CA. M. Chalapathy Rao CA. S. Murali Krishna - Visakhapatnam

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Vol # 7 of 2019 July, 2019

Chairman Secretary Editor

CA. M. Chalapathy Rao CA. S. Murali Krishna CA. Prasanth Kumar P.

email : visakhapatnam@icai.org For Private Circulation only website : www.icaivisakhapatnam.org

Chairman Writes . . . .

Dear Esteemed Colleagues,

I extend my hearty wishes to each one of you on the

occasion of Chartered Accountants’ Day.

This is a land mark day in the history of ICAI, as we

complete 70 years and step into 71st year of formation.

It is indeed a matter of great honour and pride for us

that our Hon’ble Prime Minister Shri Narendra Modi ji

sent Greetings to ICAI and remarked “Chartered

Accountants have earned laurels across the globe for

the dexterity in financial skills”.

The Institute has been at the forefront in the

development of the accountancy profession in the

Bangalore and GST Audit was dealt by S. Ramakrishna

country. Today ICAI has earned the trust and

from Visakhapatnam. Both the speakers have

confidence of the society and more importantly

explained the practical issues we face while filing GST

has reached the distinction of becoming one amongst

Annual returns and GST Audit.

accounting bodies in the world.

On 12th June 2019 we have conducted a CPE Study

Being partners-in-nation-building, the Indian

circle meeting on recent changes in Gifts under

Chartered Accountants have committed themselves

Income Tax by CA. T. Ram Prasad.

to the expected responsibilities of our country in the

past and will continue to do that with complete On 15th June 2019 we have conducted a full day CPE

dedication. Seminar on Recent changes in Income Tax Returns,

Practical Issues in Presumptive Taxation under Sec

As we enter into 71st year of our service to the nation,

44AD and

it’s time to renew our resolve to continue serving our

Nation and other stakeholders in the spirit of 44ADA of the Income tax Act and Computation of

Excellence, Independence and Integrity. On this Total Income under Sec 12A and 10(23C) of the Income

historic day let us re-dedicate ourselves to give Tax Act by CA. E. K. Harish from Vizianagaram, CA.

transparent and truthful accounting, audit and Samvit Durga from Vizianagaram and CA. Suresh

governance service to the industry and the Nation Kumar Kejriwal from Kolkata.

Pleasure in sharing details about Upcoming On 17 th June 2019 AGM was conducted at

Programs: Visakhapatnam Branch of SIRC of ICAI which was

attended by members.

Members please block your dates for Shreyas 6th Sub

Regional Conference in the State of Andhra Pradesh On 19th June 2019 we have conducted CPE Study

on 5th & 6th July 2019. We have renowned speakers Circle meeting on Corporate Fallouts- A case study

taking sessions on topics of Current relevance. A by CA. Narendra Boyina from Srikakulam.

Spiritual session on “Yogic secretes of Happy Living”

On 21st June 2019 5th International Day was celebrated

by Dr. C.A. K Parvathi Kumar. Detailed program is

at Visakhapatnam Branch of SIRC OF ICAI. The

given in news letter.

speakers Mr. D. Anil Reddy and Ms. D. Sirisha teached

To keep pace with changes in Auditing Standards we the importance that Yoga brings in one’s daily life.

are organising three Study circle meetings the details

I thank all the speakers for their efforts in sharing the

of which are given in forthcoming programs.

valuable knowledge with the members.

Successful June 2019 report:

CA Day Week:

On 3rd June 2019 we conducted a CPE study circle

A)Programs:

meeting on GST regarding recent changes in GST by

CA. Sunil Gabhawalla from Mumbai. On 26th June we have conducted Investors awareness

program, CA. B. Kumar, DGM, Zonal Manager, and

On 8th June 2019 we have conducted a full day seminar

Bank of India Attended as Chief Guest for the event.

on GST Annual returns and GST audit. The topic GST

The Speakers Mr. Satish Kumar Arya MD, Steel City

Annual returns was dealt by CA. T. R. Rajesh from

Securities and Mr. Abhishek Goud Associate NSE

discussed recent developments in Investors front with we have distributed Literacy kits to students of GVMC

members and general public. Government School at Railway New Colony,

Visakhapatnam. I thank CA. A. Chandra Sekhar for

On 29th June we conducted career counselling and

his contribution of Bags in literacy kits and CA. N. S. S.

