LPs and Zombie Funds in - Private Equity Investment

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

LPs and Zombie Funds in

Private Equity Investment

This report was prepared by Stefano Migliorini (MBA Class, July 2014) in the first half of 2014 under the supervision of Claudia Zeisberger, Academic Director of the Global Private Equity Initiative (GPEI) and Professor of Decision Sciences and Entrepreneurship and Family Enterprises at INSEAD, and Michael Prahl, Executive Director of the GPEI. The data presented was extracted from Preqin. We wish to thank them for their engagement with GPEI and support on this project. GPEI welcomes private equity investors interested in the centre’s research efforts to reach out to us in Europe or Singapore. For further information on INSEAD’s Global Private Equity Initiative, please visit www.insead.edu/gpei.

Introduction and Overview

Through the last cycle following the global financial crisis (GFC), stagnant

economic growth in mature economies, greater economic and political

uncertainty, increased sovereign risks, and a reduction in the amount of available

bank financing led to a significant reduction in the performance of the private

equity (PE) industry overall. In response to lower performance and higher

uncertainty, many investors (limited partners or LPs) reduced their allocations to

PE funds raised by fund sponsors (general partners or GPs). As a result, a

number of well-known PE firms had to delay fund-raising or reduce their fund-

raising targets.1

The difficult fund-raising environment extended to the mid and lower mid-market,

where a number of firms struggled and failed to raise follow-on funds. While for

the most part this occurred out of the public eye,2 it did not go unnoticed by the

LP community. In June 2013, Preqin estimated that there were about 1,200

“zombie funds”– PE funds managed by sponsors unable to raise a follow-on fund

– which had some $116 billion under management.

Zombie funds present a range of issues, chief among them a lack of resources to

execute the fund’s mandate, misalignment of interests between GPs and LPs,

and capital trapped in non-performing funds. The aim of this report is to explain

how LPs approach zombie funds in their portfolios and how GPs are managing

the situation. It draws on insights from interviews with LPs and service providers

such as lawyers and placement agents.

We start by describing what constitutes a zombie fund and the typical PE

incentive structure that can lead to conflicts of interest between GPs and LPs.

We then address the zombie fund issue in more detail, delving into (1) the

magnitude of the problem in LP portfolios, (2) the nature of the problem (why LPs

decide not to reinvest in certain GPs), (3) how LPs are addressing the problem,

and (4) steps that GPs can take to increase their chances of successfully raising

a follow-on fund. To illustrate our findings we have included several case studies

highlighting specific points and recommendations.

We hope that our comprehensive overview of this under-studied but topical issue

in the private equity industry will be of use to both LPs and GPs facing issues

resulting from zombie funds, and that our findings will help improve the efficiency

of the capital allocated to this asset class.

1

As an example, both Permira and Apax reduced fund size by about 50% and fell short of their fundraising goals.

2

Notable exceptions include Candover and Duke Street.PRIMER: PE Fundraising and Fund Incentive Structure

To understand the zombie fund issue, we begin by describing the fundraising

challenge faced by the PE industry following the global financial crisis, as well as

the incentive structure of a typical private equity fund.

Post-Crisis Fundraising Falls

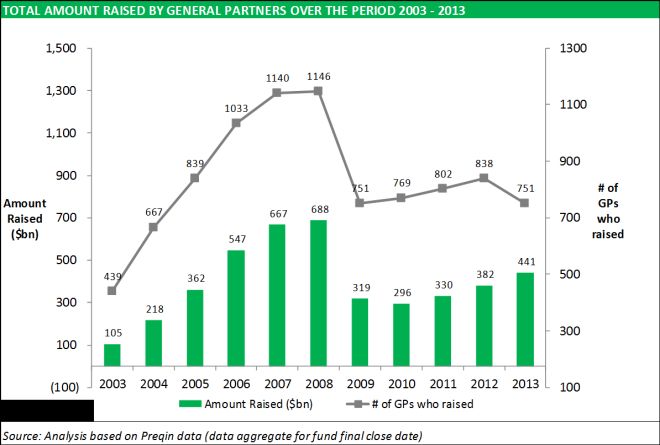

Before the GFC, the PE industry experienced what has been dubbed ‘the golden

age of PE’, with fund-raising and deal-making reaching record highs. Between

2003 and 2008, annual PE fund-raising grew at a CAGR of 46%, reaching a

combined $2.5 trillion for the five year period ending 2008. The boom saw a

sharp rise in average fund size as well as in the number of GPs that raised funds

(more than 1,100 GPs in both 2007 and 2008).

