PETROPAVLOVSK PLC Investor Presentation April 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

PETROPAVLOVSK PLC Investor Presentation April 2019

Cautionary and Forward-looking Statements

— Some statements contained in this presentation or in documents referred to in it are or may be forward-looking statements, including

references to guidance. Such statements reflect the Company’s current views with respect to future events and are subject to risks,

assumptions, uncertainties and other factors beyond the Company’s control that could cause actual results to differ from those

expressed in such statements. Although the Company believes that such forward-looking statements, which speak only as of the date

of this presentation, are reasonable, no assurance can be given that they will prove to be correct. Therefore, you should not place

undue reliance on these statements

— There can be no assurance that the results and events contemplated by the forward-looking statements contained in this presentation

will, in fact, occur. The Company will not undertake any obligation to release publicly any revisions to these forward-looking

statements to reflect events, circumstances or unanticipated events occurring after the date of this presentation, except as required by

law or by any appropriate regulatory authority. Nothing in this presentation or in documents referred to in it should be considered as a

profit forecast.

— The past performance of the Company and its securities is not, and should not be relied on as, a guide to the future performance of

the Company and its securities

— This presentation does not constitute, or form part of or contain any invitation, recommendation or offer to any person to underwrite,

subscribe for, buy, sell, otherwise acquire, exchange or dispose of any shares or securities in the Company or advise persons to do

so in any jurisdiction, including, but not limited to, the Russian Federation, nor shall it, or any part of it, form the basis of or be relied on

in any connection with or act as an inducement to enter into any contract or commitment therefore or engage in any other investment

activity. In particular, this presentation and the information contained herein are not an offer of securities for sale in the United States.

This presentation does not constitute an advertisement of any securities in the Russian Federation

— No reliance may be placed for any purpose whatsoever on the information or opinions contained in this presentation or on its

completeness and no liability whatsoever is accepted for any loss howsoever arising from any use of this presentation or its contents

or otherwise in connection therewith.

— The development and production plans and estimates set out herein represent the current views of the Company's management. The

Company’s Board reviews the production estimates on an ongoing basis. All planning is subject, inter alia, to available funding and

capital allocation decisions

— English law and English courts will have exclusive jurisdiction over any disputes arising from or connected with this presentation

2

Introduction 3

qwas

Top 5 Russian Gold Miner With One Of Only Two Pressure Oxidation Plants

Vertically integrated gold mining business, operating throughout the entire mining cycle

3 x gold mines, mix of open pit + underground, c.7.1Moz of gold produced to

date(1)

8.21Moz of JORC Reserves, 20.52Moz of JORC Resources(2)

c.14Mtpa of RIP processing capacity

FY2019F gold production c.450-500Koz, with growing contribution from refractory

ore treatment

Pressure Oxidation (POX) Hub successfully commissioned in Q4 2018

Experienced management team + skilled workforce

Significant untapped exploration potential, with combined licence area

c.2,600km2

31% equity interest in low cost Hong Kong listed iron ore producer IRC Ltd.

(US$153m market cap)(3)

(1) As at 31 Dec 2018, incl. historical production from our alluvial operations and JVs (2) As at 31 Dec 2018, in accordance with the JORC Code.

Resources (M,I&I) are incl. of Reserves (3) IRC market capitalisation as at close 26 April 2019 (US$153m, source: Bloomberg) x Petropavlovsk’s 4

equity interest (31.1%) = US$48m

Company Snapshot (1/2)

Proven track record of execution from exploration and development to mining and processing

Brief Overview FY 2018 Russian Gold Mine Production

— Petropavlovsk is one of Russia’s major gold mining companies with assets located in the

Amur region, the Russian Far East

Polymetal, 14%

— Founded in 1994, accounted for c.6% of Russia’s total gold production in 2018 Polyus, 35%

— Total JORC Resources 20.5Moz(1) including 8.2Moz of Reserves Kinross Gold, 7%

— Petropavlovsk has 4 production sites, including the technically advanced Pressure Oxidation

