Introducing Electric Vehicles in Southern Africa - Brian Hastie Electrification Project Leader and Dealer Network Director Jaguar Land Rover ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Introducing Electric Vehicles in Southern Africa Brian Hastie Electrification Project Leader and Dealer Network Director Jaguar Land Rover (South Africa & Sub-Sahara Africa)

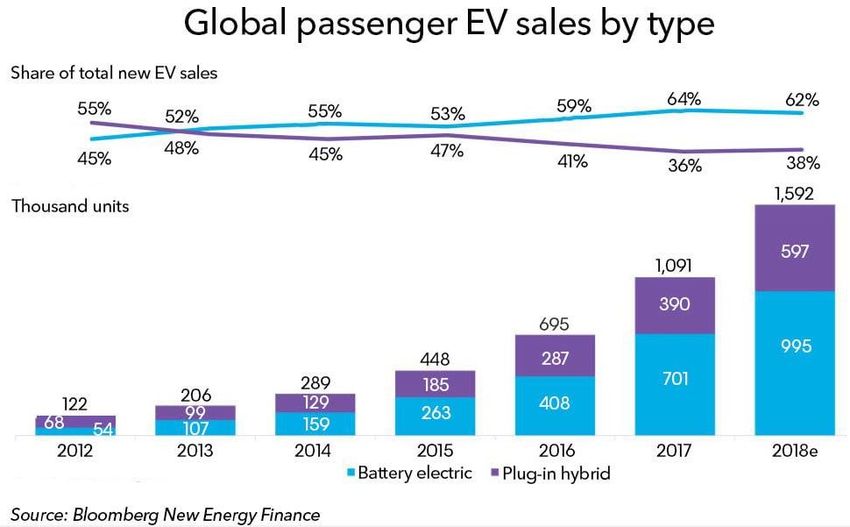

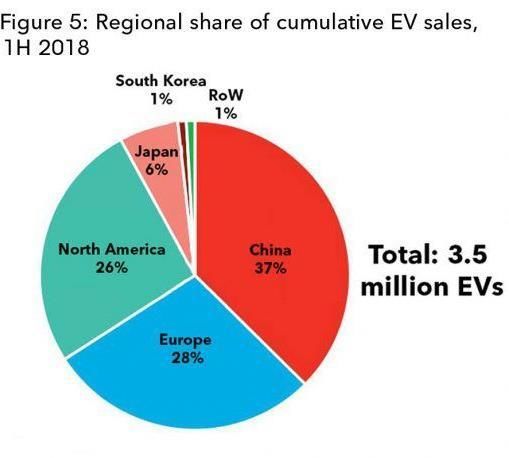

The rate of EV sales has rapidly increased globally Exponential growth since inception

EV sales has universal uptake

EV has Global

take-up

EV Sales by Country Shift from “Compliance cars” to Electric cars that deliver and compete against ICE Mix of mass & premium Brands

EV Product to Market

600

500

90

400

86

300 72

200 101

100

66

96

0

2018 2019 2020 2021 2022 2023

No. BEV & PHEV Model Launches

Source: HIS Market, McKinsey analysis

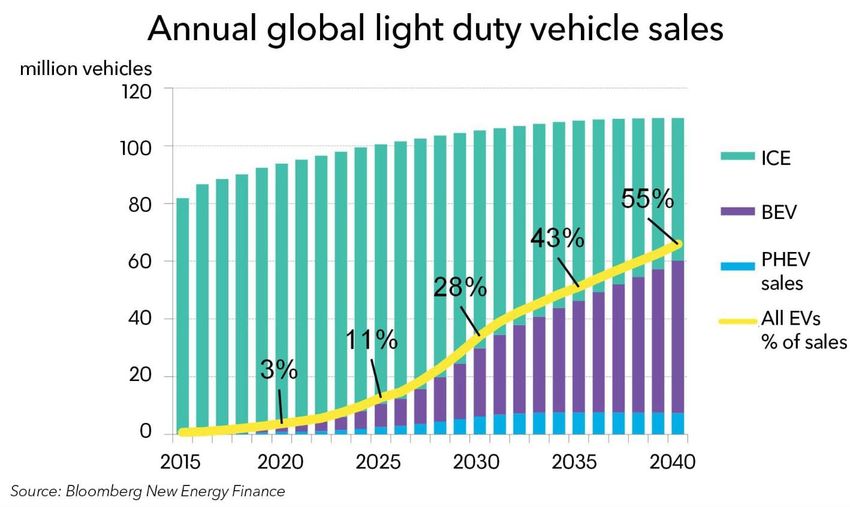

The rapid growth of EV’s will continue into the future

EV sales could reach 60

million by 2040, 55% of

all light-duty vehicles.