As the chart shows, the GFC had

a significant negative impact on

PE fund-raising, both in terms of

the amount of funds raised and

the number of PE firms raising a

fund. While fund-raising has

picked up significantly from its

lowest point, the number of GPs

raising a fund has stagnated,

reflecting LPs unwillingness to

back smaller and first-time funds,

preferring to direct their allocations to established GPs.

The fallout from the GFC was felt

differently across the regions.

Funds raised by European and

North American buyout firms fell

most steeply, reflecting the

negative headwinds facing these

economies in the wake of the

crisis. While the GFC was not the

undoing of the PE industry, as

some commentators had foretold,3 the sharp fall in fund-raising resulted in a

large number of PE firms unable to raise a follow-on fund. As a result, the

number of zombie funds rose dramatically.

3

For example, BCG’s (2008) Get Ready for the Private-Equity Shakeout never materialized.PE Fund Incentive Structure

To see how potential conflicts of interests arise between LPs and GPs in the

case of a zombie fund, it is important to understand the incentive structure of a

PE firm. There are four main sources of revenue:

Management fees: Management fees, the primary source of income for

GPs, cover all the expenses incurred by the PE firm including salaries,

day-to-day operating costs, and the cost of monitoring portfolio

companies. They typically range from 1.3% and 2.5%, and are assessed

on a different basis at different stages in the fund’s lifecycle, according to:

o committed capital during the investment period, typically 3 to 6

years following a fund’s first close, and

o the lower of i) invested capital, and ii) the fair value of the existing

portfolio following the expiry of the investment period.

Carried interest: Carried interest represents a ‘performance’ fee, usually

equal to 20% of the capital gains realized from a fund’s investments.

Carried interest is payable to the GP after a hurdle rate or preferred return

is realized by the fund’s LPs, typically 8%. If the hurdle rate is not reached,

no carried interest will accrue to the GP. Carried interest can be assessed

on a deal-by-deal basis (an American-style waterfall), or on the overall

fund favored by LPs (a European-style waterfall), as all capital committed

to a fund must be returned before a GP is entitled to carried interest.

Deal fees: Each time a GP completes an acquisition or an exit, it may

charge a deal fee, typically between 0.5% and 1.5% of the deal’s equity or

the enterprise value. Charging deal fees was common practice until a few

years ago, when LPs started to exert more pressure on GPs to improve

their fee structure. Management fee offsets, a mechanism now typically

employed via limited partner agreements, minimize the impact and

subsequently the frequency of deal fees.

Monitoring Fees: Once an investment is made, many GPs charge a

monitoring fee, paid by the portfolio company, for consulting and advisory

services, which accrues directly to the GP or an affiliated entity. The object

of the service will depend on the specific situation. Fees are typically

charged every year for the duration of the investment. As with deal fees,

management fee offsets can significantly reduce the impact on LPs net

realized fund performance.Focus on Zombie Funds

Post the financial crisis and the global economic downturn, performance in the

private equity industry fell sharply, evidenced by a reduction in the median

internal rate of return (IRR) for global buyout funds from 19.5% to 10.5%. 4 The

GFC’s impact on lower performing funds was no less dramatic – the median IRR

for third quartile buyout funds fell from 10.5% to 6%. As a result of poor

performance and a decreased appetite for investing in PE funds following the

crisis, the number of managers who failed to raise a follow-on fund increased.

The graph below details the prevalence of zombie funds as of year-end 2013.

Each annual data pair reflects the number of funds and amount of capital by

managers who have not raised a new fund from the date indicated. For example,

the “2008 or before” dataset indicates that 379 funds with commitments of $217

billion dollars are by firms unable to raise a follow-on fund.