GST Awareness programs in Visakha Govt Degree

Prakash Rao towards contribution of Books.

College for women. The speaker for the program was

Miss Prachi Jain CA Final student explained the basics B) Sports:

and overview of GST. The Managing Committee

We have conducted a cricket match for members on

members Chairman CA. M. Chalapathy Rao, Vice

16th June in which 3 teams have participated.

Chairperson CA. G. Bharati Devi, SICASA chairman

CA. Y. Surya Chandra Rao attended the event and We have conducted a Shuttle match for members on

College Members Principal Smt S Shobha Rani, Vice 23rd June and games for family members and children

Principal Mr. P. V. Ramana Reddy Commerce head on 23 rd June. Many members have actively

Mr. SVS Prasad, commerce lecturer Mrs. S. Anuradha participated in the event.

have Participated in the program.

Similarly SICASA organised Cricket match, shettle,

On 30 th June SICASA jointly with Visakhapatnam chess for students in which students have actively

Branch of SIRC of ICAI has conducted a blood participated.

donation campaign in which 71 students have donated

blood. I Thank and appreciate all the students for the With ward regards

efforts they made for a good cause. CA. M. Chalapathy Rao

Chairman

As part of Professional Social Responsibility activities,

MEMBERS DIARY FOR THE MONTH OF JULY 2019

Date & Day Venue & Time CPE Hours Name of the Programme & Speaker

01.07.2019 ICAI Bhawan CPE Seminar Overview of Accounting Standards

Monday 9.30 am to 12.30 pm CPE 3 Hours and its applicability

CA.Chilakala Lakshmi Srinivasa Reddy

05.07.2019 Daily 10.00 am to CPE 12 Hours Enclosed Invitation

Friday & 5.00 pm

06.07.2019

Saturday

08.07.2019 ICAI Bhawan CPE 3 Hours Finance Bill 2019

Monday 5.30 pm to 8.30 pm CA.PVSS Prasad, Hyderababd

10.07.2019 ICAI Bhawan CPE Study Circle Meeting CPE Study Circle Meeting on

Wednesday 5.30 pm to 8.30 pm CPE 3 Hours Standards of Auditing - SQC 1 and

SA 200-299 General Principles and

Responsibilities

CA.N. Abilah

17.07.2019 ICAI Bhawan CPE Study Circle Meeting CPE Study Circle Meeting on Standards

Wednesday 5.30 pm to 8.30 pm CPE 3 Hours of Auditing -SA 700-799 Audit

Conclusions and Reporting

CA. T.S.S. Vinay

24.07.2019 ICAI Bhawan CPE Study Circle Meeting CPE Study Circle Meeting on Standards

Wednesday 5.30 pm to 8.30 pm CPE 3 Hours of Auditing - SA 500-599 Audit Evidence

CA. Satya Dev Anupindi

TAX UPDATE

AP VAT / GST Update CA. Ambati Chinna Gangaiah, agcpower@icai.org, Cell : 08801032969

HIGH COURT

NATIONAL ANTI PROFITEERING AUTHORITY ADVANCE RULINGS GIVEN IN 2019

NOTIFICATIONS ISUUED UNDER GST (CBIC)

Income Tax Updates

GIST OF JUDGMENTS OF SUPREME COURT

GIST OF JUDGMENTS OF HIGH COURTS

INCOME TAX APPELIATE TRIBUNAL

REPRESENTATION IN APPEALS BEFORE COMMISSIONER

(APPEALS)

…. A ‘Right’ and a ‘Remedy’

By CA. Malladi Muralidhar, AIII, LLB

“The young man knows the rules, but the old man knows the exceptions.” –

Oliver Wendell Holmes. The remedy available to Asseesee is a

fundamental right envisaged in income tax law. Unless one

knows the “Next step Forward”, one cannot get justice.

