PIRAEUS BANK INVESTOR UPDATE - London, 15 July 2019 - Piraeus Bank Group

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

PIRAEUS BANK

INVESTOR UPDATE

London, 15 July 2019

TODAY’S AGENDA 10:00 Welcome 10:00-10:30 Christos Megalou Chief Executive Officer 10:30-10:50 Elias Lekkos Chief Economist 10.50-11:20 Theodore Gnardellis | George Christopoulos Piraeus Legacy Unit Strategy | Asset Sales 11:20-12:00 Q&A 12:00-12:10 Break 12:10-12:30 Eleni Vrettou Corporate & Investment Banking 12:30-12:50 George Georgakopoulos Piraeus Legacy Unit | NPE Servicer 12:50-13:20 Q&A 13:20-13:30 Christos Megalou Chief Executive Officer 13:30 Closing Additional participants in Q&A: Tom Arvanitis (Piraeus Financial Markets), Chryssanthi Berbati (Investor Relations)

Discussion Items

STRATEGIC OVERVIEW 01

GREEK ECONOMY & OUTLOOK 02

NPE STRATEGY & EXECUTION 03

CIB PERFORMANCE & TRENDS 04

NPE SERVICING AGREEMENT 0501 STRATEGIC OVERVIEW

01 1.1 OUR DEVELOPMENTS | AT A GLANCE

A 2018 Capital Strengthening Plan Completion

B Enhancement of Capital Buffers by Recent Tier 2 Issue

C Strategic Partnership with Intrum on NPE Servicing

D New Roadmap “Agenda 2023”

E 2015 Restructuring Plan Completion

F NPE Strategy Execution on Track

G New Business Picking-Up & Positive Jaws

5 | STRATEGIC OVERVIEW01 1.2 OUR DEVELOPMENTS | CAPITAL

A 2018 Capital Strengthening Plan Completion

• The internal capital actions of 2018 have been concluded €0.5bn

• A 10NC5 Tier 2 was issued on 26 June 2019 €0.4bn

• Additional initiatives are executed (eg NPE servicing agreement) €0.4bn

€1.3bn

6 | STRATEGIC OVERVIEW01 1.3 OUR DEVELOPMENTS | TIER 2

B Enhancement of Capital Buffers by Recent Tier 2 Issue

Allocation by Investor Type Allocation by Geography

7 | STRATEGIC OVERVIEW01 1.4 OUR DEVELOPMENTS | NPE SERVICING

C Strategic Partnership with Intrum on NPE Servicing

• New servicer company for the management of NPEs & REOs

• Market-leading independent NPE servicer

• 80% of the new servicer company will be held by Intrum & 20% by Piraeus Bank

• Expectation for a material boost to the execution of Piraeus’ de-risking strategy

8 | STRATEGIC OVERVIEW01 1.5 OUR DEVELOPMENTS | STRATEGY

D New Roadmap “Agenda 2023”

• Piraeus Bank introduced its new strategic roadmap with the following targets:

Cost-to-Income ratio at low 40s

Non Performing Exposures at single-digit ratio

Return on Tangible Equity at high single-digit

Regulatory Capital ratio at ~200bps above requirement

9 | STRATEGIC OVERVIEW01 1.6 OUR DEVELOPMENTS | RESTRUCTURING PLAN

E 2015 Restructuring Plan Completion

• Greek operations commitments completed (eg headcount, branches, costs, LDR)

• International divestments concluded (eg Serbia, Romania, Albania, Bulgaria)

10 | STRATEGIC OVERVIEW01 1.7 OUR DEVELOPMENTS | NPE REDUCTION

F NPE Strategy Execution on Track

• 6M.19 NPE reduction as per target

• NPE sales of €2.3bn GBV completed in one year, €0.7bn NPE sale at BO phase

• More than €2bn RRE-based securitization in preparation, planned for early 2020

11 | STRATEGIC OVERVIEW01 1.8 OUR DEVELOPMENTS | PROFITABILITY

G New Business Picking-Up & Positive Jaws

• Healthy business demand emerging in sectors geared to growth and exports

• Target for €4bn new loans in 2019 vs €3bn in 2018; €1.9bn in H1.19

• Credit decisions based on the Bank’s Adjusted Returns Tool (“ART”)

• Earnings capacity supported by both top line and OpEx improvement

12 | STRATEGIC OVERVIEW01 1.9 2018 CAPITAL ENHANCEMENT PLAN

The €3.6bn RWA Relief is Equivalent to €0.5bn Capital Enhancement for the Bank

RWA

Actions Announcement Status

Relief

>> Avis [operating leasing company] Q1.18 ~€0.2bn

>> Serbia [banking subsidiary] Q2.18 ~€0.3bn

>> Romania [banking subsidiary] Q2.18 ~€0.6bn

>> Amoeba [secured NPL portfolio] Q2.18 ~€0.4bn

>> Arctos [unsecured NPL portfolio] Q2.18 ~€0.1bn

>> Albania [banking subsidiary] Q3.18 ~€0.4bn

>> Bulgaria [banking subsidiary] Q4.18 ~€0.7bn

>> Other de-risking actions [non-core assets de-risking] Q4.18 ~€0.6bn

>> Nemo [secured NPL portfolio] Q2.19 ~€0.3bn

Total ~€3.6bn

13 | STRATEGIC OVERVIEW01 1.10 2019 CAPITAL ENHANCEMENT PLAN

Capital Position Strengthening through a Number of Additional Initiatives

Targeted Capital

Management Actions

Improvement

Issued

A. Tier 2 debt issuance 26 Jun.19

~85bps

NPE servicing

B. Sale of operations, non-core subs & participations agreement

~80bps

C. Review of high capital-consuming businesses

D. Enhanced organic revenue generation

E. Accelerated cost efficiency actions

F. Balance sheet optimization | RWA management

160-200 bps

total initial guidance

14 | STRATEGIC OVERVIEW01 1.11 CAPITAL TRAJECTORY POST RECENT TRANSACTIONS

Recent Transactions, Coupled with Return to Profitability, Strengthen Capital Position

