Deloitte 2021 M&A Tax Virtual Conference Break-out session Germany: RETT Reform with a focus on the "New Shareholder Rule" and future RETT ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Deloitte 2021 M&A Tax Virtual Conference Break-out session Germany: RETT Reform with a focus on the “New Shareholder Rule” and future RETT blockers possibilities 02 MARCH 2021

Day 1: Global and regional private equity topics

Introduction and Contacts

Nevin Borucu

Partner

Munich

E-Mail: nborucu@deloitte.de

Half of everything you know will be

obsolete in 18-24 months - Moore's

Law

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 2

Contents Overview of Legislation in Germany 4 Current vs. potential future law RETT law 6 Case studies 9 Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 3

Overview of Legislation in Germany Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 4

Overview of Legislation in Germany

Real Estate Transfer Tax Reform - Overview

Retrospective application?

25.09.2020

01.01.2020

31.07.2019

Legislative procedures

Potential retro- New RETT rules to come

Federal Government

picked up again – up to

spectivity for into force for RETT

issues draft act on the

date NO UPDATE

observation periods triggering events as of 1

RETT reform

RETT reform January 2020

24.10.2019 H1 2020

Government press release: new RETT rules will Expected timeline for

08.05.2019 NOT come into force as of 1 January 2020 new RETT rules to

Federal Ministry of Finance come into force

issues RETT reform draft bill

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 5

Current vs. potential future law RETT law Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 6

Current vs. new RETT law

Transactions subject to RETT (new law)

PropCo vehicle Partnership Corporation Corporation & Partnership

direct / indirect share transfer of direct / indirect share transfer of direct / indirect, legal / economic

RETT triggering event 95% 90% within 5 10 years to new 90% within 10 years to new unification of 95% 90% of the

shareholders shareholders shares

Unification in the hands unification requirement in the

irrelevant irrelevant

of 1 buyer? hands of one acquirer

Time frame 5 10 years 10 years irrelevant

Land-rich requirement No No No

Date of the triggering event Closing Closing Signing

Share seller and purchaser jointly

RETT liable party partnership itself corporation itself

liable

typically FMV of underlying real typically FMV of underlying real typically FMV of underlying real

RETT basis

estate estate estate

RETT rate 3.5% - 6.5% 3.5% - 6.5% 3.5% - 6.5%

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 7

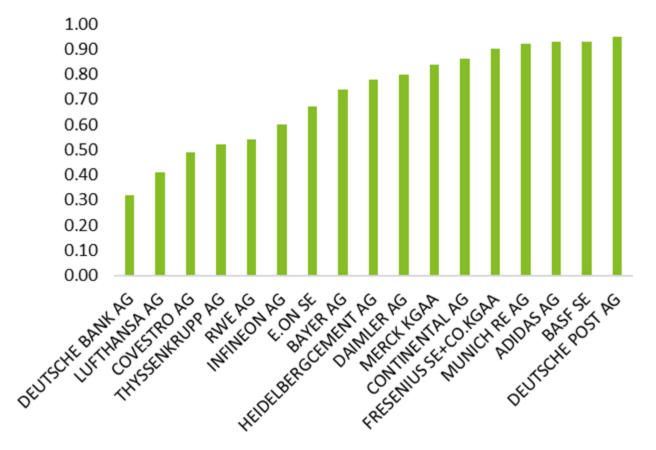

Listed corporations

Change in shareholder structure

Problem

Free float

• In the case of listed corporations, the shareholders structure changes

Anchor frequently.

investor?

• The chart on the left shows the time to reach a 90% turnover in years

of selected DAX stocks (e.g. Deutsche Bank AG, based on the

computations, would have to pay RETT on its entire real estate

portfolio every 0.32 years on average).

(listed)

PropCo

• Simplified computation approach: market capitalization

(01.02.2019)/revenue of transactions (year 2018). No consideration

Year of anchor investors. 18 out of 30 of the DAX companies do not have

an anchor shareholder.

Solution: Stock exchange exemption (still under discussion)

• Change in shareholder structure would not be applicable for listed

companies.

Source: Deutsches Aktieninstitut e. V.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 8

Case Studies Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 9

Case Studies

Current RETT law

RETT triggering event?

2020

• RETT triggered in case of unification of at least 95% in one hand or in

Seller Buyer 1

the hands of company controlled entities.

• Buyer1 unifies 100%.

100% • Transaction is subject to RETT

Lux Hold Co

* German RETT applies on the transfer of the shares on HoldCo

irrespective whether HoldCo is German land rich or not.

100% 100% 100%

Lux PropCo Lux PropCo Lux PropCo

(Germany) (France) (United Kingdom)

Fair Value: 1,000k€ 4,000k€ 5,000k€

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 10Case Studies

Current RETT law vs. potential new law

RETT triggering event?

2021 2021 • RETT triggered in case of unification of at least 95% in one hand or in

the hands of company controlled entities.

Seller Buyer 1 Buyer 2

• Buyer 1 unifies only 89% an Buyer 2 only 11% (assuming Buyer 1 is

89% fully independent from Buyer2).

11%

• Buyer 2 act as RETT-Blocker

Lux PropCo • Transactions are not subject to RETT

RETT triggering event?

• RETT triggered in case of unification of at least 90% or shareholder

change of at least 90%

• 100% transfer of shares to new shareholders

• Transactions IS subject to RETT

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 11Case Studies

Potential future law

RETT triggering event?

2018 2022

• 2019: Buyer 1 unifies only 89%: no RETT

Seller Buyer 1 Buyer 2

• 2022: Buyer 2 unifies only 11%. Shareholder change only 11%.

89%

11% • Retrospective application of the 10 year observation period?

• Position sill unclear

Lux PropCo

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 12Case Studies

Potential future law

RETT triggering event?

2021 • RETT triggered in case of unification of at least 90% or shareholder

change of at least 90%

Seller Buyer 1

• Only 89% transfer of shares to a new shareholder

89%

11% • Seller acts as RETT-Blocker

• Transactions is NOT subject to RETT

Lux PropCo

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 13Share-Deal

Example (potential future law)

RETT triggering event?

