National Space Technology Strategy - April 2014 Space

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Special

Knowledge

Interest

Transfer

Group

Network

Space

Aerospace & Defence

National Space

Technology Strategy

April 2014

Written By

The UK National Space Technology Steering Group.

Executive Summary

“We have a tremendous opportunity in front of us. We remain committed

to the goal of raising our share of the expected £400 billion global space-

enabled market to 10% by 2030. We have added an interim goal of

growing the UK space industry to £19 billion turnover by 2020.”

Andy Green, Space Growth Action Plan, 2014.

This document has been prepared by the UK National Space Technology Steering Group as

part of to the Space Innovation and Growth Strategy (IGS) 2014-2030 Space Growth Action

plan, to articulate a national space technology strategy that forms a crucial element of the

IGS delivery plan.

As future terrestrial technologies become increasingly unable to meet the needs of growing

international markets, there will be an increasing need for ‘Smart Space’ that is connected,

capable, adaptable, accessible and affordable. To achieve this vision a coherent set of key

aims have been identified:

• Smart and Connected;

• Lower Cost and Timeliness;

• Sustainable;

• Secure, Safe and Resilient;

• Forward Looking

This document sets out the vision, aims, technology themes and specific technologies

that will meet the needs of the IGS identified markets with the highest growth potential, as

illustrated below:

The realisation of the vision will involve, in the short term, the delivery of products and

services based on existing technologies, and in the medium to long term, the progressive

introduction of smart, potentially disruptive space technologies and services.

The successful implementation of this strategy requires a continued and deepening

partnership between government, academia and industry, enhancing uptake of STEM

subjects in education, and embracing innovative working practices.

Patrick Wood, Airbus

Ben Olivier, SEA Ltd

On behalf of the National Space Technology Steering Group

Supported by the Space Special Interest Group

2

Contents

1 Vision & Aims 4

2 Introduction 7

3 Background 8

4 Examples of current UK Strengths 11

5 Technology Themes 12

6 Linking to the Existing Five Space Technology Domains 13

7 Delivery 17

8 Appendices - Space National Technical Committee Updates 18

3

1 Vision & Aims

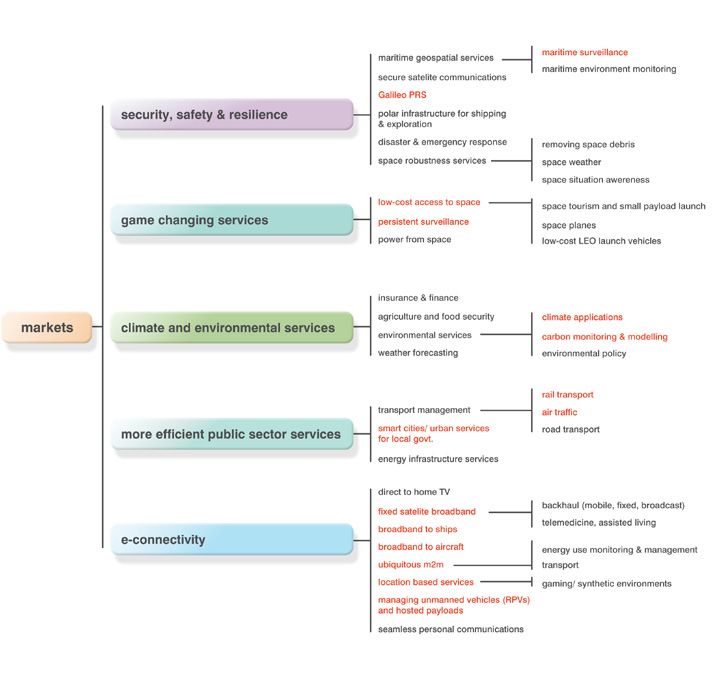

Space is a maturing and growing market sector and The Space Growth Action Plan detailed growth market

it is important that the UK influence, prepare for and opportunities and 15 priority markets where the UK has

embrace, the changes that lie ahead. It is vital that the the greatest opportunity to enter the space market and

UK positions itself to contribute to and benefit from stimulate growth (Figure 1). Each market is predicted

future ‘game changing’ technologies, in so far that they to be worth at least £1 billion annually to UK-based

can be predicted. To this end this report is intended to suppliers within 20 years.

guide both the Space IGS, and the implementation of

the Space Technology Roadmaps.

Figure 1 Space Action Growth Plan – Markets (Priority Markets identified in Red)

4

Smart Space – A Vision future potential that this opens up. Inspiring future

generations to expand knowledge and help make

As society moves from National to Global, it will no

the most of the resources that lie just beyond our

longer be acceptable to maintain the patchwork

fingertips today is an essential goal.

infrastructure of today. The intrusive and expensive

nature of surface-based solutions will become

antiquated within half a generation, giving way to

Imagine reaching into the universe with ease

capable, adaptable, accessible and affordable Space-

based systems. Going way beyond the excitement ...imagine a universe opened by Smart Space.

of today’s e-connectivity, with social and economic

benefits beyond imagination, the era of Smart Space is Access to these markets will come through the

rapidly upon us. Stories of large swathes of the planet systematic removal of barriers as well as through

remaining ‘unserved’ will be relegated to the history technology innovation. The UK Space Technology

books or to folk lore used by parents to amaze their Strategy provides a translation of the priority market

children. needs into a set of technology-enabled themes

which will provide the foundation for delivering the

Space Action Growth Plan. The aims listed in the

Imagine a world with no ‘not spots’ ...imagine a following table address the market opportunities

world enabled by Smart Space. that encompass “Smart Space – A Vision”. Figure 2

following the table illustrates the current and existing

barriers to be overcome in achieving these aims.

