No - Beef + Lamb New Zealand

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

no 0

Contents

LAMB 23

CONTENTS .............................................................................1 MUTTON 23

FOREWORD ...........................................................................3 BEEF OUTLOOK 2020-21 – OPPORTUNITIES AND CHALLENGES

© 2020 Beef + Lamb New EXECUTIVE SUMMARY – OUTLOOK 2020-21 ..........................4 ............................................................................................ 24

Zealand Limited also OVERVIEW 4 BEEF & VEAL EXPORTS ......................................................... 25

referred to as B+LNZ,

B+LNZ - Economic Service ECONOMIC CONDITIONS 4 BEEF – INTERNATIONAL SITUATION ..................................... 27

and the Economic Service. LAMB AND MUTTON 4 OVERVIEW 27

BEEF 4 CHINA 27

All rights reserved. This

work is covered by

LIVESTOCK NUMBERS 5 UNITED STATES 29

copyright and may not be SHEEP AND BEEF FARMS 5 AUSTRALIA 30

stored, reproduced or ECONOMIC CONDITIONS .......................................................6 SOUTH AMERICA 30

copied without the prior THE GLOBAL ECONOMY 6 CATTLE PRICES – FARM-GATE .............................................. 32

written permission of Beef + NEW ZEALAND 7 BEEF PRODUCTION .............................................................. 33

Lamb New Zealand Limited. CONSUMER PRICES 8 CATTLE SLAUGHTER 33

Beef + Lamb New Zealand INTEREST RATES 9 CATTLE WEIGHTS 33

Limited, its employees and EXCHANGE RATES 9 BEEF PRODUCTION 33

Directors shall not be liable GLOBAL TRADE 10 PRICES 34

for any loss or damage

sustained by any person

TRADE CHALLENGES 10 EXPORTS 34

relying on the forecasts TRADE OPPORTUNITIES 10 WOOL1................................................................................. 34

contained in this document, EXCHANGE RATE SENSITIVITY – 2020-21 .............................. 11 PRODUCTION 35

whatever the cause of such SHEEP 12 SHEARING 35

loss or damage. LIVESTOCK NUMBERS .......................................................... 12 AUTUMN 2020 SUMMARY 36

Beef + Lamb New Zealand BEEF CATTLE 12 CLIMATIC CONDITIONS ........................................................ 36

PO Box 121 DAIRY CATTLE 12 OUTLOOK – AUGUST TO OCTOBER 2020 37

Wellington 6140 SHEEPMEAT OUTLOOK 2020-21 – OPPORTUNITIES AND FARM REVENUE, EXPENDITURE & PROFIT – NEW ZEALAND 38

New Zealand CHALLENGES ........................................................................ 13 REVENUE 38

Phone: 04 473 9150

Fax: 04 474 0800 LAMB 14 EXPENDITURE 38

E-mail: econ@beeflambnz.com LAMB & MUTTON EXPORTS ................................................. 14 FARM PROFIT BEFORE TAX 39

MUTTON 16 FARM REVENUE, EXPENDITURE & PROFIT – REGIONAL ....... 41

Contact:

OVERVIEW 17 EBITRM 41

Andrew Burtt: 04 474 0842

Chief Economist LAMB & MUTTON – INTERNATIONAL SITUATION ................ 17 NORTH ISLAND SUMMARY 41

Rob Davison: 04 471 6034 CHINA 17 SOUTH ISLAND SUMMARY 41

Executive Director AUSTRALIA 18 REGIONAL COMMENT – NORTH ISLAND .............................. 42

Rachel Agnew: EU-27 & UK 19 NORTHLAND–WAIKATO–BAY OF PLENTY 42

027 294 1276 UNITED STATES 20 EAST COAST 43

Senior Agricultural Analyst

James Cho: 04 474 8030

LAMB & SHEEP PRICES – FARM-GATE .................................. 22 TARANAKI–MANAWATU 43

Senior Agricultural Analyst LAMB & MUTTON PRODUCTION.......................................... 23 REGIONAL COMMENT – SOUTH ISLAND .............................. 44

1

MARLBOROUGH–

CANTERBURY 44

OTAGO–SOUTHLAND 44

2Foreword About this report The New Season Outlook 2020-21 presents projections for sheepmeat and beef production, exports, farm-gate prices and on-farm profitability. It also provides an overview of key international markets. It has been prepared at a time of considerable volatility and uncertainty. The outlook is based on market intelligence available until mid-September 2020 and reflects the COVID-19 impact domestically and globally to that point in time. There is little certainty around the continued spread of the virus. The forecasts in this report are subject to the limitations of the uncertainty and the constantly evolving situation. 3

Executive Summary – Outlook 2020-21

Overview Economic Conditions Lamb and Mutton The outlook for mutton in 2020-21 is

also uncertain, driven by the same

Beef and sheepmeat exports face an There are many variables that will For 2020-21, total lamb export factors as for lamb.

uncertain outlook for the 2020-21 influence the outlook for global growth receipts are forecast at $2.94 billion

season as economic disruptions from in the 2020-21 season. These include FOB, down 14.8 per cent on 2019-20. In 2020-21, mutton export production

the COVID-19 pandemic continue to the persistence of the spread of Co-products are forecast to decline a is forecast to decline 10 per cent, as

impact consumer demand. COVID-19, with many countries further 7.9 per cent. farmers maintain their breeding ewe

experiencing second waves, the flocks following the 2020 drought.

Despite this, there are solid underlying Lamb exports are forecast to be down

market fundamentals that will continue duration and reoccurrence of 6.5 per cent to 280,000 tonnes The average FOB value per tonne is

to support demand for New Zealand lockdown restrictions, the subsequent shipped weight, driven by a lower forecast to decline 7 per cent but will

sheep and beef exports. Chinese impact on economic activity and the 2020 lamb crop. still be above the five-year average.

demand for meat protein continues to implementation of fiscal and monetary

policy support in individual countries. Average export returns for the season Total mutton export receipts are

be fuelled by African Swine Fever pork

are forecast to decline 9.3 per cent to forecast to decline 15.6 per cent on

shortages and there is growing On a positive note for the New $9,841 per tonne but remain 3 per 2019-20, to $605 million, dropping

demand for high quality, nutritionally Zealand red meat sector, the primary cent above the five-year average. below the five-year average.

rich proteins. A shifting consumer food sector is expected to show

preference towards food safety will significantly more resilience to the COVID-19 has introduced uncertainty The annual average mutton price for

also support demand for New Zealand pandemic crisis compared to other into the outlook for sheepmeat. the 2020-21 season is forecast at

sheepmeat and beef. sectors. The demand for food Consumer demand has been 415-485 cents per kg with a midpoint

products has been more stable impacted by weaker economic of 447 cents per kg, a decline of

The global meat trading environment

compared to other commodities. conditions and the disruption to the 9 per cent on the 2019-20 estimate of

will face challenges in the 2020-21

foodservice sector will continue to be 490 cents per kg.