Total Regulatory Capital (%, phased-in) Total Regulatory Capital (%, fully loaded)

15 | STRATEGIC OVERVIEW01 1.12 PROJECTED CAPITAL EVOLUTION

Organic Capital Generation Supports Capital Development Going Forward

Total Regulatory Capital (%)

+0.9% +0.8% +0.4%

14.0% to 14.5% OCR

e: estimate; f: forecast

16 | STRATEGIC OVERVIEW01 1.13 GREEK MARKET NPE TRAJECTORY

The 3-year NPE Targeted Reduction Equals ~30% of GDP; Ambitious yet Feasible

NPE ratio 48% 48% 47% 45%01 1.14 REAL ESTATE MARKET TREND

Upside Potential to Collateral Valuations from Acceleration of Real Estate Price Recovery

Outlook for Real Estate Prices Embedded in Existing Plan

2017a 2018a 2019e 2020f 2021f

Non-residential real estate price change 1.6% 5.0% 4.0% 3.6% 3.6%

Residential real estate price change -1.0% 1.5% 2.6% 3.2% 3.6%

a: actual, e: estimate, f: forecast

Source: Piraeus Economic Research, baseline scenario

• Current Run-Rate of Non-Residential RE prices at +6% and Residential at +4% yoy

• Piraeus Bank has €23bn of real estate assets as underlying collateral for loans and €3bn οf own

assets. Almost €11bn relates to NPE portfolio

• For every 100bps incremental shift in Real Estate prices, estimated value improvement is

approximately at €50-100mn

18 | STRATEGIC OVERVIEW01 1.15 IMPROVED LIQUIDITY PROFILE

Satisfactory Liquidity on the back of Deposit Restoration and Macroeconomic Stabilization

Domestic Deposits | €bn Liquidity Coverage Ratio (%)

LDR c.85%

>95%

19 | STRATEGIC OVERVIEW01 1.16 LOAN BALANCES

Loan Evolution Incorporates the Parallel Dynamics of De-risking and Healthy Loan Growth

Gross Loans (€bn) New Loans (€bn, %)

~6

53 ~5

48

-15 ~4

NPE

3.1

PE +10

Non performing exposures to be reduced as per plan Business lending is the driver of loan growth

Performing exposures: €15bn new loans and €2bn net

curings to be offset by €7bn amortization and other e: estimate; f: forecast

20 | STRATEGIC OVERVIEW01 1.17 ADJUSTED RETURNS TOOL

Adjusted Returns Tool Developed for Risk-Based Pricing, Fully Adopted by the Bank’s Business Units

Cost of Cost

Credit Risk ARoC

Spread

Cost of

Capital

Cost of Hurdle Profit Final Yield

Liquidity Rate Margin / Spread

Operating

Expenses*

The overall methodology aims at:

Ancillary optimizing capital allocation

Revenues** establishing a hurdle rate for every loan decision

capturing term profitability, focusing on return

maximization and credit loss mitigation

* Operating expenses soon to be introduced into the methodology enhancing the risk culture across the Bank

** Ancillary revenues have a positive contribution, thus reducing the Hurdle rate

21 | STRATEGIC OVERVIEW01 1.18 REVENUES & OPEX| POSITIVE JAWS

Positive Jaws Supported by Frontloaded Cost Cuts and Revenue Increase post 2020

Operating Jaws (€bn)

• Xxx

• Xxx

1.2

• Xxx

a: actual; e: estimate; f: forecast

22 | STRATEGIC OVERVIEW01 1.19 NET INTEREST INCOME

Resilient NII Going Forward as Improvement on the Asset Side Offsets Debt Issuance Costs

(€mn) 2018a 2019e

● Current NII run rate at mid single digit increase

Interest Income 1,874 1,830

Loans & Bonds 1,770 1,715 ● NII going forward growing at low single digit pace per

Other 105 115 annum: yield from new assets will outpace increasing

Interest Expense 465 430 debt securities issuance costs

Deposits 199 180

● Loan income to move into positive trajectory in line

Interbank Funding 50 15

with new healthy disbursements

Debt Securities 6 25

Other 210 210

Net Interest Income 1,410 1,400

a: actual; e: estimate

23 | STRATEGIC OVERVIEW01 1.20 FEE & COMMISSION INCOME

NFI to Grow Along with the Macro Recovery & Increasing Penetration to Specific Areas of Business

