LONDON RESIDENTIAL REVIEW - LONG-TERM REWARDS, SHORT-TERM UNCERTAINTY WINTER 2015

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

RESIDENTIAL RESEARCH

LONDON

RESIDENTIAL

REVIEW

LONG-TERM REWARDS,

SHORT-TERM UNCERTAINTY

WINTER 2015

IMPACT OF TAX CHANGES MANSION TAX AND AREAS OF

THE LETTINGS MARKET OUTPERFORMANCE

KEY FINDINGS LONG-TERM REWARDS

New stamp duty changes add

OUTWEIGH SHORT-TERM RISKS

to short-term uncertainties but Growing uncertainty has caused demand to become more

are outweighed by strong longer-

term fundamentals subdued in the prime London market. As high-value property

comes under political focus in the short-term, the grounds

Annual growth in prime central for longer-term optimism remain strong, says Tom Bill.

London eased to 6.1% in

November, with the strongest At the start of 2014, the prime London Accordingly, the stamp duty changes have

increases away from traditional

residential property market was largely put a significant question-mark over the

prime areas

unaffected by the prospect of the viability of the mansion tax proposal.

upcoming UK general election. By the

With opinion polls indicating that a

Price growth of 9% in prime end of year, it was operating wholly in

majority government is unlikely in May,

outer London was led by the its shadow.

the uncertainty looks likely to continue in

eastern areas of Canary Wharf

and Wapping The impact of the election became the first half of 2015.

notable by Q2 2014, causing demand to

Whatever the result of the election,

become more subdued as uncertainty

Knight Frank analysis shows growth is unlikely to be as headline-

grew over the prospect of tax changes.

there are approximately 20,000 grabbing over the next five years as the

rental properties in London By November prices had begun to last five. This fact, however, should be put

with a capital value of more soften and in December Chancellor in the context of an exceptionally strong

than £2 million George Osborne increased stamp duty and prolonged period of growth that has

for properties above £937,500 in a produced a 73% rise in prime central

move designed to outflank his political London since the post-Lehman Brothers

Total returns for prime London

opponents five months from the election. low point in March 2009.

property far exceeded other

asset classes in the year to In the short-term, the stamp duty We forecast cumulative growth of 22%

October 2014 changes will lead to some harder between 2015 and 2019 as demand

negotiations between buyers and continues to exceed supply. Forecasts

vendors and instances where values may indicate the London population will grow

adjust downwards slightly to account for by in excess of 100,000 every year for the

the new higher charge. next ten years while it remains the city of

choice for the global wealthy.

Given the phlegmatic way in which the

London property market has reacted These longer-term fundamentals of the

to previous similar changes, history prime London property market are likely to

indicates it will absorb the changes in continue to underpin its future performance.

the short to medium-term.

However, the stamp duty changes have

FIGURE 1

also redrawn the parameters of a long-

standing debate surrounding the taxation Price growth in the year to

November 2014 (Rebased to 100)

of high-value residential property.

After numerous changes in recent years

110

that include capital gains tax reform

for overseas-based buyers and higher 108

taxation on ‘enveloped dwellings’, the

106

stamp duty changes mean it is now

TOM BILL difficult to argue that high-value property 104

Head of London Residential Research is under-taxed.

102

“The stamp duty changes A comparison of taxation in New York, PRIME OUTER LONDON

100

have redrawn the parameters Paris, Singapore and Hong Kong shows UK

PRIME CENTRAL LONDON

of a long-standing debate London is in the middle of the pack in 98

terms of property taxation. Stamp duty is

May 14

Nov 13

Nov 14

Dec 13

Aug 14

Sep 14

Mar 14

Feb 14

Jun 14

Jan 14

Oct 14

Apr 14

Jul 14

surrounding the taxation of

higher in both Asian markets while, unlike

high-value residential property.” London, New York residents are taxed on Source: Knight Frank Residential Research /

their global wealth. Nationwide

2LONDON REVIEW WINTER 2015 RESIDENTIAL RESEARCH

HAMPSTEAD

SALES RENTS

PRIME LONDON

3-month

Prime London sales and rental market performance, 1.6% 0.9% price change ISLINGTON

year to November 2014 SALES RENTS

12-month

4.9% -7.5% price change 3-month

0.0% -0.8% price change MARKET

Prime gross yield: 2.52% 12-month

11.2% 0.8% price change PERFORMANCE

NOTTING HILL Annual growth in prime central London was

SALES RENTS ST JOHN’S WOOD MARYLEBONE 6.1% in November, driven by residential

3-month SALES RENTS SALES RENTS

-3.5% 1.1% price change markets north of Hyde Park as well as

3-month

0.2% 2.1% price change

3-month CITY & FRINGE

-0.3% -0.1% price change Islington and City & Fringe in the east.

