Local Aggregate Assessment - Joint Minerals & Waste Plan Central & Eastern Berkshire Authorities - February 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Central & Eastern Berkshire Authorities

Joint Minerals & Waste Plan

Local Aggregate Assessment

February 2021

Prepared by Hampshire Services Hampshire County Council www.hants.gov.uk/sharedexpertise

Table of Contents 1. Introduction .......................................................................................................... 3 2. Land Won Aggregate ........................................................................................... 7 3. Crushed Rock .................................................................................................... 12 4. Marine-won sand and gravel ............................................................................. 14 5. Recycled/Secondary Aggregates....................................................................... 15 6. Future Aggregate Supply ................................................................................... 18 7. Future provision of sand and gravel ................................................................... 22 8. Conclusions and review of the LAA .................................................................... 25 Tables and Figures Table 1: Permitted active quarries in Central and Eastern Berkshire, 2019 ............... 9 Table 2: Land-won sand and gravel sales in Central and Eastern Berkshire, 2010- 2019 (Thousand tonnes, Tt) ..................................................................................... 10 Table 3: Total consumption of Primary Aggregate in Berkshire, 2009 and 2014 ...... 12 Table 4: Crushed rock sales from rail depots and wharves in Berkshire (Berks) and Hampshire (Hants), 2010-2019 (Thousand tonnes, Tt) ............................................ 14 Table 5: Recycled aggregate capacity, 2019 ........................................................... 16 Table 6: Recycled and Secondary aggregate sales in Central and Eastern Berkshire, 2010-2019 (Thousand tonnes, Tt) ............................................................................ 17 Table 7: Central and Eastern Berkshire sand and gravel reserves and landbank 2019 ................................................................................................................................. 21 Table 8: Total sales and estimated production capacity, 2019 ................................. 23 Figure 1: Sand and gravel resources in Central and Eastern Berkshire. .................... 7 Figure 2: Location of active quarries in Central and Eastern Berkshire, 2019 ............ 8 Figure 3: Sales of land-won Sand and Gravel in Central and Eastern Berkshire ..... 10 Figure 4: Sales of land-won sand and gravel in South-East England and Central and Eastern Berkshire ..................................................................................................... 11 Figure 5: Location map of active recycled aggregate sites in Central and Eastern Berkshire, 2019 ........................................................................................................ 17

A 2014 Summary – Central and Eastern Berkshire (for the calendar year 2019)

2019 Average Average Trend Trend

LAA Reserve Landbank Capacity

Sales (10 yr) (3yr) Sales (10 yr (3 yr Comments

Rate (Mt) (Mt) (years) (Mtpa)

(Mt) Sales (Mt) (Mt) sales) sales)

There are no active soft sand sites within the Plan

Soft Sand

area.

Figures are combined with soft sand to provide ‘All

Sharp Sand & Sand & Gravel’ figures.

Gravel

The landbank is above the minimum 7-year

0.528 0.635 0.51 0.628 7.407 11.8 1.11 requirement. The LAA Rate remains unchanged due

All Sand & Gravel

to economic uncertainties. Please note capacity is

based on 2018 data.

Central and Eastern Berkshire does not have any

Crushed Rock natural hard rock resources and therefore relies on

imports of this material.

Figures for Central and Eastern Berkshire are only

Recycled / available for the last 6 years. The LAA Rate reflects

0.092 0.121 0.121 0.148 the 3-year average to account for economic

Secondary uncertainty but also (temporary) capacity information.

Aggregates Agg recycling capacity has been significantly reduced

at Bray Quarry.

There are no wharves in Central and Eastern

Marine Sand &

Berkshire.

Gravel

Rock Imports by Not relevant to the Plan area.

Sea

Rail Depot Sales

(Sand & Gravel

There are no rail depots in Central and Eastern

Berkshire, although the area is likely to be served by

rail depots in neighbouring mineral planning areas.

Rail Depot Sales

(Crushed Rock)

1It is likely that there will be in an overall increase in future aggregate demand to account for the increased level of planned future infrastructure

delivery, but this is set in the context of a current recession and future economic uncertainty. The LAA Rate of 0.628Mt for sand and gravel is

unchanged from 2018, taking account of future uncertainty. However, the LAA Rate for recycled aggregate has been reduced to 0.121 to

Comments reflect economic uncertainties but also known changes in capacity. The LAA Rates will continue to be revisited yearly to establish whether the

Central and Eastern Berkshire Authorities are making a full contribution to the Managed Aggregate Supply System. The current sales figures

show a trend of the Plan area rising to meet demand, but it is unclear whether this trend will continue based on current economic

circumstances.

2Executive Summary

Introduction

This is the Local Aggregate Assessment (LAA) for Central and Eastern

Berkshire and covers the administrative areas of the plan-making partners

(Bracknell Forest Council, Reading Borough Council, the Royal Borough of

Windsor & Maidenhead and Wokingham Borough Council). In addition,

information has been provided for Slough, where available. The purpose of the

LAA is to detail the current and predicted situation in Central and Eastern

Berkshire with respect to all aspects of aggregate supply.

Land-won Aggregate

Sand and Gravel

In terms of aggregates, Central and Eastern Berkshire’s geology provides both

sharp sand and gravel and soft sand. Aggregates used within Central and

Eastern Berkshire are sourced from land-won resources, recycled aggregate

and imports.

Within Central and Eastern Berkshire, there were three active quarries in 2018.

There have been no operational quarries within Slough Borough Council for 12

years.

Soft sand resources in the area are generally poor quality and are no longer

principally extracted within Central and Eastern Berkshire. This places a

reliance on imports to address the lack of local supply.

Sales of sand and gravel increased slightly in 2019 by 17,000 Tonnes. The

overall trajectory of 10-year sales is increasing and the pattern of sales is

broadly similar to the South East.

Crushed Rock

Central and Eastern Berkshire is dependent on imports of crushed rock

predominately from Somerset who have confirmed no issues with ongoing

supply.

