October 2018 - BMO 2018 Global Energy Leadership Forum NYSE American: SRCI - SRC Energy Inc

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

October 2018 – BMO 2018 Global Energy Leadership Forum

NYSE American: SRCI

Forward-looking Statements and Other Disclaimers

This presentation contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange

Act of 1934. All statements, other than statements of historical fact, included in this presentation that address activities, events or developments that SRC Energy

Inc. (the “Company”) expects, believes or anticipates will or may occur in the future are forward-looking statements.

Forward-looking statements contained in this presentation include statements, estimates and projections regarding the availability of midstream services and

infrastructure and the Company's future financial position, operations, performance, costs, business strategy, oil and natural gas reserves, drilling program, capital

expenditure budget and sources of financing for the budget, liquidity and capital resources, the timing and success of projects, derivative activities and matters

relating to Initiatives 97 and 74. The words “estimate,” “project,” “predict,” “believe,” “expect,” “anticipate,” “potential,” “could,” “may,” “foresee,” “plan,” “goal”

or other similar expressions that convey the uncertainty of future events or outcomes are intended to identify forward-looking statements. However, the absence

of these words does not mean that the statements are not forward-looking. These statements are based on certain assumptions made by the Company based on

management's experience, expectations and perception of historical trends, current conditions, anticipated future developments and other factors believed to be

appropriate. Forward-looking statements are not guarantees of performance. Although the Company believes the expectations reflected in its forward-looking

statements are reasonable and are based on reasonable assumptions, no assurance can be given that these assumptions are accurate or that any of these

expectations will be achieved (in full or at all) or will prove to have been correct. Moreover, such statements are subject to a number of assumptions, risks and

uncertainties, many of which are beyond the control of the Company, which may cause actual results to differ materially from those implied or expressed by the

forward-looking statements. These include the risk factors discussed or referenced in the Company's most recent Form 10-K; risks relating to declines in the prices

the Company receives, or sustained depressed prices the company receives, for its oil and natural gas; uncertainties about the estimated quantities of oil and

natural gas reserves; drilling and operating risks; the adequacy of the Company’s capital resources and liquidity including, but not limited to, access to additional

borrowing capacity under the Company’s credit facility; the effects of government regulation, permitting and other legal requirements, including new legislation or

regulation of hydraulic fracturing and the export of oil and natural gas; the impact of potential changes in the Company’s credit ratings; environmental hazards,

such as uncontrollable flows of oil, natural gas, brine, well fluids, toxic gas or other pollution into the environment, including groundwater contamination; difficult

and adverse conditions in the domestic and global capital and credit markets; risks related to the concentration of the Company’s operations in the DJ Basin of

northeast Colorado; disruptions to, capacity constraints in or other limitations on the pipeline systems that deliver the Company’s oil, natural gas liquids and natural

gas and other processing and transportation considerations; the costs and availability of equipment, resources, services and personnel required to perform the

Company’s drilling and operating activities; potential financial losses or earnings reductions from the Company’s commodity price risk-management program; risks

and liabilities related to the integration of acquired properties or businesses; uncertainties about the Company’s ability to replace reserves and economically

develop its current reserves; general economic and business conditions, either internationally or domestically; competition in the oil and natural gas industry;

uncertainty concerning the Company’s assumed or possible future results of operations; and other important factors that could cause actual results to differ

materially from those projected. Estimates of the net present value of a property do not necessarily correspond to the current or future fair market value of the

property in part due to the foregoing risks and uncertainties.

Accordingly, you should not place undue reliance on any of the Company’s forward-looking statements. Any forward-looking statement speaks only as of the date

on which such statement is made, and the Company undertakes no obligation to correct or update any forward-looking statement, whether as a result of new

information, future events or otherwise, except as required by applicable law.

