Investor Presentation May 2018 - Finance Flanders

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Investor Presentation

May 2018

2 I. Main Facts & Figures II. Key Strengths III. Public Finances IV. Consolidated Debt V. Flanders in a nutshell

3

Main Facts & Figures

Key Data

Capital Brussels

Language Dutch

Surface 13 684 km²

Population 6 509 894 (1/1/2017)

Density 485 hab./km² (2016)

Currency Euro

N° of Companies 509,660 (subject to VAT)

Nominal GDP (PPS) EUR 228 bn (2016)

GDP/Capita (PPS) EUR 35 100 (2016)

Real GDP growth rate 1.4% (2016)

Unemployment rate 4.4% (2017)

PPS = purchasing power standards

4

Main Facts & Figures

High GDP per Capita (2016)

40.000

35.000

30.000

25.000

20.000

15.000

10.000

5.000

0

Flanders EU-28 Belgium Germany France Netherlands United Kingdom

Source: Eurostat

5

Main Facts & Figures

Strong Economic Fundamentals

Flanders benefits from very strong economic fundamentals.

Flanders France Germany Netherlands EU - 28

Unemployment Rate (2017) 4.4% 9.4% 3.8% 4.9% 7.6%

Real GDP Growth Rate (average

2011 – 2016)

1.3% 1.0% 1.6% 1.0% 1.2%

• In 2016 the real GDP growth rate was 1.4% in Flanders which was much higher compared to

the other regions (Walloon Region 1.1% and Brussels Region 0.8%)

Source: Eurostat - Labour Force Survey, Study Office of the Governement of Flanders

6 I. Main Facts & Figures II. Key Strengths III. Public Finances IV. Consolidated Debt V. Flanders in a nutshell

7

Key Strengths

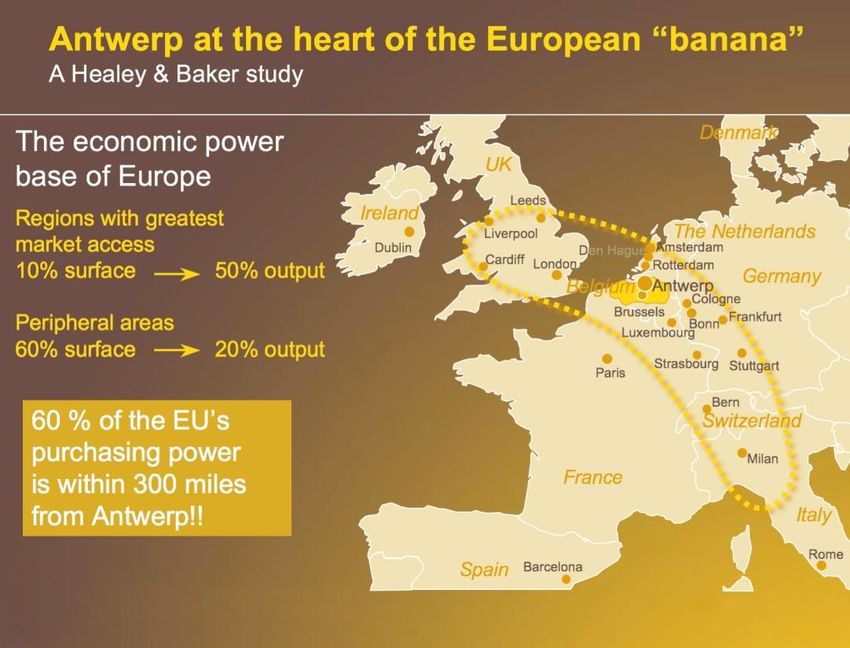

Located in the Heart of Europe

Flanders lies at the center of the EU’s

wealthiest and most populated area;

Highly developed transport and

communications systems so that

companies can take full advantage of this

fact;

Strong stimulus for companies to locate

in Flanders – central location;

