Islamic Banking Opportunities Across Small and Medium Enterprises in MENA

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Public Disclosure Authorized

Public Disclosure Authorized

Public Disclosure Authorized

Public Disclosure Authorized

Xavier Reille

Islamic Banking Opportunities

Financial Institutions Group

Advisory Services Manager Across Small and Medium

Europe, Middle East and North Africa

E-mail: xreille@ifc.org

Enterprises in MENA

Kaiser Naseem

Executive Summary

Program Manager

Banking Advisory Services In partnership with the Canadian Department of Foreign Affairs,

Middle East and North Africa Trade and Development, the Danish International Development

E-mail: knaseem@ifc.org Agency, Japan, Switzerland’s State Secretariat for Economic

Cornich El Nil, Ramlet Boulac, Cairo, Egypt Affairs and UKaid.

Print Right Adv.

Tel: + 20 (2) 2461-9140 / 45 / 50

Fax: + 20 (2) 2461-9130 / 60

DISCLAIMER “IFC, a member of the World Bank Group, creates opportunity for people to escape poverty and improve their lives.We foster sustainable economic growth in developing countries by supporting private sector development, mobilizing private capital, and providing advisory and risk mitigation services to businesses and governments. This report was commissioned by IFC through its Access to Finance Business Line in the Middle East and North Africa to highlight the need for Islamic Banking across the region.” “The conclusions and judgments contained in this report should not be attributed to, and do not necessarily represent the views of, IFC or its Board of Directors or the World Bank or its Executive Directors, or the countries they represent. IFC and the World Bank do not guarantee the accuracy of the data in this publication and accept no responsibility for any consequences of their use.”

“This research is funded under the MENA MSME Technical Assistance Facility, a joint initiative

between IFC and the World Bank. The facility is supported by the Canadian Department of

Foreign Affairs, Trade and Development, the Danish International Development Agency, Japan,

Switzerland’s State Secretariat for Economic Affairs and UKaid.

Contents

01. Preface 7

02. SME sector overview 9

SME Definition and Classification 9

SME Universe 10

SME Sector Overview 11

Key Enablers for SME Growth 13

Key Challenges for SMEs 13

Government Initiatives to Support SME Growth 16

World Bank Group Initiatives to Support SME Growth 17

03. Financial Sector Overview 19

Banking Penetration 19

Commercial Banking sector 20

Islamic Banking Sector 22

SME Sector 23

Non-performing loans 25

Islamic Financial Sector Regulations and Enabling Environment 26

04. SME Access to Islamic Finance 28

SME Penetration 28

Obstacles Faced by Banks in SME Financing 29

Supply side Analysis of Banks in the Region 30

Islamic Products Availability and Recommended Products 31

05. Opportunities for Islamic SME Banking 33

Funding Opportunity 33

Sectors to be Targeted 38

Factors Affecting Growth of Islamic SME Banking 39

06. Conclusion 41

Strategic Operational Adjustments Can Help Islamic Banks Target SMEs More Effectively 41

Proposed Strategy Framework 42

Ideal Business Model 43

Road Map for Islamic SME Banking Inception and Growth 44

Appendix 46

Research Scope 46

Methodology 47

About IFC 51

Bibliography 52

Annexures 57

Index of Figures and Tables Figure 1: Islamic Funding and Deposit Potential Across MENA and Pakistan ($bn) 8 Figure 2: Segmentation of SME Universe Across Countries 10 Figure 3: SME Contribution to GDP 12 Figure 4: Key Challenges Faced by SMEs During its Evolution Phases 14 Figure 5: Challenges Faced by SMEs Across Countries 14 Figure 6: Major Constraints Faced by Businesses 15 Figure 7: Banking Penetration Across Countries 19 Figure 8: Loan and Deposit Growth Across Countries (2010–2012) 20 Figure 9: Islamic Banking Market Overview 22 Figure 10: Islamic Assets and Deposits Growth (2010-2012) 23 Figure 11: NPL Overview 26 Figure 12: SME Sector – Existing Penetration 28 Figure 13: Obstacles Faced in SME Financing 29 Figure 14: Aggregate Supply Side Analysis 30 Figure 15: Factorial Analysis of SME / Islamic SME Proposition 31 Figure 16: Evolving Financial Requirements of SMEs 32 Figure 17: Preference for Shariah-compliant Products Percentagewise 34 Figure 18: Funding Potential % Across Countries 34 Figure 19: Enabling Environment and Supply Side Analysis (SME and Islamic SME) 35 Figure 20: Comparative Islamic Funding Opportunity 37 Figure 21: Islamic Conversion Opportunity Across MENA and Pakistan ($mn) 38 Figure 22: Strategic Operational Adjustments to Target SMEs 42 Figure 23: Strategic Initiatives to be Undertaken by Countries 43 Figure 24: Integration of Islamic Banking SME Model 44 Figure 25: Roadmap for Islamic SME Banking 45 Figure 26: Strategic Initiatives to be Undertaken by Countries 49 Table 1: SME Definitions 9 Table 2: Importance of SMEs to Economic Development 11 Table 3: SME Distribution by Sector 12 Table 4: SME Enablers by Country 13 Table 5: Government Initiatives to Support SME Growth 16 Table 6: IFC Initiatives to Support A2F for SMEs 17 Table 7: Commercial Banking Sector Overview 20 Table 8: Banking Penetration in SME Sector (2012) 24 Table 9: Trend in SME Portfolio Growth 24 Table 10: Regulatory Overview 26 Table 11: Islamic Banking Initiatives 27 Table 12: Total SME Universe 36 Table 13: Islamic Depository Potential by Country 37 Table 14: Attractive Sectors for Islamic Finance Across Countries 39 Table 15: Drivers and Challenges Faced by Islamic banks 15 Annexure 1: Common Shariah Structures Used Across Countries 57 Annexure 2: Commonly Used Products and Recommended Products 58 Annexure 3: Questionnaire for Banks 59 Annexure 4: Questionnaire for SMEs and SME Associations 60 Annexure 5: List of Respondents from Banking Sector 61 Annexure 6: List of Respondents from SME 64

Abbreviations and Glossary ANPME National Association of Small and Medium Enterprises BAS Bank Advisory Services BMCE Banque Marocaine du Commerce Extérieur CIB Commercial International Bank CAC Cooperative and Agriculture Credit CAGR Compounded Annual Growth Rate GDP Gross Domestic Product HSBC Hongkong Shanghai Banking Corporation ICD Islamic Corporation for the Development of the Private Sector ICT Information and Communication Technologies IDB Islamic Development Bank IFC International Finance Corporation IT Information Technology JEDCO Jordan Enterprise Development Corporation JLGC Jordan Loan Guarantee Corporation KSA Kingdom of Saudi Arabia MENA Middle East and North Africa NCB National Commercial Bank NPL Non-Performing Loan NSGB National Societe Generale Bank PPP Public Private Partnership SFD Social Fund for Development SME Small and Medium Enterprise SMEDA Small and Medium Enterprise Development Authority USAID United States Agency for International Development

01.

