Prospects for Financial and Capital Markets 2nd quarter 2021 - Zurich, 07 April 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Prospects for Financial and

Capital Markets

2nd quarter 2021

Zurich, 07 April 2021

Foreword

The first quarter of 2021 ended more posi- from a very low level, almost doubling, and

tively than many expected. It seems that the within a very short time. Overall, the financial

economy has weathered 2020 less badly than and capital markets have been able to cope

feared and has been able to master the first with the effects well so far. The stock mar-

three months with strength despite continued kets continued their upward trend. But some

uncertainty from the pandemic. The purchas- cracks in the markets are becoming visible.

ing managers' indices (PMI) for the manufac- For example, the stock markets experienced

turing sector in the US and Europe are cur- the "Robinhooders" who, in the case of

rently on excellent levels. The service sector GameStop, drove the price up in an organised

still shows a divided picture depending on the manner, triggering a so-called "short-

regional progress in vaccinating the popula- squeeze" and inflicting material losses on

tion. While the US and the UK are advancing some short sellers. Trading in call options

rather rapidly, vaccination campaigns in con- reached record volumes in the US in February

tinental Europe seem to be struggling. Rela- and towards the end of March a very large

tive to other regions of the world, progress is hedge fund/family office (Archegos) col-

nevertheless notable and likely to gain mo- lapsed, causing billions in losses for some in-

mentum. The Chinese economy took a pause vestment banks. What the three cases have

and the recovery of the global economy is still in common are, in our view, signs of a bull

facing headwinds from struggling supply market that is in its final phase: Concentrated

chains and scarce commodities as a result of positions, very high use of leverage, forced

underinvestment in the previous years. As a liquidation into an illiquid market. Another

result, producer prices are rising sharply. warning sign are the eternally rising real es-

tate prices in the USA.

The political noise has clearly become quieter

since November. Nevertheless, much is hap- For the second quarter, we expect interest

pening. Fiscal policy continues to hold the rates to rise at a significantly slower pace.

wheel firmly in its hands. The US government The higher interest rate level will keep volatil-

is in the process of launching a total of two to ity rather high on the markets. However, the

three substantial programmes with a volume pressure on the fault lines in the system will

of up to USD 6 trillion. The trade conflict be- remain too low for the time being. Thus, the

tween China and the West is increasingly equity markets should manage to hang on for

turning into a conflict over financial and capi- another positive quarter. In the case of gold,

tal markets. Although liquidity seems to be we assume that the bottom will finally be

available more than enough, the battle for in- reached in the next three months.

vestment money has been launched. Mone-

tary policy is currently staying in the back- Bank von Roll Ltd

ground and seems to be letting things run Bleicherweg 37

their course for the time being. CH-8027 Zurich

Economic recovery, rising producer prices

and inflation expectations as well as in-

creased demand for money lead to rising in-

terest rates. In particular, 10-year US interest

rates experienced an increase of around 0.8%

Foreword 2

Strategic cornerstones - Q2 2021

For the 2nd quarter of 2021, our investment policy is guided by the following key points:

The fourth quarter of 2020 performed less poorly than expected and the first quarter of

2021 also surprised positively. Growth estimates were subsequently increased. The

Economy

purchasing managers' indices can also boast excellent values. We expect the strongest

growth in the Asian regions. But the USA should also grow strongly, as vaccine distri-

bution is clearly progressing the fastest there. In Europe, the upswing in services and

consumption is delayed again, but will be more than compensated by a very positive

development in the manufacturing sector.

The focus in the second quarter will continue to be on fiscal policy and thus debt is

Monetary policy

expected to continue to rise. Monetary policy will remain rather passive and reactive.

They will keep an eye on the long-term interest rates determined by market forces. Ac-

tive intervention is only likely to take place if there are signs of a break in the financial

and capital markets, which we do not expect in the second quarter.

The inflation potential is enormous due to the ultra-expansive monetary policy and rec-

ord high debt. Inflation rates have already picked up quite significantly, as we expected,

Inflation

and as a result nominal interest rates have also risen. In the second quarter we expect

the trend to continue in a weakened form. Whether inflation is sustainable will only be-

come clear in the second half of the year.

We expect the following asset class development in the second quarter:

• Equities with positive trend, but higher volatility

Markets

• Commodities should continue to perform positively

• Only slightly rising interest rates after the jump in the first quarter and a wait -and-

see attitude with regard to the further development of inflation. Corporate bonds

should perform slightly better than government bonds.

The long-term drivers are intact and gold continues to be underrepresented in institu-

tional investors' portfolios. We expect a sideways trend and the final phase of the con-

Gold

solidation that has already lasted 8 months. Real interest rates should continue to fall

and support the gold price. We expect prices to be well above USD 2,000 per ounce

when the bottoming phase is complete.

With an increasingly better economic outlook, we had again slightly increased the equity

allocation in the first quarter. Our preference for "old economy" sectors is correct and

Investment strategy

the trend is likely to continue. We consider the weakness of Asian equities to be tempo-

rary.

We are holding on to the overweighting of gold with conviction. The correlation to equi-

ties is negative, which brings diversification effects. Despite the underperformance in

the first quarter, we are positive for the rest of the year.

Bonds offer hardly any earnings prospects. We remain underweighted, focusing on

solid quality and inflation-protected bonds.

