Reports - Sponsored by - Sifted

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Reports

Sponsored by

Questions? Feedback?

Would you like to partner with Sifted on

the next repport into your sector?

Or help us profile your emerging tech hub?

Get in touch with Christopher Sisserian,

head of Sifted Intelligence via chris@sifted.eu

FINTECH UNWRAPPED 1

2 SIFTED REPORTS

Fintech

every

y where

An unseen army of software startups is

democratising financial services.

From social media companies launching digital currencies to ride-hailing platforms lending to

their drivers, financial services have moved from something your bank does to a facility you can find

everywhere. The early revolution came from the payment platforms that made e-commerce viable,

most obviously PayPal. More recently, the consumer-facing digital banks delighted customers with

their neat design, excellent user experience, service perks and rapid onboarding. Alongside them

came an explosion of apps offering financial conveniences; from consolidating pension pots to

providing more accessible investing, or digitising invoices, giving consumers and companies alike

greater visibility and control over their finances. Today, thanks to a combination of Europe’s new

open banking rules, improvements in software Application Programming Interfaces (APIs) and the

harnessing of machine learning and analytics, a larger ecosystem of startups is bringing financial

capabilities to the wider economy.

Across geographies, fintech is becoming ubiquitous — but in different ways. Asia has produced

financial ‘super-apps’ led by the likes of China’s Ant Financial, Paytm in India and Gojek in Indonesia,

through which consumers do everything from food delivery to loans to booking on-demand

massages. In the US, the story is dominated by the plans of big tech companies — especially Amazon,

Google, Apple and Facebook — to move deeper into financial services. North America has also

produced the payments titans, like Square, Stripe and Toronto-based Shopify, whose infrastructure

has brought financial capabilities to millions of companies and merchants. Meanwhile Snap, which

counts Tencent as an investor, is currently showing signs of following the super-app model.

FINTECH UNWRAPPED 3

Europe has lagged behind Asia and the US across many tech sectors, but in finance it is hoping

for more than a bronze position, having produced trend-setting neobanks like Monzo and Revolut,

which are now taking their businesses global. The continent — particularly in London — is also

producing another set of startups whose contribution is lesser known, but whose implications are

far greater: we call them the ‘Fintech Enablers’ — software companies building tools to democratise

banking and bring financial capabilities to all companies.

The Enablers are liberating Europe’s incumbent banks from their costly legacy systems, allowing

them to focus more on customer service innovation. They help challenger banks come to market

faster by providing them with core chunks of the banking technology ‘stack’ — or all of it — such

as compliance, authentication and payment processing. Most importantly, by turning financial

services into modular software, the Enablers will let every company become a fintech of sorts, either

by vastly improving their own financial management, or by extending their value proposition to

customers in new ways. This report, sponsored by Plaid, provides a definitive breakdown of Europe’s

Enablers that are working behind the scenes to build the infrastructure making fintech ubiquitous.

THE EVOLUTION OF BANKING

TRADITIONAL MODEL

PAST 10-20 YEARS

EMERGING MODEL

Branches

and bankers Web

and mobile

Third party

applications

SOURCE: Plaid

4 SIFTED REPORTS

Contents

5

Covid-19: Digital finance, accelerated

From digitising invoices to the retail investment boom, the pandemic

is quickening the transformation of consumer and enterprise finance

10

Opening up finance

A Q&A with Eric Sager, chief operating officer at Plaid, on how fintech

innovation is democratising finance

13

Banking on software

How Europe’s incumbents are partnering with fintechs to divest of

their legacy infrastructures

19

Disrupters under the hood

White label banking services are democratising fintech, allowing

challenger banks to quickly set up shop

27

Open up: Europe’s activist regulators

How Europe’s regulators made open banking a reality - and where

they are heading next

32 Conclusion

Love the plumbers

FINTECH UNWRAPPED 5

Covid-19:

Dig

g ital finance,

accelerated

The global pandemic has forced citizens

and businesses to embrace digital financial

services at unprecedented speed, laying the

foundations for a new era in fintech.

6 SIFTED REPORTS

D uring the last European

and North

pandemic, the telephone came

American

digitise has had to remedy that

sharply. Companies pushed

through years of digital transition

digitisation because they want to

cut costs or accelerate cash flow.”

For the companies building

into its own for those who could in a matter of weeks as they shifted software that improves financial

afford it. But as Spanish flu spread, to distributed structures. management, the pandemic is a

so many telephone operators “We saw all the trends underway huge opportunity. In April alone,

became ill from working in close before Covid-19,” Michele Likvido, the Copenhagen-based

proximity that their companies Foradori, an investment manager automated invoice collection

pleaded with customers to only at European venture capital firm startup, took on 300 more

make emergency calls. BlackFin Tech, tells Sifted, “the customers and doubled its sales.

Fast forward to today’s pandemic is accelerating them.” “Our conversion rates from cold

pandemic, and our digital The pandemic has proven calls increased three times during

telecommunications to be an opportunity, even if the pandemic,” says chief executive

“We saw all infrastructure has under duress, to finally fix all of Max Frimmer.

been our saving the inefficient manual and even Digital invoicing is especially

the trends grace, allowing paper-based processes to which important at a time when many

underway millions of people companies were still often stuck. suppliers and partners are going

before to continue working “You’d be surprised how many bust — or are about to. French

and socialising, companies still have files full of software company Sidetrade,

Covid-19” which also digitises invoices and

albeit at a distance, different coloured papers in their

Michele Foradori and helping to offices, full of paid and unpaid cash systems, claims that unpaid

avert a complete invoices,” Foradori adds. “Suddenly invoices owed to its clients have

shutdown. Any business yet to companies see the value of jumped by 97.6%, from 19.3%

% INCREASE OF UNPAID INVOICES SINCE PANDEMIC

SOURCE: Sidetrade

FINTECH UNWRAPPED 7

FOUNDED: 2011

FOUNDERS: Daniel Klein, Jan

Deepen, Marc-Alexander

Christ, Petter Made, Stefan

Jeschonnek Consumers, too, are quickly 10% of consumers in Britain and

HQ: London shifting their behaviour. Their 17% in Italy have used online

relationship with cards is banking, contactless payments

TEAM SIZE: 2,000+

changing, with reluctance to use and wallets for the first time since

MONEY RAISED: €500m

shared chip-and-pin terminals lockdowns began. Chime, a digital

MARKETS: 32 including driving an increase in contactless bank, has onboarded record

Europe, US and Brazil payments. At SumUp, the London- numbers of customers, while

HOW MANY CLIENTS: Over 2m based software company that direct deposit volumes at Square,

globally digitises payments for SMEs that the US-based payments company,

are reliant on cash payments, vice increased threefold between

president for Europe Alexander March and April.