(€mn) Q1.2019 % Assets

● Enhancement initiatives implemented to

Loans 13.1 0.09%

boost fees from all areas of business at par

Acquiring 12.1 0.08%

with gradual macroeconomic recovery

Funds Transfer 11.9 0.08%

Cards Issuance 9.5 0.07%

Bancassurance 8.4 0.06% ● Fees stemming from transaction banking,

Letters of Guarantee 8.3 0.06% credit cards, payments and asset

Payments 6.1 0.04% management / brokerage are expected to

AM & Brokerage 5.5 0.04%

perform in line with our strategy

FX Fees 3.8 0.03%

Deposits 1.6 0.01%

Other 7.7 0.05%

Total Fee Income 88.0 0.61% above 0.8% in the medium term

24 | STRATEGIC OVERVIEW01 1.21 G&A COSTS

G&A Costs Running at -20% Reduction Rate Boosting the Bank’s Efficiency Ratio

(€mn) 5M.18 5M.19 yoy

Rents 17 15 -12% ● Current run rate of more than 15% reduction yoy

Maintenance 14 11 -22%

● Going forward, high single-digit pace of reduction

IT 13 10 -28%

Third Parties 25 20 -22% ● Efficiencies to be further increased along with

Promotion, Subscriptions 14 12 -19% increasing digitalization, as well as the

Taxes 56 48 -14% implementation of the NPE servicing agreement

Other 18 12 -34%

Total G&A Costs 158 126 -20%

Preliminary data for 5M.19

25 | STRATEGIC OVERVIEW01 1.22 REVAMP OF GOVERNANCE & CONTROLS

• Reshuffling of Top Management

• Revamp of Internal Policies and Controls

• Adjusted Return on Capital Methodology and Process

• Cultural Transformation: work- in-progress as of 2017

• Roadmap for the Future

26 | STRATEGIC OVERVIEW01 1.23 LATEST FINANCIAL TRENDS

€1bn customer deposits increase in Q2.19

LDR at ~ 85%; LCR at ~ 95%

Deposit cost further contained

NPE movement on track with the yearly 2019 target

More than €2bn RRE-based securitization in preparation, placement in 2020

Positive tailwinds from real estate collateral revaluation

Performing loan book increased in 6M.19 by more than €500mn (€1.9bn new loans)

Resilient new loan production yields

OpEx running at high single digit reduction pace yoy

27 | STRATEGIC OVERVIEW02

GREEK ECONOMY & OUTLOOK

Can the New Government Revive the Greek “Animal Spirits”?02

Since 2017, the Greek Economy has been Range-bound Between 1.5%-2.0%

2.1 ECONOMIC RECOVERY

2019e

1.6%

Source: ELSTAT, Piraeus Bank Research

29 | GREEK ECONOMY & OUTLOOK02

The New Government’s Plan to Reach “Escape Velocity”

2.2 NEW GOVERNMENT’S PLAN

Fiscal Stimulus Investment “Shock” Escape Velocity €4bn

€0.5bn corporate tax rates cut in 2-years €60bn 4.0% Real GDP = €4.0bn tax revenues

€0.45bn dividend tax rate cut Special incentives (doubling of the time for Efficiency Savings €2bn

offsetting losses, 200% over-depreciation

€2.6bn personal income tax rate cut (up new investments) €0.2bn public consumption spending cut

to €10,000)

€12bn in infrastructures €1.19bn rationalization & improvement in

€0.8bn increase in the tax free income DEKO & General Government Legal Entities

threshold by €1,000 for each child €20-€25bn in tourism and shipping

€0.14bn interest payments cut for T-bills

€1.02bn VAT rate cuts €15-€20bn in primary sector and food

processing manufacturing €0.15bn no public sector wage increase

€0.3bn business fee gradual abolishment

€0.4bn special solidarity levy gradual cut €9bn in energy and the environment €0.3bn hiring / retirement ratio (1/5)

€0.4bn ENFIA (property tax) cut in 2-years €10bn in R&D, Industry, logistics and PPP €0.02bn unused real estate exploitation

€6bn €6bn

Source: ND Elections 2019 Programme, Piraeus Bank Research

Fiscal Neutrality

30 | GREEK ECONOMY & OUTLOOK02

For 2.0% Average GDP Growth we Need to “Crowd-in” €325bn of Investments

2.3 INVESTMENTS ENVIRONMENT

Non Financial Corporations Investments & Net Capital Stock (€bn)

Net vs Gross Fixed Capital Formation (€bn, current prices)

20.0

1990 - 1999 2000 - 2008 2009 - 2018 2019 - 2027

15.0

10.0

5.0

0.0

Disinvestment

-5.0

through depreciation

-10.0 Capital Capital Capital

Stock 1989 Capital GFCF GFCF GFCF GFCF Stock 2027

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Consumption Consumption Consumption Consumption

Gross Fixed Capital Formation Net Fixed Capital Formation

Source: ELSTAT, Piraeus Bank Research

31 | GREEK ECONOMY & OUTLOOK02

But after a Long Recession “Animal Spirits” are Dormant

2.4 ANIMAL SPIRITS

Source: EC DG ECFIN, Piraeus Bank Research

32 | GREEK ECONOMY & OUTLOOK02 2.5 GREEK CORPORATES (i)

Despite Popular Belief, Greece has a Substantial “Bankable” Corporate Universe

outperformers a

(7.9%)

668

good performers b

(35.5%)

2,985

c

medium performers

(41.3%) 3,477

d

underperformers

(15.3%) 1,289

Source: ICAP DATA, Piraeus Bank Research

33 | GREEK ECONOMY & OUTLOOK02

Dormant “Animal Spirits” Drive Defensive Corporate Balance-sheets to Extremes

2.6 GREEK CORPORATES (ii)

EBITDA margin Total liabilities to equity Net debt to EBITDA

d. 3.6 d. 25.0

d. -8.1%

c. 2.8 c. 13.6

c. 7.1% Total Total

Total b. 1.2 b. 3.8

b. 14.7%

a. 0.5 a. 0.1

a. 24.9%

d. 1.8% d. 4.0 d. 26.4

c. 6.9% c. 3.6 c. 11.6

Large Large Large

b. 13.0% b. 1.2 b. 4.1

a. 33.0% a. 0.7 a. 2.2

d. -8.3% d. 3.6 d. 24.9

c. 7.1% c. 2.7 c. 13.7

SMEs SMEs SMEs

b. 14.8% b. 1.2 b. 3.8

a. 24.7% a. 0.5 a. 0.1

-20% -10% 0% 10% 20% 30% 40% 0 1 2 3 4 0 10 20 30

Source: ICAP DATA, Piraeus Bank Research

34 | GREEK ECONOMY & OUTLOOK02

But Corporate Credit is Recovering…

2.7 CREDIT ENVIRONMENT

Corporate Loans (annual % change) Corporate Loans (net flows €bn) Corporate Loans by sector (annual % change, Apr.19)

