Overview OVERVIEW UNDER CONTRUTION

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Overview

April 2019

OVERVIEW

UNDER CONTRUTION

SciPlay Second Quarter Results

Ended June 30, 2019

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE

Agenda

Overview

2019 Second Quarter

Results Review

Why we Win

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 1

Overview

April 2019

OVERVIEW

UNDER CONTRUTION

Overview

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATESciPlay at a Glance

OFFERING 7 CORE GAMES…

$118mm 18%

Revenue Growth

44%

AEBITDA Growth

83%

Mobile Penetration

Revenue (Q2 2019) (Q218 – Q219) (Q218 – Q219)1 (Q2 2019)

$33mm 8.1mm

Average MAUs

6.0%

Payer Conversion

$81.42 AMRPU

AEBITDA (Q2 2019)1 (Q2 2019) Rate (Q2 2019) (Q2 2019)

∼28% 2.7mm

Average DAUs

$0.48 ARPDAUMobile Gaming is Large and Highly Engaging

Mobile Gaming Market Target Audience in the Casual Genre

Target Demographic Casual Games

~$85bn Females/Males, Age 35+

Global mobile and tablet

gaming market in 2019(1)

1.5bn

people played games on

mobile or tablet in 2017(1)

80%

of spend on Apple and Google

Play stores in 2017(2)

Game

3 hrs 35 min Higher

+ Genres + +

spent per day on mobile devices Greater Better

by the average American in 2018(3) Engagement Loyalty Monetization

(1) Source: IDC Worldwide Mobile and Handheld Gaming Forecast, 2019 – 2023. (2) Source: App Annie. (3) Source: eMarketer.

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 4Expanding Market Across Attractive Genres

Further Expansion into …Anchored by Evergreen

Growing Casual Genre… Social Casino

Top Grossing iOS Games’ Rank Trajectory

After Hitting Top 25(4)

Months (After Hitting Top 25)

$85bn 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Mobile Gaming(1) 1

Our Market Opportunity

$30bn

Ranking

Casual (2)

$5bn

Social Casino(3)

100

Social Casino Median All Other Games Median

(1) Source: IDC Worldwide Mobile and Handheld Gaming Forecast, 2019 –2023. Total projected worldwide market in 2019 for smartphone and tablet gaming revenue.

(2) Source: Eilers & Krejcik. Total projected market in 2019 for social casino mobile games and other casual mobile games, such as puzzle, card and match three games.

(3) Source: Eilers & Krejcik. Total projected market in 2019 for social casino mobile games.

(4) Source: App Annie for top grossing games in the US on iPhone (as of October 2018). Includes only games that first achieved top 25 US grossing rank within the time period of 1/1/2012

through 7/1/2017.

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 5Overview

April 2019

OVERVIEW

UNDER CONTRUTION

2019 Second Quarter Results

Review

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE2Q19 Highlights

• SciPlay completed an initial public offering (“IPO”) on May 7th and began

trading on The NASDAQ Global Select Market under the symbol “SCPL”

• Revenue grew 18% to $118 million, which was more than double the market rate

of growth according to Eilers & Krejcik

• Mobile revenue increased 28% to $98 million

• Net income increased $14 million to $26 million; margin of 22%

• AEBITDA grew 44% to $33 million; robust AEBITDA margin of 28%

• Payer conversion rates increased to 6% driven by the growing popularity of our

games and increased interaction with the games by our players as a result of

the introduction of new game features

• Jackpot Party, our largest game by revenue, grew 28% or 3x market growth

driven by improved player engagement and monetization

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 7Revenue up 18% in Q2, to $118M

Revenue growth more than double the industry, and record growth of

24% year-over-year during the month of June

($ in millions)

2Q’ 18 Revenue: $100mm +18% 2Q’ 19 Revenue: $118mm

$114 $118 $118

$105

$96 $98 $100

$91 $95

$80

Q1' 17 Q2 '17 Q3 '17 Q4'17 Q1' 18 Q2 '18 Q3 '18 Q4'18 Q1' 19 Q2 '19

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 8AEBITDA up 44% in Q2 2019

AEBITDA Growing at a Faster Rate than Revenue While the Company

Launches and Invests in Games

($ in millions)