2021 2022 • RETT triggered in case of unification of at least 90% or shareholder

change of at least 90%

Seller Buyer 1 Buyer 2

• 2021: Buyer 1 is a new shareholder, however less than 90% are

Sale of 89% Sale of 89% transferred to new shareholder: NO RETT

11% 89%

• 2022: Buyer 2 is a new shareholder, however less than 90% are

transferred to new shareholder: NO RETT

Lux PropCo

• Conclusion: As long as Seller – as Anchor Investor - remains in Lux

PropCo as shareholder in a rolling period of ten years, with respect to

new shareholders, no RETT is triggered.

2033 2022

Seller Buyer X Buyer 2

• 2033: Buyer X is a new shareholder, however less than 90% are

transferred to new shareholders within ten years.

Sale of 11%

11% 89% • In 2033: After a holding period of 10 years by Buyer 2, Buyer 2

become an Anchor Investor.

Lux PropCo • Transaction in NOT subject to RETT

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 14Deloitte 2021 M&A Tax Virtual Conference Break-out session Germany: Fiscal authorities re-open new options for RETT-exempt intra-group restructurings 02 MARCH 2021

Day 2: Real estate and debt funds

Introduction and Contacts

Andrea Bilitewski

Partner, Tax & Legal | M&A

Hamburg, Germany

E-Mail: abilitewski@deloitte.de

Structuring various post-merger

integration processes

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 2Fiscal authorities re-open new options for RETT-exempt intra-group restructurings Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 3

Day 2: Real estate and debt funds

RETT exemption for certain intra-group restructurings by Sec. 6a German RETTA

Transactions covered • Merger

• Spin-off

• Split-off

• Hive-down

• Asset/share transfers on the basis of articles of association (contribution in kind,

distribution in kind, liquidation)

The exemption is also available for cross-border transfers within the EU

Requirements for RETT • Controlling entity

exemption regarding involved • can be any legal entity (corporation or partnership) as well as individuals.

entities • needs to be “economically active”.

• Tax Authorities conclude that a mere holding company does not

qualify as controlling entity

• It is doubtful whether this conclusion is consistent with the view of

the FCJ.

• Controlled entity

• A direct or indirect shareholding of at least 95% must have already existed

for the 5 years prior to the transaction as well as for at least 5 years

subsequent to the transaction (so-called prior and subsequent holding

periods).

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 4Day 2: Real estate and debt funds

Intra-group merger of real estate owning companies

Opinion of Tax Authorities

P GmbH • Up-stream merger of a controlled company to the controlling company

does not qualify for RETT exemption because the “subsequent holding

period” of 5 years cannot be met due to the merger.

> 95% within 5 years

• However, RETT exemption regarding a side-stream merger was already

„prior holding period“

accepted b tax authorities if

• the transferring entity fulfills the 5 years holding period prior to the

transaction

S GmbH

• The acquiring entity fulfills both 5 years period (prior and

subsequent holding period)

Ruling of the Federal Fiscal Court

• Sec. 6a RETT Act is to be interpreted that the 5 years “subsequent holding

period” does not apply in cases of a (side-stream/up-stream) merger as the

nature of the qualifying restructuring transaction does not allow this

P GmbH

requirement to be met.

• Consequence for up-stream merger: RETT exemption applies if the 5 years

> 95% within 5 years > 95% within 5 years „prior + “prior holding period” was fulfilled.

„prior holding period“ subsequent holding period“

• Rulings: FFC II R 18/19 as of 22 August 2019

FFC II R 15/19 as of 21 August 2019

S1 GmbH S2 GmbH

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 5Day 2: Real estate and debt funds

Intra-group merger of real estate owning companies

Side-stream merger involving two subsidiaries

P GmbH Opinion of Tax Authorities

• RETT exemption does not apply because the acquiring entity does not

fulfil the 5 years “prior holding period”.

> 95% within 5 years > 95% within the prior 3

„prior holding period“ years and the subsequent Ruling of the Federal Fiscal Court

5 years

• Shared the legal opinion of Tax Authorities

• The fact that the real estate itself was owned by the group for 5 years prior

and 5 years after the transaction was not relevant to the decision as Sec. 6a

RETTA refers to shareholding periods and not to ownership periods

regarding the real estate.

S 1 GmbH S 2 GmbH

• Ruling: FFC II R 17/19 as of 22 August 2019.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 6Day 2: Real estate and debt funds

Hive-down to a newly established subsidiary

Opinion of the tax authorities

P GmbH • RETT exemption (Sec. 6a RETTA) does not apply as the shareholding in the

acquiring entity does not fulfil the the 5 years “prior holding period”.

> 95% within 5 years „prior +

subsequent holding period“ Ruling of the Federal Fiscal Court

S GmbH • RETT exemption acc. to sec 6a RETTA is applicable.

• The fact that the 5 years “prior holding period” cannot be fulfilled in cases

> 95% within the of a reorganization to a newly established controlled entity is harmless.

„subsequent holding period“

• The same applies in cases of intra-group mergers or spin-offs to a newly

controlled entity.

NewCo

• In case of a spin-off for new establishment, the dominant entity needs to

fulfill the retention period of five years. However, the reservation period

with regard to the newly established entity does not need to be met

because the fulfillment of the reservation period requirement is not

P GmbH possible due to the spin-off.

> 95% within 5 years „prior + > 95% within the • Ruling: FFC II R 16/19 as of 21 August 2019

subsequent holding period“ „subsequent holding period“ FFC II R 21/19 as of 21 August 2019

S GmbH NewCo

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 7Day 2: Real estate and debt funds

Spin-off in a foreign EU jurisdiction

Facts

P AG - Austria • Austrian S 1 GmbH transfers all shares in German S 2 GmbH

to newly established Austrian NewCo.

> 95% within the • The transaction generally triggers RETT with regard to the real

> 95% within 5 years

„subsequent holding period“ estate of S 2 GmbH as well as S 3 GmbH.

„prior + subsequent

holding period“ Opinion of the tax authorities

• The spin-off under Austrian law corresponds to a spin-off

under German Law.

S 1 GmbH - Austria NewCo

• However, no RETT exemption as NewCo cannot meet the 5

year “prior holding period.