Source: Healey & Baker study8

Key Strengths

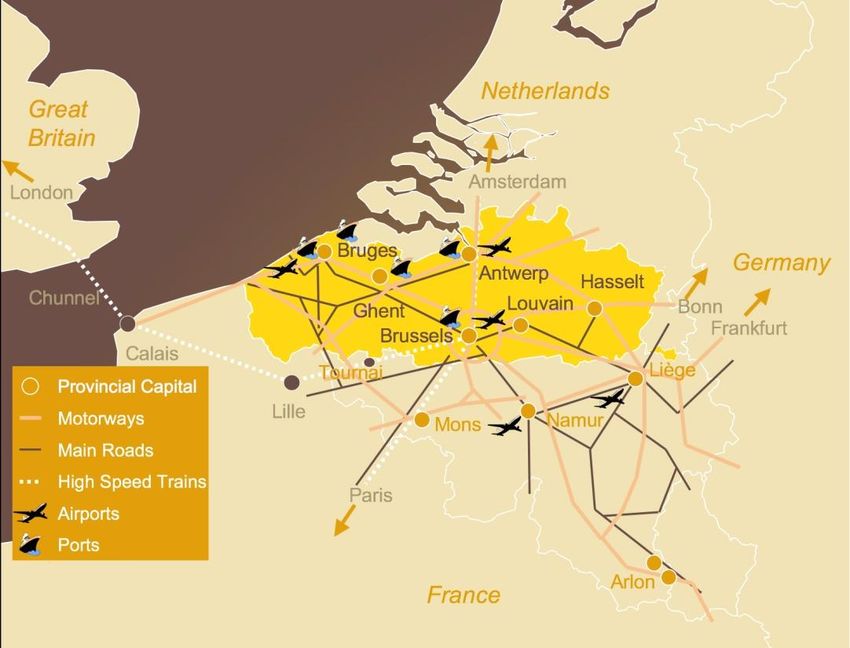

A Unique European Hub

Flanders offers companies rapid and efficient supply

and distribution links with other major European

centers and beyond.

Leading ports Antwerp, Ghent, Ostend,

Zeebrugge

Airport freight & logistic Brussels, Ostend

hubs

Extensive inland Linking into the European

waterway system system

High density of freeways Connecting directly to

other European countries

High density rail network Dedicated freight lines to

other parts of Europe

Source: Healey & Baker study9

Key Strengths

An Economy based on Trade and Services (2016)

Flemish GDP-Sector contribution

primary sector; Construction 6.1%

0,9% Chemicals 3.2%

Iron, Metal & Steel 2.1%

Food & Tobacco 2.7%

secondary sector; Other 11.6%

25,8%

tertiary sector;

73,3%

Real Estate and Business Services 23.8%

Wholesale and Retail 13.6%

Transport 6.4%

Health Services 4.6%

Other 24.9%

Source: Institute of National Accounts10

Key Strengths

Strong Export-Driven Economy

Regional Distribution of Belgian exports (%) Flemish Exports

(2017) (EUR billion)

2,6% 350

14,2%

300

250

Brussels 200

Flanders 150

Wallonie

100

50

0

83,2% 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

The Flemish economy is strongly export oriented: Flanders’ exports represent 83.2% of Belgium’s

total export in volume;

Flemish exports grow steadily over time (+4.99% in 2017);

The region’s most successful export products are chemicals, transport equipment, machines and

equipments, pharmaceuticals and minerals.

Source: Institute for the National Accounts11

Key Strengths

Diversified Base of Trading Partners

Top 10 of Flemish Export Markets in 2017 (as % of total)

18,00%

16,00%

14,00%

12,00%

10,00%

8,00%

6,00%

4,00%

2,00%

0,00%

Germany France Netherlands UK Italy USA Spain India China Poland

The EU28 is the most important Flemish export market and the 3 neighbouring countries (Germany, France

and the Netherlands) are Flanders main trading partners. Also emerging economies like India and China are

steadily becoming more important for Flemish exports.

Source: Institute of National Accounts12

Key Strengths

Foreign Direct Investment Figures & Trade Partnerships

Flanders has a proven track record of welcoming foreign Type of Investments (2017)

businesses to its region.