2

SRC Energy – Enhancing Quality of Life

▪ Pure Play DJ Basin Operator with Contiguous Acreage Position

▪ 2018 operations funded by cash flow and existing liquidity

▪ Multi-year inventory of high return development

▪ Expanding infrastructure

▪ Strong balance sheet with over $475 million of liquidity

providing capital flexibility

▪ Active pursuit of environmental and social excellence

▪ Engaged with local communities in which we live and operate

3

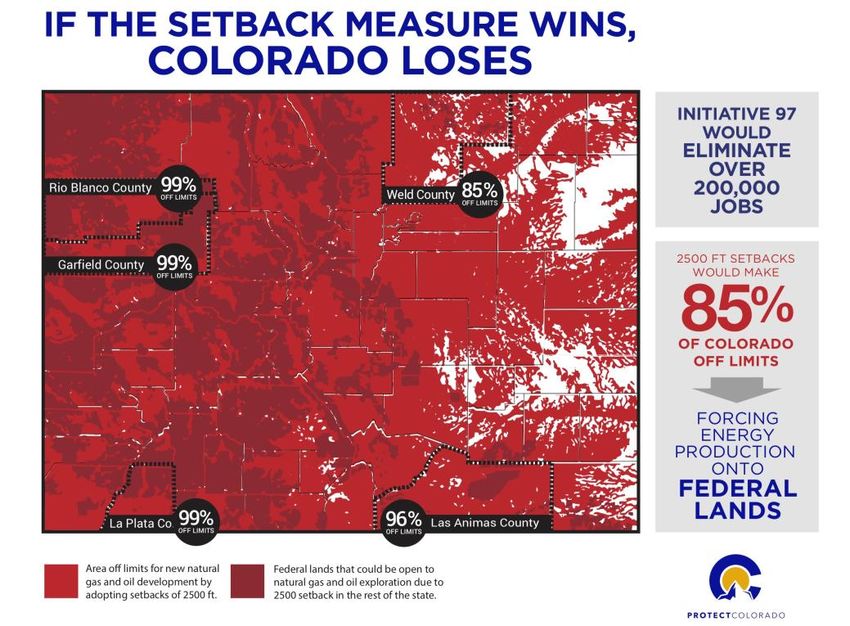

Activists’ Attempt to Ban Oil & Gas Putting Private

Property Values at Stake

Walker Stapleton (2018 Republican candidate for Governor of Colorado) “ I oppose the

Proposition #112 [Initiative #97] – 2,500’ Setback energy ban disguised as initiative 97“

requirement for oil and gas development Jared Polis (2018 Democratic candidate for Governor of Colorado) “In spite of the

challenges we face, Colorado’s economy remains today the envy of the nation. And if we

• Effectively bans oil and gas development in want to keep it that way, we can’t ignore the role that the oil and gas industry has played in

our growth, or the significant wages and tax revenue it creates in our state”. He also said,

Colorado “Let me be very clear where I stand on this: As I said during the Democratic primary, I

oppose initiative 97.”

• Both candidates for the Colorado State Ken Salazar (Former Secretary of the Interior under the Obama Administration and former

Colorado Attorney General) Called the initiative “fundamentally unconstitutional” because it

Governor’s office have publicly apposed the would effectively seize mineral rights from private property owners.