AMOUNT RAISED BY GENERAL PARTNERS BEFORE A SPECIFIC DATE

$bn/# of funds

$400bn 379

$350bn

$300bn

$250bn 223

$217bn

$200bn

$150bn

108

$95bn

$100bn

56

$50bn 19 $35bn

$3bn $11bn

$0bn

2004 or before 2005 or before 2006 or before 2007 or before 2008 or before

Last Fund raised

# of Zombie Funds # of Zombie Fund GP

The “2008 or before” dataset assumes a PE fund becomes a zombie fund after a

five year period during which the PE firm did not raise a follow-on fund. This is

broadly in line with the 4-5 year investment period of most PE funds and the

follow-on fund-raising that typically occurs (or is at least underway) towards the

4

Performance reflects global buyout funds from pre-crisis vintages (2001-2004) and post-crisis vintages (2005-

2008). Source: Preqin.end of that period.5 According to this dataset, there are currently 379 ‘zombies’

managing funds with committed capital of $217 billion. If we take a more

conservative approach and assume that PE firms can delay fund-raising by

another year without major economic consequences, then we count 223 zombies

managing funds with committed capital of $95 billion, as reflected by the “2007 or

before” data set in the graph.

The data on called capital and unrealized value for all global buyout funds

between 2005 and 2008 allow us to estimate the amount of capital currently

under management by zombie funds raised in 2008 or before. The median

buyout fund from these vintage years has called 93% of the capital committed

during fundraising, with 74% of it still invested in portfolio companies as of year-

end 2013.6 By applying this to our broader data set, we can estimate that zombie

funds raised in or before 2008 are currently managing portfolios with an

unrealized value of approximately $150 billion. If we apply the same methodology

to zombie funds raised in or before 2007, zombie funds are currently managing

about $63 billion in unrealized investments.7

Turning our focus to GPs that raised buyout funds in the US and Europe – the

markets most affected by the global financial crisis – we find that 999 US and

European firms in the Preqin database have raised a total of $1.5 trillion since

2003 (inclusive). This represents approximately 86% of the total capital raised by

the 1,468 GPs for buyout funds globally in the past 11 years. Of this, 295 GPs –

or roughly 30% of the population – manage zombie funds raised in or before

2008, with $180 billion of total capital committed.8 By applying capital called and

unrealized value data from the 2005 to 2008 vintage year fund set, we estimate

that US and European-based GPs zombie buyout funds raised in or before 2008

are currently managing approximately $124 billion in unrealized investments.

GPs # of Zombie Unrealized Avg. Per

Headquarter GPs Value ($bn) GP ($m)

US 155 69 443

EU 140 55 393

Total 295 124 419

5

Over 53% of PE funds have an investment period of 5 years, according to Preqin. Source: Schwartz, P. A. and

th

Breslow, S. (2014). Private Equity Funds: Formation and Operation (5 ed). New York: Practising Law Institute.

Accessed from: https://www.pli.edu/product_files/EN00000000049875/93868.pdf.

6

Source: Preqin Performance Analyst – Custom Benchmarks

7

This estimate is based data on called capital and unrealized value for all global buyout funds with vintages

between 2005 and 2007, as above. The percentage of called capital was 94% and unrealized value equal to 70% of

called capital. Source: Preqin Performance Analyst – Custom Benchmarks

8

This total can be divided further, with 155 US-based GPs managing funds with capital commitments of $100

billion, and 140 European-based GPs managing funds with $80 billion in commitments.ZOMBIE FUND DYNAMICS Reasons why LPs lose confidence in a GP To understand the nature of a zombie fund, we need to understand why GPs are unable to raise a follow-on fund. Based on interviews conducted with LPs, service providers and placement agents, and former employees of Motion Equity Partners and BS Private Equity, the main reasons why GPs fail to raise a follow- on fund are: 1) LP’s loss of faith in the GP 2) Underperformance 3) Significant changes (turnover) in the investment team 4) Unclear succession plan LPs’ reduced allocations to private equity and a narrower investment focus (e.g. limiting private equity exposure to a specific geography) were also cited. Among the above factors, loss of faith in the investment team was the most prominent explanation for not reinvesting with a GP. Some LPs said they would consider backing a GP with an underperforming fund provided they still trusted the team and the reasons for the underperformance had been identified and addressed. The crucial role played by the team and other people in an allocation decision is underlined by points (3) and (4) above. GP Incentives: Potential Conflict Once it’s apparent that a large number of LPs are struggling with any of the above issues, the GP’s chances of finding enough fresh money to successfully raise even a reduced follow-on fund are small. This puts the GP’s last fund(s) squarely on the path to becoming zombie funds and introduces a number of potential conflicts of interest between a fund’s GP and its LPs. In the case of a strong-performing, well-regarded fund, whose GP is confident of raising a follow-on fund (or even an underperforming fund with the ability to raise a follow-on fund), the incentive structure described earlier will align the interests of GPs and LPs. The need to show strong early realizations and attractive time-weighted returns (IRRs or similar) in order to successfully raise a fund incentivizes the PE firm to exit from portfolio investments in a timely fashion. Any incentive to hold onto portfolio investments to maximize