Mergers&Ac

quisitions:

25,58%

Top 10 biggest investors in 2017 Greenfield:

40,93%

1 USA 21,4%

2 Netherlands 11,6%

3 Germany 10,7% Expansions:

33,49%

4 France 8,4%

Type of Activities (2017)

5 China 6,5%

Sales &

6 Japan 6,1% Marketing:

16,28%

7 Sweden 4,7% Manufaturin

HQ: 1,40%

g: 33,20%

8 United Kingdom 4,2%

R&D: 20,00%

9 Switzerland 3,7%

10 Italy 1,9%

Logistics:

24,65%

Source: Flanders Investment and Trade Office13

Key Strengths

Low Unemployment Rate

25

20

14,9

15 13,5

(%)

12,2

9,7

10 10,8

10,7

8,2

5 4,4

4,4 4,0 3,9

0

Flemish Region Walloon Region Brussels Capitol Region EU 15 countries

Source: Statistics Belgium EAK, Eurostat, Labour Force Survey

Website Steunpunt Werk: http://www.steunpuntwerk.be/

Other graphs on labour market see appendix14

Key Strengths

R&D budget evolution (in million euro)

2500

2000

1500

1000

500

0

Research and Development (R&D) Education and Training (E&T) Scientific and Technological Services (STS)

Source: Department of Economy, Science and Innovation15 I. Main Facts & Figures II. Key Strengths III. Public Finances IV. Consolidated Debt V. Flanders in a nutshell

16

Public Finances

Return to a balanced budget

• Several budgettary challenges in last years

• Financial-economical crisis: Deficit in 2009 and 2010, but within 2 years return to

balanced budget

• Stricter European budgetary surveillance: considerable negative impact on budget from

2013, but gradually integrated in budget (completed in 2016)

• Sixth state reform:

• Financial autonomy raised to 34% (levy surtax on Personal income tax)

• more competences and increase in financial means (approx. 9,7 bn EUR for 2015)

• Recurrent contribution of 1,55 bn EUR to consolidation of public finances of

federal government and social security

• Enhancement of federal tax shift (> 300 mln EUR)

• Budget 2016 : deficit of 468 mln EUR, in realisation deficit reduced to 127 mln EUR

• Budget 2017: surplus of 2 mln EUR, in realisation surplus of 470 mln EUR

• Budget 2018: Balanced budget17

Public Finances

Revenues by Segment

45.000.000

40.000.000

35.000.000

In keuro

30.000.000

25.000.000

20.000.000

15.000.000

10.000.000

5.000.000

0

2014 ACT 2015 ACT 2016 ACT 2017 ACT AB 2018

Institutions within scope of consolidation Lottery funds Own non-tax non-allocated income

Own non-tax allocated income Regional taxes Specific allocations SFA

Regional and Community resources SFA Gross additional personal income tax charge

2014 - the 6th State Reform

• Large increase in revenues

• Major transfer of powers and resources

Comparison budget 2016 / 2017: Increase of 2.7 bn €

reasons?

1. Increase of the regional taxes and grants from the federal level

2. Expansion of the consolidation perimeter

Budget 2018: Revenues at the same level as in the budget 201718

Public Finances

Revenues by Segment

Key revenues 2018:

56% Regional and Community resources from Federal level

33,2% own fiscal instruments:

• 15,4% regional taxes

• 17,8% additional personal income tax charge ( = surcharges)19

Public Finances

Regional Taxes

4%

6% Regional taxes AB 2018

- Registration tax

37%

- Tax on real estate

23% - Road tax (cars)

- Registration tax 2.432.946

- Tax on real estate 156.461

- Tax on first use of car

- Road tax (cars) 1.097.369

- Heavy goods vehicles charge - Tax on first use of car 247.848

- Inheritance tax - Heavy goods vehicles charge 444.267

- Donation tax - Inheritance tax 1.507.653

7% - Donation tax 388.699

2% - Other taxes

- Other taxes 281.327

4%

17% 6.556.570

In keuro

Key regional taxes of Flanders:

Registration tax

Inheritance tax

Road tax for cars20

Public Finances

Breakdown of Public Spending

Education and Training

Welfare, Public Health and Family

Work, professional training and social economy

Chancellory and general government

Mobility and Public Works

Finance and Budget

Other

Economic development, science and innovation

Culture, sport, youth, media

0 4.000.000 8.000.000 12.000.000 16.000.000

2018 AB 2014 ACT

Also in the expenditures we see a large increase, as a result of the Sixth State Reform, in the

adjusted budget 2018 (2018 AB) compared to the realizations 2014 (ACT).

