end-use they are designed to cater to. These products account for approximately

28% of the sales in FY20. To create demand for their differentiated products, Indigo Paints initially tapped Tier 3, Tier 4 Cities,

and rural areas, where brand penetration is easier and dealers have greater ability to influence customer purchase decisions

(Source: F&S Report). They subsequently leveraged this network to engage with dealers in Tier 1 and Tier 2 Cities and Metros as

well.

Indigo’s slow and steady distribution which meant addition of only one state every year and focusing on smaller markets has

helped build a decent dealer network of 11,000 dealers vs 25,000-30,000 for Berger and Kansai.

Please Turn Over Page No 3IPO UPDATE

Indigo Paints Limited

About the Company (contd.):

Competitive Strengths:

Track record of consistent growth in a fast growing industry with significant entry barriers

Differentiated products leading to greater brand recognition and enabling expansion into a complete range of decorative

paint products

Focused brand-building initiatives to gradually build brand equity

Extensive distribution network for better brand penetration

Leveraged brand equity and distribution network to populate tinting machines

Strategically located manufacturing facilities with proximity to raw materials

Strategies:

Continue to focus on developing differentiated products to grow market share

Further strengthen the brand to consolidate position as a leading paint company in India

Deepen penetration in existing markets and expand presence in select new territories by populating tinting machines

Expand the manufacturing capacities

Proposed Expansion Plans:

The company will utilise funds from its fresh issue for the expansion of the manufacturing facility at Pudukkottai in Tamil Nadu,

purchasing tinting machines and gyroshakers and repaying borrowings. In order to meet the growing demand for water-based

paints, the company has proposed to expand its Pudukkottai facility to include capacities for manufacturing water-based paints,

distempers and primers on a land parcel that it owns which is adjacent to the existing manufacturing unit. Consistent with past

practice, it will look to add capacity in a phased manner to ensure that it utilizes capacity at optimal levels. Post completion of

the proposed expansion plans, the expansion unit is expected to have an estimated installed capacity of 50,000 KLPA and is

expected to be operational during FY23. The company is also in the process of carrying out capacity expansion plans at its

existing Jodhpur facility. These additions are being carried out at both Unit I and Unit II with respect to liquid paints such as

emulsions and primers, and powder paints such as putties.

Financials:

During FY20, Indigo reported revenue of Rs6,248mn net profit of Rs478mn. The operating leverage doubled the PBT to Rs670mn

for the same period. The company has clocked 47% sales CAGR over FY15-20 (organic growth CAGR: 40%+; relative market share

has moved from near-zero to 2.5% over FY15-20 in decorative paints). The company has incurred high ad spends in the last 4-5

years and is now leveraging its brand equity to strengthen the presence of tinting machines across retailers. The average working

capital cycle of 23 days is the lowest in the business. Over the last 2-3 years, the company has been aggressively expanding its

geographical footprint and increasing its brand salience. Post the IPO, Indigo would be a debt free company. Compared to the

peers, in FY20, Indigo reported ROE of 24.3% which is slightly lower than Asian Paints and Berger Paints India but better than

Kansai Nerolac Paints and Akzonobel. The firm has doubled its PAT margins from 3.2% in FY18 to 7.7% in FY20 while peers like

Asian Paints and Berger Paints India were able to increase margins by 2.5% and 3.4%, respectively. As the differentiated products

account for 28% of the sales, the company’s material cost at 51% to the revenues is the lowest among all the listed peers. The

balance sheet remains healthy with D/E ratio merely at 0.13x as on 1HFY21.

Exhibit 6: Financials Snapshot

Revenues (Rs mn) FY18 FY19 FY20 6M ending Sept,2020

Sales 3,951 5,356 6,248 2,594

EBITDA 258 541 910 481

EBITDA Margin % 6.5 10.1 14.6 18.5

Net Profit After Tax 129 269 478 272

Net Profit Margin % 3.3 5.0 7.7 10.5

Earning Per Share 2.9 6.0 10.6 6.0

RoNW (%) 10.1 18.2 24.3 12.1

Source: Company RHP, Progressive Research

Please Turn Over Page No 4IPO UPDATE

Indigo Paints Limited

Risks & Concerns:

Inability to protect, strengthen and enhance the existing brand could adversely affect business prospects and financial

performance

The continuing impact of Covid-19 pandemic on business and operations is uncertain

It is a highly competitive business and any failure to effectively compete could have a material adverse effect

The company does not enter into long-term arrangements with dealers and any failure to continue the existing

arrangements could negatively affect business and results of operations

The proposed capacity expansion plans relating to manufacturing facilities are subject to the risk of unanticipated delays

in implementation and cost overruns

A significant portion of the sales are derived from the state of Kerala and any adverse developments in this market could

adversely affect business

The business is working capital intensive. If the company experiences insufficient cash flows from operations or is unable

to borrow to meet the working capital requirements, it may materially and adversely affect business and results of

operations

Improper storage, processing and handling of raw materials and finished products may cause damage to inventory

leading to an adverse effect on business, results of operations and cash flow

The business is subject to seasonal variations and cyclicality that could result in fluctuations in results of operations

Outlook and Recommendations:

Indigo is the 5th largest player in the highly competitive paint industry. With zero industrial paints, (which is a drag for the peers

off late) the differentiated products and heavy advertising spends of the company would help it make inroads in the highly

competitive industry with high entry barriers. Indigo Paints clocks healthy margins despite the lower scale leaving scope for some

more operating leverage going forward. The company stands strong to grow in the oligopolistic sector of the consumption space

which is already growing in double digits. The IPO is valued at 140x FY20 and 123x FY21 annualized earnings, which appears to be

priced aggressively, but then the growth prospects look to be better than peers. Considering factors like the expansion

programme, increasing brand awareness, debt reduction, cost controlling measures and huge opportunity from affordable

housing segment, the company does justify the premium valuations. With a positive outlook on the paints sector, we feel that

the company with its strong margins and future growth potential is a promising candidate both from the listing as well as long

term portfolio addition perspective. We thereby recommend a Subscribe to the IPO.