We leave foreign currency risks at a relatively low level.

Strategic cornerstones - Q2 2021 3

Strategic asset allocation

Balanced CHF

Asset Class

Liquidity 7%

Fixed Income 30%

Corporate Bonds BBB 15%

Inflation-Protected Government Bonds 15%

Highy Yield Bonds 0%

Equities 48%

Switzerland 15%

Europe 14%

USA 10%

Emerging Markets 6%

Gold Mines 4%

Precious Metals 15%

Currencies

CHF 80%

EUR 10%

USD 5%

Other Currencies 5%

in percent % 10 20 30 40 50 60 70 80 90 100

Our focus for the second quarter of 2021

• We are underweighting this segment. Solid quality and inflation-protected bonds are

preferred.

• We remain positive about the equity markets and keep an overweight position. Value

should continue to outperform growth. We do not expect a major correction yet, but

volatility is likely to increase.

• Growth in expected earnings is highest in Europe. With a relatively late opening of the

economy during the second quarter, stock market advances should be supported. Eu-

ropean equities remain attractive.

• Emerging markets and Asia remain favourites despite a setback in the first quarter after

a strong start, as demographics, rising consumption, an expected weaker USD and tech-

nology/digitisation will provide increased positive momentum.

• The infrastructure sector continues to look positive, especially in the USA. The sector

includes: basic materials, industrial metals, mechanical engineering and capital goods

as well as energy and data infrastructure ("cybersecurity").

• We are maintaining our overweight allocation in gold and gold mining stocks.

Risk factors

• A stronger than expected economic development leads to a rapid rise in interest rates ,

which brings down the highly valued asset classes.

• Uneven distribution of vaccines leads to geopolitical tensions.

• A new strain of the virus emerges that destroys any progress.

• Major social tensions in the USA, political assassination.

• Insolvency phase in the context of the pandemic crisis.

• Food shortages, rising prices of agricultural goods, distribution struggles.

• Large-scale cyberattacks with negative consequences for the internet.

Strategic asset allocation 4

Economic environment

Asynchronous upswing

Covid-19 - Advancing vaccination campaigns, new waves and mutants

While the pandemic has lost influence in the financial

Overall, the situation is improving

and capital markets, it continues to dominate politics,

from month to month. Vaccina-

news and the real economy. The focus is on the pro-

tion campaigns are picking up

gress of vaccines and the seasonal waves. Globally, 10

speed, but new waves of infection

vaccines are currently available, of which 2 are from Eu-

cannot yet be prevented. Herd im-

rope/USA, 2 from USA, 3 from China, 2 from Russia and

munity is illusory for the time

1 from India. From the distribution of approvals, one can

being.

get to some degree the impression of vaccine national-

ism (see graphs and tables in the appendix). Of the large economic blocs, the USA is currently

making the fastest progress. The first states are already beginning to make vaccinations avail-

able to all adults. Although three vaccines are licensed in Europe, vaccination progress is much

slower than in the USA. Relative to the

rest of the world, however, the situa-

tion in Europe is better than it might

appear. There are no figures from

China, but the goal seems to reach a

vaccination coverage of 40% by the

end of June. As expected, the estab-

lished methods (i.e. lock-downs) are

needed for the time being to keep the

risk of new waves and further muta-

tions reasonably under control. In Eu-

rope, but also in India, we can assume

that the spring wave is underway, while

in the southern hemisphere the corre-

sponding autumn wave is underway. It

will be interesting to see whether and

how a new wave will form in the USA in

view of the vaccination progress on the

one hand and a complete opening in a

number of states on the other. The big-

gest and not really tangible risk factor

remains the virus mutations, most re-

cently reported from Brazil and India.

Source: Our World in Data

Overall, the pandemic situation is improving from month to month. The logistical and political

challenges remain high, a pandemic-weary population must be kept happy and risks of more

dangerous mutations exist. For the time being, the goal of vaccination campaigns will have to

be limited to quickly returning people and the economy to a normal life and at the same time

Economic environment 5

drastically reducing the negative aspects (deaths, long-term consequences, burden on the

health system). So-called herd immunity is illusory for the time being.

Economy - Manufacturing as driving factor / Rising producer prices

The latest Purchasing Managers' Indices (PMIs) sug-

The economy continues to sur-

gest that the economy is looking beyond any remaining

prise in the first quarter. Globally

short-term difficulties due to the pandemic. The manu-

oriented manufacturing as a

facturing sector is proving to be the driving force. For

bright spot and consumption im-

example, the German manufacturing PMI in March

proving. Producer prices rise

reached its best value since the financial crisis and the

more than having seen in a long

third best value since the index was calculated. The PMI

time due to several factors.

for the Eurozone as a whole was also convincing and

exceeded expectations for March. In the US, unlike in Europe, the service sector now also seems

to be performing very well. This is likely to be an impact of the faster progress on vaccinations

described above. The weather-related setback in the USA in February was temporary at best.

So-called "nowcast" estimates suggest that

the US is at the beginning of a very strong

growth phase. The PMIs for China currently

signal that the Chinese economy needs to di-

gest the recovery ahead of the other blocs.

