ISAA Fall School 2021 - October 11, 2021 - Iowa Department of Revenue

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ISAA Fall School 2021

October 11, 2021

MR, Dual Class, & BOR

October 11, 2021

Julie Roisen, Division Administrator

Why are we here? Serve Iowa Taxpayers

We are willing to: • Listen, ask questions and accept that we may not fully understand • Acknowledge what you do well • Recognize your strengths • Hold you accountable • Thank you for your effort • Talk about resolving challenges

HF418

441.21 New subsection 14a Multi-residential classification eliminated effective 2022 assessment • (1) Property for human habitation containing 2 or fewer dwelling units • (6) Parcels primarily used for human habitation containing 3 or more dwelling units

441.21 Subsection 14a & b

• Dual Classification

• (7) Parcel primarily used for commercial or

industrial property

– Any portion used for human habitation is

classed as residential

• (6) 3 or more dwelling units

– Any portion used for commercial or industrial

classed as commercial or industrial441.21 Subsection 14a & c • (2) Mobile home parks • (3) Manufactured home communities • (4) Land-leased communities • (5) Assisted living facilities • (c) Section 42 housing not withdrawn from special valuation procedures continues to be commercial; as do hotels, motels, inns, rented for less than 30 days

MR Rules • Draft rules addressing the elimination of the multiresidential classification and the impact on dual classification have been filed with LSA. Department attorneys are currently working with LSA staff to finalize the rules for the Notice of Intended Action. The rules will be published in the October 20th Iowa Administrative Bulletin with a comment deadline of November 9th and an anticipated effective date of January 19, 2022.

368.8 SMID Districts • Property classed as residential under 441.21 Subsection 14 paragraph “a” subparagraph (6) continue to be subject so SMID district taxes • (property with 3 or more dwelling units)

404.3 • Residential development area exemption • Notwithstanding the schedules provided for in section 404.2, all qualified real estate assessed as residential property, excluding property classed as residential property under section 441.21, subsection 14 paragraph “a”, subparagraph (6) • (3 or more dwelling units)

HF 865

BPTC 4226C

• If a portion of a parcel or property unit allowed a

credit changes ownership only the new owner

must reapply for the credit

• Original owner that retains a portion of a parcel

or unit does not have to reapply for the creditHF 871

441.32 BOR Removal

• Allows for the Director of Revenue to remove

board of review members for:

• Violation of law or administrative rule applicable

to member’s duties

• Failure to comply with an order from the

Director

• Provides for written request for hearing in

regard to removal

• Order removing a member is subject to judicial

reviewBOR Rules • Board of Review removal appeal and hearing rules will be effective on October 27, 2021. You can read the rules here: https://www.legis.iowa.gov/docs/aco/arc/5930C. pdf. • It is likely that the “Duties and Responsibilities of Local Boards of Review” document will be updated, but only to restate the contents of the new legislation and to cite to the rule.

SF 342

9E.7 Subsection 4A

• Upon request by a program participant the

assessor shall redact the requestor’s name

contained in electronic documents that are

displayed for public access through an internet

site. A fee shall not be charged for the

administration of this paragraph

• Victims of assault, domestic abuse, active or

retired judicial officers, federal judges, or their

spouses or children, prosecutors, peace offices

or their spouses or childrenSF 366

441.17 Subsection 2

• Assessor and deputy shall not assess their own

property

• Removal of the language of the assessor’s or

deputy’s immediate familyARC 5887C • 701.71.27(1) and (2) • Removed immediate family of assessor and deputy • Removed reporting requirements and provides for a certification only to be provided to the Director by January 1st of each year

ARC 5885 C Assessor Appointment Appeals • Iowa Code section 17A.17(8) defines the decision maker in a contested case • Ensures that the agency can meet a litigant’s right to procedural due process by providing a fair trial or fair tribunal, while recognizing the agency’s role in technical matters • Can then appeal to district court

IAC 701.71.3(1)

Agricultural Adjustments

• Adjustments to cropland with “high” CSR ratings

defined within this rule

• Only exceptions for adjusting CSR’s outside the

rule: Iowa Manual Land section pages:

2-26 and 2-27

• Special considerations

– Crop land

– Non croplandIowa Laws Course • Iowa Laws being offered in November • Intend to record the course and offer it again within the same month via recording • Bound books with Iowa Laws and IAC are available