WHAT IT DOES: von Schirmeister has seen a “The speed of adoption of

Sumup is a payments noticeable trend. In France, cashless payment technology has

provider. The company contactless payments have gone increased dramatically in just three

enables businesses to from 46% of all card payments to months,” says Pär Hedberg, chief

accept card payments in executive of Sting, the Swedish

nearly 60% since the start of the

multiple ways.

lockdown, he tells Sifted. accelerator and incubator. “But

WHY IT’S INTERESTING: In Germany, the use of we need to move faster

SumUp is the only company contactless payments has jumped now, to leapfrog over

to offer an end-to-end after supermarkets and chemists credit cards to touchless

“The speed

EMV card acceptance of adoption

began asking people to pay by payment systems.”

solution built on proprietary

hardware.

card if possible. Major retailers and Hedberg believes that of cashless

small grocery stores have done the growth of e-gaming,

entertainment and

payment

the same, and even cash-loving

German consumers are switching sports will accelerate technology

to 38.1%, making for its busiest to plastic. the payment solution has increased

period since the financial crisis. The trend is global. In market more than the

dramatically

European software companies early March, the World Health current surge in online

are adapting their own offerings, Organisation (WHO) advised retail and food delivery. in just three

and pricing, to support rapid against using physical cash “Cards are a months”

adoption. In March, Sidetrade and recommended making stepping-stone,” agrees

Pär Hedberg

launched a free cash control contactless payments to reduce Dr Francesc Rodriguez

service for new clients that will virus transmission. Since then, Tous, a lecturer in

operate until the end of June. use of cash has fallen dramatically banking at Cass Business School.

“Typically, it takes 12 to 16 weeks — by as much as 90% in Spain. “It’s going to be more about

to implement our systems with In the UK, at the beginning of online transactions in a cashless

clients; we created one without the lockdown, ATM transactions were society, where there is no need

bells and whistles in one week,” down by as much as 62% year on for a card.” For most consumers,

says David Turner, chief marketing year, according to data from Link, the phone is replacing the card. In

officer. Once clients digitise, which runs the UK’s cash machine Sweden, Swish, the bank-owned

Turner says, they never go back. network. telephone banking app, has seen

If a system is easier, faster and At home, more people are a rise in users from 7m to nearly

cheaper to operate than one that paying for goods and services 7.5m — which means that almost

relies on vast quantities of paper, online to be delivered directly. all of the Swedish population old

no one will revert to their old ways. Research from Forrester shows enough to have a bank account is

8 SIFTED REPORTS

now on Swish. If we are using our consolidate their financial lives. also saving more, says Henrik

phones more for banking, we’ll London-based PensionBee, for Rosvall, Dreams’ chief executive.

likely use them for other financial instance, transfers old pensions “People who were saving for a kite

services too. The logic of having into a single online repository. surfing trip or yoga

everything in one place in a single Wealth management and robo- retreat last spring are

app, particularly at a time when advisory platforms can provide now setting up buffers,

“Everyone

life is exceptionally complicated, detailed savings projections and putting money aside is having a

is proving a winning formula with even guide consumers about for their children.” harder time

consumers. how much they need to put away Tara Reeves, partner

financially

Even Asia, ahead of Europe to meet specific future spending at Omers Ventures,

when it comes to moving from goals. Startups like Nutmeg pride thinks the pandemic since the

cash to digital payments, thanks themselves on far greater fee will lead to a number of pandemic,

to the ‘super-app’ phenomena transparency than old-school retail changes in the overall

particularly

led by WeChat Pay and Alipay, investment platforms. packaging of financial

has seen this trend accelerate There is growing demand services. “Everyone is those

during the pandemic. Consumer during the current crisis for clarity having a harder time approaching

attitudes and retail patterns may over our financial future, and tools financially since the

retirement”

be different, but the trend towards that help us to save and invest. pandemic, particularly

consolidating everything financial Young people are increasingly those approaching Tara Reeves

in one place may follow here. being helped to save more thanks retirement,” she says.

to easy-to-use savings platforms. “There are also signs that the bank

Stockholm-based Dreams, an app of Mum and Dad is taking a knock.”

ALL TOGETHER NOW

aimed at encouraging savings and She predicts that mortgage

Thanks to open banking investment, has seen an 11% jump lenders will have to change their

regulations (see last article in this in new users since March 1. Existing products to appeal to people in

report), there is now a community customers are also making more changed circumstances. Gifts

of startups helping users transactions, suggesting they are have been an important source

of capital for the deposits of first-

time buyers for some time — over

the last five years, 61% of first-

time buyers relied on help from

their families. But with less family

money available, Reeves expects

more first-time buyers to buy

with friends, and a ready market

of apps offering and managing

shared mortgages.

To her, one of the more

surprising effects of the pandemic

has been the surge in retail

investment in stock markets. A

report by the French stock market

regulator showed that retail

investors’ transaction volumes

Image: SumUp

have increased four times sinceFINTECH UNWRAPPED 9

it’s less surprising that low-cost 200 years.” When it comes to

investment fintechs, such as protecting personal data, most

Nutmeg, Trade Republic and individuals trust their bank more

Freetrade, have benefited. than any organisation other than

their employer.