The “Demand notice” under sec 156 served on

assessee as per the assessment order

triggers assessee with a right of

Appeal

as remedy. An assessment orders

based on pre-conceived notion fails the litmus test,

that’s why it should not be based on an opinion, persuasion,

sentiment, thought, view, a personal belief or judgment that is

not founded on proof or certainty. The Aggrieved tax payer always can

file an appeal before the Commissioner (Appeals) having, jurisdiction over the tax payer.

PROLOGUE:

“More important than your obligation to follow your conscience, or at least prior to it, is your obligation to

form your conscience correctly” - Antonin Scalia. This is very True that experience counts while defending

the cases before Appellate authorities.

If any demand is raised by the Assessing Officer in the assessment, remedy for Assessee is to file an Ap-

peal. The Remedy is always to be mentioned in the notice as assessee can appeal to Commissioner (Ap-

peals), with whom appeal is to be filed in the notice of demand issued by the Assessing Officer under

section 156 of Income Tax Act. Otherwise notice itself is invalid.

Assessment proceedings not properly attended to will complicate the appeal proceedings. An appeal is

only the continuation of the original proceedings and the powers of the appellate authority are co-exten-

sive with those of the original assessing authority. This point is very important to note that CIT(A) has the

power to conduct all such inquiries apart from power to levy the penalty where the Assessing officer has

omitted to do so.

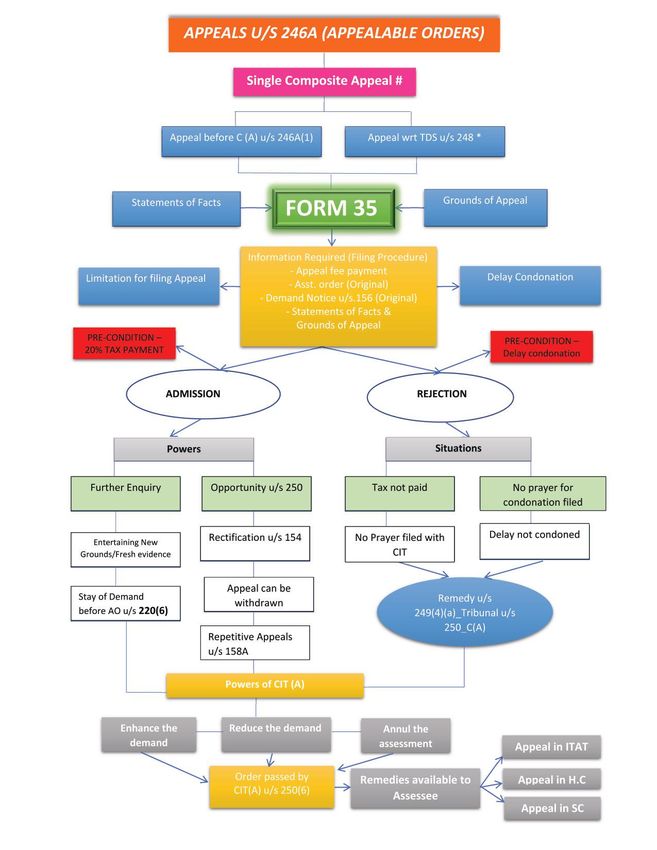

The Chart drawn is for easy reference of whole gamut of Appeals u/s 246 in a nut shell:# though there is no indication in the section when several issues are emerging out of an as-

sessment order, appealable under different subsections of 246A is Maintainable since appeal

is a substantive right, rules being procedural cannot negate the right.

* Denial Any kind may be appealed u/s 246A(1)[Person denying his liability to be assessed], but

only the denial of Liability to deduct tax alone can be brought under sec 248 [Only person who

claims no tax deduction required on certain income].

