4finance Investor Presentation - Autumn 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

4finance Investor Presentation Autumn 2019

Disclaimer

While all reasonable care has been taken to ensure that the facts stated herein are accurate and that the forecasts, opinions and expectations contained herein, are fair and reasonable, no representation

or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information, or opinions contained herein. Neither 4finance

nor any of 4finance`s advisors or representatives shall have any responsibility or liability whatsoever (for negligence or otherwise) for any loss howsoever arising from any use of this document or its

contents or otherwise arising in connection with this document. The information set out herein may be subject to updating, completion, revision, verification and amendment and such information may

change materially.

This presentation is based on the economic, regulatory, market and other conditions as in effect on the date hereof. It should be understood that subsequent developments may affect the information

contained in this document, which neither 4finance nor its advisors are under an obligation to update, revise or affirm.

The distribution of this presentation in certain jurisdictions may be restricted by law. Persons into whose possession this presentation comes are required to inform themselves about and to observe any

such restrictions.

The following information contains, or may be deemed to contain, “forward-looking statements”. These statements relate to future events or our future financial performance, including, but not limited to,

strategic plans, potential growth, planned operational changes, expected capital expenditures, future cash sources and requirements, liquidity and cost savings that involve known and unknown risks,

uncertainties and other factors that may cause 4finance’s or its businesses’ actual results, levels of activity, performance or achievements to be materially different from those expressed or implied by any

forward-looking statements. In some cases, such forward-looking statements can be identified by terminology such as “may,” “will,” “could,” “would,” “should,” “expect,” “plan,” “anticipate,” “intend,”

“believe,” “estimate,” “predict,” “potential,” or “continue,” or the negative of those terms or other comparable terminology. By their nature, forward-looking statements involve risks and uncertainties because

they relate to events and depend on circumstances that may or may not occur in the future. Future results may vary from the results expressed in, or implied by, the following forward-looking statements,

possibly to a material degree. All forward-looking statements made in this presentation are based on information presently available to management and 4finance assumes no obligation to update any

forward-looking statements.

2Presenting team

Oyvind Oanes Paul Goldfinch James Etherington

Chief Executive Officer Chief Financial Officer Head of Investor Relations

Oyvind combines experience of leading Prior to joining 4finance Paul was CFO James has over 15 years of experience

Fintech consumer banking platform, of the Corporate and Investment Bank in capital markets advice within

Numbrs, with nearly two decades of retail Division of Sberbank, Russia’s largest investment banking (Morgan Stanley,

banking across Europe, including building a Bank. He has also held a number of RBS and Renaissance Capital) and then

consumer finance business for GE Capital senior roles at UBS, including EMEA investor relations (Head of IR with

in Russia, leading the turnaround of Regional Head of Accounting and Ecobank, the largest sub-Saharan

Austria’s Bawag PSK’s retail business and Controlling, and COO/CEO of UBS Bank African bank). James has been Head of

running Raiffeisen’s multi-country online Russia. Paul graduated from the IR for 4finance for the last 4 years, and

bank ZUNO. Oyvind has a Business University of Auckland in New Zealand has been involved in EUR, SEK and

Economics degree from the BI Norwegian and commenced his career with KPMG USD bond issues. James graduated

Business School, an MA in Management and Citibank before moving to Europe. from Cambridge University with an MSc

from the University of Stavanger and an in Natural Sciences (Physics).

MSc in Marketing from the University of the

West of Scotland.

3Topics

• Business overview

• Strategy: evolving and broadening the business model

• Regulatory overview

• Financial performance

• Funding strategy and summary

4Current business snapshot

Founded in 2008, 4finance today is one of the largest digital consumer lending groups in Europe

Founded / HQ in Latvia with Active

Operations in 14 Countries

€7+ BN ~740,000 5

Online Loans issued Active customers(1) Main lending products

since establishment in 2008

~84% >70% ~2,750 EU-Licensed Banking Subsidiary

Enabling Deposit-Taking and Passporting

Of customers apply Full-time staff, of which

Returning customer business(2)

via their mobile phones ~1,350 in TBI Bank

€213 MM €27 MM 52%

H1 2019 Interest income H1 2019 Pre-tax profit H1 2019 Cost to income ratio

Access to Debt Capital Markets

Credit Ratings (B2/B+) (3)

€551 MM €176 MM €459 MM

H1 2019 Net receivables H1 2019 Equity H1 2019 Public traded debt(3)

Notes:

(1) Active customers represents online lending customers with open loans that are up to 30 days past due. Includes 0.4 MM active TBI Bank customers.

(2) Issuance volumes to online customers who have returned (i.e. taken out and repaid at least one loan).

(3) Includes principal and accrued interest, net of buybacks; the issuer of the bonds, 4finance S.A. is an indirect subsidiary of 4finance Holding S.A.

5Multi-product offering

4finance markets a variety of convenient financial solutions to serve its customers in a continuously evolving landscape

Lending Products Deposit Products

Single Instalment Line of Credit / Point of SME Loans

Payment Loan Loan Credit Card Sale (Bank Only) Bank Non-Bank

Typical Amount €200 to €400 €500 to €1,500 €400 to €600 €300 to €800 ~€30k ABL(5) (Bulgaria) €100,000 state guarantee ~€5,000 limit

€1,000 to €3,000 (‘near- ~€150k ABL(5) (Romania) limit

prime’) ~€15k cash loans

Payment Type Single payment including Repayment in fixed Minimum monthly Repayment in fixed Credit line loans (with bullet At maturity Annual or at maturity

the principal repayment monthly instalments with repayment and flexible monthly instalments payment) - repayment in

and loan fee amortising principal additional repayment fixed monthly instalments

Term Up to 30 to 65 days Typically 3 to 48 months Open-ended revolving Up to 1 to 5 years 12 months to 48 months Current accounts and term Current and term deposits

depending on the market depending on the market credit line depending on the market (up to 60 months) deposits (up to 3 years) (up to 2 years)

Pricing Monthly interest rates: Annual interest rates: Monthly interest rates: Annual interest rates: Annual interest rates: Annual interest rate: 0.5% Annual interest rate: 5.5%

5% to 35% 20% to 100% ~3% (credit cards) 30% to 50%(4) ~11% to ~31%(6) to 4.5% to 8.1%

3% to 15% (online LoC) Deposits in EUR, USD,

10% to 20% (MTP) BGN and RON

Markets 9 markets(1) 11 markets(2) 7 markets(3) Bulgaria, Romania Bulgaria, Romania Bulgaria, Romania and Sweden

passported activity in

Germany

‘Near-Prime’ Instalment Loans in Bulgaria (TBI),

Romania (TBI), Lithuania, Spain and Sweden

Notes:

(1) Single Payment Loan: Argentina, Bulgaria, Czech Republic, Finland, Lithuania, Mexico, Poland, Slovakia, Spain.