management fees and carried interest is eliminated.9 For a GP, the ability to

raise a new fund improves the visibility of a future source of regular income

(i.e. the management fees on a new fund) with carried interest opportunities

from prior funds providing an opportunity for substantial performance-driven

gains.

However, when a fund is underperforming (i.e. poor performance that

indicates a fund will not reach its hurdle rate) and a GP fails to raise a new

fund, the incentive structure can give rise to a major conflict of interest

between GPs and LPs. Where the probability of collecting carried interest from

a fund is low – and lacking visibility of possible fees from a future fund – GPs

must rely solely on current management and monitoring fees as their main

source of income. As a result, exiting investments promptly would reduce their

fee-based income and could necessitate restructuring (such as lay-offs) to

adjust the GP’s cost structure. Hence there is no tangible incentive to do so.

LP Fallout

In addition to affecting the GP’s continuity and survival, the quality of the team

and investments can be negatively impacted by a zombie fund, and in turn

hurt the returns to LPs. If a GP with an underperforming fund perceives

dwindling investor support for a future fund-raising effort, a number of things

may happen:

- The revenue structure may incentivize the partners of the GP to

prioritize their own interests at the expense of those of LPs in the way

the existing portfolio is managed. To preserve the management fees,

the GP may postpone exiting from investments, or in distressed situations

inject new equity to stop the banks taking over portfolio investments due to

breach of covenant. In this way, the GP avoids the “step down” in

management fees when an investment is exited or written down.

- The investment team can quickly evaporate. As soon as investment

professionals see no future for a struggling GP, they are likely to quit or

start looking for a new job, undermining commitment to the fund. The best

tend to leave first; less experienced, less skilled professionals stay longer.

Hence the quality of the team in which the LP originally ‘invested’ declines.

9

As long as the IRR (of the fund or investment depending on the carried interest model) remains

comfortably above the hurdle rate, GPs have an incentive to hold portfolio companies longer to

maximise absolute dollar gains.- The management of portfolio companies may lose faith in the GP.

Portfolio company management may be willing to work more for the

interest of financing banks (for highly leveraged transactions) or to push for

a change of shareholding structure to increase the company’s prospects

and opportunities.

- Advisors’ commitment to the GP wanes. Advisors who know that a GP

will not raise a new fund may provide better service to other funds once

they perceive a reduced potential for business from the zombie fund.

These adverse events may result in:

1) A lack of commitment and attention to portfolio management

2) Higher management fees (paid by LPs)

3) A delay in capital distribution to fund LPs, reducing the time value of the

investment

4) Lower exit valuation as a delayed sale may necessitate a semi-forced

exit with lower bids (the sale will be orchestrated by a disenchanted

fund manager with little incentive to maximize value).

Given the above scenario, it is critical for LPs to address the problem of

zombie funds.LP Solutions: Managing Zombie Fund Investments To minimize the prevalence and impact of zombie funds on PE portfolios, LPs have two options: (i) short-term actions to address specific instances of zombie fund investment, (ii) long-term actions that help them avoid investing in potential zombie funds. Short-term actions Based on our interviews, we identified four possible actions for LPs when invested in a zombie fund: 1) Restructuring the terms of the fund 2) Selling a majority of the portfolio to a secondary investor 3) Sale of the GP 4) Removal of the GP Each alternative is illustrated by a case study below.

Option 1: Restructuring of Fund Terms

This option envisages the review and alteration of certain terms of a PE fund’s

limited partnership agreement (LPA) to reduce any conflict of interest between

the LPs and the GP, and to re-incentivize the team. The following measures are

common restructuring techniques:

- Reset of Carried Interest: Carried interest is often substantially reduced in

percentage terms – for example from 20% to 5% – but calculated on the basis

of a fund’s fair value at the time of restructuring (not considering the initial

cost). A hurdle rate – typically in the range of 8% – is usually included in the

restructured terms.