Supply is imported via rail depots in West Berkshire. There is currently no

evidence that suggests a need to increase capacity at rail depots for imports.

3Marine Sand & Gravel

Marine-won sand and gravel is a small but growing proportion of the total

aggregate consumed in Berkshire. Marine imports are predominately from

London Wharves and Hampshire. Currently there is no evidence to increase

capacity at the rail depots and the 2018 data for Hampshire1 suggests that

there is unlikely to be headroom at their wharves to serve an increase in

demand.

Recycled & Secondary Aggregate

Sales of recycled aggregate in Central and Eastern Berkshire increased in

2019. Capacity survey information was limited but indicates that recycled

aggregate sites capacity has dropped significantly.

Future Aggregate Supply

There are a number of major infrastructure projects as well as local housing

and transport projects which indicate growth and therefore, an increase in

aggregate demand.

Reserves of sand and gravel in Central & Eastern Berkshire with planning

permission for extraction (permitted reserves) at 31st December 2019 were

7,407,000 tonnes (discounting Star Works as this is inactive).

The total landbank for all land-won aggregate based on 10-year average is 11.7

yrs. Based on three-year average sales, the landbank is 14.5 years, although

the landbank is not necessarily an accurate reflection of supply. The 2019 LAA

Rate remains unchanged from 2018 and is 0.628Mt. The LAA Rate has not

been updated to reflect the increase in the 10-average due to current recession

and uncertain economic recovery period.

The Central & Eastern Berkshire Authorities are working together to produce a

Joint Minerals & Waste Plan up to 2036.

The Proposed Submission Plan was subject to consultation during 2020. The

Plan includes proposed allocations for sharp sand and gravel, an aggregate

wharf and a recycled aggregate site. However, the proposals do not meet the

required demands for Central and Eastern Berkshire and therefore, the sites

are supported by criteria-based policies and an ‘Area of Search’ for sand and

gravel.

1

Hampshire 2019 LAA: http://www3.hants.gov.uk/mineralsandwaste/pd-facts-and-figures.htm

4It is estimated that the demand for soft sand over the Plan period will be in the

region of 1.0 million tonnes (65,000 tonnes per year). Sources will need to be

secured from elsewhere.

Conclusions

Central and Eastern Berkshire’s current local aggregate provision will impact on

the wider South East region as a whole if new development is not enabled to

meet the forecasted demand up to 2036. Central and Eastern Berkshire is

reliant on supplies from other mineral planning authority areas and as such this

will need to be given consideration in other relevant Mineral Local Plans

through the duty to cooperate and strategic cross-boundary liaison.

51. Introduction

1.1 The purpose of this Local Aggregate Assessment (LAA) is to detail the current

and predicted situation in Central and Eastern Berkshire with respect to all

aspects of aggregate supply.

1.2 The National Planning Policy Framework (NPPF)2 set out the requirement for

local authorities to produce an annual LAA, stating that ‘Minerals planning

authorities should plan for a steady and adequate supply of aggregates by

preparing an annual Local Aggregate Assessment, either individually or jointly

by agreement with other mineral planning authorities based on a rolling

average of 10 years sales data and other relevant local information, and an

assessment of all supply options (including marine dredged, secondary and

recycled sources)’.

1.3 Bracknell Forest Council, Reading Borough Council, the Royal Borough of

Windsor and Maidenhead and Wokingham Borough Council (collectively

referred to as the ‘Central & Eastern Berkshire Authorities’) are working in

partnership to produce the Central and Eastern Berkshire - Joint Minerals &

Waste Plan. The Plan will indicate what provision of minerals is required, where

these may be located; when they are to be provided and how they will be

delivered during the Plan period to 2036.

1.4 This is the Local Aggregate Assessment (LAA) for Central and Eastern

Berkshire and covers the administrative areas of the plan making partners. In

addition, information has been provided for Slough, where available. The

purpose of the LAA is to detail the current and predicted situation in Central and

Eastern Berkshire with respect to all aspects of aggregate supply, in particular

with regard to land-won aggregate provision up to 2036.

1.5 It is important to note that the data used in the preparation of this LAA

predominantly comes from the annual monitoring of aggregates sales by the

Central & Eastern Berkshire Authorities on behalf of the South East England

Aggregate Working Party (SEEAWP). The Aggregate Monitoring (AM) survey is

used to collect annual sales data from active mineral extraction sites, aggregate

wharves, aggregate rail depots and recycled aggregate processing sites.

2

National Planning Policy Framework, paragraph 207(a):

https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/810197/

NPPF_Feb_2019_revised.pdf

62. Land Won Aggregate

Geology of Central and Eastern Berkshire

2.1 The geology of Central and Eastern Berkshire is underlain by three main types

of minerals: sand and gravel, chalk and clay. There are no deposits of crushed

rock.

2.2 In terms of aggregates, Central and Eastern Berkshire’s geology (see Figure 1)

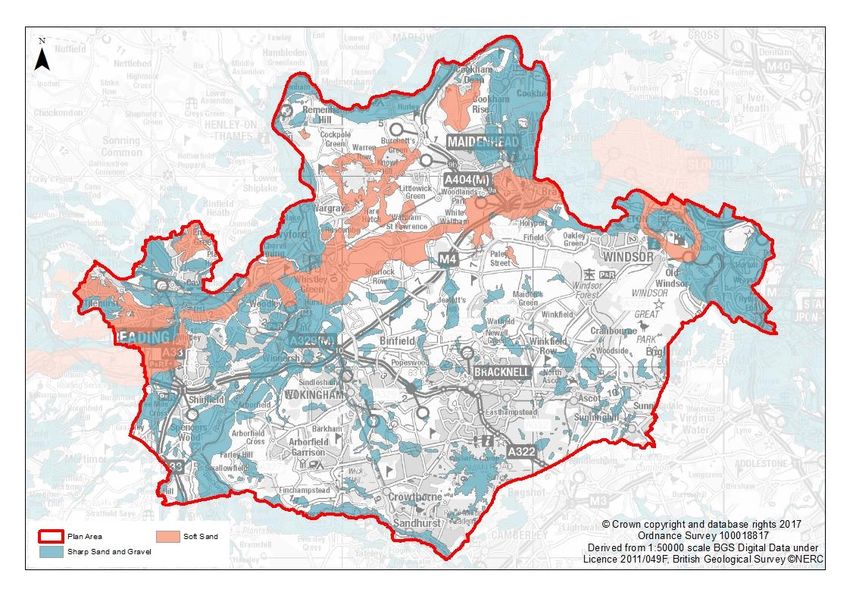

provides the following:

• Sharp sand and gravel; and

• Soft sand.