The largest increases are situated in Welfare, Public Health and Family and in Employment and

Social Economy.21

Public Finances

Breakdown of Public Spending

Breakdown of the expenditures 2018 AB Education and training

5% 3% 1%

3% Welfare, public health and family

6% 30%

Chancellory and general government

8%

Mobility and public works

Work, professional training and social economy

8% Finance and budget

Economic development, science and innovation

9%

Environment

27%

Culture, sport, youth, media

other

Key competences in the Flemish budget:

Education

welfare, public health, family22

Public Finances

Realisations

Budgetary targets and results (in mio euro)

1.000

500

0

budget

realisation

-500

-1.000

-1.500

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Despite budgetary difficulties in 2009-2010 (financial and economic crisis) and 2013-2014 (stricter

European surveillance) the Flemish Community has taken immediately the necessary measures to

set the budget back on track.

Budget surplus in 2017: 470 million euro23 I. Main Facts & Figures II. Key Strengths III. Public Finances IV. Consolidated Debt V. Flanders in a nutshell

24

Consolidated Debt

Overview of the Strategy

• Diversified financing strategy: Combination of banking and non-banking financing tools;

• Large and diversified access to short term liquidity: Belgian Commercial Paper programme combined

with a short term credit line of EUR 3.25bn;

• Conservative Risk management:

• Conservative interest rate risk management : indexation linked to fixed rates or simple floating

rates in the Euro zone (Euribor…); distribution fixed rate / floating rate adjusted depending on

the long term economic trends; 95% of the outstanding debt at fixed rate as of 31/12/2017

• Complete hedging of currency risk: no currency risk incurred by the Flemish Community;

• Systematic hedging at the issuance via swaps in EUR;

• Conservative approach on derivatives: No structured products;

• Issuance of bonds as main medium and long term financing tool: Flanders is a recognized issuer in the

capital markets. Purpose is to build a reference benchmark curve;

• Diversification of the investor base;25

Consolidated Debt

Consolidated Debt position

in mio EUR 2015 2016 2017

Direct and indirect debt 4.126,00 4.642,12 5.313,89

VMSW (social housing) 6.313,15 6.282,50 6.112,95

VWF (social housing) 3.005,41 2.842,66 2.705,57

EKM's (social housing) 596,9 590,59 595,41

VIPA (including debt infrastructure

hospitals and rest homes) 1.846,55 1.760,22 1.670,24

DBFM "Schools of Tomorrow" 369,7 393,88 181,96

PPP debt 782,84 779,06 756,93

Hospital infrastructure 0 4.963,21 4.726,93

Rest 1.909,36 1.554,19 1.321,86

TOTAL 18.949,91 23.808,43 23.385,74

In 2016 there was an increase of 4,86 billion EUR. This is mainly due to the take over of the imputed

loans from the federal level (Hospital infrastructure). Without this take over the consolidated debt

would have slightly decreased.

In 2017 the consolidated debt decreased with 420 million euro while an increase of 920 million euro

was expected in the budget 2017.26

Consolidated Debt

Direct Debt position

31/12/2015 31/12/2016 31/12/2017

EMTN 3.201,50 3.516,50 4.836,50

Direct debt instruments 2017

Schuldschein 37,5 37,5

2% 0% 5%

Bank loans 150,44 97,8 95,16 1% 1%

BCP 755 250 0 EMTN

Current account 17,27 738,73 262,27 Schuldschein

Bank loans

FRGE 5,88

BCP

Amoras 50,42

Current account

Ground lease 26,16 91% Rest

TOTAL 4.124,21 4.640,53 5.313,89

95% Fixed Average duration (end 2017):

5% Floating 12 years and 10 months

By the end of 2017 92% of direct debt was financed with the EMTN programme

(EMTN + Schuldschein).

