MARKET COMMENTARY WINTER 2021 - ONWARD & UPWARD extraordinary 2020 - JFL Group

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

MARKET COMMENTARY J o efo rd L ee

CIM , CFP®, FCSI

Portfolio Manager, Investment Advisor

HollisWealth, a division of Industrial

WINTER 2021 Alliance Securities Inc.

Insurance Advisor, Hollis Insurance

ONWARD & UPWARD extraordinary 2020

We entered into the fourth quarter with

heightened trepidation. In typical fashion, October played

out as a volatile month but was followed by a strong

November rally after a muddied US Presidential election

and first COVID19 vaccine by Pfizer/BioNtech approved

for distribution. Although meaningful improvement to

normality is still months away, it was enough for the global

markets to finish on an upswing with a big asterisk on

2020.

The S&P/TSX Composite gained 2.1% in 2020

with most of the recovery coming from a sprint to the

finish line this final quarter. The index popping 8.1% with

the bounce in Energy 40.7% and Financial 16.8% Sectors.

The dividend yields of many financial services companies

and their reasonable forward looking valuations continue

to offer substantial value in a zero rate environment. The

pace of earnings recovery for energy and financials will Perhaps investors’ confidence was strengthened

likely follow the path of past recessions but the successful when a Republican President in the Oval office passed

vaccination of the population will shorten that time. This America’s first Basic Universal Income benefit. Crude

applies to commercial real estate which is too early to call oil prices briefly traded at negative values for the first

with the TSX Capped REIT index falling (13.08%) this time in history. This may also be one of the shortest

year. US Recession on record if the economy can avoid

Commodities as an asset class underperformed another contraction from this more devastating second

equities for the tenth straight year. In a world that has wave of Covid19.

seemingly transformed to a digital life, it has been a lost There was a very significant performance

decade for commodities. Performance of Precious Metals disparity this year based on some interesting data. The

were muted in this final quarter partly due to an improved country with the highest Covid infection and mortality

economic outlook however, it was still golden with bullion cases had one of the strongest stock market returns.

prices up almost 25% this year. While the S&P 500 is up 18%, the average stock in the

It is an understatement to say 2020 is a most index is up just 8%. This means the largest stocks in the

unique year in U.S. financial markets since the 2008 credit index are up a lot more than the smallest stocks. The

crisis. It started with rapid government mandated biggest component of the large cap US index is

shutdowns which triggered the fastest bear market in Technology with 27.7% representation, an increase

history with the Dow Jones Industrials plummeting 30% in from 24.2% just at the beginning of the Pandemic.

just 22 days to end the longest bull market in history. This This may not seem out of line until we think about the

market drop was followed by the fastest bull market in 15 typical retired conservative investor. A diversified

days declared on April 7th after propelling 20% from portfolio with almost 30% of the stock allocation in

March 23rd lows. Technology would be an exception rather than the rule.

… continues on page 2

PAGE 1

ONWARD and UPWARD MARKET COMMENTARY WINTER 2021

… continued from page 1

Value disciplined investors like Warren Buffet and negative-yielding bonds; investors have been forced to

Berkshire Hathaway (BRK.b) missed out on big returns in gorge on risky corporate bonds at record valuations.

this momentum market. Buffet’s BRK.b had only Current US Fed chair Powell is determined to keep

managed a gain of 2.4% in 2020. Similar traditional brick rates on the mat with a single minded focus of

and mortar businesses, stocks with the lowest P/E ratios, economic recovery. Their action of buying up junk

the lowest price to sales ratios, and the highest dividend bonds, Mortgage Backed Securities beyond Treasuries

yields underperformed stocks with the highest valuations will only encourage money flows to stocks and higher

and low or no dividend yields by a wide margin. risk speculation.

Investors with a case of FOMO (fear of missing

out) partied in IPOs like it was 1999. Debuts from big tech

and consumer names like Snowflake Inc., Airbnb Inc. and

DoorDash took this year’s initial public offerings volume to

a record $175 billion. The first-day return for IPOs

averaged 40% this year, the highest ever other than in

1999/2000. Additionally digital currencies were all the rage

with Bitcoin catapulting up 300% in 2020 almost doubling

its value just since mid-December.