Manufacturing,

Mining & Quarrying 18.8

Electricity, Gas &

Water Supply

Accommodation & Food

Service Activities (Tourism) 51.5

Storage & Transportation

other than shipping

Professional, scientific,

technical, administrative &

support activities

Source: Bank of Greece, Piraeus Bank

35 | GREEK ECONOMY & OUTLOOK02

…as well as Real Estate Valuations

2.8 REAL ESTATE ENVIRONMENT

Residential Real Estate Prices (annual % change) Non Residential Prices (annual % change) Real Estate FDI in Greece (€mn)

6.4% €392mn

500.0

4.0%

400.0

300.0

200.0

100.0

0.0

-100.0

Q1/07

Q4/07

Q3/08

Q2/09

Q1/10

Q4/10

Q3/11

Q2/12

Q1/13

Q4/13

Q3/14

Q2/15

Q1/16

Q4/16

Q3/17

Q2/18

Q1/19

Source: Bank of Greece, Piraeus Bank

36 | GREEK ECONOMY & OUTLOOK02

With Plenty of Entry Points for New Capital

2.9 TRENDS & OPPORTUNITIES

Greece needs to reorient itself from a Greece has a number of competitive In several sectors and for a variety of

consumption-based to an export-based advantages but needs to move up reasons, a massive consolidation process

economy the Value Added Chain has started

Even in sectors with a competitive In sectors with less stellar prospects such

Emphasis on export-oriented sectors: as retail and wholesale trade, fish-

advantage Greece needs infrastructure

Tourism, farming, food processing, oil farming, passenger shipping, telecoms,

upgrades, ie 5-star resorts, yachting,

refining, basic metals & minerals, consolidation will create sectoral

convention centers, marketing &

chemicals, pharmaceuticals champions with improved margins

branding

More funding, either in the form of equity Greece is facing regulatory pressures to Greek banks have committed to reduce

or loans, will be required liberalize and privatize a number of sectors NPLs and restructure their balance sheets

Banks commitment to reduce NPLs & Non

Privatized assets & natural resources Clusters can be created around privatized

Core Assets will create opportunities in

development will require substantial assets, ie ship-repair zone, logistics, cargo

real estate, insurance and leasing, hotels

investment (equity or loans) management, cruise tourism

and in over-indebted but viable

Regulatory pressures to liberalize companies

industries such as electricity, natural gas,

waste processing & management,

Source: Piraeus Bank Research renewable energy

37 | GREEK ECONOMY & OUTLOOK03 NPE STRATEGY & EXECUTION

03 3.1 OUR WORK UNTIL NOW

NPE Reduction of €5.5bn in 2018, the Largest Annual Reduction in the Greek Market

Group NPE Development (€bn)

96%

Restructuring Volumes (€bn)

-€12.0bn

Coverage

39 | NPE STRATEGY & EXECUTION03 3.3 GROUP NPE UP TO 2021

NPE Reduction of €15bn until YE.21, of which Almost Half o/w Securitizations €6.0bn

via Inorganic Actions • loss budget already

embedded in CoR guidance

• >100% coverage by

provisions and collateral

Inflows: €6.1bn

amounts in €bn

40 | NPE STRATEGY & EXECUTION03 3.2 NPE MOVEMENT DECOMPOSITION

NPEs | Bank data (€bn) Required effort

per quarter on

30.8 28.3 27.5 26.4 25.9 average until

Dec.2021

Re-defaults

Defaults

Average Average

Q1.18-Q1.19 Q2.19-Q4.21

Curings, Curings (0.6) George Curings (0.6)

Collections, Collections (0.2) Collections (0.1)

Liquidations Liquidations (0.1) Handji Liquidations (0.2)

Write-offs

nicolao

u

Sales

Q1.18 Q2.18 Q3.18 Q4.18 Q1.19 Q2.19 - Q4.21

41 | NPE STRATEGY & EXECUTION03 3.4 SIGNIFICANT CURING POTENTIAL

25% of NPEs have 0days of Arrears; Pace of NPE Exits from Curings at €0.6bn per quarter

NPEs per Bucket (Mar.19) Cash Coverage Ratio (Mar.19) Forborne Loans (€12.3bn, Mar.19)

[1] [2] [3] [4] [1+2+3+4]

(€bn) 0 dpd 1-89dpd >90dpd Denounced NPEs

Business 5.6 1.9 2.0 8.4 17.9

Mortgages 0.9 0.8 0.8 3.8 6.2

Consumer 0.2 0.2 0.5 1.8 2.8

TOTAL 6.7 2.8 3.3 14.1 26.9

NPΕ mix 25% 10% 12% 52% 100%

42 | NPE STRATEGY & EXECUTION03 Business

3.5 COVERAGE BY SEGMENT

Business

Total 95% Total 130%

Mortgages Mortgages

Total NPE Total NPL

coverage at coverage at

96% 121%

Total 100% Total 108%

Consumer Consumer

Total 94% Total 104%

43 | NPE STRATEGY & EXECUTION03 3.6 SYSTEMIC SOLUTIONS UNDER CONSIDERATION

Asset Protection Scheme Asset Management Company

• Sponsored by the HFSF and the Ministry of Finance • Sponsored by the Bank of Greece

• Similar to the Italian GACS scheme introduced in 2016 • Transfer of NPE portfolio along with part of the

deferred tax credits (DTCs) to SPV

• NPL portfolio Securitisation with Senior notes retained

by the Bank and Mezzanine sold to third party • SPV funded through Securitisation issue (Senior,

investors Mezzanine, Subordinated)

