Private Equity in China: The Impact of Regulatory Systems on Private Equity Firms - Intercollegiate US-China Journal

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

26 icUJ research article

Private Equity in China: The Impact of Regulatory

Systems on Private Equity Firms

Hannah Bradford[1] and Riley McKinzie[2]

[1] Hannah is a fourth-year student at The University of Texas at Austin. She is double majoring in philosophy and East Asian

studies with minors in business and Chinese.

[2] Riley is a third-year student at The University of Texas at Austin. She is double majoring in international relations global stud-

ies and East Asian studies with minors in gender studies and Chinese.

Abstract This research paper examines China’s economy, private equity, and the impact of Published online

China’s regulatory system on foreign and local private equity firms. To have a more nuanced January 2021

understanding of the relationships between the economy, the financial market, and the sectors,

we will examine each individually. Initially, we outline China’s economic growth through the Citation

transition away from central planning in 1978. Then, the history and development of China’s Bradford, Hannah and Riley

financial systems, including the banking and financial sectors, are explained in section two. McKinzie. 2020. “Private

We provide a closer look into private equity and investment methods from a Western and Equity in China: The Impact of

Chinese perspective throughout section three. Sections four and five examine capital growth Regulatory Systems on Private

and sector trends among foreign and local private equity funds. In the final section, we discuss Equity Firms.” IUCJ 1, no. 1

the impact of the newly introduced Foreign Investment Law on current and future foreign (Winter 2021), 26-33.

investment enterprises.

Keywords: private equity; Chinese economy; global financial systems; Foreign Investment

Law

Introduction zones, and partial trade liberalization, all of which allowed the

Chinese economy to rapidly grow. From 1978-2018, China

I n the last several decades, China’s economy has seen ex- experienced an annual GDP growth rate of 9.8% (6). When

traordinary growth and development. From joining the World the global financial crisis of 2008 hit, China’s (U.S.) $586

Trade Organization and becoming the second-largest economy billion stimulus package focused on investing in infrastructure

in the world to expanding its financial and banking sectors, and loosening bank lending, and this led to a quick economic

China’s economic growth since the early 2000s has surpassed recovery, allowing for China’s GDP growth rate to rebound (7).

almost every prediction. China now ranks first in GDP based That said, for the past six years, China’s GDP growth rate has

on purchasing power parity, as well as merchandise trade and slowed, reaching 6.1% in 2019 (9). Many economists warn that

foreign exchange reserves (Morrison 2019, 11).1 Not only if trade tensions with the United States persist, then China’s

does China rank number one in GDPP PP, at (U.S.) $27 trillion real GDP growth rate could decline to 5% in 2021 (6).

(2019), but China’s GDPP PP is almost (U.S.) $6 trillion larger

than the United States’ GDPP PP at (U.S.) $21 trillion (2019) The Chinese government’s policies and plans have supported

(11). While China’s real GDP growth rate has begun to slow, substantial growth for the Chinese economy in the past 40

China’s growth is still larger than most developing countries years, while China has allowed increased domestic free market

and Western nations. activity and international trade. The World Bank has char-

acterized China’s economic growth as “the fastest sustained

Prior to 1979, China practiced economic nationalism and expansion by a major economy in history” (11). For example,

protectionism in which a majority of China’s economy was China’s recent “Made in China 2025” plan seeks growth in sev-

centrally planned and controlled by the state. This allowed the eral high-tech areas such as: modern manufacturing; agriculture

Chinese government to allocate resources toward critical in- machinery; basic material products; high-tech maritime vessels;

dustries and infrastructure for development and growth. These electric vehicles, batteries, and engines; core components

policies were implemented to ensure that the Chinese economy of medical devices; high-performance computers; industrial

was relatively self-sufficient and not reliant on foreign trade. robotics; advanced medical devices; and improving innovation

Although China developed a number of modern industries capabilities (Congressional Research Service 2020, 1).

and infrastructure from 1949-1978, many Western economists

believe central planning was inefficient, even though China State-Led Development

had a nominal GDP growth rate of 6.7% annually (6). During

this time, China remained a relatively poor nation by Western In 1978, China began to transition away from central planning,

standards. and today, China utilizes state-led development to promote eco-

nomic growth and development. State-led development is gen-

In 1978, China began its era of “Reform and Opening,” which erally considered to be macroeconomic planning that allows for

included agricultural reforms, opening portions of the econ- states to guide the economy and certain industries or projects

omy to the free market, and creating four special economic through incentives, investment, or ownership. However, the

state does not have sole control over the planning, production,

1 PPP compares the purchasing power of currencies throughout the world to and distribution of goods and services, as it would under central

determine their theoretical exchange rate that allows for the purchase of the

same amount of goods and service. planning. Under state-led development, China employs several

research article IUCJ 27

mechanisms such as: the creation of Special Economic Zones owned banks: (1) the People’s Construction Bank of China;

and Free Trade Zones; short, medium and long-term develop- (2) the Agricultural Bank of China; and (3) the Industrial and

ment plans and priorities; governmental incentives for projects Commercial Bank of China. These three banks began handling

in certain industries; and state ownership and investment in key a large portion of the commercial banking business. During this