Preface

Small and medium enterprises (SMEs) are now widely recognized as engines of economic growth and key contributors to sustainable

gross domestic product (GDP) of all countries, including those in the Middle East and North Africa (MENA) region. These businesses

predominantly operate in the manufacturing and service sectors and create employment opportunities for both skilled and unskilled persons.

However, market conditions and regulatory environments are not always supportive of the growth of SMEs and access to formal finance

is one of the main obstacles they face.

IFC’s Financial Institutions Group (FIG) in MENA provides investment and advisory services to the region’s banks and other financial

institutions to build their capacity in SME banking so that they can profitably and sustainably reach out to the SME sector. This is achieved

through providing equity finance, lines of credit, risk sharing facilities, trade finance, disseminating best practices, improving processes and

products, and streamlining delivery channels. Ultimately, IFC’s goal is to increase the number of banks and financial institutions that offer

financial and banking services to SMEs in a profitable and sustainable manner. IFC is recognized globally as an SME finance market leader

owing to its global expertise and knowledge.

There is a huge demand for Islamic products by SMEs in the MENA region and, according to this study, approximately 32 percent of such

businesses remain excluded from the formal banking sector because of a lack of Shariah-compliant products.

In order to reach out to SMEs demanding Islamic products, and as part of IFC’s initiative to enhance its SME investment and advisory services

offerings to Islamic financial institutions, we needed to better understand the market from both the demand and supply sides in order to identify any

gaps or niches where IFC could assist and add value. With this objective, IFC commissioned a study in nine countries of the MENA region, which

includes Pakistan, to better understand the demand and supply for Islamic banking products (both asset and liability products and other banking

services) in the SME sector. The countries chosen for this study are: (1) Iraq, (2) Pakistan, (3) Yemen, (4) Kingdom of Saudi Arabia, (5) Egypt, (6)

Lebanon, (7) Morocco, (8) Tunisia, and (9) Jordan.

The scope of the study was to: (i) identify the countries in the MENA region facing gaps in financing and banking needs of SMEs in the Islamic

products space; (ii) conduct a supply side benchmarking to review current capacity of financial institutions to offer Islamic products to this sector;

(iii) conduct a demand side benchmarking to identify key SME customer needs for Islamic products and see how well they are currently being served;

and (iv) review the current enabling environment and readiness levels of banks in terms of the regulatory framework and Shariah compliance.

The study reiterates several of the now well researched and documented reasons for the lack of access to finance for SMEs. However, more

importantly, the study reveals that, there is a potential gap of $8.63 billion to $13.20 billion for Islamic SME financing within un-served and

underserved SMEs categories, with a corresponding deposit potential of $9.71 billion to $15.05 billion across these countries. This is due to the

fact these un-served and underserved SMEs do not borrow from conventional banks, only owing to religious reasons. This potential is a “new to

bank” funding opportunity, which is still untapped, as banks and other financial institutions lack adequate strategic focus on this segment to offer

Shariah-compliant products.

Islamic banking opportunities across Small and Medium Enterprises in MENA (including Pakistan) 7Figure 1: Islamic Funding and Deposit Potential Across MENA and Pakistan ($bn) This Regional Executive Summary provides a comparative analysis of the SME potential across these countries and the opportunities available to Islamic institutions to tap this potential. The nine individual country reports provide a deeper insight into the SME landscape and potential opportunities for Islamic banks in each country. The reports also highlight the measures that banks may need to take to successfully target the Islamic banking potential of SMEs. IFC acknowledges the commitment and cooperation of Israa Capital Management Consultants, Dubai, who carried out this study on our behalf. IFC thanks them for their dedicated efforts and contribution in compiling the individual country reports and the comparative analysis contained in this executive summary. Mouayed Makhlouf Regional Director IFC – Middle East and North Africa 8 Executive Summary

02.

SME Sector Overview

The SME sector forms the backbone of economic development, private

sector employment, capital investments, and GDP growth. Despite their

importance to economic output, SMEs still have inadequate access to

finance and other banking services. As a result, most of the SMEs tend

to be concentrated in less capital intensive sectors, such as retail and

wholesale trade. This scenario not only restricts the development of smaller

enterprises, but also retards economic activity in these countries.

Government initiatives and assistance from multilateral institutions like IFC

have been instrumental in these countries to enable the SME sector to grow

by providing business and technical expertise to enhance access to finance.

SME Definition and Classification

There is no standard definition for classifying small and medium enterprises (SMEs) across various countries. The most commonly used

criteria by government agencies (central banks and government departments) and commercial banks are based on employee size, asset

size, and annual turnover. However, application of the same classification criteria across countries results in disparities due to different

classification thresholds. These disparities exist because of the differences in economic structure, size of the economy, and the degree of

development in each country. The following definitions used for the target countries are derived from definitions used by the commercial

banks, central banks, and/or the statistic or trade departments of the respective countries.

The lack of a standard definition makes it difficult to compare the SME sector across countries. A standard definition would enable a

meaningful comparison, leading to the replication and implementation of effective policies and programs (such as credit guarantee programs,

skill development programs, etc.) for SME development across countries.

Table 1: SME Definitions

Small Medium

Countries Definition derived from

Employee size Annual turnover Employee size Annual turnover

Egypt* Ministry of Trade and Industry 10–50 $87,864–878,659 50–100 $878,659–1,757,318

Pakistan Central Bank Up to 20 employees and annual turnover of up to $757,500

Saudi Arabia Dept. of Statistics 5–19 $1.3–6.7mn More than 20 $6.7–33.3mn

Jordan# Central Bank 5–20 Less than $1.4mn 21–100 $3–4.2mn

$344,400–

Morocco Central Bank -- -- $1.15– 20.10mn

$1.15mn

Tunisia Commercial Banks -- $1–10mn -- $10–19mn

Yemen Commercial Banks -- $10,000–50,000 -- $50,000–225,000

Iraq^ Commercial Banks -- $5,001–250,000 -- More than $250,000

Lebanon Commercial Banks Enterprises with turnover of less than $4mn classified as SMEs

Note:* For Egypt, the definition is based on registered capital instead of turnover.