(POX) Hub, launched Q4 2018 Uzhuralzoloto, 7%

— In 2018, produced 422Koz of gold, generating US$500m of revenue and US$143m of EBITDA

— The company holds 31% share in IRC Ltd, a Hong Kong listed premium grade iron ore Other, 32% Petropavlovsk, 6%

producer

— After listing on AIM in 2002, Petropavlovsk moved to the Main Market of the LSE in 2009

Mining + Production Facilities JORC Resources(1)

— One of the largest gold mines in Russia in terms of mineral resources(2)

— Acquired as a greenfield in 2003. Licence area of c.75km2

Malomir — RIP plant throughput: 3.0Mtpa, commissioned 2010 Ca tegor y 1

97% 3% 6.9Moz

— Flotation plant with current stage I capacity of 3.6Mtpa launched H2 2018

— Stage 2 will increase capacity to 5.4Mtpa via addition of third 1.8Mtpa line

— One of Russia’s largest gold mines in terms of processing capacity

— Acquired as a greenfield in 2001. Licence area of c.1,300km2

Pioneer — Expected >15 year life of mine

Ca tegor y 1

76% 24% 5.9Moz

— RIP plant throughput: 6.7Mtpa, commissioned 2007

— The Group’s newest mine with an expected >15 year mine life

Albyn — Acquired 2005 as a greenfield. Licence area of 1,053km2 Ca tegor y 1

21% 79% 5.4Moz

— RIP plant throughput: 4.7Mtpa, commissioned 2011

— The Group’s oldest mine, now closed, and which has been converted to host the Pressure

Pokrovskiy Refractory Resources

Oxidation (POX) Hub and supporting infrastructure Ca tegor y 1

100% 0.9Moz

— Historically has produced c.2.0Moz of gold Non-Refractory Resources

(1)Total JORC Resources as at 31 Dec 2018, in accordance with JORC Code. Resources (M,I&I) are inclusive of Reserves. For full details and asset

by asset breakdown please refer to the 2018 Petropavlovsk annual report 5

(2) Based on management estimatesCompany Snapshot (2/2)

Gold mining business supported by a range of complementary in-house service companies

Operating mine Analytical labs

Underground mine R&D

POX Offices Mining assets

London Pioneer

Petropavlovsk Plc

Corporate headquarters St Petersburg Albyn

RDC

Hydrometallurgy Malomir

Pokrovskiy

Moscow

Petropavlovsk Moscow

PHM Engineering

Blagoveschensk (Amur region)

Regis Exploration

Kapstroi Construction

Irkutsk

Irgiredmet Institute

IRC Ltd. (associate company)

6Investment Highlights

1

One of the major gold mining companies in Russia

2

Experienced management team + skilled workforce, in-house technical expertise

and R&D facilities

3

Efficient mining + processing operations

4

Potential to grow production via refractory ore processing at the

Pressure Oxidation (POX) Hub

5

Strong track record of mine development, expansion + asset optimisation

6

Strategic location + access to developed infrastructure

7

Exploitable + long life mineral resource base with high expansion potential

7FY 2018 Highlights

2018 Highlights

Restoring leadership and progressing growth ambitions

Commissioning of the POX Hub + Malomir flotation plant Improved operating performance

— Unlocks value embedded in c.5.3Moz of refractory reserves — H2 2018 operational turnaround enabled FY 2018 targets to be

met: production in line with guidance, costs reduced

— Significantly increases optionality of the Group to process own

refractory ores or treat 3rd party material — IRC: ongoing ramp-up of K&S

— Production growth to resume in 2019, from higher grades +

material contribution from POX

Balance sheet de-risking Board and management teams strengthened

— New US$240m facility signed between Gazprombank and IRC, — Leadership restored: return of Dr Pavel Maslovskiy as CEO

payment schedule aligned with K&S ramp-up

— Additions of Sir Roderic Lyne (Non-Executive Chairman),

— New gold sales agreement for c.175Koz signed Robert Jenkins, James Cameron Jr , Damien Hackett, Harry