2Q’18 AEBITDA: $23mm(1) +44% 2Q ‘19 AEBITDA: $33mm(1)

$33

$23 $23 $24 $25 $25

$21 $19

$13 $16

Q1' 17 Q2 '17 Q3 '17 Q4'17 Q1' 18 Q2 '18 Q3 '18 Q4'18 Q1' 19 Q2 '19

(1) 2Q2019 AEBITDA and 2Q2018 AEBITDA include intellectual property royalties paid to Scientific Games that will no longer be paid subsequent to the IPO and the entering into of a new IP

Licensing Agreement (as defined in Appendix A). Such royalty expenses were $2.9mm in 2Q2019 and $6.3mm in 2Q2018.

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 9Engaged User Base Driving Results

Payer Conversion

ARPDAU Average MPUs Rate

$0.48 0.5 6.0%

$0.42 0.4 5.4%

2Q18 2Q19 2Q18 2Q19 2Q18 2Q19

Note: Payer conversion rate represents average number of players who made a purchase at least once in a month by average MAUs. “Average MPUs” means average monthly paid

users. “ARPDAU” means average revenue per daily active user.

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 10Annual Revenue Outlook - 2019

For the full year 2019, the company expects

revenue to be in a range of $480 to $490 million

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 11Long-Term AEBITDA Margin Goal

Continue profit margin expansion through strong revenue growth and

operational leverage as games scale and enter growth stage

Goal

>35%

Current

28%

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 12Valuation Gap

Current valuation gap to peer set provides compelling entry point and

significant upside potential

~14x

EBITDA1

~7x

EBITDA1

Peer Set

(1) EBITDA and EBITDA ratio are non-GAAP financial measures that are presented on a supplemental basis. We do not provide reconciliations for forward-looking non-GAAP financial measures

because we cannot forecast and quantify, without unreasonable effort, certain amounts that are necessary for such reconciliations, in cluding [] in its reconciliation of historic numbers, the amount

of which, based on historical experience, could be significant.

Valuations based on FactSet data 7.22.19; peer set represents median valuation; peer set includes Zynga, Tencent, Netmarble and Glu

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 13Overview

April 2019

OVERVIEW

UNDER CONTRUTION

Why we Win

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATESciPlay Platform Built to Scale

GAMES ACROSS MULTIPLE GENRES

FUTURE PIPELINE

User Monetization

Acquisition Engagement

TECHNOLOGY STACK

BREADTH AND DEPTH OF EXPERIENCE

Seamless and Integrated Across Games

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 15Deep and Largely Exclusive Library of Content

Market Leading, Proven Gaming Content Library Leads to Efficient Cost

Structure

1,500+ Titles Large In-House library

3rd Party Brands

Marquee Partnerships

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 16Significant Growth Opportunities

Untapped strategic growth

Selective M&A opportunities

Growth from new

New Models monetization models

8.6% international Continue international

International revenue in 2018

growth and expansion

Historically released 1-2 Develop and scale new

New games games every 12-18

months

social casino and casual

titles

Diversified portfolio of Continue to grow DAU,

Existing games successful games with

strong cohort dynamics

payer conversion and

ARPDAU

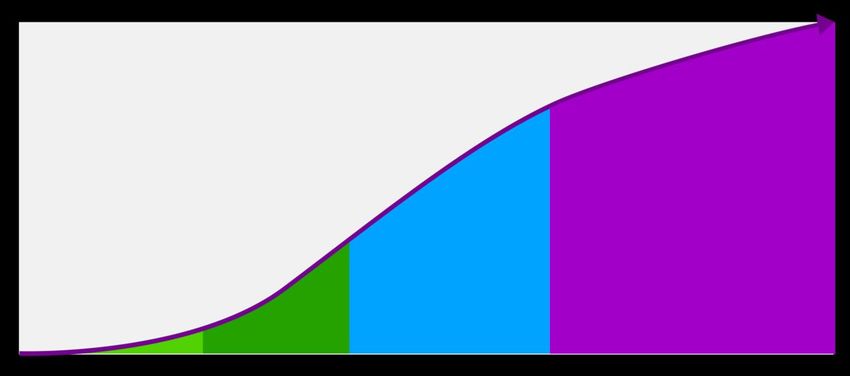

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 17Games in Various Stages of Growth