# For Jordan, the definition is based on either assets or sales volumes.

^ For Iraq, the definition is based on loan size.

-- Means there is no official response or definition available

Islamic banking opportunities across Small and Medium Enterprises in MENA (including Pakistan) 9Domestic agencies, such as central banks and government departments, are unlikely to possess an international perspective. Therefore,

multilateral agencies need to play an active role in the development of a standard definition for SMEs on the basis of annual turnover or any

other suitable parameter.

SME Universe

The enterprise population across each country is usually divided into two distinct segments:

• SMEs that operate in the formal sector, and

• Very small (or micro) enterprises that operate in the informal/parallel economy.

SMEs operate in high economic impact sectors such as manufacturing and construction. As a result, they are able to generate employment

and significant economic value. Very small enterprises on the other hand generally operate in the trade and commerce sectors, which have

low economic potential, as they serve local markets and do not add significant value to final products.

The current enterprise population in the target countries is dominated by very small enterprises that do not offer the same economic

advantages as SMEs. The composition of very small enterprises in the enterprise population is as high as 91 percent (Tunisia) to about 40

percent to 60 percent (Yemen and Saudi Arabia). Therefore, there is a need for the government and multilateral institutions to assist these

very small enterprises to develop into SMEs. In order to achieve this, governments are looking at:

A. Developing very small (micro) enterprises capabilities through training on various facets (financial knowledge, business planning,

management, product quality)

B. Creating an enabling environment for the SMEs (easy access to basic infrastructure, smooth approval process in governmentdepartments, and

prudent regulation)

C. Providing access to finance (special government bodies to channel finance to the sector, guarantee schemes and incentives to banks for targeting

very small enterprises)

Figure 2: Segmentation of SME Universe Across Countries

10 Executive SummarySME Sector Overview

SMEs contribute significantly to GDP growth, private sector employment, and capital investments

SMEs form an important component of a country’s economy. They play a significant role in generating private sector employment, driving

gross domestic product (GDP) growth, and domestic capital investments.

Table 2: Importance of SMEs to Economic Development

Contribution to GDP Contribution to exports Contribution to employment

Egypt 80% of economic output* -- 75% of private sector employment

99% of non-agricultural sector employment

Pakistan 30% of GDP and 35% of 25% to manufacturing Absorb 78% of non-agricultural workforce

manufacturing value added sector exports

Saudi Arabia 33% of economic output -- Accounts for ~25% of total employment

Jordan ~50% of GDP 45% of exports 60% of the workforce and 70% of new job

opportunities

Morocco ~38% of GDP, 40% of production, 30% of exports 50% of population

and 50% of investment

Tunisia 51% of GDP -- 69% of employment

Yemen -- -- --

Iraq -- -- --

Lebanon Over 99% of GDP -- 82% of employment generated

Note: (--) signifies data is unavailable; (*) Includes contribution of microenterprises as well

In Egypt and Lebanon, SMEs are important contributors to GDP (accounting for 80 percent and 99 percent of GDP, respectively). In

Pakistan, Morocco, and Tunisia, the SME contribution is lower, but significant (38 percent to 51 percent of GDP).

In addition to their GDP contribution, SMEs are the largest job creators in the formal and informal sectors. Except for Saudi Arabia, SMEs

employ more than 50 percent of the working population across the countries. In Egypt, for example, they account for almost 99 percent

of the employment in the non-agricultural sector and 75 percent of private sector employment. As SMEs are less capital intensive and

high employment generators, they can play an important role in the economic development of Middle Eastern countries such as Morocco,

Lebanon, and Tunisia, which have a sizable unemployed youth population. This is also true for vulnerable countries such as Yemen and Iraq.

Islamic banking opportunities across Small and Medium Enterprises in MENA (including Pakistan) 11Figure 3: SME Contribution to GDP

• Account for 50% • Contributes to • 80% of economic • Account for • Play a key role in

of employment, 51% of GDP output over 99% of reviving the economy,

• ~20% of value • 68% of the • 75% of GDP generating employment

employment private sector • 82% of and increasing per

added

employment employment capita income

• 30% of exports

• 99% of non- generated

• 40% of production agricultural sector

• 50% of investments employment

• 38% of GDP

• Employ 78% of

• Contribute ~50% non agricultural

to GDP workforce

• Employ 60% of the • Play an important role in • Account for 33%

• 30% of GDP

workforce generating employment, of economic output

• 35% of

• Accounts for 45% economic diversification • 25% of total

manufacturing

of exports and reducing poverty employment

value added

Note: Statistics on the contribution of SMEs to the economies of Yemen and Iraq are unavailable

Besides contributing to GDP and employment, SMEs are instrumental in promoting investments (in Morocco), increasing per capita income

(in Iraq), and ensuring economic diversification (in Yemen). Given their important role in economic development, governments in the Middle

East and North Africa (MENA) and Pakistan should work to identify and promote various factors/enablers for the development of the SME

sector. Policies targeting these factors/enablers need to be formulated for the long-term development of the SME sector.

In most countries, SMEs are concentrated in the trading sector, which primarily comprises retail and wholesale establishments, and the services

sector. The main reason for this concentration pattern is the low capital intensity, limited skill requirements, and the ease of establishment

of these enterprises. Other sectors with a high representation of SMEs include the manufacturing and construction sectors, in countries like

Egypt, Pakistan and Tunisia, primarily due to cottage industry. However, in most cases, the concentration of SMEs in these sectors is low due

to the high capital intensity and complexity of operations.

Financial, regulatory, and infrastructural factors prevent SMEs from entering and operating effectively in these complex, capital-intensive

sectors. Thus, there is a need for cooperation among government, private, and multilateral agencies to frame and execute strategies that

would ensure growing SME participation in these sectors. Greater SME participation in these sectors would help combat poverty, low per

capita income, and unemployment, which these countries suffer from.

Table 3: SME Distribution by Sector

Trade and Hotels and Misc. Industries

Country Manufacturing Construction Transport Services Tourism

Commerce Restaurants / Services

Egypt 51% 40% 2% 3% 4%

Pakistan 49% 40% 11%

Saudi Arabia 11% 32% 40% 17%

Jordan 24% 27% 42% 7%

Morocco 12% 31% 53% 4%

Tunisia 41% 21% 6% 8% 4% 11% 9%

Yemen 25% 22% 20% 13% 20%

Iraq -- -- -- -- -- -- -- --

Lebanon 48% 5% 47%

-- Please note, in Iraq industry wise SME statistics are not available.