2021 Equalization

• Confidence Intervals and Math

Mistake

• Any number divided by it’s %

gives you the whole – IDR Method2021 Equalization

• Focus on Sales Lists

• MR appeals

– Kudos

• Joe Kronin, Ida County

• Mindy Schaefer, Union County

• Dixie Saunders, Van Buren

County2021 Commercial Orders Not Applied Because of Confidence Intervals Count 53 Min -8% Max 19% Median 9% Mean 9% Avg. & Median Revaluation 1% and 2

2023 Equalization Increasing number of jurisdictions using the confidence interval as their guide and not the required 100% found in 441.21 with a 5% tolerance Department is increasing the number of jurisdictions that have appraisals to increase the sample size Will eliminate the use of confidence intervals for 2023

DOV & Equalization

October 11, 2021

Susan Chambers, Executive OfficerEqualization Team Responsibilities

Assessment

Limitations

Equalization

Abstract & Reconciliation

Ag Productivity Model

Declaration of Value/Sales ListScope of Support:

• Review of required reports

– Completeness

– Reconciliation

• Statutory Compliance

– Deadlines

– Actions

Outside of Scope:

Legal interpretation of statute and rule

Determination of applicability of statute and rule

34Housekeeping:

Declaration of Value

Processing

35DOVs – Iowa Code 428A.1 See Iowa Code

428A.2(10) No

DOV No GWH

428A.1 Amount of tax on transfers — declaration of value.

1. a. There is imposed on each deed, instrument, or writing by which any lands, tenements, or other realty in this state are granted, assigned,

transferred, or otherwise conveyed, a tax determined in the following manner:

(1) When there is no consideration or when the deed, instrument, or writing is executed and tendered for recording as an instrument corrective

of title, and so states, there is no tax.

(2) When there is consideration and the actual market value of the real property transferred is in excess of five hundred dollars, the tax is eighty

cents for each five hundred dollars or fractional part of five hundred dollars in excess of five hundred dollars.

b. The term “consideration”, as used in this chapter, means the full amount of the actual sale price of the real property involved, paid or to be

paid, including the amount of an encumbrance or lien on the property, if assumed by the grantee.

c. It is presumed that the sale price so stated includes the value of all personal property transferred as part of the sale unless the dollar value of

personal property is stated on the instrument of conveyance. When the dollar value of the personal property included in the sale is so stated, it

shall be deducted from the consideration shown on the instrument for the purpose of determining the tax.

2. When each deed, instrument, or writing by which any real property in this state is granted, assigned, transferred, or otherwise conveyed is

presented for recording to the county recorder, a declaration of value signed by at least one of the sellers or one of the buyers or their agents

shall be submitted to the county recorder. However, if the deed, instrument, or writing contains multiple parcels some of which are located in

more than one county, separate declarations of value shall be submitted on the parcels located in each county and submitted to the county

recorder of that county when paying the tax as provided in section 428A.5. A declaration of value is not required for those instruments described

in section 428A.2, subsections 2 to 5, 7 to 13, and 16 to 21, or described in section 428A.2, subsection 6, except in the case of a federal agency

or instrumentality, or if a transfer is the result of acquisition of lands, whether by contract or condemnation, for public purposes through an

exercise of the power of eminent domain.

3. The declaration of value shall state the full consideration paid for the real property transferred. If agricultural land, as defined in section 9H.1,

is purchased by a corporation, limited partnership, trust, alien or nonresident alien, the declaration of value shall include the name and address

of the buyer, the name and address of the seller, a legal description of the agricultural land, and identify the buyer as a corporation, limited

partnership, trust, alien, or nonresident alien. The county recorder shall not record the declaration of value, but shall enter on the declaration of

value information the director of revenue requires for the production of the sales/assessment ratio study and transmit all declarations of value to

the city or county assessor in whose jurisdiction the property is located. The city or county assessor shall provide the information the director of

revenue requires for the production of the sales/assessment ratio study at times as directed by the director of revenue. The assessor shall retain

for three years from December 31 of the year in which the transfer of realty for which the declaration was filed took place. The director of

revenue shall, upon receipt of the information required to be filed under this chapter by the city or county assessor, send to the office of the

secretary of state that part of the declaration of value which identifies a corporation, limited partnership, trust, alien, or nonresident alien as a

purchaser of agricultural land as defined in section 9H.1.Iowa Administrative Code 701 71.10(2) Responsibility of recorders and assessors. County recorders and city and county assessors shall complete the prescribed forms as required by Iowa Code subsection 421.17(6) and rule 701—79.3(428A) in accordance with instructions issued by the department. Assessed values entered on the prescribed form shall be those established as of January 1 of the year in which the sale takes place. (Instrument Date is the date that the parties entered into their agreement, the “sale date” – not the recording date.) 71.10(3) Normal sales. All real estate transfers shall be considered by the department of revenue to be normal sales unless there exists definite information which would indicate the transfer was not an arms-length transaction or is of an excludable nature as provided in Iowa Code section 441.21. This rule is intended to implement Iowa Code section 421.17. 79.3(3) Transmittal of forms. Real estate transfer-declaration of value forms filed with the county recorder shall be transmitted promptly to the department. Nothing in this subrule shall be construed to relieve, limit, or prohibit city and county assessors from completing the requirements set forth in Iowa Code sections 421.17(6)“a” and 421.17(6)“b.”