I. The Provision coupled with Procedure to File an Appeal:

Provision / Section under which appeal is filed : 246A

Appellate Authority : CIT (A)

Application Form : 35 [See Rule 45]

Time limit for Filing of Appeal : 30 days from the receipt of the order

Time limit for Disposal of Appeal : 1 Year from the end of the FY 4 Year

from the end of the FY

Filing/Uplaoding : E-Filing of the From in Log in

Stay of Demand : Not possible

Recovery of Tax : No power to stay the recovery of Tax

Appeal Fees to be paid : Table below

Sr.no Total Income determined by the Assessing Officer Appeal Fees

1 Less than Rs. 1,00,000/- Rs. 250

2 More than Rs.1,00,000/- but less than Rs.2,00,000/- Rs. 500

3 More than Rs. 2,00,000/- Rs. 1,000

*Where the subject matter of appeal relates to any other matter, fee of Rs. 250/- is to be paid.

II. WHEN APPEAL CAN BE FILED BEFORE COMMISSIONER (APPEALS), i.e. APPEALABLE ORDERS:

Appeal can be filed before Commissioner (Appeals),

a. when a tax payer is adversely affected by Orders as under passed by various Income tax authorities:

b. All or any Orders against tax payer where the tax payer denies liability to be assessed under Income

Tax Act;

c. All Appealable orders except Orders of CIT u/s 263 /264.

d. Against any Penalty orders served may be filed u/s 246A.

e. Any denial of Liability to deduct tax on certain income alone can be brought under sec 248.

III. FORM OF APPEAL AND PROCEDURE TO FILL THE SAME:

The Form No. 35 contains details such as name and address of the tax payer, Permanent Account Number

(PAN), assessment year, details of the order against which appeal is filed etc. are to be filled in.

Salient features of Form no.35 and procedures involved in Filing an Appeal:

i. E- Form 35 is used in these day for filing appeal (Available in Log-in)

ii. No Physical documents are accepted in the department.iii. “Relief claimed in appeal”, i.e. amount sought by way of Income or any other relief to be men-

tioned.

iv. “Statement of Facts”, i.e. relevant facts in respect of each subject matter of appeal are to be men-

tioned in brief. Nature of business or profession, account books maintained etc. may also be men-

tioned in this column.

v. “Grounds of appeal”, i.e. points on which relief is sought in appeal are to be mentioned in narrative

form. For example, in an appeal against addition to the returned income by applying a gross profit

rate on estimated turnover, the ground of appeal may be, “the Ld. Assessing Officer was not justi-

fied in rejecting the results as per regular books of account and in estimating the income by applying

an adhoc rate of gross profit.”

vi. PAYMENT OF ACCEPTED TAX LIABILITY MUST BEFORE FILING APPEAL:

An appeal will be admitted by Commissioner (Appeals) only if tax as per the returned income,

where return of income is filed, or advance tax payable, where no return of income is filed has

been paid prior to filing of appeal.

The following two are to be paid being a pre-condition for admission of appeal:

1. Appeal Fees : As per schedule mentioned above in Srl no. I above.

2. 20% Pre-deposit fee: The Assessee Company need to pay 20 % of the disputed demand

before hearing the appeal matter in the office of CIT (A).

In the latter situation i.e. where return of income is not filed, tax payer can apply to the

Commissioner (Appeals) for exemption from such condition for good and sufficient rea-

sons.

vii. TIME LIMIT FOR FILING AN APPEAL & DELAY CONDONATION:

Appeal is to be filed within 30 days of the date of service of notice of demand relating to assess-

ment or penalty order or the date of service of order sought to be appealed against, as the case

may be. The Commissioner (Appeals) may,

A. i) Admit an appeal appeal filed within 30 days,

ii) May Admit by condoning the delay in filing the appeal in genuine cases with a view to

dispense substantive justice, after the expiration of period of 30 days, if he is satisfied that

there was sufficient cause for not presenting the appeal within the period of 30 days.

[An affidavit for condoning the delay citing out reasons for the delay along with necessary

evidences should be filed along with Form No. 35 at the time of filing of appeal.

• It must be grasped that the judiciary is respected not on account of its power to legalize injustice

on technical grounds but because it is capable of removing injustice and is expected to do so.