“strategic” industries, such as telecom, often through state- time, the Bank of China formally became China’s central bank.

owned enterprises.2 All of these mechanisms combined have This shift gave individuals and businesses more access to loans

allowed the Chinese government to influence the growth of and banking services.

the Chinese economy without employing central planning or

command economy techniques. Since the 1980s, the Chinese government has enabled the

growth of the banking system. In the 1990s, the banking sector

Rapid development from 1978 to approximately 1990 focused further evolved with the creation of three policy banks—Chi-

on agriculture reforms, a gradual reduction in central planning, na Development Bank, Import and Export Bank of China,

and the creation of SEZs for international trade. The Chinese and Agricultural Development Bank of China—and the three

government opened four SEZs—Shenzhen, Zhuhai, Shantou, specialized banks became state-owned commercial banks—

Xiamen—to facilitate foreign trade. After the success of these ABC, BOC, and ICBC (Chen and Vinson 2016, 1614). Addi-

SEZs, several other SEZs and “open” areas were created to fur- tionally, several rural and urban cooperatives were established.

ther global integration. While China had begun to reform and While the banking system was expanding during this time, the

open its economy from 1978, China’s entrance into the WTO Chinese government still controlled a majority of the industry

in 2001 further stimulated its economic growth and global and loaned money to low-performing SOEs. This led to many

integration. low-performing SOEs to default on their loans and shut down.

To combat this trend, the MOF restructured the four state-

China also has consistently moved up the economic value owned commercial banks and provided a capital contribution of

chain to ensure its economic growth does not become stagnant. (U.S.) $33 billion to mitigate the non-performing loans (1615).3

Throughout the years, China has shifted economic development These reforms have led to over a hundred commercial banks

from the agriculture sector to the manufacturing sector to the being authorized to operate throughout China today. While the

service sector. The service sector currently accounts for approx- banking system has expanded, the PBOC remains the central

imately 52% of the GDP. Additionally, China’s manufacturing authority in the banking system. The PBOC is responsible for:

sector is moving up the value chain by focusing on higher-val- creating monetary policy; reducing risk and promoting the

ue-added work. Further, the Chinese government invests in stability of the financial system; regulating lending and foreign

construction projects to stimulate jobs and support economic exchange; and supervising the payment and settlement systems

growth. Finally, the diversification of the Chinese economy by (1614).

encouraging private and state sector development has led to a

“mixed” economy. This shift has encouraged job growth, with Critiques of China’s banking system highlight the need for

roughly 90% of new jobs originating from the private sector. A improved efficiency, and specifically in the area of loan allo-

common misconception is that foreign direct investment is the cation. As a majority of bank credit goes to state-owned firms,

primary driver of private economic growth. FDI levels between these loans are often not repaid or repaid late, and there is

2-3% are considered average, while FDI levels between 5-6% speculation that loans to SOEs may be made based on personal

are considered significant. China’s FDI has been hovering be- connections, rather than business merit. Further, the overall

tween 2-4% of the GDP since the early 2000s (Morrison 2019, demand for loans exceeds supply. With many players unable

10). In recent years, analysts estimate that China’s state sector to access loans, there has been rapid development of other

is responsible for around 40% of the GDP compared to the banking intermediaries in recent years to meet this demand for

private sector, which is responsible for 60% of the GDP. capital.

Financial Systems Financial Markets

Banking In recent years, China’s financial sector has rapidly grown, in

large part due to free-flowing investments occurring between

The banking sector and the financial sector comprise China’s local and foreign firms. China’s financial markets consist of

financial system, and these sectors work together to encourage three stock exchanges—SHSE (Shanghai), SZSE (Shenzhen),

and facilitate investments. China’s financial system has largely and HKEX (Hong Kong)—bond markets, venture capital/

been dominated by the banking sector, which remains much private equity, and real estate (Allen and Qian 2014, 501).

larger than China’s financial markets. Throughout the 1990s, China’s financial system saw parallel

growth in the two new mainland-based stock exchanges, SHSE

Between 1949-1978, China’s banking system consisted of one and SZSE, and the real estate market (501). However, the stock

large, state-owned bank, the People’s Bank of China, which exchange and real estate markets are characterized by their high

was responsible for 93% of China’s total financial assets (Allen volatility due in part to the ongoing development of a reliable

and Qian 2014, 503-504). The PBOC was able to control legal framework. When China joined the WTO in 2001, foreign

virtually all financial transactions, personal and commercial. financial institutions were allowed to engage in more frequent

Beginning in 1978 and ending in 1984, the banking sector saw and larger-scale capital flows into the stock and real estate

major reforms. As a part of China’s shift away from central markets. Further, in 2001, China allowed institutional investors

planning, the PBOC dissociated with the Ministry of Finance in to freely withdraw capital after exiting an investment.4 This

1979 (504). This led to the creation of three additional state- 3 The four banks include PBOC, ABC, BOC, and ICBC.