With uncertainty comes a

TRUST PREMIUM

greater need for advice, argues

But this doesn’t mean paying Johan Näs, managing director

for financial advice is about to and partner at Boston Consulting

come to an end, warn some Group’s Stockholm office. It’s too

Tara Reeves,

Omers Ventures commentators. This is particularly soon to write off the banks, he

clear in conventional banking, says, and several seem to be doing

although the message is relevant well in the pandemic, particularly

the start of the pandemic, with for other financial services. A those who innovated and invested

over €3.5bn net flowing into recent survey by Forrester found in their customer service. One

equities. Some 27% of French stock that some customers are actually thing is clear: the pandemic is

market investors were new to the switching away from digital banks driving the expectations and

market or previously inactive. back to their original bank. “In needs of consumers ever deeper

New investors were 10-15 years difficult times, who are you going into the digital realm, unlocking a

younger than traditional investors to trust?” asks Forrester analyst huge fintech market opportunity

and below 40 years on average. Jacob Morgan. “You’ll trust a for the companies best positioned

Given this trend, however, bank that has been around for to compete.

NEW BROKERAGE ACCOUNTS

SOURCE: Andreessen Horowitz / Company Filings10 SIFTED REPORTS

Op

p ening

g up

finance

Q&A with Eric Sager,

chief operating officer at Plaid.

and Pandle, and, as part of its important and you are seeing that

expansion into Ireland, France, in the rise in traffic on fintech apps.

Spain and the Netherlands, will There’s been a massive migration

support integrations into banks that, in my mind, would have

including AIB, Santander and BNP happened over the next four or

Paribas. How does the company five years, but has been greatly

see Europe’s fintech ecosystem compressed. Behaviours are

evolving? How is the Covid also changing. For instance, until

pandemic influencing financial now, consumers have been very

behaviour? Sifted talked with reluctant to do their mortgages

Eric Sager, Plaid Plaid’s chief operating officer digitally. Because of Covid, they

Eric Sager about the shift to are discovering

open finance and how opening digital platforms

California-based Plaid is one up financial services further will now, and finding they

“There are

of the fintech infrastructure unleash a new wave of innovation can do a mortgage huge

innovators enabling the open — and give more people access application in 10 frictions in

banking revolution. Its platform to services they’ve been excluded minutes. Before,

financial

connects over 2,600 apps to from. there was this sense

11,600 financial institutions, of ‘If I don’t go to a transactions

Sifted: Right now, the

across the domains of personal branch, if I don’t get and practices

Covid-19 pandemic is upending

finance, payments, lending, help from someone

all aspects of our lives. How do which we can

wealth management and business to walk me through

finance. The $5.3bn fintech is

you see it changing fintech and

it all, how could I eliminate”

financial services?

highly regarded by the many possibly do a home

developers building the APIs that ES: The pandemic is definitely loan?’ Once you’ve done it, I have

are driving today’s boom in fintech accelerating the digitisation of a hard time believing anyone is

services. financial services. As branches going to go back to the world

Since coming to Europe via a are either closed or as people where you had to print out all this

UK launch early in 2019, Plaid has are more hesitant to go, digital paper and spend hours in a branch

picked up clients including Cleo solutions have become much more sorting it out.FINTECH UNWRAPPED 11

FOUNDED: 2013

FOUNDERS:William Hockey,

Zachary Perret

HQ: San Francisco

TEAM SIZE: 550+

MONEY RAISED:$310m

($5.3bn acquisition by Visa

pending)

FINANCIAL SERVICES LINKED:

11,000+

FINTECH APPS CONNECTED:

2,600+

MARKETS: The UK, Ireland,

France, Spain, the

Netherlands, the US and

Canada

WHAT IT DOES:

Plaid provides a global

network of financial data

and suite of APIs that

makes it easy to leverage the systems in place. For instance, On the consumer side, we

open banking and create I remember from my time working expected to see Europeans adopt

digital financial products at Square and BlueVine, how open banking pretty aggressively,

and services. much small businesses still use and that’s been borne out so far.

WHY IT’S INTERESTING: Excel to manage their finances. There was all this pent-up demand

It’s demonstrated one of Now, thanks to our money in and it’s clear from the data that

the most rapid rises in the Excel partnership with Microsoft, we’ve seen consumer

world of fintech startups. they can seamlessly update adoption taking off in

From a small startup in

“We see

spreadsheets with all their financial terms of the numbers

San Francisco, it’s now data, which is phenomenal. It has of accounts, percentage ourselves as

in the process of $5.3bn

been a huge hurdle, having to of people covered, the plumbing

acquisition by Visa, and

manually transcribe everything and there’s been huge that makes it

recently crossed the Atlantic

from paper statements into success of European

to make waves in Europe’s possible for

fintech space. spreadsheets, with all the back companies like Monzo,

and forth and a bunch of errors. Revolut, N26 and consumers

By building software that connects Starling. In some ways, to shop for

data and existing systems, we can it’s going faster than

How do you see fintech

take innovation to where people the US. Even countries

the right

innovations helping out on solution”

are. If they are using existing tools with affinities for more

the enterprise side? Financial

and benefiting from them, we in-person banking, like

processes are a huge workflow

want to help them there. Germany, are seeing changes now

and burden for many companies.

due to Covid, which might stick as

How do you see open

There are huge frictions banks are building more digital

banking playing out in Europe,

in financial transactions and solutions now.

both in terms of adoption and

practices which we can eliminate, On the regulatory front, Europe

regulatory support?

even by connecting software to has done a good job in enabling12 SIFTED REPORTS

open banking and the emphasis than just your bank, which could pieces, and give consumers

on consumer protection. We include investment accounts, debt greater control and visibility. For

see ourselves as the accounts and so on. It’s still very instance, it could unlock services

“A fully open plumbing that makes it difficult for companies to provide like financial nudges and analytics,

possible for consumers solutions in this wider financial such as saying, “Hey, you’ve got

finance to shop for the right space because it’s difficult to €1,000 in your cash balance, if you

ecosystem solution, from all the seamlessly integrate the data, as invest some in this money market

lets innovations they can these companies are not subject account by clicking here, you can

now leverage. You see to open banking regulations yet. be earning 4% interest”. It sounds

innovators small but done over millions of

this rise of new fintech

build players that have How would you see this shift

people over a long period of time, it

to open finance playing out, in

products grown because they are terms of its benefits?

will have big effects because this is

how wealth is built. So far, nobody

and connect innovating in their own

right, and we are trying It will give people a much is giving the general consumer

the pieces” to play a small part in better grasp of their financial this type of advice. This kind of

their success by making health and allow companies to service would disproportionately

it easier for consumers to make provide more wealth-creating help people who have been left

that connection in the first place. services. As of now, it’s like we are out. There’s so much that can be

The next step for Europe, I think, going to a doctor and they are done to make finance fairer, but

is moving towards open finance, scanning 10% of us to work out it starts with having much, much

following the lead of Australia, your overall health. We’re building better information and much less

which has been really forwarding- a world where consumers can friction. As long as there’s friction,

thinking in this area. Open finance build a total picture. A fully open and as long as there’s information

basically makes any digital finance ecosystem lets innovators asymmetry or lack of information,

financial account open, rather build products and connect the you can’t really help people.