Overall, growth in the first quarter is likely to

be better than expected. The difference in the

pace of recovery between manufacturing and

services is due to the more global nature of

the former and the more local nature of the

latter. The trend in the household savings rate

was striking, particularly in the US and Europe,

where it had risen sharply during the pan-

demic. Some of this is expected to flow into

consumption and additionally drive the econ-

omy (so-called pent-up demand). But compa-

nies globally have also built up substantial

savings cushions that offer considerable in-

vestment potential. Better-than-expected

growth is increasingly leading to an imbal-

ance between the supply of and demand for

goods. The PMI reports are peppered with

statements about rising commodity prices,

Source: Refinitiv / Own representation

sharply higher transportation costs, disrupted

supply chains, slower delivery times and increasing backlogs in order processing. The current

shortage of semiconductors (chips) also falls into this context, which is a consequence of the

technologisation during the pandemic and the trade war between the US and China. It will take

some time before additional capacity in all this segments is created. This could inhibit the speed

of the recovery and cause producer prices to rise further.

Overall, we assess the economic outlook as positive. The US economy is currently developing

very dynamically across the board. The planned economic stimulus p rogrammes could even

Economic environment 6

lead to temporarily stronger growth than in China. With the upcoming opening of the economy

in Europe, the consumer segment in this region, which has so far lagged behind, should finally

contribute to growth in the course of the second quarter. The asynchronous upswing should

then turn into a synchronous one. Whether the economy has already fully emerged from reces-

sion is a matter of interpretation. Looking at the current levels of growth and forward-looking

indicators, one can declare the recession over. On the other hand, unemployment figures are

still at a high level in many regions, which is why there is still some way to go before a full

recovery can be achieved. It is therefore not surprising that monetary policy continues to be

supportive and fiscal policy remains expansionary. For the financial and capital markets, a de-

cisive factor will be whether companies can pass on the increased input prices to consumers.

The development of the pandemic remains the biggest risk factor for our positive assessment.

Monetary and Fiscal Policy - Active fiscal policy and reactive monetary policy

Despite declining importance, US monetary policy is still

Biden administration could launch

a globally determining factor due to the USD's position

programmes totalling up to USD 6

as the current leading trade and credit currency.

trillion this year. Monetary policy

Changes in monetary policy or in the interest rate struc-

will have to deal with increasing

ture in the USA also have a certain guiding character.

challenges.

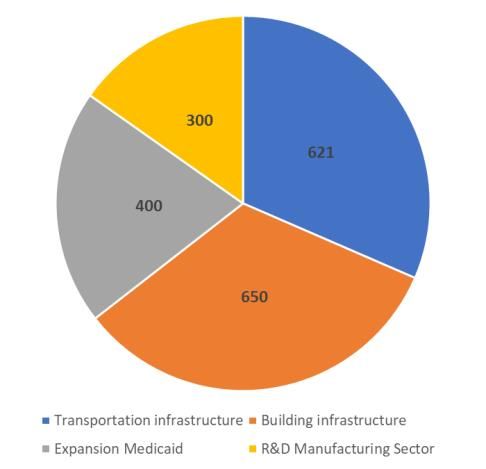

The Biden administration is intensifying efforts to imple-

ment further economic stimulus programmes. Pan-

demic aid to the tune of USD 1.9 trillion was pushed through the Democratic chambers at the

beginning of March. Next up are infrastructure programmes worth at least another USD 2 trillion,

which are likely to have a somewhat tougher time. It is

also possible that student loan debt forgiveness of Biden infrastructure programme in

billion USD

USD 1 trillion could follow. Such substantial pro-

grammes were last launched in the years after World

War II. Today, as then, the primary goal of monetary

and fiscal policy is a quick recovery of the labour mar-

ket and the economy. However, these new pro-

grammes must be financed. At present, the US gov-

ernment is still reducing the available balances at the

US-Fed. But by the third quarter at the latest, it will

have to turn increasingly to the financial and capital

markets again to find financing sources to cover the

immense new debt. There, it will encounter declining

foreign interest in US government securities, thus it

can be assumed that higher interest rates will be

Source: USA Today / Own representation

needed to make the new debt more attractive. Compli-

cating matters are the above-mentioned development of rising prices (inflation), which could be

fuelled by an economic boom at least in the short term, as well as the existing yield curve with

short-term interest rates close to zero and a general rejection in the USA of negative interest

rates. This mix could lead to sharply rising long-term interest rates and undermine the sustain-

ability of government debt, which in turn could lead to rating cuts and even higher interest rates.

As in the 1940s, the key will lie with the US Fed. To counteract this development, the Fed will

probably have to resort to so-called yield curve control ("YCC"), as it did back then, to counteract

Economic environment 7too sharp a rise at the so-called long end of the yield curve. This means a far-reaching abandon-

ment of Fed independence, further growth of the central bank balance sheet (probably to over

USD 10 trillion) and a shift in investments from short- to long-term US government bonds. Since

YCC is unpopular, it will probably take an event of some kind (bond market crash, stock market

crash, US Treasury buyer's strike, etc.) to justify a next level of intervention. Despite its current

strength, the USD is likely to suffer the most from such a possible development. Whether other

economic blocs will stand idly by and watch a collapse in the value of the USD, as was the case

in the past, remains to be seen.