2 China’s “strategic” industries include telecom, finance, energy, raw materials, 4 Institutional Investors are large accredited investors in PE funds including

and infrastructure. pension funds, banks, wealthy individuals, etc.

27 icUJ research article

Figure 1. Overview of China’s financial system (Allen and Qian 2014, 505).

transitioned the market from a closed-ended fund system to capital. Foreign companies, including PE firms, actively want-

an open-ended fund system. This transition has been lucrative ed to invest in domestic companies, and this was a new and

for PE firms, leading to an increase in total net assets value important option for domestic companies who previously relied

from (U.S.) $1.3 billion in 1998 to (U.S.) $332 billion in 2008 almost solely on state-owned banks for funding. As China’s

(505).5 In comparison to the banking sector, PE is only a small capital markets were still relatively new and underdeveloped,

portion of assets; however, the growth of the PE industry marks the entrance of foreign PE provided real value to Chinese

a change in China’s financial markets. companies. This value is in the increase in capital, managerial

skills, and overall expertise in the finance industry.

Private Equity

Types of Funds: Ownership and Currency

Private Equity in China

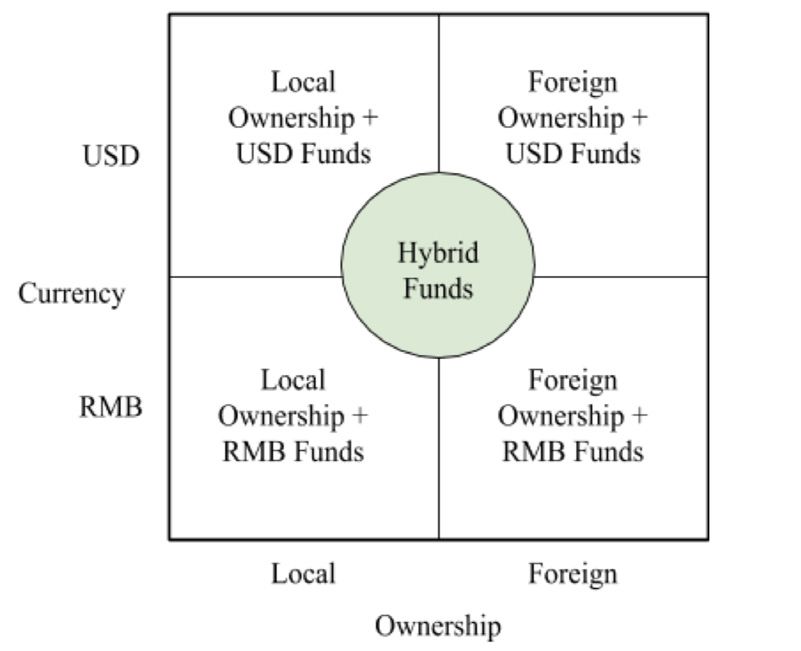

Funds in China are categorized by two main qualities: owner-

As China’s financial industry develops, China has somewhat ship and currency. Foreign investor(s) entirely own a foreign

followed the widely known Western model of PE. However, fund. China considers anyone who is not a Chinese national a

as history has shown, China is keen on creating its own path, foreigner. In this paper, when we discuss foreign ownership, we

which is evident in the PE industry. Differences between PE in are referring to a United States foreign investor. Still, potential-

the West and in China result from differing regulatory envi- ly any foreign PE fund could invest in China equities. Chinese

ronments and how PE firms have evolved (Yong 2012, 74). investor(s) entirely own a local fund.7 A fund can also have

Although China saw economic growth from 1978, private equi- a mix of foreign and local ownership and be a hybrid fund.

ty was not introduced until the early 1990s. The State Council Distinguishing ownership is necessary because, historically,

first introduced broad-based PE to increase financial innovation ownership determines which firms are subject to specific Chi-

and provide more funding opportunities (79). In the late 1990s nese financial and market regulations.8

and early 2000s, PE was little known or misunderstood by

Chinese finance personnel. The rise of PE in China has much After ownership is established, a PE fund will decide if they

to do with a 2007 deal between China Investment Corporation want to raise funds in USD, RMB, or a combination of the two.

and Blackstone, a leading global PE firm (xiii).6 This deal was Foreign and local funds are allowed to raise funds in either

highly publicized in the media for two major reasons: (1) CIC USD or RMB and are not obligated to raise funds based on

paid a lot, (U.S.) $3 billion, for an approximate 10% stake in nationality. When choosing a currency to raise funds, PE firms

Blackstone; (2) this was the CIC’s first investment deal, and it will likely consider their exits plans and the need for convert-

took place before the CIC was officially incorporated. This deal ible currency. A fund-raised with the combination of USD and

prompted the public to wonder what was “Blackstone,” and it

introduced domestic companies to PE firms, a new source of 7 A local fund is commonly referred to as a domestic fund, a Chinese-based

fund, and occasionally other terms indicating domestic ownership.