Looking out beyond our planet, it will be possible to to

reach, explore and understand our universe with all the

Smart & Connected

Why Broadband, Navigation, Surveillance, Climate Monitoring. Satellites need to be able to provide

assured coverage and availability and to be able to work with small devices on-ground build on and

enhance terrestrial technologies. Connectivity will unleash increased performance and versatility.

What • Autonomous, reconfigurable, adaptable and intelligent on-orbit platforms

• Inter-satellite communication, connected constellations of satellites, connecting a variety of on

orbit sensors and payloads, employing common interfaces and communication protocols

• Small and low cost ground assets

• Joined up approach of optimisation between space and ground elements

Lower Cost & Timeliness

Why Increased competitiveness of space solutions vs their terrestrial equivalents.

What • Delivery replenishment & servicing systems (launch & in orbit access)

• Changing the model from use and lose to launch, recover, re-launch

• Both on-orbit and ground assets

• modernise and simplify the institutional model to reduce cost & time

Sustainable

Why Competitiveness - avoiding increasing cost. Over the next twenty years we will see the gradual

transition to a new model where some or all space assets are designed to be serviced, reusable

or have constituent materials that are recoverable. If the model is not sustainable, then increasing

governance will drive costs up.

What • Replenishment, repair, servicing and disposal

• Debris removal

• Green & Sustainable technologies

Table 1: Aims within the Vision continued...

5

Secure, Safe & Resilient

Why Markets will demand increasing security, resistance to cyber-attack, the more dependent the

services become on space infrastructure. This is seen in how today’s terrestrial technology trends

and associated user requirements have evolved.

What • Surveillance

• Data Security & resilience

• Encryption

• Space Weather

Forward Looking

Why The requirement to proactively look for the next game changing and/or disruptive technology must

be serviced in any long term technology strategy. Technology advances at a frightening rate in

most sectors and therefore a key part of the national strategy must be to ensure that the technology

horizon is actively and constantly scanned.

What • Identifying future applications

• Technology Demonstration

• Space Science as a source of innovation, education and training

Table 1: Aims within the Vision

Figure 2: Aims and Barriers to be Overcome

6

2 Introduction

Space is a maturing and growing market sector and The Space Technology roadmaps helped to shape

it is important that the UK influence, prepare for and the initial technology delivery, but lacked detailed

embrace, the changes that lie ahead. It is vital that the prioritisation. However, this work goes on to deliver

UK positions itself to contribute to and benefit from a prioritised technology plan that identifies cross-

future ‘game changing’ technologies, in so far that they cutting technology themes (those relevant to multiple

can be predicted. To this end this report is intended to applications) with the potential for large market impact.

guide both the Space IGS, and the implementation of The strategic work and technology assessments carried

the Space Technology Roadmaps. out in the preparation of this report have focused on

high growth markets with greater emphasis on the

The 2010 Space Innovation and Growth Strategy (IGS) identification of cross cutting and ‘game changing’

required a National Space Technology Strategy and a technology areas. This plan is not confined to a

National Space Technology Programme. In response particular level in the supply chain but recognises its

Industry, Academia and Government have established a inherent connectivity. An assessment of our ability to

strong track record in planning technology delivery. Led reach the vision described earlier, has exposed gaps in

by industry, a National Space Technology Strategy was the UK supply chain, that this plan aims to address.

published, together with a set of associated technology The National Space Technology Strategy cannot

roadmaps, in 2011 and updated in 2012. Government be seen in isolation. ESA holds a European space

launched the National Space Technology Programme technology master plan which it rolls out though its

with £10 million in funding in 2011 and a further £25 technology programme and the EU has identified

million announced. It is estimated that the first £10 technological priorities for space as part of Horizon

million has already delivered a benefit of between 2020. Through, for instance, the Space SIG (becoming

£50m and £75m to the UK economy (Space Innovation a theme within the new look KTN) and the Satellite

and Growth Strategy 2014-2030 – Space for Growth – Applications Catapult the UK will ensure compatibility

published by Space IGS). with these wider initiatives and benefit from their funding

opportunities.

7

3 Background

Thanks to smart phones fuelling demand for mobile and reliably accessible launch services and systems

connectivity, the emergence of an ‘Internet of Things’, are critical in underpinning any economically driven

a rapidly growing range of data-driven services, the Space Programme, and therefore nationally developed

demand for global monitoring of our climate and the solutions are, and must be part of the Technology

near ubiquity of navigation-based products, our day to Strategy Agenda.

day relationship with space has changed more in the

past five years than in the previous four decades. Add to Earth Observation

this the UK’s track record in space technology together

Earth Observation provides valuable data about the

with its well-developed industrial sector and we have

Earth’s changing environment and also the validation of

both the driver and the capability for rapid and sustained

measurement techniques which can be used to develop

growth. We stand at the dawn of a New Space Age and

future commercial applications. Earth Observation has

thanks to many years of investment in space science,

spin-offs into other areas of terrestrial application such

earth observation and space technology, we are ready

as security and medicine.

to take advantage of this opportunity.