• Every day, barriers to an EV

as a credible daily drive are

falling

• The young have bought in to

an electrified future

South African manufacture supplies Global markets

South African sales are sourced from worlds major OEM’s

Potential EV Growth

Most proactive approach

• Short term implementation of Vehicle

Pricing (incentives)

50000

Potential EV Volume Growth in SA • Adoption of models available globally

45000

42961

40000 • Fast growth, but manageable in

35000

30000

terms of Dealer gearing up &

25000 capability

20000

15000 14400 • Steady and viable growth of Public

10000

5000

infrastructure

0

2018 2019 2020 2021 2022 2023 2024 2025

Most proactive approach Forced reactive growth No Change

South African Reality

Battery

Brand Model Price Units/Year

(kWh)

1 Tesla Model 3 50-75 €37k — €80k* 120,000

2 Nissan Leaf E-Plus 60 € 37,000* 80,000

3 Renault Zoe (next gen) 50? € 27,000* 60,000

Less than ¼ of available 4 BMW i3 42 € SA

In 48,000*

since 2015 40,000

5 Hyundai Kona EV 64 € 40,000* 40,000

models introduced 6 Audi e-tron quattro 95 € 85,000

Expected early 2020 30,000

7 Kia e-Niro 39-64 € 40,000* 30,000

8 Jaguar I-PACE 90 € SA

In 80,000

since April 2019 25,000

Premium only 9 Hyundai Ioniq 39 € 34,000* 20,000

10 VW ID Neo 48 € 30,000* 20,000

11 Kia Soul EV 39-64 € 40,000* 20,000

€ 35,000*

Token volume 12

13

Mini

Mercedes

Electric

EQC

42

80 € 70,000*

Expected mid/late 2020

20,000

15,000

14 VW e-Up! 37 € 21,000* 12,000

15 Porsche Taycan 90 $ 90,000

Expected early 2020 10,000

16 Skoda e-Citigo 37 € 19,000* 8,000

17 Peugeot 208 60 € 30,000* 8,000

18 Seat e-Mii 37 € 20,000* 6,000

19 Opel / Vauxhall Corsa 60 € 30,000* 5,000

20 DS DS3 Crossback 50 € 35,000* 4,000

21 Peugeot 2008 60 € 35,000* 2,000South African Reality

High Import

Cost for EV

Duties EV Myths &

Capability at

& Charging

Retailer

No IncentivesEV Eco System: South African EV status quo

Lower GHG is the motive & a key

Environment

benefit

Legislative

Electric

Car

Makers

Vehicles Commercialisation

Infrastructure

Powerway puts the public charging

infrastructure ahead of EV populationEV Eco System

• Overnight Home Charging is

the primary method, most

cost effective

• A Public Charging connected

grid is a necessity for full EV

adoption

Key factors:

Electric

• Standardisation of Chargers Vehicles

• One simple payment

platform

• Independently operated

• Commercial viability Infrastructure

underpinned by volume

Powerway puts the public charging infrastructure ahead of EV populationPowerway Public charging grid – AC22kW & DC60kW Dual Units

Motivation: remove the main purchase objection

Shopping Centre (per Retailer)

Provides “out & about” convenience

+

Highway Stopovers

Make long trips possible

Pretoria

Gauteng & To

Surrounds Durban Polokwane

(West / North To

/ East) Cape Town

Garden

Route

Compatible with all EV’s POWERWAY, in partnership withEV Eco System

• No movement on import

duty situation since 2015

Higher import • EV volume growth /

duty rate. uptake is directly linked to

the duty & rebate structure

No incentives.