The European Central Bank has so far made no change in its basic monetary policy stance. Of

note was the statement that higher market interest rates could jeopardise the recovery of the

economy, which puts the ECB in a similar position to the US Fed. In addition, fiscal policy has

so far been much less aggressive than in the US, which keeps the pressure on the central bank

high in the short term. As a result, the planned bond purchases for the second quarter were

increased. As a company whose shares are listed on the stock exchange, the Swiss National

Bank presented its balance sheet. Foreign currency reserves increased by another CHF 110 bil-

lion and the balance sheet total is expected to exceed the CHF 1 trillion threshold in the current

year. The annual profit, the provisions for currency reserves and the reserves for distributions

to the Confederation and the cantons, which reached a volume of CHF 84 billion, also rose

sharply. Remarkable for a country with just over 8.7 million inhabitants.

Despite a visibly improving economic situation, the US government under Biden is seizing the

moment to implement further substantial programmes. The infrastructure package of a planned

USD 2 trillion will probably be the subject of much discussion in the second quarter. The focus

will be on possible consequences for taxation. The second half of the year will be more im-

portant, when the US government will have to tap the bond markets again to raise the necessary

money. The first quarter saw the first disappointing auctions of US government bonds, which is

not necessarily positive in view of the enormous need for financing.

Economic environment 8Financial and capital markets

Rising volatility due to interest rates

Financial and Capital Markets - Rising interest rates and rising stock markets

Factors shaping the financial and capital markets in the

Economic hope makes the stock

first quarter were economic hopes and fears of inflation,

markets rise. Rising inflation ex-

rapidly rising long-term interest rates in the USA as well

pectations cause interest rates to

as sector rotation and episodes reminiscent of ex-

rise. Rising interest rates increase

cesses on the stock markets. Especially on the US eq-

volatility in the financial and capi-

uity markets, the performance of the last four quarters

tal markets.

up until the end of March was among the best since the

relevant equity indices came into existence. For example, the current performance from

1.4.2020 to 31.3.2021 of the Dow Jones Industrial of almost 51% was only surpassed in 1899,

1915, 1929 and 1936. A similar 12-month performance was last achieved in 1983, when the

economy was also recovering from a deep recession. Furthermore, there was a lot of talk about

the so-called "Wallstreetbets" (or "Robinhooders", derived from the corresponding free finance

portal), who significantly influenced individual stocks and triggered juicy price jumps, even c aus-

ing hefty losses for one or the other hedge fund. The massive use of options by the "Robinhood-

ers" is remarkable. At the end of the quarter, the focus shifted to a hedge fund (or family office)

that, according to current knowledge, had to engage in a forced liquidation of its equity portfolio

due to record-high margin

calls. The portfolio was appar-

ently built up on highly lever-

aged derivatives with various

banks as counterparties. This

led to sharp corrections in in-

dividual stocks that had previ-

ously seen its prices being

driven upwards and probably

to large losses at at least two

banks (Nomura and Credit

Suisse). But also, in the area of fixed income investments, there was a collapse in a fund that

was active in the area of "supply chain finance", i.e. the financing of short-term trade transac-

tions. All three examples have in common the partly excessive use of either debt or derivative

based financial products, which are the same thing from an economic point of view (so-called

"leverage").

Fixed income

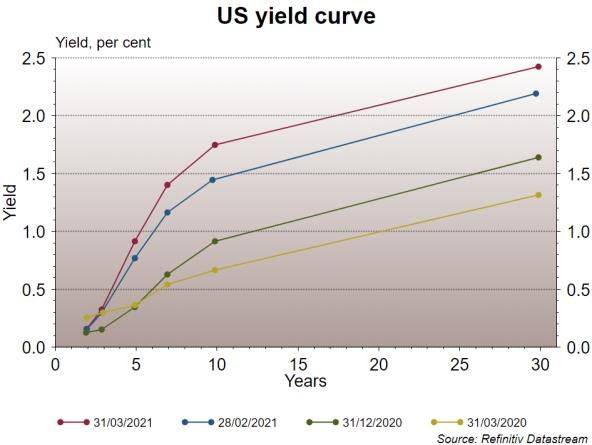

The dominant topic in the first quarter was the development of long-term interest rates in the

USA. In the last quarterly report, we had already pointed out that the yield curve had begun to

steepen due to rising economic optimism and rising inflation expectations. The speed of the

rise in the first three months surprised not only us. In absolute terms, interest rates are still at a

very low level and only the pandemic gap has been filled. However, the consequences of the

higher market interest rates have left clear traces in certain market segments. Long-dated

Financial and capital markets 9bonds in the USD area have suffered signifi-

cant losses. For example, the performance of

the so-called "TLT", an ETF (exchange-traded

fund) on US government bonds with an

average maturity of 20 years, is almost -10%

ytd. Interest rate markets are quite closely

coupled with each other. It is therefore not

surprising that long-term interest rates in

Europe also followed this rise, albeit to a

much lesser extent. The effects were

correspondingly smaller. Nevertheless, the

ultra-long 100-year Austrian government

bond, for example, suffered a loss in value of 26% in the current year. Short-term interest rates

diverged slightly between Europe (slightly higher) and the US (slightly lower) due to the different

pace of pandemic development and vaccine distribution. The dilemma central banks face is the

steepness of the yield curve, which can be seen in the difference between 2-year and 10-year

US-Treasury bonds. In past economic upswings, the difference reached a level of up to 2.5%.