• Hellenic Republic provides guarantee to Senior notes • Subordinated notes will be subscribed by the Banks

subject to conditions and the Greek State

• Favourable risk-weighting of the retained Senior notes • Private investors will absorb Senior and Mezzanine

notes

• Facilitates the execution of larger transactions volumes

• Merit of the scheme is that combines NPE deleverage

• Complementary to the Bank of Greece proposal

with improvement in quality of capital

• Proposal expected to get clearance by DGComp

• Implementation anticipated in 2020

• Implementation anticipated in 2020

44 | NPE STRATEGY & EXECUTION03 Asset Mix

3.7 DE-RISKING STRATEGY

Liability Mix

100% 100% 100% 100%

Cash, 9% 10% Interbank &

12% Debt Securities

Securities, 20%

Interbank

5%

Net NPEs 23%

75% Deposits

72%

Net PEs 42% 60%

Other

24% 12%

15% 12% Equity

assets

7% 3% Other

liabilities

2018 2023 2018 2023

45 | NPE STRATEGY & EXECUTION03 3.8 NPE CLEAN-UP TARGETS

Group NPE Balances (€bn) Agenda 2023

2018 2023

Gross NPE Ratio 53% ~9%

Net NPE Ratio 27% ~5%

Single-digit NPE ratio in 2023

Through a mix of organic and inorganic actions

More outflows and less inflows

Supported by c.€20bn restructuring volumes in 2017-2021

NPE PLAN 2021 Scheduled inorganic actions

Securitizations and NPE disposals

46 | NPE STRATEGY & EXECUTION03 3.9 NPE SALES

completed completed

Project Amoeba: Project Nemo:

€1.4bn GBV, €2.0bn legal claim c.€0.5bn GBV, equal legal claim

• Secured large SME and corporate loans • Secured shipping loans

• Sale agreed with Bain Capital Credit LP in May • Sale agreed with Davidson Kempner Capital

2018 and concluded near end of Oct. 18 Management LP in Jun.19 and concluded in

early Jul.19

2018 2019

completed

Project Arctos: Project Iris:

€0.4bn GBV, €2.2bn legal claim c.€0.7bn GBV, €1.7bn legal claim

• Unsecured personal loans and credit cards • Personal loans and credit cards, small

• Sale agreed to consortium led by APS business loans, leasing exposures

Investments Capital s.r.o. in Jun. 2018 and • Virtual Data Room opened in Mar.19

concluded at the end of Oct.18 • Non-binding offers in Apr.19; BOs in Q3.19

47 | NPE STRATEGY & EXECUTION03 3.10 KEY DATA OF COMPLETED NPE SALES

All 3 Sales Transactions have been Capital Accretive for Piraeus Bank (~25bps in total)

Amoeba Arctos Nemo Total

Gross Book Value (€bn) 1.4 0.4 0.5 2.3

Price over GBV (%) 30% 13% 47% 30%

Provision Coverage (%) 73% 90% 45% 70%

RWA (€bn) 0.4 0.1 0.3 0.8

Collateral (€bn) 0.5 n.a. 0.3 0.8

Discount over Collateral Value (%) 15% n.a. 4%

Buyer Bain Capital APS DK

48 | NPE STRATEGY & EXECUTION04 CIB PERFORMANCE & TRENDS

04 4.1 CIB | WHO WE ARE

Largest Greek Systemic Bank Customers: 10k companies

Uniquely Positioned Exposure: €15bn

to Capture Growth in

Greece Deposits: €7bn

Leading position in Corporate and SME banking

Leading Market Position Pioneer in Greek Agriculture business; leading market share in Leasing

Ranked 1st in Brokerage services

Strong liquidity and disciplined capital management approach

Longstanding relationships with proven resilience over the crisis

Our Strengths

Highly skilled professionals with deep knowledge of local market dynamics and products

Low cost-to-income ratio at high 20s% opportunity to invest

50 | CIB PERFORMANCE & TRENDS04 We serve all major sectors of the Greek economy providing full range of

4.2 OUR BUSINESS

products and services through the largest network in Greece

Segments

1 Large, Structured Finance,

Real Estate, Hotel & Tourism,

Shipping, SME & Agri

Bank

2

Product

factories

Syndications, TxB,

3

Investment Banking, Subsidiaries/

Green Banking Non Bank Products

Factoring, Leasing

& Securities

51 | CIB PERFORMANCE & TRENDS04 4.3 CIB TODAY

NII

(€mn)

Revenues of Q1.19 in line with 2019 budget

Revenues Aggressive target for 2019 NFI (+15% yoy)

Fees

Net fees +14% y-o-y in Q1.19 (€mn)

Front book yield is significant higher than New loans

yield of stock portfolio (+40bps) (€bn)

New Loans Pipeline: stands at €2bn, out of which

Generation

€0.8bn is already credit approved

50% of 2019 target achieved

52 | CIB PERFORMANCE & TRENDS04 Grow, Streamline, Protect

4.4 OUR STRATEGY

• Credit • Revenues

• Capital Protect Grow • Profitability

• Operational Risk • Market Share

The Customer

Our People

at the center

of what we do

Streamline

• Processes

• Systems

53 | CIB PERFORMANCE & TRENDS04 4.5 OUR STRATEGIC PRIORITIES

1

Achieve Sustainable Profitable Growth, Placing the Customer at the Epicenter of What We Do

Improve cross selling by taking fair share of wallet on clients’ ancillary business

Invest in Transaction Banking products

Grow Focus on sectors of Bank’s excellence: SME, Agri and Green

Claim leading underwriting position

Support FDI with acquisition financing expansion

Automate processes

Remove duplication and re-design lending process to reduce time to money / time to new product