Further increase of duration: from 3 years and 10 months at the end of 2015,

over 10 years and 4 months at the end of 2016 to 12 years and 10 months at

the end of 2017.27

Consolidated Debt

Debt Redemption Schedule

Maturities LT direct debt till 2048

1 200 000 000,00 €

1 000 000 000,00 €

800 000 000,00 €

Bank loans

Schuldschein

600 000 000,00 €

EMTN

400 000 000,00 €

200 000 000,00 €

0,00 €

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

204828

Consolidated Debt

Bond Financings 2017

MATURITY

EMTN/SCHULDSCHEIN ISSUE DATE MATURITY AMOUNT (in EUR) COUPON (%) YIELD (%)

DATE

EMTN – BE0001764183

1 (tap) 2/06/2017 13/10/2026 10 250,000,000 0.375 0.795

2 EMTN – BE0002284538 2/06/2017 2/06/2042 25 1,000,000,000 1.875

3 EMTN – BE0001773275 23/02/2017 23/02/2038 21 20,000,000 1.656

4 EMTN – BE6295854697 14/06/2017 14/06/2019 2 50,000,000 0.000 -0.440

In 2017 the Flemish Community succesfully launched a benchmark of 1.00 billion euro

with a maturity of 25 years and a 0.25 billion euro tap on the 2026 BM

Private placements on EMTN-program: 70 million euro29

Consolidated Debt

Distribution Stats Benchmark 2017

Tap Oct 2026 Bonds 2042 Bonds

Split by Geography Split by Geography

Other

Other 6% France

Scandinavia 4% 8%

6%

Germany & Austria

Germany &

France

Austria UK Benelux

33% 22%

Germany & Austria

Benelux

Benelux

Scandinavia Germany & Other

Benelux UK Austria

51% Other 64%

6%

Split by Investor Type Split by Investor Type

Others

7% Banks/Treasury Other

10% 1%

CB/Agency Insurance &

11%

Fund Managers Pension Funds

Fund

31% Insurance Companies Fund Managers

Banks/Treasury

Insurance &

Fund Managers Banks/Treasury

Banks/Treasury CB/Agency Pension Funds

38% 51%

45%

Others

Other

Insurance

Companies

6% 2930

Consolidated Debt

Bond Financings 2018

MATURITY AMOUNT (in Spread vs

EMTN/SCHULDSCHEIN ISSUE DATE MATURITY COUPON (%) YIELD (%)

DATE EUR) OLO

1 EMTN – BE6301937411 1/02/2018 1/02/2020 2 125,000,000 0 -0.318 15

2 EMTN – BE0001780346 28/02/2018 28/02/2048 30 60,000,000 1.863 9

3 EMTN – BE0001781351 28/02/2018 1/03/2038 20 30,000,000 1.603 8

4 EMTN – BE6303737959 28/03/2018 28/03/2058 40 80,000,000 1.874 9

In the first months of 2018 the Flemish Community already did several private

placements on the EMTN-program for a total amount of 295 million euro.Consolidated Debt

Financing needs 2018 - 2020

in Mio EUR 2018 2019 2020

VMSW 1,000.00 1,225.41 1,135.09

VWF 350.00 323.23 311.49

School Invest 88.53 35.53 49.88

BAM 87.50 262.50 275.1

TOTAL New funding 1,526.03 1,846.67 1,771.57

Loan redemptions 758.71 58.41 322.67

TOTAL 2,284.74 1,905.08 2,094.24

Financing 2018 (in million euro)

2018

EIB 0

BM issue 1,500.00

BCP 150.00

Private placements 400.00

Balance 234.74

3132

Consolidated Debt

Financial instruments

EMTN (updated 5th September 2016)

Flanders has a EUR10 bn EMTN programme, with public issues and/or a series of private

placements

Currently only fixed interest issues

Programme allows flexibility on rates, currencies, redemptions, etc…

Currently outstanding: EUR 4,381.5 mln EMTN and 37.5 mln Schuldschein

Arranger: ING

Dealers: ING, BNP Paribas Fortis, KBC, Belfius, HSBC, Société Générale, LBBW

ECB-eligible

PSPP eligible

Commercial Paper

Flanders has a EUR 1.5 bn BCP-programme

Arranger: KBC

Dealers: KBC, Belfius

Currently outstanding: EUR 0 mln

STEP-compliant

Cashier : ING creditline of EUR 3.25 bn33 I. Main Facts & Figures II. Key Strengths III. Public Finances IV. Consolidated Debt V. Flanders in a nutshell

34

Flanders in a nutshell

Credit rating

Long term credit rating

• Moody’s: Aa2 stable (Belgium:

Aa3 stable)