- Management Fee Review: To avoid any conflict of interest whereby GPs

extend the holding period of fund investments to maximize management fees,

LPs may ask to establish a fixed management fee until the fund term expires.

The percentage is usually set in a way that ensures attractive enough fund

economics for the GP to maintain the structure/ team required to manage the

existing portfolio.

- Fund Extensions: These are granted for two reasons: (i) to allow the GP to

market fund assets without being perceived as a forced/distressed seller, and

(ii) to allow enough time for an improvement in performance of fund

investments after a downturn/negative economic cycle.

- Team Review/Restructuring: In some cases LPs ask for a restructuring of a

GP’s investment team – in return for the types of concessions mentioned

above – and the implementation of a retention plan at all levels to ensure

stability in the investment team.

Although these options make a lot of sense for both the GP (as it realigns its

interests with those of its LPs) and LPs (as the cost of the reviewed terms is

often lower than the potential loss in value of the portfolio resulting from an

uncommitted GP), according to those we interviewed, LPs are often reluctant to

agree to restructured terms. They cited the following reasons: (i) LPs are

unwilling to set a precedent which might prompt GPs in similar conditions to ask

for restructuring, (ii) LPs who have lost faith in a GP do not want to “reward”

perceived adversarial behaviour.CASE STUDY: Cognetas Fund II10

GP Overview: Cognetas was an independent pan-European PE firm founded in

2001, following a spin-off by partners from Electra Private Equity. It principally

invested in controlling stakes in mid-sized companies in the UK, Germany, Italy

and France – out of offices in London, Paris, Frankfurt and Milan. The firm raised

two funds, a €1 billion fund in 2001 and a €1.3 billion fund in 2005.

Background: After delivering tier-1 performance on Fund I, a second fund raised

in 2005 underperformed. In the midst of fund-raising for a targeted €2.5 billion

Fund III in 2008, the global financial crisis struck. As the majority of the

investments from Fund II were made with high leverage between 2006 and 2008,

the impact was severe and the firm was forced to write off a number of portfolio

investments. Fund II performance fell below 1.0x multiple of invested capital. As

a result, Cognetas was unable to raise a follow-on fund when Fund II’s

investment period expired in 2011. The existing portfolio of Fund II was

composed of seven companies in the UK, France, Italy and Germany. As

speculation about the firm’s ability to raise a follow-on fund mounted, the existing

portfolio attracted a number of bids from other players, including Charterhouse,

all of which were rejected by the fund’s LPs.

Actions taken: As soon as the Cognetas’ management team realized that a new

fund was not forthcoming, it started focusing on alternative options for Fund II

with its LPs. By rejecting the offer from secondary players and Charterhouse, the

LPs confirmed their support for the GP’s team and their belief in the potential

upside in the existing portfolio. In December 2011, fund LPs reached an

agreement with the GP to restructure the existing terms of the fund by resetting

carried interest and stabilizing management fees. However, the GP was forced to

downsize its operation by closing its Frankfurt office, reducing its team in London,

and refocusing on Italy and France. The restructuring of terms realigned the

interests of Cognetas and Fund II LPs and stabilized the team to ensure sound

management of the existing portfolio.