Streamline

Commit on SLAs

Innovate new ways of doing things

Credit Risk minimize new NPE formation

Capital Risk prudent and disciplined RWA management

Protect

Liquidity penetrate non-lending relationships

Operational Risk management

54 | CIB PERFORMANCE & TRENDS04 Transaction Banking Suite

4.6 DIGITAL TRANSACTION BANKING

An integrated business model that will create a connected corporate banking experience and uninterrupted

transaction flow

Payments Trade Finance Treasury

All-in-one Smarter Maximize cash

financing performance

Simplify A better grip Safeguard Deep dive

bookkeeping on cash flow cash flow into data

Collections Cash Management Factoring Analytics

55 | CIB PERFORMANCE & TRENDS04 4.7 NEW STRATEGIC PARTNERSHIP

Collaboration for Solutions to Greek Business Rationale for the Strategic

Shipping Companies Partnership

In its effort to expand revenue capacity and better The opportunity relates with the effort to:

manage balance sheet, the Bank is currently increase fees and expand market share in a

exploring to enter into a strategic partnership with vital sector for the Greek economy

a major Asian Pacific financial conglomerate

possibility to increase access to capital and

The focus of the partnership will be on providing other services for the shipping sector

tailored and competitive funding solutions to

optionality with regards to expansion in other

Greek shipping companies business areas via the deepening of the

The agreement if conducted, would incorporate relationship with the said conglomerate

both a one-off fee paid to the Bank for its services The agreement allows Piraeus to leverage on its

and a recurring annual fee for ancillary services to partner’s balance sheet and lower cost of capital

be provided over the tenure of each facility allowing a more efficient and profitable use of its

experience and resources in the shipping sector

56 | CIB PERFORMANCE & TRENDS04 4.8 THE WAY FORWARD

Become the most profitable CIB franchise in Greece

Defend and grow market share at the sectors of focus

Grow revenues generate sustainable, sticky fee income

Our Ambition

Improve portfolio returns

Enhance customer experience by developing digital capabilities

Leverage our client relationships and balance sheet to lead key transaction and support the Greek economy

Positive Economic Value Added across all segments

Our Targets Cost-to-Income ratio: low 30s%

New loan generation: >10% yoy

Optimize capital allocation

57 | CIB PERFORMANCE & TRENDS05 NPE SERVICING AGREEMENT

05 5.1 PIRAEUS AND INTRUM JOIN FORCES

• Piraeus Bank and Intrum enter into a strategic partnership for the management of non-performing assets

• Establishment of the market-leading independent NPE servicer in Greece

• The servicer will manage Piraeus’ existing NPEs and REOs, as well as new inflows

• Two servicer companies, one for NPEs and one for REOs, comprising one operating platform

• The platform will also manage non-performing assets of third parties

• Piraeus’ and Intrum’s top management will join the new companies’ Board of Directors

• The NPE servicer company will be licensed and regulated by the Bank of Greece

• The transaction is subject to customary conditions, regulatory approvals and the consent of the HFSF

59 | NPE SERVICING AGREEMENT05 5.2 BENEFITS OF THE TRANSACTION

1 Facilitation of sizeable Independent servicer with the scale and capabilities to service large

inorganic actions portfolios, facilitating future securitizations and systemic solutions

2 Enhanced PPI savings (cost relief minus fixed AuM fees) of c.€50mn per annum in

operating efficiency 2020-2021; overall boost of effectiveness in the management of NPEs

3 Bank retains Participation in the enterprise value growth of the servicer companies;

upside potential Piraeus retains assets and proceeds on its balance sheet

4 Leverage with Intrum

Performance Enhancement of Piraeus’ NPE recovery prospects, facilitating the

expertise

Culture outperformance of NPE reduction targets

5 Re-focus on

core banking

Management team will re-focus on core banking activities, yielding

improved results for the Group

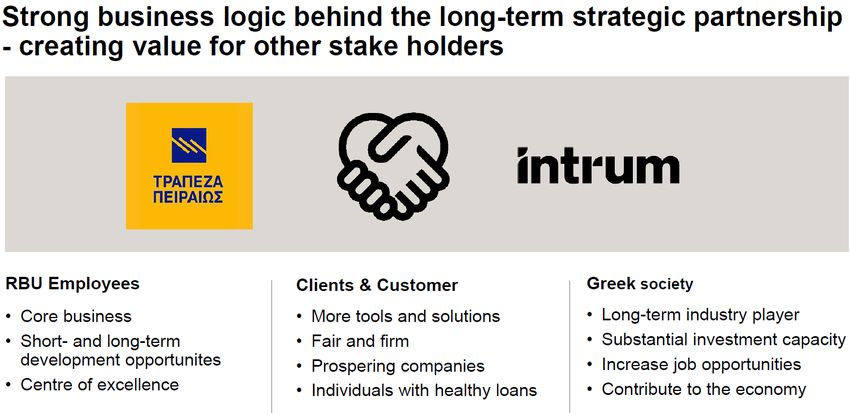

60 | NPE SERVICING AGREEMENT05 5.3 BUSINESS LOGIC AT A GLANCE

Strong business logic behind the long-term strategic partnership -

creating value for other stakeholders

RBU Employees Clients & Customers Greek Society

Core business More tools and solutions Long-term industry player

Short and long-term Fair and firm Substantial investment capacity

development opportunities Prospering companies Increase job opportunities

Centre of excellence Individuals with healthy loans Contribute to the economy

61 | NPE SERVICING AGREEMENT05 5.4 TRANSACTION FACTSHEET

Serviced Perimeter Existing non-performing loans plus forborne / early arrears loans and REOs, as well as any new inflows

€27bn loan exposures and €1bn REOs in the perimeter (est. Q4.2019 figures)

Contract Duration Initial term of 10 years

Shareholder Structure 80% of the new servicer company will be held by Intrum and 20% by Piraeus Bank

Valuation The agreement values the 100% of the platform at €410mn. Intrum has agreed to acquire 80% for a purchase price of €328mn

Timeline The two parties aim for transaction closing on 1 October 2019

Board of Directors Comprised of both parties’ executives

Management George Georgakopoulos will assume the role of CEO in the 2 servicer companies