Ruling of the Federal Fiscal Court

• RETT exemption acc. to sec. 6a RETTA applies. The fact that

NewCo does not meet the “prior holding period” is not

100% detrimental.

S 2 GmbH - • Decision: FFC II R 21/19 as of 21 August 2019

Germany

100%

S 3 GmbH -

Germany

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 8Day 2: Real estate and debt funds

Relevance to acquisition structures and post merger integration transactions

Requirement of a 5 years “prior holding period”

• hinders cross-border integration measures between existing

controlling entity

group and newly acquired target group.

• Any transactions between the groups within 5 years after the

acquisition of target group are liable to RETT (for a second

time).

Consequence for acquisition structures

• If possible, real estate of target group could be acquired

separately in advance or

• Shares in real estate owning companies of the target group

could be acquired separately by existing group companies

with which they are to be merged afterwards.

existing group newly acquired target group • In the latter case the subsequent merger might be

liable to RETT but the RETT resulting from the

purchase of the shares might be creditable.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 9Deloitte 2021 M&A Tax Virtual Conference Break-out session Germany: German Investment Tax Considerations: Developments and Trends 02 MARCH 2021

Day 2: Real estate and debt funds

Introduction and Contacts

Alexander Wenzel

Partner Financial Services

Frankfurt

E-Mail: alwenzel@deloitte.de

Be careful with German tax!

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 2German Investment Tax Considerations: Developments and Trends Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 3

Day 2: Real estate and debt funds

German Investment Tax Considerations: Developments and Trends

The activity as well as the behavior of the German tax authorities in the investment management / real estate / private equity space

have changed fundamentally in recent years.

Activity Interaction

• The activities of the tax authorities have increased • In previous years, it was sometimes difficult to reach an

enormously agreement with the tax authorities on certain tax

More tax officers technical questions

Significantly expanded tax technical expertise • From our point of view, this has changed

High audit density, which in some cases corresponds More interaction possible

to an early tax audit Tax officers are willing to participate in seminars

• In certain cases, we see significant differences between A number of tax officers who publish essays and/or

local tax office regarding tax technical views contribute to commentaries

• Sometimes we recognize the need for a more coordinated Important to recognize these activities and to value the

approach trust

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 4Day 2: Real estate and debt funds

German Investment Tax Considerations: Developments and Trends

With the GITA 2018, the scope of application of the act has been

AIF / UCITS?

significantly expanded.

• Unlike in other jurisdictions, there is no single German tax act No

covering all conceivable forms of collective investment schemes. No

It is therefore indispensable to analyse each and every Yes Fictitious investment fund?

investment vehicle on a case-by-case basis.

Yes

• Tax consequences and tax compliance obligations differ

significantly, both on fund and investor level.

Exception?

• Basically, the scope of application of the AIFMD directly results in

No Yes

the applicability of the GITA. There are however also exceptions

as well as the concept of fictitious investment funds.

GITA applicable GITA not applicable

• According to the GITA as amended by the annual tax act 2020,

there is however no binding effect of the decision of the German

financial supervisory authority. In the past, this was already

stipulated by a decree of the German Federal Ministry of Special

Finance. investment fund

Retirement

asset fund

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 5Day 2: Real estate and debt funds German Investment Tax Considerations: Developments and Trends The German Ministry of Finance recently issued a decree in relation to the retroactive correction of the equity gain (Aktiengewinn) calculated and published under the GITA 2004. • The decree follows a decision of the Finance Court of Lower Saxony, where the investment strategy as described in the sales prospectus included tying transactions (Kopplungsgeschäfte). • Tying transactions are arrangements intentionally put in place to leverage the contrary tax treatment of positive income on shares on the one hand and losses on financial derivatives on the other hand. • According to the decree, German investors need to ensure that the equity gain has been correctly calculated with respect to such conceptual arrangements. As opposed to the decision of the finance court, the decree also applies if the sales prospectus did not explicitly mention tying transactions. • German investors are now obligated to notify the competent tax office and to provide corrected equity gain figures if they were used in tax declarations and if the aforementioned arrangements were not considered correctly in the equity gain. • Unlike the GITA 2004, the GITA 2018 includes a provision to identify and to offset such transactions if they are part of a conceptual arrangement. Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 6

Day 2: Real estate and debt funds German Investment Tax Considerations: Developments and Trends Potential change to the German WHT reclaim procedure for non-German investment funds as from 1 July 2021. • According to a bill currently in the legislative process, the GITA will be amended in such a way that the WHT refund procedure according to sec. 7 para. 5 GITA would no longer be accessible for non-German investment funds. They would then need to go for the more complex German WHT reclaim procedure in line with sec. 11 GITA and sec. 50d para. 1 German Income Tax Act respectively. • Tax technical background: if German dividends are paid during a period for which a status certificate has not yet been provided, the entity responsible for the deduction of German WHT will apply the usual tax rate of 26.375% instead of the reduced tax rate of 15%. • Sec. 7 para. 5 GITA stipulates that if a status certificate is provided retroactively (within 18 months of the German dividend payment and covering the time of the payment) to the entity that has deducted the tax, this entity is obligated to refund the difference between the full and the reduced tax rate. • Recommendations? Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 7

Deloitte 2021 M&A Tax Virtual Conference Break-out session Luxembourg: Tax structuring concerns for open ended RE and Infra AIFs 02 MARCH 2021

Day 2: Real estate and debt funds

Introduction and Contacts

Francisco Da Cunha João Almeida

Partner Partner

Luxembourg Luxembourg

E-Mail: fdacunha@deloitte.lu E-Mail: joaoalmeida@deloitte.lu

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 2Tax structuring concerns for open ended RE and Infra AIFs Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 3

The global tax reset and how it influences Fund structuring

What is the outcome

Tax law Change Which Area of the Fund does impacting IRR

this impact

• Interest limitation rules • Local/Holding investment vehicles; • (Partial) Disallowance of tax deductions

• Exit Taxation • Local/Holding investment vehicles; • Exit taxes

• General anti abuse rules • Local/Holding investment vehicles; • Disallowance of tax benefits

• Controlled Foreign Company rules • Holding vehicles • Anticipate cash tax paid / double

taxation?