season. In addition to COVID-19 The deteriorating trade relationship a challenge for lamb exports in the

disruption, competitive pressure in key between the US and China is a cause 2020-21 season.

export markets is expected to increase of wariness in the global trading

and ongoing uncertainty exists around environment and some believe it has Although, the outlook is uncertain,

key trade negotiations. the potential to jeopardise underlying fundamentals remain solid,

international co-operation. driven by continued pork shortages in

New Zealand sheepmeat and beef

China, increasing demand for high

exports will not be immune to these The New Zealand economy has quality proteins and increasing

challenges, however the premium contracted in the first half of 2020 but disposable income in some Asian

attributes of New Zealand sheepmeat is expected to experience a degree of countries.

and beef make New Zealand products recovery in the second half. The

well positioned to weather the sharp contraction of global economies The weighted average lamb farm-gate

uncertainty. and the continuing closure of the price is forecast to be between 620

border are expected to weigh on the and 715 cents per kg with a midpoint

Total beef, veal and sheepmeat export

economy into the 2020-21 season. of 665 cents per kg, which is down

revenue for the 2020-21 season is

10 per cent on 2019-20. Despite the

forecast at $7.39 billion, down In response to the pandemic crisis, the decline, the midpoint forecast price is

12 per cent or $1 billion, from RBNZ is now expected to introduce a above the above the five-year

2019-20. negative OCR in 2021. average.

4Beef Livestock Numbers Wool Sheep and Beef Farms

Export revenue from beef and veal in The total number of sheep at 30 June Unfortunately, there is little optimism Gross farm revenue for the 2020-21

the 2020-21 season is forecast to be 2020 is estimated at 26.2 million, in the outlook for wool. farming year, which ends on 30 June,

$3.85 billion FOB, down 9 per cent on down 2.3 per cent on the previous is forecast to average $559,300 per

2019-20. June and 55 per cent lower than in The outlook for 2020-21 is for wool farm – down 10 per cent.

1990. exports to decline 2.8 per cent on

Beef and veal exports are forecast to 2019-20. The sheep and cattle revenue

be steady on 2019-20 at 453,000 The number of beef cattle at 30 June accounts, which combined account for

tonnes shipped weight. 2020 is estimated at 3.89 million, Average export receipts at FOB are three-quarters of gross farm revenue,

unchanged on the previous June and expected to decrease 34 per cent to are forecast to decline to levels below

The number of cattle processed for down 15 per cent on 1990-91. The $3,700 per tonne, following an

export in 2020-21 is forecast to 2017-18, while wool is forecast to be

change in the latest year was largely 18 per cent drop the previous year. about 30 per cent lower than in

decline marginally (-0.9%) on 2019-20 driven by little change in the number

and export beef production is forecast Total wool receipts are forecast to 2017-18, clearly reflecting the very

of weaners overall, after there was a challenging circumstances in the wool

to be mainly steady at 661,000 tonnes drop 36 per cent on the previous year

high base of trade cattle and weaners sector, and, revenue from dairy

carcase weight. to an estimated at $276 million.

on hand on 30 June 2019, particularly grazing is forecast to be similar to

Average export returns for the season in the South Island. The estimate for the overall auction 2017-18.

are forecast to decline 9.5 percent to wool price is down 20 per cent on

The number of dairy cattle at 30 June Sheep revenue is forecast to decrease

$7,445 per tonne. 2019-20.

2020 is estimated to have decreased by 14 per cent to average $267,500

The global beef market will face 2.1 per cent to 6.25 million. The per farm for 2020-21.

uncertainty due to COVID-19 in the number of dairy cows in milk is

2020-21 season. Consumer demand estimated to have decreased by a Cattle revenue decreases 5.0 per cent

has been weakened by economic similar percentage (-2.5%). to average $151,600 per farm due to

uncertainty and the disruption to steady international demand for New

foodservice sector demand will also Zealand beef but some easing in

impact beef demand. prices for cattle.

Global beef trade is expected to grow A 24 per cent decrease in wool

increasingly competitive in the 2020- revenue to $25,500 per farm is

21 season. forecast for 2020-21. Wool revenue

accounts for less than five per cent of

At USD0.66, the estimated 2020-21 gross farm revenue, the lowest level

average annual price for P steer/heifer on record.

(270-295kg) is 515 cents per kg. It is

forecast to average 364 cents per kg Dairy grazing revenue is forecast to be

for M cow (170-195kg), which includes almost unchanged (-0.7%) averaging

a large component of cull dairy cows, $28,400 per farm (and five per cent of

and 480 cents per kg for M bull (270- gross farm revenue) in 2020-21.

295kg).

5Economic Conditions

The Global Economy impact on economic activity and the of calendar 2020 declined recession. China’s growth prospects

implementation of fiscal and monetary 3.75 per cent. The full extent of the rely on the ability to stimulate

The COVID-19 pandemic has pushed

policy support in individual countries. impact of COVID-19 on trade in 2020 consumer demand and boost the

the global economy into the deepest service sector, which contributes more

is still unclear, however economists

recession since the Great Depression On a positive note for the New from the World Trade Organisation than 60 per cent to its economic

in the 1930s. Steep declines in Zealand red meat sector, while most growth.

(WTO) have estimated that world

economic growth are being recorded markets are projecting a major global trade could decline between 13 and

in all major economies, excluding economic downturn, the primary food Other key factors impacting China’s

32 per cent.

China, unemployment is soaring, sector is expected to show economic outlook include any

consumer spending has slumped and significantly more resilience to the The outlook is for a swift recovery in resurgence of COVID-19, the

the purchasing power of key New pandemic crisis compared to other 2021 (albeit after a precipitous fall), weakening trade relationship with the

Zealand markets has been restricted. sectors. The demand for food however expectations are that global US, which is discussed later in the

products has been more stable GDP will still remain below report, and recovery from the

There are many variables that will compared to commodities such as oil. pre-COVID-19 levels in 2021. extensive flooding experienced in

influence the outlook for global growth. mid-2020.

These include the persistence of the Global trade contracted through the The global trade environment has

spread of COVID-19, with many first half of 2020, driven by the lack of been marred by rising protectionism, Food security is an evolving issue in

countries experiencing second waves, international tourism and weaker which has been accelerated this year China. The country has endured

the duration and reoccurrence of overall demand. The volume of goods by COVID-19. The escalating months of severe flooding and insect

lockdown restrictions, the subsequent and services traded in the first quarter US-China trade war is also causing infestations, on top of African Swine

increasing wariness in the global Fever (ASF) and COVID-19. There is

Table 1 Economic Growth trading environment, and some growing speculation that the country

Annual Average % Change, March Year believe it has the potential to may be facing a shortage of grain, as

2017 2018 2019 2020e 2021f 2022f jeopardise international co-operation well as pork. This speculation was

and prospects of freer trade. fuelled by an announcement by the

% % % % % %

Chinese government in mid-August of

US +1.8 +2.6 +2.8 +1.7 -6.4 +2.2 China its Clean Plates Campaign, which is

UK +2.0 +1.6 +1.6 +0.5 -13.8 +3.2 China is one of the few economies intended to curb food waste and

Euro zone +1.9 +2.8 +1.6 +0.1 -10.1 +3.0 expected to experience growth this described the problem of food waste

Japan +0.9 +2.0 +0.3 -0.0 -6.8 +0.9 year. China’s economy contracted as “shocking and distressing”. This

sharply in the first quarter of 2020 follows a call for the need to stabilise

China +6.9 +6.9 +6.6 +2.7 +2.7 +6.5

(-10.1%), however economic activity agriculture and ensure the safety of

South Korea +3.0 +3.2 +2.5 +2.0 -1.4 +2.6 rebounded swiftly once lockdown grain and major non-staple foods.