Electric • Potential rebates:

Legislative • Carbon Tax breaks

No link to Vehicles • GTS framework

production /

components / • Secondary tax streams

• VAT on Equipment &

exports

Chargers

• Employment for

installations & trainingEV Eco System

• Higher Costs impact Retail

Price

EV’s have

additional costs

• High Retail Price impacts

volume (low uptake) Demand is low

• Model Range walk

imbalance

Electric Poor business

Vehicles Commercialisation case for Local

• EV’s are more expensive to OEM/Importer

market than ICE vehicles

• Equipment

• Competency RISK / OPPORTUNITY

Local Vehicle Manufacture

Local Component ManufactureEV Uptake: no change scenario

No change

• Status quo continues in short to

medium term, with some growth of

EV inevitable

Potential EV Volume Growth in SA

50000

45000 • Existing obstacles and lack of

42961

40000 evolution hold back EV potential

35000

30000

25000 • SA consumer has lack of choice, SA

20000 industry falls behind global

15000 14400 positioning

10000

5000

0 • Likely to impact relevance of local

2018 2019 2020 2021 2022 2023 2024 2025 manufacture

Most proactive approach Forced reactive growth No ChangeEV Uptake: catch-up scenario

Forced reactive growth

• Status quo continues in short to

medium term

50000

Potential EV Volume Growth in SA • Eventually non-EV options run out

45000

42961

and EV’s are adopted in a sudden

40000 way

35000

30000

25000 • Chaotic environment created by

20000 unrealistic demands on capability

15000 14400 • Likely lack of standardisation, poor

10000

5000 customer service

0

2018 2019 2020 2021 2022 2023 2024 2025 • Impact on Brands, further holding

Most proactive approach Forced reactive growth No Change back EV growthShort to Medium term uptake

• Short term implementation of Vehicle Pricing

(incentives)

• Adoption of models available globally

• Fast growth, but manageable in terms of Dealer

gearing up & capability

• Steady and viable growth of Public infrastructure

Potential EV Volume Growth in SA

50000 • Status quo continues in short to medium term

45000 • Eventually non-EV options run out and EV’s are

42961

40000 adopted in a sudden way

35000 • Chaotic environment created by unrealistic demands

30000

on capability

• Likely lack of standardisation, poor customer service

25000

• Impact on Brands, further holding back EV growth

20000

15000 14400 • Status quo continues in short to medium term, with

10000

some growth of EV inevitable

5000 • Existing obstacles and lack of evolution hold back EV

0 potential

2018 2019 2020 2021 2022 2023 2024 2025 • SA consumer has lack of choice, SA industry falls

behind global positioning

Most proactive approach Forced reactive growth No Change • Likely to impact relevance of local manufactureCase Study: The rise of Diesel

Diesel engine share of Premium Segment Volume

Analogy to EV introduction -

40% 37%

growth of diesel power in the luxury

35%

segment in SA:

30%

25%

25%

20% • Initial slow start

15% • Then new technology with

10% enhanced performance launched

5%

1%

• Performance and economy drives

0% popularity

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016Role Players

Environment

Legislation Electric Commercialisation

Vehicles

EV Uptake: no change scenario

Infrastructure

• APDP2

• National Environmental Management Act

• National Transport Master Plan

• Department of Energy - Energy Strategic Plan

• Dept. of Environmental Affairs - National Climate Change Response Strategy

• Department of Science and Technology - 10 Year Innovation Plan

• Department of Trade and Industry - Industrial Policy Action Plan (IPAP)

• Department of Transport - Green Transport Strategy 2050Motor Industry Strategy NAAMSA/GOVERNMENT NAAMSA/EV ECO-SYSTEM • Formation of the Electric, Hybrid & Alternative-fuel Vehicle (EHAV) Committee • Engagement with institutions • Commissioned research into the impact of • Alignment, clarification of roles EV’s, EV “eco-system” + • Co-operate & deliver • Other research & insights • NAAMSA “Position Paper” to be drafted • Engagement with all Government institutions at all levels

You can also read