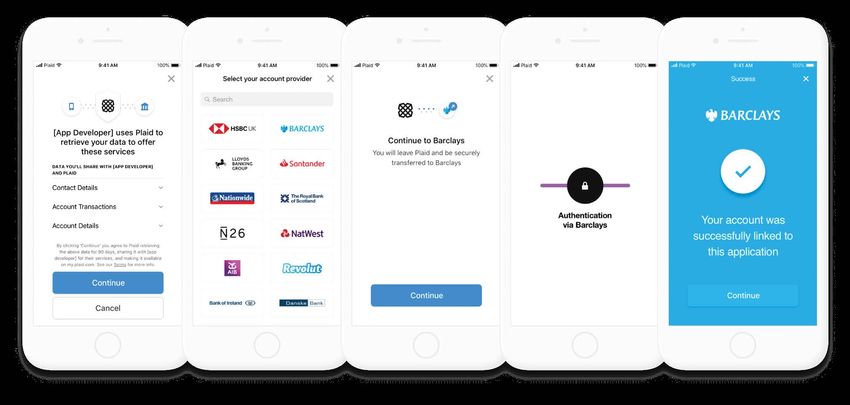

Plaid user flowFINTECH UNWRAPPED 13

Banking

g on

software

Incumbent banks have been on the

defensive, with fintechs offering more

appealing services and perks, and better

technology. To keep pace, Europe’s more

progressive banks are partnering up with

innovative startups that are liberating them

from cumbersome legacy systems and

infrastructures.14 SIFTED REPORTS

FOUNDED: 2013

ACQUIRED: 2018 (EQT)

Anders la Cour,

E

FOUNDERS:

urope’s roughly 6,000 banks IP disrupters like WhatsApp and

Laust Bertelsen

have watched on nervously Skype. “The banking industry has

HQ: Luxembourg

as challengers like Revolut, Monzo the same risk unless they invest

and N26 grow their market share. and offer more innovations,” TEAM SIZE: 200+

Incumbents are not at existential argues Stefano Vaccino, founder MONEY RAISED: $300m

risk: customers often use of Yapily. “They risk becoming (acquired by EQT in 2018)

neobanks as secondary accounts, a pure depositary. Innovative MARKETS: Global

to take advantage of perks applications will offer a new service

CLIENTS: Payments

like commission-free currency while the money sits on a current

businesses, banks

exchange or spending tracking. account, but banks don’t make

(incumbents and neos)

They also remain trusted, especially money from current accounts, but

in times of crisis, or when dealing from loans and added services.”

with complex or large transactions They also see that the innovations WHAT IT DOES:

like house purchases. Moreover, brought to market by the Fintech Banking Circle is a fully

Europe’s more imaginative banks Enablers could be useful to them. licensed bank able

are big investors in the fintech There are two ways for banks to to deliver financial

ecosystem, providing the capital avoid being left behind: one is to infrastructure at low cost,

and development re-imagine their own operations compliantly and securely to

payments businesses and

Europe’s more support that startups and architecture to be faster, more

banks - from multi-currency

need, and they are efficient and more automated; the

imaginative other is to expand what they can

accounts to fast access

investing in their

to loans, international

banks are big own digital offerings offer customers. An impressive

payments and local clearing

investors in in ways that mimic crop of European startups is to real-time FX.

helping them to do both.

the fintech what the challengers WHY IT’S IMPORTANT:

have brought to

ecosystem market, like NatWest’s Part of its mission is

SMASH THE STACK to lower the costs and

digital business bank speed of international

Mettle. Talent is also crossing the Banks are turning to startups commercial payments, and

aisle — note Barclays’ hiring of for help with overhauling increase accessibility and

former Starling executive Megan their own convoluted, clunky financial inclusion to the

Caywood. infrastructure, which is sucking digital economy for SMEs.

But that does not mean banks up massive financial resources. Banking Circle provides

can sit on their laurels. Their According to Euromoney, the the infrastructure that is

business is solid in areas that total cost of maintaining legacy currently supporting Stripe,

deliver them the least profit: systems, investing in new systems Alibaba and Shopify among

others.

current accounts. They see Big and paying IT staff amounts to

Tech companies over the pond between 15% to 25% of a typical

eyeing an entry into financial bank’s annual budget, with

services. As the circle of fintech incumbents ‘marooned in their had monolithic systems with an

innovation widens, there is a real own tech’. in-house server. The design of

possibility that banks will be the “Banking has been a tech-heavy these systems, especially the

‘dumb pipes’ on which era-defining industry for ages,” Anders la Cour, dependency and complexity

innovations are built, in the same cofounder of Banking Circle, tells that comes from years of system

way that telecoms companies were Sifted. “Their basic architecture upgrades, means that for a bank

to the streaming and voiceover- derived from a time when you today to deploy new software inFINTECH UNWRAPPED 15

an agile easy way and apply best Now, they are looking to the structured and unstructured data

practices is impossible.” Their Enablers as a kind of supermarket points about an individual, from

mindset has shifted over time as to help them re-imagine their board seats on other companies

they realised they could not fix this infrastructure and shift towards to personal associations with

alone and internally, says la Cour. software and cloud systems. The political figures, to produce a rich,

“Four years ago, a lot of banks maturation of APIs, in particular, real-time risk analysis; this was a

had this mentality that they could is helping liberate them from process that has traditionally been

do everything themselves, and their past technology stack. All done by large teams of human

didn’t need help from anyone, but told, the addressable market for researchers working manually,

many banks tried to overhaul their competitive, transferable banking sometimes via outsourcing to

legacy infrastructure and ended infrastructure could be as large as political risk consultancies.