• Hybrid and imported mismatch • All entities within the structure

rules • (Partial) Disallowance of tax deductions

• Fund vehicle

• Reverse hybrid rules • Taxation of otherwise exempt Fund

• GP / service providers profits

• Mandatory disclosure rules

• Holding vehicles • Penalties / Criminal offences

• Multilateral instrument and the

• Holding vehicles • Disallowance of tax benefits under DTTs

PPT

• ECJ court Cases • Disallowance of tax benefits under EU

Directives

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 4New dynamics between GPs and LPs

Leading to a shift in fundraise and fund structuring

Business and commercial rationale are the

Increased DD by LPs on GPs driving forces behind decision making. Tax is

second to business reasons

LPs are willing to pay more costs in an

Tax is however an increasingly

effort to have a cleaner and certain

complex area to still cater for structure

GPs still in search for yield, but

LPs seek simplicity and “When you change the way

preferably wrapped up and arising from

flexibility on Fund structures you look at things, the things

you look at change” sustainable / ethical / responsible

investment

GPs still seek maximizing the

LPs will need to be more lenient with UBO

profits whilst reducing the

information request as this is a new standard

costs

for doing business

Low tolerance for tax risk and

GPs and LPs will need to substantially change fund

no use of tax havens

subscription documentation to cater different cost

allocations (eg, provoked by reverse hybrid rules)

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 5Fund Structuring

Investment Fund set up • Management activities and fund consolidated in one

place

• Adequate level of substance and functions (including the

oversight of delegations) required

• Cross-border management allowed within the EU

• JV structures are commonly used EU Investors Non-EU Investors

due to the size and volume of the

investments

• Typically Co-investors invest Foreign IM

directly in the Fund with

preferred units.

• JVs can influence platform set up Lux AIFM Non-AIFM GP

and repatriation waterfalls

Co-Investors Lux AIF

Parallel

(e.g. SCSp) Fund

Master LuxCo

Lux SPV 1 Lux SPV 2 Lux SPV 3

• Pooling regional platform possibly

qualifying to PPT for DTT purposes EU entities

• Appropriate level of economic and EU BidCos Non-EU BidCos Lux PropCos

physical substance to be

maintained in Luxembourg. • PPT / GAAR test to be discussed

• Impact on MLI to be investigated on a

source country basis

Real Estate / Infrastructure Assets • Anti-hybrid and imported mismatch to

be considered if leverage

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 6Deloitte 2021 M&A Tax Virtual Conference Break-out session Luxembourg: AIF structures: important VAT considerations in light of recent CJEU decisions 02 MARCH 2021

AIF structures important VAT considerations in light of recent CJEU decisions Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 2

Break out sessions – AIF Structures – Important VAT considerations

Introduction and Contacts

Cédric Tussiot Tomas Papousek

Partner Directeur

Luxembourg Luxembourg

E-Mail: ctussiot@deloitte.lu E-Mail: topapousek@deloitte.lu

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 3Contents Typical AIF structures 5 Fund Management VAT exemption 6 Financial Intermediary exemption 7 Latest CJEU case law 8 AIFs as eligible vehicles 10 Case studies 11 Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 4

Day 2: AIF structures

Typical AIF structures and related management service flow

Lux GP will be acting as statutory general partner

Lux AIFM has been appointed to and will be entitled to a GP which should cover its

provide portfolio and risk operating costs and a markup

management services as well as LPs

valuation and distribution services and

in consideration will be entitled to

AIFM fee

Lux GP

GP fees

Portfolio management

and distribution AIFM services

UK Portfolio Service providers

Lux AIFM

Manager SCSp Fund accounting

(AIF) services

Lux AIFM delegates portfolio

management to UK Portfolio Manager Asset Cos

who in consideration will be entitled

to portfolio management fee and

reimbursement of ancillary costs

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 5Day 2: AIF structures

Fund Management VAT exemption

Concept of “fund management” Set Up Services Ancillary services to portfolio

management

In order to benefit from the Services (Legal / Tax / Advisory)

qualification as fund management incurred by the promoter / Services which are sourced by the

services exempt from VAT under future manager of a fund portfolio manager / investment adviser

Article 44 §1 d) LTVA, the sub- structure are generally not from third party suppliers, and incurred

delegated services must be: considered as management and in its capacity of portfolio manager /

• Specific and essential for do not benefit from the VAT investment adviser, which are specific to

management of the investment exemption (debate on the and essential for the management of a

fund; market place) qualifying vehicle, directly related to and

• Individualized (investment fund necessary for, the provision of the

by investment fund); and portfolio management / investment

• Not “isolated” services (Circular advisory, may under certain conditions,

n°723bis). be considered as ancillary to the main

portfolio management / investment

advisory services and share the VAT

exempt treatment of these main services

Illustrative overview* of application of fund management VAT exemption on typical services received by a an eligible investment vehicle

Portfolio management Exempt NAV calculation Exempt

Risk management Exempt Legal and tax services Taxable

Investment advice Exempt Transfer and/or registrar agent Exempt

Fund accounting Exempt Domiciliation Mostly exempt

Depositary Partly exempt and subject to 14% VAT Audit Taxable

* The above is only an illustrative overview and should not be in any way considered as binding. Accordingly, the VAT treatment of each service needs to be analysed on a case-by-

case basis taking into account all its specificities. In this respect, supporting documentation and/or agreements must always be reviewed to confirm the VAT treatment

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 6Day 2: AIF structures

Financial intermediary VAT exemption

According to the CJEU, “negotiation” is “a service

rendered to, and remunerated by, a contractual party as a

distinct act of mediation. It may consist, amongst other

things, in pointing out suitable opportunities for the

conclusion of such a contract, making contact with

another party or negotiating, in the name of and on

behalf of a client, the detail of the payments to be made

by either side. The purpose of negotiation is therefore to

Based on the above, the a supplier needs to be do all that is necessary in order for two parties to enter

actively involved in the bringing together the party into a contract, without the negotiator having any

seeking to sell and the party seeking to buy interest of his own in the terms of the contract”.

shares/interest in an entity and negotiating the terms

of the contract.