(2) Instalment Loan: Armenia, Czech Republic, Denmark, Finland, Latvia, Poland; ‘Near-Prime’ Instalment Loan: Bulgaria (TBI), Lithuania, Romania (TBI), Spain, Sweden.

(3) Line of Credit / Credit Card: Bulgaria (TBI), Finland, Latvia, Romania (TBI); Minimum-to-Pay (MTP): Armenia, Denmark, Latvia, Sweden.

(4) Plus insurance income for TBI, the annual interest rates are rates which TBI applies over the requested loan amount and over the insurance premium (insurance premium is capitalized and becomes part of the loan principal).

(5) ABL: asset backed loan.

(6) Range based upon annual interest rates of 11% for ABL (Bulgaria) loans and 30.6% for cash online loans in Romania. 6Overview of online lending process

Integrated and largely automated IT platform covering all steps of the customer life cycle with access to key predictive data

Marketing Application Underwriting

• A diversified multi-channel and data-driven • Prospective customer applies online or • Within a few seconds, proprietary systems

marketing and acquisition strategy through a smartphone application pull data, determine creditworthiness and

• Sophisticated in-house marketing and digital hub • Simple, convenient, transparent pricing and accept or reject

with best-in-class technology application process (‘UX’ optimized)

• Low customer acquisition costs achieved through

discipline

Collection Servicing Funding

• Well-staffed, local, in-house debt collection • ~500 in-house specialists provide support in • Customer executes legally binding loan

team local language across all markets of operation agreement online and the funds are advanced

• Strong recovery rates • Key performance indicators constantly within a few minutes

• Full regulatory compliance with no controversial monitored to improve service and enhance • Entire disbursement process built around

debt collection practices retention customer experience to ensure satisfaction

• External agencies used for 90+ DPD collections

7Robust credit scoring systems

4finance maintains a large proprietary database with valuable data enabling the development of an advanced scorecard and

adjudication system for approvals

Main Loan Applications (H1 2019)

Proprietary Database

Online SPL(1) Online IL TBI Bank Consumer

20+ MM loans issued

45+ MM applications reviewed 1.67 MM 0.23 MM 0.41 MM

Applications Applications Applications

59% 41% 26% 74% 48% 52%

Highly Developed Scorecards

• 51 credit risk scorecards, including 29 application scorecards

0.98 MM 0.68 MM 0.06 MM 0.17 MM 0.20 MM 0.21 MM

• 10 debt collection and 3 fraud scorecards Returning New Returning New Returning New

Customers Customers Customers Customers Customers Customers

• Automated scorecard dashboards updated on a daily basis

External Data Sources 78% 19% 53% 20% 63% 32%

Acceptance Acceptance Acceptance Acceptance Acceptance Acceptance

Rate Rate Rate Rate Rate Rate

35+ credit bureaus and multiple other data sources including

social security agencies

€273 MM(2) €65 MM(2) €123 MM

84% of loans are issued to returning customers (3)

Notes:

(1) Reflects the reclassification of SPL products that have recently been reconfigured to LoC products in line with the evolving local markets

(2) Total value of online issued loans in H1 2019 (main loans) 8

(3) Issuance volumes to online customers who have returned (i.e. taken out and repaid at least one prior loan)Strong collection capability

Key highlights High Quality International Partners

• Well-staffed local in-house debt collection team in all

markets

• Collection of payments delayed up to 90 days past

maturity mainly handled in-house

• Best-in-class and highly automated collection process

(automated dialers)

• Cooperation with external debt collection agencies in all Collection Process Overview

markets to increase efficiency through fair competition

• Pro-active management of NPL portfolio with increased

use of ad-hoc and forward flow debt sales as standard Early Collection Late Collection Recovery

collection tools In-House Mainly In-House Debt Collection Agencies

• Strong recovery rates (1)

• Full regulatory compliance, no controversial debt 1 to 30 31 to 90 90+

collection practices Days Days Days

• Customer satisfaction and collections efficiency is

paramount • Highly automated with customer • Partially automated phase • A feasible loan repayment

reminders processed by IT systems restructuring plan is made available

• Further phone calls are made (similar

(typically not exceeding 12 months)

• Phone calls to encourage full to early collection phase)

were appropriate

90%+ 80%+

Average recovery rate of the full Collected by in-house team

repayment, offering the customer a

repayment schedule or a loan

extension

• After a grace period of 3-5 days, delay

• Reminder letters sent by mail and

email

• Early transfers to external debt

collection agencies are performed if

• Increasing use of ad-hoc and forward

flow debt sales as standard collections

tools

principal within two years after within 30 days interest is calculated on a daily basis • Good attitude toward these customers

more efficient

maturity and varies depending on local interest

rate cap restrictions

Note:

(1) Due to (i) loan ticket size being small and (ii) significant potential negative impact on the 9

customer’s credit score relative to the small amount of debtStrategy: evolving and broadening the business model

10Evolving and broadening our business model

Segments

Prime

Young

Aspirational A multi-segment, multi-product,

consumer credit specialist

1 Optimise

Near-Prime

2 2 Diversify & Grow

Sub-Prime 1

Products

Illustrative

SPL IL LOC CC Insurance Housing

POS Auto

11Evolution of product mix

Net receivables by product (1) Interest income by product (1)

€323m €551m €183m €213m

100% 100%

10% 6%

SME (Bank) 19%

29%

15%

4% 31%

75% 75%

3% Point of Sale

12%

50% 48% Instalment loans

50%

77%

68% Line of Credit / Cards

25% 6% 25% 50%

Single Payment Loans

22%

0% 0%

30 Jun 2016 * 30 Jun 2019 H1 2016 H1 2019

Online Bank and online,

sub-prime near-prime

only and sub-prime

Note:

* Date chosen to reflect the composition of loan portfolio (1) Reflects reclassification of "Vivus" brand products in Sweden (from January 2016), Denmark (from January 2017)

immediately prior to purchase of TBI Bank

and Armenia (from launch in July 2017) to Lines of Credit

12Recap of strategic focus areas in 2019

1 Optimise 2 Diversify & Grow

• Relentless execution in European online markets in • Creation of new “4finance Next” unit to drive near-

shorter-term products prime lending and partnership opportunities

• Further cost optimisation, efficiency gains and • IT strategy revised to give more efficient support for

automation core markets, and local flexibility for smaller ones

• Grow instalment loan and line of credit business in • Launch pilots of funding projects including with TBI

selected markets Bank and our external securitisation platform

• Review growth opportunities in smaller markets (eg • TBI Bank growth and execution of next generation

partnerships in Mexico) digital lending strategy

• Adapting products to regulatory changes in Latvia

(Jan and Jul 2019) and Finland (Sep 2019)