initiative

• Intensive and well funded public education

program has begun and will ensure that

Colorado voters understand the amendment’s

devastating impact on energy development in

Colorado and on Colorado’s economy

Amendment #74 [Initiative #108]– Just compensation for

reduction in fair market value by government law or

regulation

• The Colorado Farm Bureau is the sponsor of this

constitutional amendment

4

Health, Safety and the Environment – SRC’s highest priority

▪ Engaged at multiple levels

▪ Front Range Emergency Response Committee

▪ COGA – Operational Safety, Urban Operations, HSE Committees

▪ Rocky Mountain HSE Peer Group

▪ DJ Basin Safety Council and Operators Consortium

▪ Active vertical well remediation and reclamation program

▪ ~160 wells in 2017 with ~500 acres reclaimed

▪ Similar program underway in 2018

▪ Focus on safety

▪ Incident Reporting & Tracking System

▪ Community & First Responder Engagement

▪ Stop Work Authority – any worker, any time

▪ Reduce emissions

▪ Tier-4 (low emission) engines utilized in completion fleets

▪ Significant use of vapor recovery equipment in facilities

▪ Direct pipeline take-away reduces truck traffic and vehicle emissions

5

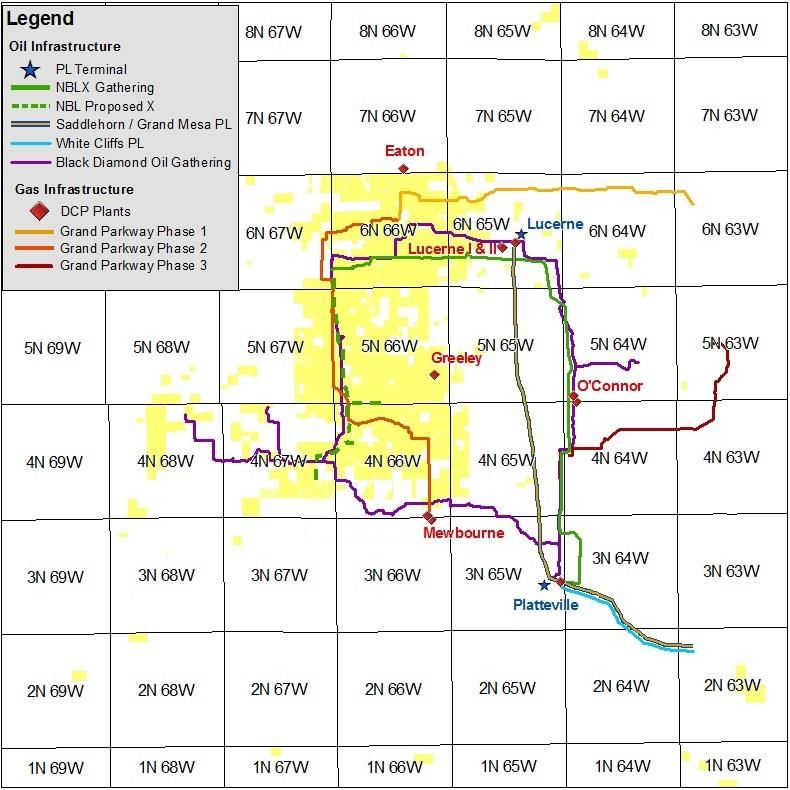

Midstream – Delivering Affordable Energy to Local

Residents and Beyond

DCP Midstream

5

▪ Mewbourn 3 processing plant with 200 MMcf/d currently

filling capacity

▪ O’Connor 2 with 200 MMcf/d of processing capacity plus 100

MMcf/d of bypass capacity is under construction and

expected to be in service Q2 of 2019

▪ Bighorn permitted for 1 Bcf/d of capacity to begin taking gas in

2020

▪ Gas and NGL pipeline expansions out of the DJ Basin aligned

with processing

1

Noble Midstream

▪ Gathering oil and water in current development area

3 2

▪ Oil trunk line being extended south through footprint,

providing access to multiple sales points

# Plant Name Operator In-Service Capacity MMcf/d

4

1 O’Connor 2 (Plant 11) DCP Q2 2019 200 +100 of bypass

22 Bighorn (Plant 12) DCP 2020 & beyond 1Bcf/d

3 Latham I/II Western Gas Partners Q1/Q3 2019 200/200

4 Ft. Lupton Discovery Midstream * Late 2018/2019 200/450

55 Pierce Rimrock 2019 200

* Discovery Midstream was recently acquired by a joint venture between KKR and Williams

6

Maximizing NPV Per Section

Niobrara/Codell

$50,000 12,000

▪ Optimizing NPV per section requires

balancing well density per section against $45,000 10,000

Value(NPV-10)/Recovery (MBOE)

EUR per well

$40,000 8,000

▪ Maximizing corporate returns focuses on

the development of the overall leasehold $35,000 6,000

position versus simplified well-level

economics $30,000 4,000

▪ SRC’s contiguous leasehold position

$25,000 2,000

enhances efficiency

$20,000 -

2 10 5 8 1125 14 17 20

40

Wells Per Section

7

Corporate Execution

Net Daily Production (MBOE/D) (1)

▪ Growth of acreage footprint and drilling locations 52

with longer laterals is supportive of efficient 47

production and reserves growth 48

34

▪ Effective management of capital and cost structure

12

leading to balancing of cash flows

2016 2017 H1 2018 2018 Est.