Kenyon-Slaney (Independent Non-Executive Directors) + Bektas

— Ongoing de-leveraging / reduction in net debt Mukazhanov (Non-Executive Director)

— Board fully compliant with UK Corporate Governance Code

9Key Achievements in 2018

Following a disappointing H1 2018, recovery is underway with strong H2 2018 under new

leadership

— Production of 422Koz Au (incl. 52Koz of gold in high-grade refractory concentrate), in line

Production + Costs with guidance

— H2 2018 TCC of US$650/oz, down 28% vs. H1 2018 (US$899/oz)

— Malomir: following flotation plant commissioning in July, c.46Kt of high-grade refractory

concentrate produced (c.36g/t), for POX processing

— Material improvement in flotation flowsheet à c.50% increase in concentrate grade

Malomir Flotation + vs. initial design and 50% – 60% decrease in concentrate yield

POX Hub

— POX Hub: autoclaves 1 + 2 commissioned Q4 2018, ahead of schedule

— Smooth ramp-up, first gold poured Dec 2018

— 3rd party refractory concentrate being acquired

— Resources of 20.5Moz Au with Reserves of 8.2Moz Au

Exploration — Reserves increased by 0.6Moz despite depletion to 8.2Moz due to new discoveries at

Pioneer + Malomir

— Net Debt reduced by US$17m to US$568m

Other

— IRC: increased production volumes + higher EBITDA

10FY 2018 Financials

FY 2018 Financial Results

Performance impacted by scheduled inventory build and sub-optimal H1 2018

Units 2018 2017 Change

Gold production Koz 422.3 (1) 439.6 (4%)

Gold sold Koz 369.6 439.8 (16%)

Avg. realised gold price US$/oz 1,263 1,262 0%

Group revenue US$m 499.8 587.4 (15%)

Total cash costs (TCC) US$/oz 786 741 +6%

All-in sustaining costs (AISC) US$/oz 1,117 963 +16%

Underlying EBITDA US$m 143.0 196.8 (27%)

Operating profit US$m 126.6 100.4 +26%

Profit before tax US$m 82.4 48.9 +69%

Profit for the period US$m 25.9 37.1 (30%)

Net cash from operating activities US$m 217.2 124.0 +75%

Net debt (as at 31 Dec) US$m (568.0) (585.1) (3%)

Development capex US$m 112.8 66.2 +70%

Exploration capex US$m 21.6 21.9 (1%)

Note: (1) Incl. c.52Koz of gold contained in high-grade refractory concentrate produced by the Malomir flotation plant

12FY 2018 Total Cash Costs (TCC)

TCC within guided range of US$750/oz – US$800/oz, despite difficult H1 2018

US$/oz 48 0.2

3 91

123 39

741 +6% 786

TCC FY2017

TCC FY2018

Deferred stripping

Co-product effect

Changes in grades

Other taxes

Higher costs

FX

/ recoveries

— TCC affected by inflation of some RUB denominated costs, higher volumes of stripping + suboptimal organisation of

mining works in H1 2018, partially mitigated by higher processed grades (Pioneer, Malomir), higher recoveries (Pioneer,

Albyn, Malomir) + effect of RUB depreciation

13Precious metals operating cash expenses 2018 vs. 2017

Cash expenses -3% yoy as inflation of certain RUB denominated costs (electricity, diesel) was

somewhat offset by the effect of RUB depreciation

Precious Metals Operating Cash Expenses Structure

FY2017 FY2018

Consumables Consumables

+ +

Other Labour Labour

Other

Materials 23% 22%

Materials

34% 31%

Fuel

Fuel 15%

Total 14% Total

US$313.4m(1) US$302.7m(2)

Consumables + Other Other

Other 7% 8%

Materials

37% Electricity Electricity

10% 9%

External Services External Services

12% 15%

2018 2017 Change

Avg. RUB/US$ FX 62.7 58.3 +7%

Avg. Gold PM Fix US$/oz 1,269 1,257 +1%

Note: (1) Before movement in ore stockpiles, GIC and bullion in process of US$19.2m;