Figure 1: Sand and gravel resources in Central and Eastern Berkshire.

2.3 Central and Eastern Berkshire has the capability of supplying aggregates from

a number of sources including:

• Land-won extraction;

• recycled and secondary aggregate; and

• imported aggregate (via rail depots)3.

3

Estimate of imports by road can be found in the AM 2014 National Collation.

72.4 Further information regarding the detailed geology can be found in the

Minerals: Background Study (2020)4 which was produced in support of the

emerging Joint Minerals and Waste Plan.

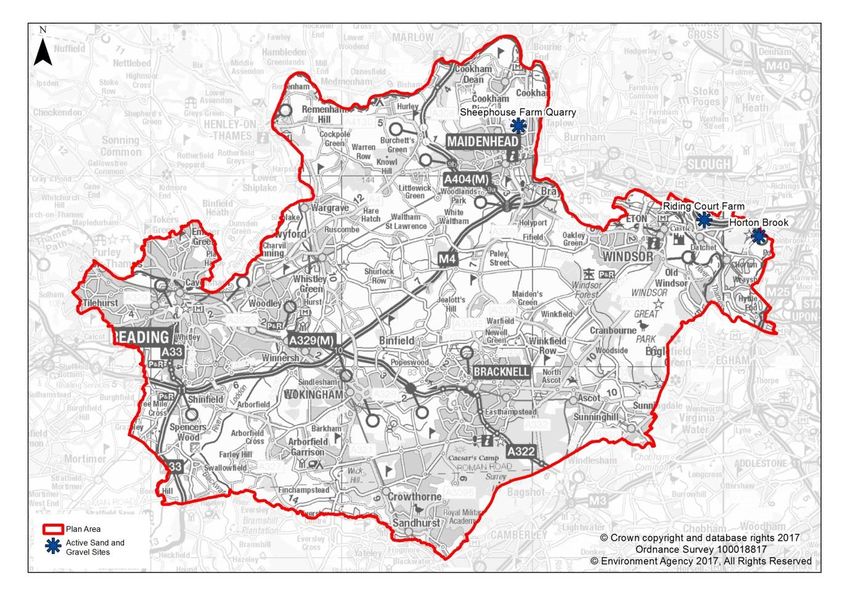

Permitted Sites Producing Sand and Gravel in Central and Eastern

Berkshire

2.5 Figure 2 shows the location of the active quarries in Central and Eastern

Berkshire in 2019 which were predominately located in the north and east

within the Royal Borough of Windsor and Maidenhead. The last quarry in the

south of the area closed in 2017, meaning that the supply of sand and gravel is

currently produced entirely in the north east of the Plan area.

Figure 2: Location of active quarries in Central and Eastern Berkshire, 2019

2.6 The number of extraction sites has decreased in recent years, with 2017 seeing

the closure of two sites; Eversley Quarry and Kingsmead Quarry. In addition,

Star Works, Knowl Hill has permitted reserves but is an inactive site.

2.7 More recently, an application was granted for an extension at Horton Brook

Quarry, Horton5 in 2018 due to greater reserves being identified and Poyle

4

Minerals Background Study (2020): https://documents.hants.gov.uk/environment/Regulation19-

ProposedSubmissionConsultation-JCEBMineralsBackgroundStudy-ProposedSubmission.pdf

8Quarry, Horton was granted permission in January 20196. However, Poyle

Quarry is not yet operational and as such has not been included in Figure 1.

2.8 Extraction sites have not been operational within the administrative area of

Slough Borough Council for over 10 years. However, a number of sites operate

on the boundary of the area.

2.9 Soft sand resources in the area are generally poor quality with pockets of

material of economic interest in a small number of areas. This is highlighted in

Table 1 by the identification of only two quarries that have been producers of

soft sand; Star Works in the North which retains permitted reserves and

Kingsmead Quarry which had some incidental extraction in the West. However,

with the closure of Kingsmead Quarry and Star Works being inactive, there are

no sites currently producing soft sand. This places a reliance on imports to

address the lack of local supply. A Soft Sand Study7 produced to support the

emerging Joint Plan highlights that soft sand is supplied by various mineral

planning authority areas in the wider Thames Valley area.

2.10 In contrast, sharp sand and gravel is more widely distributed throughout Central

and Eastern Berkshire.

2.11 Table 1 provides details of the aggregate extracted at each permitted site.

Table 1: Permitted active quarries in Central and Eastern Berkshire, 2019

Aggregate

Status in

Site Operator Sharp Sand &

Soft Sand 2019

Gravel

Aggregate Active

Horton Brook

Quarry

Industries/Jayflex x

Aggregates Ltd

Riding Court Active

Farm

CEMEX x

Sheephouse Summerleaze Active

Farm Ltd x

2.12 Sheephouse Farm, Horton Brook, Poyle and Star Works are located within the

Green Belt.

5

Horton Brook Quarry Application http://publicaccess.rbwm.gov.uk/online-

applications/applicationDetails.do?keyVal=P0UNO2NIKKC00&activeTab=summary

6

Poyle Quarry Application: http://publicaccess.rbwm.gov.uk/online-

applications/applicationDetails.do?keyVal=OYZQ75NI0QY00&activeTab=summary

7

Soft Sand Study (2020): https://www.hants.gov.uk/berksconsult

9Sand and Gravel Production and Sales

2.13 The sales of land-won sand and gravel in Central and Eastern Berkshire are

shown in Table 2. Whilst the overall trajectory of sales of the last ten years has

been increasing, sales have fluctuated over the 10-year period, with sales

peaking in 2011 and 2014.