D&C Capex vs EBITDA ($MM) Locations / Wattenberg Acreage (2) Proved Reserves (MMBOE) (1)

2,000 100,000

~90,000 227

CAPEX $480 - $540 Acreage PUD

~1,700 PDP

EBITDA $461 1,600 Locations 80,000

~69,300

38%

$447

H1 EBITDA 1,200 60,000

Annualized ~1000

~41,000

$283 800 40,000 93

$223 ~600 19%

$131 62%

H1 EBITDA 400 20,000

81%

$65

0 0

2016 2017 2018 EST. 2016 (3) 2017 2018 12/31/2016 12/31/2017

(1) 2016 production data converted to 3-stream using 3.5 GPM wet gas yield and 25% gas volume shrink

(2) Acreage and location counts based on values at the beginning of the period

(3) Well counts in 2016 are normalized to ML equivalents

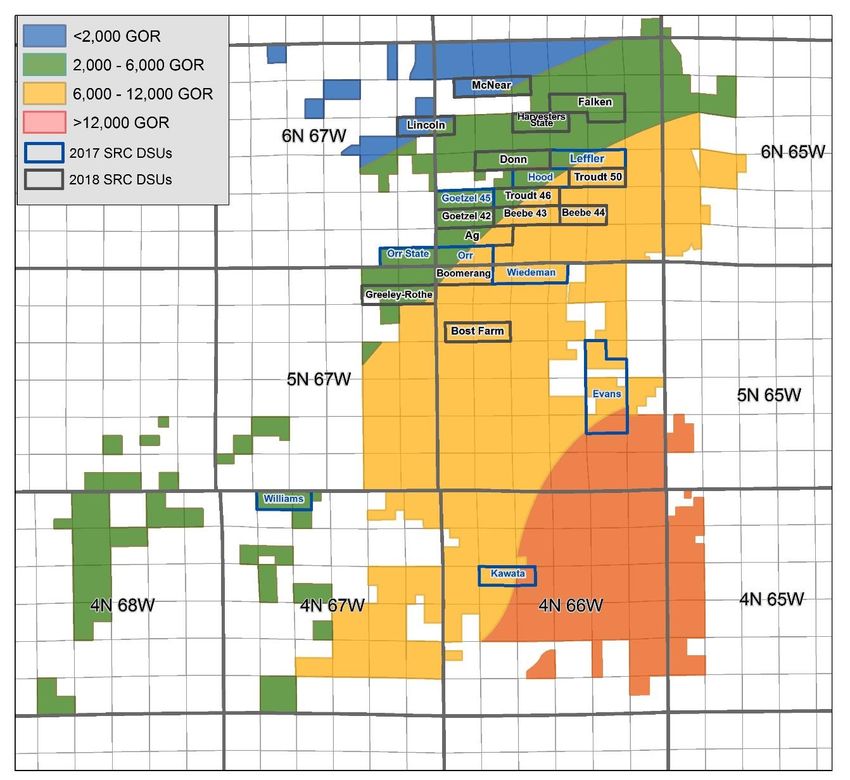

82018 Exploitation Program

2018 Guidance

Total production of 48-52 Mboe/d

D&C Capex of $480-$540 MM

2018 operations funded by operating cash flow

and existing liquidity

Protect capital program by hedging 30%-50% of

estimated production

Drill ~117 gross (100 net) wells and complete 116

gross (103 net) wells in 2018

D&C costs of ~$4.2 MM for 8,000’ ML wells and

~$5 MM for 10,000’ LL wells

Attractive returns across the GOR spectrum

2,000Current D&C Operations

Troudt Pad I: 12 (~12 Net) 12 LL

wells

Waiting on Troudt Pad II: 12 (~12 Net) 12 Completion Harvesters State Pad: 12 (~11

McNear Pad: 12 (~11 Net) LL

Drilling ML wells Net) ML wells

wells Stimulation in Progress

24 wells Lincoln Pad: 12 (~8 Net) LL wells

Greeley Rothe Federal: 12 (~8 Boomerang Pad: 16 (~13 Net)

24 wells Net) LL wells 53 wells

12 ML wells & 4 LL wells

Donn Pad: 13 (~13 Net) LL wells

On production earlier in 2018: 12 LL Leffler, 12 LL Ag, 12 ML Goetzel, 18 SL & LL Falken