Australia +2.6 +2.7 +2.4 +1.7 -1.7 +1.8 restrictions were lifted, supported by Record import volumes of wheat, rice,

fiscal and monetary policy stimulus. rapeseed, as well as meat, have been

Trading Partners +3.7 +4.2 +3.7 +1.7 -2.7 +3.7 Economic activity recovered in the recorded in 2020, and food prices in

second quarter and the economy grew China rose 10 per cent in the 12

(+11%). months to July 2020.

New Zealand +3.7 +3.2 +3.1 +1.5 -8.2 +4.5

Note: "Euro zone" are 15 Member States: Belgium, Germany, Ireland, Greece, Spain,

Economic recovery in the second half ASF, which is a highly contagious

Cyprus, Malta, France, Italy, Luxembourg, the Netherlands, Austria, Portugal, Finland and of 2020 is expected to be constrained disease in pigs but does not affect

Slovenia. by weaker consumer demand and the humans, continues to adversely

"Trading Partners" account for about 85% of New Zealand's total merchandise trade. continued expectation of a global impact Chinese meat production, and

6

e estimate, f forecast | Source: Statistics New Zealand, NZIER Quarterly Predictionsremains a key driver of demand for pork from other EU countries, Brazil more Chinese consumers to purchase and the economic this may have on

New Zealand sheepmeat and beef and the US. beef and sheepmeat. While the return the economy.

exports in 2020-21. Analysts report to full capacity pork production

that up to 45 per cent of China’s sow Chinese pork production between following recovery from ASF may The outcome of the elections on

herd have been lost to ASF, and while 2018 and 2020 is estimated to have result in Chinese consumers reverting 3 November will be a key point of

herd recovery is underway, pig dropped by just under 40 per cent or to pork as the protein of choice, there focus for the US economy, and

numbers are still expected to only be around 27 million tonnes. The Chinese are increasing signals the more financial markets will focus on this in

at 80 per cent of pre-ASF levels by the Bureau of Statistics shows that affluent consumers may choose beef the lead-up to November.

end of 2021. Chinese pork output for the first six or sheepmeat as a higher quality,

months of 2020 dropped 20 per cent New Zealand

nutritionally rich protein source.

ASF outbreaks continue to be on 2019. The New Zealand economy has faced

reported through 2020, in China as US unprecedented change during 2020.

well as other countries, signalling the Pork is the largest source of meat

The outbreak of COVID-19 has been The COVID-19 pandemic introduced a

continuing relevance of this disease in protein consumed in China. Chinese

severe in the US. Human health and new economic playing field in New

world protein demand. In September pork imports soared through 2019 and

in 2020 in response to the shortage. In economic conditions have met Zealand and across the globe, where

2020, the first case of ASF was unprecedented adversity. The the rules are largely unknown by

confirmed in Germany – in a wild boar. the first six months of 2020, China’s

pork imports rose a staggering pandemic has been slow to release anyone.

Imports of German pork were it’s grip on the US, however, at the

subsequently banned by China and 153 per cent. The New Zealand economy

time of writing in September there was contracted in the first half of 2020, with

several other countries. Germany is The shortage of pork caused prices to evidence of progress in the

the third largest supplier of pork to surge, and alternative meat protein GDP contracting by 12 per cent in the

management of COVID-19, with falling June quarter. The recession was

China following the US and Spain. sources such as beef and sheepmeat fatality rates and rising economic

However, reports indicate that the gap expected by economists, given the

to become more competitive. activity.

left by the absence of German pork in level of disruption from COVID-19.

China is likely to filled adequately by Price and the increasingly important The US economy contracted sharply The focus for the New Zealand

issue of food safety have encouraged in the second quarter of 2020. In economy for the second half of 2020

March and April, more than 20 million will shift to the speed of recovery and

Figure 1 Change in New Zealand Real GDP jobs were lost. Consumer confidence a move from recession. A lack of

was severely shaken, and consumer restrictions and sharp lift in economic

Annual % change March year activity in the third quarter of 2020 will

spending, which is a key driver of the

6.0 economy, was well down. However, support a recovery, however

macroeconomic reveals that April took economists remain wary of the sharp

4.0 the brunt of the impact, and recovery contraction of global economies and

is expected during the third quarter. the fact that the largest impact of the

Annual % change

2.0 border closure is still to be felt as

Employment has rebounded more activity typically peaks between

0.0 rapidly than expected and some

2017 2018 2019 2020e 2021f 2022f October and March.

-2.0 estimates signal that GDP has the

potential to return to the average of While economic shock of COVID-19

-4.0 2019, by the end of 2020. lockdown restrictions are, for now,

behind us, economists warn that the

-6.0 Downside risk remains significant, full impact of the closed border will be

however. The threat of a resurgence felt for many months ahead. The

-8.0 in COVID-19 cases is real, and there absence of international tourism,

is also wariness surrounding the international students and the migrant

-10.0 escalation of the US-China trade war labour force will be felt into the first

e estimate, f forecast

7Source: Beef + Lamb New Zealand Economic Service, NZIER Quarterly PredictionsTable 2 Consumer Prices from meat, dairy and horticulture, The impact of the drought on the New

particularly kiwifruit, have all displayed Zealand economy was overshadowed

Annual Average % Change, March Year resilience so far in 2020. Returns by COVID-19. Sheep and beef farm

2017 2018 2019 2020e 2021f 2022f from forestry fell as log prices revenues will be affected through loss

% % % % % % reflected the effects of reduced global of income and higher expenses. The

US +1.6 +2.1 +2.3 +1.9 +0.7 +1.6 construction demand. The annual impact will be felt most notably on the

merchandise trade balance is East Coast of the North Island. More

UK +1.1 +2.8 +2.3 +1.7 +0.7 +1.3

strengthening, with year-on-year data detail is provided below.

Euro zone +0.7 +1.4 +1.8 +1.1 +0.3 +1.0 signalling 8.6 per cent growth in

Japan -0.1 +0.7 +0.7 +0.5 +0.0 +0.1 exports over a 16 per cent decline in Consumer Prices

China +1.9 +1.8 +2.0 +3.7 +2.6 +2.1 imports. The Consumer Price Index (CPI) for

South Korea +1.3 +1.7 +1.3 +0.5 +0.2 +0.9 the June 2020 quarter dropped

The New Zealand pastoral sector has

Australia +1.5 +1.9 +1.8 +1.8 +0.1 +1.4 0.5 per cent on the March quarter –

had an extremely challenging year,

the first quarterly deflation in over five

with one of the worst, if not the worst,

years.