(2) Before movement in ore stockpiles, GIC, flotation concentrate and bullion in process of US$55.6m

14FY 2018 Development and Exploration Spend

FY 2018 exploration + development capex totalled US$134.4m

FY2018 Development US$112.8m FY2018 Exploration US$21.6m

Active development continued ahead

of scheduled Q4 commissioning

61.5

Flotation,

tailings, underground

development

Tailings, underground

development, machinery / Pioneer US$10.0m

equipment Malomir US$5.5m

Albyn US$5.0m

Other US$1.1m

Tailings, access road

21.6

19.3 19.1

10.5

2.4

POX Malomir Pioneer Albyn PPE Upgrade Exploration

15US$m

As at 1 Jan 2018

585.1

Capital expenditure

Bridge loans to IRC 134.4

57.0

Interest accrued on borrowings

2018 Change in Net Debt

55.5

Transaction costs in connection

9.0

with bank loans and notes

Interest paid on prepayment on

-3%

6.8

gold sale agreements

Income tax paid

5.0

1.9

Other

Increase in w/c

160.3

Net cash generated by

operating activities before w/c

122.6

changes

As at 31 Dec 2018

568.0

Net Debt down c.3% to US$568m due to an increase in cash + cash equivalents of c.US$15m

16Debt Profile

Net Debt at historical low for the last 7 years - a major part being long term

Debt Repayment Schedule FY 2018 Debt Composition (Nominal)

US$500m notes

maturing Nov Convertible Bond

2022 17%

Total Debt

US$100m

US$600m

convertible bond

issue maturing 500

Mar 2020 Guaranteed

Notes

83%

– 100 –

2019 2020 2021 2022

2020 Convertible Bond 2022 Guaranteed Notes

— Principal amount: US$100m — Principal amount: US$500m

— Coupon: 9% — Coupon: 8.125%

— Maturity: Mar 2020 — Maturity: Nov 2022

— Exchange price: US$0.1253 — Rating: S&P = B-, Fitch = CCC

17Petropavlovsk’s Guarantee of IRC’s New Debt Facilities

A key milestone in de-risking the Group’s finances

The Gazprombank Debt Facility Petropavlovsk Guarantee Structure

— In Dec 2018, K&S (a subsidiary of IRC) entered into a — Comprised of 5 guarantees which fluctuate over life of loan

US$240m facility with Gazprombank

— The current guarantee amount is US$160m comprising a

— Replaces an earlier facility with ICBC on more favourable terms: Corporate and Fixed Term Guarantee

— Extended repayment period through to 2026 — The Corporate Guarantee will be removed subject to certain

operational conditions at the K&S project being met(1)

— Principal repayment skewed to the latter part of the loan

term

— Amortisation schedule better aligned to the ramp-up of Corporate Fixed Term

the K&S iron ore mine Guarantee Guarantee

2019

$40m

2020 $120m

2021

$40m

2022

2023

$40m

2024

2025

$120m

2026

(1)These conditions are considered to be ‘base case’ and the Company expects these will be achieved within a 3 year time-frame

18Q1 2019 Update

Q1 2019 Production Update

A healthy start to 2019 with c.25% of output attributable to the processing our own refractory ore

Production in line — Production / sales of 108Koz - with 28Koz of refractory gold processed at the POX Hub

with target — Strong contribution from Malomir underground with grades in excess of 8g/t

Malomir flotation — Successful test work carried out on concentrate from lower grade ores: 87% recovery with

continues to produces

better than design concentrate yields (2.8% vs. 5.5%) à lower TCC

refractory concentrate with

improved parameters — c.29Kt of concentrate at 28g/t containing 26Koz of gold stockpiled for processing