5 Net Asset Value is the current value of all assets within a PE fund minus the 8 The new FIL is intended to create an even playing field between foreign and

value of all liabilities. local funds, so this should no longer be as big of an issue. However, it is un-

6 The China Investment Corporation (CIC) is a sovereign wealth fund with clear if the FIL will level the playing field, and we will not know until the five

~940 billion in assets. year transition period is complete.

research article IUCJ 28

RMB will probably be a hybrid fund under the ownership of Investment Process

foreign and local investors. A fund solely owned by foreign or

local investors will not typically raise funds in two different Foreign and local PE firms will always face challenges in

currencies. fundraising and establishing a fund. If foreign firms attempt

to raise money in China, they face the challenges of being

PE funds fall into one of the following categories: outsiders. They cannot network and connect with investors

—Foreign owned USD funds effectively, especially if they are not fluent in Chinese. Typical-

—Foreign owned RMB funds ly, foreigners have more success raising funds outside of China,

—Hybrid foreign/local USD and RMB funds while Chinese finance professionals have more success raising

—Local owned USD funds funds in China.

—Local owned RMB funds (private or state owned)

The language and culture barrier also has the potential to se-

verely impact a foreign fund’s value-add methods at the target

company and the fund’s performance; however, foreign firms

have the advantage of expertise. Knowledge and experience are

vital in the private equity sector. It is increasingly important not

only to be an expert in private equity but also to have a substan-

tial background in the industry in which the firm is investing.

The process of adequately valuing a company in China is

complicated, as financial statements are often semi-fabricated,

embellished, or Chinese companies refuse to release the state-

ments. This makes foreign investors wary. The uncertainty is

balanced with proper deal sourcing and sufficient due diligence.

Despite the concerns, PE firms may agree to a valuation ad-

Figure 2. Types of private equity funds in China (Yong 2012, justment mechanism to aid in “mitigating risk” (115). A VAM

98). can follow financial or nonfinancial measures; the figure below

summarizes possible scenarios of a VAM.

Structure: Onshore vs. Offshore

In China, private equity investments are usually in “minority

Private equity firms will legally establish themselves either growth capital with some form of broad control or pre-IPO

offshore or onshore. Being offshore enables PE firms to avoid investments” (80). Since most deals use the minority structure,

China’s capital gains taxes and lengthy forms and regulations, the PE’s firm’s influence over an investment company is often

transfer equity shares more quickly, and gain more flexibility questioned. A PE firm aims to ensure control when struc-

in converting currency. An offshore structure often “provides turing the deal, often creating contractual obligations in the

a quicker route to exit the investment through an IPO or trade agreement. Additionally, when a PE firm has a minority stake,

sale” (102). Foreign and local firms can use offshore structures, they seek to ensure active portfolio management and open

but it is less common for local firms. In the 2010s, the Chinese communication with the investment target. During the typical

government reformed regulations when they realized they were investment horizon, GPs hope to restructure the investment and

losing capital gains taxes from offshore PE firms. prepare to exit.

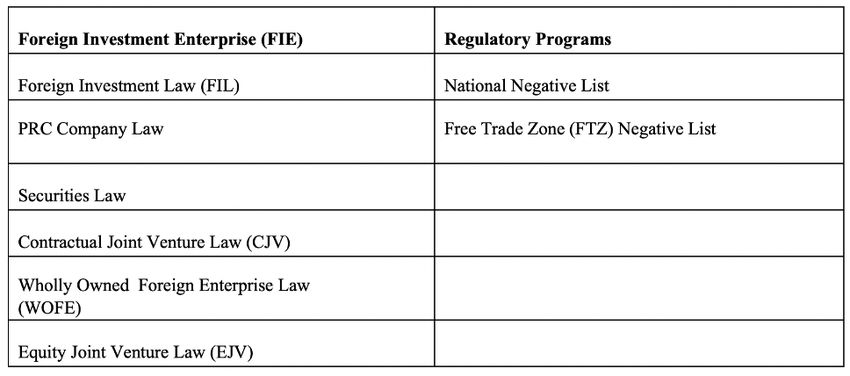

PE firms that are legally based in China—“onshore”—have The target exit strategy is usually going to differ between

different structures depending on ownership and the sectors USD funds and RMB funds. RMB funds are most likely going

the firm is targeting. In China, foreign onshore firms are called to exit domestically. If the fund decides to make an IPO, it

Foreign Investment Enterprises; FIE is an umbrella term which will likely be on a domestic exchange (e.g., SHSE) because

“refers to an enterprise incorporated under Chinese laws within foreign exchanges are costly. However, the China Securities

the territory of China, and with all or part of its investment Regulatory Commission has strict regulations, so RMB firms

from a foreign investor” (Zhou 2019). The type of FIE a PE will need to comply and prepare sufficiently, or they will be

firm will take will vary based on ownership. For example, the denied. Trade and secondary sales increased in popularity as