13Near prime market tests: Lithuania, Spain & Sweden

Lithuania (2016) Spain (2017) Sweden (2018)

“Evolve existing product “Partner-led distribution” “New product & brand on new

and brand” 4finance platform”

30%-60% APR 24%-40% APR 20%-40% APR

• Strong brand profile of existing • Partnered with Fintonic, personal • First product designed on new IT

Instalment loan product, with ‘trust’ finance manager App with 450k platform

levels close to bank brands active customers

• Clear niche in €2,000 - €5,000

• Evolved product in mid-2016 post • 30% of Fintonic users in near- ticket size with tenor up to 4 years

regulation prime/sub-prime segments, allowing

highly targeted campaigns • Build on existing strengths:

• €500 → €1,000 avg. ticket size

• Response rate and acceptance rate • Modern, innovative brand

• 2 year → 4 year tenor both >75% • Simple application

• ~80% → ~45% avg. pricing • €3,000 avg. ticket size • Fast online decision and

• €16m net portfolio at 30 Jun 2019 • 22 months avg. tenor disbursement

• Now issuing c.€2m per month • Compliant with new regulations

14TBI Bank: strong performance & benefits for broader group

Highlights of H1 2019 Interest Income Focus areas in 2019

€m

• Strong financial contribution and well capitalised +7% 39

“Next generation digital lender” strategy

36

• Interest income up 7% year-on-year to €39m

• Net profit after tax of €10m • Expand e-Commerce online POS offering

• 18.7% RoAE on well capitalised equity base • Launch Mobile App

• 20.7% capital adequacy ratio (all tier 1) at end June

• Gradually optimise/modernise branch network

• Delivering growth in loan portfolio at low funding cost and improve cost efficiency

• Loan portfolio evenly mixed between Bulgaria and Romania H1 2018 H1 2019 • Further lending growth

• 3% YTD growth in net receivables

• 30% average yield on net portfolio Net receivables by product Broader group initiatives

€m

• Average all-in deposit cost of funds of 1.6% in H1 2019

+3% 271

263 • Funding online lending via TBI balance sheet

• Several strategic initiatives implemented

SME SME • Centre of excellence for POS across the

• Current accounts provided with loans in Bulgaria, enabling Cards Cards

‘continuous scoring’ for additional lending group

• Developed e-Commerce product, a market first

POS POS • Optimise Vivus business in Bulgaria

• Diversified SME business away from asset backed lending • Continue to develop payments capabilities

• Passported deposit license to Germany to secure access to Cash Cash • Dividend payments commenced in March

Raisin platform loans loans

2019

• Purchased first c. €1m portfolio of Polish instalment loans in

September 2019 2018 30 Jun 2019

15Regulatory overview

16Sustainability through good governance and responsible lending

Operating as a mainstream consumer finance Developing meaningful and constructive

business regulatory relationships

• “Bank-like” policies and procedures with strong • Ensuring we understand the regulatory arc

compliance function

• Helping regulators and legislators gain a solid

• Continued investment in AML, GDPR and other strategic understanding of our business

compliance priorities

• Ensuring we have a seat at the table

• Robust corporate governance with strong Supervisory

• Contributing to EU Consumer Credit Directive

Board

consultation process

• Increasingly regulated by main financial supervisory

authorities

Responsible lending: putting customers first

• Diversification of portfolio and consequent reduction of

reliance on single payment loans • Offering simple, transparent and convenient products

• Clear corporate values and code of conduct • Continuous improvements in credit underwriting

• Listed bond issues with quarterly financial reporting • Ensuring products are used appropriately

• Working to ensure customers have safe landings when

they signal difficulties

17Regulatory update, ongoing changes

Engagement & business

Current Proposed Status

adaptation

• 25% APR cap • N/a • New legislation in force • Products adapted, with

Latvia • Marketing restrictions as of July 2019 voluntary fast disbursement

fee

• Positive initial customer

response

• 20% interest cap • N/a • New legislation in force • Products adapted, with ‘mini-

Finland • Limits on fees and as of September 2019 instalment loan’ on new

extensions platform & voluntary fast

disbursement fee

• Non-interest fees 25% • Non-interest fees of 10% • Draft proposed end June • Contributed to EC review

Poland fixed and 30% annual fixed and 10% annual 2019 process

• Consumer protection • Polish FSA regulator • Currently in EC referral • Ongoing consultation

regulator • Six month until end September

implementation period • Polish elections mid-

October

• No interest or fee caps • Early stage political • Licensing applications to • Active contribution to political

Denmark • Licensing regime, led by discussion on additional be submitted by end consultation process ongoing

Danish FSA regulation 2019

• No draft regulation or

timetable currently

Continued focus on responsible lending, including EU consumer credit directive consultations

18Financial performance

19Summary of six month 2019 results

Interest Income Adjusted EBITDA

• Solid performance in second quarter. Stable quarterly revenue, Adjusted €m €m

EBITDA up 13% QoQ, with highest quarterly PBT for two years

Quarter-on-quarter

• H1’19 interest income down 13%, Adjusted EBITDA of €62.5m, down 16% +0.4% 106.9 +13%

106.5 33.1

year-on-year 29.4

• Reduction in interest income largely attributable to products and/or markets that

were rationalised during 2018

• Interest coverage ratio for H1’19 of 2.1x (full covenant calculation ratio of 2.7x)

• Post-provision operating profit of €31.0m, vs. €40.8m in H1’18 (impacted by

significant post IFRS 9 debt sales income in H1’18)

• Interest income highlights by market and product Q1 2019 Q2 2019 Q1 2019 Q2 2019

• Solid performance in key online markets (Denmark, Poland, Spain) and TBI Bank

• Stable contribution of instalment loan interest income quarter-on-quarter Year-on-year

• TBI Bank increasing its own online operations and transfer of vivus.bg operations 245.4 -13% 213.4 74.2 -16%

62.5

• Continued progress on cost reduction

• Year-on-year reduction in costs of 17%

• Strong operating cashflow and robust cash position

• Operating cashflow before movements in portfolio & deposits of €110m

• Full repayment of $68m August 2019 bond maturity from cash on hand

H1 2018 H1 2019 H1 2018 H1 2019

• Overall stable risk performance

• Overall gross NPL ratio of 17.9% (from 19.4% in December 2018)

• Net impairment/interest income at 28.4% for H1’19 (vs 25.8% in H1’18)

See appendix for definitions of key metrics and ratios

20Interest income – remains well diversified

Interest income by country H1 2019 interest income: €213m

245.4 -13%

€240m

213.4 Other * Latin America 3%

Mexico

€200m Argentina Other Europe 8%

Armenia

Slovakia

€160m Czech Republic BG/RO 20%

Romania

Bulgaria

Spain 19%

€120m Spain

Poland

Denmark Poland 27%

€80m Sweden

Finland

Lithuania Nordics 15%

Latvia

€40m

Baltics 8%

€0m

H1 2018 H1 2019

* Other represents countries exited during 2018 (Dominican Republic and Georgia) 21Operating cost drivers