It is not negotiation where one of the parties entrusts to a

sub-contractor some of the clerical formalities related to

the contract, such as providing information to the other

party and receiving and processing applications for

subscription to the securities which form the subject-

matter of the contract.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 7Day 2: AIF structures

Latest CJEU case-law

Eligible

vehicles

Supply of Alladin IT

system

BlackRock US BlackRock UK

CJEU decision Not

• The fund management VAT exemption cannot apply to delegated services which eligible

are rendered as a single supply to a fund manager who manages both vehicles

eligible under this VAT exemption and vehicles that are not eligible. Otherwise this

would go against the need to construe VAT exemptions narrowly.

• In particular, the CJEU is concerned that a manager may have funds under

management that are mostly eligible under the fund management VAT exemption,

and if the exemption were permitted to apply, funds not eligible under the fund

management VAT exemption could also benefit from the VAT exemption.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 8Day 2: AIF structures

Latest CJEU case-law

DBKAG (C-59/20) CJEU hearing hold on 3 February 2021

Could the granting by a third-party licensor to an investment management

• Parties are mostly in agreement that the services are essential but

company (‘IMC’) of a right to use specialist software specifically designed for the

• Discussion around the specificity of the services (tax services more complex than

management of special investment funds, where the software is intended

‘standard’ tax services – question around the responsibility of the services

exclusively to perform “specific and essential” activities in connection with the

provider of the software)

management of the fund but runs on the systems of the IMC (with minor

• Discussion around neutrality between PME that need to outsource the services

participation by the IMC), and uses market data provided by the IMC, be VAT

and big companies that can do it in-house

exempt?

Decision expected before summer

Finanzamt N (K) (C-58/20)

Could tax-related responsibilities entrusted by the management company to a

third party, consisting of ensuring that the income received by unit-holders from

investment funds is taxed in accordance with the law be VAT exempt?

The IMC was under a statutory duty to provide information to unit-holders to

allow them to comply with their tax obligations, and outsourced this to K. The

CJEU will rule on whether this outsourced service amounted to “management”

of investment fund in its own right.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 9Day 2: AIF structures

AIFs as eligible investment vehicles?

• Fiscale Eenheid X (Case C-595/13) – investment companies may qualify as a SIF, if (i) capital is pooled by several investors; (ii) investment risk is borne /

profits are received by the investors; and (iii) the investment company is subject to “state supervision”.

• “State supervision” – application? - The CJEU introduced the concept, but left it to Member States to interpret what it actually means.

• EU VAT Committee guidelines (July 2018) defined 5 criteria a fund must meet to qualify as a SIF:

1) The fund is a collective investment

2) The fund must operate on the principle of risk-spreading

3) The return on the investment depends on the performance of the investments, and the holders bear the risk connected with the fund

4) The fund must be subject to State supervision

5) The fund must be subject to the same conditions of competition and appeal to the same circle of investors as UCITS.

• No intention at present to (i) amend the list of funds qualifying as SIF under the Luxembourg VAT law and/or to (ii) require that such funds are subject to

“the same conditions of competition and appeal to the same circle of investors as UCITS”

• Luxembourg VAT authorities have so far not issued any guidelines or comments on the “state supervision” point

• Regarding AIFs, the view in Luxembourg is that the indirect supervision through their AIFM is sufficient in that respect

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 10Day 2: AIF structures

Case studies of routing management services within AIF structures

Limited grounds to consider the application of fund Stronger arguments to consider the

management VAT exemption on services performed to application of fund management VAT

Lux AIF exemption on services performed to Lux

AIF

Luxembourg VAT likely due on the GP fee

Lux GP Lux GP

Lux AIFM Lux AIFM

Management

services Management

AIFM services Appointment services

Lux of Lux AIFM Lux

AIF AIF

Management services to benefit from the

AIFM services to benefit from the fund fund management VAT exemption - proper

management VAT exemption - proper documentation supporting the nature of the

documentation supporting the nature of the AssetCos AssetCos

services as management of investment fund

services as management of investment fund and and clear description of Lux AIF as beneficiary

clear description of Lux AIF as beneficiary of of services

services No entitlement to VAT deduction at the level

No entitlement to VAT deduction at the level of of AIF (but VATable costs should be limited)

AIF (but VATable costs should be limited)

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 11Day 2: AIF structures

Case studies of routing management services within AIF structures

In Luxembourg services qualifying as management of investment funds Foreign Investment

Transaction costs (including

(including AIFs) can benefit from a VAT exemption. Therefore: Manager (UK/US) Investment

dead deal costs) covering

management

• Investment management / advisory services rendered to the Lux AIFM by the tax, legal, accounting,

services and

foreign investment manager for the benefit of the AIF should be VAT exempt administration, etc. reimbursement of

ancillary costs

• AIFM services (portfolio, risk and administrative management) rendered to

the AIF by the AIFM should benefit from a VAT exemption

3rd party

service providers Lux AIFM

• Custody and central administration services rendered for the benefit of the

AIF should be VAT exempt Investment

management

• 3rd Party costs (tax / legal / other transaction services) are generally taxable services and

and when charged by the third party to the AIFM or directly to the AIF will reimbursement of

create a VAT cost in Luxembourg Transaction costs (including ancillary costs

dead deal costs) covering

• In case 3rd party costs (in particular transaction costs), instead of being tax, legal, accounting, Lux AIF

charged to the AIF, would be incurred at the level of the Foreign investment administration, etc.

manager, as costs directly necessary for and connected to the provision of

the investment management services, and when they can be incorporated in

the investment management fee or added as ancillary expenses, they could

share the VAT treatment of the main services and benefit from the VAT

exemption

Points of attention

• Proof of taxable person status of Lux AIFM (Lux VAT Id Nr)

Proper documentation supporting the nature of the services as

management of investment fund

• Clear description of Lux AIF as ultimate beneficiary of services

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 12Day 2: AIF structures

Case studies of routing management services within AIF structures

Foreign investment

Investment manager / advisor

management/advisory

services

Investment advisory fee paid directly to

Third Party the foreign investment manager /

Lux GP

AIFM (Lux) advisor

AIFM services

Fee for AIFM services paid to third party Lux

AIFM reduced by investment AIF

management / advisory fee paid

directly to foreign investment manager/

advisor

EU entities

The investment management / advisory service flow in the above

example differs from the investment management / advisory fee flow.