12-month SALES RENTS

6.6% 0.4% price change 3-month

12-month 12-month Buyers are seeking value away from

2.6% 9.5% price change 5.9% 10.9% price change 1.1% 0.7% price change

Prime gross yield: 2.97% traditional prime postcodes to the immediate

Prime gross yield: 3.66% Prime gross yield: 3.09% 12-month west, south and east of the park due to strong

10.8% 3.1% price change WAPPING growth in these areas which has driven prices

KENSINGTON SALES RENTS

higher in areas like the Hyde Park Estate.

SALES RENTS HYDE PARK ESTATE MAYFAIR 1.0%

3-month

0.7% price change

3-month SALES RENTS SALES RENTS We forecast cumulative growth of 22%

-1.5% 3.1% price change

3-month 3-month 12-month between 2015 and 2019 as demand

1.4% 0.0% price change 1.0% -0.5% price change 12.7% 3.9% price change

SOUTH KENSINGTON 1.4%

12-month

5.3% price change continues to exceed supply. However, a

SALES RENTS 12-month 12-month Prime gross yield: 3.10% trend among buyers to focus increasingly

12.9% 1.3% price change

3-month Prime gross yield: 2.62%

3.3% -4.1% price change CANARY WHARF on the right specification and facilities and

-0.6% 2.4% price change SALES RENTS

Prime gross yield: 2.69% less narrowly on the right postcode suggests

Prime gross yield: 2.01% 3-month

12-month 1.9% 1.4% price change overlooked residential areas like Bayswater,

5.8% 6.0% price change

Victoria, the City and the Midtown district,

12-month

Prime gross yield: 3.04% 13.9% 4.3% price change which includes Holborn, Covent Garden and

Bloomsbury, are likely to outperform the

Prime gross yield: 4.23%

prime central London average due to the

high-quality new-build pipeline in these areas.

KNIGHTSBRIDGE

SALES RENTS In prime outer London, growth in the eastern

3-month districts of Wapping and Canary Wharf

0.3% -0.1% price change

exceeded that in south-west London or

12-month Hampstead. Both eastern areas benefit

5.5% 0.2% price change

from their relative proximity to London’s

Prime gross yield: 2.41% RIVERSIDE two financial centres of the City and Canary

SOUTH BANK

SALES RENTS SALES Wharf, a series of high-quality new-build

CHELSEA 3-month 3-month schemes and the fact they have fewer

2.1% 0.0% price change 1.6% price change £2 million-plus properties that could be

SALES RENTS

3-month 12-month 12-month subject to a mansion tax.

0.9% 0.7% price change 10.9% -2.7% price change 10.2% price change

BELGRAVIA For the same reason, prices in Fulham have

12-month SALES RENTS

3.0% 1.3% price change Prime gross yield: 3.47% softened in recent months due to its high

3-month

0.9% 1.1% price change proportion of family homes between

Prime gross yield: 3.32% £2 million and £4 million.

RICHMOND 2.2%

12-month

1.8% price change

SALES Further afield in south-west London, prices

3-month Prime gross yield: 2.84% continue to be underpinned by a flow of

0.1% price change

FULHAM buyers from more central areas like Notting

12-month SALES RENTS Hill and Kensington seeking more space for

5.6% price change

3-month

-4.2% -0.2% price change their money.

BATTERSEA

12-month SALES RENTS

2.0% -0.4% price change

3-month

2.0% -1.2% price change

Prime gross yield: 2.97%

12-month

11.6% -4.1% price change PRIME CENTRAL PRIME OUTER

LONDON LONDON

SALES RENTS SALES RENTS

WANDSWORTH

& CLAPHAM 0.2% 0.7% 3-month 3-month

0.6% 0.1% price change

WIMBLEDON SALES

price change

SALES RENTS

3-month 12-month 12-month

3-month 0.9% price change 6.1% 2.9% price change 9.0% -0.3% price change

0.2% -1.4% price change

12-month

12-month 13.9% price change Prime gross yield: 2.92% Prime gross yield: 3.59%

6.3% 3.6% price change

Prime gross yield: 4.48%LONDON REVIEW WINTER 2015 RESIDENTIAL RESEARCH

MANSION TAX AND Tim Hyatt,

Head of Lettings

THE LETTINGS MARKET There has not been any clarification

as to whether the proposed

mansion tax would be the

In the five years since the possibility of a in the form of higher rents as landlords responsibility of the landlord or

mansion tax was first raised, the debate make their investment viable as opposed the tenant but our assumption is

surrounding its impact on the London to reducing maintenance budgets or that it will be the landlord.