Earth Observation is an important tool in many

This ‘New Space Age’ must build on the infrastructure

international contexts, from weather forecasting to

that has evolved over the past forty years. That heritage

climate change and disaster monitoring. Commercial

is an undoubted strength: space works, and works

Earth Observation sometimes appears to sit a little

well. Yet we must be cautious of traditional models

awkwardly within this context with services being

that become a source of inertia, increasing complexity,

provided by a limited number of operators who are

slowing progress, keeping costs high and stifling

reliant on institutional funding for the majority of

innovation. The technological risk aversion of the major

their business. However, businesses recognise the

space institutions leads to very long programmes but

value of Earth Observation data – e.g. in the areas of

also to peremptory technology development (e.g.

precision farming, geological exploitation, insurance,

through its technology programmes) which often has

and shipping. There is a need to provide a range of

wider application. Bilateral programmes can lever

Earth observation services across differing markets that

engagement with 1st world and BRIC countries etc. and

integrate a mixed asset base that includes a variety of

also provide a rapid route to space demonstration.

satellite capabilities and orbits. Geostationary satellites

can provide near global and continuous coverage, but

The following paragraphs briefly describe the usage

the data may lack the detail required for many emerging

domains identified to be of key importance, and also

business applications, while low Earth orbit (LEO)

outlines the existing academic and industrial supply

satellite data provide the detail but are not continuous.

chain. Ground Infrastructure underpins the capabilities

Integrating and enhancing this EO capability e.g.

in all these areas.

through the creation of constellations in LEO and a

European Data Relay Satellite (the program by ESA

Access to Space

specifically to meet the demands of data upload from

Access to Space is principally about delivering LEO satellites) is a necessary way forward.

spacecraft into orbit, or launch services, but in the IGS

and National Space Strategy context, it also includes Navigation

the means to accommodate and support payloads,

Satellite navigation has become an integral part of

(experiments, sensors etc) in orbit and therefore

business and consumer life. Within the European

includes satellite platforms and associated technologies

context the Galileo programme is becoming established

such as transfer propulsion. The UK has a strong track

and there is now a need to exploit this capability through

record and capability in this area, with revolutionary

applications. Moreover, the next generation Galileo is

technologies such as the SABRE air breathing rocket

already under consideration with satellite programmes

engine under development and also a world leading

beginning in 2018 and the UK needs to prepare for

capability in developing short lead time, low cost

this new opportunity through the development of

satellite platforms. Whilst there is no current operational

enabling new technologies. Also of note have been the

capability in terms of conventional (chemical,

navigation augmentation payloads such as EGNOS

expendable rocket) launch systems in the UK, the core

and WAAS hosted on commercial telecommunications

expertise and knowledge is present, from historical UK

satellites. The UK has a very strong market share in

launcher projects such as Black Arrow and the newer

the commercial development and manufacture of

generation of launch systems pioneers engaged in

navigation-related technology and is very well placed

project such as SKYLON. Timely access to space for

to develop future mainstream and niche consumer

small payloads is currently problematic. The need to

equipment and applications.

share launches often leads to delay (such has been

the case for TechDemoSat and UKube-1). Affordable

8

The evolution of the Galileo capability is driven by a

number of key factors, such as increased platform &

launcher flexibility, robustness, service performance and

utilisation.

A strategy for navigation would include;

• developing applications and associated ground

technology to allow revenue earning from the

largely free navigation signals;

• long term technology development to ensure that

the UK will be a major supplier in future systems

Science and Exploration

Science and Exploration programmes address some

of the most profound questions (is there life elsewhere

in the universe? How were the Sun and Earth formed?

…). The UK has an outstanding track record in this

area with a breadth of capability in the area of sensing

and sensor data processing. UK-built instruments are

at the heart of most of the major European missions

and many of those of the USA, Japan and elsewhere.

These necessarily bespoke and challenging satellite

developments provide opportunity for innovation,

in-flight demonstration and training that feeds the

commercial sector. The science and exploration

programmes ‘spin-along’ technology developments

with other sectors for mutual benefit. It is essential to

maintain participation in a portfolio of space science

SAFER Field Trials © SCISYS Ltd

missions including large, long-timescale, observatory

class ESA missions, supplemented by shorter timescale

(e.g. bilateral) programmes, which have declined in

recent years. Science missions provide an important

inspiration factor in the training of the next generation of Secure satellite communication are an essential element

scientists and engineers. of all major national defence and security services and

represent a significant market opportunity. The four

Telecommunications Skynet 5 satellites, developed in the UK, provide secure

communications within the UK defence sector and

There are approximately 1,100 discrete

earn valuable revenue from sale of excess capacity to

telecommunications satellites in space, mostly

friendly nations. Work has now begun on defining the

in geosynchronous orbit (36,000km from Earth)

requirements and technologies for their successors.

providing services anywhere. Ubiquitous in broadcast,

satellites facilitate multiple applications as well as a

The UK Space Sector Supply Chain

host of ‘life support’ services ranging from maritime

communications to consumer broadband. The majority The differentiating characteristic of the current space

of this infrastructure is operated commercially, with supply chain is that one or more high-value assets are

time and bandwidth sub-let to third parties such as TV launched into space, at very great cost, maintained there

stations. The wider commercial market is becoming for a certain period, then discarded. Thus leverage of

increasingly competitive as many nations view satellite the supply chain’s efforts is a focus of the many supply

telecommunications as critical national capability, chain stakeholders – Government, Academia and

while nations such as China and India are recognising Industry.

telecommunication to be a valuable commercial

opportunity. It is therefore critical in the face of this The academic sector (e.g. University space groups

increasing competition, to support and preserve our interested in Earth observation, space science and

core strengths in payloads and platforms, and to bring space engineering) has been engaged with space

forward new and potentially disruptive technologies since the early 1950’s and much of our understanding

such as the all-electric spacecraft. of its particular challenges comes as a result of this

early investment. University and other research groups

9

develop enabling technologies for future missions and roll out this capability through knowledge exchange, teaching and training programmes as well as specialist services. The academic space sector continues to score well above its weight in all international science output assessments and inspires individuals into STEM careers. Space research provides a natural vehicle for technological innovation, international collaboration and associated commercial leverage and also spins out into many other sectors e.g. biomedical, aerospace and energy. Sustaining this aspect of Space alongside industry is hence essential for medium to long term growth. The space sector supply chain comprises technology creators (often within academia), component and equipment suppliers, prime contractors, launcher providers, satellite operators, ground segment providers including data processors and service providers. In all areas except launch services, the UK is already well established (see e.g ‘The Size and Health of the UK Space Industry, published by the UK Space Agency, 2010). The case is made below that the UK should increase its footprint in launcher technologies, – see Access to Space. Autonomous navigation © SCISYS 10

4 Examples of current UK Strengths

There are very many examples of UK excellence in the space sector at every level of the supply chain.