POX: Q1 recoveries — c.32Kt of high-grade concentrate at 32g/t processed via POX Hub

reached 91%, — POX recoveries reached 91% in March, targeting 94% in H2 2019

autoclaves 3 + 4 ready for — Autoclaves 3 + 4 tested + shown to be fully-functioning. Ready to begin operating at full

launch capacity once supply of 3rd party concentrate secured

Acquisition / trial of

3rd party concentrate to — Concentrate successfully trialled from two different sources

optimise POX utilisation — 2 x batches of concentrate secured, incl. 17Kt at 65g/t – 75g/t + 20Kt at 40g/t – 60g/t

rates

IRC: successful — New loan facility with Gazprombank on better terms

refinancing of ICBC — Petropavlovsk has received c.US$57m as full repayment for 2 x bridge loans advanced to

project finance facility IRC in 2018

20Q1 2019 Operations Review

Strong performance let down by water issues at Pioneer(2) – remain on track to meet 2019

guidance

Q1 2019 Au Production by Mine(1) Q1 2019 Production Highlights

Malomir production above budget

— Non-refractory ore via RIP: gold recoveries exceeded

budget by 6.2Koz due to larger quantity of high-grade ore

Malomir (incl. POX) mined from underground + higher recoveries

45Koz (41%)

— Flotation: 25Kt of concentrate produced at avg. grade of

23g/t

— POX Hub: 32Kt of concentrate processed at avg. grade of

Total 32g/t, with 2.8Koz of metal produced above quarterly

production budget

Pioneer

108Koz 22Koz Albyn production above budget

(20%)

— c.200Kt of ore at 1.2g/t was mined above budget, resulting

Albyn in 4.3Koz of production above plan

41Koz (38%)

Pioneer production below budget

— Underground delays caused by persistence of water inflow

+ lower grade material from open pit(2)

— Production 6.7Koz below budget

Company remains on course to meet FY2019 guidance

(1) Percentages may not add up due to rounding

(2) At Pioneer, all water has been pumped out of mine, cement backfill has been implemented and pump size increased 212019 Outlook

222019 Outlook

Guidance has improved following successful commissioning of POX Hub

— Targeting 450Koz – 500Koz Au, an increase vs. 2018 due to contribution from POX Hub facility (incl.

gold in concentrate stockpiles from FY 2018), but excluding potential upside from 3rd party concentrate

Gold processing

production — c.125Kt – 145Kt of refractory concentrate expected to be produced by Malomir flotation plant at 29gt –

32g/t

— c.155Kt – 175Kt of refractory gold concentrate at 30g/t – 31g/t to be treated at POX Hub

— TCC FY 2019: US$850 – 950/oz, based on a RUB:US$ FX of 66, reflecting additional POX Hub

ramp-up costs

Costs

— Once POX is operating at full production from 2020, TCC expected to normalise at c.15% below 2019

guidance

Capex — US$45m – US$55m, consisting of sustaining, exploration + remaining POX capex

— Autoclaves 3 + 4 to begin operating at full capacity once supplies of 3rd party concentrate secured

Development — Management + Board are considering benefits of accelerating construction of additional flotation lines

at Pioneer / Malomir

De-leveraging — Net debt to continue to fall in line with ramp-up of production + increase in free cash flow(1)

(1) Net debt (unaudited) as of 31 March 2019 reduced to c.US$550m

23Malomir Flotation Plant

24

24Malomir Flotation Plant

Production rates expected to increase from Q2 2019 once the Malomir flotation plant begins

processing higher grade material to produce higher grade concentrate

Background Stage 2 flotation plant expansion

— Malomir flotation plant is a two-stage development — Stage 2 will expand Malomir flotation to 5.4Mtpa by adding a

third 1.8Mtpa line to the existing two

— Stage 1: 3.6Mtpa capacity across 2 x 1.8Mtpa processing lines

(line 1 launched Jul, line 2 Oct 2018) — Management considering fast-tracking expansion to maximise

utilisation of POX Hub capacity (currently 2020)

— With both lines ramped-up, the flotation plant produced c.46Kt of

high-grade refractory concentrate with grades of up to 36g/t in

2018

Flotation process flowsheet improvements

— Gold losses reduced: more efficient flotation reagent to suppress

carbon has eliminated need for carbon flotation stage

— c.50% improvement in concentrate grade vs. original design

parameters (c.24g/t vs. c.36g/t – 40g/t)

— Concentrate mass pull improved from 5.5% to c.2.8% (using

lower grade ores), reducing volume of material transported

Tests work has produced 25Kt of concentrate from low grade

material

— Low grade trial material (c.0.7g/t), stripped ahead of accessing

main ore body was processed, achieving concentrate grades of

22g/t – 24g/t at 87% recovery

— Resulting concentrate yield of c.2.8% significantly better vs.