up finding it too hard.” $500bn, according to CB Insights. Charles Delingpole, the founder,

“Legacy systems work differently started the company after seeing

and updating them is becoming banks pull back from remittances

harder,” says Evgeny Likhoded, to Somalia in 2015 due

founder of ClauseMatch, a to fears of fines, which

“Many

London-based regtech startup cut off vital remittances

that automates and streamlines to the region. He argues banks tried

2016

FOUNDED:

policy management and that banks were also to overhaul

FOUNDERS:Matty Cusden- regulatory change. APIs let new hesitant to seek out their legacy

Ross, Tom Reay, Veronique software interoperate with existing opportunities in eastern

Merriam Barbosa infrastructures. “Through APIs you Europe in the early 2000s,

infrastructure

HQ: London can get data from one system missing opportunities and ended

TEAM SIZE: Approx 30 in another. Previously you had because they feared that up finding it

to export and import that data,” the risks outweighed the

MONEY RAISED: Undisclosed,

says Likhoded. Gone are the days gains. While Delingpole

too hard”

but raised $7.5m in Series A

when banks look to one full-stack initially focused on Anders la Cour

and in 2020, Barclays took a

stake in the company for an solution for everything — “they’d fintechs, over time he

undisclosed amount rather have a number of solutions shifted to large banks, working

that talk to each other via API,” he with the likes of Santander, Bank

MARKETS: UK

says. of America and BBVA.

USERS: Around 300,000 on

Even sensitive and core back- A second operational shift for

Starling and Monzo

office processes could be better banks has been to reimagine their

DIGITAL RECEIPTS DELIVERED: done via algorithms and software workflows, including using artificial

Over 1.8m compared to banks’ conventional intelligence and machine learning.

approaches, and it takes the fresh Ky Nichol, founder of workflow

perspective of startups to design platform Cutover, identified

WHAT IT DOES: better workflows — even in areas financial services as having a ‘huge

Flux keeps a track of like anti-money laundering and gap’ in terms of orchestrating

payment receipts via its

terrorism financing, which banks, work and making it observable,

software platform by

intuitively, would seem to be the especially fast-paced work like

automatically linking them

experts on. ComplyAdvantage, a initial public offerings or foreign

to payment cards.

London-based fintech, has built exchange trading. There is also a

WHY IT’S IMPORTANT:

an artificial intelligence-based pressing need to optimise daily

By digitising receipt data

platform that crunches millions of workflows, for which people still

Flux allows customers to

access retail information

from their connected bank

accounts.16 SIFTED REPORTS

too often use Excel spreadsheets, not focus on giving customers

phone calls and emails. Cutover is the frictionless services they are

being used by clients that include accustomed to. Here too, Enablers

Barclays, Barclaycard, Tesco Bank are helping them by offering

and Nationwide. smarter software. London-based

A common criticism of Flux, which digitises receipts to

incumbent banks is that they do offer granular data on spending for

individuals and businesses, is one

example. “Customer confusion on

certain transactions is a problem

for banks, they’ll often have calls

from customers where they believe

Roisin Levine, Flux

FOUNDED: 2012 fraud has taken place because

the merchant data showing on

FOUNDERS:Evgeny Likhoded

and Andrey Dokuchaev their statement can be pretty whose value proposition is strong

confusing,” says Roisin Levine, for organisations encumbered by

HQ: London

Flux’s head of banks. Using a Flux- legacy infrastructure.

TEAM SIZE: 53 enabled bank card, transactions How banks engage with fintechs

MONEY RAISED: $9.3m can be presented in the banking is evolving, from incubators

INVESTORS: Techstars, app with a digital receipt attached. and accelerators through to

SparkLabs Global Ventures, By tidying up and enriching this venture investment arms, startup

Speedinvest, Deepbridge spending information, Flux is competitions and scouting

Capital, Index Ventures, reducing hassle for customers networks. Madrid-based BBVA

Talis Capital, Silicon Valley and banks, and helping banks add has won praise as one of Europe’s

Bank (venture debt) value through more personalised more innovation-centric banks; its

MARKETS: The UK and services like spending rewards. “A methods include an

Europe, APAC, US digital receipt tells a bank more open innovation unit

“Accelerators

than just the cafe you shop at, that works with fast-

NUMBER OF USERS: 1000+ at and labs

Barclays global bank alone it also provides the item level growth companies,

in the UK, plus more across information, like the fact that you and Open Talent, its help you to

Europe and the US often buy soy flat whites,” says startup competition bridge the

Levine. that helps it keep its

ear to the ground.

gap between

WHAT IT DOES: BBVA’s venture unit, their need

FRUITFUL PARTNERSHIP

ClauseMatch is a regtech Propel Venture and your

company providing Banks and fintechs have Partners, has nurtured

software as a service for closer ties than disrupters and financial infrastructure

solution”

both incumbents such as incumbents in sectors like retail innovators like Evgeny Likhoded

Barclays and neobanks like — they are interdependent and ChargeAfter, an Israeli-

Monzo.

each offers the other something American company that provides

WHY IT’S INTERESTING: that would be hard to build retailers with a single channel to

Working simultaneously themselves. This is especially tap into lenders. This gives lenders

with traditional and true in financial infrastructure, a chance to scale up — and gives

challenger banks

where banks are often the biggest merchants access to competitive

ClauseMatch allows them

market opportunity for startups lending options.

to focus on product by

powering compliance in

a changing regulatory

environment.FINTECH UNWRAPPED 17

Talent scouting

g

To spot Fintech Enablers, Royal Bank of Scotland leveraging the work VCs have done to filter the best

has developed a scouting strategy to identify from the rest. Even with that shortlist, a partnership

startups that can help it to develop new customer only makes sense if it meets a specific set of criteria.

solutions and solve key challenges in areas including “It needs to solve a problem that is a priority for us at

digitisation of customer interactions, payments, that moment, that can be implemented and that will

security, data analytics, payments, and on-boarding, ultimately benefit a customer. Those stars all have

as well as internal tools and colleague platforms such to align,” says Stewart. Some companies are exciting

as Zoom. “We shouldn’t try to build security or anti- but perhaps don’t cover the bases. Others fall by the

fraud tools when there are so many great companies wayside because the solution creates too many new

out there building that” says John Stewart, who leads problems.

the scouting teams globally. “While rarely offering Rather than looking for interesting ideas and

100% fit off-the-shelf solutions, these companies finding ways to syndicate them with the bank, RBS

have put thousands of days or hours of effort into has flipped the model to identify key problems in the

building solutions — which we can deploy”. bank or for customers, taking those as “the starting

RBS works closely with the venture capital point to do a matching exercise with our database

communities in Silicon Valley, Israel and the UK, of companies”.