Total operating costs (1)

• Operating costs down 17% year-on-year €m

• H1’19 cost/income ratio at 52.2% compared to 53.6% in

58% 58% 58%

H1’18 70.0 60%

54%

• 2017 costs in bar graph do not include capex that would 53% 53% 52% 52% 52%

have been expensed under more conservative approach 60.0 5.4

3.7 49% 50%

3.3

from 2018 3.1 3.4

10.8 1.5

3.7 10.1

• Some cost reduction effect from IFRS 16, with €2.4m of 50.0 9.8 1.6

8.0 9.9

costs in H1’19 effectively moved to D&A and interest 11.2 40%

10.8 10.7 11.7

10.7

expense lines

40.0

• Q2’19 costs include annual TBI Bank state deposit

guarantee fund payment of €1.0m 30%

30.0

• Cost efficiency projects ongoing with focus on cost/income ratio

47.8 47.2 45.9 20%

• Friendly Finance integration fully complete 44.5 43.6

41.0

20.0 39.7 38.7 39.2 38.6

• Continued headcount reduction of 14% year-on-year

• Lower above-the-line marketing spend due to efficiency 10.0

10%

savings from econometric modelling (seasonal increase

in Q4’18 as expected)

0.0 0%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

Notes: 2018(3) 2019

(1) As of Q1 2019 costs are no longer shown separately for Friendly Finance as it is fully integrated into the

2017(2)

Group’s online operations

4finance TBI Friendly Finance Quarterly cost/income ratio, %

(2) 2017 quarterly costs reflect as-reported quarterly numbers. Totals do not match with 2017 audited

financials due to capex de-recognition as part of year end one-off adjustments to intangible assets

(3) Q4 2018 costs have been adjusted to reflect audited figures

22

See appendix for definitions of key metrics and ratiosFinancial highlights – strong credit metrics

Interest income Adjusted EBITDA Equity / assets ratio

€m €m 149

%

475 137

448 135 40%

393 119

318

24%

245 74

213 63 18% 17%

14% 16%

2015 2016 2017 2018 H1 2018 H1 2019 2015 2016 2017 2018 H1 2018 H1 2019 2015 2016 2017 1 Jan 2018* 2018 30 Jun 2019

* Post IFRS 9

Profit before tax Adjusted interest coverage ratio (1) Equity / net receivables

€m Times %

56%

81 4.1x

46%

74 3.6x

53 32% 32%

2.4x 2.4x 29%

2.2x 2.1x 26%

27

24 20%

11 min.

2015 2016 2017 2018 H1 2018 H1 2019 2015 2016 2017 2018 H1 2018 H1 2019 2015 2016 2017 1 Jan 2018* 2018 30 Jun 2019

* Post IFRS 9

Note (1): The full covenant calculation of interest coverage ratio is based on proforma last twelve month figures, and is currently 2.7x

See appendix for definitions of key metrics and ratios 23Diversified loan portfolio 750.0

Net receivables (1)

600.0 €m 591

553 551

• Online loan issuance volume down 19% YoY to €523m in H1’19 42 529

49

492 64 42 55

• Overall net receivables totals €551m 450.0

47 63 83 81

58

• Relatively stable during H1 2019, 1% increase during Q2 308

242

300.0 159 215

• 90% consumer loans 241 97

255 263

• 51% online loans / 49% banking 67 18 45

37

150.0 34 32

211 211

Net receivables, 30 June 2019 174 199 171

131 120

0.0

2014 2015 2016 2017 1 Jan 2018* 2018 30 Jun 2019

TBI Bank: 49% Online: 51%

(funded @ c.1.5%) SME (TBI) Baltics (funded @ c.12%) Single Payment loans Line of Credit / Cards Instalment loans Point of Sale SME (Bank)

10% 10%

Nordics * Introduction of IFRS 9 as of 1-Jan-2018 reduced net receivables by €62 million to €529 million

7%

Romania (TBI) Online loans issued (1)

16%

€m

1,277

1,157 1,209

1,064 136

Poland 52 152

112 163

22% 138 197

805

86 643 -19%

75 523

Bulgaria (TBI) 992 978 108 66

23% 926 861

Spain 719 91

6% 459 366

2014 2015 2016 2017 2018 H1 2018 H1 2019

BG (online)

0.5% CZ/SK, 2% Single Payment loans Instalment loans Line of Credit, Point of Sale

LatAm 0.9% GE/AM Note:

2% (1) Reflects reclassification of "Vivus" brand products in Sweden (from January 2016), Denmark (from January 2017) and

Armenia (from launch in July 2017) to Lines of Credit

24

See appendix for definitions of key metrics and ratiosAnalysis of net impairments and cost of risk

Net impairment charges by quarter (1)

• H1 2019 net impairment charges down 4% year-on-year

€m

60.0 36.4 40.0

• Gross impairment charges significantly reduced from H1’18

30.5 32.4 • Continued focus on earlier collections and forward flow

55.0 29.1 28.1

26.9 30.0

50.0 agreements (also reducing debt collection costs)

45.0 20.0

• Stronger debt sales activity in Q2, particularly ILs (Poland,

40.0 Net impairment Sweden), LOC (Denmark) and TBI Bank (Romania)

35.0 10.0 losses

30.0

0.0

Gross • Overall cost of risk relatively stable

impairments

25.0 48.6 46.4 • Overall cost of risk 17.4% (H1’19, including TBI Bank) vs

42.6 41.3 Over provisioning

20.0

35.9 37.3

-10.0

on debt sales (net 18.2% (H1’18)

15.0

-20.0

gain/loss)

• Online cost of risk 27.2% (H1’19) vs 22.7% (H1’18)

10.0

Recoveries from • Net impairment / interest income 28.4% (H1’19) vs 25.8%

5.0 -30.0 written off loans (H1’18)

0.0 0.1

(3.6) (5.7)

(6.7) (7.8) (7.7) -40.0

(5.0)

(10.0) (5.5)

(14.3)

(4.2) (4.5)

(3.4) • Focus on continuous improvement in credit underwriting and

-50.0

(15.0)

collection

(5.2)

(20.0) -60.0 • Integration of additional data sources

Q1 Q2 Q3 Q4 Q1 Q2

2018 2019 • Faster iterations of scorecards with regular recalibration

20.8% 15.1% 17.4% 16.6% 18.4% 16.2% Overall cost of risk

Note: (1) Q4 2018 figures have been adjusted to reflect audited figures

See appendix for definitions of key metrics and ratios 25Asset quality and provisioning

• Gross NPL ratios at record lows, with coverage ratios well over 100%

• Online gross NPL ratio 19.3% as of June 2019, an improvement from 22.0% as of December 2018