Page No 5IPO UPDATE

Indigo Paints Limited

DISCLAIMERS AND DISCLOSURES-

Progressive Share Brokers Pvt. Ltd. and its affiliates are a full-service, brokerage and financing group. Progressive Share Brokers Pvt. Ltd. (PSBPL) along with its affiliates

are participants in virtually all securities trading markets in India. PSBPL started its operation on the National Stock Exchange (NSE) in 1996. PSBPL is a corporate

trading member of Bombay Stock Exchange Limited (BSE), National Stock Exchange of India Limited (NSE) for its stock broking services and is Depository Participant

with Central Depository Services Limited (CDSL) and is a member of Association of Mutual Funds of India (AMFI) for distribution of financial products.

PSBPL is SEBI registered Research Analyst under SEBI (Research Analysts) Regulations, 2014 with SEBI Registration No. INH000000859. PSBPL hereby declares that it

has not defaulted with any stock exchange nor its activities were suspended by any stock exchange with whom it is registered in last five years. PSBPL has not been

debarred from doing business by any Stock Exchange / SEBI or any other authorities; nor has its certificate of registration been cancelled by SEBI at any point of time.

PSBPL offers research services to clients as well as prospects. The analyst for this report certifies that all of the views expressed in this report accurately reflect his or

her personal views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly

related to specific recommendations or views expressed in this report.

Other disclosures by Progressive Share Brokers Pvt. Ltd. (Research Entity) and its Research Analyst under SEBI (Research Analyst) Regulations, 2014 with reference to

the subject company (s) covered in this report-:

· PSBPL or its associates financial interest in the subject company: NO

· Research Analyst (s) or his/her relative's financial interest in the subject company: NO

· PSBPL or its associates and Research Analyst or his/her relative's does not have any material

conflict of interest in the subject company. The research Analyst or research entity (PSBPL) has not been engaged in market making activity for the subject company.

· PSBPL or its associates actual/beneficial ownership of 1% or more securities of the subject company at the end of the month immediately preceding the date of

publication of Research Report: NO

· Research Analyst or his/her relatives have actual/beneficial ownership of 1% or more securities of the subject company at t he end of the month immediately

preceding the date of publication of Research Report: NO

· PSBPL or its associates may have received any compensation including for brokerage services from the subject company in the past 12 months. PSBPL or its associates

may have received compensation for products or services other than brokerage services from the subject company in the past 12 months. PSBPL or its associates have

not received any compensation or other benefits from the Subject Company or third party in connection with the research report. Subject Company may have been

client of PSBPL or its associates during twelve months preceding the date of distribution of the research report and PSBPL may have co-managed public offering of

securities for the subject company in the past twelve months.

· The research Analyst has served as officer, director or employee of the subject company: NO

PSBPL and/or its affiliates may seek investment banking or other business from the company or companies that are the subject of this material. Our sales people,

traders, and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to the

opinions expressed herein, and our proprietary trading and investing businesses (if any) may make investment decisions that may be inconsistent with the

recommendations expressed herein. In reviewing these materials, you should be aware that any or all of the foregoing, among other things, may give rise to real or

potential conflicts of interest including but not limited to those stated herein. Additionally, other important information regarding our relationships with the company

or companies that are the subject of this material is provided herein. This report is not directed to, or intended for distribution to or use by, any person or entity who is

a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution publication, availability or use would be contrary to law or

regulation or which would subject PSBPL or its group companies to any registration or licensing requirement within such juris diction. If this document is sent or has

reached any individual in such country, especially, USA, the same may be ignored. Unless otherwise stated, this message should not be construed as official confirma-

tion of any transaction. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party,

without the prior express written permission of PSBPL. All trademarks, service marks and logos used in this report are trademarks or registered trademarks of PSBPL or

its Group Companies. The information contained herein is not intended for publication or distribution or circulation in any manner whatsoever and any unauthorized

reading, dissemination, distribution or copying of this communication is prohibited unless otherwise expressly authorized. Please ensure that you have read “Risk

Disclosure Document for Capital Market and Derivatives Segments” as prescribed by Securities and Exchange Board of India before investing in Indian Securities

Market. In so far as this report includes current or historic information, it is believed to be reliable, although its accuracy and completeness cannot be guaranteed.

Terms & Conditions:

This report has been prepared by PSBPL and is meant for sole use by the recipient and not for circulation. The report and information contained herein is strictly

confidential and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any

form, without prior written consent of PSBPL. The report is based on the facts, figures and information that are considered t rue, correct, reliable and accurate. The

intent of this report is not recommendatory in nature. The information is obtained from publicly available media or other sources believed to be reliable. Such

information has not been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy, completeness or

correctness. All such information and opinions are subject to change without notice. The report is prepared solely for informational purpose and does not constitute

an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments for the clients. Though disseminated to all the

customers simultaneously, not all customers may receive this report at the same time. PSBPL will not treat recipients as customers by virtue of their receiving this

report.

Registered Office Address: Compliance Officer:

Progressive Share Brokers Pvt. Ltd,

Mr. Shyam Agrawal,

122-124, Laxmi Plaza, Laxmi Indl Estate,

New Link Rd, Andheri West, Email Id: compliance@progressiveshares.com,

Mumbai-400053;

Contact No.:022-40777500.

www.progressiveshares.com | research@progressiveshares.comYou can also read