2.14 More recently, sales of sand and gravel have shown a small but steady

increase since 2016. The sales for 2019 are 17 thousand tonnes higher than

2018 and the sales for 2018 are 20 thousand tonnes higher than 2017.

Table 2: Land-won sand and gravel sales in Central and Eastern Berkshire, 2010-2019

(Thousand tonnes, Tt)

Last 3 Last 10

Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 yr yr

average average

Total 611 852 631 590 920 751 469 491 511 528 510 635

Sales

Footnotes

Soft sand (SS) sales are contained with the total soft sand/sharp sand and gravel figure. SS

sales are so small they cannot be individually revealed

Source: Aggregate Monitoring Surveys, 2010-2019

Figure 3: Sales of land-won Sand and Gravel in Central and Eastern Berkshire

1000

900

800

Thousand tonnes

700

600

500

400

300

200

100

0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Year

Source: Aggregate Monitoring Surveys, 2010-2019

2.15 Figure 3 shows the sales of land-won sand and gravel in Central and Eastern

Berkshire since 2008. Following a period of decline, a modest increase has

been observed since 2016.

102.16 When compared to the sales for South-East England (see Figure 4), the trends

in Central and Eastern Berkshire appear to be broadly similar and follow the

pattern between 2009 and 2019. South-East figures8 for sand and gravel sales

estimate a decline in 2019 which contrasts with an increase in sales in Central

and Eastern Berkshire.

Figure 4: Sales of land-won sand and gravel in South-East England and Central and

Eastern Berkshire

Source: South-East England Aggregates Monitoring Report 2019

*South East sales figures are estimated for 2019.

2.17 Mineral planning authority boundaries do not influence the flow of minerals. The

market dictates that sand and gravel will be obtained from the cheapest

location for that material. Where the demand in Central and Eastern Berkshire

can be satisfied most efficiently and cost effectively from locations in other

areas, then it will.

2.18 Table 3 shows the consumption of aggregate both imported from external areas

and supplied from sources within Berkshire.

8

South- East England Aggregates Working Party Annual Report 2019 (January 2021)

11Table 3: Total consumption of Primary Aggregate in Berkshire, 2009 and 2014

Land Won Marine Sand Total sand Crushed Rock Total Primary

Sand and and Gravel and gravel Aggregates

Gravel

Berkshire 2009 2014

2009 2014 2009 2014 2009 2014 2009 2014

Imports (Tt) 298 98 353

152 396 505 861 1,161 1257 1,666

Consumption*

807 601 98 152 905 753 875** 1,161 1780 1,914

(Tt)

Consumption

45.3% 31% 5.5% 8% 50.8% 39% 49.20% 61% 100% 100%

%

Imports/

Consumption 36.93% 58.7% 100% 100% 43.76% 67% 98.40% 100% 71% 87%

%

Source: Collation of the results of the 2009 and 2014 Aggregate Minerals survey for England &

Wales (Department for Communities and Local Government).

*Consumption is determined by total sold internally plus total imported.

**The difference in import and consumption amounts are due to known historic inaccuracies in

the 2009 National Collation data and is not considered significant. There is no reported evidence

of further flows of crushed rock from Berkshire to other areas.

2.19 In 2014, Berkshire was producing 1051 Thousand tonnes (Tt) with sales split by

248 Tt sold internally within Berkshire. A further 548 Tt was sold in the South

East region, the principal destinations being Surrey and Buckinghamshire

(including Milton Keynes) and 255 Tt sold to locations elsewhere

(predominantly West London).

2.20 There is no marine-won sand and gravel produced within Berkshire as it is land

locked nor is there any crushed tock due to geological constraints. In 2014,

Berkshire was also importing 353 Tt of land-won sand and gravel.

2.21 Although it is not possible to determine exactly what level of these imports

reach Central and Eastern Berkshire, the movements need to be taken into

consideration as a when forecasting future demand.

2.22 Table 3 shows an overall increase in supply of primary aggregates from

sources within Berkshire during this period but also an increasing reliance on

Primary Aggregate imports.

3. Crushed Rock

3.1 Central and Eastern Berkshire does not have any natural hard rock resources

and therefore relies on imports of crushed rock such as limestone and granite

to meet demand for this type of aggregate.

3.2 Information from the BGS shows that Somerset is the dominant source of

crushed rock for Berkshire. Somerset has some 380 million tonnes of approved

12reserves of crushed rock (equivalent to 28.4 years landbank at the most recent

sub regional apportionment rate)9. While not all the quarries in Somerset whose

reserves are included in the landbank have rail connections, those that do form

a significant proportion of the total. Provided Somerset maintains its productive

capacity it is estimated that there are sufficient reserves available to supply

ongoing market demand.

3.3 The importation and consumption of crushed rock within Berkshire is captured

within the aggregate monitoring data. Data is only available for the wider

Berkshire area which shows that all the crushed rock that is imported into

Berkshire is then consumed within Berkshire (see Table 3). Therefore, there is

no reported evidence of further flows of crushed rock from Berkshire to other

areas.

3.4 There are currently no operational rail depots to receive crushed rock imports

within Central and Eastern Berkshire. As such, it is assumed that the area is

served predominately by the rail depots in the wider Berkshire area, most

notably at Theale, West Berkshire. All crushed rock is then transported by road

within the Plan area.

3.5 The West Berkshire Local Aggregate Assessment (LAA) (April 2019)10

identifies that a large proportion of the aggregate sold from the two rail depots

at Theale is then exported out of West Berkshire by road, to the other Berkshire

Unitary Authorities or surrounding Authorities. The LAA also states that there is

sufficient capacity at the rail depots for an increase in demand should this occur

in the future.