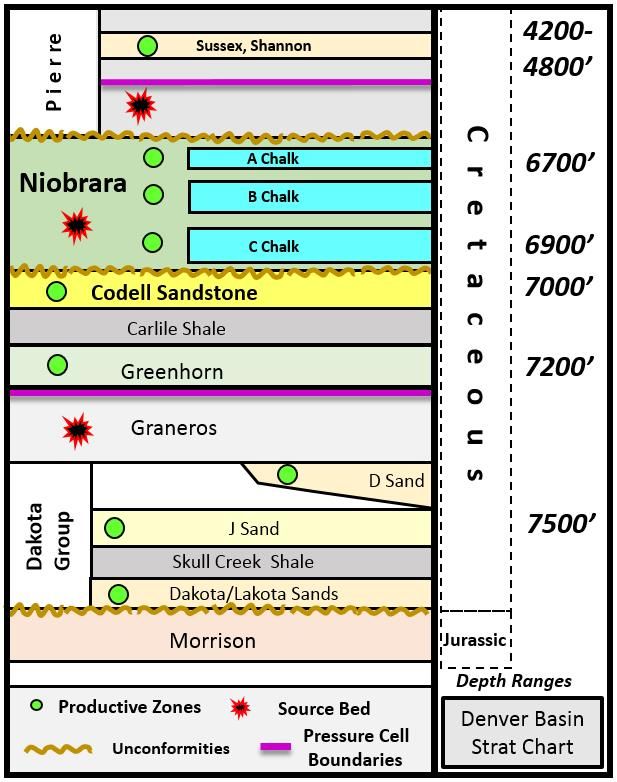

Standard Completion Niobrara Niobrara Comments 4200-

Design A & Codell B&C 4800’

Average stage length 200’ 200’ 36 stages in ML, 50 stages in LLs and 60 stages in XLs

6750’

Perf clusters/stage 4 4 Actively managing entry points to improve proppant

distribution and stimulated reservoir volume

Average Proppant load 800#/ft 1,300#/ft Engineered completions will pinpoint proppant 7050’

placement to optimize productivity

Surfactant yes yes Surfactant designed for higher GOR reservoirs 7200’

Frac Fluid Slickwater Hybrid Experimenting with fluid designs in some zones

Other completion details:

7500’

▪ Utilize monobore, plug & perf designs with the added implementation of dissolvable plugs

▪ Utilizing a completion fleet with integrated noise reduction technology in an effort to further reduce environmental

impact in urban areas

10Appendix

11Operational and Financial Performance

Commodity Mix Cash Cost ($ / Boe)

Gas NGLs Oil Cash G&A Production Taxes LOE

36% 35% 33% 31% 31% 34%

$7.59

$6.71 $6.54 $6.56 $6.89

20% 18% 19% $1.44

21% 22% 23% $5.58

$1.66 $1.39 $1.67

$3.46 $1.47 $3.47

$3.19 $3.63 $3.29

47% 51% 50% $0.92 $2.71

43% 43% 43%

$2.33 $1.93 $2.68

$1.69 $1.40 $1.54

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18

Cash Margin ($/Boe) Net Leverage (Net Debt / LTM EBITDAX)

1.8x

$29.15

$26.79 $26.33

$22.31 1.3x

$20.70 1.2x

$18.74 1.1x

1.0x

0.5x

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18

12Reserves Report Summary

Ryder Scott Reserves – YE 2017 (1)

Proved Reserves by Category Proved Reserves by Commodity Pre-tax PV-10 by Category (2)

NGL 28% OIL 31%

PDP 33%

227 227 PUD 43%

$1.8 B PDP 49%

MMBoe MMBoe

PUD 62%

PDNP 5%

GAS 41% PDNP 8%

▪ Reserves based on a 3-year development plan

▪ Represents development of approximately 15% of identified locations

(1) Reserves per SEC price deck reserve report representing pricing of $51.34 WTI / $2.98 HH

(2) Reserves split based on NYMEX pricing at 1/2/2018

13Delivering Long-Term Shareholder Value

Full-Cycle NPV & IRR Per Well Economics

NPV ($MM)

Acreage Cost ~600 MBOE ~800 MBOE ~1 MMBOE

$20k/acre $2.5 $3.5 $4.7

$15k/acre $2.7 $3.9 $4.9

IRR

Acreage Cost ~600 MBOE ~800 MBOE ~1 MMBOE

$20k/acre 45% 53% 57%

$15k/acre 50% 59% 64%

▪ Full cycle Wattenberg well economics are

competitive with other major basins

Note: Price Deck: Oil = $60 Flat, NGL = 30% of WTI, Natural Gas = $3.00 Flat

Assumed differentials: oil = $6.50 / NGL = 17% / gas = $0.45

• Full cycle NPV and IRR information assumes $4.2 MM ML lateral well costs and $5 MM LL lateral well cost.