In this case, the Lux AIF pays each the third party AIFM and the foreign

investment manager / advisor their net share. Commercially and

accounting and invoicing wise, however, foreign investment manager /

advisor is rendering and raising its invoice to third party AIFM and the

third party AIFM raises its invoices for the full AIFM fee directly to the

Fund

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 13Deloitte 2021 M&A Tax Virtual Conference Break-out session Luxembourg: Business model of the private debt in light of current/future challenges 02 MARCH 2021

Day 2: Real estate and debt funds

Breakout on the business model of the private debt in light of current/future challenges

Clemens Petersen Olivier Venzal

Tax Partner Tax Partner

Germany - Frankfurt France - Paris

clepetersen@deloitte.de ovenzal@taj.fr

Ben Toussaint

Tax partner & (Lux) debt leader

Luxembourg

btoussaint@deloitte.lu

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 2Day 2: breakout on the business model of the private debt

Introduction and objective of today

• The idea of this session originated from an exercise we performed some time ago at Deloitte when BEPS/ATAD were under

discussion.

• We did a mapping of our private debt clients in order to assess whether this industry was on par with private equity/real estate:

the reality was that debt funds were not necessarily on par with the rest of the alternative industry.

• Questions are (i) whether the business model of private debt changed in the light of all the legislative developments of the last

couple of years; and (ii) how source countries look at these funds.

Offshore addiction: non-EU funds were used in majority by asset managers

(especially US).

Low substance & operating model.

Our historical

mapping

No rationalization of the use of jurisdictions: no pooling & case by case.

Randomly focusing on beneficial ownership.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 3Day 2: breakout on the business model of the private debt

Evolution of the business model

From To

• The old model was randomly using Luxembourg as an intermediate • We saw an increasing number of setups relying on a Luxembourg platform

jurisdiction along side with other jurisdictions on a case by case basis with or without an AIF depending on the case at hand.

depending on tax needs.

• Management activities and fund can be consolidated in one place.

• There was no substance or it was rather cosmetic.

• These platforms have more and more substance (increase of the nbr. of

• Limited functions were performed. employees) and a min level of functions above routine functions are

performed.

• Specific requirements of the AIFM are considered (risk management,

oversight of delegation to the investment manager, distribution of the AIF to

EU investors)

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 4Day 2: breakout on the business model of the private debt

Challenges (theory)

• The beneficial ownership (BO)

is already a requirement of the

OECD model tax convention

within an international context.

• A BO test is also included in

the EU Interest and royalties

Directive (within an EU

context).

• It was also interpreted & re-

emphasized by the European

Court of Justice on 26 Feb.

2019 (so-called Danish case).

• Generally speaking, there are 2 • The principal purpose test (PPT) is a general anti-

concepts which could be abuse measure addressing cases of treaty abuse,

applied by foreign tax including treaty-shopping situations, such as

authorities when assessing certain conduit financing arrangements that are

whether the recipient of an not covered by more specific anti-abuse rules.

interest income is eligible for a • The PPT is one of the possible options (alongside

WHT reduction or exemption with the PPT completed by a simplified LOB) for

under a tax treaty, certain EU jurisdictions that have chosen to sign the

Directives or a domestic rule. Multilateral Instrument (“MLI”) released by the

OECD under the BEPS initiative.

• A similar provision to the PPT was introduced

within the EU through the EU Directive 2015/121

dated 27 January 2015 (amending the EU Parent-

Subsidiary regime) and more broadly in the EU

Directive 2016/1164 (introducing ATAD I).

• There is no clear visibility on the application of the

PPT test in each jurisdictions.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 5Day 2: breakout on the business model of the private debt

Challenges (examples)

1st Non-CIV paper German tax circular German draft bill

issued by the OECD of April 2018 on (Jan. 2021) on German

in 2016 dividends WHT on dividends

Eqiom (Sept. 2017) & ECJ decision 26 Feb.

Diester (Dec. 2017) 2019 (Danish cases)

ECJ cases on int. & div.

Is there a sustainable business

model?

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 6Day 2: breakout on the business model of the private debt

Germany – Case where the Lux lender solely receives interest income

• Case where the Lux lender solely engage into a loan origination

transaction and expects to receive interest income on the loan

receivable.

• German WHT on interest payments?

Lux

AIF ‒ Profit participating loan.

Master • Lux SPV becomes limited tax liable in Germany?

Luxco

‒ Loan secured with real estate located in Germany.

Lux SPV Lux SPV Lux SPV

• Limited interest deductibility at Borrower‘s level?

Interest

payments

‒ Possible application of the German interest limitation rule.

Borrower Borrower Borrower

Germany Germany Germany ‒ 25% of the tax deductible interest expenses are not tax

deductible for Trade Tax purposes.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 7Day 2: breakout on the business model of the private debt

Germany – Case where the Lux lender has an equity kicker

• Case where the Lux lender engage into a loan origination gets

an incentive in the form of an equity kicker.

• German WHT on dividends to Lux SPV?

Lux • Shareholding < 10%

AIF

‒ 15% due to DTA

Master

Luxco • Shareholding at least 10%

‒ 0% due to Parent Subsidiary Directive

Lux SPV Lux SPV Lux SPV

Equity

Equity like • However, 26.325% if the German anti-treaty shopping

return

kicker provisions are not fulfilled: Draft bill (20 January 2021)

Borrower Borrower Borrower

Germany Germany Germany ‒ Shareholder Test

‒ Business income Test

‒ Benefit Test

…expected to be enacted during 2021

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 8Day 2: breakout on the business model of the private debt

France – Case where the Lux lender solely receives interest income

• Case where the Lux lender solely engage into a loan origination

transaction and expects to receive interest income on the loan

receivable.

• French WHT on interest payments?

Lux

AIF ‒ No (unless made to a non-cooperative country).