• Overall gross NPL ratio 17.9% as of June 2019 from 19.4% as of December 2018

• Additional portfolio disclosure provided by loan principal and accrued interest in results report and appendix

• Increased debt sales activity in Q2’19, with over €35m of 91+ dpd receivables sold, including Poland, Denmark and Sweden

30 June 2019 31 December 2018

Gross Impairment Net % of Gross Gross Impairment Net % of Gross

amount allowance amount Amount amount allowance amount Amount

€m, except percentages

Online receivables

Performing (1) 310.4 (48.9) 261.5 80.7% 316.2 (49.8) 266.4 78.0%

Non-performing (2) 74.1 (54.3) 19.8 19.3% 89.3 (64.1) 25.2 22.0%

Online total 384.5 (103.2) 281.3 100.0% 405.4 (113.9) 291.6 100.0%

TBI Bank receivables

Performing (1) 258.7 (11.6) 247.1 83.8% 252.3 (13.0) 239.3 84.1%

Non-performing (2) 49.8 (26.9) 22.9 16.2% 47.6 (25.3) 22.3 15.9%

TBI Bank total 308.5 (38.5) 270.0 100.0% 299.9 (38.3) 261.6 100.0%

Overall group receivables

Performing (1) 569.1 (60.4) 508.7 82.1% 568.5 (62.7) 505.7 80.6%

Non-performing (2) 124.0 (81.3) 42.7 17.9% 136.9 (89.4) 47.4 19.4%

Overall total 693.0 (141.7) 551.3 100.0% 705.3 (152.2) 553.2 100.0%

Notes:

(1) Performing receivables 0-90 DPD

(2) Non-performing receivables 91+ DPD (and, for TBI Bank, shown on a customer level basis)

26Funding strategy and summary

27Funding strategy

Debt maturity schedule, 30 June 2019 (1)

Strategy to diversify sources of funding and reduce overall €m

funding cost over time

244

• Bond markets remain strategically important source of funding Repaid in

Aug 2019

• Retain flexibility to buy back bonds with spare liquidity given attractive

147

market yield

• Early stage preparation for refinancing of EUR 2021 bonds, with sizing &

60

approach dependent on progress with other funding sources and

business development over next 12-18 months 0 0

2019 2020 2021 2022 2023+

• Accessing TBI Bank balance sheet to fund online loans

• Bulgarian vivus.bg online business moved to TBI Bank (c.€5m funding

benefit) Overview of funding structure, 30 June 2019 (2)

• Portfolio sales of Polish instalment loans expected to start in early Q4

• Reviewing approach in other markets, focusing on near-prime TBI deposits from 2019 Notes Repaid in

banks 8.3% Aug 2019

3.2%

• Developing secured funding alternatives

• ‘Internal pilot’ of Luxembourg securitisation launched, with Danish LOC

loans sold to SPV in June TBI customer 2021 Notes

deposits 19.4%

• Reviewing approach in other markets, including partnering with local 35.7%

banks

€755m

• Strong and improving capital position

• Improving tangible equity ratios since end of 2017

• €5m dividend paid in August 2019 4finance customer 2022 Notes

deposits 31.4%

1.9%

Notes:

(1) Represents the principal value of public bonds outstanding that comes due in each respective period, net of buybacks

(2) The chart reflects the principal and accrued interest amounts of each of the instruments, net of buybacks

28Summary

• The opportunity for 4finance is significant, with a huge addressable market in Europe and beyond

• Uniquely positioned given existing scale and experience

• Solid results demonstrate continued resilience of larger online markets and TBI Bank

• €7bn online loan issuance milestone surpassed in June

• Stable quarterly revenue, Adjusted EBITDA up 13% QoQ, with highest quarterly PBT for two years

• Continued progress on cost reduction, with operating costs down 17% year-on-year

• Asset quality stable overall and cost of risk in line with expectations

• Strategic initiatives in place to take advantage of medium term opportunities

• Increased focus on near-prime and partnership opportunities in selected markets

• Supported by clear funding strategy to diversify sources of funds and lower funding costs

• Evolving and broadening the business model, with clear focus areas for 2019 and beyond

• ‘Optimise’ and ‘Diversify & Grow’

• Maintain appropriate balance to ensure continued strong financial performance

4finance: building a multi-segment, multi-product, consumer credit specialist

29Thank you and Questions

30Appendix – corporate governance and management

31Corporate Governance Framework

4finance Group S.A.

Supervisory Board

(William Aaron Horwitz, David Geovanis,

Evgeny Sytnik)

Nomination and Remuneration Audit Committee

Committee Asset and Liability Committee (Edgars Dupats, Alexander

(William Aaron Horwitz, David (William Aaron Horwitz, Evgeny Sytnik) Alexandrov, Konstantin Ter-

Geovanis) Martirosyan, Evgeny Sytnik)

4finance Group S.A.

Management Board Internal

(Oyvind Oanes, Paul Goldfinch, Audit

Fabrice Hablot, Daniela Roca)

Remuneration Committee Executive Committee Disclosure Committee

(Oyvind Oanes, Paul Goldfinch, Edgars Dupats, (Oyvind Oanes, Paul Goldfinch, Olivier A Frühwirth, Martin (Oyvind Oanes, James Etherington, Paul Goldfinch)

Daiga Ērgle) Muransky, Daiga Ērgle, Sergio Crespo Martin-Albo, Olga

Pavlikova)

32Summary corporate structure

4finance Group S.A. Issuer of EUR and

(Luxembourg) USD bonds

100%

4finance Holding S.A. Guarantors of

(Luxembourg) 4finance S.A. issued

bonds

100% 100% 100%

TBIF Financial Credit Service Non-

UAB AS 4finance guarantor

Services B.V. (The

(Lithuania) (Latvia) subsidiaries

Netherlands)

100% 100%

99%

4finance AB (Sweden)

TBI Bank EAD Non-guarantor 4finance S.A.