3.6 Whilst capacity does exist at these rail depots, Central and Eastern Berkshire is

fully reliant on the continued operation of these depots and any threat to this

provision would have a significant impact.

3.7 The crushed rock sales (from rail imports) in Berkshire and Hampshire

recorded over the last 10 years are detailed in Table 4.

9

Somerset Local Aggregate Assessment (Fourth Edition):

www.somerset.gov.uk/EasySiteWeb/GatewayLink.aspx?alId=124408

10

West Berkshire 2018 Local Aggregate Assessment (April 2019):

https://info.westberks.gov.uk/CHttpHandler.ashx?id=43576&p=0

13Table 4: Crushed rock sales from rail depots and wharves in Berkshire (Berks) and

Hampshire (Hants), 2010-2019 (Thousand tonnes, Tt)

10 yr 3 yr

Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

average average

Berks

& 1054 1215 1222 1090 1208 1565 1517 1733 2042 N/A N/A N/A

Hants

Footnotes

Source: AM Surveys

In 2018, 91% of the aggregates sold from wharves and rail depots were crushed rock, 6% were

marine aggregate and 3% were Land won Sand and Gravel.

3.8 Sales of crushed rock fell between 2008 and 2013, decreasing by 21%. Since

2013, sales have increased with a significant increase in 2017 which is likely to

reflect that one of the rail depots at Theale in West Berkshire which previously

imported cement has started to import aggregate11, this high level of increase

continued into 2018. Published data is not yet available to determine the sales

figure for 2019 and therefore, the current 10 and 3-year averages. However,

draft figures estimate that crushed rock sales increased at the rail depots West

Berkshire and sales were static in Hampshire12.

3.9 Somerset County Council have sufficient reserves to meet current needs and

do not foresee any likely issues that would affect the future supply of crushed

rock to the South East Region which includes Berkshire. Should future demand

increase, the issue lies with the capacity of the rail depots to manage a higher

level of imports, rather than with future supply.

3.10 The safeguarding of the rail depots at Theale, West Berkshire will be important

for Central and Eastern Berkshire to ensure a supply of crushed rock, unless a

suitable rail depot is located within the Plan area.

4. Marine-won sand and gravel

4.1 Central and Eastern Berkshire has no wharves for the landing of marine-won

sand and gravel. However, the Aggregate Monitoring (AM) 2014 National

Collation data (see Table 4) highlighted that Berkshire’s level of imported

marine-won sand and gravel represented 5.5% of the total primary aggregate

consumed in 2009 and this rose to approximately 8% in 201413.

11

Information provided in the West Berkshire Council response to the Draft Joint Minerals & Waste Plan

consultation (17/09/2018).

12

As reported at SEEAWP meeting 24/11/2020

13

Collation of the results of the2014 Aggregate Minerals Survey for England and Wales -

www.gov.uk/government/uploads/system/uploads/attachment_data/file/563423/Aggregate_Minerals_Surve

y_England___Wales_2014.pdf

144.2 Imports into Berkshire in 2009 were 98 Tt which equated to nearly 8% of the

total primary aggregates. This rose to 9% in 2014 with 152 Tt of imported

marine aggregate. As such, marine-won sand and gravel forms a small but

growing proportion of the overall supply of aggregate to Berkshire. Although, it

is not possible to determine exactly what level of this supply reaches Central

and Eastern Berkshire, it needs to be taken into consideration when

considering future demand.

4.3 The AM2014 National collation data provides details on the sources of the

imported marine sand and gravel and highlights that the main source is from

Greater London which suggests that this is marine dredged material that has

been landed at London wharves, probably by rail. The second greatest source

is Hampshire. This is material that will have been landed at Hampshire’s

wharves. It is likely that this material will have travelled into Berkshire by road,

but it is also possible that the mineral was transported via the rail depots in

Hampshire to the depots at Hillingdon.

4.4 Any additional provision would preferably be by rail. As with the importation of

crushed rock, there is no current evidence to suggest a need for increased

capacity at the rail depots surrounding and servicing Central and Eastern

Berkshire, although existing capacity should be safeguarded.

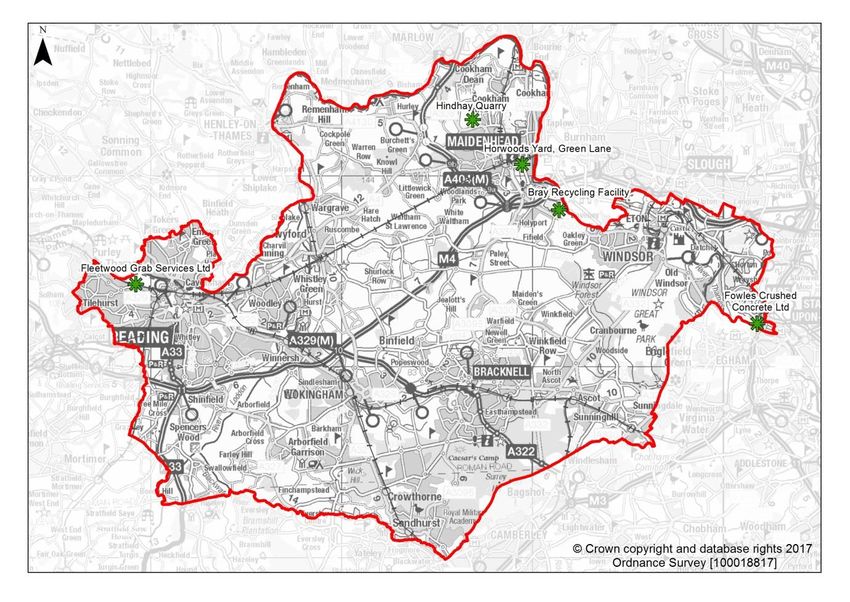

5. Recycled/Secondary Aggregates

5.1 Data pertaining to sales of recycled or secondary aggregates is collected

annually as part of the AM surveys carried out by mineral planning authorities.