Flotation cells at the Malomir flotation plant

5.5% long-term plan, reducing transport volumes / costs

25The Pokrovskiy POX Hub

Our New Pressure Oxidation (POX) Hub Presents Growth Opportunities

Commissioned in Q4 2018, the POX plant is the result of almost a decade of work by our in-house

group of scientific experts + engineers

§ Over 50% of Russia’s defined gold resources are refractory or partially

refractory

§ Extraction of gold from refractory ore requires additional stages eg.

flotation, then pressure oxidation (POX) to extract gold from flotation

concentrate

§ POX is a globally recognised process for treating refractory ore and

flotation concentrate

§ The POX Hub repositions the Group as a technological + operational

leader, within Russia + in a global context

§ Optionality / growth: treatment of 3rd party concentrate, acquisition of

refractory deposits

External view of the POX Hub complex We expect to unlock c.60% of our R&R via the POX Hub

JORC Resources(1) JORC Reserves(1)

Refractory Refractory

60% / 12.3Moz 65% / 5.3Moz

20.5 8.2

Moz Moz

Non-refractory Non-refractory

40% / 8.2Moz 35% / 2.9Moz

Autoclaves

(1) In accordance with the JORC Code, as at 31 Dec 2018. Resources (M,I&I) are inclusive of Reserves. For full details and asset by asset breakdown

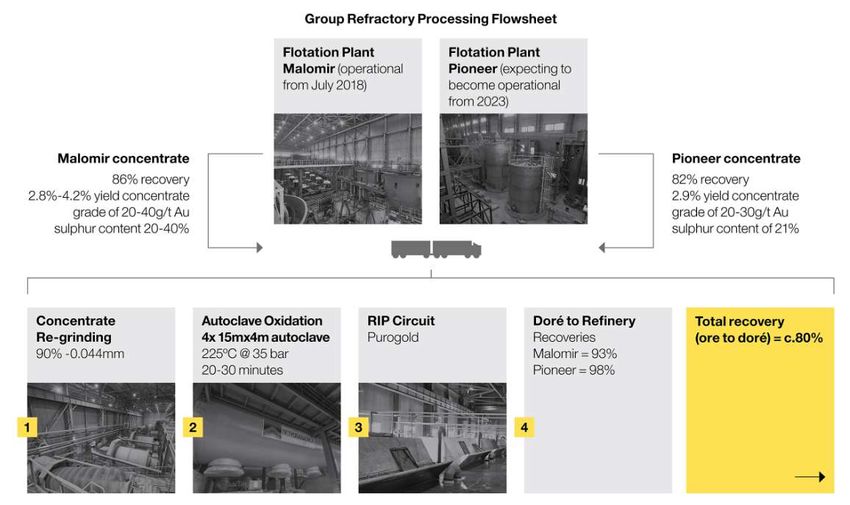

please refer to the 2018 Petropavlovsk annual report 27Refractory Gold – the Journey from Mined Ore to Doré

Process flowsheet and parameters

28POX Hub: Successfully Commissioned End of 2018

Total installed capacity of 400Ktpa – 500Ktpa(1)

2019 plans

Autoclaves 1 + 2 Autoclaves 3 + 4

— Lines 1 + 2 at POX expected to treat 155Kt – 175Kt of

– Commissioned Q4 2018 – Tested in Q1 2019 à fully- refractory concentrate in 2019 at 30g/t – 31g/t

functioning

– 32Kt of concentrate — This includes:

processed at avg. c.32g/t – Ready to start once 3rd

— 125Kt –145Kt at 29g/t – 32g/t representing

in Q1 2019 party concentrate secured

material mined in 2019

— 29Kt at 28.2g/t representing material mined in

2018 and stockpiled

100 - 125Ktpa(1) 100 - 125Ktpa(1) 100 - 125Ktpa(1) 100 - 125Ktpa(1)