(Bulgaria) 100%

subsidiaries (Luxembourg) 4finance Oy (Finland)

100%

4finance ApS (Denmark)

100% 5.31%

4finance EOOD BRAbank ASA 4finance Spain Financial 100%

Other subsidiaries Services S.A.U. (Spain)

(Bulgaria) (Norway)

Microfinance

100%

Organization 4finance

LLC (Georgia)

Vivus Finance Sp. z o.o. 100%

(Poland)

4finance UAB 100%

(Lithuania)

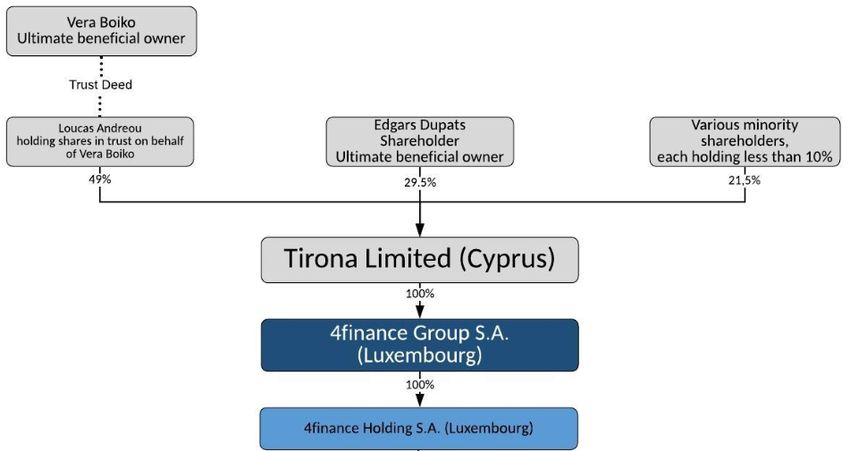

33Shareholder structure

34Management team

Oyvind Oanes Paul Goldfinch Martin Muransky Olivier A Frühwirth

Chief Executive Officer Chief Financial Officer Chief Risk Officer Chief Legal Officer

Oyvind combines experience of leading Fintech Prior to joining 4finance Paul was CFO Martin has more than 20 years of banking Prior to joining 4finance, Olivier served as

consumer banking platform, Numbrs, with nearly of the Corporate and Investment Bank and risk experience from leading institutions the Head of Group Legal of a bank operating

two decades of retail banking across Europe, Division of Sberbank, Russia’s largest such as GE, Raiffeisen Bank International in several countries in the Balkans. His

including building a consumer finance business Bank. He has also held a number of and Sberbank where he held various professional experience also includes

for GE Capital in Russia, leading the turnaround senior roles at UBS, including EMEA leadership roles. Prior to joining 4finance as several leading functions heading legal

of Austria’s Bawag PSK’s retail business and Regional Head of Accounting and Chief Risk Officer, Martin was Chief Credit departments, a restructuring division of a

running Raiffeisen’s multi-country online bank Controlling, and COO/CEO of UBS Bank Officer at TBI Bank. Martin has a MSc in bank, a restructuring company, as well as

ZUNO. Oyvind has a Business Economics Russia. Paul graduated from the Business Economics from the University of working as an attorney. Olivier holds a

degree from the BI Norwegian Business School, University of Auckland in New Zealand Economics in Bratislava, Slovakia and an magister iuris and a doctor iuris degree from

an MA in Management from the University of and commenced his career with KPMG Executive MBA from IMD Business School in the University of Vienna, an LLM from

Stavanger and an MSc in Marketing from the and Citibank before moving to Europe. Lausanne, Switzerland. Boston University, and an MBA from the

University of the West of Scotland. Frankfurt School for Finance and

Management.

Sergio Crespo Martin-Albo Daiga Ērgle Olga Pavlikova Hermann Tischendorf

Chief Marketing Officer Chief People Officer Chief Operations Officer Chief Technology Officer

Sergio started his career at 4finance in 2016 as Daiga has over 20 years of people Prior to joining 4finance, Olga spent more than Hermann brings more than 25 years of

Marketing and Sales Director for Spain before management and leadership experience six years in charge of operations as Director of experience from leading financial services

becoming interim Country Manager. He has over from various organisations and industries. the Centre of Excellence at Dixons Carphone. companies in Austria, Russia, Kazakhstan and

14 years of marketing and sales professional Prior to joining 4finance, Daiga was Senior Before that Olga was leading two EMEA Vietnam. Prior to joining 4finance he was CIO

experience including as Digital Marketing and Vice President HR at airBaltic, Latvian shared services centers for HSBC and Regus. at FE Credit, the biggest consumer lending

Multichannel Director at Mutua Madrileña, a large national airline. Before that, she led the She started her career in the banking industry organisation in Vietnam. Hermann has also

non-profit Spanish insurance company. Before Executive Search branch of HR consulting where she spent more than 7 years at GE been CIO/CTO at Raiffeisen Bank Russia,

that Sergio held various positions, like Head of company Fontes. Daiga also teaches HRM Money Bank performing various roles across Renaissance Credit, Russian Standard Bank

Marketing of New Markets and Head of Internet & Leadership for MBA and Executive MBA Finance, Operations and Process Re- and Eurasia Bank. He holds a Master’s degree

Sales at Linea Directa Aseguradora. Sergio holds students at Riga Business School, and for engineering. Olga is a certified Six Sigma / in Economics and Information/Data Sciences.

a BA in Communication Science from the her PhD research, she focuses on LEAN Black Belt, has an MBA degree from

Complutense University of Madrid and a Employee Engagement and Gamification University of Northern Iowa, USA and a Master

Executive Program from IE Business School. in HR. of Economics from the University of 35

Economics in Bratislava, Slovakia.High quality supervisory board

4finance aims to operate as a “quasi-public” company in terms of board structures, investor transparency and public reporting

Mr. Horwitz is an independent FinTech advisor with over 20 years of experience in financial services, including

William Aaron Horwitz Barclays (as Director of Collections & Recoveries for Europe Retail & Business Bank) and Capital One (14

Chairman of the Supervisory Board years, including as VP of US card recoveries and MD of Capital One Spain). He was formerly president of

of 4finance Group S.A. WDFC SA (Wonga), guiding the restructuring of the company for FCA licensing and suitability. Bill is a

founding member of the 4finance Group supervisory board.

Mr. Geovanis has over 30 years of international investment experience and was a partner at Soros Private

David Geovanis Equity Partners.

Member of the Board

Mr. Sytnik is a Senior Vice President of Finstar Financial Group and has over 10 years of professional

experience in corporate finance, private equity and investment management. He has worked on sourcing and

Evgeny Sytnik executing private equity and early stage deals, as well as multiple financing transactions. He currently holds

Member of the Board board positions in fintech companies. Prior to joining Finstar, Evgeny worked at Pangeo Capital, Russian

Direct Investment Fund, Goldman Sachs and UBS.