Figure 5 shows the location of all active recycled aggregate sites in operation in

Central and Eastern Berkshire during 2019 that were surveyed. It should be

noted that whilst all sites were surveyed, not all responded. As such, the results

should be treated with caution and used to only indicate a general trend of what

is happening.

5.2 There are 6 sites which have been surveyed as producers of recycled and

secondary aggregates in Central and Eastern Berkshire. Of these sites, three

responded. Where capacity information has not been made available

Environment Permit information has been used (see Table 5).

15Table 5: Recycled aggregate capacity, 2019

Facility Name Unitary Authority Recorded(1) Estimated(2)

Capacity Permanent

(tonnes) 2019 Capacity

(tonnes) 2019

Datchet/Riding Windsor & Maidenhead 30,000 0

Court Farm

Hindhay Quarry Windsor & Maidenhead 25,000 0

Bray Quarry Windsor & Maidenhead 5,000 5,000

Horwoods, Kimber Windsor & Maidenhead 4,800* 4,800*

Lane

Fowles Crushed Windsor & Maidenhead 125,000* 5,000

Concrete Ltd

Fleetwood Grab Reading 75,000* 5,000

Services

Total 264,800 19,800

Source: (1) AM2019 returns, EA Permit (*) or Planning Permission where no return

information available. (2) Permanent capacity only and likely operational capacity.

5.3 The permission at Hindhay is temporary. The operational capacity at Fleetwood

and Fowles is likely to be similar to Horwoods as the capacities provided in EA

Permits are given as ranges or are for all activities on a site. Should this be the

case, the reality of permanent aggregate recycling capacity is likely to be

approximately 20,000 tonnes (75,000 tonnes temporary capacity).

5.4 Permission was granted for aggregate recycling at Riding Court Farm/Datchet

Quarry14 in 2018 which is time limited to the life of the Quarry but is currently

yet to commence production.

5.5 Figure 5 shows the location of active recycled sites in Central and Eastern

Berkshire.

14

Riding Court Farm/Datchet Quarry Application: http://publicaccess.rbwm.gov.uk/online-

applications/applicationDetails.do?keyVal=P5ZAR3NIJW700&activeTab=summary

16Figure 5: Location map of active recycled aggregate sites in Central and Eastern

Berkshire, 2019

5.6 The sales figures of the recycled and secondary aggregate in Berkshire for the

most recent 10-year period, 2010-2019 are shown in Table 6.

Table 6: Recycled and Secondary aggregate sales in Central and Eastern Berkshire,

2010-2019 (Thousand tonnes, Tt)

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 10 yr 3 yr

Year average average

Berkshire n/a 200 320 404 587 602 498 450 459 459 442 456

Central & 85 103 128 131 138 92 121

Eastern

Berkshire

Footnotes

Source: Aggregate Monitoring Surveys, 2010-2019

5.7 Sales for Central and Eastern Berkshire dropped significantly by 33% in 2019

breaking the previous trend of increasing sales.

5.8 Sales data for the Central and Eastern Berkshire area is only available for a six-

year period and which indicates a trend of 113 Tt per year. The Central and

Eastern Berkshire sales represent an average of 23% of the Berkshire Total. If

17this average was applied to the Berkshire 10-year sales, this would suggest a

10-year trend of 101 Tt per year for Central and Eastern Berkshire.

6. Future Aggregate Supply

6.1 The Central & Eastern Berkshire Authorities are working together to produce a

Joint Minerals & Waste Plan to supersede the Replacement Minerals Local

Plan for Berkshire adopted in 1995 and subsequently adopted alterations in

1997 and 200115. The current adopted Minerals Local Plan covers the

administrative areas covered by the Central & Eastern Berkshire Authorities, as

well as Slough Borough Council and West Berkshire Council. While this plan

covers the period until 2006, the Secretary of State has directed that several

policies in them should be saved16 indefinitely until replaced by national,

regional or local minerals and waste policies. For Central and Eastern

Berkshire, these saved policies will be replaced by the Joint Minerals & Waste

Plan, when it is adopted.

Construction project demands

6.2 Infrastructure projects that are likely to place an additional demand of future

aggregate demand in Central and Eastern Berkshire relate to both housing and

transport projects. There are in the region of 55,000 remaining new homes

projected within the area over the plan period, up to 203617. Using the updated

‘Standard Method for Housing Need’18 published in February 2019, the

requirement for Central and Eastern Berkshire over the plan period is in the

region of 46,000 new homes.

6.3 Other National Infrastructure projects within 30-50 miles of Central and Eastern

Berkshire include Cross Rail, the additional runway at Heathrow19,

improvements to the M25, M3 and M4, as well as the Datchet to Teddington

flood defences. A distance of 30-50 miles is the estimated distance over which

the majority of sand and gravel produced is transported.

6.4 All these projects are of significant scale and require the future demand to be

accounted for in future aggregate supplies, over and above the annual

15

Replacement Minerals Local Plan for Berkshire (2001) - www.bracknell-forest.gov.uk/replacement-minerals-

local-plan-for-berkshire-2001.pdf

16

Mineral Local Plan Saved Policies - www.bracknell-forest.gov.uk/mineral-local-plan-saved-policies-

schedule.pdf

17

SHMA (2016) – Berkshire (including South Bucks) Strategic Housing Market Assessment

18

Housing and Economic Needs Assessment (2019) – National Planning Practice Guidance

https://www.gov.uk/guidance/housing-and-economic-development-needs-assessments

19

On 27 February 2020, the Court of Appeal ruled the decision to allow the expansion was unlawful because it

did not take climate commitments into account. The future of the proposal remains unclear.

18infrastructure delivery programme. The emerging Infrastructure Delivery

Statements contain more information on the level of future development

planned for the area, which cumulatively will place additional pressure on

aggregate supplies.

6.5 The indication is of an increase in future infrastructure delivery in the Central

and Eastern Berkshire area, leading to an increase in future aggregate

demand.