Trading Partners +3.5 +1.7 +1.7 +1.8 +0.6 +1.4 droughts recorded. On 12 March 2020

the entire North Island, parts of the Transport was the largest contributor

South Island and the Chatham Islands to the decline (-4.9%), driven by a

New Zealand +1.1 +1.6 +1.7 +1.9 +1.0 +1.0

were declared as being in drought by 12 per cent drop in petrol prices for

Note: "Euro zone" are 15 Member States: Belgium, Germany, Ireland, Greece, Spain, Agriculture Minister Damien O’Connor. the quarter, the largest fall since the

Cyprus, Malta, France, Italy, Luxembourg, the Netherlands, Austria, Portugal, Finland and The impact of the 2020 drought was 2008 financial crisis. This reflects the

Slovenia.

felt throughout the entire North Island weak demand for oil during March and

"Trading Partners" account for about 85% of New Zealand's total merchandise trade.

and upper South Island, with the full April as major economies shut down.

e estimate, f forecast | Source: Statistics New Zealand, NZIER Quarterly Predictions

impact hitting the East Coast of the

quarter of 2021, or until border spread of the virus overseas, also North Island.

restrictions are eased. adds to the uncertainty. Policy

The extent of Government fiscal

makers as well as the New Zealand Table 3 Short-term Interest Rates

population were reminded that the

stimulus in the first half of 2020 has risk of further outbreaks is very real.

% p.a., March Year

supported the New Zealand economy 2017 2018 2019 2020e 2021f 2022f

successfully, as indicated by better The overall confidence of New % % % % % %

than expected data from the Zealand consumers and businesses

US 0.5 1.4 2.5 1.6 0.1 0.4

pre-election fiscal update (PREFU) in has been shaken, and caution has

September 2020. However, there is grown. Unemployment is rising, job UK 0.0 0.3 0.7 0.7 0.0 0.0

some wariness surrounding how this security is uncertain for some, and Euro zone -0.4 -0.3 -0.3 -0.4 -0.5 -0.5

stimulus may be sheltering the investment and spending will be Japan 0.1 0.1 0.0 0.0 0.0 0.2

economy and the impact as the down. Australia 1.8 1.8 2.1 0.9 0.1 0.3

support spending of wage subsidies

and COVID-19 relief payments begin The second wave of COVID-19 in

to roll off. These factors all provide New Zealand also resulted in the New Zealand 2.0 1.9 1.9 1.1 0.4 -0.1

uncertainty to the outlook for the New general election being delayed four Note: "Euro zone" are 15 Member States: Belgium, Germany, Ireland, Greece, Spain,

Zealand economy weeks to 17 October 2020. Cyprus, Malta, France, Italy, Luxembourg, the Netherlands, Austria, Portugal, Finland and

New Zealand’s food exports have Slovenia.

The emergence of the second wave of "Trading Partners" account for about 85% of New Zealand's total merchandise trade.

COVID-19 in New Zealand in August performed solidly during the

e estimate, f forecast | Source: Statistics New Zealand, NZIER Quarterly Predictions

2020, combined with the continuing COVID-19 disruption as international

demand for food lifts. Export returns

8Food prices lifted 1.1 per cent, commitment was made to keep it at Figure 3 Meat Exports by Currency of Trade

influenced by a 16 per cent rise in that level for at least 12 months.

vegetable prices, which was driven by Oct 2019 - Aug 2020

disruption to the food production In mid-August 2020, the RBNZ

signalled increasing monetary policy 0% 20% 40% 60% 80% 100%

process during the period of

COVID-19 lockdown. support for the COVID-19-affected

economy, by expressing a preference Beef

Annual inflation was 1.5 per cent in to move to a negative OCR. It also

the year ending June 2020. The key introduced a “funding for lending”

drivers of the increase were higher programme to provide support for Lamb

housing costs (+3.2%), and higher banks in a negative interest rate

food costs (+3.7%). scenario. This programme would lend

money directly to the banks to ensure Mutton

The impact of COVID-19 is expected that a lower benchmark rate would be

to continue to be felt in the medium passed onto customers. Economists

and long term. Projections are for the are now forecasting a move to a Total

CPI to ease as the economic negative OCR in April 2021.

contraction weighs on inflation.

USD EUR CNY GBP Other

Exchange Rates

Interest Rates Source: Beef + Lamb New Zealand Economic Service | New Zealand Customs

Interest rates have dropped to all-time Exchange rate forecasts are

lows in 2020 as the Reserve Bank of challenging even when global markets

weaker NZD through March and April major global economies and the

New Zealand (RBNZ) attempts to are stable. A combination of

provided some support for New deteriorating relationship between the

soften the impact of COVID-19 on the COVID-19 and subsequent economic

Zealand exporters in an otherwise US and China.

New Zealand economy. impacts, and geopolitical tension

disrupted market.

makes a volatile backdrop for foreign The outlook for 2020-21 is for the NZD

All around the world, central banks exchange projections. The rapidly Despite continued easing in monetary to appreciate against the USD by

quickly responded to COVID-19 with changing global and domestic policy by the RBNZ, the NZD began to 3.6 per cent on 2019-20 (Table 4).

expansionary monetary policy environment introduces risk to the lift from May. This partly reflected the

measures. forecasts in this report. success of New Zealand in eliminating For the first eleven months of

the virus as well as ongoing strong 2019-20, 76 per cent of total meat

The initial outbreak of COVID-19 in The NZD depreciated sharply as the export volume was reported as being

New Zealand in March 2020 resulted commodity prices.

impact of the initial wave of COVID-19 traded in USD-denominated contracts.

in the RBNZ making an emergency hit the economy and weakened the The NZD remained strong through The Chinese yuan has maintained its

75 basis points cut to the Official Cash growth outlook. The NZD dropped to mid-2020 with the NZD reaching a position as the next most significant

Rate (OCR) – to 0.25 per cent. A a low of USD0.5670 in March 2020. A 16-month high in September of currency, with 7.4 per cent of New

USD0.6798. The stronger tone was Zealand’s red meat exports traded in

Table 4 New Zealand Dollar Exchange Rates despite signals from the RBNZ of this currency. However, this

Annual Average further cuts to the OCR in early 2021. decreased from 8.1 per cent in the

Sep Year USD GBP EUR Monetary policy measures expected in 2018-19 season, reflecting the

2021 will be a key driver of the disruption in the Chinese market

2018-19 0.67 0.52 0.59 direction of the NZD. during COVID-19. The EUR and GBP

2019-20e 0.64 0.52 0.59 account for 5.9 and 4.4 per cent of red

Global risk is also a factor in the meat exports respectively.