* Please also note, in Lebanon, most of the industry wise SME statistics are not available.

12 Executive SummaryKey Enablers for SME Growth

As already outlined in several IFC studies, there are a number of key enablers that contribute to the development of a country’s SME sector. These

enablers are macro-level factors related to political and economic stability, sound infrastructure, a transparent governance structure, and access

to finance. The development of a country’s SME sector would be limited in the absence of any of these factors, as each has a unique role to play.

Governments should, therefore, recognize such linkages and take measures to develop these factors.

The table below provides an overview of the current state of the enabling factors across countries. Most of the countries lack a conducive,

enabling environment for SME growth owing to which the sector is unable to emerge from its low growth spiral.

Table 4: SME Enablers by Country

Parameter

Countries Political stability Economic Corruption Infrastructure Regulatory Access to

conditions Environment finance

Egypt Fragile Low High Medium Poor Low

Pakistan Semi stable Low High Low Strong Low

Saudi Arabia Stable Medium Low High Strong Low

Jordan Stable Medium Low High Strong Medium

Morocco Semi stable Medium Medium Medium Strong High

Tunisia Semi stable Medium Low High Strong Medium

Yemen Fragile Low High Low Poor High

Iraq Fragile High High Low Poor Low

Lebanon Semi stable Low High Low Poor Medium

Politically, Yemen and Iraq will continue to be impacted by factors that will affect SME prospects. In the case of other countries, the SME

sector is expected to be well insulated from such factors. Economically, SMEs in Saudi Arabia, Jordan, Morocco, and Tunisia can expect a

stable economic environment; while there will be risks to the economy in Lebanon, Pakistan, and Egypt in the short term.

With the exception of Saudi Arabia, Jordan, and Tunisia, corruption and poor infrastructure will be key problems facing SME operations

across the remainder of the countries. The regulatory environment across Yemen, Iraq, Lebanon, and Egypt is weak and likely to affect long-

term growth prospects of the SME sector. Thus, there are significant lessons that these countries could learn and emulate from their neighbors

such as Saudi Arabia, Morocco, Tunisia, and Jordan. In terms of access to finance, apart from Yemen and Tunisia, other countries have a

long way to go to ensure financial inclusiveness among SMEs.

Key Challenges for SMEs

SMEs in general face a number of challenges despite the assistance provided by government and multilateral agencies. These challenges are

faced during each phase of development and generally are internal (lack of managerial expertise among proprietors) and external (inadequate

access to finance, government inefficiencies, and infrastructural concerns).

Islamic banking opportunities across Small and Medium Enterprises in MENA (including Pakistan) 13Figure 4: Key Challenges Faced by Smes During its Evolution Phases

TIME

• ABSENCE OF SEED CAPITAL

FOR ESTABLISHING

BUSINESSES

• BUREAUCRATIC HURDLES IN • INSUFFICIENT DEMAND

REGISTERING BUSINESS

• UNSTABLE POLITICAL

• LACK OF WELL TRAINED • INADEQUATE FUNDS FOR ENVIRONMENT

LABOR FORCE EXPANSION OF OPERATIONS

MARKET MATURITY

• POOR INFRASTRUCTURE

• UNSTABLE POLITICAL • LACK OF BUSINESS SKILLS FOR

ENVIRONMENT • THREST FROMK

MANAGING OPERATIONS

INFORMAL SECTOR

• POOR INFRASTRUCTURE

• LACK OF INTRA-

• LACK OF A WELL TRAINED INDUSTRY

LABOR FORCE PARTNERSHIPS

• WEAK BUSINESS

ENVIRONMENT AND

CORRUPTION

INCEPTION DEVELOPING MATURE

Challenges faced by SMEs vary across countries due to differences in the level of development, degree of human development, efficiency

of governance, and the political situation in the respective countries. There exist several common challenges, such as lack of a well-trained

workforce, poor infrastructure, corruption, and bureaucratic hurdles.

The biggest challenge, however, is access to finance. SMEs at various stages of development face severe challenges when accessing finance.

Concerns include prohibitive interest rates, high collateral rates, and procedural hurdles in applying for a loan. This is despite the fact that

there are government-supported finance schemes, incubators, and venture capital funds to finance SMEs across various countries.

Figure 5: Challenges Faced by SMEs Across Countries

• High political risks

• Weak business environment and corruption • Insufficient demand due to political problems

• High collateral and lack of alternative to bank funding • Political instability

• Infrastructure Deficit

• Access to finance

• Constraint in access to finance

• Deficit of managerial expertise

• Low level of financial intermediation

• Low level of skill and training

• Sustainable access to finance

• Technological constraints

• Human resource constraints

• Poor infrastructure

• Lack of access to IT

• Corruption

• Infrastructure constraints

• Procedural hurdles

• Financial challenges

• Attitudinal problems • Low access to finance

• Unstable security scenario • Dearth of market linkages

• Marketing limitations • Government inefficiencies

• Lack of business skills • Saudization initiative

• Low level of organization

• Inadequate access to finance

• Lack of access to finance • Inadequate investment in technology

• Government inefficiencies and corruption • High energy costs

• Unbalanced tax policy • Lack of intra-industry partnerships

• Restrictive Labor regulations • Structural problems

• Inefficient management

• Inadequate access to finance

• Lack of skilled workforce

• Lack of technology infusion

• Threat from a informal sector

• Rationalization of costs

• Rapidity in market evolution

14 Executive SummaryThe chart below (Fig.7) outlines the major constraints facing SMEs across the various countries. SMEs in Egypt, Lebanon, Yemen, and Iraq

are facing numerous challenges with respect to political factors, economic conditions, the regulatory environment, and infrastructure. Unless

these constraints are remedied, it is unlikely that the SME sector will witness strong growth in these countries.

In the countries of Pakistan, Morocco, and Tunisia, the operating environment is less challenging with SMEs operating more efficiently.

However, there does exist infrastructural and transparency issues in these countries that must be addressed if the SME sector is to reach its

full potential.

Jordan and the Kingdom of Saudi Arabia (KSA) are relatively well placed as they have sound infrastructure, a strong regulatory environment,

and low levels of corruption. But SMEs operating in these countries have issues accessing finance, which is a very critical growth component.