Employees c.1,300 people will be employed in the new servicer companies

Structure The majority of the serviced NPE portfolio to be transferred to and held by a securitization SPV

62 | NPE SERVICING AGREEMENT05 5.5 PROGRESS AT A GLANCE

Step 1: Transfer of RBU Business to ServiceCo Step 2: Sale of ServiceCo, including a long-term SLA

Shares in

ServiceCo

Piraeus Bank Piraeus Bank Intrum

Recovery Consideration

Banking Shares 80%

Unit Long-term SLA

ServiceCo ServiceCo

20%

Note: diagrams do not explicitly show the creation and sale of the REO servicing company, which follows the same structure

63 | NPE SERVICING AGREEMENT05 Piraeus' Recovery Banking Unit

5.6 PIRAEUS’ RBU OVERVIEW

The most advanced NPE management unit in Greece

Formal establishment of the RBU in Q4.2013, ~1,300

based on internal workout and restructuring

FTEs

teams, as well as top talent from the core Bank

Servicing retail and commercial exposures across

a variety of specialized sub-segments

~€27bn

servicing perimeter

Significant investments in the operating platform,

processes, product suite and governance

RBU Core Activities

Active involvement and facilitation of previous

and ongoing NPE transactions by the RBU; the

best NPE reduction performance in 2018

Collections Restructuring Legal actions

64 | NPE SERVICING AGREEMENT05 5.7 INTRUM OVERVIEW

• Holistic service offering, covering the entire credit

management chain; c.80k clients

• Local presence in 24 European markets -

market leader in the majority of them; 160 partner countries

• Strong operational performance and collection results

• Significant transaction and partnership experience

Intrum Key Metrics - Q1 2019 LTM (SEKmn) (EURmn)

Revenues 14,079 1,357

EBIT Adjusted 4,877 470

Cash EBITDA 10,283 991

Employees >10,000 >10,000

65 | NPE SERVICING AGREEMENT05 End of

5.8 PREPARATIONS FRONTLOADED

End of

May September

SCOPE APPROACH

Pre-Signing Pre-Signing Post-Signing - Implementation Completion

▪ Piraeus and Intrum have ▪ Implementation Launch implementation of the transfer of ▪ New servicer

started preparations for steps for the business to ensure autonomous operational companies fully

the implementation transfer of the continuity of the servicer companies, by: up and running

phase of the transaction Piraeus RBU - Segregating IT systems

early in the process business defined - Separating premises

- Setting up the billing processes and

▪ Target is for the new

servicer companies to be ▪ Operational calculation tools

readiness and set- - Managing the transfer of resources

ready by 1 October 2019

up of 13 dedicated - Defining Compliance / GDPR obligations

▪ The new NPE servicer workstreams

company will be licensed Stress-test systems and processes of

by the Bank of Greece servicer companies

66 | NPE SERVICING AGREEMENT05 Steering Committee

5.9 EXECUTION

Weekly Jour Fixe Cost

PMO Team

PMO Meeting Monitoring

Intrum ownership

1 2 3 4 5 6 7 8 9 10 11 12

PB Credit & Core Ops set-up Securitization

Regulatory & Billing Engine, Compliance Communicati ServiceCo

Organization Delegated Processes and Technology HR (premises, facilities, and related

Incorporation branches) KPIs & GDPR on set-up

& Governance authorities Invoicing processes

Steering Committee Owners

Workstream Managers

▪ Corporate ▪ Regulatory ▪ Credit ▪ Organosis ▪ Organosis ▪ IT ▪ Branches ▪ IT ▪ IT ▪ IT ▪ Inv. Relations

Governance Affairs ▪ Organosis ▪ IT ▪ IT ▪ Organosis ▪ Finance & MIS ▪ Organosis ▪ Operations ▪ Organosis ▪ HR

▪ Organosis ▪ Legal ▪ IT ▪ Finance ▪ Legal ▪ Legal ▪ Finance ▪ Treasury ▪ Legal

Functions ▪ Finance & MIS ▪ Strategy ▪ Procurement ▪ IT Facilities ▪ Tax ▪ Operations

▪ RBU ▪ HR ▪ Accounting

involved

▪ HR ▪ Organosis ▪ Corporate

▪ Participations Servicing

▪ Finance Unit

▪ Compliance

67 | NPE SERVICING AGREEMENT05 5.10 FINANCIAL IMPACT

2019 Up to 2021 10-year period

Capital accretion of c.80bps Positive impact on PPI (cost relief NPV of the 10-year

will arise from the €0.4bn minus fixed AuM fees) of c.€115mn cumulative net income

valuation of the NPE cumulatively (Q4.19 to end-2021) impact c.€100mn, including

servicing platform upfront consideration

Success fee for the execution of the

Closing expected 1 October proceeds

existing NPE plan expected to be

2019; marginal operating booked in the CoR line This impact does not

P&L impact from Q4.2019 include any acceleration in

All-inclusive positive impact to capital the execution of Piraeus’

through to 2021 of c.55-60bps as per NPE reduction strategy

existing NPE plan

In a scenario of 10% over-

performance vs existing NPE plan,

net capital result through to 2021

increases to c.100bps

68 | NPE SERVICING AGREEMENT05 5.11 BASELINE FINANCIAL PROJECTIONS

The Illustrated Impact Takes into Account the Baseline Scenario of our NPE Plan Execution

2019-2021 PPI (€bn) 2019-2021 Net Income (€bn)