2020-21f 0.66 0.50 0.57

outlook. Economists are monitoring

2020-21f % change +3.6% -4.0% -3.3% closely the spread of COVID-19 in

e estimate, f forecast

9Source: Beef + Lamb New Zealand Economic Service, Reserve Bank of New ZealandGlobal Trade and the UK domestic market becomes eliminated tariffs for a certain number commitments may become less easy

oversupplied. of agricultural products, including beef. to enforce.

Brexit The US now enjoys the same tariffs

The UK's departure from the EU, US-China on beef into Japan as New Zealand Trade opportunities

scheduled for 31 December 2020, is The relationship between the US and and Australia do under the New Zealand is continuing to pursue

one of the most concerning trade China is deteriorating. The two Comprehensive and Progressive new trade arrangements and

issues for New Zealand red meat, countries are engaging in a cycle of Agreement for Trans-Pacific innovative trade policy approaches.

particularly sheep, exporters. retaliation against each other, Partnership (CPTPP). The US New Zealand is currently negotiating

including stepping up sanctions on responded quickly to the lower tariff Free Trade Agreements (FTAs) with

While the UK and EU are currently officials. This escalating situation is rate; Japan’s imports of US beef lifted the EU and the UK, aiming to

negotiating a trade deal that will apply

creating significant risk to the “Phase 8.5 per cent in the first half of 2020. conclude in 2021. As long-established

after departure date, at the time of One” deal, which was struck late in The increased presence of US beef in high-value markets, these FTAs

writing, the outcome did not look 2019 and sought to resolve the US- increased competitive pressure for present important opportunities,

promising. The risk of a “hard Brexit” China tensions. It included an New Zealand. particularly for beef exports, which are

was growing in probability. A “hard

undertaking by China to make very currently constrained by EU and UK

Brexit” would leave the UK with no significant purchases of US agriculture Trade challenges policy settings, but both the EU and

preferential trade access to the EU. exports, including red meat.

For New Zealand, the relevance of Outside of trade negotiations between UK have already signalled a high

this will be the UK’s loss of free trade The deal potentially placed New specific countries, there are other degree of sensitivity around opening

access to the continental EU for UK Zealand exports to China at a headwinds to consider. up their agriculture markets.

sheepmeat exports. While the UK is competitive disadvantage, particularly Rising protectionism has been a Separately, the Regional

seeking new trade avenues with other given China’s stated intention to growing concern for New Zealand Comprehensive Economic Partnership

countries, the outcome of these are loosen restrictions on the use of trade officials over the past three (RCEP) negotiations with a range of

long-term. In the short-term, a “hard hormone growth promotants in years. COVID-19 has accelerated this Asian trading partners and Australia

Brexit” may result in a decline in imported beef. trend, as major economies dispense have concluded, with likely modest

demand for New Zealand sheepmeat support to farmers. Both tariff and improvements in market access, but

exports to the UK as domestic product To date, however, the volumes of US

agricultural exports purchased by non-tariff barriers are a growing India (a big potential market for New

saturates the market. concern for the red-meat industry. Zealand lamb) pulling out of the deal

China have been well below the

New Zealand would be further mandated levels. The magnitude of Non-tariff barriers include subsidies before conclusion. Other negotiations

impacted by a decision from the EU the deficit increases the risk of China and other mechanisms that are in prospect include expansion of the

and UK, as part of the Brexit process, not meeting its commitment, unless it becoming more prevalent such as CPTPP to more trading partners in

to split New Zealand's current makes some unprecedented animal welfare and environmental Asia and potentially the UK and

sheepmeat and goat meat tariff-rate purchases in the second half of the standards. strengthened trade arrangements with

quota (TRQ) access equally between year. That is possible given the main countries in Latin America – but these

The World Trade Organisation (WTO) are likely to have a longer timeframe.

the UK and EU. Currently, the TRQ crop harvest occurs in the second half dispute settlement system is current

applies to the two markets combined. of the year in the US. being destabilised. The appeals

Splitting the TRQ would result in the process is no longer operational as a

loss of flexibility for New Zealand There is growing speculation that

tensions between the two countries result of US blocking new

exporters to shift sheepmeat between appointments to the Appellate Body.

the two markets in response to will be a long-term trend, with phases

of escalation and de-escalation. to appoint the necessary judges,

changing demand and price trends. While New Zealand has signed on to

The impact of this will be even more US-Japan an interim mechanism alongside a

pronounced if UK sheepmeat exports group of other WTO members, long-

In September 2019, Japan and the US

lose preferential access to the EU, established WTO rules and

signed a limited trade deal that

10Exchange Rate Sensitivity – 2020-21

Exchange rate movements have a from late November through to June, mutton and wool and thus farm

significant leveraged effect on which means that the value of the revenue.

farm-gate prices. NZD during this period is crucial to

farmers and export companies.

Table 5 shows farm-gate prices under Exchange rate movements during that

five different exchange rate scenarios. period strongly influence the

This approach provides an indication

season-average prices for beef, lamb,

of the impact of exchange rate

volatility on the prices paid to farmers. Table 5 Exchange Rate Sensitivity

The shaded column represents our NZD Exchange Rates

forecasts of exchange rates for the Exchange Rate Change from USD 0.66

major currencies and the related -10% -5% Forecast +5% +10% to USD 0.6 to USD 0.73

farm-gate prices used to derive the USD 0.60 0.63 0.66 0.69 0.73 -10% +10%

base estimates of export receipts and GBP 0.45 0.48 0.50 0.53 0.55 -10% +10%

farm revenue in this report. The four

other scenarios show the impact on EUR 0.51 0.54 0.57 0.60 0.63 -10% +10%

farm-gate prices of variations of ±5 Farm-Gate Prices Received

and ±10 per cent in the exchange $ / head

rates for the USD, GBP, and EUR.

Lamb 146 135 126 118 110 +15.5% -12.7%

In 2020-21, the NZD is expected to Mutton 137 126 116 107 99 +18.1% -14.8%

strengthen against the USD and ease Steer/Heifer 1,672 1,552 1,445 1,348 1,260 +15.7% -12.8%

against the GBP and EUR. Exchange

rate movement with the USD has the Cow 837 777 723 675 631 +15.7% -12.8%

greatest effect because 75 per cent of Bull 1,677 1,558 1,450 1,353 1,264 +15.7% -12.8%

New Zealand’s red meat exports are All Beef 1,348 1,252 1,165 1,087 1,016 +15.7% -12.8%

traded in this currency (Figure 3). c / kg

1

All other things being equal, a Lamb 768 714 665 621 581 +15.5% -12.7%

1

10 per cent decrease in the NZD Mutton 528 486 447 413 381 +18.1% -14.8%

against the USD – from 0.66 to 0.60 – Steer/Heifer 596 554 515 481 449 +15.7% -12.8%

and the associated cross rates against

Cow 421 391 364 339 317 +15.7% -12.8%

the GBP and the EUR, increases the

average lamb price received by Bull 555 516 480 448 419 +15.7% -12.8%

farmers by 15 per cent. Alternatively, if All Beef 532 494 460 429 401 +15.7% -12.8%

2

the NZD appreciates by 10 per cent – Fine 1,148 1,054 970 894 824 +18.4% -15.0%

from 0.66 to 0.73 against the USD –

Medium2 541 497 457 421 388 +18.4% -15.0%

then the weighted average farm-gate 2

price for lamb for the season would Crossbred 168 154 142 131 121 +18.4% -15.0%

2

decrease by 12 per cent. All Wool 251 230 212 195 180 +18.4% -15.0%

Meat and wool production is seasonal 1 includes wool and skin 2 wool ¢/kg greasy | Source: Beef + Lamb New Zealand Economic Service

with the majority of production sold

11Livestock Numbers

Sheep 2020 and the number of breeding Table 6 Livestock Numbers (million head)

ewes decreased 1.2 per cent.