Sales Condition Codes

2 - Sale to/by Government/Exempt Organization

(see 482A.2(6) – there will be no transfer tax for a

political subdivision sale) (there will be tax for an

exempt organization.)

Being not-for-profit is not the same as “exempt”. Do they pay property

tax?

There will be tax when the Seller is not a government entity

(political subdivision).

Exempt properties have an assessed value.16 – Improvements or demolition after January 1 of

the year of the sale but prior to actual date of sale

(Fire or flood damage must occur after January 1 but prior to the sale date.)

A copy of the assessment notice in the next assessment

year is required to use this NUTC to exclude the sale from

use in equalization. *other options – digital list of parcels

with assessment notice.

25 – Partial Assessment

(New construction or incomplete structural changes as of

January 1) This does not include replacement or update of

existing improvements. Do not use this for a vacant lot sale

– use NUTC 3450 – Other (With explanation; documentation of the date, time and who was contacted and who in the assessor’s office made the contact is required.) If there is another NUTC that applies, use that NUTC. If you had the opportunity to revalue the property then it is “normal”. See NUTC 16 or 25.

DOV Application New Release Information

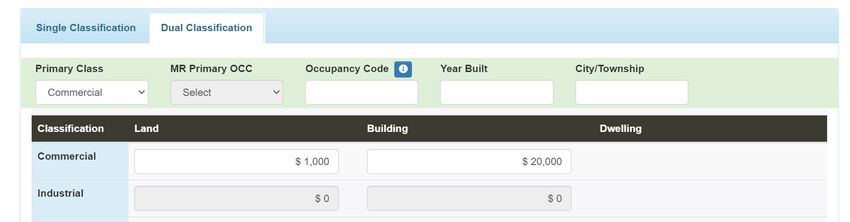

Dual Classification - entering values Select the secondary classification first to populate the assessed values on the Dual Classification tab. Select the primary classification – this will set the primary classification for equalization. Dual Class primarily commercial properties are used for commercial equalization. Primarily residential dual class properties will be used for equalization as residential.

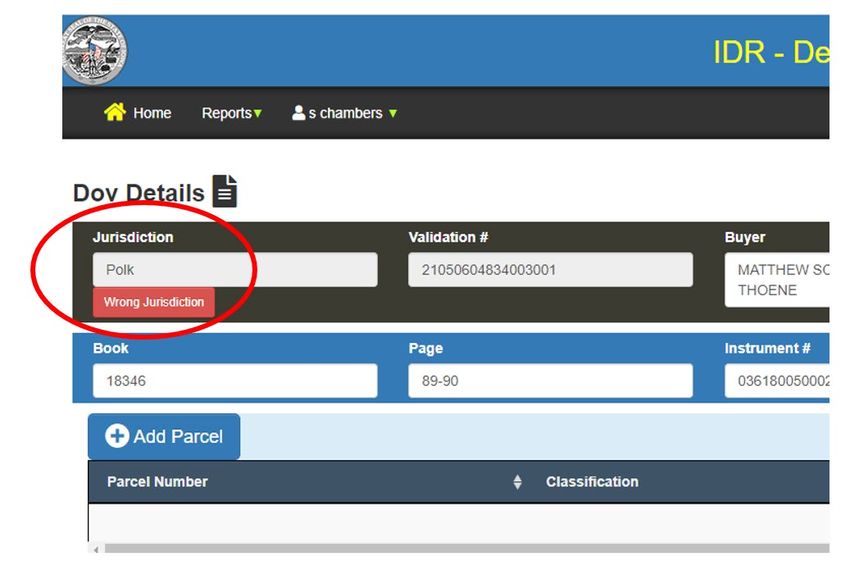

This doesn’t appear to be my DOV – one

click solution.

Open the record (right-click and select “open in

new tab”. Select “Wrong Jurisdiction” button.What Comes Next for DOV?