Master • Limited interest deductibility at Borrower‘s level?

Luxco

‒ Possible application of the French interest limitation rule.

Lux SPV Lux SPV Lux SPV

‒ EBITDA limitations: external debt as well as related-party debt

Interest falls within the scope of the EBITDA limitation. Interest

payments

expenses are deductible up to €3m or 30% of the borrower

Borrower Borrower Borrower EBITDA.

France France France

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 9Day 2: breakout on the business model of the private debt

France – Case where the Lux lender has an equity kicker

• Case where the Lux lender engaged into a loan origination gets

an incentive in the form of an equity kicker.

• French WHT on dividends to Lux SPV?

‒ 28%, possibly reduced to nil if shareholding >5%

‒ However, access to WHT exemption is subject to (i) existence

of economic substance in the Lux SPV, (ii) Lux SPV being the

beneficial owner of the dividends and (iii) compliance with

Lux

Principal Purpose Test.

AIF

• Interest rate

‒ Interest rate must in principle be set at arm’s length.

Master

Luxco

‒ For lenders who own a minority share in the capital of the

Lux SPV Lux SPV Lux SPV borrower, interest rate is however capped at a very low rate

Equity like

(c. 1.2% currently) pursuant to the law.

Equity

return

kicker • Anti-hybrid legislation (ATAD2)

Borrower Borrower Borrower

France France France ‒ Arrangements targeted by ATAD 2 rules are mainly (i)

situations that give rise to a deduction without inclusion of a

payment made under a hybrid instrument, or to a hybrid

entity, (ii) situations that give rise to a double deduction and

(iii) certain other specific situations.

‒ Should not apply to a minority private lender, save if it owns

more than 25% of the borrower.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 10Day 2: breakout on the business model of the private debt

Take away

Is your organization planning to restructure your current operating model

and fund structure as a result of the principal purpose test (PPT) and

scrutiny on BO?

A. We already adapted ourselves to these new challenges

B. Yes for sure

C. Probably

D. Not sure yet

E. No for sure

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 11Deloitte 2021 M&A Tax Virtual Conference Break-out session Luxembourg: Wave of onshorisation in Asia : structuring considerations and typical alternative set-up for RE managers 02 MARCH 2021

Day 2: Real estate and debt funds

Contacts

Yves Knel Cedric Carnoye

Part Cross-border Tax Director, International and M&A Tax Services

Deloitte Luxembourg Deloitte China (Hong Kong)

E-Mail: yknel@deloitte.lu E-Mail: cecarnoye@deloitte.com.hk

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 2Day 2: Real estate and debt funds

Cayman economic substance law (“Cayman ES Law”)

Cayman

GP

Banking Insurance

Fund Cayman

Holding LP

Cayman

entities Mgmt. Manager

Intellectual

property Relevant Financing Cayman Co Advisor

Activities

Loan

Dist. &

Service

Leasing SPV

Shipping Headquarters

RE

• The requirements impact certain companies and partnerships established or doing business in Bermuda, the BVI, or the Cayman Islands,

if these entities are engaged in a “relevant activity”

• Entities which are able to demonstrate tax residency in another jurisdiction are deemed out of scope for the purposes of the economic

substance requirements

• The list of relevant activities was defined by the EU and as such is mostly consistent across all jurisdictions

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 3Day 2: Real estate and debt funds

Luxembourg Pan Asian Investment Structures

Distribution

• Worldwide recognition of the Luxembourg brand (EU distribution

passports not accessible for non-EU/AIFMD funds)

Asia fund structure Lux (parallel) fund Legal forms to accommodate any promoter and

Non-EU investors EU investors investors needs

• Corporate (public or private companies)

Foreign • Partnerships (limited , limited by shares, etc.)

IM • FCP (trust)

• Possible check-the-box election for US tax purposes

Portfolio mgt.

delegation Onshore tax neutral platform in a post-BEPS world

• Tax neutrality for all funds in principle

Fund Fund • Tax transparent or opaque structures available

management management

Lux • Treaty access (for certain forms)

Fund ManCo Lux • BEPS – MLI/PPT: convergence between regulatory and tax

AIFM AIF requirements

Risk mgt. &

oversight

delegation Regulation and easy ongoing process

• Regulated and unregulated options available

HoldCo • “rent” third party licensed ManCo (AIFM) with portfolio delegation

• Compliance aspects managed by EU licensed entity (trustworthy)

• Very affordable unregulated versions of partnership available (if

size < 500M EUR)

Structure (for Asia based managers)

• Structuring of tax neutral carried interest and management fee for

Investments Asia-based asset managers

• Standalone or compatible with any existing fund structure

• Operating model similar to offshore structure (Cayman LP vs. Lux

SCSP for example)

• Asian outbound is also possible: for example Asian platform into a

Lux fund platform

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 4Day 2: Real estate and debt funds

Distributing in Asia: Qualified Domestic Limited Partnership (“QDLP”) Structure

China considerations

PRC LP’s • Flow through for PRC direct tax purposes:

Taxable in the hands of LP’s

25% PRC EIT for corporate (No withholding

obligations by QDLP Fund)

GP

PRC IIT at (i) 20% or (ii) 5% to 35% for

Management Individual investors (withholding obligations

company by QDLP Fund)

QDLP

China • PRC VAT:

Overseas

Not a flow through

Overseas LP’s

Unclear from a tax technical perspective

Offshore Fund whether disposal of offshore investment

(Lux etc.) product is VAT taxable

Practically we haven't seen QDLP paying VAT

Investmen • Management fee and carried fully taxable

t portfolio

• Transfer pricing issue on the management fee split

between PRC FMC and offshore FMC

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 5Day 2: Real estate and debt funds

Luxembourg FCP

General features of the Luxembourg FCP

• A FCP in Luxembourg is the acronym from “Fonds Commun du

Placement”, which represents a common investment fund that is

registered as an open-ended mutual fund.

• FCP does not have a legal personality.

Japanese Investors

FCP as a tax efficient vehicle

• Tax neutrality for Luxembourg FCP funds.

• Tax transparency – no WHT levied on distributions.