Barclays has created one bank’s insurance arm, and Cathay legacy and challenger banks, each

of Europe’s more prominent Innovation, led to investments getting different benefits. Flux, for

accelerator schemes — graduates in infrastructure innovators, instance, saw quick initial take-

believe it kicks the tyres on their including leading French up from neobanks like

product and allows them to engage blockchain company Stratumn. Monzo and Starling. “It is

“It is easier

potential users in a productive easier to do integration

development conversation, of new tech when you to do

MAKE HASTE SLOWLY

rather than hawking a product. are smaller and already integration

“Accelerators and labs help you to Far from being displaced by API-led,” says Flux’s of new tech

bridge the gap between their need fintech, incumbent banks are in Roisin Levine. Over time,

and your solution. It’s a friendlier, the middle of it: they are investors though, large banks

when you

more consultative process, rather in the fintech ecosystem, a huge became more interested are smaller

than a sales pitch,” says Evgeny market for startups and a trusted “because, ultimately, and already

Likhoded at ClauseMatch. foundation on which many apps this offers an amazing

API-led”

Ky Nichol at Cutover says that and products are built. Their customer experience”.

access to a top tier bank like problem, however, is that their At times, neobanks and Roisin Levine

Barclays, working with “forward- business is safest where it makes incumbents are using the

thinking technologists, helps them limited money. Fintech same software to solve different

batter the product from a prototype Enablers can transform their challenges. In compliance, for

into an enterprise solution”. business by slashing costs and instance, large banks have

Direct investments are another deconstructing cumbersome the manpower, but they use

way that banks are working with infrastructure, freeing up slower systems and have more

startups. BNP Paribas launched resources to invest in innovation fragmentation and coordination

an investment fund in early and a more customer-centric problems, whereas neobanks’

2018 to take minority stakes in approach. How will the ecosystem problem is a lack of manpower

startups, and another partnership play out in the coming years? or familiarity with compliance

between BNP Paribas Cardif, the First, Enablers will sell to both regulations. For incumbents,18 SIFTED REPORTS

FOUNDED: 2014

FOUNDER: Paul Taylor

HQ: London

TEAM SIZE: 340

ClauseMatch’s software centralises do, it could be worth it, since big

and organises to give visibility banks don’t change vendors for MONEY RAISED: £82m

and traceability. For neobanks, it around 17 years on average,” says INVESTORS: IQ Capital,

allows them to “do more with less”, Likhoded. Backed VC, Lloyds Banking

says Evgeny Likhoded. “Ultimately, Lastly, not all parts of the tech Group, Draper Esprit,

both are after peace of mind that stack will be outsourced. There is Playfair Capital

compliance documentation is no single rule on how much banks MARKETS: UK, APAC and US

done in a central way so you can should give to Enablers, and how NUMBER OF CLIENTS: 4 publicly

easily answer questions from much they keep in-house. Some announced

regulators and auditors.” startups are trying to build a

Second, some European cloud-native full stack approach;

WHAT IT DOES:

incumbents are still hesitant Thought Machine’s Vault product,

Cloud native core banking

to engage with startups. While for instance, is completely cloud

technology.

European companies sing the native, with no legacy or pre-

praises of a clutch of European cloud technology and each service FUN FACT:

banks that are actively seeking representing a key bank function. Founder Paul Taylor had

no experience in financial

out new collaborations through It is working with European banks

technology prior to the

accelerators, partnerships and including Lloyds, Santander and

business. He spent years

investments, the continent as a Sweden’s SEB, and recently closed

as an academic, working

whole is still lagging. “US banks an $83m funding round. in speech technology and

have already figured out where Other startups see banks taking then at Google.

the gaps are in their systems and a case-by-case approach to re-

are more opportunistic in using designing their infrastructure.

new tools, whereas European “We’ve turned off lots of legacy

banks are at the beginning of that solutions and kludges of banking systems, we realised a lot

journey,” says Evgeny Likhoded. spreadsheets, sharepoint sites, of banks are basically brownfield

The problem for startups is and fragmented communications sites with a mix of technologies

whether they have the funding that make it difficult to have a and in amongst that they’ve got

and patience to get through the structured and efficient way of some bits that are really cool,” says

sales cycle for a large bank. “If they working. But in terms of the core Cutover’s Ky Nichol.

Thought Machine teamFINTECH UNWRAPPED 19

Disrup

p ters

under

the hood

Fintech Enablers are not just helping

incumbent banks rebuild their

infrastructure; they are allowing consumer-

facing fintechs to come to market faster

and cheaper through white-label banking

services. Some are going further, creating

software that helps huge but often

antiquated industries like law and the

property sector to boost their financial

offerings.20 SIFTED REPORTS

T oday, a dizzying array of

companies offer financial

services, from challenger banks to

though. In the years to come,

Enablers will bring more advanced

financial capabilities across the

alternative lenders) are powered

by Enablers like solarisBank, as well

as niche expense management

Big Tech companies. That means economy, from the property and specialists like Spendesk and

consumers can borrow, store legal sectors to ride-hailing and credit providers like Wollit. Indeed,

deposits, spend, track finances mobility. In some cases, Enablers fintechs launched after around

and make payments with a will help companies manage their 2015 have been able to tap into

variety of apps outside their main own finances more efficiently than a community of infrastructure

bank. This is largely thanks to an their banks or internal finance providers — helping them

influential but hidden army of departments ever could, using save resources,

tech startups, which have created automation and machine learning minimise costs and

to manage payroll, expenses and get to market far

“Brand and

banking infrastructure that can be

neatly packaged and rented out. employee benefits, for instance. In quicker — reaching proposition