36Appendix – detailed regulatory overview

37Regulatory overview

% of interest

License Interest rate

Country income Products (1) Regulator CB (2) Status

required (3) cap (1)

(H1 2019)

Argentina 1% SPL Consumer Protection Directorate - - -

Central Bank of the Republic of

Armenia 3% LOC, IL Yes Yes Nominal

Armenia

Bulgaria – Online 1% SPL

Bulgarian National Bank APR

Yes Yes

(inc. fees)

Bulgaria - Bank 11% IL, LOC, POS, SME

Czech Republic 4% SPL, IL Czech National Bank Yes Yes -

New licensing regime from July 2019 led by

Denmark 11% LOC, IL Consumer Ombudsman Yes Yes -

Danish FSA

Finnish Competition and Consumer Nominal New rate caps in force from September

Finland 3% IL(4) - -

Authority & fees 2019

Nominal, fees New regulation on interest rate cap came

Latvia 6% MTP, IL Consumer Rights Protection Centre - Yes

& TCOC into force in July 2019

Notes:

(1) Abbreviations:

APR – Annual Percentage Rate; IL – Instalment loans; LOC – Line of Credit / Credit Cards; MTP – Minimum to pay; POS – Point of Sale; SPL – Single Payment Loans; SME – Business

Banking (Small-Medium Sized Enterprise); TCOC – Total Cost of Credit

(2) Indicates whether the regulator is also the main banking supervisory authority in the relevant market

(3) Indicates license or specific registration requirement

(4) ‘Mini-IL’ (4 monthly instalments) from September 2019

38Regulatory overview (continued)

% of interest

License Interest rate

Country income Products (1) Regulator CB (2) Status

required (3) cap (1)

(H1 2019)

Nominal, fees

Lithuania 2% SPL, IL Central Bank of Lithuania Yes Yes

& TCOC

National Financial Services Consumer

Mexico 1% SPL - Yes -

Protection Commission

Office of Competition and Consumer Nominal, fees New consultation launched in

Poland 27% SPL, IL - -

Protection & TCOC February 2019

Affordability DTI limits introduced in

Romania 7% IL, LOC, POS, SME National Bank of Romania Yes Yes -

Jan 2019

APR

SlovakiaAppendix – financials and key ratios

40Income statement

H1 2019 H1 2018 % change

In millions of €

(unaudited) (unaudited) YoY

Interest Income 213.4 245.4 (13)%

Interest Expense (30.0) (30.4) (1)%

Net Interest Income 183.4 215.0 (15)%

Net F&C Income 4.0 4.6 (13)%

Other operating income 4.3 4.4 (2)%

Non-Interest Income 8.3 9.0 (8)%

Operating Income (Revenue) 191.7 224.0 (14)%

Total operating costs (100.1) (120.0) (17)%

Pre-provision operating profit 91.5 104.0 (12)%

Net impairment charges (60.5) (63.3) (4)%

Post-provision operating profit 31.0 40.8 (24)%

Depreciation and amortisation (7.1) (5.0) +43%

Non-recurring income/(expense) 0.2 0.9 nm

Net FX gain/(loss) 3.2 (12.3) (126)%

One-off adjustments to intangible assets (0.2) — nm

Profit before tax 27.1 24.5 +11%

Income tax expense (11.9) (7.7) +55%

Net profit/(loss) after tax 15.2 16.8 (10)%

Adjusted EBITDA 62.5 74.2 (16)%

41Balance sheet

30 June 2019 31 December 2018

In millions of € (unaudited)

Cash and cash equivalents, of which: 156.8 172.2

- Online 105.3 110.5

- TBI Bank 51.5 61.6

Placement with other banks 7.4 8.8

Gross receivables due from customers 693.0 705.3

Allowance for impairment (141.7) (152.2)

Net receivables due from customers, of which: 551.3 553.2

- Principal 519.5 521.6

- Accrued interest 31.8 31.6

Net investments in finance leases 5.0 7.3

Net loans to related parties 64.6 66.2

Property and equipment 20.2 8.8

Financial assets available for sale 65.4 38.4

Prepaid expenses 7.6 8.2

Tax assets 32.9 16.6

Deferred tax assets 35.6 37.6

Intangible IT assets 20.0 22.3

Goodwill 17.5 17.5

Other assets 41.5 37.5

Total assets

Calculation for Presentation - other assets (not loans 1,025.8 994.3

Loans and borrowings 446.5 459.4

Deposits from customers 283.8 285.0

Deposits from banks 24.2 2.6

Corporate income tax payable 21.0 18.1

Other liabilities 74.7 70.9

Total liabilities 850.2 836.0

Share capital 35.8 35.8

Retained earnings 169.1 153.9

Reserves (29.2) (31.4)

Total attributable equity 175.6 158.3

Non-controlling interests 0.0 0.1

Total equity 175.6 158.3

Total shareholders' equity and liabilities 1,025.8 994.3

42Statement of Cash Flows

12 months to 31

In millions of € 6 months to 30 June

December

2019 2018 2018

Cash flows from operating activities

Profit before taxes 27.1 24.5 52.6

Adjustments for:

Depreciation and amortisation 7.1 5.0 12.1

Impairment of goodwill and intangible assets (0.2) — 5.7

Net (gain) / loss on foreign exchange from borrowings and other monetary items 2.7 16.3 19.9

Impairment losses on loans 73.2 95.0 178.9

Reversal of provision on debt portfolio sales (5.6) (21.0) (36.6)

Write-off and disposal of intangible and property and equipment assets 0.8 0.3 2.9

Provisions for unused vacations 0.0 0.4 —

Interest income from non-customers loans (3.8) (4.1) (8.1)

Interest expense on loans and borrowings and deposits from customers 30.0 30.4 62.1

Other non-cash items 0.6 2.1 2.5

Profit before adjustments for the effect of changes to current assets and short- 131.9 148.7 291.8

term liabilities

Adjustments for:

Change in financial instruments measured at fair value through profit or loss (2.6) (4.2) (11.3)

(Increase) / decrease in other assets (including TBI statutory reserve,

(12.4) 0.1 (0.3)

placements & leases)

Increase / (decrease) in accounts payable to suppliers, contractors and other

(7.2) (2.9) 3.7

creditors

Operating cash flow before movements in portfolio and deposits 109.6 141.7 284.0

Increase in loans due from customers (103.3) (134.6) (255.1)

Proceeds from sale of portfolio 38.7 44.3 81.9

Increase in deposits (customer and bank deposits) 20.3 26.1 16.5

Deposit interest payments (2.0) (1.7) (4.0)

Gross cash flows from operating activities 63.4 75.9 123.3

Corporate income tax paid (23.3) (20.3) (27.5)

Net cash flows from operating activities 40.1 55.6 95.9

43Statement of Cash Flows (continued)

12 months to 31

In millions of € 6 months to 30 June

December

2019 2018 2018

Cash flows used in investing activities

Purchase of property and equipment and intangible assets (3.1) (3.2) (8.4)

Purchase of financial instruments (30.7) — (13.6)

Loans issued to related parties — (2.3) (2.6)

Loans repaid from related parties 4.0 7.4 7.4

Interest received from related parties 0.3 2.2 2.8

Disposal of subsidiaries, net of cash disposed — (0.1) (0.1)

(Acquisition) / Disposal of equity investments 4.8 — (5.9)

Acquisition of non-controlling interests (0.4) (1.9) (4.4)