• 2022 version without multiresidential

– Run tandem with 2021 version

• Reporting and process improvements to improve data

quality

• Accountability measures

• Integration of Abstract & Reconciliation, Equalization

Worksheets and Assessment Limitations

44DEPARTMENT OF REVENUE CONTACTS

Susan Chambers (515) 474-4002

Susan.chambers@iowa.gov

Carmen Putzier (515) 661-7282

carmen.putzier@iowa.gov

Trisha Jones (515) 805-7244

trisha.jones@iowa.gov

Jeni Lara (515) 661-7942

Jenifer.Lara@iowa.govSolar Energy Property

October 11, 2021

Roland Simmons, AppraiserSolar Energy Property

• Replacement Tax Solar

• Solar energy conversion facilities where the acquisition

cost of all interests exceed one million dollars.

• 476C.1(14) “Solar energy conversion facility” means a

solar energy facility in this state that collects and

converts incident solar radiation into energy to generate

electricity.

– Legislative change effective July 1, 2021

– Major addition for existing utility companies

– Tax neutrality

– Not previously subject to the replacement tax

48Solar Energy Property

• Potential Tax Imposition

– Generation Tax six hundredths of a cent (.0006) per

kilowatt-hour (437A.6)

– Electric Delivery Tax

• Delivery tax rates by service area (437A.4)

• Deliveries to a consumer/end user within the state (437A.3)

– Transmission Line Tax

• Determined by the size of the line (437A.7)

• Number of line miles

49Solar Energy Property

• Statewide Property Tax

– Annual $.03 cents per thousand dollars of assessed value

(437A.18)

– Assessed value determination

• Acquisition cost of all operation property

• Property that is owned or leased

• Including leased land

– Statewide Property Tax Proceed

• General Fund Deposit (437A.23)

50Solar Energy Property

• Local vs Replacement Tax?

– Assessor will determine if the property should be

locally assessed (441.21)

– What you need to know as you investigate

• Self-generator (437A.23)

• Who’s consuming the electricity

• Sold to a consumer

• Sold to a utility company

• Inadvertent and unscheduled deliveries to the grid

– Who owns the property

51Solar Energy Property

– Date of service

– Valuation Date

– Solar and land

– Property unrelated to Solar

52Solar Energy Property

• Replacement Tax Property

– Generation, Transmission and Deliveries

– Total replacement tax for property

• Tax allocation

• All replacement tax dollars are allocated among local taxing districts in

accordance with the general allocation formula determined by the

Department of Management

• Tax dollars received from the replacement tax are billed and collected in

the same manner as residential or commercial property taxesDEPARTMENT OF REVENUE CONTACTS

Roland Simmons (515) 661-7315

Roland.Simmons@iowa.gov

Ksenia Gardino (515) 661-7715

Ksenia.Gardino@iowa.gov

Mark Berkenpas (515) 661-7027

Mark.Berkenpas@iowa.govTelecommunications

October 11, 2021

Mark Berkenpas, AppraiserTelecommunications

• IDR values the entire operating property of a telephone

company

– Operating property - all property owned or leased to a utility

company that is necessary to perform the activities for which

the utility is formed

– 222 telephone companies

• How is this done?

– Annual utility report filings (confidential)

• Financials, Plant Detail, Income Statements

57Telecommunications

• Senate File 2388 changed everything

– Phased-out transmission equipment of telecommunications

companies not subject to IA Code chapter 433

• At 75% (AY19), 50% (AY20), 30% (AY21) of the transmission property’s

actual value

• For AY22 and each subsequent assessment year, transmission property

shall not be assessed and taxed as real property

58Telecommunications

• SF2388

– Phased-in an additional exemption of telephone property under

IA Code chapter 433

• 25% (AY19), 50% (AY20), 70% (AY21)

• Future Assessment Years

– For AY22 and after, telephone and telegraph company property

shall be assessed by local assessors

– In the same manner and on the same basis as other

commercial property located in the assessing jurisdiction where

situated

59Telecommunications

• HOW to accomplish the task?

– Identify, locate, and inventory

– Cross-check with the county auditor’s public utility lists and plat

maps

• IDR certifies assessments to the auditor

• Telephone company value is allocated by line miles

– IDR has contact information

– IDR does NOT have:

• Building locations, sizes, construction detail

• Land sizes, plat maps

60DEPARTMENT OF REVENUE CONTACTS

Mark Berkenpas (515) 661-7027

Mark.Berkenpas@iowa.gov

Roland Simmons (515) 661-7315

Roland.Simmons@iowa.govThank you

You can also read