Wholly Owned Foreign Enterprise has foreigners exclusively exit strategies for RMB funds with the creation of the Beijing

contributing to capital, and the Equity Joint Venture has foreign Financial Assets Exchange in 2010. Trade sales are much

and local partners contributing to capital. quicker and relatively cheaper; “a trade sale to a strategic buyer

will be paid in cash (equity swaps are not common in China)”

Each FIE has corresponding laws for the enterprises to follow. (179). Leveraged buyouts are the least common exit structure

For example, a company who is structured as an EJV must ad- for RMB PE funds. This often occurs because such funds take

here to the 1979 PRC Equity Joint Venture Law. With an EJV, minority stakes in investments, and LBOs are unnecessary. The

foreigners need to contribute a minimum of 25% of capital. The funds usually opt for minority ownership for the efficiency of

EJV states that the “profits and losses are shared according to deal closing and exiting (131).

the ratio of capital contributions of each partner” (Yong 2012,

109). Each law will articulate the capital contribution, the own- The most common exit strategy for USD funds is through an

ership structure, other laws that must be adhered to, and more. IPO or trade sale. Exiting through an IPO means the invest-

The structures listed above are not an exhaustive list but are the ment will be listed on a public exchange for the first time. The

most popular structures among FIE. investment company is not required to list on an exchange near

its geographical location and many companies will choose to29 icUJ research article

Figure 3. Valuation adjustment mechanism (Yong 2012, 115).

list based on its sector or target audience. Common stock ex- logistics company, Logicor, to the CIC for (U.S.) $14.5 billion,

changes that are not located in China are the NASDAQ, NYSE, and Blackstone’s 2016 sale of a 25% stake in Hilton Worldwide

and HXEX. The most popular stock exchanges in China are Holdings to the Chinese company, HNA group, for (U.S.) $6.5

the SHSE and the SZSE. In 2019, there were 120 IPO listings billion (Blackstone 2020).

on the SHSE, and 77 IPO listings on the SZSE (Ernest Young

2019). These IPO listings brought in approximately (U.S.) $40 In China, foreign USD PE funds have declined in AUM and

billion (Ernest Young 2019). capital raised since 2014, while local RMB funds have in-

creased in AUM and capital raised in the same time period.9

Trade sales are usually implemented offshore to avoid taxes In 2018, PE firms in China had (U.S.) $600 billion in AUM

and regulations; however, some deals will still require the with a majority of the AUM growth from the increase in local

approval of the CSRC. The equity shares and ownership will be RMB funds raised in recent years (Freehills 2018, 9). There has

transferred to the buyer through an offshore entity. The buyer been a decrease in USD capital raised, with (U.S.) $18 billion

will then funnel the shares back through an offshore holding raised in 2008 and (U.S.) $15 billion in 2017 (Preqin 2019, 8).

company to bring it back to China (Yong 2012, 130). Foreign funds’ decline in AUM and capital raised is attributed

to the complexity of investing regulations and lengthy currency

Secondary sales and leveraged recapitalization are less com- conversions for foreign-denominated funds. In addition, the

mon than IPOs and trade sales. Secondary sales are low profile, capital released in the 2014 IPO boom has shifted the capital

require fewer regulations, and are relatively simple compared from USD funds to domestic RMB funds. Further, Western

to other exits. A secondary sale will happen between two firms’ concern over the Sino-U.S. trade disputes has contributed

private equity firms, and is straightforward compared to other to the decrease in PE investments (Madi 2020, 75). Addition-

exits. The terms of the deal can be negotiated between both ally, foreign PE investments between 2018-2019 decreased by

parties without government intervention allowing for a profit- 64%, with (U.S.) $5 billion invested in China in 2019 (Preqin

able exit (131). 2019, 7). In 2015, over 1,300 PE firms were operating in China,

For leveraged recapitalization exits, China has strict restrictions with foreign funds accounting for approximately 400 firms.

on payment distributions to shareholders. Chinese regulations These foreign funds have an average of (U.S.) $100 million in

often do not allow for equity to be withdrawn at any time, cre- assets under management (Freehills 2018, 13).

ating an additional roadblock. Also, companies generally do not

have enough liquid cash for a leveraged recapitalization (132).

Foreign Private Equity Firms

In recent years, a few leading foreign PE firms operating in

China have been Blackstone, the Carlyle Group, BlackRock,

Bain, and UBS (JP Morgan 2019, 3). Blackstone is one of the

world’s largest PE firms, with (U.S.) $95 billion in assets under

management worldwide, and it is a major foreign PE fund

operating in China (Blackstone 2020). Their large amount of

capital has allowed them to become one of the most influential

foreign funds in China’s PE industry, specifically in the real es-

tate market; however, Blackstone has been involved in several Figure 4. Aggregate capital raised by foreign and local PE

major deals in China in multiple industries. Two examples of funds in China.