Given below are just a few.

The UK national programme NovaSAR-S is an innovative, low cost approach

to all weather synthetic aperture radar imaging. Based on an existing SSTL-300

platform the satellite is designed to operate either independently or part of a

small constellation. Its principle applications will include disaster monitoring,

ship detection, crop management and ice detection.

Contributions to the ESA ExoMars programme have enabled UK industry to

develop a lead in space robotics and in particular vision based navigation in

harsh environments. A series of successful trials in the Atacama desert have

demonstrated how robust the technology now is and is allowing its deployment

in other sectors such as mining, utilities and defence.

© SCISYS

The Eurostar 3000 telecommunications bus was developed with significant UK

support through the ESA ARTES programme and has gone on to form the basis

of more than 40 spacecraft development contracts worth more than 650 million

pounds to the UK, including the UK Skynet 5 and Inmarsat 4 series.

The UK leads the world in the development of future air-breathing rocket

engines and space planes. With £60m of UK government support and matching

private funding the Reaction Engines teams has begun its next phase of engine

and light weight heat exchanger development.

The Gaia spacecraft, launched in 2013 will study the dynamics of our galaxy

using the largest focal plane ever flown in space. 106 e2v charge couple devices

make up this 0.5 m2 structure and deliver almost a 1 Giga-pixel array.

Terrafix is a mobile computing and navigation system for the emergency

and security services that uses GNSS signals. The picture shows a typical

Emergency Ambulance; in all some 10,000 operational ambulances are

supported, and a single trust (out of14) attends 2000-3000 incidents per day of

7 minutes average duration. The system is high pressure, life critical, 365/24/7

and has enabled improvements in individual incident response times despite

reduction in the number of assets.

115 Technology Themes

The work of the National Space Technology Steering

Group and the Space National Technical Committees

sought to bring together the insights so that prioritisation

and cross cutting technology themes could be identified.

The insights included:

• Market research through the Space Innovation and

Growth Strategy (2014 – 2030);

• The Technology Roadmaps which detailed a range

of technologies across technology readiness levels;

• The space sector supply chain.

A review and mapping of these three “data sets”

provided insights into a series of cross-cutting themes

and specific technologies that, if focused on, will

produce capabilities that will allow the markets identified

in the IGS to be addressed, therefore enabling space

infrastructure solutions to be deployed. This will enable

the required revenue generating services, and hence the

economic growth required, to be delivered. LISA Pathfinder

The translation of the market requirements into

required capabilities, technology themes and specific

technologies, all under the banner of the overall vision

for the strategy is broadly illustrated in the figure below.

This also shows the role of the Technology Roadmaps

Referring back to the vision for the Technology Strategy,

the majority of the markets identified in the IGS can

be delivered through the establishing of a number of

constellations of on orbit assets (i.e. satellites), all of

which can work together in a coherent and transparent

manner, from the user’s viewpoint. This ‘neural’ network

could then make the full range of satellite services

achievable and accessible utilizing continental broadcast

to low latency single hop communications including

enabling 24-hour data relay for Earth observing satellite

constellations .This would provide the benefits of near-

real time data for personal and national use.

Figure 3 : Linking Markets to Technologies

126

Linking to the Existing Five

Space Technology Domains

The following 5 domains and associated National

Technology Committees relate to the usage domains

mentioned earlier:

• Access to Space

• Position, Navigation and Timing

• Robotics and Exploration

• Sensing

• Telecommunications

The National Space Technology Roadmaps are

contained within these five domains, and these

roadmaps identify which broad and specific

technologies are required in order to enable market

linked capabilities to be realised. Whilst some

capabilities are clearly satisfied by technologies

contained within a single domain, others require

contributions from multiple domains, and therefore a

robust mapping of the markets across to the roadmaps

as a whole is clearly required.

The following Technology Themes are identified as

key to realisation and delivery of the services required

by the priority markets. These themes can be applied

in a variety of combinations in order to provide the

capabilities required to deliver the services

• Sensors: Optical, Radar, Thermal

• Communication & Navigation Payloads: (Inter-

satellite and Space-Ground)

• Next Generation, Autonomous and Intelligent

Satellite Platforms: (For use in multiple and varying

orbits)

• Satellite Delivery Systems, i.e. Launch Vehicles &

Systems

• On Orbit Maintenance, Servicing, Disposal

• Ground Segment Infrastructure (including data

processing/mining) and User Terminals

• Data Security

• Future Applications

The table below identifies the technologies, by domain,

that are key to enabling the capabilities demanded by

the markets. All of these technologies are captured

in the current roadmaps, identified by the NTCs, and

therefore serve to inform the entire UK space industry

on which technologies are required to facilitate the

delivery of the IGS as a whole. In the main, these build

on existing technologies and capabilities.

Cyclone Nargis

13Nature & Magnitude of Development generation control systems and mobile terminals)

Programmes Required require relatively low levels of investment and time,

whilst others (such as launcher developments) would

Whilst the following tables indicate which technologies require orders of magnitude more in funding and many

are required to enable the market associated services years to be realised – these would also constitute major

and capabilities, they clearly do not give an indication development projects which would require review,

of the maturity of the technologies, nor the likely approval and funding mechanisms over and above

magnitude of the development programmes (in terms those within the perimeter of the UK’s government

of investment and time) required to realise them. Some space bodies.

of the technologies and capabilities (such as next

Technology Domain Specific Technology Technology Theme (Primary) Market Relevance

Low cost chemical propulsion for high

Launch Vehicles & Systems

thrust (small launch vehicle) systems All (Underpinning Theme)

Low cost chemical propulsion for lower

Satellite Platforms All (Underpinning Theme)

thrust (orbit transfer) systems.