Fund

management

• Not subject to CIT/MBT/NWT but to an annual subscription tax

ManCo charged at the rate of 0.01% on its total NAV.

FCP

Regulation and easy ongoing process

• Regulated and unregulated options available.

Structure (for Asia based managers)

HoldCo

• Operating model similar to offshore structure.

• Asian outbound is also possible : for example Asian platform into

a Lux fund platform.

• Japanese investors may have a clear preference for the "unit" of

Investments an FCP since it provides for easier accounting valuations in their

books.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 6Day 2: Real estate and debt funds

Another typical Pan Asian Real Estate Structure

Investors Investors

Lux Fund

HK/SG/Lux

Only for

qualifying

investors

Non resident GK REF/ MIT

SG PropCo SPV (HK/SG/Lux)

PropCo TK PQIF

China

Bank Property Trust

debt

HK Sing Japan Korea China Australia

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 7Day 2: Real estate and debt funds

AM in China with foreign investors: Qualified Foreign Limited Partnership (“QFLP”)

China considerations

Overseas LP’s

• Obtain QFLP License

• Facilitated foreign exchange control

WHT • Allow foreign and local investors to co-live in a

Overseas China managed fund

China • QFLP is tax transparent and not subject to EIT on its

PRC LP’s profit

GP

• Taxation on a withholding basis upon remittance

• 10% or 25% tax uncertainty: Permanent

establishment issue

QFLP

x

SPV

Investment

portfolio

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 8Appendix Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 9

Day 2: Real estate and debt funds

Luxembourg fund toolbox (1/2)

Largest cross-border investment Prime location in EU for alternative

Leader in global fund investments

fund center worldwide

distribution

€ 4,9 + trillion Total Net AuM (regulated only) 1200+ RAIF setup in 3.5 years as well as many partnerships

Luxembourg funds are distributed in more

More than doubled over the past 10 years due to AIFMD, set up

than 70 countries

Brexit, BEPs, etc.

58% Global market share in cross-border 90% of global private equity investments are structured using

€ 815 billion in AuM by regulated alternative funds Luxembourg vehicles

investment funds

and a significant amount unknown in non regulated Presence of largest players :

products (RAIF, AIF SCS/SCSp, SPV) 9/ 10 global PE players

14/15 global RE players

10/ 20 global Hedge funds players have operations in Luxembourg

601 AIFMs (licensed alternative managers) registered with the CSSF

Non Regulated

SCS / SCSP

(Partnership) SOPARFI

Lightly

(SPV)

Regulated

Securitization

SIF RAIF

UCI II

UCITS SICAR

More

Regulated

* Under conditions

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 10Day 2: Real estate and debt funds

Luxembourg fund toolbox (2/2)

Type of fund Legal forms Compar Type Risk Time to Reg. Investors’ Global reach Taxation Double

available? tment? Assets spread? market Approv type tax

? treaty*

UCITS Corporate or Yes listed High Up to 6 Yes All including Distributed in Tax exempt, Yes (50pc

transparent transferra months retail 70+jurisdictions small dtt network

ble EU Passport subscription tax for

securities with exemption corporate

forms)

UCI II Corporate or Yes Private Moderate Up to 6 Yes All including Worldwide Tax exempt, Yes (50pc

transparent Equity, months retail EUP possible small dtt network

Real subscription tax for

Estate with exemption corporate

and forms)

Hedge

Funds

SIF Corporate or Yes All Low (at least Up to 3 Yes Institutional, Worldwide Tax exempt, Yes (50pc

transparent 3 assets) months professional EUP possible small network for

and HNW eg subscription tax corporate

Well-informed with exemption forms)

SICAR Corporate or Yes PE / risk None Up to 3 Yes Well-informed Worldwide Taxable but Yes (full)

transparent capital months EUP possible exempt on

eligible securities

and transit funds

RAIF Corporate or Yes (All/risk (Low / Days No (only Well-informed Worldwide (SIF / Sicar Yes (50pc /

(SIF/SICAR) transparent capital) None) AIFM) EUP possible regime) full)

SCS / SCSP Transparent No All None Days None No restriction Worldwide Tax transparent No

(as Alternative SCSP legal EUP possible

Investment personality

Fund)

SOPARFI (SPV) corporate No All None Days None No restriction Worldwide Taxable with Yes (full)

exemptions

available

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 11Deloitte 2021 M&A Tax Virtual Conference Break-out session France: Current trends in the structuring of French RE deals 02 MARCH 2021

Day 2: Real estate and debt funds

Introduction and Contacts

Sarvi Keyhani

Tax Partner

Paris

E-Mail: skeyhani@taj.fr

“Real estate is an imperishable asset,

ever increasing in value. It is the most

solid security that human ingenuity has

devised. It is the basis of all security

and about the only indestructible

security.” -Russell Sage

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 2Contents Typical French Real Estate Investment Structures 4 • Overview • REIT type structures (OPCI) • Standard “corporate” structures Areas of tax audit and Challenges with the FTA 8 • Interest rate on related party debt • French 3% tax on property Legislative measures of interest 12 • Sale and leaseback • Free revaluation of assets Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 3

Typical French Real Estate Investment Structures Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 4

Day 2: Real estate and debt funds

Typical French Real Estate Investment structures

REAL ESTATE INVESTMENT

Typical structures IN FRANCE

Option 1 Option 2 Assumptions:

• French property acquired for investment purposes (vs. trading)

• The investment Fund is established in the EU

Investors Investors

• Investors are composed of private or public, natural or legal, EU or non-

EU residents

At acquisition

Fund

IBL

Fund

IBL

• Standard CIT structure vs. OPCI ?

IBL IBL

• Choice of legal form / tax regime (REIT vs. Non-REIT, opaque vs. tax

transparency)

• Transfer tax costs and VAT

HoldCo

OPCI SAS • Debt?

During the holding period

• Taxation of rental income

• Transfer pricing, interest rate and other rules for deductibility of financial

expenses

• Cash repatriation

SCI 1 SCI 2 SCI 1 SCI 2 • Local taxes

• 3% tax obligations

At exit

• Share deal or asset deal

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 5You can also read