recent deals include Blackstone’s 2017 sale of their European

9 AUM is also referred to as the size of the fund.research article IUCJ 30

billion in UK-based PizzaExpress (Hony Capital 2019). A piv-

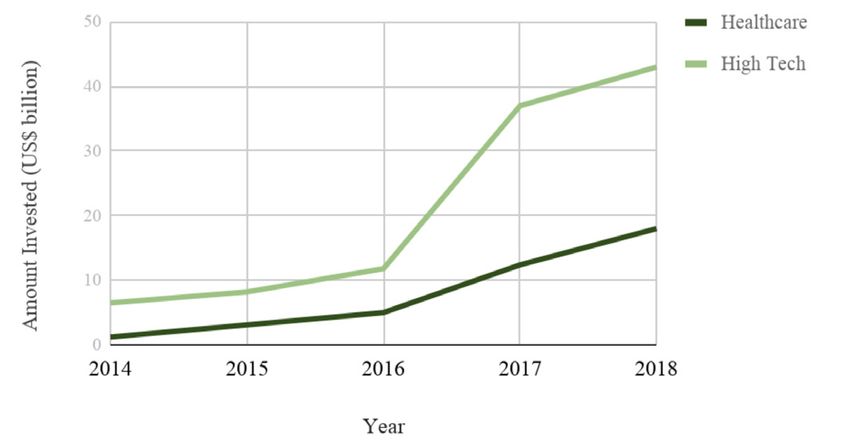

In recent years, the leading sectors for foreign PE investment otal element to Hony’s strategy are cross-border investments.

in China have been consumer, healthcare, and technology (JP

Morgan 2019, 3). The top emerging industries are healthcare In China, local RMB PE funds have increased in AUM and

and high tech. In 2018, the healthcare industry accounted for capital raised since the late 2000s (Preqin 2019, 7-8). In 2018,

(U.S.) $43 billion total capital invested, and foreign funds were the majority of the (U.S.) $600 billion AUM (16) in China

accounted for (U.S.) $18 billion of the total capital invested came from the increase in capital raised by local RMB funds

(Preqin 2019, 16). In 2019, the healthcare industry grew an in recent years, with (U.S.) $4 billion capital raised in 2008,

additional 22% in capital invested with investment occurring in (U.S.) $21 billion in 2013, and (U.S.) $105 billion in 2017 (20).

pharmaceutical and biotechnology companies (17). This growth These increases are attributed to the local PE market’s acceler-

is partly due to the novel coronavirus outbreak at the end of ated maturity, local fund managers increasing the scale of local

2019. For example, Blackstone invested (U.S.) $400 million firms and the influx of capital following the 2014 IPO boom

in HEC Pharm, one of China’s fastest-growing pharmaceutical for Chinese SOEs. In 2015, over 1,300 PE firms were operat-

companies (Blackstone 2020). This investment illustrates the ing in China, with local funds accounting for approximately

trend of influential foreign firms investing in China’s emerging 900 firms. Local funds’ AUM range from (U.S.) $32 million to

industries. (U.S.) $90 million (Freehills 2018, 14).

Figure 5. Foreign PE capital invested in healthcare and high Figure 6. Local PE capital invested in healthcare.

tech.

In recent years, the leading sectors for local PE investment in

Foreign PE investments into technology-intensive sectors are China have been healthcare, consumer discretionary, tech-

increasing at rapid rates (Bain & Company 2019, 12). Infor- nology, media, and telecom (JP Morgan 2019, 4). Similar to

mation technology is one of the top markets in the high tech foreign funds’ investment trends, local PE funds target the

sector. In 2018, the information technology sector accounted healthcare and technology industries. In 2018, the healthcare

for (U.S.) $103 billion total capital invested, and foreign funds industry accounted for (U.S.) $43 billion total capital invested,

accounting for (U.S.) $43 billion of the total capital invested and local funds accounted for (U.S.) $17 billion of the total

(Preqin 2019, 22). Further, China’s internet and technology capital invested (Prequin 2019, 16). In 2019, healthcare grew

deals have accounted for 85% of foreign PE investment growth an additional 22% in capital invested, and in 2019, local funds

between 2013-2017 (Bain & Company 2019, 13). The average accounted for (U.S.) $21 billion of capital invested (23). This

deal size rose from (U.S.) $30 million in 2013 to (U.S.) $213 growth can be seen through local PE firms’ recent investments

million in 2018 for internet and technology deals (17). Bain by CITIC Capital and Layal Valley Capital. CITIC Capital

& Company’s survey showed that approximately 85% of PE invested (U.S.) $447 million in Harbin Pharmaceuticals, and

investors find it difficult to evaluate “new-economy companies” Loyal Valley Capital invested (U.S.) $150 million in Akeso

in China due to the discrepancies between traditional methods Biopharma. These investments demonstrate local PE firms’

of PE valuations and Chinese market valuations (13). How- and the Chinese government’s role in aiding investment in the

ever, China’s PE market is growing and creating increasing healthcare industry.

opportunities for foreign PE investment in various industries.