Improved electric propulsion for orbital

Satellite Platforms All (Underpinning Theme)

transfer and station keeping

Systems engineering tools for launch

Launch Vehicles & Systems All (Underpinning Theme)

systems

Access to Space

Avionics for launch vehicles Launch Vehicles & Systems All (Underpinning Theme)

Lightweight and low cost

thermostructural materials with

Launch Vehicles & Systems, Satellite

potential both for game changing All (Underpinning Theme)

Platforms

reusable launch vehicles, and ultra low

cost expendable vehicles

Spacecraft platform designs that

enable miniaturisation and significant Satellite Platforms All (Underpinning Theme)

cost savings

Payload (Galileo and EGNOS) future Security & Safety, Public Sector

Communication & Navigation Payloads

development, Services

Galileo Public Regulated Service Security & Safety, Public Sector

Data Security

(PRS), encryption; Services

GNSS robustness and Interference Security & Safety, Public Sector

Data Security

Positioning, Navigation & detection and mitigation; Services

Timing

Ground Segment Infrastructure and

Advanced and innovative receiver Public Sector Services, Security &

User Terminals

development and commercialisation; Safety

Next generation EGNOS (V3) design,

Public Sector Services, Security &

implementation and services plus Communication & Navigation Payloads

Safety

associated Galileo Mission activities;

On Orbit Maintenance, Servicing,

Autonomous/Intelligent Vehicles Security & Safety

Disposal

On Orbit Maintenance, Servicing,

Robotic Manipulators Security & Safety

Disposal

Robotics & Exploration

Penetrators and Landers Game Changing Services

Robotic Support of Manned

Game Changing Services

Exploration

Table 2: Technology Development links to Markets

14Maritime surveillance, Disaster

Technologies for low cost radar management , Persistent Surveillance,

Sensors

systems, including NovaSAR Climate & Environment Services,

Security & Safety

Imaging systems with infra-red (IR) Climate & Environment Services,

capability -shortwave, medium wave Sensors Security & Safety, Smart cities ,

Sensors and thermal IR Maritime surveillance

Low cost imaging spectrometers

Sensing Climate & Environment Services,

for atmospheric greenhouse gas Sensors

Security & Safety, carbon monitoring

monitoring

Persistent Surveillance, Climate &

Detectors (IR and visible) for EO,

Sensors Environment Services, Security &

defence and surveillance

Safety, Smart cities, carbon monitoring

Climate & Environment, Services,

High performance computing, data

Satellite Platforms Smart cities, Disaster monitoring,

mining and image processing

Security & Safety

Public Sector Services, Security &

Next generation communications

Satellite Platforms Safety, E-Connectivity,

satellite platforms.

High throughput payloads for Public Sector Services, Security &

broadband, broadcast and fixed Communication & Navigation Payloads Safety, E-Connectivity,

services

Public Sector Services, Security &

Transparent and regenerative digital Satellite Platforms,

Safety, E-Connectivity

processors Communication & Navigation Payloads

Telecommunications

Public Sector Services, Security &

Analogue flexible payload equipment Communication & Navigation Payloads Safety, E-Connectivity

Communication & Navigation Public Sector Services, Security &

Advanced antenna solutions for

Payloads, Ground Segment Safety, E-Connectivity

broadband applications

Infrastructure and User Terminals

Ground Segment Infrastructure and Public Sector Services, Security &

Low cost terminals for business and

User Terminals Safety, E-Connectivity

consumer applications.

Table 2: Technology Development links to Markets

15The following table describes how the specific

technologies link to the aims. The majority of

technologies support multiple aims from the strategy.

Technology Specific Technology Area

Secure, Safe

Sustainable

Lower Cost

Connected

Domains

& resilient

Forward

Looking

Smart &

Access to Space Low cost chemical propulsion for high thrust (small launch vehicle) ✓ ✓ ✓

Lower thrust (orbit transfer) systems. ✓ ✓

Improved electric propulsion for orbital transfer and station keeping ✓ ✓

Systems engineering tools for launch systems ✓ ✓ ✓

Avionics for launch vehicles which build on UK strengths in low cost ✓ ✓

space craft avionics

Lightweight and low cost thermostructural materials with potential ✓ ✓ ✓

both for game changing reusable launch vehicles, and ultra low cost

expendable vehicles

Spacecraft platform designs that enable miniaturisation and ✓ ✓ ✓

significant cost savings

Positioning, Payload (Galileo and EGNOS) future development, ✓ ✓ ✓

Navigation & Timing

Galileo Public Regulated Service (PRS), encryption; ✓

GNSS robustness and Interference detection and mitigation; ✓ ✓

Advanced and innovative receiver development and ✓ ✓ ✓ ✓

commercialisation;

Next generation EGNOS (V3) design, implementation and services ✓ ✓

plus associated Galileo Mission activities;