Short term credit rating

• Moody’s: P-1

ISSUER MOODY'S FITCH STANDARD & POORS

FLEMISH COMMUNITY Aa2 Stable

BELGIUM FEDERAL STATE Aa3 Stable AA- Stable AA Stable

FRENCH COMMUNITY OF BELGIUM Aa3 Stable

WALLOON REGION A2 Stable

BRUSSELS CAPITAL REGION AA Stable35

Flanders in a nutshell

Key Points and Major Strengths

A wealthy, diversified and strong economy, with one of the highest

European GDP per capita combined with a low and stable

unemployment rate. Flanders is considered as Belgian economic

engine;

Strong track record of Budgetary discipline and continued commitment

to fiscal consolidation;

Modest debt burden and ample access to liquidity;

Strong credit rating of Aa2 Stable by Moody’s; above the rating of the

Belgian federal state.36

Questions ?

Questions by email are also possible

For more information please also consult:

http://www.financeflanders.be

3637

Contacts

Koen Algoed

Secretary – general

Flemish Community, Department of Finance and Budget

+32 493 31 63 02

koen.algoed@fb.vlaanderen.be

Hugues Mommens

Senior advisor, head of financial operations

Flemish Community, Department of Finance and Budget

+32 493 51 22 94

hugues.mommens@fb.vlaanderen.be

Luc Keereman

Senior advisor

Flemish Community, Department of Finance and Budget

+32 493 31 63 07

luc.keereman@fb.vlaanderen.be38

Contacts (2)

Kristien Hantson

Advisor

Flemish Community, Department of Finance and Budget

+32 493 31 63 08

kristien.hantson@fb.vlaanderen.be

Heidi Debedts

Assistant to the director

Flemish Community, Department of Finance and Budget

+32 492 15 38 48

Heidi.debedts@fb.vlaanderen.be

For more information please also consult:

http://www.financeflanders.be39 Disclaimer This presentation has been prepared by Flanders for informational purposes only. Although the information in this presentation has been obtained from sources which Flanders believes to be reliable, we do not represent or warrant its accuracy, and such information may be incomplete or condensed. This presentation report is not intended to provide the sole basis for any evaluation of the transactions discussed herein. All estimates and opinions included in this presentation constitute our judgment as of the date of the presentation and may be subject to change without notice. Changes to assumptions may have a material impact on any recommendations made herein. Flanders will not accept any liability whatsoever for any loss howsoever arising, directly or indirectly, from the use of this presentation or the information provided for in this presentation or otherwise arising in connection with this presentation. This presentation is confidential and is provided to you for information purposes only and does not constitute a public offering or an investment service in Belgium. This presentation is being submitted to selected recipients only and neither this presentation nor any other offering materials may be distributed, published or made available to the public in Belgium. This presentation may not be reproduced or passed on (in whole or in part) to any other person than the selected recipients. Neither this presentation nor any offering materials may be used in relation to any investment service in Belgium unless all conditions of directive 2004/39/EC, as implemented in Belgium, are satisfied. Neither this document nor any offering materials can be used to publicly solicit, provide advice or information to, or otherwise provoke requests from, the public in Belgium in relation to the offering. Any offering in Belgium is made exclusively on a private basis in accordance with article 3 of the Belgian law of 16 June 2006 on the public offering of investment instruments and the admission of investment instruments to the trading on a regulated market. © May 2018 Flanders. All rights reserved.

40 APPENDIX

41

Flanders in a Nutshell

Key Investment Highlights

One of the strongest Flanders has a wealthy, diversified and strong economy with one of Europe’s highest

regions in Europe GDP per capita; unemployment rate close to Germany and solid economic growth

Flanders is collecting a greater part of its revenues via own fiscal instruments; which is

Solid Financial

positive in the context of economic growth and increasing GDP per capita levels

Situation

Fiscal flexibility: Flanders can levy more taxes rapidly if needed

Through the 6th state reform, Flanders has received a greater range of competences

Fiscal Autonomy

and benefits from an increased tax autonomy (own fiscal instruments)

Positive track record Over recent years, Flanders has demonstrated its ability to reduce deficits while

of Budgetary discipline maintaining economic growth and social welfare.

