Issues Paper on Climate Change Risks to the Insurance Sector - July 2018 Issues Paper on Climate Change Risks to the Insurance Sector - UNEP FI

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Issues Paper on Climate Change Risks

to the Insurance Sector

July 2018

Issues Paper on Climate Change Risks to the Insurance Sector

About the Sustainable Insurance Forum (SIF) The Sustainable Insurance Forum (SIF) is a network of leading insurance supervisors and regulators working together to strengthen their understanding of, and responses to sustainability issues for the business of insurance. Launched in December 2016, the SIF serves as a global platform for international collaboration by insurance regulators and supervisors on sustainability issues. The SIF is convened by UN Environment. More information on the SIF is available at: www.sustainableinsuranceforum.org. About the IAIS The International Association of Insurance Supervisors (IAIS) is a voluntary membership organisation of insurance supervisors and regulators from more than 200 jurisdictions. The mission of the IAIS is to promote effective and globally consistent supervision of the insurance industry in order to develop and maintain fair, safe and stable insurance markets for the benefit and protection of policyholders and to contribute to global financial stability. Established in 1994, the IAIS is the international standard setting body responsible for developing principles, standards and other supporting material for the supervision of the insurance sector and assisting in their implementation. The IAIS also provides a forum for Members to share their experiences and understanding of insurance supervision and insurance markets. The IAIS coordinates its work with other international financial policymakers and associations of supervisors or regulators, and assists in shaping financial systems globally. In particular, the IAIS is a member of the Financial Stability Board (FSB), member of the Standards Advisory Council of the International Accounting Standards Board (IASB), and partner in the Access to Insurance Initiative (A2ii). In recognition of its collective expertise, the IAIS also is routinely called upon by the G20 leaders and other international standard setting bodies for input on insurance issues as well as on issues related to the regulation and supervision of the global financial sector. Issue Papers provide background on particular topics, describe current practices, actual examples or case studies pertaining to a particular topic and/or identify related regulatory and supervisory issues and challenges. Issues Papers are primarily descriptive and not meant to create expectations on how supervisors should implement supervisory material. Issues Papers often form part of the preparatory work for developing standards and may contain recommendations for future work by the IAIS. Issues Paper on Climate Change Risks to the Insurance Sector Approved by the IAIS Executive Committee and the Sustainable Insurance Forum on 25 July 2018 Page 2 of 81

International Association of Insurance Supervisors c/o Bank for International Settlements CH-4002 Basel Switzerland Tel: +41 61 280 8090 Fax: +41 61 280 9151 www.iaisweb.org This document is available on the IAIS website (www.iaisweb.org). © International Association of Insurance Supervisors (IAIS), 2018. All rights reserved. Brief excerpts may be reproduced or translated provided the source is stated. Issues Paper on Climate Change Risks to the Insurance Sector Approved by the IAIS Executive Committee and the Sustainable Insurance Forum on 25 July 2018 Page 3 of 81

Contents

Acronyms .............................................................................................................................. 7

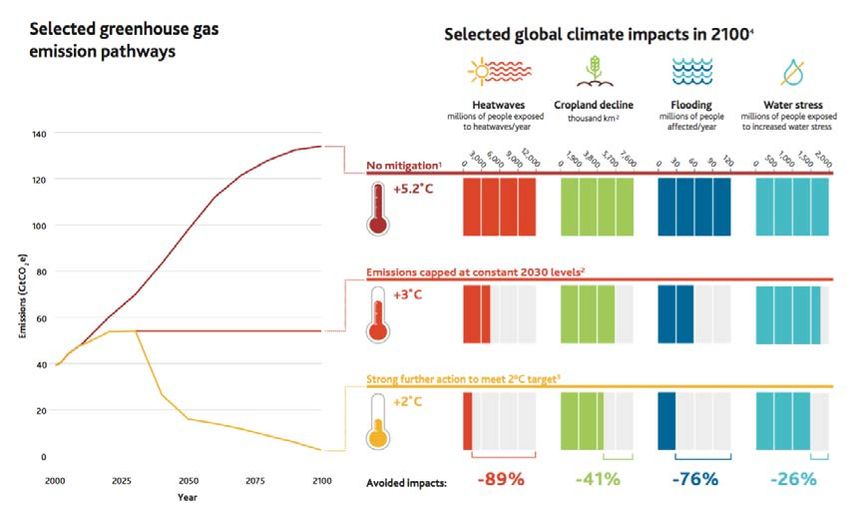

1 Introduction .................................................................................................................... 9