• Rate of return and NPV estimates do not reflect corporate, general and administrative expenses.

• Estimated EURs may not correspond to estimates of reserves as defined under SEC rules.

• Production volumes reflect 3-stream equivalent

14Hedging Summary as of October 2018

2018 2019

4th QTR Total 1st QTR 2nd QTR 3rd QTR 4th QTR Total

Oil Costless Collars

Volume (Bbl) 920,000 920,000 540,000 546,000 552,000 552,000 2,190,000

Ceiling Price per Bbl $ 61.29 $ 61.29 $ 74.31 $ 74.31 $ 74.31 $ 74.31 $ 74.31

Floor price per Bbl $ 43.63 $ 43.63 $ 55.00 $ 55.00 $ 55.00 $ 55.00 $ 55.00

Gas CIG Costless Collars

Volume (MMBtu) 1,380,000 1,380,000

Ceiling Price per MMBtu $ 2.82 $ 2.82

Floor price per MMBtu $ 2.25 $ 2.25

Gas CIG Price Swaps

Volume (MMBtu) 1,800,000 1,820,000 1,840,000 1,840,000 7,300,000

Price per MMBtu $ (0.76) $ (0.76) $ (0.76) $ (0.76) $ (0.76)

Propane Price Swaps

Volume (Gallons) 3,864,000 3,864,000 7,560,000 7,644,000 7,728,000 7,728,000 30,660,000

Price per Gallon $ 0.80 $ 0.80 $ 0.89 $ 0.89 $ 0.89 $ 0.89 $ 0.89

* Oil price is based on NYMEX WTI, gas price is based on NYMEX Henry Hub or CIG, and propane is based on Mont Belvieu

Disclosure on Derivative Instruments

The Company has entered, or may enter in the future, into commodity derivative instruments utilizing, price swaps, collars, put or call options to reduce the effect of

price changes on a portion of future oil and gas production. The Company’s commodity derivative instruments are measured at fair value and are included in the

condensed balance sheet as derivative assets and liabilities.

All derivative positions are carried at their fair value on the condensed balance sheet and are marked-to-market at the end of each period. Both the unrealized and

realized gains and losses resulting from the contract settlement of derivatives are recorded in the gain on derivatives line on the condensed statement of operations.

The Company has a master netting agreement on each of the individual oil and gas contracts and therefore the current asset and liability are netted on the

condensed balance sheet and the non-current asset and liability are netted on the condensed balance sheet.

15Adjusted EBITDA Reconciliation

SRC ENERGY INC.

RECONCILIATION OF NON-GAAP FINANCIAL MEASURES

(unaudited, in thousands)

Three months ended Six months ended

6/30/2018 6/30/2017 6/30/2018 6/30/2017

Adjusted EBITDA

Net Income (loss) $ 49,624 $ 27,936 $ 115,420 $ 47,816

Add back:

Depreciation, depletionand amortization 41,877 26,427 78,958 39,656

Full cost ceiling impairment 0 0 0 0

Income tax expense (benefit) 3,347 0 9,158 0

Stock based compensation 3,146 2,685 5,942 5,360

Mark to market of commodity derivatives contracts:

Total (gain) loss on commodity derivatives contracts 14,294 (1,328) 20,075 (4,707)

Cash settlements on commodity derivatives contracts (4,566) 153 (6,121) 234

Cash premiums paid for commodity derivatives contracts 0 0 0 0

Interest, net (5) (20) (14) (31)

Adjusted EBITDA $ 107,717 $ 55,853 $ 223,418 $ 88,328

16PV-10 Reconciliation

SRC ENERGY INC.

RECONCILIATION OF NON-GAAP FINANCIAL MEASURES

(unaudited, in thousands)

12/31/2017 12/31/2016 12/31/2015

Standardized measure of discounted future net cash flows:

Add: 10 percent annual discount, net of income taxes $ 1,600,675 $ 434,261 $ 390,953

Add: future undiscounted income taxes 1,267,258 427,587 408,939

Future pre-tax net cash flows 285,349 90,195 108,172

Less: 10 percent annual discount, pre-tax 3,153,282 952,043 908,064

(1,396,998) (475,695) (469,921)

PV-10 $ 1,756,284 $ 476,348 $ 438,143

17You can also read