The total number of sheep at 30 June Breeding Total Beef Dairy

Decreases in the number of breeding

2020 is estimated at 26.2 million, ewes occurred in East Coast (-2.7%) Ewes Hoggets Sheep Cattle Cattle

down 2.3 per cent on the previous and Taranaki-Manawatu (-1.1%) while 30 June 2019 16.85 9.14 26.82 3.89 6.26

June and 55 per cent lower than in there was an increase in Northland-

1990. This is the second year in a row 30 June 2020e 16.86 8.40 26.21 3.89 6.25

Waikato-Bay of Plenty (+1.6%). The

that sheep numbers have been below number of hoggets in the North Island

27 million. Within this, the number of 19-20 to 20-21 % change +0.1% -8.1% -2.3% +0.1% -0.1%

decreased 8.6 per cent with East

breeding ewes was unchanged and Coast estimated to have decreased by

e estimate

the number of hoggets decreased Source: Beef + Lamb New Zealand Economic Service | Statistics New Zealand

12 per cent, primarily in response to

8.1 per cent, which reflects two drought.

factors: carryover trade lambs on hand June 2019 that were processed in the The number of beef breeding cows

at 30 June 2019 that were processed In the South Island, the total number September 2019 quarter. The number decreased 7.8 per cent with the

in the September quarter of 2019, and of sheep decreased 1.1 per cent. This of breeding ewes increased largest decrease in East Coast

underlying changes in the retention of was made up of a small increase of 1.2 per cent after decreasing for many (-11.3%) in response to drought. The

younger animals. less than one per cent in years, due to several factors including magnitude of the change also

Otago/Southland and a larger conversions to dairy farming and the reflected an increase in the number of

In the North Island, the number of decrease in Marlborough (-3.5%), impacts of drought. trade cattle, underpinned by

sheep decreased 3.5 per cent dairy-beef, on hand as at 30 June

which reflected a relatively high After excellent lamb and mutton prices

(-466,000) to 12.7 million at 30 June 2019.

number of trade lambs on hand at 30 underwrote a deeper culling than

Figure 4 Livestock Numbers usual of poorer-performing sheep in In the South Island, the number of

70,000 7,000 2017-18 – partly offset by farmers beef cattle increased 2.5 per cent to

retaining ewe lambs – the younger 1.21 million at 30 June 2020.

breeding flock matured resulting in a

60,000 6,000 The number of beef cows decreased

decrease in the number of hoggets.

3.5 per cent, while the number of other

50,000 5,000 Beef Cattle cattle increased modestly (+1.3%).

Sheep (000)

Cattle (000)

40,000 4,000

The number of beef cattle at 30 June Dairy Cattle

2020 is estimated at 3.89 million,

unchanged on the previous June. This The number of dairy cattle at 30 June

30,000 3,000 was largely driven by little change in 2020 is estimated to have remained

the number of weaners overall (but static (-0.1%) at 6.25 million. The

20,000 2,000 some differences between regions), number of dairy cows in milk is also

and a high base of trade cattle and estimated to remain static (-0.2%).

1990-91

1992-93

1994-95

1996-97

1998-99

2000-01

2002-03

2004-05

2006-07

2008-09

2010-11

2012-13

2014-15

2016-17

2018-19

2020-21e

weaners on hand on 30 June 2019, The South Island contains 39 per cent

particularly in the South Island. of the New Zealand dairy herd, up

from around 35 per cent 10 years

Sheep Beef Dairy In the North Island, the number of beef earlier.

Source: Beef + Lamb New Zealand Economic Service | Statistics New Zealand cattle decreased 1.0 per cent to

2.68 million at 30 June 2020.

12Sheepmeat Outlook 2020-21 – Opportunities and Challenges 13

Lamb & Mutton Exports

Lamb 4 per cent on the same period in Figure 5 New Zealand Lamb Average Export Value

2018-19.

2019-20

A weaker NZD supported export 13,000

The 2019-20 sheepmeat export

Average FOB value ($/tonne)

season has been one of two returns in 2019-20. The annual 12,000

extremes. Exceptionally strong average value of the NZD was

11,000

demand from China, fuelled by the 4 per cent down on the 2018-19.

10,000

ASF-induced pork shortage, drove Export lamb production for the 2019-

record export returns for the first 20 season is expected to be down 9,000

quarter of the season. However, 1.6 per cent on 2018-19. A smaller 8,000

export returns slumped in late lamb crop in spring 2019, the 2020

December as Chinese demand 7,000

drought and COVID-19 have been

slowed following government drivers of export volumes. 6,000

intervention in the protein market. This 5,000

was followed closely by COVID-19 COVID-19 disruption has been the

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

disrupting all New Zealand’s key leading issue in New Zealand’s key

sheepmeat export markets. lamb export markets in 2020. The Prev. 5yr range 2017-2018 2018-2019 2019-2020

sharp decline in foodservice demand Source: Beef + Lamb New Zealand Economic Serv ice | New Zealand Customs

A weaker NZD buffered export returns has impacted the US, China, UK and

from the full impact of the EU-27. While retail demand is steadily The outbreak of COVID-19 has months from October 2019 to August

COVID-19-induced drop in export increasing in some of these markets, weakened the global economic 2020, export volumes to this market

prices in markets, however, the growth is not enough to offset the outlook. Consumers are wary lifted 7 per cent year-on-year and

disruptions to the foodservice sector deterioration in the foodservice trade. regarding emerging new waves of accounted for 45 per cent of total lamb

and weakening economic conditions COVID-19 and deteriorating economic exports, up from 35 per cent just two

have weighed on average export Sales of frozen middle lamb items in conditions. Exporters note that seasons earlier (in 2017-18). In the

values (Figure 5). particular, have been impacted by the consumers are increasingly price same two-year period, the average

decline in foodservice demand. sensitive, and the threat of protein FOB value of exports lifted an

The strong start to the export season

held up total receipts for lamb In the five months from April 2020 to substitution with cheaper pork and impressive 30 per cent, from $6,600

(including co-products) for the August 2020, the average export poultry products will challenge growth per tonne to $8,600. From October

2019-20 season. An increase of value of lamb racks was 21 per cent in demand for lamb. 2019 to August 2020 the average

1.7 per cent is estimated (Table 7). lower than in the same period of export value was 13 per cent higher

Growth in lamb import demand in the than in the same period of 2018-19.