They are the innovators behind the others, they will allow companies customer-readiness are now

curtain who have turbo-charged to offer new services that add value in six months rather

more

the growth of popular consumer- to their customers; e-commerce than two years.

facing fintechs, helping them get platforms and ride-hailing services, “Once you’ve got important

to market far quicker than if they for instance, could lend to their the license and than tech

had to become a licensed bank merchants or drivers by leveraging platform, all you

spend”

from scratch. “Any new startup their intimate knowledge about need to worry about

can have the benefit of millions sales trends or working hours is the logo and David Chan

of dollars of investment for a low norms, respectively. getting customers,”

price; it should make any startup says open banking expert Rolands

bank capable of competing with Mesters. A few lines of code

THE HUMBLE PLUMBERS

either a Revolut or a Barclays,” effectively allows fintechs to build

says ComplyAdvantage founder So far, consumer-facing fintechs on regulatory-compliant current

Charles Delingpole. have been the main beneficiaries and savings accounts.

We are only in phase one, of the Enablers and their behind- Aside from the ease and

the-scenes technology. By practicality offered by the Enablers,

simply plugging into banking their success has also been fuelled

infrastructure, fintechs have by a fundamental shift in mindset

gotten cheap and quick access around building technology

to flexible back-end solutions, on from scratch, says David Chan,

top of which they have built their chief executive of Monedo, a

products and services, focusing buy-now-pay-later digital lender.

more on the user experience. “Ten years ago, the mentality

Enablers take on the role of was to build everything yourself.

safely storing and moving users’ But, reinventing the wheel on

money on behalf of fintechs everything doesn’t make sense

and can absorb complex, costly anymore. Brand and proposition

workflows that come with building are now more important than tech

a financial offering from scratch, spend,” he says.

like regulatory compliance. In doing so, several newcomers

Today, major fintechs like are already threatening the

David Chan, Monedo

Smava (one of Germany’s largest margins of incumbent players.FINTECH UNWRAPPED 21 Exp p lainer To store and move users’ money, you must connect Therefore, fintechs must either build their own APIs to into a bank or licensed entity like the Bank of England. do this or plug into a software partner that provides Fintechs have several options here: ready-make banking APIs. They can then build on top 1. In some countries, fintechs can obtain an of that. e-money license and then use a licensed bank to 2. A more simple route is to use Banking as a Service house their users’ money (known as an ‘agent bank’). (BaaS) platforms, which offer the full banking stack; But most agent banks do not yet have the tools to some even have their own bank licenses (as shown divvy up users’ funds into thousands of individual on the left-hand side below). They are the “mother” accounts, which is what gives us payment capabilities. group of Enablers, offering multiple features. Once the fundamentals are sorted, the trend is can use Enablers that specialise in single areas like for fintechs to stitch together different software payment upgrades or ‘data as a service’ (see below), providers that offer best-in-class add-ons. Here, they and which serve banks too.

22 SIFTED REPORTS

infrastructure eventually,”

TO BUILD OR NOT TO

Ozcan tells Sifted. “But this has

BUILD

compliance-related consequences.

Despite the benefits brought When you change tech stack,

by the Enablers, some experts you expose your system to

believe they only help fintechs up vulnerability. Fraud attacks sky-

to a certain point. Pinar Ozcan, rocket at this time.”

professor of entrepreneurship at Meanwhile, business banking

Oxford University’s Saïd Business app Tide has been criticised

School, says that outsourcing by some pundits for “not really

infrastructure means fintechs competing” with serious banks,

have less “agency” over their tech says one source, because they’ve

stack and lose “flexibility” in their outsourced their tech stack and

product offerings later down the depend on ClearBank (a leading

line. Enabler) for their banking license. Pinar Ozcan

“A lot of fintechs, because As a result, open banking

they have limited resources, first expert Mesters says that “it’s still

focus on the customer-facing pretty tempting to build your own is the smart way forward.

technology and make the user [infrastructure]” — especially for “Investors say, ‘We like that you

interface as good as those with big ambitions that don’t didn’t try to build your own core

simply want to be acquired. banking system’. Investors that

“A lot of possible, but then

in the back end they Nonetheless, the consensus really understand banking won’t

fintechs rely on third parties, remains that fintechs should opt see value in just a random tech

rely on third which gives them for pre-made banking software stack,” Tide chief executive Oliver

parties in less control,” Ozcan until they have proven their Prill tells Sifted. He adds that

told the Financial business model and have pulled Tide builds where they feel they

the back Times. in investors with deep pockets. can “differentiate”, for example

end, which Ozcan also tells RBS’s now-defunct neobank Bó proprietary features like its VAT

gives them Sifted that once and Starling are some of the only pots, automated invoicing and

fintechs reach a neobanks known to have built in-app credit access, but that “it

less control” certain size, it’s their own stack from the outset. doesn’t make sense to build a

Pinar Ozcan incredibly expensive Moreover, as Enablers get ledger or accounts” — or to get its

to leverage third better, the temptation to avoid own license.

parties (they typically charge per taking on the complexity and Meanwhile, even big banks are

user). As such, many larger fintechs heavy lifting of testing, legal and starting to use certain Enablers

have been forced to build their compliance work becomes even to outsource and update their

own tech stacks retrospectively stronger, especially for smaller own infrastructure. For example,

once they are up and running. fintechs. “We can do current London-based startup Thought

This is the route Monzo went accounts for 10p, instead of Machine has won clients like

down, forcing them to eventually £45,” points out Railsbank chief Standard Chartered, Lloyds and

undergo a difficult migration onto executive Nigel Verdon. Sweden’s SEB (as well as new

their own systems. For its part, Tide is resolute that banks like Atom Bank) by offering

“The most aggressive, most its “horizontal platform” approach, them a cost-effective, secure,

competitive fintechs need to made up of infrastructure cloud-based “core system-as-a-

pivot and build their own native providers like Clearbank and Xero, service”.FINTECH UNWRAPPED 23

FOUNDED: 2015

FOUNDERS: Jakub Zmuda,

Martin Threakall, Myles

Stephenson, Ritesh

economy, whether for their own cloud-based software.