Robotics & Autonomous/Intelligent Vehicles ✓ ✓ ✓ ✓

Exploration

Robotic Manipulators ✓ ✓

Penetrators and Landers ✓

Robotic Support of Manned Exploration ✓

Sensing Technologies for low cost radar systems, including NovaSAR ✓ ✓ ✓ ✓ ✓

Imaging systems with infra-red (IR) capability -shortwave, medium ✓ ✓

wave and thermal IR

Low cost imaging spectrometers for atmospheric greenhouse gas ✓ ✓ ✓

monitoring

Detectors (IR and visible) for EO, defence and surveillance ✓ ✓ ✓

High performance computing, data mining and image processing ✓ ✓ ✓ ✓

Telecommunications Next generation communications satellite platforms. ✓

High throughput payloads for broadband, broadcast and fixed services ✓

Transparent and regenerative digital processors ✓ ✓

Analogue flexible payload equipment ✓ ✓

Advanced antenna solutions for broadband applications ✓

Low cost terminals for business and consumer applications. ✓ ✓

Table 3: Links between specific technologies and Aims

167

The work to date has enabled the National Space

Delivery

• managing transition of technologies from non-

Technology Steering Group to provide a timeline of commercial to commercial markets, with relatively

technology needs with linkages to markets, including long return-on-investment times;

when interventions would best be provided. The work • encouraging new enabling technologies and

has identified priority technology themes including training through science/institutional investment;

specific technologies which could shape a national

• supporting SMEs as a catalyst for innovation.

technology programme, stimulate innovation and

interest in collaborative research and development, and

It is apparent that there needs to be a continued and

benefit from rapid in-orbit demonstration.

deepening partnership between Government and

Industry. Each stakeholder has an important role to

Further, these roadmaps have been generated by a

play and responsibilities to bear alongside the UK

wide range of experts, knowledgeable about European

Space Agency and industry will sit key actors such

capabilities. They achieve a balance between the

as the Technology Strategy Board, KTNs, the Satellite

ESA technology harmonisation process, associated

Applications Catapult as well as European bodies such

European roadmaps and commercial & strategic

as ESA and the EU.

UK needs. In this way, UK investment is targeted to

maximum effect, leveraging impact through alignment

Measurement of successful implementation should be

with European capabilities.

established by the UK Space Agency in the context

of the IGS targets, across the short, medium and long

In order to be successful, the right business

terms. Key metrics should be directly linked to the

environment must be created, the right delivery

realisation of the aims highlighted in the Smart Space

mechanisms need to be available and the right

vision.

investment decisions should be made at the appropriate

time. An increasingly sophisticated approach to

Realistically, everything on the roadmaps is unlikely to

technology funding is needed, taking full account

be afforded at the same time – either from the public or

of parameters such as market size and maturity as

private purses. Therefore, a phase approach will offer a

well as return-on-investment timescales. Government

practical model, leading to decisions on prioritisation.

intervention needs to take account of market and/or

The figure below shows an approach to a phased

technology maturity, with the aims of:

implementation, which recognises the situation today

• encouraging a commercially viable environment for and logical steps to be taken. The intermediate steps

private investment; provide measurable way-points for monitoring success.

• enabling self-standing, robust commercial

markets that do not require ongoing government

investment in order to make them viable;

178

Appendices - Space National

Technical Committee Updates

Robotics and Exploration • A thriving Cross Sectorial collaboration to enable spin in and

out of technologies between space and related sectors

Exploration and Robotics includes all types of robotics for the • A regular set of Field Trials and demonstrations held in

exploration of a planet surface as well as robotics used in orbit around appropriate challenging locations that help build confidence

the earth and the sensors needed by the platform for navigation or and show the applicability of systems.

control.

• European Centre of Excellence in developing technologies for

Exploration and Robotics is an area of the space industry that is driven Autonomous and Intelligent Systems.

heavily by technology and which faces huge challenges to achieve the

mission science goals. It is mainly concerned with upstream activities

R&E Vision Longer term (>10 years)

with very little direct downstream benefits to the space industry. It does

The technologies for these systems are becoming pervasive in

however have excellent potential for spin along activities allowing the

terrestrial applications, which can be characterised as dirty, dull and

spinning in of terrestrial technologies from other sectors as well as

dangerous. The facilities from the medium term vision are enabling

then spinning out the resulting technology advances. The very nature

technologies to be adopted and by building on those future space

of exploration of other planets requires cutting edge solutions to

missions such as Mars Sample Return are becoming more capable

successfully deploy robotics in remote and hazardous locations and

and cost efficient. The next generation of niche technologies include:

then operate them without ever having the option of human assistance

to perform repairs or recover from accidents. • Collaborative, and SWARM robotics - allow Exploration

Missions to be much more capable and collaborative either

From this market a strategy has been developed that builds on the between several robots or astronauts and robots.

existing excellence in certain niche technologies through to deployed • In-Situ Resource Utilisation mining of resources for use in

space and terrestrial systems that will generate growth. exploration of Mars, Moon etc

• Novel Locomotion Technologies – Includes aerobots, beneath

R&E Vision – Short term (Access to Space • Low cost chemical propulsion for high thrust (small launch

vehicle) and lower thrust (orbit transfer) systems. High thrust

Access to Space is principally about chemical propulsion test facilities. Improved electric propulsion

delivering spacecraft into orbit, or for orbital transfer and station keeping. Systems engineering

launch services. If the UK cannot If there is tools for launch systems.

one technology

guarantee regular, affordable

which symbolises

• Avionics for launch vehicles which build on UK strengths in low

and responsive access to any cost spacecraft avionics

Earth orbit, then our space the revival of a strong

British space sector it is • Lightweight and low cost thermostructural materials with

technologies and downstream potential both for game changing reusable launch vehicles, and

applications either become Launchers. Britain should

be at the forefront of the ultra low cost expendable vehicles.

irrelevant or entirely dependant

on foreign partners or suppliers.

next generation of launch • Spacecraft platform designs that enable miniaturisation and

and propulsion significant cost savings. Coupled with this, regular flight of

In this regard, access to space is

technologies. demonstration platforms to test new technologies in space.

unique in that it underpins all other

space markets: telecomms, robotics • Facilities and systems that can simulate the space environment

in particular low gravity: sounding rockets, drop towers &

& exploration, positioning navigation &

parabolic flights.

timing and sensing.