10

Source: https://realdeals.eu.com/article/19616Option 2: Sale of Portfolio to a Secondary Investor Under this option, the majority of fund LPs’ interests are sold to a secondary buyer that becomes the main – if not sole – LP in the fund following completion of the deal. It typically occurs when: (i) there is disagreement among LPs on what to do with a fund’s GP, (ii) most LPs want or need liquidity, and (iii) the GP has the credibility to continue managing the portfolio and to eventually raise a new fund. In many instances zombie funds are run by solid teams and good investors who made mistakes that were amplified by external events like the GFC or unanticipated shifts in the team. For many LPs it is too complex to sell these “difficult equity stories” to their internal committee: they must have good reason to retain a fund that has clearly underperformed. As a result, many LPs prefer to drop the fund and refocus on better-performing GPs, leaving an opportunity for players to acquire the portfolio of a zombie fund – possibly at an attractive price. CASE STUDY: Motion Equity Partners GP Overview: Motion Equity Partners is a rebranding of Cognetas (Case Study 1), a mid-market Pan-European PE firm with €1.3 billion under management. The GP was rebranded after Cognetas completed a restructuring with its LPs and reshuffled its management team in 2011. Background: Despite the successful reset of terms highlighted in Case Study 1, the restructured fund continued to struggle under the weight of a second market disruption, the European sovereign debt crisis. After the initial restructuring, the firm operated out of just two offices in Milan and Paris, with a small investment team and no fresh capital to pursue new deals. The sovereign debt crisis produced additional headwinds, which made the restructured exit timing and valuations accepted by fund LPs in 2011 unrealistic, thus requiring further action. Actions Taken: After a (reported) unsolicited approach by CPPIB to purchase the existing portfolio in summer 2013, LPs launched a formal process to sell the portfolio with the help of placement agent Rede Partners. Harbourvest, a secondary investor, purchased the majority of the portfolio from fund LPs. The terms of the sale also included a second restructuring of fund terms, as Motion Equity Partners was reported to have secured a two-year extension to the existing fund, a new set of fund incentives, and fresh capital to invest in new deals. This gave Motion Equity another opportunity to prove its ability as a fund manager. Meanwhile, initial fund LPs were able to exit a complex situation that had required a second round of restructuring. Finally, Harbourvest benefited by investing in a promising portfolio with a short duration, as most of the assets are expected to be sold within the next three years.

Option 3: Sale of the GP Another option available to LPs is to strongly encourage the GP to reach an agreement with another established GP to merge operations in the hope of stabilizing the investment team, mitigating the risk of a conflict of interest arising in the management of the existing portfolio, and increasing the investment team’s ability to raise a new fund. CASE STUDY: Duke Street GP Overview: Duke Street is an independent PE firm initially founded in 1988 as Hambro European Ventures; the firm changed its name to Duke Street after it was bought out in 1998. The firm principally invests in established mid-market pan-European businesses, with a core focus on majority investments in UK and French companies. Although it considers most sectors, it has a particular interest in business services, healthcare, financial services, and consumer products and services. Since its founding, the firm has raised four funds for a total of approximately €2.8 billion. Its last fund, raised in 2006, had committed capital of €963 million, well above the €850 million fundraising target. Background: Duke Street fund performance has been disappointing since 2005. According to Preqin, the fund raised in 2006 delivered significant losses, with a cash-on-cash return of 0.56x as of year-end 2013. Despite these headwinds, the GP tried to raise a fifth fund of €850 million in 2012, but did not enjoy LP support and was unable to raise fresh capital. In February 2012, following unsuccessful fund-raising, Duke Street announced its intention to proceed under a new investment structure, raising equity to finance deals on a deal-by-deal basis. In April 2012, Duke Street announced an investment in LM Funerals, the first under its new strategy. However, GPs often struggle under a deal-by-deal structure as it does not offer long-term stability. Similarly, LPs often question the credibility of GPs executing this structure and the stability of a team not supported by the income of a committed fund. Actions Taken: In June 2013, Duke Street announced that it had sold 35% of its shares to Tikehau, a Paris-based investment firm. The deal allowed Duke Street to stabilize its firm and raise fresh capital to invest in new deals. This step was expected to improve investors’ confidence in Duke Street’s long-term viability, enable it to pursue a deal-by-deal model in the short term, and eventually raise a new fund in the medium term. In December 2013, Duke Street announced the successful acquisition of Homecare Business.