Fans of Elon Musk celebrated more than a

successful SpaceX launch, Tesla stock had stratospheric

gains of more than 743% but this comes with trading at a

PE multiple of 1435x compared to 29x for S&P500. At

this level, investors are getting a feel on what a ride to Mars

with Elon is like. People are now buying and selling TSLA

at a higher volume than even the S&P 500 ETF. It is insane

to think that $1.2 Trillion in Tesla stock traded in the final

weeks of the year is more than Facebook traded in all of

2020. Incredible events shaped this year of global mayhem In Global Markets, 4 out of G7 economies ended in

but the best investment strategy this year was to be positive territory. China with the second largest

aggressive and buy the most expensive stocks and ignore economy has the fourth lowest P/E ratio (less

the cheapest stocks that pay a steady dividend. Only time expensive) among this select group of countries but it

will tell but the current market momentum is on the side of also has the highest forecasted GDP growth rate for

the optimists. 2021. Some notable countries with better growth

The market participants have friends in high prospects going forward are Malaysia, Hong Kong,

places. Like the aftermath of the Financial Crisis in 2008, Russia, and Singapore which top the list. The US

stocks got strong support from US government spending meanwhile ranks in the middle of the pack. Canada

and stimulus triggered from the severe economic shock of ranks ninth which expected growth is to be higher than

the pandemic. Central bankers around the world pushed the US. In the US, the Manufacturing and Services

borrowing rates so low that there are $18 trillion of global indices are back to pre-COVID levels.

… continues on page 3

PAGE 2

ONWARD and UPWARD MARKET COMMENTARY WINTER 2021

… continued from page 2

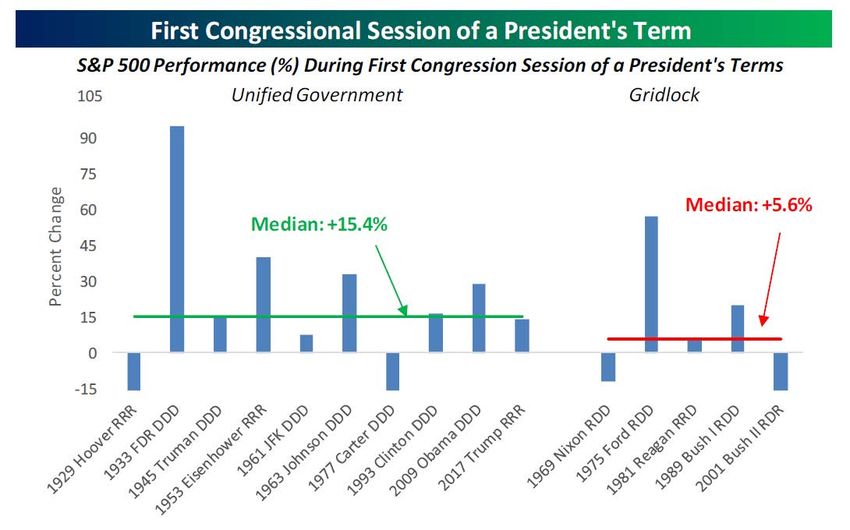

In fact, the US Manufacturing PMI is at its highest Highlights of the Presidencies with full control of government.

Obama's first term

level since September 2014 while the Services sector is at

Democratic majorities in the 111th Congress, 2009-11

its best levels since March 2015. On a global basis, while With strong majorities in both the Senate and House, Congress

Manufacturing has rebounded to its pre-COVID levels, the passed the Affordable Care Act, an aggressive economic stimulus

Services sector has not. package and the Dodd-Frank financial reforms.