Currently the difference is 1.55%. Since it is no longer possible to lower interest rates at the

short end, the steepening can only occur

due to higher long-term interest rates. Yield difference USD 10yrs

Renditedifferenz USD– 10j

2yrs- 2j

Moreover, long-term interest rates are 4 1

0.9

mainly influenced by market forces, 3

0.8

whereas short-term interest rates can be 2 0.7

controlled more directly by monetary 1 0.6

0.5

policy (see the remarks on "yield curve 0 0.4

control"). In summary, this means that in -1 0.3

light of the current economic upswing a -2 0.2

0.1

level of 10-year US interest rates of around -3 0

2.6% would be quite opportune, i.e.

another 1% higher than at present. We

grey areas = recessions in the USA

doubt that the financial and capital Source: Refinitiv / Own representation

markets can absorb such an increase

without complications.

Despite the recent rise, interest rates in the largest economic areas are likely to remain at a low

level. For the second quarter, we expect only slight further progress in interest rates, as we wait

for the first indications about the further development of inflation and its sustainability. Whether

inflation will also be sustainably higher, which we currently assume, will become clear in the

second half of the year when the year-on-year base effects will subside. The US government's

enormous financing needs will be accentuated from the second quarter onwards. Thus, nothing

should stand in the way of interest rates rising again more strongly in the third quarter. Overall,

it will remain difficult to generate reasonable returns with bonds in 2021. Corporate bonds are

likely to outperform government bonds, and in our view inflati on-linked bonds belong in well-

diversified portfolios. Keep duration short.

Financial and capital markets 10Equities

Overall, the positive trend on the Annual performance of the sectors in the Stoxx Eu-

global stock markets, which has rope 600 as at 29.3.2021

been ongoing since last November, STOXX Europe 600 Automobiles & Parts EUR Price Index 20.50

STOXX Europe 600 Travel & Leisure EUR Price Index 17.79

continued. The rather high volatility in

STOXX Europe 600 Banks EUR Price Index 17.48

individual market segments and STOXX Europe 600 Basic Resources EUR Price Index 12.86

shares was striking. From the STOXX Europe 600 Telecommunications EUR Price Index 11.91

STOXX Europe 600 Insurance EUR Price Index 11.66

perspective of both regions and STOXX Europe 600 Construction & Materials EUR Price Index 11.46

sectors, there was a change in STOXX Europe 600 Technology EUR Price Index 10.88

STOXX Europe 600 Media EUR Price Index 10.42

leadership and economic optimism

STOXX Europe 600 Oil & Gas EUR Price Index 9.92

and rising interest rates left their STOXX Europe 600 Industrial Goods & Services EUR Price Index 8.11

mark. Cyclically sensitive equity STOXX Europe 600 Chemicals EUR Price Index 7.27

STOXX Europe 600 Financial Services EUR Price Index 6.03

markets and sectors were able to STOXX Europe 600 Retail EUR Price Index 5.38

outperform the more defensive and STOXX Europe 600 Personal & Household Goods EUR Price Index 3.72

STOXX Europe 600 Food & Beverage EUR Price Index 2.21

interest rate sensitive sectors quite STOXX Europe 600 Health Care EUR Price Index 1.20

clearly. Shares from the "old STOXX Europe 600 Utilities EUR Price Index -0.67

economy" segment performed STOXX Europe 600 Real Estate EUR Price Index -2.69

Source: Refinitiv / Own representation

significantly better than the

previous stock market favourite, technology. In other words, the value stocks were able to beat

the growth stocks. Furthermore, the shares of small and medium-sized stocks performed better

on average than the shares of the so-called "large caps". In the emerging markets, the high

volatility of Chinese equities stood out. Financial market sanctions by the USA and the Chinese

government's influence on large companies have been weighing on share prices since mid -

February. The problems at the hedge fund/family office mentioned above may also have played

a certain role.

Many equity markets have already been able to outperform an average annual performance in

the first quarter. Historically, it is not particularly unusual for equity markets that are in a strong

upward trend to achieve positive performance for more than 4 quarters in a row; especially when

the economy was in a phase of growth after a recession. We therefore see a good chance for

another positive quarter. However,

rising interest rates meeting high val-

uations will lead to an environment of

continued high volatility especially for

growth stocks. Some technical indi-

cators point to certain signs of fa-

tigue in the equity markets in the

short term. Nevertheless, we do not

expect a possible hot phase on the

equity markets until the course of the

third quarter. We are not making any

significant adjustments to our sector Source: Refinitiv / Own representation

preference. We continue to favour companies from the "old economy", especially those related

to infrastructure. In the meantime, European stocks exhibit the strongest earnings growth ex-

pectations. We consider the Asian economic area to be the region with the strongest sustaina-

ble growth. Despite generally rather high valuations In the USA, attractive investments can still

be found in the value segment. However, our regional focus is on Europe and the emerging

Financial and capital markets 11markets. In financials, we prefer insurance companies. Rising interest rates and steep yield

curves argue for a stronger exposure to banks. However, recent events once again impressively

showed that the risks in banks are hardly discernible and can strike out of nowhere. Inflationary

trends are usually a good environment for equities, as profits, unlike interest rates, are variable.

However, one challenge for companies will be to pass on rising costs to consumers. Those that

fail to do so will have to live with lower margins. Quality companies usuall y find it easier to pass

on higher costs.