2018-19. In contrast, demand for lamb short term is also being challenged by

Average export returns for 2019-20 sold in the retail trade, or that could be

are estimated to be up 4 per cent on reports of larger than typical volumes COVID-19 has disrupted trade to the

easily transferred to the retail sector, of sheepmeat held in storage. The EU (including UK) this season. From

the previous season, to average a fared much better. Exporters reported

record $10,850 per tonne. Data for decline in foodservice sector sales has October 2019 to August 2020, exports

the volume and value of chilled lamb resulted in key markets accumulating were 5 per cent lower than in 2018-19.

October 2019 to August 2020 sales were maintained and export

provides a solid foundation for this lamb in cool stores. For China, the

statistics show both chilled and frozen During April and May exports were 47

estimate, with approximately 95 per problem was exacerbated by high

legs maintained value in the months and 37 per cent lower than in the

cent of volume exported in this period. imported growth in late 2019.

following the initial outbreak. same months in 2019. Exports

This data shows an average export China continues to be New Zealand’s declined to the UK (-2%), Netherlands

value of $10,815 per tonne - up leading market for lamb. In the eleven (-9%) and France (-3%), but Germany

14Table 7 New Zealand Lamb Exports Lamb exports are forecast to be down

6.5 per cent to 284,000 tonnes

Lamb meat Co-Products Total Lamb Lamb Meat

shipped weight. A lower lamb crop in

Sep Year 000 tonnes $ / tonne $m FOB $m FOB $m FOB %* 2020 is the predominant driver of the

2016-17 295 8,603 2,538 168 2,706 94% decline. Average export returns for the

2017-18 313 10,086 3,156 199 3,355 94% season are forecast to decline

2018-19 305 10,445 3,186 203 3,389 94% 9.3 per cent to $9,841 per tonne.

2019-20e 300 10,850 3,255 190 3,445 94% While the decline is significant,

2020-21f 280 9,841 2,760 175 2,935 94% average export values remain

2020-21f % change -6.5% -9.3% -15.2% -7.9% -14.8% 3 per cent above the five-year average

of $9,500 per tonne. As discussed

* Lamb Meat value as a percentage of the value of Total Lamb exports, including Co-Products above, there are some strong

e estimate, f forecast | Source: Beef + Lamb New Zealand Economic Service, Statistics New Zealand

fundamentals supporting lamb

demand, despite the risk posed by

lifted (+5%). The average value of Of the items included in this category, For 2020-21, total lamb export COVID-19-related market disruption.

lamb exports to the EU lifted there is only good news coming from receipts (including co-products) are First quarter lamb exports will be

5 per cent. Exceptionally strong the tallow and meat-and-bone meal forecast at $2.94 billion FOB, down traded into an uncertain market;

returns in the first quarter of the (MBM). Hides and pelts have suffered 14.8 per cent on 2019-20, and 5 per however, we expect market sentiment

season supported the weaker market a loss in value due to changes in cent below the five-year average. to improve as 2020-21 progresses.

as COVID-19 spread. fashion and a shift in consumer Co-products are forecast to decline a

preferences. further 7.9 per cent. The outlook for Two windows of international demand

Export sales to the US have suffered pelt demand is weak as consumer that will provide insight into the

severely from COVID-19. Export 2020-21 spending remains low. direction export returns might take in

volumes dropped 23 per cent from The outlook is one of uncertainty for the outlook period are the peak buying

October 2019 to August 2020 and the lamb. Underlying fundamentals remain periods of Chinese New Year and

average FOB value of exports strong, driven by continued pork

declined 6 per cent. This market shortages in China, increasing

Figure 6 New Zealand Lamb Exports

remains New Zealand’s third largest, demand for high quality proteins and

accounting for 7 per cent of volumes; Oct to Aug, $m FOB

increasing disposable income in some

down from 8 per cent in 2018-19. Asian countries. EU 27

Exports to the Middle East lifted The economies of most of New UK

significantly (+20%) from October Zealand’s key markets are also

2019 to August 2020, driven by North America

expected to recover rapidly in the

market diversification in response to outlook period. Middle East

the impact of COVID-19.

The challenges for lamb exports North Asia

The value of co-products has been in outlined above, are, however,

decline in recent years, and COVID-19 Pacific

expected to persist in 2020-21.

placed further pressure on this “fifth Sheepmeat inventories in key markets Other

quarter” of the meat industry. The total will need to be shifted and foodservice

value of New Zealand’s exports of sector demand in key markets is still 0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

co-products is estimated to decline expected to be below pre-COVID-19 2018-19 2019-20

6 per cent in 2019-20. levels. Source: Beef + Lamb New Zealand Economic Service, New Zealand Customs,

New Zealand Meat Board

15chilled lamb exports to the UK and EU Table 8 New Zealand Mutton Exports

for Christmas. Typically, these

windows of demand drive high export Mutton meat Co-Products Total Mutton Mutton Meat

returns in the first quarter of the Sep Year 000 tonnes $ / tonne $m FOB $m FOB $m FOB %*

processing season. 2016-17 81 5,247 424 120 544 78%

Current market sentiment for both 2017-18 94 6,460 606 154 760 80%

China and the UK/EU is uncertainty 2018-19 84 6,715 564 100 664 85%

around solid price expectations for 2019-20e 83 7,482 625 92 717 87%

these periods. Despite chilled lamb 2020-21f 75 6,948 522 83 605 86%

sales at retail performing well so far

this year, the reduction in consumer 2020-21f % change -10.1% -7.1% -16.5% -9.5% -15.6%

disposable income may impact * Mutton Meat value as a percentage of the value of Total Mutton exports, including Co-Products

demand in the lead into Christmas. e estimate, f forecast | Source: Beef + Lamb New Zealand Economic Service, Statistics New Zealand

The volatility of the Chinese market

means demand could go either way as season on a record high of $7,482 per ASF and the shift towards high quality The average FOB value per tonne is

their peak demand window opens tonne, up 11 per cent on the previous protein are expected to maintain forecast to decline 7 per cent,

from September. Consumer season and 32 per cent up on the five- export returns at historically high however, will still trend 12 per cent

sentiment, however, will need to be year average. Export volumes are prices, however there will be downside above the five-year average.

significantly stimulated to see a lift in estimated to hold steady on 2018-19. risk in the forecast.

Total mutton export receipts (including Total mutton export receipts are

export prices. In 2020-21, mutton export production forecast to decline 15.6 per cent on

co-products) are estimated to lift

The outcome of Brexit will also be a 8 per cent for the season. is forecast to decline 10 per cent as 2019-20. The large drop in export

contributing factor to the export the farmers rebuild breeding ewe production combined with lower

outlook for lamb. This has been A weaker NZD/USD also supported flocks following drought-induced turn- average export values results in 2020-

discussed in detail earlier in the report. mutton returns, with most Chinese off in the autumn 2020. 21 mutton export receipts dropping 5

trade undertaken in US dollars. per cent below the five-year average.