Collector, Land Acquisition Vs. Mrs. Kataji & Ors. (1987) 167 ITR 471 (SC)

• When substantial justice and technical considerations are pitted against each other, the cause of

substantial justice deserves to be preferred, for the other side cannot claim to have vested right

in injustice being done because of a non-deliberate delay

• Sufficient cause – Connotation of

It was held in Encon Furnaces (P) Ltd. v. CIT (1996) 56 ITD 14 (Del-Trib), that the use of both words

‘good’ and ‘sufficient’ suggests that the common test whether a cause is sufficient or not is tosay whether it could have been avoided by the party by the exercise of due care and attention.

• Mistake of counsel

There is no general proposition that mistake of counsel by itself is always a sufficient ground for

condoning the delay though it may in certain circumstances be taken into account in condoning

the delay. It is always a question whether the mistake was bona fide or was merely a device to

cover an ulterior purpose such as the laches on the part of the litigant or an attempt to save

limitation in an underhand way. –– Refer to Mata Din v. A. Narayanan AIR 1970 SC 1953, India

Insurance Co.Ltd. v. Smt. Nirmal Devi (1979) 118 ITR 507 (SC), Avtar Krishan Dass v. CIT (1982) 133

ITR 338 (Del) and Raju Ramchandra Bhangde v. CIT (1984) 148 ITR 391 (Bom).

B. Reject an appeal specifying the reasons thereof in writing.

IV. APPEAL PROCEDURE RELATED IMPORTANT POINTS:

- Fixing a date and place for hearing the appeal by issuing notice to the tax payer and the Assessing

Officer, against whose order appeal is preferred.

- Limitation as to Filing: The period of limitation starts from date of notice. The following cases, the

Limitation to run beyond are:

i. Date of Knowledge of contents of the order

ii. Date of Service of Demand

iii. Service of order on person not authorised to receive

iv. As per sec 249(2)(a), appeal by person denying liability to deduct tax starts from date of

payment of tax.

v. Exclusion of Time taken for obtaining a certified copy.

vi. Date of filing where memorandum of appeal is sent through post.

- Pre-conditions:

There are two pre-conditions or twin requisites for admitting an appeal

A. 20% Pre-deposit of Tax is Paid

B. Delay if any to be condoned followed by an application

- The tax payer has a right to be heard either personally or through an Authorized Representative.

- Submission of Delay condonation petition: It may be

a) Admitted being CIT(A) empowered & also discretion or if construed liberally or a sufficient cause

is shown, i.e. Delay due to Illness, mistake of counsel or Halt of business operation or change in

address, but should not be a negligence or inaction. Or

- b) Refused, but the Order refusing to condone the delay must be a speaking order.

- Submission of POA for appearing for the hearing not uploaded along with Form.35

- Submission of Paper Book: Generally these days, all replies are submitted to the CIT (A) in form of

Paper Book.

Detail of sample format of Indexing of Paper Book as follows:Sr.no Particulars Page No

1 Notice of Assessment u/s 143

2 Reply filed against the notice

3 Letter of adjournment filed with AO

4 Reply filed with AO ( In respective addition made)

5 Case laws

6 Assessment Order

- CIT(A) May adjourn it from time to time till the hearing is over.

- Written submissions shall contain the arguments as well as the case laws relied upon.

- Additional grounds of appeal:

Commissioner (Appeals) may allow the tax payer to go into additional grounds of appeal, i.e. grounds

not specified in the appeal memo, i.e. on being satisfied that omission of those grounds from the

form of appeal was

a) not wilful, or

b) unreasonable

Filing of Additional ground is permissible, if the ground so raised could not have been raised at

that particular stage when a) the return was filed or b) when the assessment order was made,

or c) that the ground became available on account of change of circumstances or law. But it

should be Bonafide and same could not be raised earlier for good reasons.

[Note that Separate petition to be filed for admission of additional grounds of appeal or for

admission of additional evidence ]

- Filing of Additional Evidence:

During appeal proceedings, the tax payer is not entitled to produce any evidence, whether oral or

documentary other than what was already produced before the Assessing Officer. Any document

not filed before the assessing officer must be marked as additional evidence.