6.6 To meet future aggregate demand, including the infrastructure projects

discussed above, Central and Eastern Berkshire needs to maintain a sufficient

aggregate landbank and a greater emphasis should be placed on encouraging

recycled and secondary aggregate sites to supply future demand.

6.7 Central and Eastern Berkshire is reliant on imports of aggregates, therefore

looking at sales of aggregate in isolation does not represent current demand.

Economic Forecasts

6.8 A range of growth forecasting approached have been utilised previously to

make an assessment of future demand.

6.9 This has included the MPA growth factor of 1.1% which was applied to the

sales figures, 3-year average and 10-year average, the forecasted figures over

the plan period. In addition, the construction growth rate of 1.4% was applied to

the same set of figures.

6.10 A Population growth factor of 5.725% was applied based on ONS figures for

the Berkshire area. Finally, GDP was looked at with a 2% compound growth

rate applied.

6.11 However, current aggregate figures have outlined that there is uncertainty over

the impact of the United Kingdom leaving the European Union (‘Brexit’) on the

economy and the effect on growth.

6.12 More recently, there has been concern over the impact of the national

emergency to the Coronavirus (COVID-19) pandemic on the minerals industry.

This is expressed clearly in the Minerals Products Association Press Release20:

‘Sales volumes of ready-mixed concrete and aggregates (crushed rock and

sand & gravel), two materials that are used across most types of construction

20

MPA Press Release (05/05/2020): https://www.mineralproducts.org/20-release15.htm

19work, declined by 5.7% and 4.0% respectively over the quarter. For ready-

mixed concrete, this follows three consecutive years of market declines since

2017, as Brexit-related uncertainties put a brake on commercial construction

work, notably for offices, whilst housebuilding slowed in the capital. Housing

and the commercial sectors have also been significantly impacted by the

COVID-19 lockdown, with most major housebuilders having closed sites

throughout the last week of March and April, and office construction impacted

by the collapse in business and consumer confidence. Simultaneously, mortar

sales, which are primarily used in housebuilding, fell by a further 1.6% in the

first quarter of 2020, after a 7.9% fall at the end of last year. The trend in mortar

sales volumes has been subdued over the past 18 months, a clear indication of

the underlying weaknesses in housebuilding even before accounting for the

impact of the COVID-19 lockdown.’ The press release suggests that the impact

of Brexit was already starting to have an impact at the start of 2020 on the

construction industry which supports the OBR forecasts.

6.13 These figures have been updated for the following quarter21, suggesting

unprecedented declines with aggregate sales (crushed rock -37%, sand and

gravel -39% and mortar -61.3%). The MPA state that the ‘swift closure of

housebuilding sites as the lockdown was announced in March resulted in the

mortar market suffering an even sharper fall in demand, with sales volumes

down by 61% over the quarter. Overall, the impact of the Covid-19 lockdown

has been worse than the financial crash between 2007 and 2009’.

6.14 The sand and gravel LAA Rate in 2018 of 0.628Mt was based on the 10-year

average which also echoed the five-year average.

6.15 In light of the current economic uncertainties, the 2018 LAA Rate of 0.628Mt is

being retained. Whilst sales figures increased in 2019 which increased the

three-year average, an increase in the forecast would not account for the

unprecedented decline in 2020. It is also recognised that with the

Government’s drive for housing and infrastructure delivery, sales will recover.

However, it is not yet clear the rate and shape of the recovery. Recent

permissions at Poyle and Land south of Windsor Road will enable sales

recovery once operational.

6.16 The recycled and secondary aggregate 2018 LAA rate was consistent with 3-

year average sales. This approach has been taken in 2019 and therefore, the

LAA Rate is 0.121Mt. This is a reduction from the 2018 Rate and reflects the

change in capacity. Bray Quarry has significantly reduced the recycled

21

MPA Press Release (03/08/2020): https://www.mineralproducts.org/20-release26.htm

20aggregate capacity. However, permission was granted for aggregate recycled

at Datchet Quarry which has not yet been activated.

Landbank

6.17 The NPPF22 requires Mineral Planning Authorities to make provision for the

maintenance of a landbank of at least seven years for sand and gravel. The

seven-year landbank stipulated is the absolute minimum level of provision

required and Mineral Planning Authorities should seek to maintain a landbank

above this level.

6.18 Reserves of sand and gravel in Central & Eastern Berkshire with planning

permission for extraction (permitted reserves) at 31 December 2019 were

7,407,000 tonnes (discounting Star Works as this is inactive).

6.19 Table 7 shows that a landbank based on 2019 sales figures is 14 years. Sales

were significantly lower in 2016 and 2017 than previous years resulting in a

higher landbank figure.

6.20 The total landbank for all land-won aggregate based on 10-year average is 11.6

years which is comfortably above the 7 years required by the NPPF. Based on

3-year average sales the landbank is 14.5 years which has increased due to

the lower sales in 2016, 2017 and 2018.

6.21 Application of the 2019 LAA Rate results in a landbank of 11.8 years.

Table 7: Central and Eastern Berkshire sand and gravel reserves and landbank 2019

Landbank based Landbank based

Landbank Landbank

Permitted upon 10yr upon 3yr

based upon based on

Reserve average sales average sale

2019 sales 2019 LAA

(Tt) between 2010- between 2017-

(years) Rate

2019 (years) 2019 (years)

Total

Sand

7,407 11.6 14.5 14.0 11.8

&

Gravel

Source: Aggregate Monitoring survey data.

18

National Planning Policy Framework (Feb 2019)

https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/810197/

NPPF_Feb_2019_revised.pdf

21Future provision of sand and gravel

6.22 The emerging Joint Plan period is up to 2036 and outlines a requirement of

5,447,000 tonnes of sand and gravel during the life of the Plan.

6.23 Poyle Quarry (the last remaining allocation from the adopted Plan in the area)

was granted planning permission in January 201923. An application for Water

Oakley, Holyport was permitted July 202024. Permission was refused in August

2019 for the extraction of 3.6mt at land known as Bridge Farm, Arborfield25.