Legal Regulatory Systems

Local Private Equity Firms

Local PE funds’ influence in the PE market has continued to Ministries and Commissions

grow, as their AUM, capital raised, and deal exit value has

increased. In recent years, the leading local PE firms in China China’s legal system is relatively new, as it began its mod-

have been: Hony Capital, CITIC Capital, Boyu Capital, and ernization with the economy’s growth after 1978. The current

Jiuzhou Ventures (Freehills 2018, 9).10 Hony Capital has (U.S.) Chinese legal system does not hold itself to the same standards

$12 billion AUM (2019). This capital has enabled Hony Capital as Western legal systems do. However, the Chinese government

to invest in over 100 Chinese companies and become an indus- has made efforts to increase the sophistication of the system

try leader. Their portfolio is diverse, and Hony Capital played and decrease inconsistencies. This is especially apparent in

a significant role in the 2015-2019 trend of Chinese PE firms foreign investment regulations. The new laws and regulations

making foreign investments in Western-based companies. For implemented in the past five years aim to level the playing field

example, Hony Capital made a 2014 investment of (U.S.) $1 between local and foreign firms.

10 CITIC is a private equity firm owned by the MOF.31 icUJ research article

Table 1. Regulatory bodies in China.

All “laws” are “passed by the National People’s Congress, the —Judicial interpretation → Interpretations of the Supreme Peo-

highest legislative authority,” and all “administrative regula- ple’s Court on several issues concerning the application of the

tions” are “issued by the State Council, the highest administra- FIL of the PRC (The Supreme People’s Court of the People’s

tive and executive authority” (Fosh and Yang 2017). The State Republic 2019).

Council is responsible for overseeing the regulatory commis- —Cleaning up → MOFCOMs decision on abolishing specific

sions and ministries (Yong 2012, 285). There are many minis- regulations (MOFCOM 2019).

tries and commissions; each is responsible for a different sector Under the FIL, foreign investment will include:

or role. The laws, ministries, and commissions are essential for —Establishment of an FIE, independently or jointly.

regulating the financial markets, foreign investment and foreign —Acquisition of shares, equity, or property in an FIE.

enterprises are shown in tables 1 and 2.11 —Investment in a new project in China, independently or

jointly.

Foreign Investment Law —Investment in any other way as may be stipulated by laws or

regulations of the State Council.

The enactment of the Foreign Investment Law on January 1,

2020, resulted in all previous FIE laws being repealed. These It is unclear if variable interest entities, round-trip investments,

laws include EJV, WOFE, and CJV; all of these laws formerly investments made by Chinese citizens currently abroad, or

served as the governing law on foreign investments and the foreign governmental organizations will be considered foreign

flow of foreign capital (PWCCN 2020).12 The introduction of investments under the FIL.13 The VIE’s clarification will likely

the FIL is one of China’s most significant reforms in corporate be of interest to PE firms because PE firms commonly use this

governance and foreign investment to date. The FIL applies to structure.

all companies who make foreign investments in China, and it

makes those companies subject to the PRC Company Law. The The FIL’s critical components can be noted in four categories:

goal of the FIL is to enforce equal treatment between foreign investment promotion, investment administration, investment

and local firms. The designated regulations are primarily the protection, and legal responsibilities. Investment promotion

same, with only a few different regulations occurring. Ancillary includes equal treatment for foreign and local funds and

rules to the FIL show some of the areas where foreign and local increased transparency in legislative processes. Investment

investments are treated differently. The rules highlighted below administration includes: pre-market national treatment14 access

are not all-inclusive, but they are representative. and negative list administration; new investment reporting

system; project-based regulations by the NDRC; sector-specific

Example ancillary rules concerning FDI (1): regulations; and continued standardization of corporate struc-

—Information reporting → Announcement on matters regard- tures between local and foreign firms.15 Investment protection

ing the reporting of information on foreign investment (MOF- includes funds’ remittance, protection of intellectual property,

13 A VIE occurs when an investor has contractual control despite not having

COM 2019). voting rights. Frequently, a domestic Chinese company will be controlled by its

—FIE registration → Circular of the state administration for foreign investors. This is used to avoid capital and sector restrictions.

market regulation on effective work on registration of for- 14 According to Matthew Dresden and Sara Xia, national treatment “means that

eign-invested enterprises to implement the FIL (JianZhu 2019). foreign investors will be treated no less favorably than Chinese investors at the

“entrance stage,” so long as the invested industry is not on the negative list.” This

11 This list is not all-encompassing, but the ministries, commissions, laws, means that the Chinese government cannot officially discriminate against FIE

and programs we believed to be most important in understanding the financial because they are foreign. No discriminatory regulations are being repealed that

industry. are not on the negative list.