Figure 6: Major Constraints Faced by Businesses

Political stability

Economic conditions

Corruption

Infrastructure

Regulatory Environment

Access to finance

Low / Fragile Moderate High / Stable

Lebanon Iraq Yemen Tunisia Morocco Jordan Saudi Arabia Pakistan Egypt

Source: Cumulative rankings based on the evaluation and analysis of key factors that are likely to impact SME growth

Islamic banking opportunities across Small and Medium Enterprises in MENA (including Pakistan) 15Government Initiatives to Support SME Growth

A country’s government has a very important role to play in the development of its SME sector by providing both financial and non-financial

support to promote SMEs. Financial support generally includes credit guarantee schemes, collateral waivers or reduction policies, and

provisions of seed capital. Non-financial support includes capacity building through training programs, improvement in competitiveness

through quality improvement initiatives, business incubation centers, and business development assistance through export development

programs.

Table 5: Government Initiatives to Support SME Growth

Countries Financial support programs/agencies SME development organizations

Egypt Social Fund for Development Industrial Modernization Centre

Egypt Technology Transfer and Innovation Centers

Industrial Development Authority

National Suppliers Development Program

Ministry of Investment/General Authority for Investment

Pakistan SME Bank Small and Medium Enterprise Development Authority

Khushhali Bank (SMEDA)

Trade Development Authority of Pakistan

Ministry of Science and Technology

Pakistan Software Export Board

Pakistan Horticulture Export Board

National Productivity Organization

Saudi Saudi Credit and Savings Bank National Competitiveness Center

Arabia Saudi Industrial Development Fund (Kafalah program) Ministry of Economy and Planning

Prince Sultan bin Abdul Aziz Fund to Support Women’s Saudi Arabia Monetary Agency

Small Enterprises Human Resource Development Fund

Centennial Fund

Jordan Jordan Loan Guarantee Corporation Jordan Enterprise Development Corporation

Governorates Development Fund National Fund for Enterprise Support

Development and Employment Fun Vocational Training Corporation

Morocco Central Guarantee Fund National Association of Small and Medium Enterprises

The Office of Vocational Training and Employment Promotion

National Agency for Promotion of Jobs and Skills

Tunisia Fund for the Promotion and Industrial Decentralization The Agency for the Promotion of Industry and Innovation

Tunisian Guarantee Company The Centre de Soutien à la Création d›Entreprises (Support

Société d’investissement en capital à risqué (Risk Capital center for business creation)

Fund) Centres d’Affaire (business centers)

Banque de Financement des Petites et Moyennes (Bank for Bureau de Mise à Niveau

financing small and medium enterprises)

16 Executive SummaryYemen Small Enterprise Development Fund Social Fund for Development /Small and Microenterprises

Small and Micro Enterprise Development Promotion Agency

Ministry of Agriculture

Ministry of Technical and Vocational Training

Ministry of Fisheries

Ministry of Tourism

Iraq Ministry of Labor and Social Affairs

Ministry of Industry and Minerals

Lebanon Economic and Social Fund for Development The Ministry of Economy and Trade (SME support unit)

Kafalat loan guarantee Euro-Lebanese Centre for Industrial Modernization

Ministry of Education

Ministry of Finance

World Bank Group Initiatives to Support SME Growth

IFC has several programs targeting the development of the SME sector. This includes both investment and advisory services to banks and to

SMEs directly. IFC has provided assistance to commercial banks for setting up SME banking operations. It has also assisted in establishing

financial infrastructure, such as credit bureaus and provided specific credit lines, risk sharing, and trade finance facilities targeting SMEs. IFC

has also provided training and awareness raising programs for SMEs.

Table 6: IFC Initiatives to Support Access to Finance for SMEs

Countries IFC

Egypt • Egypt Junior Business Association: Helped train SMEs on corporate governance standards

• Alexandria Business Association: Assessed business environment and advocated regulatory reforms

Pakistan • 2012 (Bank Alfalah): Capacity Building for SME Banking

• 2011–2012 (HBL Bank): Capacity Building for SME Banking and Agri Finance

• 2009 (Standard Chartered Saadiq): Launched pilot program for SME training

• 2009 (United Bank Limited): Boosted SME trade finance

Saudi • 2011 (Saudi Hollandi Bank): Capacity building for SME Banking

Arabia

• 2010 (Saudi Orix Leasing Company): Invested $20mn to expand sustainable energy financing and increase access to finance

• 2005 (Riyad Bank): Capacity building for SME Banking. Non Financial Advisory Services.

Jordan • 2012 (Ahli Bank): Assisted SMEs in acquiring skills for business expansion and job creation

• 2009: Supported leasing legislation and promoted leasing awareness

• 2006: Worked with government to streamline licensing and inspection process

• Assisted government in establishing a private credit bureau industry

• Raised awareness in the banking sector regarding sustainable energy financing, opportunities targeting women, low-income

households, and environment-friendly initiatives

Islamic banking opportunities across Small and Medium Enterprises in MENA (including Pakistan) 17Morocco • 2012 (Banque Centrale Populaire): Invested $204mn to acquire 5% stake to improve access to credit for SMEs

• 2011 (Moroccan Female Entrepreneurs Association): Promoted alternative dispute resolution among women entrepreneurs

• 2011 (Maghreb Private Equity Fund): Set up fund to invest in SMEs in Tunisia, Morocco, Algeria, Libya, and Egypt

• 2007 (Al Amana): Improved credit operations and followed a sustained growth path

• Established fund to invest $150mn annually over the next three years in SMEs, agribusinesses, IT, and high value-added businesses

Tunisia • 2013 (Amen Bank): Agreement between IFC and two funds managed by IFC Asset Management Company to invest up to

$48mn to help bank increase lending

• 2011–2012(Maghreb Private Equity Fund III): A $22mn commitment to provide guidance and financial support to SMEs across

North Africa

• 2012 (Amen Bank): Offered guarantees to assist Tunisian companies increase cross-border trade

• 2011 (The Arab Institute of Entrepreneurs): Helped promote sound corporate governance practices

Yemen • 2010 (Al Amal Microfinance Bank): Strengthened technical capacity by focusing on product development and finance

• Trained 5,100 people in Yemen using Business Edge

• Played important role in framing new laws to improve business climate

• Channelizing private investments in the infrastructure sector through launch of various initiatives, including the Middle East and

North Africa SME Facility, the Arab Financing Facility for Infrastructure, the e4e Initiative for Arab Youth, and the MENA Fund

Iraq • To invest $100–130mn annually over the next few years in the private sector (includes SMEs) in banking, telecommunications,

construction, logistics, hospitality, and manufacturing

• 2011–2012: Launched $38mn facility to support financial infrastructure strengthening, capacity building of the banking/SME

sector, bank risk management, SME management training (for women), and promotion of Public private partnerships (PPP)