Acquisition of subsidiaries, net of cash acquired (0.3) — —

Prepayment for potential acquisition — 20.8 20.8

Net cash flows from investing activities (25.3) 23.1 (3.8)

Cash flows from financing activities

Loans received and notes issued — 0.5 0.5

Repayment and repurchase of loans and notes (17.8) (2.8) (27.2)

Interest payments (25.1) (26.1) (52.7)

FX hedging margin 4.5 — 4.2

Payment of lease liabilities (2.4) — —

Dividend payments — (0.1) (0.1)

Net cash flows used in financing activities (40.8) (28.5) (75.3)

Net increase / (decrease) in cash and cash equivalents (26.0) 50.2 16.8

Cash and cash equivalents at the beginning of the period 148.8 131.9 131.9

Effect of exchange rate fluctuations on cash 0.0 (0.2) 0.1

Cash and cash equivalents at the end of the period 122.8 181.9 148.8

TBI Bank minimum statutory reserve 34.0 17.6 23.4

Total cash on hand and cash at central banks 156.8 199.4 172.2

44Key financial ratios

6M 2019 6M 2018 12M 2018

Capitalisation

Equity / assets 17.1% 14.9% 15.9%

Equity / net receivables 31.9% 27.9% 28.6%

Adjusted interest coverage 2.1x 2.4x 2.4x

TBI Bank consolidated capital adequacy 20.7% 25.5% 22.4%

Profitability

Net interest margin:

- Online 81.8% 89.4% 88.9%

- TBI Bank 25.1% 28.3% 26.8%

- Overall group 56.1% 66.2% 63.5%

Cost / income ratio 52.2% 53.6% 52.1%

Normalised Profit before tax margin 11.2% 14.6% 15.2%

Normalised Return on average equity 14.4% 39.3% 32.7%

Normalised Return on average assets 2.4% 5.7% 4.9%

Asset quality

Cost of risk:

- Online 27.2% 22.7% 24.0%

- TBI Bank 4.5% 10.4% 8.0%

- Overall group 17.4% 18.2% 17.7%

Net impairment / interest income 28.4% 25.8% 25.9%

Gross NPL ratio:

- Online 19.3% 22.0% 22.0%

- TBI Bank 16.2% 16.6% 15.9%

- Overall group 17.9% 20.0% 19.4%

Overall group NPL coverage ratio 114.3% 118.6% 110.6%

See appendix for definitions of key metrics and ratios

45TBI Bank’s financial highlights

(€m) 2017 2018 H1 2018 H1 2019

Net Interest Income 59 72 35 37

Net F&C Income 8 10 5 4

Other Operating Income 1 (0) 0 0

Total Operating Income 68 82 40 42

Operating Costs (36) (43) (20) (22)

Provisions (9) (22) (13) (7)

Other Income/Expenses 0 0 (1) (2)

PBT 23 17 6 11

Net Income 20 14 5 10

Net Receivables 238 272 240 277

Total Assets 367 397 397 428

Customer Deposits 257 271 268 275

Bank Deposits 0 3 16 24

Equity 95 105 97 108

3.1% 20.7% 1.6%

YTD Growth of Capital adequacy YTD Growth of

loan portfolio ratio deposits

4.8% 30.0% 18.7%

Return on Return on Return on

total assets working portfolio average equity

4.5% 1,350 1.6%

Cost of

Cost of risk Employees funding

46Glossary/Definitions

• Adjusted EBITDA – a non-IFRS measure that represents EBITDA (profit for the period plus tax, plus interest expense, plus depreciation and amortization) as adjusted by income/loss from discontinued operations, non-cash gains and losses

attributable to movement in the mark-to-market valuation of hedging obligations under IFRS, goodwill write-offs and certain other one-off or non-cash items. Adjusted EBITDA, as presented here, may not be comparable to similarly-titled

measures that are reported by other companies due to differences in the way these measures are calculated. Further details of covenant adjustments can be found in the relevant bond prospectuses, available on our website

• Adjusted interest coverage – Adjusted EBITDA / interest expense

• Cost of risk – Annualised net impairment loss / average gross receivables (total gross receivables as of the start and end of each period divided by two)

• Cost / income ratio – Operating costs / operating income (revenue)

• Equity / assets ratio – Total equity / total assets

• Equity / net receivables – Total equity / net customer receivables (including accrued interest)

• Gross NPL ratio – Non-performing receivables (including accrued interest) with a delay of over 90 days / gross receivables (including accrued interest)

• Gross receivables – Total amount receivable from customers, including principal and accrued interest, after deduction of deferred income

• Intangible assets – consists of deferred tax assets, intangible IT assets and goodwill

• Interest income – Interest and similar income generated from our customer loan portfolio

• Loss given default – Loss on non-performing receivables (i.e. 1 - recovery rate) based on recoveries during the appropriate time window for the specific product, reduced by costs of collection, discounted at the weighted average effective

interest rate

• Net effective annualised yield – annualised interest income (excluding penalties) / average net loan principal

• Net impairment to interest income ratio – Net impairment losses on loans and receivables / interest income

• Net interest margin – Annualised net interest income / average gross loan principal (total gross loan principal as of the start and end of each period divided by two)

• Net receivables – Gross receivables (including accrued interest) less impairment provisions

• Non-performing loans (NPLs) – Loan principal or receivables (as applicable) that are over 90 days past due (and, for TBI Bank, shown on a customer level basis)

• Normalised – Adjusted to remove the effect of non-recurring items, net FX and one-off adjustments to intangible assets, and for 2018 ratios only, adjusted to reflect the opening balance of 2018 balance sheet after IFRS 9 effects

• Overall group NPL coverage ratio– Overall receivables allowance account / non-performing receivables

• Profit before tax margin – Profit before tax / interest income

• Return on Average Assets – Annualised profit from continuing operations / average assets (total assets as of the start and end of each period divided by two)

• Return on Average Equity – Annualised profit from continuing operations / average equity (total equity as of the start and end of each period divided by two)

• Return on Average Tangible Equity – Annualised profit from continuing operations / average tangible equity (tangible equity as of the start and end of each period divided by two)

• Tangible Equity – Total equity minus intangible assets

• TBI Bank Capital adequacy ratio – (Tier One Capital + Tier Two Capital) / Risk weighted assets (calculated according to the prevailing regulations of the Bulgarian National Bank)

47Contacts

Investor Relations

investorrelations@4finance.com

Paul Goldfinch James Etherington Liene Kuģeniece

Chief Financial Officer Head of Investor Relations Investor Relations Coordinator

Phone: +371 2572 6422 Phone: +44 7766 697 950 Phone: +371 2617 7782

E-mail: paul.goldfinch@4finance.com E-mail: james.etherington@4finance.com E-mail: liene.kugeniece@4finance.com

Headquarters

17a-8 Lielirbes street, Riga, LV-1046, Latvia

48You can also read