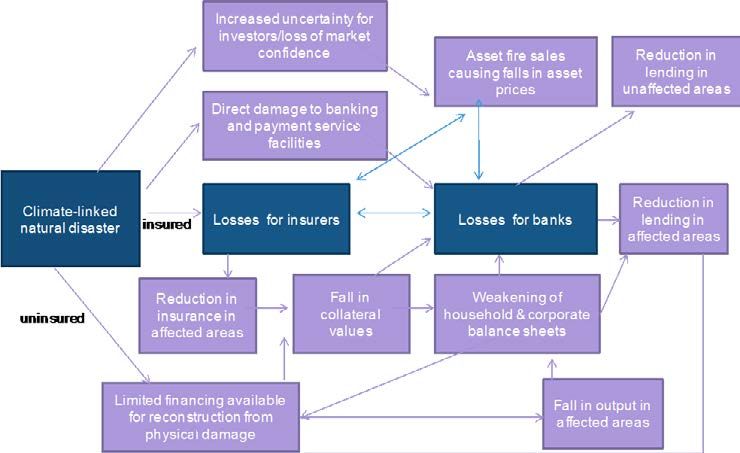

2 The Climate Risk Landscape ....................................................................................... 11

2.1 Examples of Climate Impacts ................................................................................ 11

3 How Climate Change may affect the Insurance Sector ................................................ 14

3.1 Understanding Climate Risks ................................................................................ 14

3.2 Examples of Climate Risks across Insurance Business, Strategy, and Operations 17

3.2.1 Underwriting Activities.................................................................................... 18

3.2.2 Investment Activities ...................................................................................... 20

4 Industry responses to climate risks .............................................................................. 22

4.1 Observed industry practices.................................................................................. 22

4.2 Strategies for climate resilience ............................................................................ 23

5 Relevance for Insurance Supervisors........................................................................... 25

6 Applicability of Insurance Core Principles to Climate Change ...................................... 29

6.1 ICPs of relevance to climate change risks............................................................. 29

7 Supervisory Approaches to Climate Change Risks ...................................................... 36

7.1 Assessing Climate Change as an Emerging Risk ................................................. 36

7.1.1 Mandates and Objectives .............................................................................. 36

7.1.2 Initial Assessment .......................................................................................... 37

7.1.3 Signalling Expectations .................................................................................. 37

7.2 Responding to Climate Change risks through Supervisory Practice ...................... 37

7.2.1 Risk Frameworks ........................................................................................... 37

7.2.2 Information and Data gathering ...................................................................... 38

7.2.3 Engagement strategies and Examination Tools ............................................. 38

7.2.4 Examining current exposures: Stress Testing & Exposure Assessment ......... 39

7.2.5 Exploring future risk: Scenario Analysis & Alignment ..................................... 41

7.3 Collaboration and Cooperation.............................................................................. 42

7.3.1 Convening ..................................................................................................... 42

7.3.2 Engagement with other public authorities....................................................... 43

7.3.3 International Engagement .............................................................................. 43

8 Observed Practices: Case Studies ............................................................................... 44

8.1 Australia: Australian Prudential Regulation Authority ............................................ 44

8.1.1 Motivation and Rationale ............................................................................... 44

Issues Paper on Climate Change Risks to the Insurance Sector

Approved by the IAIS Executive Committee and the Sustainable Insurance Forum on 25 July 2018 Page 4 of 818.1.2 Approach and Methodology ........................................................................... 45

8.1.3 Key Findings .................................................................................................. 45

8.1.4 Lessons: Key Challenges and areas for improvement ................................... 45

8.1.5 Impacts on Supervisory Practice .................................................................... 46

8.1.6 Next Steps ..................................................................................................... 46

8.2 Brazil: Superintendência de Seguros Privados (SUSEP) ...................................... 47

8.2.1 Motivation and rationale ................................................................................. 47

8.2.2 Approach(es) and Methodology(ies) .............................................................. 47

8.2.3 Key Findings .................................................................................................. 47

8.2.4 Lessons: Key challenges, areas for improvement .......................................... 48

8.2.5 Impacts on supervisory practice ..................................................................... 48

8.2.6 Next steps...................................................................................................... 48

8.3 France: Autorité de Contrôle Prudentiel et de Résolution (ACPR)......................... 48

8.3.1 Motivation and Rationale ............................................................................... 48

8.3.2 Approach and Methodology ........................................................................... 49

8.3.3 Key Findings .................................................................................................. 50

8.3.4 Lessons: Key Challenges and areas for improvement ................................... 51

8.3.5 Impacts on Supervisory Practice .................................................................... 52

8.3.6 Next Steps ..................................................................................................... 53

8.4 Italy: Istituto per la Vigilanza Sulle Assicurazioni (IVASS) ..................................... 53

8.4.1 Approach and Methodology ........................................................................... 53

8.4.2 Key Findings .................................................................................................. 53

8.4.3 Lessons: Key Challenges and Areas for Improvement ................................... 53

8.4.4 Next Steps ..................................................................................................... 54

8.5 Netherlands: De Nederlandsche Bank (DNB) ....................................................... 54

8.5.1 Motivation and Rationale ............................................................................... 54

8.5.2 Approach and Methodology ........................................................................... 54

8.5.3 Key Findings .................................................................................................. 56

8.5.4 Lessons: Key Challenges and areas for improvement ................................... 57

8.5.5 Impacts on Supervisory Practice .................................................................... 58

8.5.6 Next Steps ..................................................................................................... 58

8.6 Sweden: Finansinspektionen ................................................................................ 58

8.6.1 Motivation and Rationale ............................................................................... 58

8.6.2 Approach and Methodology ........................................................................... 59

Issues Paper on Climate Change Risks to the Insurance Sector

Approved by the IAIS Executive Committee and the Sustainable Insurance Forum on 25 July 2018 Page 5 of 818.6.3 Key Findings .................................................................................................. 59

8.6.4 Lessons: Key Challenges and Areas for Improvement ................................... 60

8.6.5 Impacts on Supervisory Practice .................................................................... 60

8.6.6 Next Steps ..................................................................................................... 60

8.7 UK: Bank of England Prudential Regulation Authority ........................................... 60

8.7.1 Motivation and Rationale ............................................................................... 60

8.7.2 Approach and Methodology ........................................................................... 61

8.7.3 Key Findings .................................................................................................. 62

8.7.4 Lessons: Key Challenges and areas for improvement ................................... 62

8.7.5 Impacts on Supervisory Practice .................................................................... 62

8.7.6 Next Steps ..................................................................................................... 63

8.8 USA: National Association of Insurance Commissioners (NAIC) ........................... 63

8.8.1 Motivation and Rationale ............................................................................... 63

8.8.2 Approach and Methodology ........................................................................... 64

8.8.3 Key Findings .................................................................................................. 64

8.8.4 Lessons: Key Challenges and areas for improvement ................................... 64

8.8.5 Impacts on Supervisory Practice .................................................................... 64

8.8.6 Next Steps ..................................................................................................... 65

8.9 USA – California: California Department of Insurance........................................... 65

8.9.1 Motivation and Rationale ............................................................................... 65

8.9.2 Approach and Methodology ........................................................................... 65

8.9.3 Key Findings .................................................................................................. 66

8.9.4 Lessons: Key Challenges and areas for improvement ................................... 67

8.9.5 Impacts on Supervisory Practice .................................................................... 67

8.9.6 Next Steps ..................................................................................................... 68