• 2012 (Relief International): Scaled up outreach to SMEs in Iraq

Lebanon • 2005–2011: Total commitment over $737mn, including $150mn for local banks to facilitate lending to SMEs

• Provided over $1bn in trade guarantees to banks and financial institutions to facilitate global export and import trade

• 2011 (BLC Bank): Designed and launched products, specifically for SMEs and women-owned business

• 2007: Collaborated with World Bank and pledged $250–275mn through the Lebanon Rebuild Program

• 2007 (Bank of Beirut): Set up SME risk-sharing facility worth $25mn

• 2007 (Fransabank): $50mn project to establish an SME risk-sharing and corporate credit line

• 2007 (Société Financière du Liban): Feasibility study for establishment of private credit bureau

• Supported Central Bank of Lebanon in encouraging banks to strengthen SME setup

18 Executive Summary03.

Financial Sector Overview

The commercial banking sector across most countries witnessed

strong growth despite the 2007-2008 financial crises. The Islamic

banking sector has, however, been more resilient due to prudent

practices and the rising preferences for Islamic banking services

among the resident population. The growth in Islamic banking

has also been supported by government initiatives aimed at

enhancing the penetration of banking services. Overall SME

lending by banks has been gradually rising across most countries

in recent years, but the situation is still far from perfect.

Banking Penetration

The banking sector across the countries is in different stages of market maturity. Although countries such as Lebanon have a well-established,

competitive banking structure, nations such as Iraq have a small, underdeveloped banking system that would mature only in the long term.

In developed countries such as Lebanon, Jordan, and Morocco, the evolution of banking began early. Jordan’s banking sector emerged in

1925, while the Moroccan banking system dates back to the 18th century. Lebanon was a late entrant; the country emerged as a financial

hub during 1950–1975. In these countries, the common factor aiding the banking sector’s growth was the government’s liberalization of the

sector, which led to competition and the gradual sophistication within the sector.

In countries such as Tunisia, Pakistan, and Saudi Arabia, the banking sector’s inception and growth has been relatively late. Additionally, the

banking sector’s development in these countries has been affected periodically by unhealthy competition (Pakistan), economic turmoil (Saudi

Arabia), and political interference (Tunisia).

Countries such as Yemen and Iraq have underdeveloped banking sectors characterized by low branch penetration and lack of a credit culture

among the population. Historically, the banking sector in Yemen and Iraq has been underdeveloped as the poor regulatory framework and

limited competition has stunted its growth. Political turmoil added to the woes, limiting the sector’s development.

Figure 7: Banking Penetration Across Countries

• 1,483 deposit accounts per 1000 adults

• 573 loan accounts per 1,000 Adults

• 31.52 commercial bank branches per 100,000 adults

HIGH

• 898 out of 1,000 adults have a deposit account with a bank (2010)

PENETRATION

• Loan penetration- 200 adults per 1,000 adults (2010)

• ~39% of the population had access to banks

• 706 Bank deposits per 1,000 people

• One bank branches for 6,300 people

• 8.97 commercial bank branches per 100,000 adults

• 25.7 borrowers from commercial banks per 1,000 adults

• 28.98 loan accounts with commercial banks per 1,000 adults

• 0.7% of the total deposits with commercial banks are SMEs

• 1396 bank branches

MEDIUM • 7,600 Inhabitants per bank branch -

PENETRATION • 639 bank deposits per 1,000 adults

• Population per branch 17,075 (2012)

• Deposit penetration approximately 53% (2012)

• 10% of the adult population in the country owned or shared

a bank account

• Banking density - 22.7 per thousand

• 8.7% of adult population had access to bank accounts

• 1.8 branches per 100,000 adults

LOW

PENETRATION • 4.8 Bank branches per 100,000 adults

• 2.1 commercial bank branches per 1,000 km2

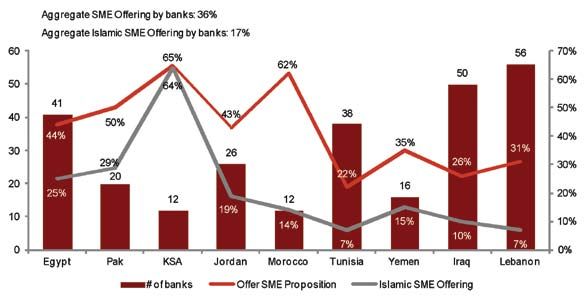

Islamic banking opportunities across Small and Medium Enterprises in MENA (including Pakistan) 19Commercial Banking Sector

The commercial banking sector across the countries is generally concentrated with the largest players accounting for most assets and

deposits. However, despite high concentration, the commercial banking sector is competitive with large players making consistent efforts to

increase market share. This has led to product innovation, expansion of branch networks, and greater financial inclusion.

Table 7: Commercial Banking Sector Overview

Banking structure Industry overview

41 Commercial banks The banking sector is dominated by two public sector banks, National

• 26 commercial banks, Bank of Egypt and Banquet Mira, accounting for more than 50% of

Egypt • 12 commercial banks with Islamic the country’s banking assets. Other leading banks include Commercial

windows and International Bank (CIB), National Society Generale Bank (NSGB) and

• 3 full fledged Islamic banks HSBC.

34 Commercial banks The top six banks -National Bank of Pakistan, Habib Bank, United

• 22 local private banks Bank Limited, MCB Bank Limited and Allied Bank Limited - accounted

Pakistan

• 7 foreign banks for ~57% of total assets and ~45% of all deposits

• 5 public sector banks

12 domestic banks and 11 foreign banks. Dominated by Al Rajhi Bank (accounting for 16% of all financing by

• 4 full fledged Islamic banks 8 banks offer Saudi banks, and 26% of all Saudi Islamic financing ), NCB and Riyadh

Saudi Arabia conventional and Islamic products Bank, which together account for 48% of total deposits and 45% of the

• The remainder of the banks are total loans outstanding .

conventional banks

16 national banks Banking system dominated by Arab Bank and Housing Bank for Trade

• 13 conventional banks and 3 Islamic banks and Finance (HBTF) which jointly account for one-third of the total

Jordan • 10 foreign banks financing and more than one-fourth of total deposits. Jordan Islamic

• 9 conventional banks and 1 Islamic bank Bank, the third-largest bank and the largest Islamic bank in the country,

accounts for 14% of financing and 11% of deposit share.