A supposedly free market exists for launch services, which to date Some of the above roadmap items , for example high thrust chemical

has provided the UK’s space industry adequate access to space. propulsion test facilities, thermostructural materials and sounding

Access to space is in reality highly political: launch service availability rockets also facilitate the SABRE advanced propulsion programme

and pricing, hence all space activity is controlled by the few nations and Skylon reusable launcher, where a large investment is already

that possess it. A further market feature is that large, traditional taking place outside of the NSTS.

spacecraft, ranging from commercial telecomsats to ESA science

missions benefit from oversupply of launch services: Growth based

on such ‘business as usual’ infrastructure will not meet UK targets,

unless a step change in access to space occurs. If the UK wishes to

grow its space activities, it needs independent control of its access to

space. Air breathing rocket engines and reusable single stage to orbit

spaceplanes such as Skylon could change the ‘business as usual’

scenario, but this approach carries many technical and market risks,

may take more than a decade to realise and does not match the UK’s

core competency in small satellites.

High thrust chemical propulsion (Airborne Engineering)

The value of small satellite technologies, low cost space missions and

their applications, from Earth observation to navigation are clear, and

represent one of the highest growth sectors in the space market. The

UK should continue to lead through development of next generation

small satellites, building on existing strong brands (2011 National

Space Technology Strategy). What is missing is a short to medium

term, low cost and with clearly defined risk, development of a UK

based small satellite launch service (UK Launch Space CITI study,

2013) The small satellite success of the UK, stimulated by BNSC’s

MOSAIC programme in 2000, was only possible because of low cost

launchers available from Russia. These launchers either no longer

exist or are only available in an irregular fashion that cannot support

the long term growth potential from small satellites. A UK small

launcher, a 21st century rebuild of Black Arrow but to a commercial

business plan with government infrastructure and development

support, will meet UK industry needs, can be developed from a UK

supply chain, and will not compete with current or planned European

launch infrastructure. This needs to be UK led due to the risks of

international partnership for a strategic, sovereign capability. UK

access to space in the short and long term, the industry ‘ask’ and

roadmap will require:

Vertical launch of sounding rocket (Newton

Launch Systems)

19Position Navigation and Timing 1. Security/resilience applications and services in the downstream

2. Payload integration capability in the upstream, in addition to

Position, Navigation and Timing technology has become embedded explicitly adding PRS as a standalone theme within the roadmap.

in many applications impacting societal challenges such as location

aware services, transport, timing and synchronisation and security The more widely accessible and profitable growth area is in the

and safety, and this will continue. Involvement in the Galileo and development of applications and services that use these technologies.

EGNOS programmes as well as R&D through both the European A step change, within three years, will be the evolution from GPS

GNSS Evolution Programme (EGEP) and Integrated Applications based location to multi-constellation GNSS, and integration with other

Promotion (IAP) ensures UK industry can capitalise on the emergent positioning capabilities to extend robust, secure and seamless PNT

commercial sector. These European-funded programmes will provide into challenging applications and environments.

UK industry with the ability to maintain momentum and international

competitiveness ahead of the EU’s proposed 7bn investment in the With respect to the infrastructure market as Galileo is deployed and

Galileo and EGNOS programmes from 2014-2020. refreshed and EGNOS is updated the current prime positioning of

UK companies becomes increasingly important. Capitalising on

The PNT NTC has ensured that this long term provides a framework this strong UK position, for example in GNSS resilience related

for scientific, technological and commercial GNSS research within opportunities through the provision of the PRS, requires a clear

UK that is well aligned and fully responsive to the European situation. national roadmap to inform all required support actions allied with a

The PNT NTC, made up of market leaders in delivery and generation strong collaboration with the Satellite Applications Catapult Centre.

of PNT capabilities, has evolved in the last 12 months, with a focus on

the whole PNT end-to-end value chain.

The PNT roadmap refresh highlights the technology focus areas

in which the UK should invest, within the context of the relevant

programmes and market timescales. A summary of where UK industry

could target early capitalisation for growth includes;

• Payload (Galileo and EGNOS) leadership retention and future

development, including potential for a further experimental

Galileo spacecraft to test new technologies;

• Galileo Public Regulated Service (PRS) and security related

evolutions in GNSS infrastructure and downstream services

including in encryption;

• GNSS robustness and Interference detection and mitigation;

• Next generation EGNOS (V3) design, implementation and

services plus associated Galileo Mission activities; advanced

and innovative receiver development and commercialisation;

• Potential hosting of future EGNOS payloads by UK satellite

operators;

• Retention of the UK’s academic leadership in European GNSS

technologies and the scientific advancement led by the UK’s

five key GNSS expert university groups.

The next 24 months will also see the concept definition of the next

generation of Galileo and UK industry involvement in the ESA

Evolution programme is critical to influence design and secure future

procurement work. The refresh exercise has re-established the

importance of two key market areas for the PNT sector in the UK:

20Satellite Telecommunications Summary of Technologies Required over the next

3 to 5 Years

Definition of Areas Covered Technology development themes have been identified which

The telecommunications market covers both the upstream will maintain and improve the competitiveness of the UK satellite

manufacturing and downstream applications / services aspects of the telecommunications industry. These are:

satellite telecommunications sector. • Increased telecommunications satellite capacity and flexibility

• Reducing cost to manufacturer, operator and user

Telecommunications dominates the UK Space industry in terms of

earnings, exports and employment for both upstream manufacturing

• Enabling new innovative services and market opportunities

and downstream services and applications.

Specific Technologies identified include:

UK industrial strengths are highlighted for the required Next generation communications satellite platforms. High throughput

telecommunications satellite systems across the full value chain: payloads for broadband, broadcast and fixed services. Transparent

and regenerative digital processors. Analogue flexible payload

• Service level (for satellite operations and service provision)

equipment, Advanced antenna solutions for broadband applications.