Commissioner (Appeals) would admit additional evidence filed only in following situations :

a. (i) where the Assessing Officer has refused to admit evidence which ought to have been admit-

ted; or

(ii) where the appellant was prevented by sufficient cause from producing the

- evidence which he was called upon to be produced by the Assessing Officer; or

- evidence which is relevant to any ground of appeal; or

b. where the Assessing Officer has made the order appealed against without giving sufficient

opportunity to the appellant to adduce evidence relevant to any ground of appeal.

Additional evidence where necessary for disposal of appeal:

Where assessing officer refused to accept the requisite details filed by assessee, and further, those

evidences were from government agency and the same were essential for disposal of the appeal,

Commissioner (Appeals) was justified in admitting new evidences in terms of rule 46A of Income Tax

Rules, 1962. –– Vide ITO v. Bhagwan Dass (2012) 47 (II) ITCL 212 (Chd ‘B’-Trib): (2012) 17 ITR 446 (Chd

‘B’-Trib): (2012) 137 ITD 120 (Chd ‘B’-Trib): (2012) 147 TTJ (Chd’B’-Trib) 41.- Commissioner (Appeals) may carry out further enquiry himself or through the Assessing Officer.

- Petition for Stay of Demand: Sec 220 empower CIT(A) to stay the recovery of taxes and discre-

tionary. The stay is restricted or confined to period of pendency of appeal order.

- Possibility of withdrawl of Appeal: There is nothing illegal to withdraw, but may withdraw with the

permission of appellate authority.

- Ex parte dismissal of appeal is also not allowed, even if appellant doesnot appear.

- The appeal should be decided on Merits of the case.

- Legal issue raised for first time:

For first time asessee had raised an additional legal issue, which was not taken before assessing

authority. It is only after assessing authority passed a fresh assessment order and that order when it

was called in question before first appellate authority, for first time an additional issue was raised

and canvassed. This had been rightly allowed by first appellate authority as the issue raised was

legal issue. –– Vide CIT v. Smt. Madhu Patani (2009) 26 (I) ITCL 544 (Ker-HC).

V. PREPARATION OF GROUNDS OF APPEAL:

Everyone know how to prepare grounds of appeal, but few important things to make it a better

drafting to make the appeal favourable to assessee are mentioned below:

i. There may be several arguments in support of a claim, But all arguments cannot form

grounds of appeal.

ii. A simple Language should be used while framing grounds which should be very Clear

and convey exactly what is intended to be conveyed.

iii. Grounds must be Precise, Concise and Neither argumentative nor Lengthy.

iv. Nature of dispute and expected relief to be highlighted and stated for each grounds of

appeal.

v. Generally references to caselaws to be avoided which can create a controversy and

ultimately rejection of appeal.

vi. Grounds specified to be given Preference wise.

vii. Grounds challenging Jurisdiction should be mentioned as First ground.

viii. Sufficient Opportunity not provided by AO should be given more weightage.

ix. Facts and Grounds should be matched and should be clearly shown whether they were

highlighted before ITO or not.

VI. PRECUATIONS / CHECK LIST WRT FILING AN APPEAL:

While accepting a case or while drafting an appeal before CIT(Appeals), the following may be checked for

better clarity,

1. Verify whether the appeal /Relief exists: Decide after analysing the orders thoroughly.

2. Ascertain the Validity of Jurisdiction of AO.

3. Check the limitation period of 30 days and condonation petition requirement.

4. Compute Pre-deposit of 20% of the Tax dispute and pay.

5. Ensure whether Order was passed within Time limits prescribed under the provisions.

6. Plan for widest possible alternative grounds of appeal.

7. Statement of facts ought be framed with clarity.8. Application for Stay as & where required.

9. Prompt reply to be filed in case of any show cause notice.

10. Any claim had missed out after filing, a fresh plea can be raised.

11. Any additional ground or additional evidence may be explained fully the importance of

the same wrt the case may be pressed wherever required.