8.10 USA - Washington State: Office of the Insurance Commissioner (OIC)................. 68

8.10.1 Motivation and Rationale ............................................................................... 68

8.10.2 Approach and Methodology ........................................................................... 68

8.10.3 Key Findings .................................................................................................. 69

8.10.4 Lessons: Key Challenges and areas for improvement ................................... 69

8.10.5 Impacts on Supervisory Practice .................................................................... 70

8.10.6 Next Steps ..................................................................................................... 70

9 Conclusions ................................................................................................................. 71

Annex: Recommendations of the FSB TCFD ...................................................................... 73

Issues Paper on Climate Change Risks to the Insurance Sector

Approved by the IAIS Executive Committee and the Sustainable Insurance Forum on 25 July 2018 Page 6 of 81Acronyms ACAPS Autorité de Contrôle des Assurances et de la Prévoyance Sociale (Morocco) ACPR Autorité de Contrôle Prudentiel et de Résolution (France) ASSAL Asociación de Supervisores de Seguros de América Latina APRA Australian Prudential Regulation Authority BIS Bank for International Settlements BNDES Brazilian Development Bank BoE Bank of England CDI California Department of Insurance CVM Brazilian Securities Commission COP Conference of the Parties CRCI Climate Risk Carbon Initiative DEFRA Department for Environment, Food and Rural Affairs (UK) DNB De Nederlandsche Bank (Netherlands) ERM Enterprise Risk Management ESG Environment, Social and Governance FI Finansinspektionen (Sweden) FSB Financial Stability Board GFSG Green Finance Study Group GHG Greenhouse Gas IAIS International Association of Insurance Supervisors ICP Insurance Core Principle IADB Inter-American Development Bank IMF International Monetary Fund IPCC Intergovernmental Panel on Climate Change IVASS Istituto per la Vigilanza Sulle Assicurazioni (Italy) NAIC National Association of Insurance Commissioners (US) OIC Washington State Office of the Insurance Commissioner ORSA Own Risk Solvency Assessment OSFI Office of the Superintendent of Financial Institutions (Canada) PPM Parts Per Million PPP Public-Private Partnerships Issues Paper on Climate Change Risks to the Insurance Sector Approved by the IAIS Executive Committee and the Sustainable Insurance Forum on 25 July 2018 Page 7 of 81

PRA Bank of England Prudential Regulation Authority PSI Principles for Sustainable Insurance SIF Sustainable Insurance Forum SME Small and medium enterprises SUSEP Superintendência de Seguros Privados (Brazil) TCFD Task Force on Climate-related Financial Disclosures UNFCCC United Nations Framework Convention on Climate Change Issues Paper on Climate Change Risks to the Insurance Sector Approved by the IAIS Executive Committee and the Sustainable Insurance Forum on 25 July 2018 Page 8 of 81

1 Introduction

1. Climate change – the warming of the world’s climate system, including its atmosphere,

oceans, and land surfaces – is advancing around the world. Climate change is recognised by

the world’s governments, the private sector, and civil society as a top global threat, which is

having impacts today on human, environmental, and economic systems – including, for

instance, through an increasing frequency and severity of natural catastrophes and extreme

weather events. Society’s responses to climate change – including new policies, market

dynamics, technological innovation, and social change – may have wide-ranging impacts on

the structure and function of the global economy.

2. In recent years, there has been increasing recognition at the international level that

climate change will also affect the financial system, including insurers.

• In 2015, the world’s governments signed the Paris Agreement on Climate Change at

the 21st Conference of the Parties (COP) of the United Nations Framework Convention

on Climate Change (UNFCCC), which sets the pathway for the reductions of

Greenhouse Gas (GHG) emissions to limit climate change to two degrees of warming

by the end of the century. Article 2.1(c) of the Paris Agreement specifically sets out a

goal of “making finance flows consistent with a pathway towards low greenhouse gas

emissions and climate-resilient development.” 1 Since 2015, several new initiatives

have been launched to harness the expertise of the insurance industry to address

climate challenges.

• In 2015, following a request from G20 Finance Ministers, the Financial Stability Board

(FSB) launched an industry-led Task Force on Climate-related Financial Disclosures

(TCFD). The TCFD released its final recommendations in June 2017, setting a

coherent framework for the identification, assessment, management and disclosure of

climate risks and opportunities across sectors, with specific guidance for application

by financial institutions – including insurers as both underwriters and asset owners.

• In 2016, under its G20 Presidency, China established the Green Finance Study Group

(GFSG) to develop options on how to enhance the ability of the financial system to

mobilise private capital for green investment. 2 At the 2016 Hangzhou Summit, G20

heads of state for the first time recognised the need to “scale up green finance” and

endorsed a set of options to achieve this goal—with information elements, such as

product standards, established as a core aspect of frameworks to promote the

development of markets for green assets (such as green bonds).

• In 2017, under the German G20 Presidency, the GFSG concentrated its efforts on the

information agenda with two specific research tracks on Environmental Risk

Assessment and Data.

• In March, 2018, the European Commission presented its Action Plan on Sustainable

Finance, 3 underlining the importance of involving the finance industry in addressing

climate change and specifically involving both the European supervisory authority for

insurance EIOPA as well as national supervisors in follow up actions.

3. Since 2015, an increasing number of governments, central banks, regulators and

financial sector stakeholders are working to drive climate risks and other sustainability factors

into the core of the financial system function, through different measures and actions. 4,5, 6

Action on climate change is also a core aspect of many national-level policy processes relating

to sustainable finance. Several countries, including Argentina, China, Indonesia, Italy,

Issues Paper on Climate Change Risks to the Insurance Sector

Approved by the IAIS Executive Committee and the Sustainable Insurance Forum on 25 July 2018 Page 9 of 81Mongolia, Morocco, Nigeria, Singapore, South Africa, and most recently Canada, have

undertaken or initiated strategic policy processes and roadmaps for sustainable finance, with

climate risks often a central priority. 7

4. These and other developments have prompted insurance supervisors to begin

examining the relevance of climate change for insurance supervision, both individually and

collaboratively through the Sustainable Insurance Forum (SIF).