Moderate direct debt Despite ESA 2010 rules, moderate levels of debt combined with a sound financial

levels management strategy (no debt wall)42

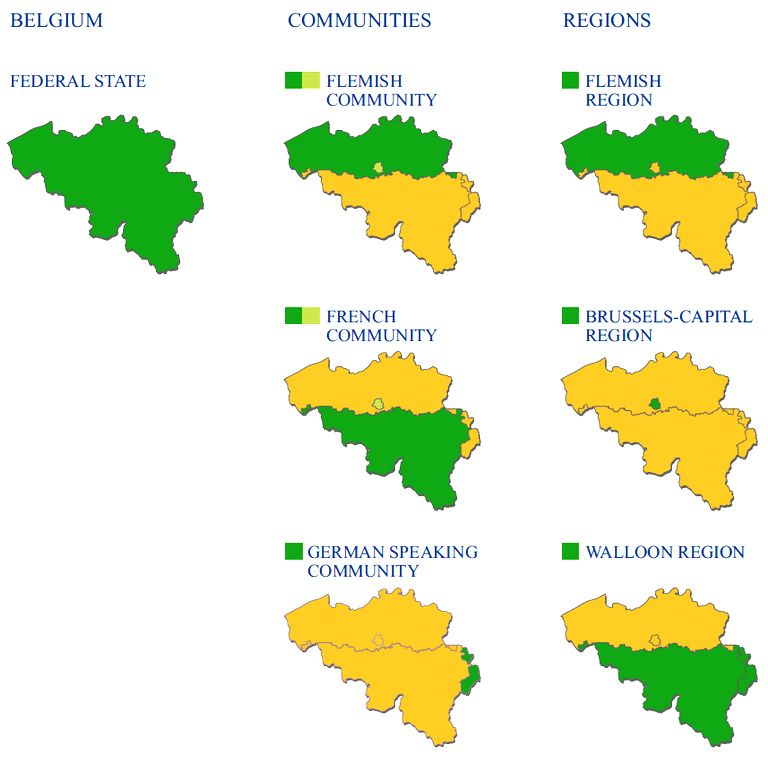

Flanders Part of the Federal State Belgium

Belgium Federal Structure

Since the 2nd State Reform

3 Regions: 3 Communities:

in 1980, the Flemish

Flanders Flemish

Federal State

Wallonia French Community and the

Brussels German

Flemish Region

10 Provinces immediately decided to

merge their competences.

589 Towns and Cities

As a result, Flanders has

one Flemish Parliament,

one Flemish Government

and one public

administration, responsible

for community and

regional matters.43

Flanders Part of the Federal State Belgium

Competence Distribution

Federal State Flemish Community Flemish Region

“powers related to public interest” “powers related to language “powers related to territory

and culture” and economy”

Economic development & co-

Public Finances Education

Defense Culture operation

Security Public health (prevention) Public infrastructure

Justice Welfare Town & country planning

Social Security Language issues Environment

Public Health Child protection Energy

Domestic & International Family Affairs Employment

politics Agriculture

Transport & Communication Foreign Trade

Regional transport

Control & organization of

local governments44

Contribution to the consolidated debt

(Maastricht in million euro)

Consolidated debt of Belgium

2013 2014 2015 2016 2017

Federal Gov and Soc Security 345.167,00 354.636,00 361.995,00 366.083,00 371.154,57

Communities and Regions 45.756,00 48.705,00 48.939,00 57.214,00 57.284,23

Local entities 22.803,00 24.163,00 23.964,00 23.915,00 23.915,00

Total 413.727,00 427.503,00 434.898,00 447.212,00 452.353,80

2013 2014 2015 2016 2017

Walloon Region 18.284,80 19.435,50 20.360,30 21.271,00 21.339,23

Brussels Region 4.278,20 4.219,10 3.893,50 3.799,00 4.146,06

Flemish Community 16.710,80 18.285,20 17.341,10 18.187,10 18.157,27

French speaking Community 5.916,50 5.958,10 6.408,10 7.075,20 7.105,50

Interregional 366,70 460,80 476,00 6.428,90 6.056,65

Rest 198,90 346,00 459,80 452,50 479,52

Total 45.755,90 48.704,70 48.938,80 57.213,70 57.284,2345

Contribution to the consolidated debt

Regional & Local debt

Regional & Local debt (% GDP - 2015)

35,0

Regional Government

30,0

Local Government

25,0

20,0

15,0

10,0

5,0

0,0

Austria Belgium Germany Spain SwitzerlandYou can also read