property market has grown. trading out of the sector. Some landlords

However, there is a degree of

Politicians from all parties have criticised may re-invest in less expensive property,

uncertainty in the run-up to the

the plan for its disproportionate impact a move that could potentially drive

election and we are aware of

on London and Knight Frank analysis prices higher in lower price brackets instances of tenants asking to be

shows 74% of all £2 million-plus and impact affordability. protected from any liability arising

properties in Greater London are either The impact of higher costs would be from a possible mansion tax and

flats or terraced houses, demonstrating felt more strongly by young professional for that to be written into the

the mismatch between perception, in renters who have chosen to share tenancy contract.

particular the term ‘mansion’, and the

a house in areas like Wandsworth From a landlord’s point of view,

reality of the London property market.

or Clapham because of affordability any hit on their gross to net yield

After recent increases in stamp duty constraints in the sales market. calculations will be a deterrent,

for properties over £937,500, the particularly bearing in mind that

While the mansion tax debate has

questions over the feasibility of the yields in many instances are

remained in the realm of theory over only marginally higher than their

proposal have grown louder.

the last five years, strong price growth all-time lows.

Here, we examine the potential impact in areas like Wandsworth and Clapham

of a mansion tax on the London during the same period means many The impact in terms of pricing for

lettings market, which raises its own more properties are now in the £2 million- rental stock and to what extent costs

questions in terms of the proposal’s are passed on remains to be seen

plus price bracket.

unintended consequences. and will be dependent on the supply/

In both the sales and lettings market, demand dynamic at the time.

Knight Frank analysis shows there the uncertainty is likely to mount as the

are about 20,000 rental properties in election approaches.

London worth £2 million or more, which

represents about a fifth of the UK’s

housing stock in the price bracket.

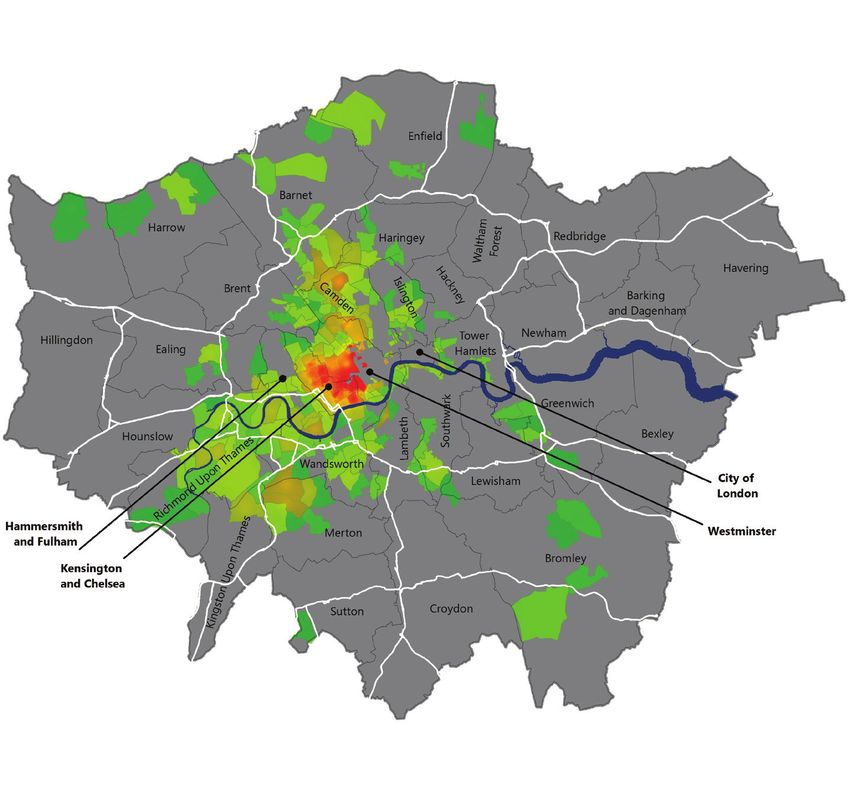

FIGURE 2

As the map in figure 2 shows, the highest Location of £2 million-plus rental properties in London

concentration is in the prime central

London boroughs of Westminster and

Kensington & Chelsea and there are

clusters in Camden and an area of

south-west London that stretches from

Hammersmith & Fulham to Richmond.

While the widespread assumption is

that any cost would be met by the

landlord, a degree of uncertainty will

inevitably surround the drafting of

lettings contracts until any new

legislation is enacted.

For landlords, any additional annual

cost would make their investment less

viable. This is especially true in prime

London, where the contribution of the

rental income is outweighed by capital

value growth in terms of calculating

total returns.