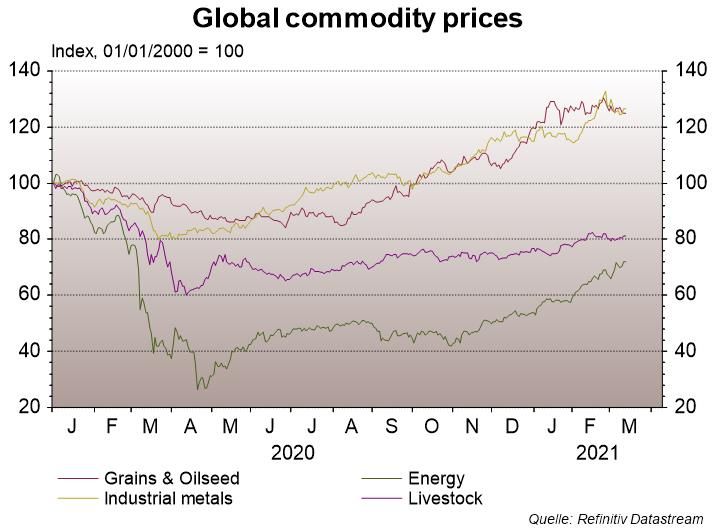

Precious metals and commodities

The better-than-expected development of

the economy and the shift to more sus-

tainable forms of energy production, that

is consuming a lot of basic resources and

industrial metals, is coming up against a

commodity sector that has had to shrink

in recent years at the expense of new in-

vestments. It takes years for new capacity

(mining projects) to come to market. The

result is a supply deficit and consequently

rising prices. Especially in lesser-known

metals, there have already been substan-

tial price increases. Even copper is showing signs of a supply deficit. Some argue that US Pres-

ident Biden was the best thing that could have happened to the oil price. Here they point to the

fact that under Biden oil supply is going to be restricted, which benefits the oil price. The Suez

Canal accident also made us realise the fragility of the already strained global supply chains

after the pandemic. Overall, commodity prices continued the upward trend of the fourth quarter,

led by oil and copper.

The recent decline in gold's relative attractiveness due to rising interest rates, a stronger USD

and economic optimism currently still outweighs the above-described prospects of rising infla-

tion, further growing central bank balance sheets, negative real interest rat es and a potentially

prolonged loss of confidence in paper currencies. Physical gold continues to play a very im-

portant role in maintaining the real purchasing power of a portfolio over the long term. Not only

inflation can destroy the real purchasing power of assets, but also a wave of bankruptcies

caused by deflation. Gold has proven its

worth in both cases. However, there is no

denying that this positioning is currently

weighing on the performance of a portfolio.

We see this as a temporary development; it

remains to be seen when it will end, but

sentiment and capital flows suggest that

we are nearing the end of this phase, which

has already lasted more than seven

months. For us, the situation with inflation

and gold is comparable to the tsunami ef-

fect, where the sea recedes before the tidal

wave reaches land.

Financial and capital markets 12Commodities have already performed much stronger than we anticipated at the beginning of

the year. Increasing supply deficits should continue to support prices. We therefore expect the

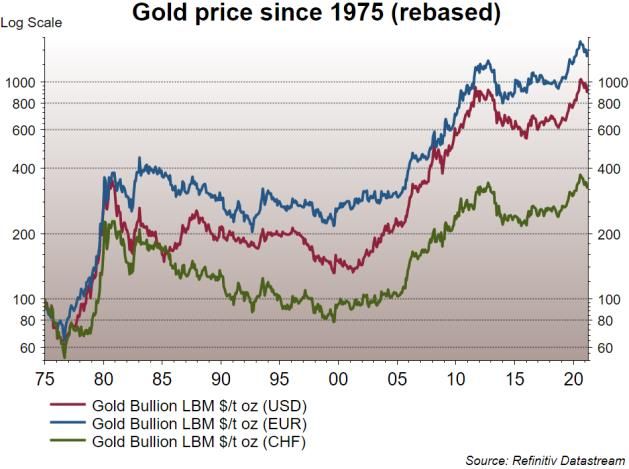

positive trend to continue. After a difficult phase, precious metals – gold and silver – should

soon start to perform better again. From a longer-term perspective, we consider the still ongoing

downward movement to be a trend-confirming consolidation. The next wave is likely to be the

most pronounced and longest, carrying the gold price well above USD 2,000 per ounce. With a

downside risk to the USD 1,650 per ounce range, this seems to us a very attractive risk -return

ratio. The negative correlation of gold to equities should also be mentioned positively, as bonds

now only offer limited protection in view of the existing low interest rates, the inflation outlook

and losses in value when interest rates rise. We also have not changed our opinion on silver and

see this metal as even more attractive due to its industrial use. But silver will not follow a linear

path either.

Currencies

An extremely one-sided attitude in the financial markets often brings the opposite of what was

expected. This is what happened with the USD. We were not alone in thinking that the USD would

depreciate in the face of twin deficits and new debt. Short positions reached record levels. In

addition to purchases due to short-covering, investors were probably also convinced by the ex-

cellent growth prospects, the comparatively rapid progress on vaccinations and rising interest

rates. Thus, USD weakness suddenly turned into USD strength. However, the "strength" mainly

refers to the EUR and some emerging market currencies that are struggling with specific prob-

lems (Turkey and Brazil). One of the weaker currencies was the Swiss franc, which is again less

in demand in an environment supported by economic optimism. In the case of the JPY, inves-

tors must increasingly ask themselves to what extent this currency can still be considered a

safe haven.