All Games Go Most Games in Margins Improving as

Though a Similar Early Stages of Games Progress Along a

Life Cycle Life Cycle Predictable Trajectory

FUTURE PIPELINE

Develop Launch Ramp Growth

(9-12 Months) (3-6 Months) (1-1½ Years) (2+ Years)

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 18High Operating Leverage as Games Launch, Ramp and Grow

2018 Percentage Contribution Margin by Game

% Contribution Margin(1)

2017 2014-15(2) 2012

Year Launched

Significant operational leverage as

game scales and enters growth stage

2018

(1) Represents revenue less platform fees, IP royalties, marketing and dedicated game team expenses.

(2) Bingo Showdown acquired by SciPlay in 2017.

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 19Why We Win

Perfect Balance of Art and Science

Superior Game Live Ops Built on a Scalable Platform

Exceptional Monetization Engines Fueled by Data-Driven Approach

Access to a Wealth of Owned and Licensed Authentic IP

Strategic Approach to Market Segmentation and Portfolio Development

Strong Talent Mix Comprised of Industry Veterans

Core Values and Culture of Innovation, Passion and Creativity

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 20Overview

April 2019

OVERVIEW

UNDER CONTRUTION

Appendix

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATEForward-Looking Statements; Additional Notes

Throughout this presentation, we make "forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking

statements describe future expectations, guidance, plans, results or strategies and can often be identified by the use of terminology such as "may,” "will,” "estimate,”

"intend,” "plan,” "continue,” "believe,” "expect,” "anticipate,” "target,” "should,” "could,” "potential,” "opportunity,” "goal” or similar terminology, and include, without

limitation, SciPlay's revenue guidance for full year 2019. These statements are based upon management’s current expectations, assumptions and estimates and are not

guarantees of timing, future results or performance. Therefore, you should not rely on any of these forward-looking statements as predictions of future events. Actual

results may differ materially from those contemplated in these statements due to a variety of risks and uncertainties and other factors, including, among other things: our

ability to attract and retain players; our reliance on third-party platforms; our dependence on the optional purchases of virtual currency to supplement the availability of

periodically offered free virtual currency; our ability to continue to launch and enhance games that attract and retain a significant number of paying players; our

reliance on a small percentage of our players for nearly all of our revenue; our ability to adapt to, and offer games that keep pace with, changing technology and

evolving industry standards; competition; the impact of legal and regulatory restrictions on our business, including significant opposition in some jurisdictions to interactive

social gaming, including social casinos, and how such opposition could lead these jurisdictions to adopt legislation or impose a regulatory framework to govern

interactive social gaming or social casinos specifically, and how this could result in a prohibition on interactive social gaming or social casinos altogether, restrict our

ability to advertise our games, or substantially increase our costs to comply with these regulations; laws and government regulations, both foreign and domestic, including

those relating to our parent, Scientific Games Corporation, and to data privacy and security, including with respect to the collection, storage, use, transmission, sharing

and protection of personal information and other consumer data, and those laws and regulations that affect companies conducting business on the internet, including

ours; the continuing evolution of the scope of data privacy and security regulations, and our belief that the adoption of increasingly restrictive regulations in this area is

likely within the U.S. and other jurisdictions; our ability to use the intellectual property rights of our parent, Scientific Games Corporation, and other third parties, including

the third-party intellectual property rights licensed to Scientific Games Corporation, under our intellectual property license agreement ("IP License Agreement”) with our

parent; protection of our proprietary information and intellectual property, inability to license third-party intellectual property and the intellectual property rights of others;

security and integrity of our games and systems; security breaches, cyber-attacks or other privacy or data security incidents, challenges or disruptions; reliance on or

failures in information technology and other systems; our ability to complete acquisitions and integrate businesses successfully; our ability to pursue and execute new