19 commercial banks The banking sector is dominated by three players – Attijariwafa Bank,

• 6 public owned banks, Groupe Banquet Populaire, and Banquet Marocaine du Commerce

Morocco

• 6 offshore banks Exterieur (BMCE). These banks together account for ~77% of the

• 7 foreign owned banks country’s total bank lending, and ~80% of deposits .

29 commercial banks Banquet National Agricole and Société Tunisienne De Banquet (both

• 6 state owned banks state-controlled banks) are the two largest banks in the country by

• 15 private banks deposits, but account for only 9% and 6% of the loans disbursed by the

Tunisia

• 8 off shore banks banks, respectively. Banquet d’Habitat is the largest, bank by loans, with

a 34% share of the market, followed by Amen Bank (10%) and Arab

Tunisian Bank (10%).

16 commercial banks Tadhamon International Islamic Bank accounted for 21% (largest

• 4 private domestic banks, share) of total banking assets with assets worth ~$1.7bn, followed by

• 4 Islamic banks Cooperative and Agriculture Credit (CAC) Bank (13%), with an asset

Yemen

• 5 private foreign banks base of ~$1.1bn . Tadhamon International Islamic Bank, Cooperative

• 3 state-controlled banks and Agriculture Credit and Arab Bank account for one third of the

deposit base.

50 commercial banks The banking sector is dominated by seven state-owned banks that

• 40 conventional banks control 97% of the total banking assets, 89% of the total bank deposits,

Iraq

• 10 Islamic banks and over 75% of the total loans extended in 2010. Most private

commercial banks are rather small and relatively new.

55 commercial banks Banking activity in Lebanon is dominated by nine large banks, which

• 31 private domestic banks, account for more than 90% of the financing activity and depository

Lebanon • 19 regional banks base of commercial banks. Bank Audi and BLOM Bank are the two

• 5 foreign banks largest banks accounting for more than 35% of loans and deposits of

commercial banks

20 Executive SummaryAfter the global economic downturn, most Middle East and North Africa (MENA) countries initiated regulatory reforms to strengthen the

banking sector. This resulted in a strong growth in depository base and financing activity within banks in MENA countries.

Most countries in the region witnessed strong growth in the banking system in recent years. Iraq witnessed the highest growth in the region

(loans grew 104 percent and deposits increased 24 percent during 2010-2012), along with Lebanon, Jordan, and Saudi Arabia. Other

countries in the region witnessed high single-digit growth in the banking sector. However, the Arab Spring and the resulting political and

economic uncertainties have impacted the short-term growth of the region’s banking sector.

Figure 8: Loan and Deposit Growth Across Countries (2010–2012)

Note: The figures in the box reprصesent the Compounded annual growth rate (CAGR) for the period

Islamic banking opportunities across Small and Medium Enterprises in MENA (including Pakistan) 21Islamic Banking Sector

Islamic banking has not developed uniformly across MENA countries, as its inception and development across the countries occurred at

different points of time in history. For example, Egypt was the birthplace of Islamic banking, with the first Islamic bank beginning operations

in 1960. On the other hand, in Morocco and Lebanon, Islamic banking has just begun to emerge, with the recent government authorization

of Islamic banking operations.

Egypt’s first-mover advantage, however, did not lead to the sector’s rapid growth and development. Despite an early introduction of Islamic

banking, Egypt has witnessed muted growth over the years. In contrast, Pakistan and Saudi Arabia, which introduced Islamic banking later,

witnessed strong growth over the years. Jordan, Yemen, Iraq, and Tunisia introduced Islamic banking in the 1970s and 1980s; however, the

lack of government support in the past to promote Islamic banking has affected growth prospects.

In recent years, most countries in the region saw the establishment of new Islamic banks. Morocco and Tunisia have initiated steps to

establish and expand Islamic banking activities. In addition to government support, the growth of Islamic banking in these countries has been

aided by strong positive perception for Shariah-compliant banking among the people of MENA and Pakistan.

Figure 9: Islamic Banking Market Overview

Islamic banking sector is underdeveloped, accounting

Five Islamic banks operate in the country

for less than 1% of the total banking assets.

Dar Assafaa is the only full-fledged alternative non-banking financial No full-fledged Islamic banks. Eight financial

institution, the rest offer such products through windows institutions offering Shariah-compliant products

Market dominated by Kurdistan 10 full-fledged Islamic banks were in operation

International Bank and Al Bilad Bank Currently nascent market is expected to witness

Bank Zitouna only bank authorized to offer strong growth in the medium and long term.

Shariah-compliant financial products and services

Four full-fledged Islamic banks and three

Tadhamon International Bank is dominant player

conventional banks with Islamic windows

accounting for 65% of assets and deposits

Four full-fledged Islamic banks. Central bank has

Jordan Islamic Bank accounts for more than two-thirds

not allowed conventional banks to offer Shariah-

of the total Islamic financing and deposits

compliant products through Islamic windows.

Among banks with Islamic branches, Bank Alfalah Five full-fledged Islamic banks and 12 conventional

and Standard Chartered are the largest players banks with Islamic banking windows. Meezan

bank largest full-fledged Islamic bank by assets and

Faisal Islamic Bank is the leading Islamic bank, deposits

accounting for more than half of the country’s Three full-fledged Islamic banks. In all, 14

Islamic banking assets and deposits banks have Islamic banking licenses

Al Rajhi largest Islamic bank accounting

for 26% of Islamic financing and 29% of Four fully Shariah-compliant banks, as well as

Shariah-compliant deposits, followed by eight conventional banks with Islamic windows

NCB and Riyad Bank

In the last few years, most MENA countries (including Pakistan) have witnessed an expansion in Islamic banking activity. All countries in the

region witnessed strong growth in Islamic deposits and financing activities, except Yemen, which was impacted by political instability and a

deteriorating economic environment, especially after the Arab Spring.

22 Executive SummaryFigure 10: Islamic Assets and Deposits Growth (20102012-)

Note: The figures in the box represent the CAGR for the period

Please note that in the left hand charts figures for Egypt. Pakistan and Tunisia represent total Islamic assets while for the remainder of the

countries it represents total financing

SME Sector

The banking sector (Islamic and conventional) has been able to meet some of the needs of the SME sector. Despite the expansion in banking

operations and the corresponding growth of loans and deposits, SMEs still remain underfunded. The lack of penetration of the SME sector

is due to demand- and supply-side factors (explained later in the report).