We assume that the USD strength is of temporary nature and that with the improvement of the

pandemic situation in Europe, the twin deficits of the USA will come to the fore again. The cur-

rencies will therefore return to the familiar ranges. We see a range of 0.87-0.92 for the USD

against the CHF, 1.07-1.09 for the EUR against the CHF and 1.19-1.25 for the USD against the

EUR. We are fundamentally positive about emerging market currencies due to the long-term

growth advantages, especially in Asia.

Financial and capital markets 13Graphics and tables

Key economic expectations for the year 2021

Source: M.M.Warburg Bank, IMF, ECB, US Fed, KOF, own estimates

Vaccine approvals

globally - April 2021

Source: N.Y.Times

Graphics and tables 14Development of house prices in the USA measured by the S&P Case-Shiller Home Price Index

Development of the GameStop and ViacomCBS shares - To the moon and back again

GameStop ViacomCBS

Source: Refinitiv / Own representation

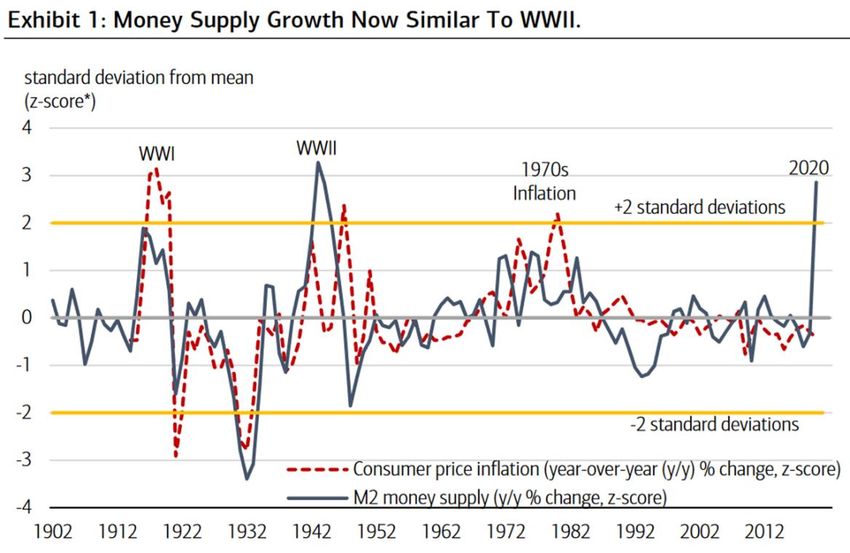

Money supply development and inflation in the USA in long-term comparison

Source: Merrill Lynch

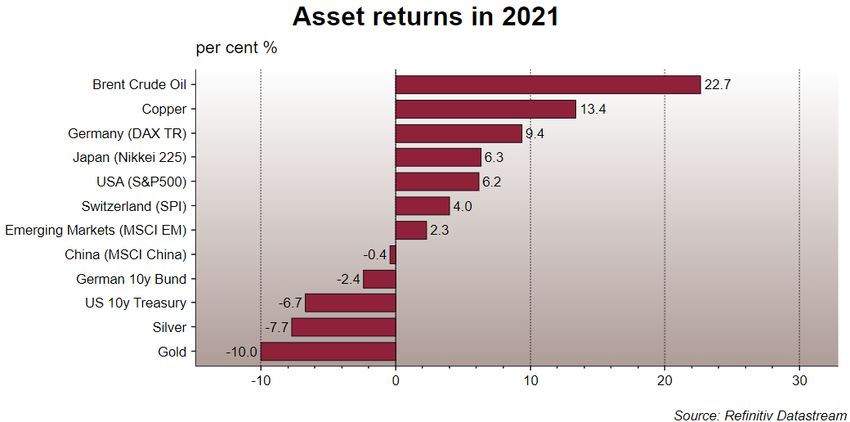

Graphics and tables 15Market Overview 2020

So urce: Reuters per 31.03.2021/ Equity M arkets in lo cal currency

Economic Indicators per Close Close prev. Year YTD

University o f M ichigan Co nsumer Sentiment Index 30.09.2020 79.0 80.7 -1.7

ISM M anufacturing P M I SA 31.03.2021 64.7 60.5 4.2

ISM No n-M anufacturing NM I 31.03.2021 63.7 57.7 6.0

US Leading Indicato r Index 28.02.2021 110.5 109.7 0.8

ZEW Euro zo ne Expectatio n o f Eco no mic Gro wth 31.03.2021 74.0 54.4 19.6

Ifo P an Germany B usiness Climate 31.03.2021 100.4 93.1 7.3

S&P Co reLo gic Case-Shiller 20-City Co mp. Ho me P rice NSA Index

31.01.2021 243.0 240.9 2.1

Currency vs. CHF per Close Close prev. Year YTD

EUR 31.03.2021 1.1070 1.0807 +2.4%

USD 31.03.2021 0.9434 0.8851 +6.6%

GB P 31.03.2021 1.3000 1.2102 +7.4%

SEK 31.03.2021 10.8000 10.7400 +0.6%

JP Y 31.03.2021 0.8520 0.8571 -0.6%

A UD 31.03.2021 0.7168 0.6806 +5.3%

Currency vs. EUR YTD

USD 31.03.2021 1.1732 1.2217 -4.0%

CHF 31.03.2021 0.9038 0.9251 -2.3%

GB P 31.03.2021 1.1751 1.1189 +5.0%

SEK 31.03.2021 0.0977 0.0995 -1.8%

JP Y 31.03.2021 0.7700 0.7926 -2.9%

A UD 31.03.2021 0.6477 0.6298 +2.8%

Equity Markets in local currency per Close Close prev. Year YTD

M SCI Wo rld Index (USD) 31.03.2021 2’ 811.7 2’ 690.0 +4.5%

M SCI Emerging M arkets Index (USD) 31.03.2021 1’ 316.4 1’ 291.3 +1.9%

Do w Jo nes (USD) 31.03.2021 32’ 981.6 30’ 606.5 +7.8%