Mutton The impact of COVID-19 has only Figure 7 New Zealand Mutton Exports

2019-20 recently taken its toll on mutton

Mutton was a strong export performer average export values, with values Oct to Aug, $m FOB

in 2019-20, despite COVID-19. The declining year-on-year from June to

August. This has been driven by EU 27

key drivers of the strong performance

were the large decline in Australian weaker sentiment in China as UK

mutton exports and the speed at uncertain economic conditions and

geopolitical tension weigh on demand North America

which the Chinese economy

recovered from COVID-19. for sheepmeat imports. Middle East

For the eleven months from October 2020-21 North Asia

2019 to August 2020, China The outlook for mutton in 2020-21 is Pacific

accounted for 70 per cent of total one of uncertainty. The same drivers

mutton exports. Demand trends in this outlined in the lamb section will Other

market are the sole driver of export underpin the season ahead for

performance. mutton. Economic and political 0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

sentiment in China will be key to 2018-19 2019-20

Average export values for mutton are

import demand patterns. Source: Beef + Lamb New Zealand Economic Service, New Zealand Customs,

estimated to finish the 2019-20

New Zealand Meat Board

16Lamb & Mutton – International Situation

Overview sheepmeat prices typically induced by Sheepmeat consumption in China is sheepmeat in the medium to long

tighter supplies. small, making up only 6 per cent of term.

The outlook period for global

total meat consumed in 2019.

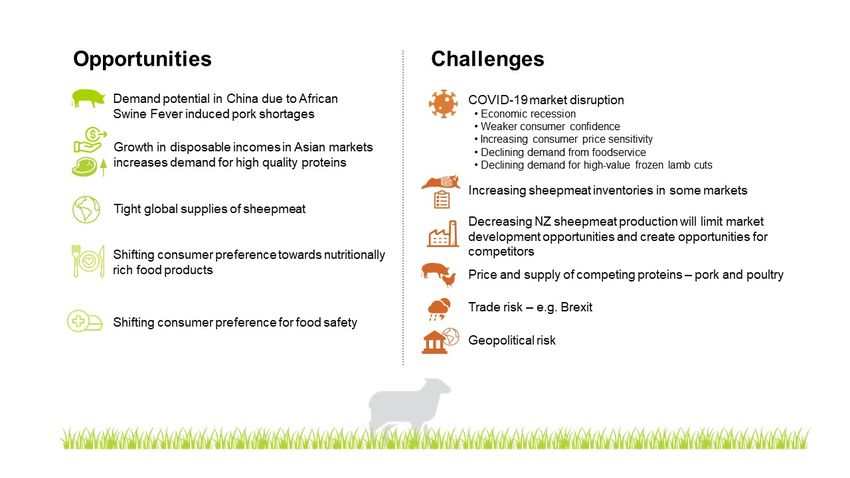

sheepmeat trade is one of uncertainty. Brexit uncertainties continue to plague However, the market has experienced ASF continues to drive demand for

Markets have been dramatically the UK and EU-27 markets, however, considerable growth from 2018 due to sheepmeat in the outlook period. As

altered by COVID-19. The disruption have been overshadowed by COVID- ASF and increasing consumer discussed earlier in this report, while

to the foodservice sector has resulted 19. An outcome will become clear significant investment into recovery for

incomes. There is growing demand

in a sharp decline for high-value early in 2021 and current signals from the affluent Chinese consumer the Chinese pork industry is occurring,

frozen lamb cuts. Consumer demand suggest that there is the potential for for high quality, nutritionally rich pork production is not expected to lift

has weakened, and price sensitivity significant disruption for New Zealand protein, and imported sheepmeat is to pre-ASF levels for at least 24

has lifted, driven by deteriorating sheepmeat exporters. months. Given the risks outlined

expected to fill this demand going

economic conditions. The drop in forward. Consumption is expected to earlier, it is unlikely that demand will

consumption has resulted in an Geopolitical tension between the US lift to the ASF-driven highs seen in late

and China is escalating and will be a lift 3 per cent in 2020 and growth rates

increase in protein inventories in some of 1-2 per cent are forecast out to 2019, however prices are expected to

key markets. Trade uncertainties and risk to be monitored during 2020-21. remain at historically high levels.

2025. While there is a risk demand for

geopolitical tension also contribute to China sheepmeat may decline as China

the volatile outlook. The outbreak of COVID-19 in China

China is one of the only major global recovers from ASF, it is thought that resulted in a sharp drop in sheepmeat

Underlying the uncertainty, however, economies forecast to experience there may be a permanent shift by the consumption in the months from April

there remains solid fundamentals to annual growth in 2020. While it is more affluent consumer towards to August 2020. An estimated

support sheepmeat demand. leading the way globally with COVID- higher quality proteins. 60 per cent of Chinese sheepmeat

ASF-induced pork shortages and tight 19 recovery, the market continues to Sheepmeat production in China is consumption occurs in the foodservice

global supplies will be leading demand face challenges in the 2020-21 expected to lift in 2020 and into the sector, and the majority of New

drivers. In addition, there continues to outlook period. Zealand product is destined for this

medium term. The most recent

be growth in middle class incomes sector. While there has been strong

Weaker economic conditions prevail estimates of growth from FAO signal a

across Asia, and a shift in affluent 2 per cent growth in production as growth in on-line and retail sales in the

consumer demand toward high quality post COVID-19. Following years of months following the Chinese COVID-

economic growth, the sharp change record high sheepmeat prices in late

protein sources. 2019 provided incentive for Chinese 19 outbreak, volumes are still minor

has created uncertainty for compared to foodservice sector sales.

World sheepmeat production is consumers. Demand has weakened sheepmeat producers to increase

expected to lift by 1 per cent in 2020, and price sensitivity has lifted. The flocks. Chinese import data for the first six

with most of the growth coming from decline in foodservice demand is also The estimated gains in domestic months of 2020 shows evidence of the

China. World trade of sheepmeat, of concern for sheepmeat demand. In Chinese production remain insufficient challenges COVID-19 has inflicted on

however, is expected to contract in the addition, the escalating tension sheepmeat demand. For the first six

to meet consumption requirements.

2020-21 season, with both Australia between China and the US is a This market will continue to be reliant months, Chinese sheepmeat imports

and New Zealand recovering from growing concern for the Chinese on imports, although the gap between from all countries are down 4 per cent

drought. consumer. the two is shrinking. While there is on 2019 levels. This is in contrast to a

much volatility in Chinese domestic 43 per cent lift in beef imports from all

While tighter sheepmeat supplies will Despite this risk, the underlying

production trends, there is potential for countries.

provide support for demand, factors fundamentals for sheepmeat demand

such as consumer price sensitivity and remain solid, driven by ASF induced increasing domestic production to The COVID-19 outbreak in China

increasing competition from pork and pork shortages and continued growth dampen demand for imported came on the back of a record month of

poultry, will constrain the lift in global in consumer disposable incomes. sheepmeat imports in December

17You can also read