Islamic banking opportunities across Small and Medium Enterprises in MENA (including Pakistan) 23Table 8: Banking Penetration in SME Sector (2012)

Banks lending to SME lending as % of Total SME lending Total SME deposits

private sector ($bn) total lending ($bn) ($bn) **

Egypt Conventional 69.5 8.00% 5.6 --

Islamic 5.5 8.00% 0.4 --

Pakistan Conventional 33.2 7.3% 2.4 --

Islamic 6.3 4.10% 0.3 --

Saudi Arabia Conventional 88 2.00% 1.8 2.3

Islamic 179 2.00% 3.6 4.6

Jordan Conventional 20.0 12.50% 2.5 3.6

Islamic 5.1 7% 0.4 0.6

Morocco Conventional 88 24.00% 21.0 20.3

Tunisia Conventional 33.9 15.00% 5.1 4.1

Yemen Conventional 1.7 20.30% 0.3 0.5

Iraq* Conventional 9.4 5% 0.5 1.9

Lebanon Conventional 45 16.14% 7.3 20.3

Total Conventional 388.7 n.a 46.5 53.0

Islamic 195.9 n.a 4.70 5.2

Grand Total 584.6 8.75%** 51.2 58.2

-- Data for selected countries is unavailable

* For Iraq, the data is for 2010

** Average SME lending, as a percentage to total private sector lending.

The ability of banks to meet the financing needs of the SME sector represents a mixed picture. While Morocco, Lebanon, Egypt, and Saudi

Arabia have witnessed a strong increase in lending to the SME sector, in the case of other countries (Jordan, Tunisia, and Iraq) SME lending

has been more muted due to a number of reasons (lack of focus, a weak banking system, and a fragile political environment respectively).

Table 9: Trend in SME Portfolio Growth

Country SME Portfolio Growth

Egypt Rising • Lending to SMEs by Egyptian banks has increased at a CAGR of 10.4% over 2009-2012. Yet, the

proportion of SME loans to the total outstanding loans by banks has remained in the range of 7-8%

during this period.

• Of the 26 banks operating in the country, 17 operate a separate SME business unit. However, of these

only 9 banks offer adequate SME products.

Pakistan Declining • Lending by banks to the SME sector has declined at a compounded rate of 8.5% over 2009-2012 largely

due to an increase in the non-performing loan (NPL) rate for the sector.

• As a result, banks have become more cautious in financing SMEs, instead diverting funds to safer

investment opportunities. Thus, the SME lending penetration rate also declined from 10.3% in 2009 to

6.8% in 2012.

24 Executive SummarySaudi Rising • Although the SME lending penetration rate in the KSA is only ~2%, there is greater impetus on SME

Arabia financing by banks, supported by the Shariah-compliant Kafalah program (a financing guarantee

program for SMEs).

• Hence, SME financing by banks has increased at a CAGR of 23% during the period of 2009-2012.

A large part of this growth has been driven by Shariah-compliant financing (backed by the Kafalah

program), which has increased at a CAGR of 28.4% during this period.

Jordan Stagnant • Although lending by banks to the private sector has increased over the years, disbursements to the SME

sector has remained conservative, with 12.5% of the total loans being directed toward this sector.

• This is mainly due to less risky and more profitable investment avenues available to banks in the form

of corporate or government lending.

Morocco Rising • Although credit disbursements by banks to the SME sector has only increased at a CAGR of 7.7% for

the period of 2009-2012, the SME penetration rate in the country stands at 24%, much higher than the

MENA average of 7.6%.

• The higher penetration rate has been on account of proactive measures implemented by the government

through the National Association of Small and Medium Enterprises (ANPME) that not only encourage

SMEs but also facilitates financial access to these enterprises.

Tunisia Stagnant • The SME lending rate in Tunisia, which is 15.3%, is comparatively higher than the MENA average of

7.6%. Yet, growth of lending to the sector has been slow, increasing at a CAGR of 6.5% during the

period of 2010-2012.

• However, this slow growth is largely a result of problems plaguing the banking sector as a whole, such

as weak corporate governance and efficiency standards and a high NPL rate.

Yemen Declining • Yemen’s private sector predominantly consists of SMEs. As a result, any increase in lending to the

private sector positively impacts financial access to SMEs.

• However, credit disbursements to private enterprises have been declining over the years, from 43% in

2009 to 30% in 2012.

Iraq* Stagnant • SME lending penetration in Iraq has been stagnant at around 5% in the last few years.

• Although there has been a lot of activity in terms of providing financial access to SMEs, the banking

institutions in Iraq have been reluctant to advance financing to them because this sector is considered

to be highly risky.

Lebanon Rising • SME lending penetration rate in Lebanon is currently at 16.14%.

• This is expected to increase as banks reduce exposure to government debts and instead divert these

funds to the private sector.

Non-performing Loans

Financial institutions in MENA have always adopted a cautious lending approach. Therefore, asset quality of conventional and Islamic

banks has remained strong. Although countries such as Egypt, Yemen, and Tunisia have a NPL ratio of 11 percent to 18 percent, it has been

declining over the last few years due to the adoption of better risk management policies and improved banking infrastructure.

The rise in banking sector NPLs resulted from the Arab Spring and the effects of the 2007–2008 financial crises. Both factors affected the

repayment capacities of the private sector, leading to a high rate of NPLs. The problem was exacerbated by the existing weak economic and

political conditions in Egypt, Jordan, and Yemen. In addition to political and economic factors, a poor regulatory (Tunisia) and business

environment (Pakistan) contributed to the rise in NPLs. There is a disparity between the NPLs of the conventional and Islamic banking

sectors. The NPLs of Islamic banks have traditionally been lower than those of conventional banks as they are more prudent with regard to

lending to various sectors.

Islamic banking opportunities across Small and Medium Enterprises in MENA (including Pakistan) 25Figure 11: NPL Overview

Please note that in Egypt data on the Islamic banking sector i s unavailable

The growth of NPLs in the financial sector presents an opportunity to establish credit bureaus in such countries for capturing and disseminating

credit-related data to financial institutions and other lenders.

Islamic Financial Sector Regulations and Enabling Environment

Although central banks in MENA have proactively regulated the banking sector following the global financial crisis, great disparity exists

across the countries in terms of quality and implementation of reforms.

Regulatory authorities in these countries have initiated reforms and amended existing banking laws to include specific regulations for Islamic

banks. However, most of these countries, such as Egypt, Tunisia, Morocco, Lebanon, and Iraq, are still developing separate laws on Islamic

banking.

Table 10: Regulatory Overview

Country State of Regulations

Banking Sector Islamic Banking SME

Egypt Well defined Inception Non existent

Pakistan Well defined Well defined Well defined

Saudi Arabia Well defined Transitional Transitional

26 Executive SummaryYou can also read