Option 4: Removal of the GPs An extreme measure is the removal of the GP by the fund’s LPs. A typical LPA includes a no-fault removal clause that allows LPs to terminate the GP’s mandate to manage the fund at any time, subject to the payment of a pre-agreed penalty often equal to 18 to 24 months of the management fee. Based on feedback collected from interviews and from the case studies available, this option is rarely, if ever, pursued. Removing a fund’s GP can often be more risky and expensive than maintaining the status quo. If LPs do decide to exercise this right, they not only have to pay the management fee penalty but also hire a new GP at 2+20 market terms. Moreover, the new GP will know less about the portfolio than the departing GP and will take time to get up to speed. For these reasons, LPs only remove a GP in extreme situations, e.g., (i) they lose faith in the GP, or (ii) when key members of the GP experience serious legal problems. One interviewee stated: “Trust is one of the most important asset a GP has. Gaining such trust is difficult, but losing it may also be difficult. For this reason, I believe that a GP has to really misbehave to force its LPs to exercise the no-fault removal.” CASE STUDY: BS Private Equity Fund Overview: Founded in 1990 by Messrs. Balbo and Sala, BS Private Equity was one of the largest Italian private equity firms. The GP raised four funds in total for approximately €1 billion, the last in 2003 at €550 million. BS primarily invested in manufacturing and service companies in Italy through management buy-outs, buy-ins and development capital. Background: Fund performance before and after the GFC was disappointing. According to Preqin data, the last two funds delivered negative returns: 0.9x for the 1999 vintage fund and 0.82x for the 2003 vintage. Against this backdrop, the GP was unable to raise a fifth fund. As a result, BS opened negotiations with potential secondary buyers, but failed to reach agreement. Actions Taken: In October 2011, the LPs of BS Private Equity – led by an advisory committee composed of HarbourVest Partners, Adams Street Partners and Danske Private Equity – decided to fire the GP per a “no fault” divorce clause, terminating the GP’s mandate without there being a breach of contract. This was the first time in seven years that a European GP had been removed from running a fund without breaching the terms of its LPA. Sources say it was driven by both the negative performance and the perceived absence of commitment of senior management. Following the removal of the GP, LPs awarded the mandate to Synergo, an Italian GP managing a €200m fund.

Long-term Solutions

In addition to the short-term solutions highlighted in the previous section, an LP

can take steps to strengthen its screening process to avoid allocating to weak

GPs. This section focuses on the actions LPs can take when allocating capital to

GPs to reduce and mitigate the risk of having zombie funds in their portfolio.

From our interviews, LPs can take one of three different paths:

1) Review the fund structure / LPA for new commitments

2) Strengthen portfolio monitoring to identify risks at GPs early

3) Back managers with multiple funds

Option 1: Review Fund Structure / LPA:

The link between invested capital and a fund’s management fees after the

investment period has expired is the main source of conflict of interest between

the LPs and the GP. Possible solutions to mitigate this problem are:

- Review the fee structure upfront. For primary commitments, the typical

2+20 PE fund fee structure can be adjusted in a way in which the

management fee will reduce by a fixed amount following expiry of the

investment period. This will reduce the GP’s incentive to postpone the sale of

the existing assets.

Although this may be regarded as a viable option, most of the practitioners

interviewed agreed that it would be difficult to implement. Interviewees felt

that LPs would prefer to deal with the zombie funds issue on a case-by-case

basis rather than adjusting all fund terms ex-ante and possibly incurring

higher fees. In addition, such a change would require broad consensus as

attempts to change a market standard might meet resistance from many GPs.

- Reduce threshold and penalty for GPs removal (no fault). In order to

remove a GP, a consensus among two thirds of the LPs is normally required

and a penalty equal to two years of management fees must be paid to the

GP. LPs are now pushing for lower thresholds – such as a simple majority of

LPs – and lower penalties ranging from 12 to 18 months of management fees.

This would increase LPs’ bargaining power when dealing with the GPs

managing a zombie fund and reduce the penalty for change.

- Reduce right to automatic extension. Today, most fund GPs can ask for an

automatic one year fund extension. LPs are now pushing to remove these

“automatic” rights, instead requiring LPs and/or advisory board approval for a

fund extension.- Review of Key Man Clause: As of today, some LPAs allow GPs to replace

key GP partners under certain circumstances. By doing so, GPs can reduce

the effectiveness of the initial team that an LP chose to invest with. Removing

the ability of GPs to replace these professionals ensures that funds will be

managed by the same team originally backed by the LPs.

Option 2: Strengthen monitoring to identify risks at GPs early

Several LPs mentioned that they are focusing more energy on identifying

investments in their portfolio that are at risk of becoming zombie funds early on.

By doing so, LPs might be able to sell their stakes in risky funds early on at a

higher price and avoid the need to manage a possibly complex situation.