5. The SIF was launched in December 2016 as a global platform for international

collaboration by insurance regulators and supervisors on sustainability issues, with a special

focus on climate change. 8 During 2017, the SIF undertook several joint activities relating to

climate risks, including:

• Delivery of a coordinated submission to the TCFD consultation, followed by the release

of a joint statement in July 2017 supporting the recommendations and highlighting how

supervisors can support uptake. 9

• A survey of supervisors to share knowledge and compare experience from their efforts

to address climate risks. The survey covers activities across firm-level supervision and

system-level stress testing, examining approaches, methodologies, data inputs, key

challenges, impacts on practice, and next steps.

• High-level policy engagement with the IAIS on climate risk issues, setting the

groundwork for collaboration with the Executive Committee and IAIS Secretariat into

2018.

6. At the second meeting of the SIF in July 2017, members requested the SIF Secretariat

to develop a guidance document on climate change and insurance supervision. At the third

meeting of the SIF, held alongside the IAIS annual meetings and conference in Kuala Lumpur,

Malaysia, the SIF and the IAIS agreed to advance this document jointly as an Issues Paper.

7. The objectives of this Issues Paper are to raise awareness for insurers and supervisors

of the challenges presented by climate change, including current and contemplated

supervisory approaches for addressing these risks.

8. As an Issues Paper, it provides an overview of how climate change is currently

affecting and may affect the insurance sector now and in the future, provides examples of

current material risks and impacts across underwriting and investment activities, and

describes how these risks and impacts may be of relevance for the supervision and regulation

of the sector. It explores potential and contemplated supervisory responses, and reviews

observed practices in different jurisdictions. In doing so, it identifies gaps and emerging areas

which need to be resolved to allow for effective supervision. Finally, the paper offers

preliminary insights from practice, and initial conclusions relating to the supervision of climate

change risks to the insurance sector.

9. The Paper is intended to be primarily descriptive and is not meant to create supervisory

expectations. Nevertheless, the Paper may shed light on the need for additional, more specific

joint material from the IAIS and the SIF to support supervisors in their efforts to better

understand and address climate change risks.

Issues Paper on Climate Change Risks to the Insurance Sector

Approved by the IAIS Executive Committee and the Sustainable Insurance Forum on 25 July 2018 Page 10 of 812 The Climate Risk Landscape

10. Warming of the climate system is unequivocal, with recent climate changes causing

widespread impacts on human and natural systems. 10 The scientific link between increasing

carbon emissions and warming temperatures is irrefutable. The Intergovernmental Panel on

Climate Change (IPCC) has declared that human influence on the climate system is clear, and

recent anthropogenic emissions of greenhouse gases have driven atmospheric

concentrations to their highest levels in human history: 11

• Concentrations of CO2 have increased by over 40% from approximately 280PPM to

over 400PPM since the preindustrial period, accompanied by an approx.1-degree

Celsius rise in global annual mean temperature. 12

• Over the last decade, most emissions have come from energy, industry, and transport

sectors, with other major emitting sectors including agriculture and land use. 13

• While some evidence suggests that global emissions growth has plateaued since

2014, 2016 was the first full year in which atmospheric CO2 concentration stayed

above the 400PPM milestone. 14,15

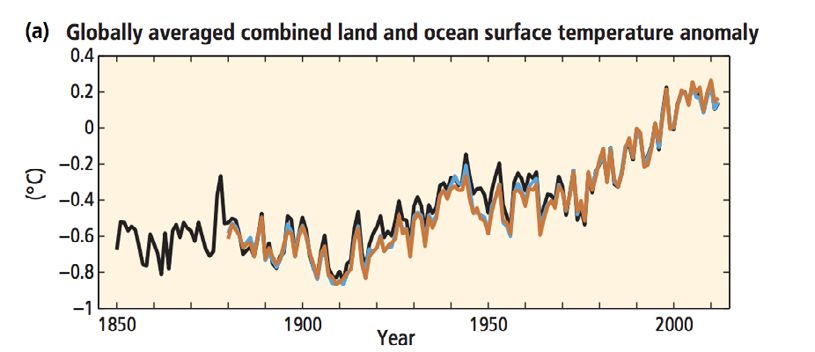

11. Each of the last three decades have been successively warmer at the Earth’s surface

than any preceding decade since 1850 (Figure 1). Most warming has occurred in the past 35

years, with 16 of the 17 warmest years on record occurring since 2001. 16 2017 was the second

warmest year on record since 1880, and the warmest without an El Nino event. 17

Figure 1: Tracking Global Warming, 1850-2014

Source: IPCC AR5 SPM 2014

2.1 Examples of Climate Impacts

12. Climate change is having widespread effects on environmental systems, and

exacerbating negative impacts upon stocks and flows of natural capital, upon which society

and the economy rely. Key indicators of this shift include:

• Natural Catastrophes and Extreme Weather Events: As documented by the IPCC,

there is strong scientific evidence to suggest that climate change is having an influence

on the frequency, severity, and distribution of natural catastrophes and extreme

Issues Paper on Climate Change Risks to the Insurance Sector

Approved by the IAIS Executive Committee and the Sustainable Insurance Forum on 25 July 2018 Page 11 of 81weather events. In recent years, several notable studies have explored this question

in detail:

o Research by the World Meteorological Organization has concluded that 80%

of natural disasters between 2005 and 2015 were in some way climate-

related; 18

o A recent meta-analysis of 59 studies in English-language scientific journals

published between 2016-2017 found that 70% of studies concluded that

climate change has increased the risk of a given extreme event, such as heat,

drought, rainfall, wildfires, and storms; 19

o Analysis by MunichRe has identified a long-term trend in an increase in the

number of natural catastrophes around the globe, predominantly attributable to

weather-related events like storms and floods. 20 As there has been no relevant

increase in geophysical events such as earthquakes, tsunamis, and volcanic

eruptions, there is some justification in assuming that changes in the

atmosphere, and global warming in particular, play a relevant role.