business initiatives; fluctuations in our results due to seasonality and other factors; dependence on skilled employees with creative and technical backgrounds; natural

events that disrupt our operations or those of our providers or suppliers; risks relating to foreign operations, including the complexity of foreign laws, regulations and

markets; the uncertainty of enforcement of remedies in foreign jurisdictions; the effect of currency exchange rate fluctuations; the impact of foreign labor laws and

disputes; the ability to attract and retain key personnel in foreign jurisdictions; the economic, tax and regulatory policies of local governments; and compliance with

applicable anti-money laundering, anti-bribery and anti-corruption laws; U.S. and international economic and industry conditions; changes in tax laws or tax rulings, or the

examination of our tax positions; litigation and other liabilities relating to our business, including litigation and liabilities relating to consumer protection, gambling-related

matters, employee matters, alleged service and system malfunctions, alleged intellectual property infringement and claims relating to our contracts, licenses and

strategic investments; restrictions and covenants in debt agreements, including those that could result in acceleration of the maturity of our indebtedness; failure to

maintain adequate internal control over financial reporting; influence of certain stockholders, including decisions that may conflict with the interests of other

stockholders; our ability to achieve some or all of the anticipated benefits of being a standalone public company; our dependence on distributions from SciPlay Parent

Company, LLC to pay our taxes and expenses, including substantial payments we will be required to make under the Tax Receivable Agreement; and stock price

volatility.

Additional information regarding risks and uncertainties and other factors that could cause actual results to differ materially from those contemplated in forward-looking

statements is included from time to time in our filings with the SEC, including the company’s current reports on Form 8-k and quarterly reports. Forward-looking statements

speak only as of the date they are made and, except for our ongoing obligations under the U.S. federal securities laws, we undertake no and expressly disclaim any

obligation to publicly update any forward-looking statements whether as a result of new information, future events or otherwise.

You should also note that this presentation may contain references to industry market data and certain industry forecasts. Industry market data and industry forecasts are

obtained from publicly available information and industry publications. Industry publications generally state that the information contained therein has been obtained

from sources believed to be reliable, but that the accuracy and completeness of that information is not guaranteed. Although we believe industry information to be

accurate, it is not independently verified by us. In general, we believe there is less publicly available information concerning international social gaming industries than

the same industries in the U.S. Some data is also based on our good faith estimates, which are derived from our review of internal surveys or data, as well as the

independent sources referenced above. Assumptions and estimates of our and our industry's future performance are necessarily subject to a high degree of uncertainty

and risk due to a variety of factors, including those described in the company’s quarterly reports on Form 10-Q. These and other factors could cause future performance

to differ materially from our assumptions and estimates.

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 22Non-GAAP Financial Measures Adjusted EBITDA, or AEBITDA, as used herein, is a non-GAAP financial measure that is presented as supplemental disclosure and is reconciled to net income as the most directly comparable GAAP measure as set forth in the below table. We define AEBITDA to include net income attributable to SciPlay before: (1) net income attributable to noncontrolling interest; (2) interest expense; (3) income tax (benefit) expense; (4) depreciation and amortization; (5) contingent acquisition consideration; (6) restructuring and other, which includes charges or expenses attributable to: (a) employee severance; (b) management changes; (c) restructuring and integration; (d) M&A and other, which includes: (i) M&A transaction costs; (ii) purchase accounting adjustments; (iii) unusual items (including certain legal settlements) and (iv) other non-cash items; and (e) cost-savings initiatives; (7) stock-based compensation; (8) loss (gain) on debt financing transactions; and (9) other expense (income) including foreign currency (gains) and losses. AEBITDA margin, as used herein, represents our AEBITDA (as defined above) as a percentage of revenue. AEBITDA margin is a non-GAAP financial measure that is presented as supplemental disclosures for illustrative purposes only and is reconciled to net income attributable to SciPlay, the most directly comparable GAAP measure. The Company’s management uses the following non-GAAP financial measures in conjunction with GAAP financial measures: Adjusted EBITDA, or AEBITDA and AEBITDA margin. These non-GAAP financial measures are presented as supplemental disclosures. They should not be considered in isolation of, as a substitute for, or superior to, the financial information prepared in accordance with GAAP, and should be read in conjunction with the Company’s financial statements filed with the SEC. The non-GAAP financial measures used by the Company may differ from similarly titled measures presented by other companies.Our management uses AEBITDA and AEBITDA margin to, among other things: (i) monitor and evaluate the performance of our business operations; (ii) facilitate our management’s internal comparisons of our historical operating performance and (iii) analyze and evaluate financial and strategic planning decisions regarding future operating investments and operating budgets. In addition, our management uses AEBITDA and AEBITDA margin to facilitate management’s external comparisons of our results to the historical operating performance of other companies that may have different capital structures and debt levels. Our management believes that AEBITDA and AEBITDA margin are useful as they provide investors with information regarding our financial condition and operating performance that is an integral part of our management’s reporting and planning processes. In particular, our management believes that AEBITDA is helpful because this non-GAAP financial measure eliminates the effects of restructuring, transaction, integration or other items that management believes have less bearing on our ongoing underlying operating performance. Management believes AEBITDA margin is useful as it provides investors with information regarding the underlying operating performance and margin generated by our business operations. CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 23