— 37Kt at 40-75g/t of 3rd party concentrate

40% 2020 onwards

— Once additional flotation lines have been installed at

Malomir + Pioneer, POX will be able to treat up to:

100% 100% 100%

30% — 200Ktpa of concentrate from Malomir (at 27%

sulphur) from 2020

— 240Ktpa from Pioneer (at 23% sulphur) from 2023

30%

Autoclave 1 Autoclave 2 Autoclave 3 Autoclave 4

Mined in 2019 Mined in 2018 and stockpiled 3rd party concentrate

(1)POX capacity determined by sulphur levels, hence capacity shown here as ranges which depend on specific qualities of 29

source material (lower sulphur = higher POX plant capacity)R&R / Exploration

Track Record of Resource Growth

As at 31 Dec 2018, Group Reserves & Resources totalled 20.5Moz Au, with Reserves of 8.2Moz

Au

— Following successful commissioning of POX, some transitional Resources and Reserves suitable for either RIP or refractory processing,

were reclassified from non-refractory to refractory.

— As a result, and due to the success of 2018 exploration campaign, total refractory Resources increased by 2.7Moz to 12.3Moz

— There was a corresponding decrease in non-refractory Resources from 11.2Moz to 8.2Moz (this change also reflects mine depletion and

disposals)

10.1 12.3 11.7 13.8

14.0 14.4 8.2

10.4 11.2

2.1 6.0

13.0 12.8 12.1 12.0 12.3

9.3 9.3 9.3 9.6

6.8 5.2

1.4 1.9 2.4 3.8 5.1 5.9 6.6 7.2

11.2 11.7 12.5

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Refractory Resources Non-Refractory Resources Depletion + Disposals

31Mine by Mine JORC Resource Breakdown

New Resources at Pioneer, Albyn, Malomir and Pokrovskiy

Total JORC Resources (as at 31/12/2018) Non-Refractory Resources

Refractory Resources

New Resources -

Explanation

8.2Moz 20.5Moz 12.3Moz

40% 60%

Malomir Pioneer Albyn Pokrovskiy

6.7Moz 4.5Moz 4.2Moz

97% 76% 79%

6.9Moz 5.9Moz 5.3Moz 0.9Moz

1.1Moz

1.4Moz 21%

24% 0.9Moz

0.2Moz 100%

3%

RIP tailings for Decrease due to

Katrin

reprocessing via Albyn main ore body + disposals +

Nikolaevskya

flotation + POX and Unglichikanskoye sterilisation due at

Ulunginskaya

Quartzitovoye POX facility

32

Note: Tokur, not shown above, contains non-refractory Resources of 1.4Moz. For full details and asset by asset breakdown please refer to the 2018 Petropavlovsk annual reportIRC Limited

33IRC Limited (1029.HK)

Petropavlovsk has a 31.1% equity share in Hong Kong-listed iron ore producer IRC

Who are IRC? POG Equity Interest In IRC

A developer + producer of industrial commodities, principally Petropavlovsk is a 31.1% shareholder

iron ore — IRC is accounted for as an associate

— Based in the Russian Far East, IRC benefits from low — Market value of US$46m as at 21 May 2018(1)

production costs and proximity to China — Petropavlovsk is assessing the best way to realise the value of its

— IRC was part of Petropavlovsk’s Non-Precious Metals Division, interest in IRC

before listing on the Hong Kong Stock Exchange in 2010 Petropavlovsk acts as a guarantor in relation to a US$240m

IRC’s key mining assets include: Gazprombank facility entered into by K&S (an IRC subsidiary) in

— K&S: a producing iron ore(1) mine with a 20 year mine life Dec 2018

— Located in the Jewish Autonomous Region, Russian — This new facility supersedes / replaces the US$340m facility