12. In normal circumstances, agreed additions cannot be appealed against.

13. Always raise one general ground seeking leave for modification of or addition to the

grounds of appeal, i.e. Any Grounds at the time of hearing.

VII. EFFECTIVE REPRESENTATION BEFORE COMMISSIONER (APPEALS):

While representing the case of the assessee before the first appellate authority the following tips may play

an effective role –

1. Case of the assessee should be communicated effectively.

2. There should be a proper index with brief description of evidences filed.

3. Case laws relied on should be gathered and submitted during arguments or with paper book. As a

case law may deal with several issues all of which may not be relevant for the appeal on hand, there-

fore, it is suggested that one should highlight or underline the relevant parts of the case law.

4. Rules of precedence are to be strictly followed.

5. There should be effective communication skills evident in the presentation.

6. Dress code for appearance before appellate authority should be followed.

7. Body language i.e., how you sit, stand, movement of arms, eye movements are very important while

representing the case.

8. Ability to think on the feet should be developed.

9. One should listen to the other side and wait for his turn.

10. Tone of speech should reflect respect for the authority and should also reflect belief in assessee’s

case.

11. Speed of speech should be appropriate, neither too fast nor slow.

12. There should be eye contact but it should not be intimidating.

VIII. CONCLUSION:

Foundation of an income tax appeal lies in assessment proceedings. Appeal is a remedy provided by law for

getting a decree of lower court or authority corrected when a party to the litigation is aggrieved. After the

hearing is concluded, Commissioner (Appeals) passes order in writing, disposing of the appeal and stating

the decision on each ground of appeal with reasons. Commissioner (Appeals) has a power through which

he may confirm, reduce or enhance it.

i. Before enhancing any assessment or penalty, Commissioner of Income-tax (Appeals) has to pro-

vide reasonable opportunity to the tax payer for showing cause against such enhancement).

ii. While disposing of an appeal, the Commissioner (Appeals) may consider and decide any matter

arising out of the proceedings in which order appealed against was passed, even if such matter was

not raised by the tax payer.

Once there is a statutory provision conferring the right of appeal, such a provision is to be con-

strued in a liberal, reasonable and practical manner, as was held in CIT Vs. Ashoka Engineering Co.

(1992) 194 ITR 645 (SC) & C.Ramaiah Reddy Vs. ACIT (2011) 244 CTR (Kar) 126.Seminar on Recent Changes in Goods and Service Tax on 3rd June, 2019

Seminar on GST Annual Returns & GST Audit on 8th June, 2019

Seminar on Recent Changes in Gifts under Income Tax on 12th June, 2019Seminar on Changes in Income Tax Returns, Presumptive Taxation and NPO Taxation on 15th June, 2019

AGM on 17th June, 2019Study Circle Meeting on Corporate Fallouts - A Case Study on 19th June, 2019

International Yoga Day on 21st June, 2019

Cricket MatchGames and other events for Women Members, Spouses and Children on 23rd June, 2019

School kits

distribution to

gvmc municipal

school students

on 6th June,

2019

Career Counseling and GST Awareness Program at Visakha Women's Degree College

Ms. Prachi JainSeminar on Investors Awareness Programme on 26th June, 2019

SICASA Students Seminar on 1st June, 2019

Published by CA. M. Chalapathy Rao, Chairman on behalf of Visakhapatnam Branch of SIRC of The Institute of Chartered Accountants of India, Visakhapatnam

and Desgined at Maruthi Printers, D.No.30-5-17, Krishna Gardens, Dabagardens, Visakhapatnam - 20, Cell : 92469 32859, email : balajiavprasad@gmail.com

and Published for Visakhapatnam Branch of SIRC of ICAI, D.No.9-36-22/2, Pithapuram Colony, Visakhapatnam - 530 003, Ph : 0891-2755019,

email : visakhapatnam@icai.org Editor : CA. Prasanth Kumar P, Visakhapatnam Branch of SIRC of ICAI

The Views expressed by contributors in this Newsletter do not necessarily reflect the opinion of the Branch or the InstituteYou can also read