6.24 A Proposed Submission Plan was produced, and a Regulation 19 consultation

undertaken between September and October 2020. The Plan contains

Development Management policies and allocations. The allocations included

two sharp sand and gravel extension sites, an aggregate wharf and one

aggregate recycling site. No soft sand sites were identified for inclusion in the

Plan. The proposed allocations are not sufficient to meet the identified needs

of Central and Eastern Berkshire and therefore, the allocations are supported

by criteria-based policies and in the case of sand and gravel, an ‘Area of

Search’ to enable further development proposals to come forward. It is

anticipated that the Plan will be submitted to Government during winter 2020.

6.25 There is no available soft sand sales data to determine what the future demand

of soft sand during the Plan period will be. A study was undertaken during

2019 to identify where soft sand is supplied from. It concluded that soft sand is

supplied to Central & Eastern Berkshire from a range of neighbouring

authorities and is not reliant on any one source.

6.26 As the Plan area is reliant in imports, sources of this supply will need to be

secured from elsewhere. However, neighbouring authorities such as West

Berkshire, Hampshire and Surrey have constrained soft sand resources due to

Areas of Outstanding Natural Beauty and the South Downs National Park.

Therefore, future supply may need to be considered from alternative sources

such as marine or brought into the Plan area from greater distances. However,

it is recognised that greater distances are less sustainable due to the transport

impacts.

23

Poyle Quarry Application: http://publicaccess.rbwm.gov.uk/online-

applications/applicationDetails.do?keyVal=OYZQ75NI0QY00&activeTab=summary

24

Water Oakley Application: http://publicaccess.rbwm.gov.uk/online-

applications/applicationDetails.do?keyVal=PHF8GVNI0CV00&activeTab=summary

25

Bridge Farm Application:

https://planning.wokingham.gov.uk/FastWebPL/detail.asp?AltRef=170433&ApplicationNumber=&AddressPref

ix=&Postcode=&KeywordSearch=bridge+farm&Submit=Search

22Capacity

6.27 Site capacity is included as part of the Aggregate Monitoring 2019 survey. By

understanding current capability of sites, through capacity, it is hoped that this

information can be used to assist planning for future demand. The results of

this are shown in Table 8.

Table 8: Total sales and estimated production capacity, 2019

% Sales / Capacity 3 yr

Sales (Mt) Capacity* (Mt)

Production average (Mt)

Land-won

0.528 1.11 47% 1.1

Aggregate

Recycled

0.092 0.148 62% 0.23

Aggregate

Footnotes

Source: Aggregate Monitoring Survey, 2019. Please note collecting capacity data from

operators in this manner is still in early stages and therefore the results should be treated with

caution

6.28 Capacity for both land-won aggregate has remained consistent over the three

years with just a small increase of 0.01Mt in comparison to the 2018 capacity.

Capacity for recycled aggregate is lower in 2019 than the three years average.

Looking at the data, this change is due to a reduced reported capacity in 2019,

which has resulted in an overall decrease.

6.29 It is possible to compare sales with capacity to understand void production

capacity. Table 8 indicates that for land-won aggregate, there is the potential

for sales to be on average over 50% higher than currently recorded, with sites

currently producing at an average rate of 47% capacity. However, land-won

sales are dictated by the needs of industry. But it does suggest that there is

sufficient capacity to accommodate uplift in demand as a result of future

development.

6.30 The returns data suggests that recycled and secondary aggregate sites are

also currently operating under capacity. There has been a significant reduction

in capacity since 2018 but overall, the indication is that there is still operational

capacity.

6.31 It is worth noting that not all operators returned information on capacity, and

therefore the capacity data provided is not 100% accurate.

6.32 Data on recycled aggregate is notoriously difficult to determine due to the

temporary nature of sites and the potential for unauthorised operations. The

23proposed recycled aggregate allocation at Riding Court Farm/Datchet Quarry26

in the Draft Plan was permitted in 2018 (subject to legal agreements). The

permission (30,000 tonnes per year maximum) is limited to the life of the

quarry.

26

Riding Court Farm/Datchet Application: http://publicaccess.rbwm.gov.uk/online-

applications/applicationDetails.do?activeTab=summary&keyVal=P5ZAR3NIJW700

247. Conclusions and review of the LAA

7.1 This LAA has shown that Central and Eastern Berkshire’s current local

aggregate provision will impact on the wider South East region as a whole if

new development is not enabled to meet the forecasted demand up to 2036.

7.2 There were no site closures in 2019 and only one planning permission granted

for Poyle Quarry during this period (January 2019), although this site remains

inactive.

7.3 Following consideration of current economic climate, the 2019 LAA Rate

remains at 0.628 mtpa for sharp sand and gravel.

7.4 Due to the lack of suitable resources, Central and Eastern Berkshire is reliant

on supplies from other mineral planning authority areas and as such will need

to be given consideration in other Mineral Local Plans through strategic cross-

boundary liaison. This could be supported by Statements of Common Ground,

which take into account the current sources of minerals whilst recognising the

constraints on resources in some neighbouring areas and the potential impact

this may have on future supply.

7.5 The need for any additional infrastructure, such as the further requirement for

land-won extraction, will be identified through the Joint Minerals and Waste

Plan and will be monitored through LAAs. Where it is not possible to identify

sufficient sites to meet the identified needs of Central and Eastern Berkshire,

the Joint Plan will contain enabling policies to allow further opportunities to

arise during the life of the Plan. The sand and gravel policy will be supported by

an ‘Area of Search’ to demonstrate the distribution of resources of sand and

gravel across the plan area to encourage suitable proposals to come forward

for consideration.

25A summary of this document can be made available in large print, in Braille or audio cassette. Copies in other languages may also be obtained. Please contact Hampshire Services by email berks.consult@hants.gov.uk or by calling 0370 779 5634.

You can also read