• There is debate within the scientific community on the possibility to accurately attribute

specific natural catastrophe events to climate change. Certain types of events – such

as extreme heat, flooding, or wildfire – can be more clearly linked with increased

temperatures, as confirmed by the IPCC. 21 There is some evidence to suggest that the

probability of very high impact events, such as tropical cyclones, is closely correlated

with temperature increases – with one recent study estimating that the proportion of

Category 4 and 5 hurricanes has increased at a rate of approx. 25–30 % per °C of

global warming. 22 Similarly, there is evidence that major cyclones are migrating

“polewards” into increasingly densely populated areas (ie New York City) as a result

of climate change. 23 However, there is still a high degree of uncertainty regarding the

current and future impacts of climate change of specific natural perils in specific

geographic areas. While scientifically-durable methods to attribute the impact of

climate change on natural disasters are increasing in sophistication, 24 multiple

methodological and data issues remain. 25 Nonetheless, there is a broad understanding

that climate trends are likely to on balance result in more frequent natural disasters –

which has been recognised as a critical threat to economic growth by major institutions

such as the International Monetary Fund (IMF). 26

• Sea Level Rise: Recent sea level rise projections range from 0.2 meters to 2.0 meters

by 2100. 27 Arctic sea ice is now declining at a rate of 13.3 percent per decade, with the

last 10 years consecutively representing the lowest 10 average September ice extents

since 1979. 28 Although only 2 percent of the world’s land lies at or below 10 meters of

elevation, these areas contain 10 percent of the world’s human population – meaning

that over 630 million people are directly threatened by sea level rise. 29 The impacts

are already being felt: roughly 20cm of sea-level rise since the 1950s increased

Superstorm Sandy’s ground-up surge losses by 30% in New York alone, contributing

to tens of billions of US dollars in damage. 30

• Biodiversity: Climate change is exacerbating negative trends on terrestrial and

marine biodiversity. Under current trends, climate change could threaten up to 1 in 6

species with extinction. 31,32 This is especially problematic where high biodiversity value

Issues Paper on Climate Change Risks to the Insurance Sector

Approved by the IAIS Executive Committee and the Sustainable Insurance Forum on 25 July 2018 Page 12 of 81supports economic activity, such as tourism. A recent study estimates that climate

change may result in 99% of the world's reefs experiencing annual bleaching in 2043. 33

• Displacement: Since 2008, an average of 26.4 million people have been displaced

from their homes by natural disasters – equivalent to one person every second. 34 2016

saw 24.2 million new displacements due to natural disasters, primarily storms and

extreme weather events. 35

• Communicable disease: Temperature rises (associated with current rates of carbon

emission) of just 2–3 degrees Celsius could increase the number of people who are

vulnerable to malaria by up to 5%, representing several hundred million people. 36

13. Going forward, climate change is set to pose mounting human and environmental costs

by the end of the century – even under scenarios reflecting mitigation and adaptation efforts

(Figure 2). Critically, exposure to climate risks is being predominately driven by individual and

collective social choices, which are putting people and assets in harm’s way. Analysis by

supervisors in Australia suggests that population expansion and urban development trends in

high-risk areas “almost guarantees” that the cost of climate-related natural catastrophe events

and associated claims will keep rising, irrespective of other factors. 37

Figure 2: Emissions Scenarios and Climate Impacts in 2100

Source: Bank of England, 2017, based on analysis by the UK Met Office and AVOID2 programme

Issues Paper on Climate Change Risks to the Insurance Sector

Approved by the IAIS Executive Committee and the Sustainable Insurance Forum on 25 July 2018 Page 13 of 813 How Climate Change may affect the Insurance Sector

3.1 Understanding Climate Risks

14. Climate factors affecting insurers can be grouped into two main categories of risks:

• Physical risks, arising from increased damage and losses from physical phenomena

associated with both climate trends (ie changing weather patterns, sea level rise) and

events (ie natural disasters, extreme weather). It is important to recognise that insurers

may be well-versed in understanding the dynamics of such extreme events, and may

able to adjust exposures through annual contract re-pricing. However, the potential for

physical climate risks may change in non-linear ways, such as a coincidence of

previous un-correlated events, resulting in unexpectedly high claims burdens. Insured

losses from climate-related natural catastrophes reached record levels in 2017 (Box

1). Beyond insured losses from physical climate damages, climate trends and shocks

can pose economic disruptions affecting insurers, the economy, and the wider financial

system. The insurance “protection gap” for weather related losses remains significant,

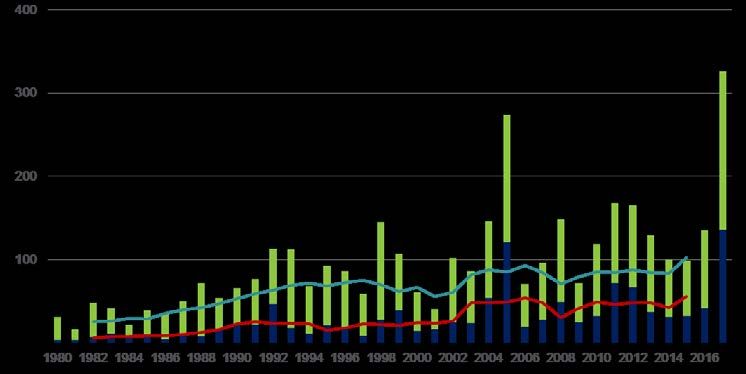

with roughly 70% of losses uninsured (Figure 3) – resulting in significant burden on

households, businesses, and governments. At the macro-economic level, uninsured

losses from physical risks may affect resource availability and economic productivity

across sectors, the profitability of firms and individual assets, pose supply chain

disruptions, and ultimately impact insurance market demand. Uninsured losses arising

from physical risks may have cascading impacts across the financial system, including

on investment companies and banks. 38 Similarly, the availability of insurance – or risk

of uninsurability due to high physical risk profiles – may have significant impacts on

the performance of credit and investment across the economy (including, for instance,

mortgage lending). 39

Figure 3: The Insurance Protection Gap for Weather-related losses

US$ bn

Uninsured losses

(in 2017 values)

Insured losses

(in 2017 values)

5-year moving average

uninsured losses

(in 2017 values)

5-year moving average

insured losses

(in 2017 values)

Inflation adjusted via

country-specific consumer

price index and

consideration of exchange

rate fluctuations between

local currency and US$.