69 | NPE SERVICING AGREEMENTCLOSING REMARKS

AGENDA 2023: KEY PILLARS

a. Strategic Targets paving the path to increasing profitability

b. Satisfying Stakeholders remaining the top priority for the Bank

c. Sustainable Solutions producing sustainable returns

De-risking Growth Efficiency &

of Legacy Assets of Core Assets Simplification

Value Creation by the Leading Bank in Greece

71 | CLOSING REMARKS2023 ROADMAP

Restoration of Fundamentals in the Baseline Scenario

2018

Cost to income 54% low 40s

NPE 51% single-digit ratio

RoTΕ losses high single-digit return

~200bps above the

Regulatory Capital 14.0%

expected requirement

72 | CLOSING REMARKSROA DRIVERS

Pre-Tax RoA Improvement Driven by Cost Efficiency

Pre- tax RoA

+0.2%

+0.5%

+0.1%

Growth and Efficiency De-risking and

development of increase and cost of risk

the business simplification normalization

a: actual; f: forecast

73 | CLOSING REMARKSDisclaimer The accompanying presentation has been prepared by Piraeus Bank S.A. and its subsidiaries and affiliates (the “Bank” or “We”) solely for informational purposes. For the purposes of this disclaimer, the presentation that follows shall mean and include materials, including and together with any oral commentary or presentation and any question-and-answer session. By attending a meeting at which the presentation is made, or otherwise viewing or accessing the presentation, whether live or recorded, you will be deemed to have agreed to the following restrictions and acknowledged that you understand the legal and regulatory sanctions attached to the misuse, disclosure or improper circulation of the presentation or any information contained herein. This presentation does not constitute an offer to sell or a solicitation of an offer to buy or a recommendation to buy or invest in any form of security issued by the Bank or its subsidiaries or affiliates nor does it constitute an offer or commitment to lend, syndicate or arrange a financing, underwrite or purchase or act as an agent or advisor or in any other capacity with respect to any transaction, or to commit capital. This presentation is not intended to provide a basis for evaluations and does not constitute investment, legal, accounting, regulatory, taxation or other advice and does not take into account your objectives or legal, accounting, regulatory, taxation or financial situation or particular needs. No representation, warranty or undertaking is being made and no reliance may be placed for any purpose whatsoever on the information contained in this presentation in making any investment decision in relation to any form of security issued by the Bank or its subsidiaries or affiliates or for any other transaction. You are solely responsible for forming your own opinions and conclusions on such matters and for making your own independent assessment of the Bank. You are solely responsible for seeking independent professional advice in relation to the Bank and you should consult with your own advisers as to the legal, tax, business, financial and related aspects and/or consequences of any investment decision. No responsibility or liability is accepted by any person for any of the information or for any action taken by you or any of your officers, employees, agents or associates on the basis of such information. This presentation does not purport to be comprehensive and no representation, warranty or undertaking is made hereby or is to be implied by any person as to the completeness, accuracy or fairness of the information contained in this presentation. The Bank, its financial and other advisors, and their respective directors, officers, employees, agents, and representatives expressly disclaim any and all liability which may arise from this presentation and any errors contained herein and/or omissions therefrom or from any use of this presentation or its contents or otherwise in connection therewith. The Bank, its financial and other advisors, and their respective directors, officers, employees, agents, and representatives accept no liability for any loss howsoever arising, directly or indirectly, from any use of the information in this presentation or in connection therewith. Certain information contained in this presentation is based on estimates or expectations of the Bank, and there can be no assurance that these estimates or expectations are or will prove to be accurate. This presentation speaks only as of the date hereof and neither the Bank nor any other person gives any undertaking, or is under any obligation, to update any of the information contained in this presentation, including forward-looking statements, for events or circumstances that occur subsequent to the date of this presentation. Each recipient acknowledges that neither it nor the Bank intends that the Bank act or be responsible as a fiduciary to such attendee or recipient, its management, stockholders, creditors or any other person. By accepting and providing this document, each attendee or recipient and the Bank, respectively, expressly disclaims any fiduciary relationship and agrees that each recipient is responsible for making its own independent judgment with respect to the Bank and any other matters regarding this document. The Bank has included certain non-IFRS financial measures in this presentation. These measurements may not be comparable to those of other companies. Reference to these non-IFRS financial measures should be considered in addition to IFRS financial measures, but should not be considered a substitute for results that are presented in accordance with IFRS. Certain statements contained in this presentation that are not statements of historical fact, including, without limitation, any statements preceded by, followed by or including the words “targets,” “believes,” “expects,” “aims,” “intends,” “may,” “anticipates,” “would,” “could” or similar expressions or the negative thereof, constitute forward-looking statements, notwithstanding that such statements are not specifically identified. Examples of forward-looking statements include, but are not limited to, statements which are not statements of historical fact and may include, among other things, statements relating to the Bank’s strategies, plans, objectives, initiatives and targets, its businesses, outlook, political, economic or other conditions in Greece or elsewhere, the Bank’s financial condition, results of operations, liquidity, capital resources and capital expenditures and development of markets and anticipated cost savings and synergies, as well as the intention and beliefs of the Bank and/or its management or directors concerning the foregoing. Forward-looking statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions which are difficult to predict and outside of the control of the Bank. Therefore, actual outcomes and results may differ materially from what is expressed in such forward-looking statements. We have based these assumptions on information currently available to us, and if any one or more of these assumptions turn out to be incorrect, actual market results may differ significantly. While we do not know what impact any such differences may have on our business, if there are such differences, our future results of operations and financial condition, could be materially adversely affected. You should not place undue reliance on these forward-looking statements. Forward-looking statements speak only as of the date on which such statements are made. The Bank expressly disclaims any obligation or undertaking to disseminate any updates or revisions to any forward-looking statement to reflect events or circumstances after the date on which such statement is made, or to reflect the occurrence of unanticipated events.

PIRAEUS BANK GROUP HEADQUARTERS

4, Amerikis Str., 105 64 Athens, Greece

T. +30 210 333 5026

www.piraeusbankgroup.comYou can also read