• System level (for Turn-Key Satellite Systems)

Low cost terminals for business and consumer applications.

• Subsystem level (e.g. Spacecraft Platforms, Payloads and Summary of how telecoms connects to markets

Antennas) Over 95% of the world commercial (non-government and institutional)

• Equipment level (e.g. Avionics, High Power Amplifiers, upstream satellite manufacturing market by value is dedicated to

Terminals) telecommunication satellites. Over 90% of the UK downstream space

• Specialist parts and services (e.g. satellite operations and market is dedicated to telecoms and satellite broadcasting.

software) UK built commercial telecommunications satellites have in recent

• Applications development (for instance maritime years secured 25% of the global market, the vast majority for export

communications) customers in Europe, the United States and the Far East. The UK

investment in telecommunications satellite capabilities has lead to the

The telecoms steering group has comprised representatives from all creation of world leading operators including Paradigm, Avanti and

these sectors of the industry. Key UK capabilities and organisations Inmarsat (a FTSE 100 company). Several hundred UK SME’s benefit

have been identified with an emphasis on securing a long-term and directly from satellite telecommunications programs.

high value of return on investment.

21Space Sensing Technologies • Traffic management and air quality monitoring

• The direct sales of high performance space instruments to

The sensing roadmap identifies the space and ground systems European and other international agencies, including for

technologies for the detection, collection and exploitation of data operational systems, which require repeat build of instruments.

for commercial, operational and scientific applications. The scope

• The spin out of technologies into non-space areas, including

is broad, including optics, detectors, instruments and supporting terrestrial and airborne environmental monitoring and health

systems for satellites and planetary landers, and also the ground applications provides further market growth potential.

technologies to handle and process the data. Many high growth

The provision of downstream EO applications is identified as an area

commercial markets - both national and export - which require sensing

of strong market growth. Developing the technologies that enable

technologies are identified in the 2014 Space IGS. These include

these applications will be a vital step in ensuring UK-based industries

maritime surveillance, persistent surveillance, climate applications and

are positioned to take advantage of this growth.

carbon monitoring.

Technologies required over the next 5 years

The sensing roadmap has been developed by the Space Sensing

Investment in innovative technology developments will be required to

National Technical Committee, with a broad representation across

secure a leading market position in the growth markets:

industry and academia. This roadmap captures in detail the main

areas of investment required in sensing technologies over the coming • Imaging systems with infra-red (IR) capability - shortwave,

5 years to capture these markets. medium wave and thermal IR

• Low cost imaging spectrometers for atmospheric greenhouse

Successes in sensing technology development gas monitoring

Recent investment by the UK Government and industry is leading to • Detectors (IR and visible) for EO, defence and surveillance

the development of an innovative low-cost radar system. NovaSAR-S and low cost radar to provide day and night all weather data

delivers all weather medium resolution Earth observation data streams

night and day at a price similar to traditional optical missions, and • Laser based systems such as LIDAR for sensing or imaging

significantly lower than any other SAR platform currently on the applications. The technologies may also be applicable for the

market, by leveraging highly efficient S-band solid state technology. communication of the high data volumes from space sensors

UK industry has been awarded a contract worth more than 100M Euro

• Expanded range and capability of sensor technologies

deployable on small and micro-satellites for Earth observation,

to build one of the main instruments, the Microwave Sounder on the including precision agriculture

Eumetsat MetOp Second Generation mission, which will make global

measurements of atmospheric temperature and pressure. • High performance computing, data mining and image

processing to improve capability for downstream applications

During 2013, UK industry won a contract to provide a compact

science and technology demonstration satellite for Kazakhstan • Continued investment into ESA science, EO and exploration

with a multispectral imaging instrument. This continues the series programmes to provide long term innovation in new

of successful exports to developing countries of small satellites to technologies.

provide state-of-the art digital imagers for a range of remote sensing The new technologies and techniques developed for science

applications programmes will develop the capability and provide technologies

for future applications in the commercial sector. The investment will

Sensing technologies for the high growth markets ensure that the UK retains front-runner status in sensing technologies

A significant export market is foreseen for sensing systems over and in international programmes.

the next 5 years for low-cost SAR radar and imaging satellites for

Earth observation, surveillance and defence. Supply of space- Additional societal benefit will arise from development of EO

based systems for homeland security to UK and other Governments applications for climate change and environment monitoring and the

provides an important market opportunity. The most significant market new sensing systems to meet demanding requirements of space

areas which will be enabled by development of innovative sensing science and planetary exploration. The growth in UK technological

technologies are: capability will enable commercial sensing developments, with

consequent increases in export sales, job retention and creation.

• Maritime surveillance, monitoring of oil spills, icebergs and

deforestation, land use categorisation, disaster management

• Services for greenhouse gas and environmental monitoring,

including deforestation:

The concept for the NovaSAR low-cost imaging radar mission

22The Alphasat communications payload and engineering team in Portsmouth

About the Space Special Interest Group

The Technology Strategy Board created the Space Special Interest Group (SIG) to connect pan-Knowledge

Transfer Network (KTN) activities, acting as a mechanism to foster a space community that spans Government,

Industry and Academia. The Space SIG is the custodian of the National Space Technology Strategy and its

underpinning technology roadmaps.

The Space SIG was hosted by the Aerospace, Aviation and Defence Knowledge Transfer Network, it is now part

of the Knowledge Transfer Network.

To connect with the Space Special Interest Group you can:

Special

Knowledge

Interest

Transfer

• Email alex.efimov@ktn-uk.org regarding getting involved in the Space SIG’s activies. Group

Network

• Register for free at https://connect.innovateuk.org/home to access services, networks

and to receive the fortnightly newsletter.

Space

Aerospace & Defence

23Special Knowledge Interest Transfer Group Network Space Aerospace & Defence

You can also read