You are probably like most people and feel

George W. Bush

enough is enough on US politics. It feels oddly

Republican majorities in the 108th and 109th Congresses, 2003-07

anticlimactic to say we have lived through one of the With narrow Senate majorities, Congress debated and approved

strangest Presidential elections in our lifetime and yet the the invasion of Iraq, passed tax cuts and approved aid in the

market was ‘meh’. The results of the election didn’t please aftermath of Hurricane Katrina.

everyone but the most positive outcome is that it is finally

Clinton's first term

over after years of political theatre. So now, what should

Democratic majorities in the 103rd Congress, 1993-95

we expect for the financial markets with a Democratic With strong majorities in the House and Senate, Congress passed

President controlling both The House of Representatives the Family and Medical Leave Act and transformed trade

and The Senate? relationships through NAFTA and other reforms on tariffs and

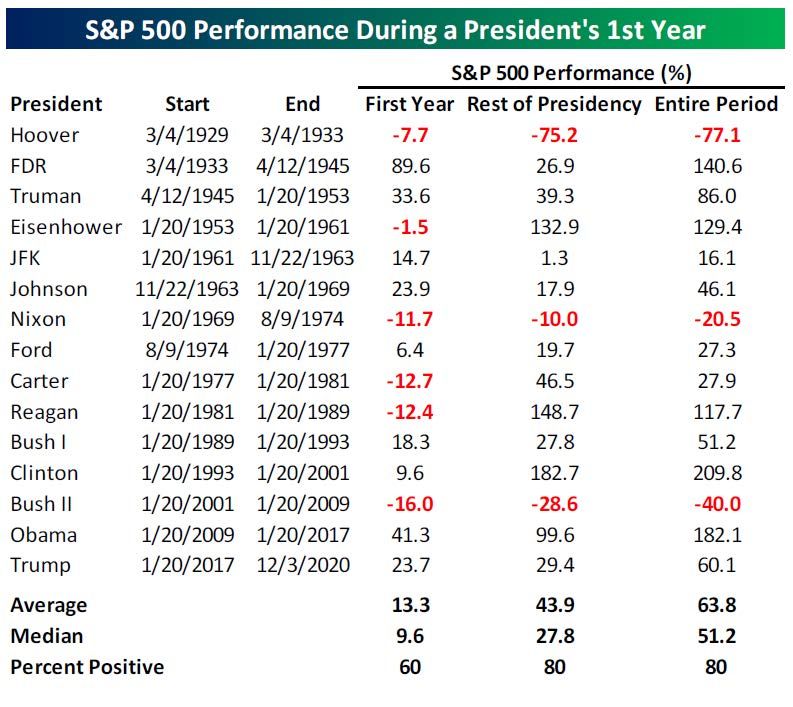

Historically, equities have rallied under trade.

Democratic Presidents, and the first year of a President’s

governance have seen a median gain of 9.6% with

positivity about 60% of the time. Since 1928, only Jimmy

Carter in his first term has the distinction of creating

negative S&P500 returns. While Democratic control of

the Senate is feared by market observers, full Democratic

control in Washington DC has typically been accompanied

by positive returns. Under Joe Biden, the Senate is a

virtual deadlock if not for the swing vote going to Vice-

president Elect Kamala Harris. This makes it unlikely for

extreme policy proposals to upset market participants. In

the end, markets care much less on politics than long-term

secular trends. This is just another distraction among all

the others that came before and coming after this new

administration.

Sources: Ycharts.com, theGlobeandMail.com, WSJ.com, Bloomberg, Bespoke Investment Group, Reuters.com, 1832 Asset Management L.P.

Disclaimer:

This information has been prepared by Joeford Lee who is an Investment Advisor for HollisWealth® and does not necessarily reflect the opinion of HollisWealth. The

information contained in this newsletter comes from sources we believe reliable, but we cannot guarantee its accuracy or reliability. The opinions expressed are based

on an analysis and interpretation dating from the date of publication and are subject to change without notice. Furthermore, they do not constitute an offer or

solicitation to buy or sell any of the securities mentioned. The information contained herein may not apply to all types of investors. The Investment Advisor can open

accounts only in the provinces in which they are registered.

HollisWealth® is a division of Industrial Alliance Securities Inc., a member of the Canadian Investor Protection Fund and the Investment Industry Regulatory

Organization of Canada.

Insurance products provided through Hollis Insurance.

PAGE 3

You can also read