12 EJV, WOFE, and CJV are all structures of foreign investment enterprises 15 Negative lists control which sectors foreign investment companies are

(FIE). There is a corresponding law to each FIE structure with the same title. allowed to invest in.research article IUCJ 32

Table 2. Private Equity Legislation.

and performance of lawful government commitments (Dresden the local PE sector is now larger than the foreign sector and is

and Xia 2020). Legal responsibilities are meant to modernize growing rapidly.

the regulatory system, protect the companies from unfair or

harsh restrictions, and to create an equal distribution of law As of January 2020, China is attempting to regulate foreign

(including the government), according to the FIL (PWCCN and local firms based on the same laws. The new FIL creates

2020, 1). Of all these changes, the FIL’s most drastic effect is standardized corporate governance structures for both foreign

the alignment of corporate governance structures. As of January and local firms. All previous laws governing foreign investment

1, 2020, the FIL is the ruling law over all existing foreign firms firms are no longer in effect, and existing firms have five years

and all-new foreign firms. Previously existing firms have five to change registration and structure to align with the FIL and

years to change registration and structure to align with the FIL adhere to the PRC company law. The impacts of these new

and adhere to the PRC company law. laws and regulations have yet to be seen; however, with clear

and equal laws and regulations governing foreign and local PE

Conclusion firms, the foreign PE sector may again grow in China.

China’s economy has grown at unprecedented rates, and this References

growth has rapidly expanded the financial system and created

a need for comprehensive regulatory systems. In 1978, China’s Bain & Company. 2019. “Global Private Equity Report.”

transition away from central planning marked the beginning of Baldwin, James G. 2019. “What is the Structure of a Private

the economy’s rapid development. With state-led development, Equity Fund.” Investopedia.

China has implemented: SEZs and FTZs; various development Blackstone. 2020. “Private Equity.”

plans; and governmental incentives in specific industries. Meth- Chen, Lili, and Stan Vinson. 2016. “An Overview of the

ods such as these allowed China to influence development, Chinese Banking System: Its History, Challenges and

including tremendous growth in the economy’s private and for- Risks.” Journal of Business and Economics.

eign sectors. China’s average GDP growth rate was 9.8% from Congressional Research Services. 2020. “’Made in China 2025’

1978-2018. However, this rapid economic growth has not been Industrial Policies: Issues for Congress.”

accompanied by similar regulatory growth for the financial Dresden, Matthew, and Sara Xia. 2020. “How China’s New

system, including the PE industry. Foreign Investment Law Affects You (Or Not).” China

Law Blog.

Private equity firms invest in mature, mid-size to large com- Ernest Young. 2019. “Global IPO trends: Q4 2019.”

panies, which have minimal risk. PE firms take an ownership Fosh, Michael and Katherine Yang. 2017. “A Brief Introduc-

stake of the companies, and the PE firms actively participate tion to PRC Government and Legal Structures.” Reed

in the company’s management to improve its financial perfor- Smith.

mance. PE firms then exit through selling the company or their GuoShi JianZhu. 2019. “Circular of the State Administration

stake in the company. for Market Regulation on Effective Work on Registra-

tion of Foreign-invested Enterprises for the Implemen-

In China, foreign PE firms entered the market before China’s tation of the Foreign Investment Law.” LexisNexis, no.

local PE industry was developed. This has led to foreign and 247.

local PE firms having different laws and regulations. Further, Herbert Smith Freehills. 2018. “Greater China Private Equity

some foreign firms were allowed to enter China if they shared Review.”

their knowledge with local firms. An example of this is the Investopedia. 2020. “Private Equity vs. Venture Capital: What’s

CIC’s 2007 purchase of a 10% share of Blackstone. China’s the Difference.”

foreign and local PE firms share many of the same market JP Morgan. 2019. “Opportunities in Public and Private Equity

interests, specifically healthcare and technology. However, in China.”33 icUJ research article

Latham & Watkins. 2019. “China Introduces New Foreign

Investment Law, Negative Lists, and Encouraged

Industries Catalogue.”

Lawrence, Susan, and Congressional Research Service. 2013.

“China’s Political Institutions and Leaders in Charts.”

Congressional Research Service.

Madi, Maria. 2020. “Private Equity and Venture Capital in

China in the Aftermath of the Sino-American Trade

Disputes.” Global Journal of Emerging Market Econ-

omies.

MOFCOM. 2019. “Case-filing of the Final Review of the

Countervailing Measures against Imports of So-

lar-grade Polysilicon Originating in the United States.”

Ministry of Commerce People’s Republic of China, no.

3.

MOFCOM. 2019. “China Foreign Trade and Economic Coop-

eration Gazette.” Ministry of

Commerce People’s Republic of China, no. 68.

Morrison, Wayne. 2019. “China’s Economic Rise: History,

Trends, Challenges, and Implications for the United

States.” Congressional Research Service.

Preqin. 2019. “Preqin Markets in Focus: Private Equity & Ven-

ture Capital in Greater China’s Innovation Economy.”

PWCCN. 2017. “Innovating with Quality in the New Era.”

———. 2020. “Private Equity Funds Webinar Series.”

The Supreme People’s Court of the People’s Republic. 2019.

“Interpretations of the Supreme People’s Court.” Fa

Shi, no. 20.

Yong, Kwek Ping. 2012. “Private Equity in China: Challenges

and Opportunities.” John Wiley & Sons Singapore Pte.

Ltd.

Zhou, Qian. 2019. “How to Read China’s New Law on Foreign

Investment.” China Briefing from Dezan Shira &

Associates.You can also read