S&P 500 (USD) 31.03.2021 3’ 972.9 3’ 756.1 +5.8%

Nasdaq Co mpo site (USD) 31.03.2021 13’ 246.9 12’ 888.3 +2.8%

Russell 3000 (USD) 31.03.2021 2’ 382.7 2’ 248.4 +6.0%

B razil B OVESP A (B RL) 31.03.2021 116’ 633.7 119’ 017.2 -2.0%

DA X (EUR) 31.03.2021 15’ 008.3 13’ 718.8 +9.4%

Euro Sto xx50 (EUR) 31.03.2021 3’ 919.2 3’ 552.6 +10.3%

IB EX 35 (EUR) 31.03.2021 8’ 580.0 8’ 073.7 +6.3%

SP I (CHF) 31.03.2021 14’ 015.0 13’ 327.9 +5.2%

SM I (CHF) 31.03.2021 11’ 047.4 10’ 703.5 +3.2%

FTSE (GB P ) 31.03.2021 6’ 713.6 6’ 460.5 +3.9%

RTS (USD) 31.03.2021 1’ 477.1 1’ 424.8 +3.7%

Nikkei 225 (JP Y) 31.03.2021 29’ 178.8 27’ 258.4 +7.0%

China Shanghai Co mp. (CYN) 31.03.2021 3’ 441.9 3’ 473.1 -0.9%

India B SE 30 (INR) 31.03.2021 49’ 509.2 47’ 751.3 +3.7%

A ustralia S&P /A SX200 (A UD) 31.03.2021 6’ 790.7 6’ 587.1 +3.1%

Interest Rates and Bond Markets per Close Close prev. Year YTD

3-M o nth Euribo r 30.03.2021 -0.54% -0.55% 0.00%

10-Years Germany Generic Go vernment 31.03.2021 -0.29% -0.58% 0.28%

10-Years EUR Swap 31.03.2021 0.07% -0.27% 0.34%

3-M o nth ICE USD-Libo r 30.03.2021 0.20% 0.24% -0.04%

10-Years US Generic Go vernment 31.03.2021 1.75% 0.91% 0.83%

10-Years USD Swap 31.03.2021 1.77% 0.92% 0.85%

3-M o nth ICE CHF-Libo r 30.03.2021 -0.76% -0.76% 0.00%

10-Years Switzerland Generic Go vernment 31.03.2021 -0.28% -0.52% 0.24%

10-Years CHF Swap 31.03.2021 0.04% -0.29% 0.33%

IB OXX Euro Go vernment 3-5 Jahre 31.03.2021 211.6 212.5 -0.4%

REX P erfo rmance Index (German Go vernment B o nds) 31.03.2021 493.7 499.2 -1.1%

IB OXX Euro Co rpo rates 3-5 Jahre 31.03.2021 242.3 244.2 -0.8%

Swiss B o nd Index A A A -B B B 31.03.2021 143.2 144.8 -1.1%

Emerging M arkets Hard Currency in USD (ETF) 31.03.2021 108.9 115.9 -6.1%

Emerging M arkets Lo cal Currency in USD (ETF) 31.03.2021 42.6 45.3 -5.9%

CS High Yield Index II 31.03.2021 1’ 512.0 1’ 498.4 +0.9%

Alternative Investments per Close Close prev. Year YTD

VIX-Index (Vo latility S&P 500) 31.03.2021 19.4 22.8 -14.7%

RICI Co mmo dity Index (To tal Return, USD) 31.03.2021 196.6 178.3 +10.2%

Go ld in USD/Oz 31.03.2021 1’ 707.0 1’ 896.5 -10.0%

Go ld in CHF/kg 31.03.2021 1’ 610.6 1’ 680.0 -4.1%

Go ld in EUR/Oz 31.03.2021 1’ 455.2 1’ 553.7 -6.3%

Silver in USD/Oz 31.03.2021 24.4 26.4 -7.5%

Crude Oil B rent USD (Future) 31.03.2021 63.5 51.8 +22.7%

Co pper (Future) 31.03.2021 400.3 351.4 +13.9%

B altic Dry Index 31.03.2021 2’ 046.0 1’ 366.0 +49.8%

HFRX Glo bal Hedge Fund Index (USD) 31.03.2021 1’ 377.9 1’ 292.5 +6.6%

LP X50 (P rivate Equity) 31.03.2021 3’ 420.6 2’ 913.0 +17.4%

Market 16You can also read