Option 3: Back Managers with multiple funds

The issue of zombie funds usually materializes on standalone funds, i.e. GPs

that manage a single fund rather than a number of funds across geographies and

investment strategies. Managing multiple funds with separate revenue streams

mitigates the risk and potential conflicts of interest when one of these funds

underperforms. In addition, a GP with more than one fund will have a broader

reputational interest in maintaining goodwill with the LP community, as it plans to

continue raising follow-up funds for those executing successful strategies.

However, LPs interviewed felt that the benefits of backing larger platforms must

be traded-off against watering down the entrepreneurial spirit and expertise of

individual managers. GPs offering a platform of funds must continue to prove

they have the capability to produce superior returns across multiple geographies,

fund sizes and investment strategies, and the issue of zombie funds is not a

major decision factor when allocating or not allocating to them.

Implementation issues

While the previously described short-term actions are viable and actionable,

oftentimes LPs are unable or unwilling to take collective action. For most large

LPs, an allocation to a single fund will represent only a fraction of a multi-billion

dollar PE portfolio; this small relative size and LP resource constraints will often

minimize an LP’s ability to actively pursue solutions to a zombie fund. The

disparity of the investor group in terms of goals, resources and sophistication

makes it challenging to create the unified front required for negotiations with a

singularly focused GP. In addition, the need for LPs to maintain their own

standing in the PE community and not be perceived as heavy-handed investors

also hampers the decision-making process and collective action.GP Solutions: Managing Zombie Funds

Having focused on the LPs’ perspective, we now discuss what a GP managing a

zombie fund can do to improve its fund-raising capability. Among our

interviewees there was consensus that these GPs face an uphill battle, yet at the

same time most believed that, if properly managed, a GP may still be able to

raise a new fund. To do so, the GP needs to perform in the following dimensions:

trust, performance and equity story.

Preserve investors’ trust. For most interviewees, this was the most

critical factor required for successful follow-on fundraising. Preserving trust

can be achieved irrespective of the last fund’s performance by maintaining

professional conduct and transparency, and not acting against the LPs

interests for short-term, opportunistic gain.

Deliver positive performance on the remaining portfolio. There was a

strong degree of consensus among interviewees that performance is

critical. To have any chance of raising a new fund, the team needs to

deliver a strong performance on the remaining portfolio companies in a

zombie fund. Those still holding a number of portfolio companies with

several years remaining until a fund’s term have an opportunity to improve

performance and increase the chances of raising a follow-on fund.

Reframe the GPs equity story. While managing a zombie portfolio, a GP

must shape and define its positioning and strategy in the light of future

fund-raising. To do so, a GP must clearly identify its value proposition to

LPs and take action to remain consistent. This means retaining a team

with skills/experience relevant to the GP’s investment strategy and

achieving strong exits on deals that are most similar to the strategy of

potential follow-on funds. Effective marketing to investors requires that this

activity and the results achieved are clearly communicated to LPs.CONCLUSIONS The global financial crisis and its impact on both financial markets and economic performance was the main impetus for a sharp increase in zombie funds in the private equity industry. In addition to the negative performance engendered by the crisis, the zombie fund issue was exacerbated by record fund-raising among the GP community leading up to the crisis and reduced allocations to the industry in the years that followed. The main issue surrounding a zombie fund is the incentive for GPs to keep managing a portfolio beyond its optimal point, in order to maximize the economics at the expense of the fund’s LPs. LPs have a number of short-term levers at their disposal that can help resolve this conflict of interest. Based on our interviews with the PE community, the main levers available to LPs include (i) restructuring fund management fees and terms, (ii) selling the investment portfolio to a secondaries investor, (iii) pushing for a sale of the GP, and (iv) outright removal of the GP from the investment portfolio. Such actions/options are case specific, and the relationship and degree of trust between a fund’s GP and its LPs is a crucial driver of the corrective measures taken. More long-term, structural solutions can also be taken to mitigate the risk of investing in a zombie fund, including (i) restructuring LPA clauses at the outset of a fund commitment to reduce the potential for conflict, (ii) screening for weak managers in order to sell positions before a fund becomes a zombie, and (iii) backing multi fund managers. Although the global crisis led to a sharp rise in zombie funds over the past five years, it has not necessarily prompted greater involvement by LPs. LPs find it hard to find the time and resources to deal with zombie funds given the relative size of their exposure to such funds and any reputational damage which may arise from pursuing an active solution.

You can also read