Relationship with Scientific Games Post-IPO

In connection with the IPO, SciPlay entered into new intercompany agreements

with Scientific Games covering back office support services, Scientific Games IP

and third party IP

Support Services: Scientific Games provides back office support services (e.g. finance, HR, IT) with fee

based on usage. Fee now in range of $5M - $6M per year – expected to stay in that range or decline

over time

Scientific Games IP: We paid $255M for 1) a perpetual, exclusive, non royalty-bearing license to use all

Scientific Games IP existing, created or acquired before the third anniversary of the IPO in our existing

and future social games and 2) a non-exclusive, perpetual, non-royalty bearing right to use Scientific

Games IP created or acquired after the third anniversary of the IPO in our existing games, in each

case, subject to certain exceptions. We also expect to receive a right of first negotiation to convert

non-exclusive licenses to exclusive licenses and to purchase rights outside of those already purchased

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 24GAAP to Non-GAAP Reconciliation

Years Ended December

Quarterly

31,

($ in millions) Q1'17 Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1’19 Q2’19 2017 2018

Net income (loss) attributable

$4.4 $8.5 $4.7 $5.5 ($1.1) $12.2 $9.2 $18.7 $13.7 $12.3 $23.1 $39.0

to SciPlay

Net income attributable to

- - - - - - - - - 13.9 - -

noncontrolling interest

Net income (loss) $4.4 $8.5 $4.7 $5.5 ($1.1) $12.2 $9.2 $18.7 $13.7 $26.2 $23.1 $39.0

Contingent acquisition

- - - - 18.0 - 8.4 1.1 0.3 1.4 - 27.5

consideration

Restructuring and other 0.2 0.1 - - 0.1 - 0.6 0.3 0.3 0.2 0.3 1.0

Depreciation and

2.4 3.2 5.7 5.7 5.8 5.8 1.7 1.8 1.7 1.8 17.0 15.1

amortization

Other expense (income), net 1.3 1.4 (0.2) 0.1 (0.1) 0.7 0.2 (3.8) 1.6 0.4 2.6 (3.0)

Income tax expense (benefit) 4.0 7.0 4.0 7.1 (0.6) 3.7 2.8 4.5 4.7 (0.7) 22.1 10.4

Stock-based compensation 1.0 1.1 1.6 0.6 0.6 0.7 0.8 1.9 2.7 3.9 4.3 4.0

AEBITDA $13.3 $21.3 $15.8 $19.0 $22.7 $23.1 $23.7 $24.5 $25.0 $33.2 $69.4 $94.0

% AEBITDA margin 16.7% 23.4% 16.6% 19.9% 23.3% 23.2% 22.5% 21.5% 21.1% 28.1% 19.2% 22.6%

Net income (loss) $4.4 $8.5 $4.7 $5.5 ($1.1) $12.2 $9.2 $18.7 $13.7 $12.3 $23.1 $39.0