Tendulkar

efficiency gains or to create One beneficiary could be

HQ: London customer value. the property sector. Currently,

TEAM SIZE: 190 The most obvious sign of paying rent to an estate agent is

MONEY RAISED: £53.3m the blurring boundary between a clunky affair, entailing several

(including £10m grant from financial services providers has direct debits and tracking so that

the Banking Competition been the Big Tech brands. Apple money can be redistributed to

Remedies’ Capability and has launched its own native landlords. “This involves a huge

Innovation Fund) credit card in partnership with number of payments, and lots of

Frog Capital,

INVESTORS: Goldman Sachs. Amazon offers flow, complexity and inefficiency,”

Blenheim Chalcot, Highland loans to distributors by working explains Myles Stephenson, chief

Europe with Bank of America. Google has executive of Modulr, the payment

MARKETS: UK (with plans to announced plans to enter current services business. Four years ago,

launch across Europe soon) accounts in the US, in partnership the property industry showed little

with banks and credit unions. Uber awareness about how software

NUMBER OF BUSINESSES USING:

has announced a mobile wallet could remove all these frictions.

100+

and debit card for its drivers, “Now, rental platforms are slowly

so that earnings can be paid waking up to an opportunity”,

faster and employees get easier propelled by the emergence of

WHAT IT DOES:

Modulr is a payments as a access to overdrafts. Rather than cloud-native, software-based

service provider API which building the banking technology property platforms that can

enables non-banks to themselves, the ride-sharing giant integrate into payment processors.

process payments. partnered with Green Dot Bank “These [new platforms]

to secure faster development and are letting agents “The ability

FUN FACT:

Modulr have processed ‘best-in-class’ infrastructure. manage tenants

“The ability to leverage banking and, rather than

to leverage

over £30bn of payments to

date. infrastructure can now be seen as payment processes banking

another part of your stack,” says being separate, they infrastructure

Tom Mendoza, deal partner at EQT can integrate it,

can now

Ventures. “One out of every six allowing agents to

EVERYONE’S A FINTECH be seen as

calls I have with founders I think, manage payments

While fintech companies were ‘if you use this infrastructure, more effectively,” another part

the first to engage and profit from you could extend the product’.” says Stephenson. The

of your stack”

the Enablers, they are by no means Angela Strange, general partner general corporate

the only beneficiaries. Anywhere at Andreessen Horowitz, stated back-office function is Tom Mendoza

that money moves or needs in a recent article that in the “not- embedding fintech too,

managing, software can help; too-distant future… nearly every using cloud platforms to deliver

from law firms overseeing M&A company will derive a significant salary and supplier payments, he

and house purchases, to general portion of its revenue from adds.

corporate back-offices managing financial services... even those that Another example is Shieldpay,

salaries and supplier payments. have nothing to do with financial a digital escrow account which is

The Enablers are helping unleash services”. The coronavirus helping a wide range of businesses

a new era of ‘embedded fintech’ pandemic will only quicken this manage large transactions — a

that brings financial capabilities transition as companies are forced process that is often complex,

to companies throughout the to shift away from desktop to inefficient and even stressful.24 SIFTED REPORTS

Tom Squire, the company’s group ‘whole-of-market’ experience,”

BAD NEWS FOR BANKS?

commercial director, saw first- he says, pointing to the likes of

hand the problem of limited funds If every tech company can turn WeChat in China as an example.

visibility for large transactions itself into a bank, many are asking “Now the floodgates have

while working in M&A. “You what’s the point of the banks? Are been opened,” concludes Oxford

go through months of work in they going to get crushed by the University’s Ozcan. “These other

putting together a deal, making likes of Amazon and Facebook players provide much more of a

sure you know exactly what’s moving into financial services? threat [than most fintechs].”

happening on the day, but when “Banks have a terrible customer But, it’s not all bad news.

it comes, it’s completely opaque. experience problem. They are While large banks are in one

It’s a case of calling up the bank failing to innovate, and they are sense threatened by the rise of

and asking, ‘has the money struggling with their tech stack the Enablers, there is also an

landed’, talking to the lawyer because it’s built on legacy rails,” opportunity for them to do some

who is saying ‘the money hasn’t says Tom Mendoza. “Then you have enabling themselves, creating new

landed’. It’s just horrendous.” this new wave of financial services business lines by selling back-end

Other sectors using Shieldpay for companies that are winning services to power other financial

larger-ticket transactions include market share because customers institutions.

used-car websites, art galleries want better alternatives. Now, you Goldman Sachs and JP Morgan

and high-end fashion stores. have fintech infrastructure players, have already begun building out

A broader benefit to the tools these Enablers, you will see more specialised “banking-as-a-service”

brought to market by the Enablers fintechs taking market share from (BaaS) platforms. Societe Generale

is the ability for European SMEs incumbents, but also non-fintech has also got ahead by acquiring

to build out their business across technology companies offering an existing infrastructure

a continent that remains highly financial services like Apple, Uber player in Treezor (which powers

fragmented in terms of payments and Lyft.” over 30 fintechs). Meanwhile,

infrastructure, adding complexity Alessandro Hatami, a former Norway’s DNB is experimenting

for any company building a Lloyds executive, predicts

regional footprint, that the “real losers [of this

according to Banking trend] are big banks”. Hatami

If every tech

Circle’s Anders la Cour. ultimately foresees Amazon

company can “Digital technology offering a financial marketplace

turn itself opens the world for for loans, savings accounts and

you as an SME, but to mortgages, plugging into other

into a bank,

take advantage of that banks’ products like a “Spotify”

many are requires scale. If they for banking. Unlike comparison

asking what’s go to a large bank, sites like MoneySuperMarket, an

the point of they get the standard Amazon marketplace would allow

solution and won’t users to seamlessly sign up for

the banks? get the attention they products within the platform.

require. The paradox “That will damage banks.

is that the digital world has made There’ll be a much easier interface

it easy and seamless for the for customers and the only

consumer, but the [payments] differentiation will be the rates. A

complexity behind the curtain is non-banking entity like Amazon

Alessandro Hatami

still there.” will run it for most people in aYou can also read