Source: MunichRe NatCatSERVICE, 2018

Issues Paper on Climate Change Risks to the Insurance Sector

Approved by the IAIS Executive Committee and the Sustainable Insurance Forum on 25 July 2018 Page 14 of 81Box 1: The cost of natural disasters

Total global economic losses from natural disasters between 2005-2015 were more than

US$1.3trn, with total direct losses in the range of US$2.5trn since 2000. The series of

major hurricanes and other natural disasters in 2017 made it the year of highest insured

losses ever, at US$138bn. 40 Overall economic losses from natural disasters in 2017

amounted to US$340bn – the second highest annual figure ever. 83% of the losses were

concentrated in North America – with US losses amounting for roughly 50%. 41 According

to Aon Benfield, the total economic losses from hurricanes in 2017 were nearly five times

the average of the preceding 16 years, losses from wildfire were four-times higher, and

losses from other severe storms were 60% higher. 42 In California, insured losses from

wildfires reached US$13bn, 43 stemming from damage to 21,000 homes and 2,800

businesses. 44

• Transition risks, arising from disruptions and shifts associated with the transition to a

low-carbon economy, which may affect the value of assets or the costs of doing

business for firms. Transition risks may be motivated by policy changes, market

dynamics, technological innovation, or reputational factors. Key examples of transition

risks that have been recognised by public authorities and central banks include policy

changes and regulatory reforms which affect carbon-intensive sectors, including

energy, transport, and industry. Policy and regulatory measures may affect specific

classes of financial assets relevant for insurer investment (such as real estate

portfolios), in addition to those affecting capital markets as a whole (see section 3.2.2

below). Social movements and civil society activism – such as that aiming to motivate

divestment from and cessation of underwriting to the coal sector – may pose a risk of

reputational damage to firms, if appropriate risk mitigation strategies (and

communication actions) are not implemented. Transition factors may also impact the

types of insurance products and services demanded from firms – including where new

technologies, products and services may disrupt conventional industrial organisation,

business models, and affiliated risk cover needs. For instance, some types of

renewable energy technologies (such as solar power) are already cheaper than

conventional generational technologies in certain markets – and recent analysis by

IRENA has suggested that renewable energy will be consistently cheaper than fossil

fuels by 2020. 45 While such changes may create opportunities for insurers, they may

also create risk – especially in the case of sudden policy changes which affect risk

profiles of insured assets, or significantly constrain market growth.

15. In addition to the two main types of risks above, certain insurers, public authorities,

and other stakeholders have suggested that liability risks may originate from climate change,

including the physical and transition risks described above.

• Liability risks include the risk of climate-related claims under liability policies, as well

as direct claims against insurers for failing to manage climate risks. Research by UN

Environment has found that climate-related litigation has increased significantly around

the world, including over action – or inaction – relating to climate mitigation and

adaptation efforts. 46 Liability risks could arise from management and boards of insurers

not fully considering or responding to the impacts of climate change, or appropriate

disclosure of current and future risks (including through damages and tort litigation).

There may also be exposure to under D&O, PI, and third-party environmental liability

policies. While the debate around legal precedent in this domain is ongoing, and of a

Issues Paper on Climate Change Risks to the Insurance Sector

Approved by the IAIS Executive Committee and the Sustainable Insurance Forum on 25 July 2018 Page 15 of 81protracted nature, there has been a significant increase in major lawsuits being filed

with respect to climate change over the last two years, which may be of import to the

evolution of the liability risk domain for insurers. Most recently, in January 2018, the

City of New York announced lawsuits against five major oil companies, seeking to

collect billions of dollars to fund municipal efforts to cope with climate impacts. 47 Legal

organisation Client Earth reports that several reinsurers have already been seeking

legal advice on their exposure to long-tail claims under commercial general liability

policies in connection with the climate litigation in the US state of California. 48

16. Importantly, these different types of risks are relevant across underwriting and

investment activities of insurers (Table 1).

Table 1: Potential manifestations of physical, transition, and liability risks across

underwriting and investment activities

Underwriting Investment

Physical Risks - Pricing risks arising from - Risks arising from impacts of

changing risk profiles to insured physical climate events and trends on

assets and property (non-life), assets, firms, and sectors, affecting

changing mortality profiles and profitability and cost of business,

demographic trends (life and leading to impacts on financial assets

health) and portfolios (ie debt, equity)

- Claims risk arising from

confluence of unexpected

confluence of extreme events

(ie multiple category 4 or 5

hurricanes)

- Strategic/Market Risks arising

from changing market dynamics

(ie uninsurability of property)

Transition Risks - Strategic/Market Risks arising - Risks arising from market, policy,

from contraction of market technological, and social changes,

demand in certain sectors (ie affecting profitability and cost of

coal, oil, marine transport) business of firms and sectors (ie

energy, industry, transport,

agriculture), leading to impacts on

- Strategic/Market Risks arising financial assets and portfolios (ie debt,

from market trends, equity)

technological innovation, and

policy changes related to

climate change (ie carbon

pricing, energy efficiency

regulations), affecting products

Issues Paper on Climate Change Risks to the Insurance Sector

Approved by the IAIS Executive Committee and the Sustainable Insurance Forum on 25 July 2018 Page 16 of 81and services demanded by

consumers

Liability Risks - Liability risks arising from - Risks arising from litigation (ie class

insurers liable on the basis of action) relating to the consideration of

insurance provided (ie tort or climate change in investment

negligence claims) decision-making, or inadequate

disclosure of climate risks

- Liability risks stemming from

Directors & Officers policies

3.2 Examples of Climate Risks across Insurance Business, Strategy, and

Operations

17. Physical and transition risks may pose different strategic, operational, and reputational

risks to insurers across underwriting and investment business. While certain climate-related

risk factors are long-term in nature, some are already having material impacts. Key examples

include:

• Underwriting Risk: As described in the previous sections, climate change is already

affecting the frequency and concentration of high impact natural catastrophes around

the world, leading to increases in weather-related insurance claims. For instance, the

Lloyd´s market reports to have paid out US$5.8bn in major claims, most of which were

climate-related. 49 The claims burden disasters in 2017 has had material financial

impacts for non-life insurers, with industry Return on Equity dropping from 11% in 2016

to -4% in 2017. 50

• Market Risk: From a pricing risk perspective, insurers’ capacity to write insurance

business may be constrained by increasing physical risks to insured property and

assets, if risk-based pricing rises beyond demand elasticity and customer willingness

to pay. There is evidence that domestic property in high risk areas is being rendered

uninsurable due to high exposure to physical risks, such as wildfires, storms and sea

level rise. In the United States, US$600bn of property within one mile of the coast is

covered under the National Flood Insurance Programme, much of which will not be

viable in coming decades, absent intensive adaptation investments. Market

contractions stemming from physical risks likely to further exacerbate barriers for

consumers to access insurance. Transition risks may significantly change the products

and services desired from insurers, and an inability to appropriately design products

relevant to changing needs could significantly affect market share (as well as create a

strategic risk to overall business viability).

• Investment Risk: The profitability of insurer investment portfolios may be affected if

invested in sectors or assets which may be especially at risk from either physical or

transition-related factors (see section 3.1). This could, at the extreme, constrain

insurers’ capacity to pay future claims. Clearly, the impacts of climate risks at portfolio

level will be influenced by concentration of holdings in specific firms or sectors,

diversification and hedging strategies, and the strength of efforts to actively manage

and monitor exposures. While insurers may be somewhat insulated from the effects of

Issues Paper on Climate Change Risks to the Insurance Sector

Approved by the IAIS Executive Committee and the Sustainable Insurance Forum on 25 July 2018 Page 17 of 81climate factors due to investment behaviour, only a few firms are actively seeking to

explore how portfolios may be affected by climate change now and into the future.

• Strategic Risk: Physical or transition-related climate events, trends, or scenarios may

present strategic challenges to insurers, which could inhibit or prevent an insurer from

achieving its strategic objectives. Examples may include competitiveness impacts

resulting from an inappropriate strategy relating to physical climate risk mitigation, poor

management of future plans, or failure to respond to transition factors affecting the

industry landscape.

• Operational Risk: Physical climate impacts may affect insurer’s own assets (including

property, equipment, IT systems, and human resources), leading to increased

operating costs, inhibited claims management capacity, or potentially stoppages of

operations.

• Reputational Risk: In recent years, insurance underwriting or investment in sectors

perceived as contributing to climate change has emerged as a civil society issue,

exemplified by social movements calling for divestment from fossil fuels and the

cessation of underwriting of coal-fired power infrastructure. 51,52

18. There is emerging consensus that climate change may have a wide range of impacts

across corporate sectors – and that climate risk factors may have important effects on the

capacities of financial firms, including insurers, to conduct business. This is most clearly

exemplified by the statements of major ratings agencies with respect to climate change risk 53

- including Moody’s, which recently concluded that climate change has a net negative credit

impact on P&C and reinsurance sectors. 54

19. While it may be difficult to reliably assess the potential future aggregate impacts of

climate change trends on the insurance market as a whole (in part due to persistently soft

market conditions, and high policyholder surplus in some markets), 55,56 there is increasing

recognition by insurers that climate change is likely to have critical impacts on the sector.

According to the CEO of AXA, “more than four degrees Celsius of warming this century would

make the world uninsurable”. 57

20. Clearly, climate risks may have different impacts on insurers, depending on their core

underwriting business areas, investment allocation strategies, size, speciality, geographic

reach, and domicile. Over the long term, it is clear climate change is likely to have implications

for all types of insurers, either through risk management, risk transfer, or investment channels,

or through impacts on the broader macroeconomy.

Box 2: Novel impacts of warming weather – the experience in Australia

In certain jurisdictions, climate factors are beginning to have novel impacts across

business lines – including increases in high risk behaviour. A major insurer in Australia

studying the impact of climate change on its business has come across an interesting

discovery. The insurer had pinpointed a correlation between heatwaves in Western

Sydney and an increase in alcohol consumption; leading to a spike in break-in activity

during those periods, and ultimately resulting in a higher number of homeowner insurance

claims.

3.2.1 Underwriting Activities

21. Climate change risks may manifest in different ways across different insurance

business lines.