% Net income (loss) margin 5.5% 9.3% 4.9% 5.8% (1.1%) 12.2% 8.7% 16.4% 11.6% 22.2% 6.4% 9.4%

Revenue $79.8 $91.0 $95.1 $95.5 $97.5 $99.7 $105.3 $113.7 $118.4 $118.1 $361.4 $416.2

CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 25Licensor Legends ANCHORMAN™ ©2019 Paramount Pictures. All Rights Reserved. BATTLESHIP is a trademark of Hasbro and is used with permission. © 2019 Hasbro. All Rights Reserved. Licensed by Hasbro. BETTY BOOP ©2019 King Features Syndicate, Inc./Fleischer Studios, Inc. ™ Hearst Holdings, Inc./Fleischer Studios, Inc. JAMES BOND, , and all other James Bond related materials © 1962-2019 Danjaq, LLC and Metro-Goldwyn-Mayer Studios Inc. JAMES BOND, , and all other James Bond related trademarks are trademarks of Danjaq, LLC. All Rights Reserved. CHEERS™ © 2019 CBS Studios Inc. CHEERS and related marks are trademarks of CBS Studios Inc. All Rights Reserved. Cirque du Soleil and KOOZA are trademarks owned by Cirque du Soleil and used under license. © 2007 Cirque du Soleil. All rights reserved. Licensed by Cirque du Soleil. CLUE and all related characters are trademarks of Hasbro and are used with permission. © 2019 Hasbro. All Rights Reserved. Licensed by Hasbro. DEAN MARTIN™ © The Dean Martin Family Trust 2019. Used with permission. All rights reserved. Dean Martin™ is a trademark of the Dean Martin Family Trust. JOHNNY CASH™ ©2019 John R. Cash Revocable Trust. Used with permission. All rights reserved. "Johnny Cash" is a registered trademark of the John R. Cash Revocable Trust. The Skull/KISS Depot Army Logo™ ©2019 Kiss Catalog Ltd. All rights reserved. LOTERIA ™/©: Licensed by Don Clemente, Inc. 2019. All rights reserved. MARGARITAVILLE™ © 2019 Margaritaville Enterprises, LLC. All rights reserved. MARGARITAVILLE is a registered trademark of Margaritaville Enterprises, LLC and is used under license. Michael Jackson™; Rights of the Publicity and Persona Rights: Triumph International, Inc. © 2019 Triumph International, Inc. Licensing Representative: Authentic Brands Group, LLC. The MONOPOLY name and logo, the distinctive design of the game board, the four corner squares, the MR. MONOPOLY name and character, as well as each of the distinctive elements of the board, cards, and the playing pieces are trademarks of Hasbro for its property trading game and game equipment and are used with permission. © 2019 Hasbro. All Rights Reserved. Licensed by Hasbro. OUIJA is a trademark of Hasbro and is used with permission. © 2019 Hasbro. All Rights Reserved. Licensed by Hasbro. Star Trek: TM & © 2019 CBS Studios Inc. All rights reserved. STAR TREK and related marks are trademarks of CBS Studios Inc. Tetris™ & © 1985-2019 Tetris Holding. THE FLINTSTONES™ and all related characters and elements © & ™ Hanna-Barbera. (s19) THE GAME OF LIFE is a trademark of Hasbro and is used with permission. © 2019 Hasbro. All Rights Reserved. Licensed by Hasbro. The Godfather™ and © 2019 Paramount Pictures. All Rights Reserved. WONDER WOMAN and all related characters and elements © & ™ DC Comics. (s19) YAHTZEE is a trademark of Hasbro and is used with permission. © 2019 Hasbro. All Rights Reserved. Licensed by Hasbro. Other intellectual property, including the look and feel of the games and certain individual components and displays are trade dress of Scientific Games Corp. and its Subsidiaries. TM and © 2019 Scientific Games Corp. and its Subsidiaries. All rights reserved. CONFIDENTIAL & PROPRIETARY – DO NOT DISSEMINATE PAGE 26

You can also read