Rental properties worth £2m+

The impact would be particularly marked (% of total housing stock worth £2m+

by postcode sector)

when, as is often the case, landlords are High (Max: 36%)

also paying a mortgage on the property.

Anecdotally, some are suggesting Low

Less than 0.04%

tenants may ultimately absorb the cost Source: Knight Frank Residential Research

5GLOBAL BRIEFING

For the latest news, views and analysis

on the world of prime property, visit

KnightFrankblog.com/global-briefing

RENTALS AND INVESTMENT RESIDENTIAL RESEARCH

MARKET FOCUS Tom Bill

Head of London Residential Research

+44 20 7861 1492

The prime central London lettings market to bolster their loan books after the

tom.bill@knightfrank.com

has been in recovery mode since the start introduction of stricter lending criteria earlier

of 2014, with rental values rising 3.3% this year slowed the pace of loan approvals. HEAD OF LONDON RESIDENTIAL

between January and November.

Rental values above £1,500 per week in Noel Flint

It follows a shallow two-year decline against prime central London grew 3.8% between +44 20 7861 5020

the backdrop of a faltering economy and a January and November, while the figure was noel.flint@knightfrank.com

surging sales market. 2.9% for properties below £1,500 per week,

HEAD OF LETTINGS

reflecting how properties in higher price

In prime outer London, an annual decline Tim Hyatt

brackets are performing better.

of -0.7% in November 2013 had eased to +44 20 7861 5044

-0.3% by November this year though values The super-prime market, which covers tim.hyatt@knightfrank.com

remained largely flat over the 12 months. rental values of £5,000 per week and above,

is buoyant versus last year and indicates

Prime central London rental values have how relocation budgets are growing for the

been rising this year as the UK economy most senior positions in companies.

improved, though growth was zero in

November due to a seasonal slowdown Demand has also recovered strongly

and a degree of caution over economic since last year, as figure 4 shows, with

conditions in other parts of the world. the number of viewings, new prospective

tenants and contracts started and agreed

China cut interest rates for the first time in all rising strongly in the year to November

more than two years in November and there 2014 compared to the previous twelve-

is speculation the European Central Bank month period.

is getting closer to full-blown quantitative

easing, both of which will support their Rental yields in prime central London

respective economies. rose to 2.92% in November, continuing a

climb back towards 3%, a figure they last

Next May’s general election is adding to a surpassed 18 months ago. Meanwhile in

sense of uncertainty and wider optimism prime outer London, yields were 3.59%,

among companies is tempered to some their highest level in seven months.

extent by a number of profit warnings

Prime London property remained an

and regulatory uncertainty in the financial

attractive proposition for investors in

services sector. Knight Frank Residential Research provides

2014, with total returns in prime central

In a further move that may dampen short- and prime outer London markedly higher strategic advice, consultancy services and

term demand, mortgage lenders have than other asset classes despite the forecasting to a wide range of clients worldwide

cut rates as the likelihood of an imminent backdrop of global economic uncertainties, including developers, investors, funding

interest rate rise recedes and they attempt as figure 3 shows. organisations, corporate institutions and the

1.6% public sector. All our clients recognise the need

for expert independent advice customised to

FIGURE 3 FIGURE 4 The rental recovery their specific needs.

Prime London property outperforms Year to November (2014 vs 2013)

other asset classes Knight Frank Research Reports are available at

Total return (year to October 2014) KnightFrank.com/Research

43.8% 43.8%

39.513.9%

% 39.5%

9.4%

3.5% © Knight Frank LLP 2014

0.7%

22.4% 22.4% This report is published for general information only and not to

19.9% 19.9% be relied upon in any way. Although high standards have been

used in the preparation of the information, analysis, views

and projections presented in this report, no responsibility

or liability whatsoever can be accepted by Knight Frank LLP

for any loss or damage resultant from any use of, reliance on

PRIME PRIME HEDGE SHARES or reference to the contents of this document. As a general

CENTRAL OUTER FUNDS (FTSE100

LONDON LONDON (HFRI -10.5% total return report, this material does not necessarily represent the view

1.6% composite

index) COMMODITIES

index) of Knight Frank LLP in relation to particular properties or

(S&P GSCI index) projects. Reproduction of this report in whole or in part is not

allowed without prior written approval of Knight Frank LLP to

TENANCIES TENANCIES NEW VIEWINGS the form and content within which it appears. Knight Frank

AGREED COMMENCED APPLICANTS TENANCIES TENANCIES NEW VIEWINGS LLP is a limited liability partnership registered in England

AGREED COMMENCED PROSPECTIVE

TENANTS with registered number OC305934. Our registered office is 55

Baker Street, London, W1U 8AN, where you may look at a list

Source: Knight Frank Residential Research Source: Knight Frank Residential Research of members’ names.You can also read