Issues Paper on Climate Change Risks to the Insurance Sector

Approved by the IAIS Executive Committee and the Sustainable Insurance Forum on 25 July 2018 Page 18 of 8122. General insurers are most likely to have underwriting liabilities exposed to physical risks, and as such have greater experience in identifying, pricing, and managing such risks. Increasing uptake of insurance cover for climate-related natural catastrophes and extreme weather (such as domestic flood insurance) could lead to higher premium revenue over the shorter term (as long as risks remain insurable), but could also lead to significant increases in weather-related claims. Large insurers may be insulated from the accumulation of such risks due to annual repricing, geographical diversification, and the availability of reinsurance capacity. However, future climate impacts may be non-linear and increasingly correlated – with multi-annual recurrence of “1-in-100” year events. Knowledge gaps and uncertainties around climate trends in catastrophe models may create the risk of a major catastrophic event (or confluence of multiple events) not being appropriately considered in rate setting and reserving. From a business model viability perspective, general insurance providers may be faced with a unique combination of physical and transition risks affecting demand for insurance products and services. Such changes may create pervasive risks for specialist providers, which may be reliant on underwriting specific economic activities – like shipping. 30% of global seaborne trade in 2016 by volume was in oil and gas, 58 a market which could contract significantly under an aggressive low-carbon transition scenario. 23. Life and health insurers are in many cases just beginning to explore the impacts of climate factors on their underwriting portfolios. The potential impacts of climate change on mortality are becoming a priority focus for actuarial associations, who are exploring the matter in relationship to insurance, annuity and pension programmes. 59,60 Key here are heat related health issues associated with extremes in weather events, especially where excessive heat may compound pre-existing health conditions or vulnerabilities (eg elderly populations). 24. Agricultural insurers, while well-versed in addressing extreme weather, may be affected by climate risks in unexpected and non-linear ways. For instance, businesses in certain geo-climatic zones may no longer be able to grow desired crops, while rising ocean temperatures may have significant impacts on the productivity of fish farming. 25. Reinsurers are often deeply versed in the management of complex systemic risks such as climate change. Due to their exposure across the insurance system and at international levels, reinsurers may inherently be more resilient to climate factors due to geographic diversification. However, as the severity and frequency of significant natural disasters increases, the availability and cost of reinsurance cover for weather-related risks may become prohibitive for smaller insurers in certain markets – potentially leading to a reinsurance gap. Box 3: Reinsurance Cover for Environmental Risks - the experience from Canada The Canadian GI market is comprised of many small insurers and is heavily dependent on the international reinsurance market to provide coverage for major natural catastrophes. Total payout for weather-related claims in Canada has hovered at about Can$1bn per year over the last decade, until 2017 when the Fort McMurray wildfire brought the total liabilities to about Can$4.5bn. A significant amount of this was reinsured internationally, and although Canadian liabilities did not present an issue to large reinsurers, they were also faced with large claims due to significant activity in the Caribbean region in 2017. Supervisors in Canada see potential for a reinsurance gap to emerge for weather-related losses if costs rise significantly or reinsurers stop or restrict reinsuring some of these natural catastrophes. The Office of the Superintendent of Financial Institutions (OSFI) has advised direct insurers to consider whether their reinsurers’ business is concentrated in Issues Paper on Climate Change Risks to the Insurance Sector Approved by the IAIS Executive Committee and the Sustainable Insurance Forum on 25 July 2018 Page 19 of 81

these areas, and if so, whether there is potential for loss of reinsurance coverage. To the

extent such a risk exists, OSFI expects direct insurers to identify alternatives to ensure

they can meet their liabilities to policyholders. OSFI is undertaking a broad review of the

regulatory framework for reinsurance to ensure that it remains up-to-date and appropriate.

3.2.2 Investment Activities

26. Investment activities of insurers may be impacted by both physical and transition risks

arising from climate change, which may have a significant impact on the valuation of financial

assets. If not adequately considered across sectors, disruption to financial markets stemming

from climate risk could affect reserving decisions, capacity satisfy liabilities, and ultimately

impact solvency. To date, the key focus on climate change within the investment landscape

has been from a transition risk perspective – including the potential for policy changes and

technological innovation to result in asset stranding in high-carbon sectors, such as upstream

and downstream fossil fuel sectors (oil, gas, coal) and thermal electricity generation. Research

suggests that the implementation of a 2oC transition pathway could reduce the revenues of

the upstream fossil fuel industry globally by a cumulative US$33trn by 2040, 61 and could lead

to significant macroeconomic implications for certain countries. 62 Several leading central

banks, governments, and financial industry associations are seeking to better understand how

investment portfolios may be affected by climate risks, starting with assessments of overall

capital exposure across asset classes (see section 8). In 2017, the Lloyd’s market released a

report examining actual and potential examples of how stranded assets caused by societal

and technological responses to climate change could affect assets and liabilities in the

insurance and reinsurance sector. 63

27. Some insurers may be comparatively insulated to climate-related risks in capital

markets due to allocation towards long-dated debt instruments. Moody’s has concluded that

P&C and reinsurance portfolios may be generally less exposed to climate risks due to low

asset leverage and high diversification. 64 There is evidence to suggest that the value and

stability of comparatively lower-risk securities could be affected by climate factors:

• Sovereign Debt: There is increasing evidence to suggest that physical risk factors

such as extreme weather, may affect the credit ratings of sovereigns, through direct

losses to infrastructure, as well as impacts on economic activity. Standard & Poor’s

have forecasted that tropical cyclones could potentially lead to downgrades of up to

two notches in vulnerable countries. 65 In recent years, several major agencies have

identified the role of environmental factors in contributing to the conditions leading to

a credit downgrade. In a report detailing its methodology for assessing the physical

risks of climate change to sovereign ratings, Moody’s concludes that climate change

is already exerting “some influence” on the credit ratings of sovereign nations highly

susceptible to its effects – but that near-term implications may be limited. 66 Ratings

agencies are just beginning to explore the impacts of transition risks on sovereign debt

– which could have more wide-ranging impacts across developing vs. developed

economies.

• Municipal Debt: Ratings agencies have also highlighted the potential for climate

change to affect the credit quality of municipal bonds, resulting from “sharp, immediate

and observable impacts on an issuer’s infrastructure, economy and revenue base, and

environment”. 67

• Real Estate: Policy measures and regulatory requirements relating to the

environmental performance of building stock, including energy efficiency regulations,

Issues Paper on Climate Change Risks to the Insurance Sector

Approved by the IAIS Executive Committee and the Sustainable Insurance Forum on 25 July 2018 Page 20 of 81may have impacts on the value of real estate portfolios. In the Netherlands, by 2023,

all commercial property will be required have at least a level C energy label – or be

taken out of use. Analysis by De Nederlandsche Bank (DNB) has found that 19% of

insurer investments related to commercial real estate in the Netherlands involve

collateral with lower-range energy labels (ie from D – mediocre – to G – poor) – which

could represent a potentially significant financial risk if energy efficiency is not

improved, or the assets cannot be liquidated. 68 The value of real estate portfolios may

also be affected by physical risks, if properties are located in high-risk areas.

Issues Paper on Climate Change Risks to the Insurance Sector

Approved by the IAIS Executive Committee and the Sustainable Insurance Forum on 25 July 2018 Page 21 of 81You can also read