Far East entered into between IRC and the Industrial and Commercial Bank

— Produces premium quality high grade 65% Fe iron ore of China (ICBC) in 2010, enabling IRC to construct / develop the

— Ramping up to phase I design capacity of 3.2Mtpa, with K&S mine

option to increase to 4.6Mtpa (K&S Phase 1.5) and — New facility matures 2026 and is on better terms, with payments

6.3Mtpa (K&S Phase II) aligned with the ramp-up and cash flows expected from production

— Kuranakh: on care + maintenance since Q1 2016 at K&S

— Garinskoye: project is at an early stage of exploration

(1) IRC market capitalisation as at close 25 April 2019 (US$149m, source: Bloomberg) x Petropavlovsk’s equity interest (31.1%) = US$46m

34FY 2018 IRC Results

Strong FY performance due to successful continuation of K&S ramp-up + refinancing of ICBC project

finance facility

— Total revenue +39% to US$152m (vs. US$ 109m in 2017) due to increased K&S output

— EBITDA +42% to US$29m (vs. US$20m in 2017) due to stronger revenues + stricter cost-control

Financials

— Net profit of US$68m (vs. US$113m in 2017)

— Impairment reversal of US$91m

— Iron ore concentrate production +43% to 2,235Kt (vs. 1,563Kt in 2017)

— Iron ore concentrate sales + 44% to 2,224Kt (vs. 1,539Kt in 2017)

— Avg. selling price of US$68/t (vs. US$70/t in 2017)

Operations

— In Dec 2018, K&S achieved a record-breaking monthly production by operating at an average capacity

of c.84%

— Care + maintenance at Kuranakh mine remains satisfactory

— K&S (a subsidiary of IRC), entered into a new loan facility agreement with Gazprombank to refinance

Corporate existing ICBC loan, with principal repayments better aligned with ramp-up of K&S

— Mr Peter Hambro appointed as Non-Executive Chairman of IRC

— Russian + Chinese sections of Amur river bridge successfully connected

Amur bridge — The bridge is expected to be operational in Sep 2019 once customs checkpoints + other ancillary

infrastructure are in place

35Appendix

36

36Corporate Structure + Overview

Shareholder Structure (as at 31 March 2019)

Kenges Rakishev

(via Fincraft Holdings

Ltd & VTB Bank)

Other 22.4%

36.7%

Sothic Capital

10.9%

Prosperity Capital

Everest Alliance 8.3%

4.6%

DE Shaw & Co

Slevin 7.8%

4.6% RCB Bank

4.7%

Share Price, Gold Price, FX(1) Share Price and Trading Volumes(1)

Price (GBP, pence) 8.3p 9.0p 50m

Price Vols

52 Week Range 5.2p – 8.4p 8.5p

Avg. Daily Vol (12m) 3,644,578 40m

8.0p

Shares outstanding 3,307,151,712

Market Cap. £274m (US$356m) 7.5p 30m

EV £711m (US$924m) 7.0p

6.5p 20m

Gold PM Fix $1,284/oz

52 Week Range US$1,178/oz - US$1,344/oz 6.0p

10m

5.5p

USD:RUB FX 64.8

52 Week Range 61.2 – 70.5 5.0p 0m

(1) Data as at market close 26 April 2019

37FY 2018 Operations Overview

Production summary

Mining Units FY 2018 FY 2017

Total material moved m3 000 44,383 57,539

Ore mined t 000 10,294 17,990

Average grade g/t 1.2 0.9

Processing

RIP

Total milled t 000 13,595 16,620

Average grade g/t 1.0 0.8

Gold content Koz 417 448

Recovery rate % 84% 80%

Gold recovered Koz 351 360

Heap Leach

Ore stacked t 000 701 1,250

Average grade g/t 0.5 0.4

Gold content Koz 11 18

Recovery rate % 54% 50%

Gold recovered Koz 6 9

Gold in concentrate – POX Koz 52 -

TOTAL gold production Koz 422 440

Gold sales Koz 370 440

Costs

TCC US$/oz 786 741

AISC US$/oz 1,117 963

38You can also read